transfer pricing establishing policy for an mnc pricing establishing policy for an mnc samir gandhi...

TRANSCRIPT

Transfer Pricing

Establishing policy for an MNC

Samir Gandhi & Bhupendra Kothari

©2015 Deloitte Touche Tohmatsu India Private Limited

Contents

• Structuring a Transfer Pricing Policy – Key Issues

• The Optimum Business Model

• Transfer Pricing as Planning Tool

2

Structuring a Transfer Pricing

policy

3

©2015 Deloitte Touche Tohmatsu India Private Limited

Key considerations for Transfer Pricing policy

General issues

Issues to be kept in mind while structuring a global transfer pricing policy:

• MNCs should prepare a customized pricing policy for key risk jurisdictions. Such

policy should be based on the global pricing policy

• Global Transfer Pricing policy should clearly define and document the global

supply chain of the multinational group

• Terms and conditions of cross-border transactions between related parties

should, as far as possible, be substantiated by an agreement:

‒ would ensure transparency in inter-company dealings

‒ provide comfort during audit proceedings

• Need to strengthen internal systems and processes in order to maintain

transactional level data and collate contemporaneous documents

• Transfer Pricing documentation should be robust, updated and monitored on a

yearly basis based on the jurisdictions requirement

4

©2015 Deloitte Touche Tohmatsu India Private Limited

Supply Chain Management Process

Supply chain business process starts right from

• Supply chain planning

• Forecasting, sales and marketing

• Sourcing and procurement

• Manufacturing

• Order management & Logistics management

• Delivery to customer

Manufacturing Storage Distributor Retailer

External

Supplier

Customer

Central Service Provider

5

©2015 Deloitte Touche Tohmatsu India Private Limited

Manufacturing Functions

Manufacturing

Toll Manufacturer

Inventory

Contract Manufacturer

Sales

Licensed Manufacturer

Intangible

Full Fledged Manufacturer

+ + +

Functions and Risks

6

©2015 Deloitte Touche Tohmatsu India Private Limited

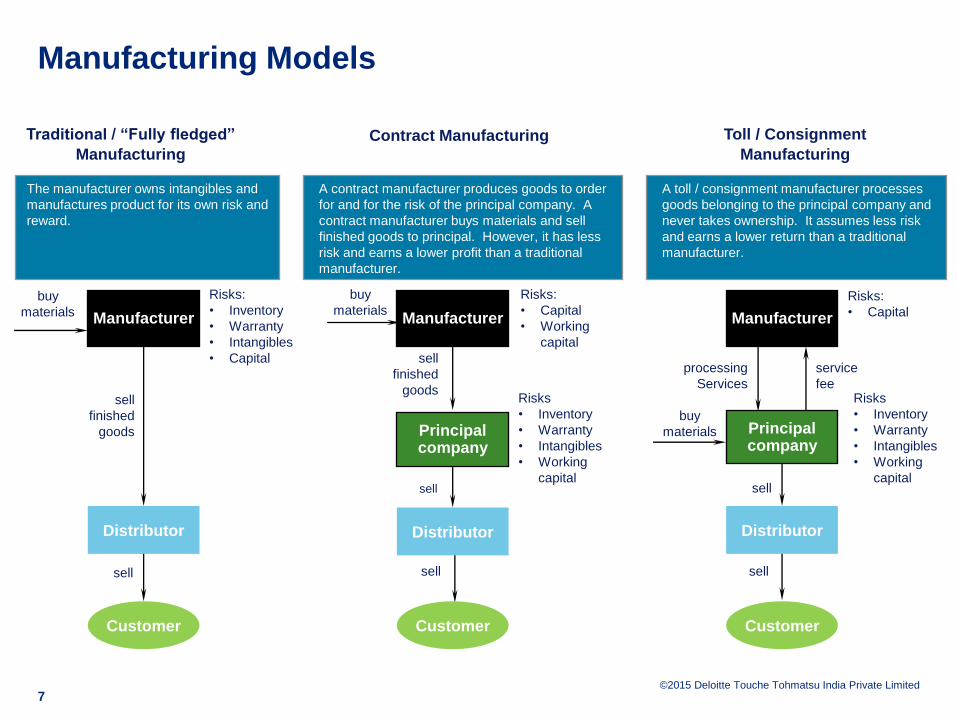

Manufacturing Models

7

Traditional / “Fully fledged”

Manufacturing

The manufacturer owns intangibles and

manufactures product for its own risk and

reward.

