trade through global value chains: can wto rules have a rolewtocentre.iift.ac.in/cbp/gvc.pdf ·...

TRANSCRIPT

Trade Through Global Value Chains: Can WTO Rules Have a Role

Abhijit Das

Professor and Head

Centre for WTO Studies, IIFT, New Delhi

Why GVCs relevant?

• During the Eight WTO Ministerial Conference held in Geneva in 2011, some Ministers said that the WTO needed to pay more attention to global value chains.

• Considerable work being done on GVCs in various international organisations

• OECD WTO TIVA

• Specific reference to GVCs in G20 Los CabosDeclaration

Los Cabos Declaration

• We value the discussion held by our Trade Ministers in Puerto Vallarta on the relevance of regional and global value chains to world trade, recognizing their role in fostering economic growth, employment and development and emphasizing the need to enhance the participation of developing countries in such value chains. We encourage a deepening of these discussions in the WTO, UNCTAD and OECD within their respective mandates, and we call on them to accelerate their work on analyzing the functioning of global value chains and their relationship with trade and investment flows, development and jobs, as well as on how to measure trade flows, to better understand how our actions affect our countries and others, and to report on progress under Russia's Presidency

Structure of presentation

• What are GVCs, why are they important

• Drivers of GVC integration

• How are gains distributed in GVCs

• Implications of GVCs for trade policy and trade negotiations

What are GVCs, why are they important ?

What is a GVC

• A global value chain (GVC) is a chain of separate but inter-linked and coordinatedactivities, which can be undertaken within a single firm or be divided among multiple firms in different geographical locations to bring out a product or a service from conception to complete production and delivery to final consumers.

Structure of GVCs

• Structured around a lead firm and network of contract manufacturers, suppliers, logistics providers etc.

• Lead firms take key decisions in the GVC and exercise control over other players, even in absence of ownership.

• Lead firm – supplier relationship determined by perceived risk to the buyer arising on account of failure of the producer to supply quality products on a reliable and timely basis

Buyer/ supplier driven GVCs

• Buyer- driven GVC: Lead firms are large retailers marketers and brand owners (Walmart, Nike etc.)

Product specification prescribed by leadfirm, manufacturing done by decentralized developingcountry manufacturers.

Lead firms retain close control on the suppliers• Producer driven chains: Lead firms are manufacturers

making advance products Exert control over backward linkages for raw materials and

component suppliers; forward linkage in distribution and retailing

Automobile manufactures, PC manufacturers are good examples of producer driven GVCs

