training futurum : restructuring transactions under common control

TRANSCRIPT

Restructuring

Transactions under

Common Control

The Most Common Types of Restructurings Involving

Entities Under Common Control

Creation of a New Company and transfer of business to the new company (also referred

to as spin-offs) in anticipation of a listing of securities or sale of business or debt raising

or taking benefit of a tax advantageous territory etc.

Group reorganisation involving moving of assets or entities within the group mainly

driven by tax or financial considerations or for simplification of group structure. Similar

to spin-offs, these could take several forms as these reorganisations are driven by

varied necessities. Mergers and amalgamations of group entities are the most common

forms of reorganisations.

Corporate Restructuring

Expansion

• Amalgamation

• Absorption

• Tender Offer

• Asset Acquisition

• Joint Venture

Contraction

• Asset Sale

• Demerger :

• Spin off

• Equity carve out

• Split off

• Split up

• Divestitures

Corporate Control

• Going Private

• Equity Buyback

• Leveraged Buyouts

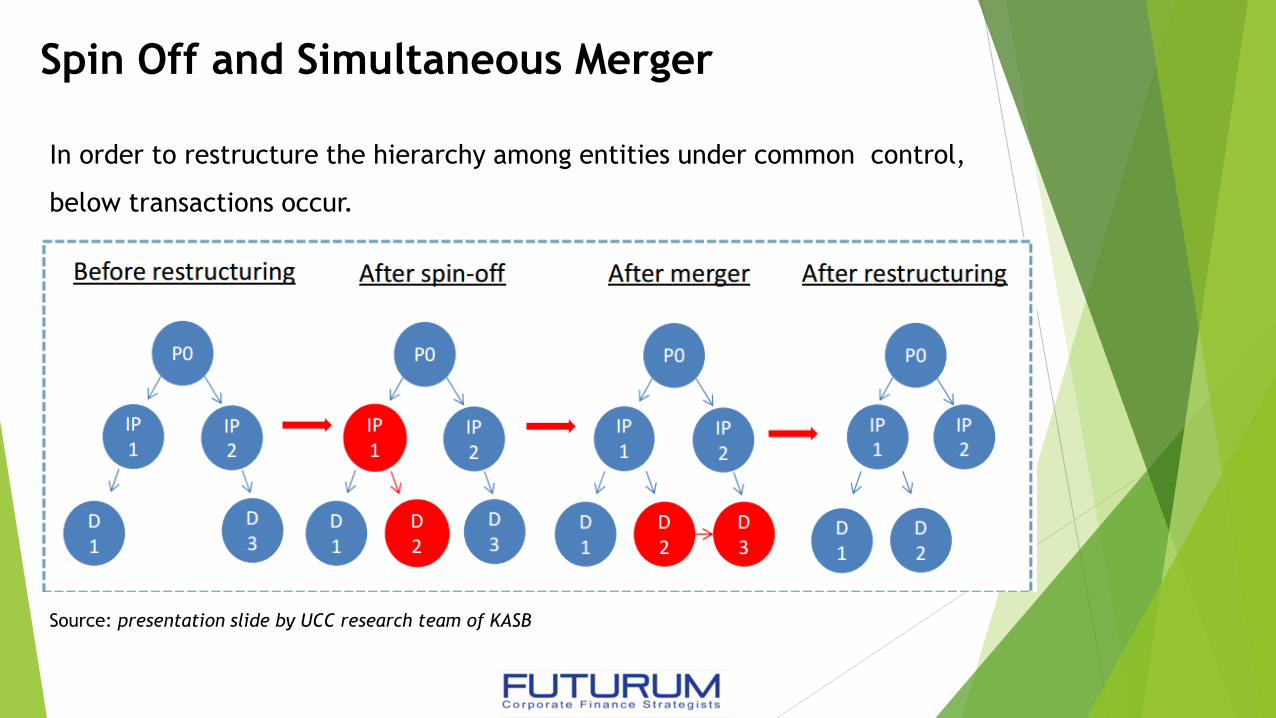

Spin Off and Simultaneous Merger

In order to restructure the hierarchy among entities under common control,

below transactions occur.

Source: presentation slide by UCC research team of KASB

Group Reorganizations

Group reorganizations involve the restructuring of the relationships between

companies in a group (or under common control) and can take many forms, for

example:

Setting up a new holding company

Changing the direct ownership of subsidiaries within the group (possibly

involving the creation of a new intermediate holding company)

Transferring businesses from one company to another

Group Reorganization : How to Account For?