A contract manufacturer produces goods to order

for and for the risk of the principal company. A

contract manufacturer buys materials and sell

finished goods to principal. However, it has less

risk and earns a lower profit than a traditional

manufacturer.

A toll / consignment manufacturer processes

goods belonging to the principal company and

never takes ownership. It assumes less risk

and earns a lower return than a traditional

manufacturer.

Distributor

sell

finished

goods

sell

Risks:

• Inventory

• Warranty

• Intangibles

• Capital

buy

materials

Customer

Manufacturer

sell

Risks

• Inventory

• Warranty

• Intangibles

• Working

capital

sell

finished

goods

Risks:

• Capital

• Working

capital

buy

materials

Principalcompany

Distributor

Manufacturer

sell

Customer

Principalcompany

Distributor

Manufacturer

Customer

buy

materials

service

fee

processing

Services

sell

sell

Risks:

• Capital

Risks

• Inventory

• Warranty

• Intangibles

• Working

capital

Contract Manufacturing Toll / Consignment

Manufacturing

©2015 Deloitte Touche Tohmatsu India Private Limited

Key considerations for Transfer Pricing policy

Manufacturing activity

• Transfer Pricing policy for manufacturing is complex and has to take into

consideration possibility of internal comparable

• Typical manufacturing structures may include a) few subsidiaries focused on

manufacturing and rest distribution b) one overseas entity in manufacturing

(mother plant) rest all distribution entities

• In the below structure, AE manufacturing entity imports raw materials from parent

and manufactures component for domestic and export consumption

• Gross level comparison of sales to AE vis-à-vis 3rd party sales can be made to

review the profitability

Indian parent

(exports raw

materials)

AE

manufacturing

entity (country X)

Export sales to

AE (country Y)

Sales to 3rd

parties (country

X)

8

©2015 Deloitte Touche Tohmatsu India Private Limited

Key considerations for Transfer Pricing policy

Manufacturing activity

• Pricing of imported raw materials by the AE is an essential consideration for

establishing a effective TP policy:

‒ Price sensitivity of the sale market also important consideration

‒ Local regulatory environment favoring manufacturing (e.g., special economic

zones) also impacts costs and price

• Another important issue is the extent of value addition made by the AE in

manufacturing process

• Manufacturing set-up could range from assembly operation at the very low end of

the scale to fully integrated manufacturing activity and being an OEM

• The extent of value addition would be a key determinant in establishing transfer

pricing allowing an arm‟s length compensation for such functions

• The overseas AE may be licensed to use technology and know-how in return for

royalty payments

• Separate benchmarking for royalty and benefit test documentation

9

©2015 Deloitte Touche Tohmatsu India Private Limited

Judicial precedents

Sona Okegawa Precision Forgings (2011)

• TPO disallowed royalty payment considering that the assesse is a contract

manufacturer and no royalty needs to be paid if it is using the technical know

how to manufacture goods and sell the same to its group companies itself.

• ITAT has upheld that it is not a contract manufacturer as it manufactures goods

and sells only a fraction of the goods to the group companies and rest of it is

sold to the third parties and thus allowed the payment of royalty.

SC Enviro Agro India Pvt. Ltd. (2013)

• Assessee purchased raw material and other consumables on its own account

and entire risk of manufacturing was borne by the assesse.

• TPO has disallowed royalty payment considering that the assesse is a contract

manufacturer and no royalty needs to be paid.

• ITAT was of the opinion that the assessee was manufacturing goods only on the

instructions of the principal company but however, selling goods to third parties

also and the facts of the case were unlike a contract manufacturer.

• Thus, ITAT allowed the payment of royalty to its group company.