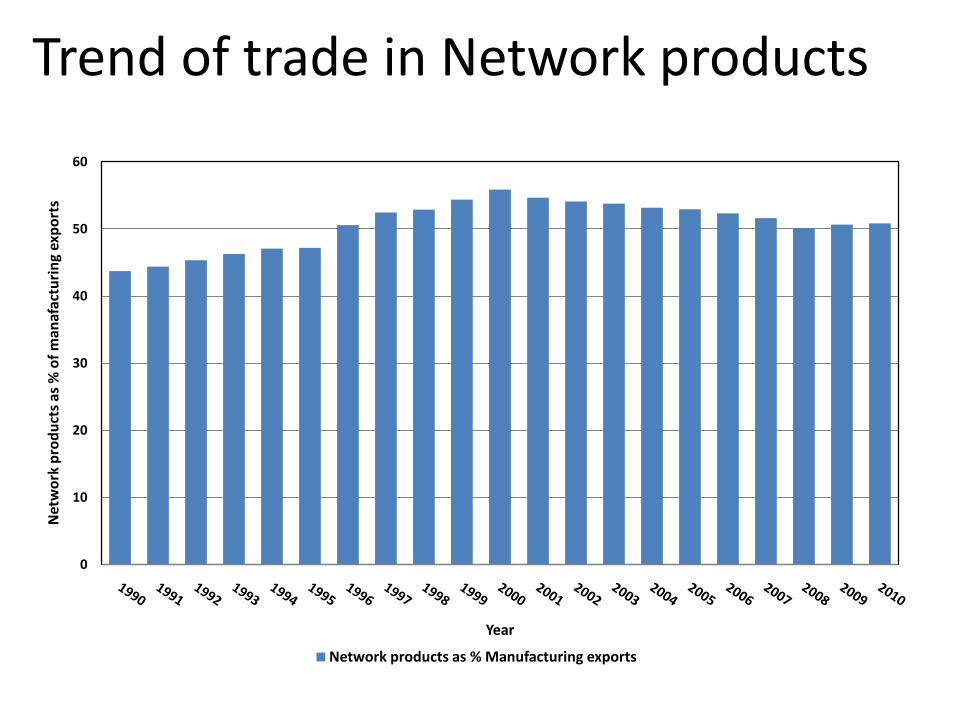

Trend of trade in Network products

0

10

20

30

40

50

60

Net

wo

rk p

rod

uct

s as

% o

f m

anaf

actu

rin

g ex

po

rts

Year

Network products as % Manufacturing exports

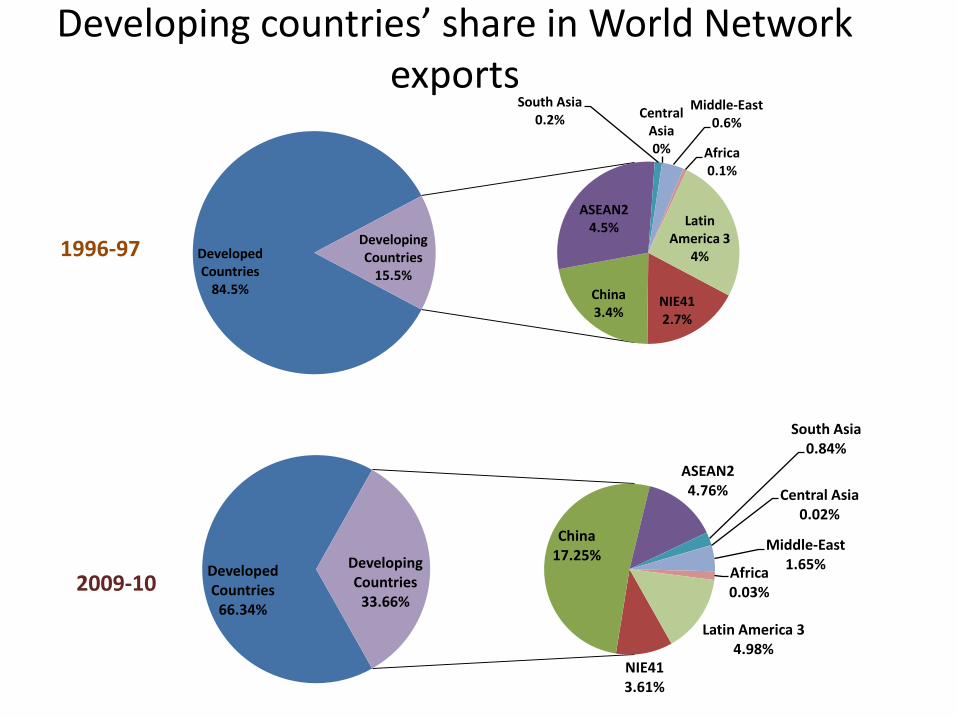

Developing countries’ share in World Network exports

Developed Countries

84.5%NIE412.7%

China3.4%

ASEAN24.5%

South Asia0.2% Central

Asia0%

Middle-East0.6%

Africa0.1%

Latin America 3

4%Developing Countries

15.5%

1996-97

Developed Countries

66.34%

NIE413.61%

China17.25%

ASEAN24.76%

South Asia0.84%

Central Asia0.02%

Middle-East1.65%

Africa0.03%

Latin America 34.98%

Developing Countries

33.66%2009-10

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

Icel

and

Esto

nia

Ne

w Z

eala

nd

Slo

ven

ia

Luxe

mb

ou

rg

Slo

vak

Re

pu

blic

Po

rtu

gal

Isra

el

Gre

ece

Hu

nga

ry

Fin

lan

d

Ch

ile

Sou

th A

fric

a

Cze

ch R

ep

ub

lic

Turk

ey

De

nm

ark

Me

xico

Ire

lan

d

Po

lan

d

Au

stri

a

Swed

en

Ind

on

esia

Bra

zil

Swit

zerl

and

Ind

ia

Bel

giu

m

Spai

n

Can

ada

Au

stra

lia

No

rway

Net

her

lan

ds

Ital

y

Fran

ce

Ko

rea

UK

Ru

ssia

n F

eder

atio

n

Jap

an

Ch

ina

Ger

man

y

Un

ite

d S

tate

s

Re

st o

f th

e W

orl

d

Value Added Exports in GVC (2009)

Value- Added exports (FDDVA) VA exports of a country embodied in gross exports of other countries (based on EXGR_FVA)