Did I buy a group of assets or a business?

Why should I care?

Determining whether an acquired group of assets is a business has proven to

be one of the more challenging aspects of applying the current M&A

accounting guidance

Asset Acquisition Business

Combination

DO WE BUY BUSINESS OR ASSETS?

HAVE ACCOUNTING AND TAX DIFFERENCES

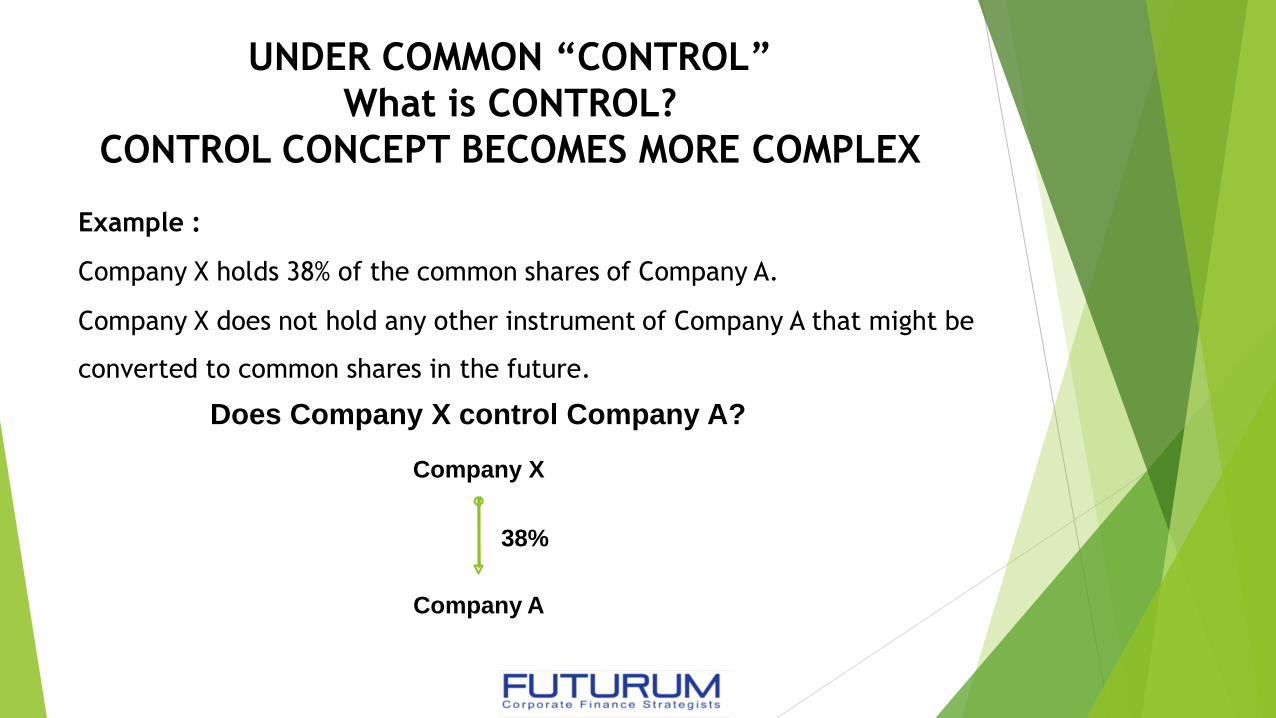

UNDER COMMON “CONTROL”

What is CONTROL?

CONTROL CONCEPT BECOMES MORE COMPLEX

Example :

Company X holds 38% of the common shares of Company A.

Company X does not hold any other instrument of Company A that might be

converted to common shares in the future.

Does Company X control Company A?