10

©2015 Deloitte Touche Tohmatsu India Private Limited

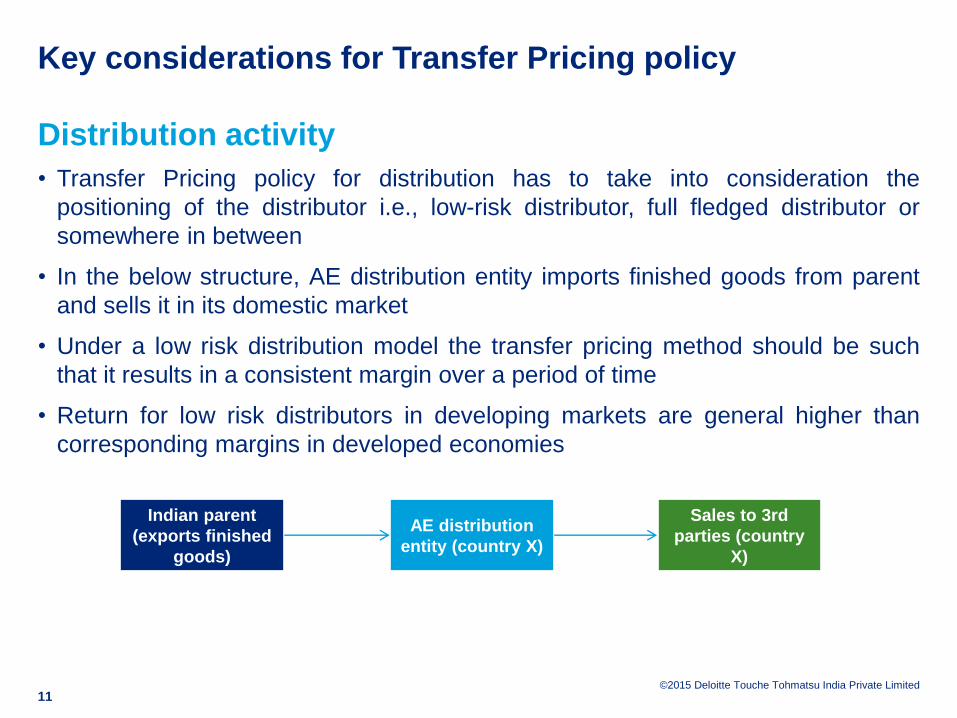

Key considerations for Transfer Pricing policy

Distribution activity

• Transfer Pricing policy for distribution has to take into consideration the

positioning of the distributor i.e., low-risk distributor, full fledged distributor or

somewhere in between

• In the below structure, AE distribution entity imports finished goods from parent

and sells it in its domestic market

• Under a low risk distribution model the transfer pricing method should be such

that it results in a consistent margin over a period of time

• Return for low risk distributors in developing markets are general higher than

corresponding margins in developed economies

Indian parent

(exports finished

goods)

AE distribution

entity (country X)

Sales to 3rd

parties (country

X)

11

©2015 Deloitte Touche Tohmatsu India Private Limited

Key considerations for Transfer Pricing policy

Distribution activity• In contrast, a full fledged distributor would:

‒ take marketing and credit risk

‒ perform significant brand building exercises

‒ be willing to dynamically change pricing strategies to increase its market share

‒ Perform value added services such as packing and labeling, logistics, pre-sales

presentation and after sale services

• Accordingly, a full fledged distributor has to have a policy that compensates for

such value added functions

• The determination of the “most appropriate method” will depend on the level of

value addition also considering any marketing intangibles created

• Profitability of a distributor also depends on the selling strategy and channel

adopted

• If distributor undertakes to establish its own distribution network it may result in

initial year losses do to disproportionate costs incurred

• However in later years greater profits are expected on account of improved

efficiencies

12

©2015 Deloitte Touche Tohmatsu India Private Limited

Distribution Functions

Sales – disclosed Principal

Commission Agent

Undisclosed Principal

Commissionaire

Inventory

Buy-sell distributor / Reseller

Marketing Intangible

Full Fledged Distributor

+ + +

Functions and Risks

13

©2015 Deloitte Touche Tohmatsu India Private Limited

Sales Models

14

Fully fledged Distributor

A full distributor bears market

risk, holds inventory for its own

risk and sells to the customer as

principal. The distributors profit

margin reflects its risks and

functions.

Limited Risk Distributor

A master distributor bears market

risk and inventory risk. The local

limited risk distributors buy product

from the master distributor and

resell the product to the customer.

The limited risk distributors earn a

lower profit than a full distributor,

consistent with their reduced

functions and risks.

Commissionaire

A civil law concept whereby the

commissionaire sells product in its own

name but for the account of the

principal. The risks and benefits of the

sale (and the profit) rest with the

principal. The commissionaire

receives a commission which provides

it with a lower profit than a full

distributor, consistent with its reduced

functions and risks.