Drivers of GVC integration

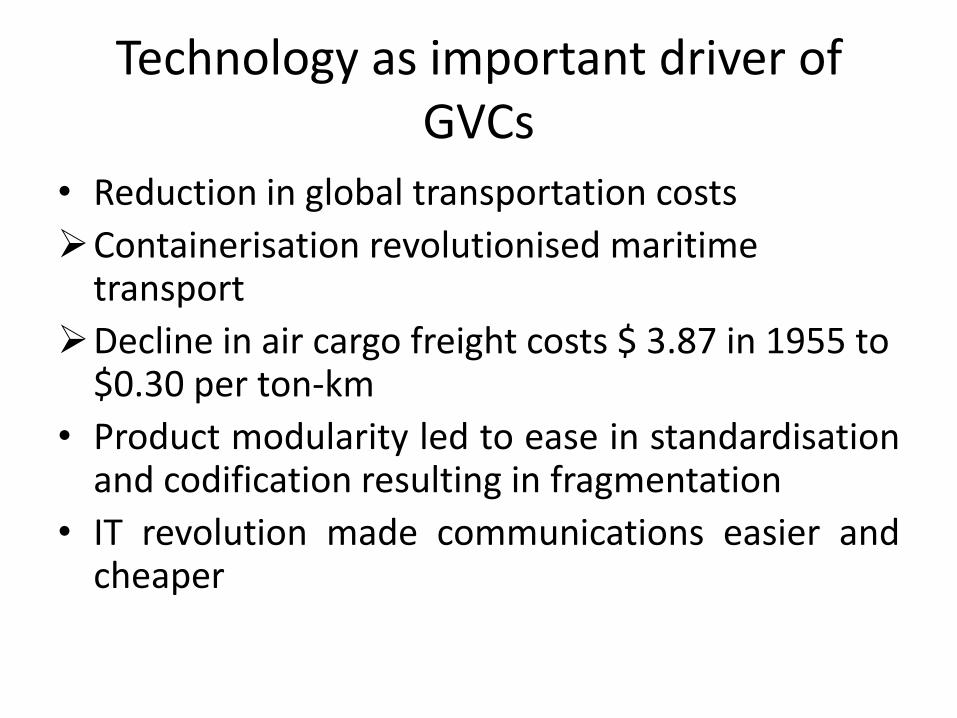

Technology as important driver of GVCs

• Reduction in global transportation costs

Containerisation revolutionised maritime transport

Decline in air cargo freight costs $ 3.87 in 1955 to $0.30 per ton-km

• Product modularity led to ease in standardisationand codification resulting in fragmentation

• IT revolution made communications easier andcheaper

What factors determine decision of lead firms to link with suppliers?

• Labour cost arbitrage• Skilled labour and managers• Availability of trade-related physical

infrastructure• Trade logistics and support services• Ease of doing business• Proximity to markets• Role of tariffs• Duty free access to markets• Ability to comply with standards