Company X

38%

Company A

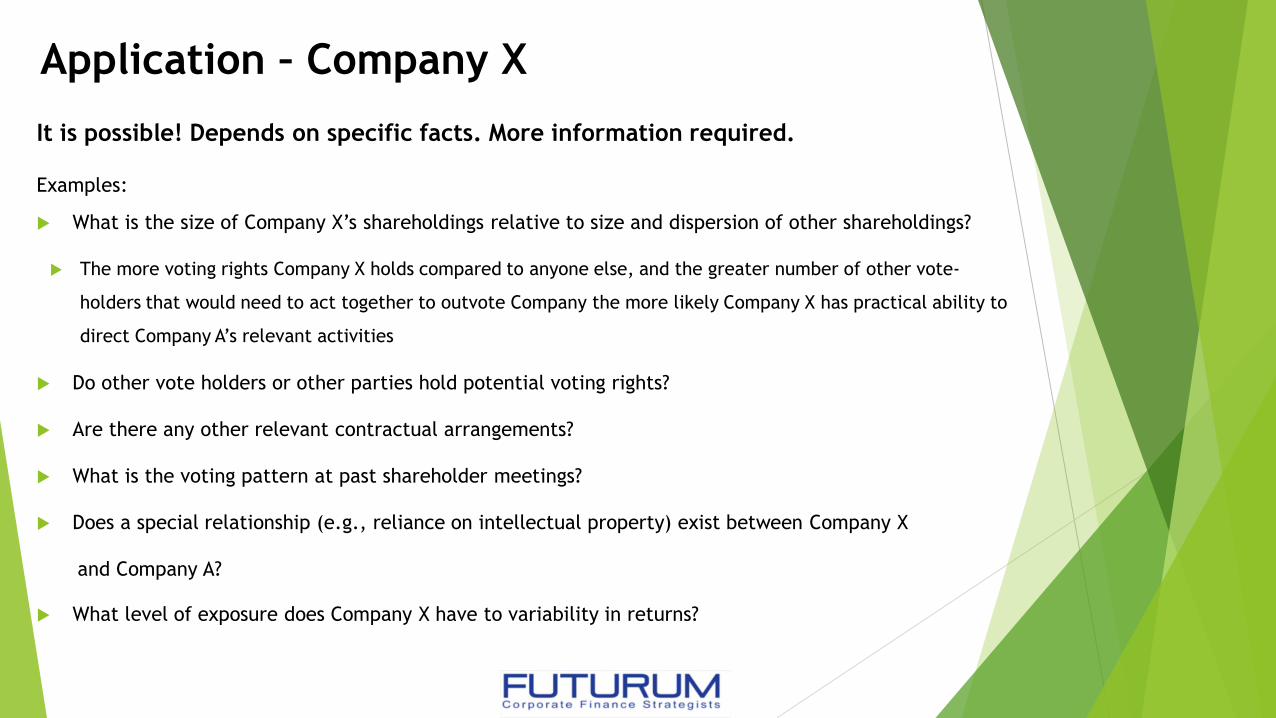

Application – Company X

It is possible! Depends on specific facts. More information required.

Examples:

What is the size of Company X’s shareholdings relative to size and dispersion of other shareholdings?

The more voting rights Company X holds compared to anyone else, and the greater number of other vote-

holders that would need to act together to outvote Company the more likely Company X has practical ability to

direct Company A’s relevant activities

Do other vote holders or other parties hold potential voting rights?

Are there any other relevant contractual arrangements?

What is the voting pattern at past shareholder meetings?

Does a special relationship (e.g., reliance on intellectual property) exist between Company X

and Company A?

What level of exposure does Company X have to variability in returns?

The Control Model : An Overview

An investor controls an investee when

it is exposed, or has rights, to variable

returns from its involvement with the

investee and has the ability to affect

those returns through its power over

the investee.

Exposure to

variable returns

Power

Link power- returns

control

Assessing Control of An Investee

Rights Ability to

use power

over the

investee to

affect its

own returns

Exposure

(or rights)

to variable

returns of

the investee Relevant activities

Q: Advice for Assessing The Existence of

Control

Hint: Call an IFRS expert!

New Companies in Common Control

Transactions and Transfer within Group

Formation of a new company to facilitate disposal of business

Business brought together into a new company before an IPO

Setting up a new top holding company in exchange for equity

Setting up a new top holding company : transactions including cash consideration

Inserting a new intermediate parent within an existing group

Transferring businesses outside an existing group using a new company

Transferring associates/joint ventures within an existing group

Accounting for Business Combinations involving

entities or businesses under common control

Pooling of interests method or Predecessor accounting

Acquisition method

The fresh-start method

Capital reorganization accounting

PSAK 38 (revisi 2012)

Training Desktop

Date : See at the website “futurum corfinan” (2-day training)

Venue : Hotel at Jakarta Pusat

Notes :

• Presentation slides will be distributed in softcopy

• Minimum participants = 10 persons

• After the training, participants are allowed to discuss about the training materials via

email in the website

Contact email : [email protected]

Visit Website and Training Testimonials : google “futurum corfinan”