Distributor

sell

finished

goods

sell

Customer

Manufacturer

• Price risk• Volume risk• Inventory risk• Credit risk• Marketing

intangibles

Principalcompany

Commissionaire

Customer

sell

commission

• Price risk

• Volume risk

• Inventory risk

• Credit risk

• Marketing

intangiblessell

Principalcompany

Distributor

sell

Customer

• Price risk

• Volume risk

• Inventory risk

• Credit risk

• Marketing

intangibles

The local sales company acts as a

representative that is not directly involved

in making sales. It merely provides

product information and performs

customer service. The principal receives

sales orders directly from customers -

either in a call centre or electronically.

The local representative earns a lower

profit than a full distributor, consistent with

its reduced functions and risks.

Representative

Principalcompany

Representative

Customer

sell

Service fee

• Price risk

• Volume risk

• Inventory risk

• Credit risk

• Marketing

intangibles

Product info

and customer

services

Order

©2015 Deloitte Touche Tohmatsu India Private Limited

Distributorship and Berry Ratio

Berry ratio is the ratio of gross profit to operating expenses.

It is primarily used in the case of

• pure/routine distributors;

• entitled to a return on its operating expenses alone;

• the return is primarily dependent on the extent of services provided and not on

the market value of the products distributed;

• does not perform any value addition to goods; and

• does not own non-routine intangibles.

It relies on the fact that there is consistency between the level of gross margins and

operating expenses (i.e. greater the operating expenses, greater is the gross profit

needed, to sustain the operating expenses).

15

©2015 Deloitte Touche Tohmatsu India Private Limited

Judicial precedents

Mitsubishi Corporation India Pvt. Ltd. (2014)

• Assessee was acting as a medium of communication through which they can

compete with its associated enterprises competitors in India performing

distribution activities.

• Assessee believed since it was only front ending the group companies

operations, it was a service provider.

• However, ITAT stated that the assesse was an intermediary (distributor)

performing buy sell activities and not carrying inventory risk and since all its

expenses which an assesse needs to be compensated for, were captured in its

operating expenses, berry ratio would be appropriate to be used.

E.I. DuPont de Nemours & Co. (2011)

• The assessee performed distribution services for its associated enterprise in

US.

• Since distributors should earn a return commensurate to its services and the

cost of which is covered in its operating expenses, Berry suggested berry ratio

as an appropriate profit level indicator for a pure distributor not owing non

routine intangibles.

16

©2015 Deloitte Touche Tohmatsu India Private Limited

Key considerations for Transfer Pricing policy

Services• Indian MNCs provide a variety of IT and ITeS to global multinationals, including

engineering design, back office, procurement, financial and analytical services

• In the below structure, Indian parent has a central development center in country

Y and an onsite delivery entity in country X to provide the final product

• Most development centers are set-up as risk free service providers which are

guaranteed return on a time-cost basis or a cost plus mark-up basis

• The intellectual property rights for the software they develop vests with the Indian

parent

• The onsite entity is primarily engaged in marketing, understanding client

requirements and implementation of the software developed

Indian parent

(service

company)

AE onsite entity

(country X)

Service to 3rd

parties (country

X)

AE development

center (country

Y)

17

©2015 Deloitte Touche Tohmatsu India Private Limited

Service Providers

Provision of Services

Contract Service Provider

Varied Functions

Shared Service Center

Sophisticated Work-force

Routine Service Provider

Non Routine Intangible

Sophisticated Service Provider

+ + +

Functions and Risks

18

©2015 Deloitte Touche Tohmatsu India Private Limited

Key considerations for Transfer Pricing policy

Services• Foreign parent takes decision on conceptualization and functionality of the

software and the development center operate in India on the instructions of the

Foreign parent

• The key issue is between adopting a cost-based model or a man-hour rate model

for the development center

• Cost based model would ensure a risk free return without regard to efficiencies

and capacity utilization

• Man-hour rate model is now increasingly used for reasons that it addresses

issues of efficiency and idle time

19

©2015 Deloitte Touche Tohmatsu India Private Limited

Intra group services

The OECD Guidelines categorize costs incurred in relation to the intra-group

services according to their type and purpose; of which the key segment involves

categorization of costs as chargeable and non-chargeable :-

Costs

"Chargeable"

Associated with services that provide an economic benefit to group

companies

“Directly Allocable costs”

Services that can be identified as

directly benefiting a particular group company, thus allowing for the

costs for the provision of these

services to be directly assigned

"Indirectly Allocable costs”

Services that benefit a number of companies,

but where the costs cannot be readily identified with a specific service performed for a

particular company, in such instances,

allocation keys are used to allocate costs and services provided

"Non-Chargeable"

Costs related to services for which no direct or measurable benefit is bestowed on existing companies

"Shareholder Services”

Any cost related to activities that a parent company

carries out in relation to its capacity as

shareholder of the group

"Services to Acquire/Develop a New Business"

Activities related to the acquisition and divestment of companies and

any type of market or strategy study relating to new markets and

raising funds for acquisitions

"Duplicate Activities and

Incidental Benefit"

Activities undertaken by the service provider

that merely duplicate a

service that a company is

performing for itself or that is

being performed for the company by a third party

20

©2015 Deloitte Touche Tohmatsu India Private Limited

Evidence of benefit – benefit test

Arm‟s length principle test for intra group services is whether the company:-

• receiving the service would have been willing to purchase the service from an

unrelated company or would have incurred the cost to produce the service

internally;

• the activity provides a respective group member with economic or commercial

value to enhance its commercial position; and

• such service is both needed and non-duplicative.

Yes

Cost of

Services

provided

Cost of

Services

provided

Charge to affiliates by

appropriate method

Charge to affiliates by

appropriate method

Incurred to develop

intangibles?

Incurred to develop

intangibles?

Charge ShareholdersCharge Shareholders

Exclude

from allocation

Exclude

from allocation

Set aside for

royalty charge

Set aside for

royalty charge

No

No

YesTo acquire, integrate or develop

new business?

To acquire, integrate or develop

new business?

No

Yes

Performed for specific

affiliates?

Performed for specific

affiliates?

On behalf of

Shareholders?

On behalf of

Shareholders?

Yes

No

Duplicates activities

performed by affiliates?

Duplicates activities

performed by affiliates? Exclude

from allocation

Exclude

from allocation

Yes

Charge ShareholdersCharge Shareholders

OR

Yes

Cost of

Services

provided

Cost of

Services

provided

Charge to affiliates by

appropriate method

Charge to affiliates by

appropriate method

Incurred to develop

intangibles?

Incurred to develop

intangibles?

Charge ShareholdersCharge Shareholders

Exclude

from allocation

Exclude

from allocation

Set aside for

royalty charge

Set aside for

royalty charge

No

No

YesTo acquire, integrate or develop

new business?

To acquire, integrate or develop

new business?

No

Yes

Performed for specific

affiliates?

Performed for specific

affiliates?

On behalf of

Shareholders?

On behalf of

Shareholders?

Yes

No

Duplicates activities

performed by affiliates?

Duplicates activities

performed by affiliates? Exclude

from allocation

Exclude

from allocation

Yes

Charge ShareholdersCharge Shareholders

OR

21

The Optimum Business Model

22

©2015 Deloitte Touche Tohmatsu India Private Limited

BMO - The critical element which links operational strategy with tax strategy

Business Model Optimization (BMO)

• Businesses essentially consist of Assets, Functions, and Risks that generate a

return to their owner.

• Locating value-added Assets, Functions, and Risks efficiently can drive

significant operational and tax savings

• It‟s not enough to locate just the Assets and Risks in a tax-efficient

jurisdiction…must also have functions (i.e., the people)

• BMO is the methodology we use to align the relevant Assets, Functions and

Risks to optimize a multinational company‟s global or regional business model

• BMO is not about tax shifting but about integrating tax in operational outcome

and business transformation

23

©2015 Deloitte Touche Tohmatsu India Private Limited

The Evolution of Operating Models

Highly Tax Efficient

More local

More Centralized

Least Tax Efficient

Quantum of Total Financial Benefits

Supply Chain Principal

Supply Chain Centralized

Brand Management Local

Innovation Local

What is the right model for Newell?

Op

era

tin

g M

od

el

As the operating model evolves, the optimal Tax Aligned Value Chain strategy will change over time.

Full Principal

Supply Chain Centralized

Brand Management Centralized

Innovation Centralized

Country Model

Supply Chain Local

Brand Management Local

Innovation Local

24

©2015 Deloitte Touche Tohmatsu India Private Limited

The trend for the centralization of management aligns

with the centralization of profits

Evolving from a country-led model to a center-led

model:

Transferring the management of functions,

assets, and risks may allow the transfer of

local profits to a jurisdiction suitable for

regional/global management (and, if possible,

complimentary tax efficiency).

Profit from In-CountryOperationsProfit from

In-CountryOperations

Manufacturing Sales and

Distribution

Profit from in-countryoperations

Principal

Operating

Company

Value-addedprofit

Risk-based profit

Value-addedprofit

Risk-based profit

Value-addedprofit

Risk-based profit

Country 1

Country 2

Country 3

Center-led Structure

Profit from In-CountryOperationsProfit from

In-CountryOperationsProfit from

in-countryoperations

Support

Functions

Profit from In-CountryOperationsProfit from

In-CountryOperationsProfit from

in-countryoperations

Country 1 Country 3Country 2

Profit from in-countryoperations

Value-addedprofit

Risk-based profit

Profit from in-countryoperations

Value-addedprofit

Risk-basedprofit

Profit from in-countryoperations

Value-addedprofit

Risk-based profit

Country-led Structure

25

Transfer Pricing as Planning

Tool

26

©2015 Deloitte Touche Tohmatsu India Private Limited

Typical Planning Objectives

Managing the Global Effective Tax Rate

Cash Repatriation

27

©2015 Deloitte Touche Tohmatsu India Private Limited

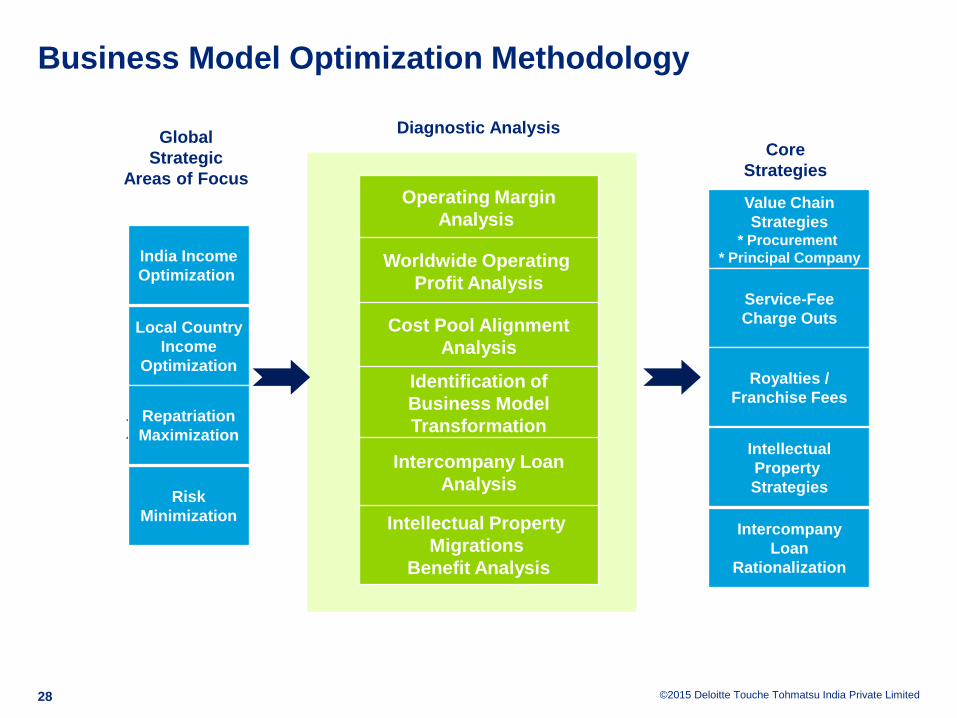

Business Model Optimization Methodology

Core

Strategies

Diagnostic AnalysisGlobal

Strategic

Areas of Focus

India Income

Optimization

Local Country

Income

Optimization

Repatriation

Maximization

Risk

Minimization

Value Chain

Strategies* Procurement

* Principal Company

Service-Fee

Charge Outs

Royalties /

Franchise Fees

Intellectual

Property

Strategies

Intercompany

Loan

Rationalization

Operating Margin

Analysis

Worldwide Operating

Profit Analysis

Cost Pool Alignment

Analysis

Identification of

Business Model

Transformation

Intercompany Loan

Analysis

Intellectual Property

Migrations

Benefit Analysis

28

©2015 Deloitte Touche Tohmatsu India Private Limited

Operating Margin Analysis – An Example

Operating Margin as a % of Sales

Actual Margin Over/(Under) Target

ETR

Segment 1 Domestic 12.00% 33,134

Segment 2 Domestic 9.00% 75,879

Other Domestic 12.00% 28,556

Home Country Total 11.00% 137,569

Country 1 20.92% 65,989 34.70%

Country 2 18.87% 35,040 20.80%

Country 3 22.62% 31,106 29.20%

Country 4 16.37% 27,692 36.70%

Country 4 30.62% 17,833 26.40%

Country 5 17.71% 17,118 10.90%

Country 6 17.26% 11,747 31.20%

Country 7 22.68% 9,487 31.60%

Country 8 10.40% 6,645 14.50%

Country 9 7.34% (7,605) 25.50%

Country 10 10.54% 12,551

Foreign Total 17.76% 227,601 -

Grand Total 16.31% 365,170

• Intended to identify excess (or

inadequate) margin over the

routine returns expected for the

type of function performed

‒ „Excess Margins‟ may indicate

the presence of non-routine

intangibles

• The existence of a “significant”

excess (or lower) return suggests

that the entity should be

investigated further to understand

the variance

‒ Country 1 is a high-tax country

earning excess margins!!

• Understanding these variances

helps identify appropriate global

planning strategies

29

©2015 Deloitte Touche Tohmatsu India Private Limited

Cost Pool Analysis - An Example where a policy is

requiredCharge-out of Service Fee / Franchise Fee / Royalty

• Intended to identify situations where costs are incurred in a particular geography which

bring value to other members of the affiliated group

• Focuses on the concept that the beneficiaries of the endeavor must pay for its costs,

regardless of geographic location

• This analysis helps identify opportunities to create tax efficient income streams, reduce tax

risks, and increase repatriation

Home Country Corporate Cost Pool Per Books 2008

Home Country Foreign Total

Total Home Country Corporate Costs 272,257 18,573

Less: Charge Outs to Business Units (14,884) 14,884

Residual 257,373 33,457 290,830

Percentage 88% 12%

Key Material Cost Pools 2008

Home Country Foreign Total

Sales and Marketing 148,000 149,294 297,294

Percentage 50% 50%

Administrative 257,373 45,380 302,753

Percentage 85% 15%

Total 405,373 194,675 600,047

Worldwide Sales

Home Country Foreign Total

2008 1,926,314 3,922,563 5,848,877

Percentage 33% 67%

67% of sales are foreign yet 88% of corporate costs are borne by home country

30

©2015 Deloitte Touche Tohmatsu India Private Limited

Key Intercompany Loans & Treasury Analysis - An

Example

• Interest rates ranges from 4.00% to 12.50%

• FX management issues

• Negative arbitrage in Netherlands on certain loans

Borrower Country

Borrower Tax

Rate Lender Country

Lender Tax

Rate Currency Principal Interest Rate

Netherlands ¹ 29.60% United States 35.00% EUR 125,689,309.00 8.750%

Netherlands 29.60% Netherlands 29.60% EUR 125,689,309.00 8.880%

Netherlands 29.60% Belgium 17.00% EUR 99,685,000.00 7.000%

UK 30.00% Netherlands 29.60% EUR 75,448,954.00 9.000%

Netherlands 29.60% Netherlands 0.00% EUR 69,578,438.00 12.375%

Netherlands ¹ 0.00% Luxembourg 30.00% EUR 69,578,437.50 6.000%

UK 30.00% UK 30.00% GBP 58,892,221.00 9.000%

Italy ³ 37.25% Netherlands 29.60% EUR 51,785,739.52 12.500%

Netherlands ² 29.60% Denmark 29.60% EUR 45,000,000.00 ?

Netherlands ¹ 29.60% United States 35.00% EUR 43,587,697.88 7.500%

Germany ¹ 26.38% Netherlands 29.60% EUR 39,095,567.00 9.000%

Austria ¹ 25.00% Spain 35.00% EUR 34,502,080.00 4.600%

Netherlands ¹ 29.60% Luxembourg 30.00% EUR 27,211,766.00 6.750%

Sweden ¹ 28.00% Luxembourg 30.00% EUR 26,564,712.00 5.000%

Netherlands ¹ 29.60% Italy 37.25% EUR 25,000,000.00 4.600%

Netherlands 29.60% Switzerland 9.80% EUR 25,000,000.00 4.600%

United States ² 35.00% Canada 34.34% CAD 20,927,467.29 ?

Germany ¹ 26.38% Netherlands 29.60% EUR 20,111,878.99 12.500%

Canada ¹ 34.34% United States 35.00% CAD 19,715,732.00 12.250%

Netherlands 29.60% Netherlands 29.60% EUR 19,287,819.53 7.630%

Netherlands ¹ 11.00% Luxembourg 30.00% EUR 18,198,041.65 4.600%

Netherlands ¹ 29.60% France 33.33% EUR 18,000,000.00 4.600%

France 33.33% France 33.33% EUR 16,338,830.00 4.000%

Netherlands ¹ ² 29.60% Luxembourg 30.00% EUR 15,428,527.00 ?

Total Euro 990,782,107.07

Total UK Pound 58,892,221.00

Total Canadian Dollars 40,643,199.29

1. Loans have negative rate arbitrage (i.e., the lender's income tax rate is higher than the borrower's income tax rate)

2. Unable to determine interest rate for these loans (to be confirmed)

3. Assumed interest deductible in Italy

Intercompany Loan Schedule > 15 Million

31

BEPSBASE EROSION & PROFIT SHIFTING –

SHOULD IT CHANGE THE WAY WE DO TAX PLANNING?

32

©2015 Deloitte Touche Tohmatsu India Private Limited33

BEPS Objectives: a new global tax environment

33

©2015 Deloitte Touche Tohmatsu India Private Limited34

BEPS Timetable

09/2014 09/2015 12/2015

• Digital economy

• Hybrid mismatches

• Harmful tax practices – phase 1

• Treaty abuse

• Intangibles

• Transfer pricing (“TP”) documentation

• Multilateral instrument – phase 1

• Controlled Foreign Corporation (CFC) rules

• Permanent establishments

• Interest deductions – phase 1

• Harmful tax practices – phase 2

• Risk and capital, other high-risk transactions

• Disclosure of aggressive tax planning

• Dispute resolution

• Data collection and analysis measuring BEPS

• Interest deductions – phase 2

• Harmful tax practices – phase 3

• Multilateral instrument – phase 2

34

©2015 Deloitte Touche Tohmatsu India Private Limited35

BEPS Action 8, 9 & 10

Expected Output: Changes to the Transfer Pricing Guidelines and possibly to the Model Tax Convention

Deadline: September 2015

Action 8 - Intangibles

• Develop rules to prevent BEPSby moving intangibles amonggroup members.

• This will involve: (i) adopting abroad and clearly delineateddefinition of intangibles; (ii)ensuring that profits associatedwith the transfer and use ofintangibles are appropriatelyallocated in accordance with(rather than divorced from) valuecreation; (iii) developing transferpricing rules or special measuresfor transfers of hard-to-valueintangibles; and (iv) updating theguidance on cost contributionarrangements.

Action 9 - Risk & Capital

• Develop rules to prevent BEPS by transferring risks among, or allocating excessive capital to, group members.

• This will involve adopting transfer pricing rules or special measures to ensure that inappropriate returns will not accrue to an entity solely because it has contractually assumed risks or has provided capital. The rules to be developed will also require alignment of returns with value creation.

• This work will be coordinated with the work on interest expense deductions and other financial payments.

Action 10 - Other high-risks transactions

• Develop rules to prevent BEPSby engaging in transactionswhich would not, or wouldonly very rarely, occurbetween third parties.

• This will involve adopting transferpricing rules or special measuresto : (i) clarify the circumstances inwhich transactions can be re-characterized; (ii) clarify theapplication of transfer pricingmethods, in particular profitsplits, in the context of globalvalue chains; and (iii) provideprotection against common typesof base eroding payments, suchas management fees and headoffice expenses.

Assure that TP Outcomes are in line with Value Creation

35

Questions?

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee,

and its network of member firms, each of which is a legally separate and independent entity. Please

see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited

and its member firms.

This material and the information contained herein prepared by Deloitte Touche Tohmatsu India Private Limited

(DTTIPL) is intended to provide general information on a particular subject or subjects and is not an exhaustive

treatment of such subject(s). None of DTTIPL, Deloitte Touche Tohmatsu Limited, its member firms, or their related

entities (collectively, the “Deloitte Network”) is, by means of this material, rendering professional advice or

services. The information is not intended to be relied upon as the sole basis for any decision which may affect you

or your business. Before making any decision or taking any action that might affect your personal finances or

business, you should consult a qualified professional adviser.

No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies

on this material.

©2015 Deloitte Touche Tohmatsu India Private Limited. Member of Deloitte Touche Tohmatsu Limited