How are gains distributed in GVCs

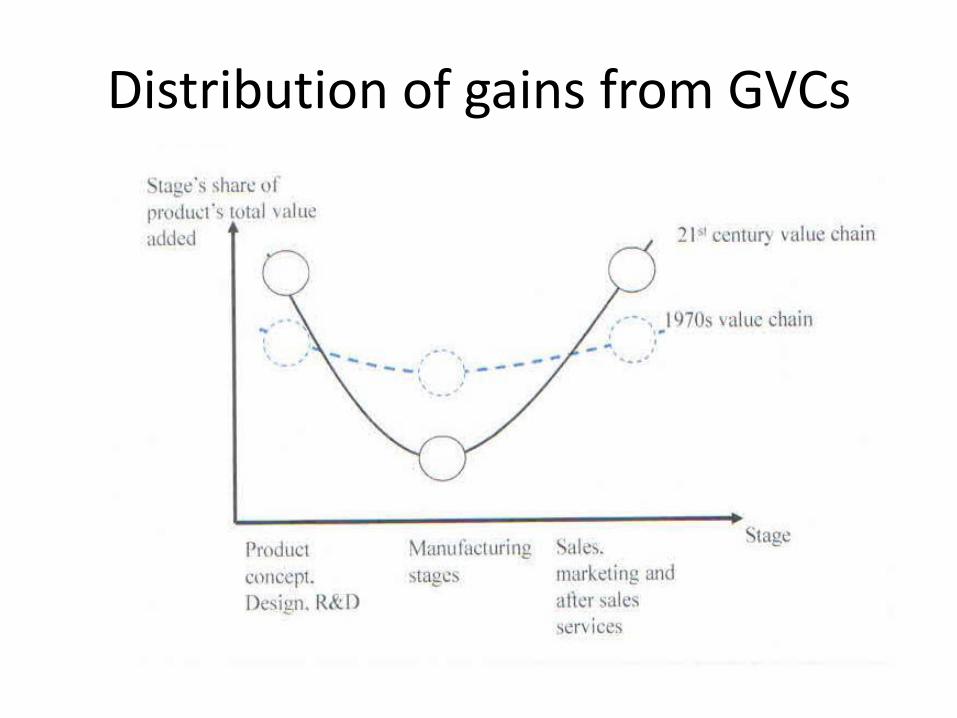

Distribution of gains from GVCs

Case studies on distribution of gains in GVCs

• i-Pod: value added in China $ 4 out of retail price of $ 299

• Nokia N-95: assembled in China but 68 % va in Europe

• i-Pad: Apple’s gross margin 54%

• Dell PCs: 50% profit to IBM, 20% to Dell but less than 5% to Quanta (Taiwan manufacturer)

• Home furnishing: Indian producer’s unit price $ 20/m, retailed at 5 – 6 times price in US/EC

Case studies on distribution of gains in GVCs

• Coffee: 40% of gains to traders, 45% gains to roasters and remaining 15% to 25 mn farmers

• Fresh vegetables from Kenya: producers account for 15% income, super markets for 45% income

• Canned deciduous fruits: 12.4% income to producers, 26.7% to retailers

Participation Rate (in %) of top 20 countries and economies: 2000 and 2009

0.00 2.00 4.00 6.00 8.00 10.00 12.00 14.00

Russian …

Sweden

Ireland

Singapore

Malaysia

Mexico

Spain

Chinese …

Belgium

China

Korea

Netherlands

Canada

Italy

Rest of …

France

United …

Japan

Germany

United …

50 % Backward Linkage (in perecentage)

50 % Forward Linkage(in percentage)

0.00 2.00 4.00 6.00 8.00 10.00

Sweden

India

Malaysia

Ireland

Canada

Switzerland

Spain

Belgium

Singapore

Chinese Taipei

Russian Federation

Netherlands

Italy

United Kingdom

Korea

France

Japan

Rest of the World

Germany

United States

China

Distribution of Forward Linkage in GVCs

0

50

100

150

200

250

300

350

400

450

Valu

e in

US

D B

illi

on

Forward Linkage 1995 Forward Linkage 2005 Forward Linkage 2009

Poly. (Forward Linkage 1995) Poly. (Forward Linkage 2005) Poly. (Forward Linkage 2009)

GVCs: Continue to remain a developed country story

• Italy, Japan, Spain, UK and USA are the only countries which are major players in backward and forward linkage, who also add more value to other countries exports than the value added by others in their exports.

• China’s participation high, but gains low.

China adding low value to imported inputs

Why are developing countries locked at low end value addition in GVCs

• Intrinsic reasons

Lack of specialized skills

Difficulty in accessingtechnology, inputs, market, information, creditetc.

Lack of physical infrastructure availability of resources and efficient and effective coordination in value chains

Role of GVC governance in distribution of gains

• Lead firms tend to outsource lower-value-added activities (including final assembly) while retaining control over the higher-value-added areas of their core competency, such as like R&D, intellectual property, design and distribution.

• The lead firms benefit from the severe competition among numerous and almost identical suppliers, and select the ones that meet their short-term requirements.

Role of GVC governance in distribution of gains

• Differences in market power and dependency relationships have a clear impact on the choice of governance regime in trade relationships. A powerful party can dictate governance mechanisms and distribution of gains.

• Local producers face obstacles to functional upgradation because such upgrading encroaches on their buyers' core competence: Brazil footwear, Taiwan AsusTek

Low entry barriers for manufacturing but high barriers for non-tangible

activities

• Manufacturing has low barrier to entry, resulting in high competition. Given the competitive nature of the market at the lower ends of manufacturing increases the substitution possibilities and thus reduces the bargaining power of any one firm.

• In a world in which shifting competitive advantage leads to producers being forced out of the market, it is not surprising that manufacturing tasks generate the least valued added in a GVC.

• Thus just as barriers to entry in manufacturing are falling, so barriers to entry in branded marketing are increasing.

Implications of GVCs for trade policy and trade

negotiations

Trade policy challenges of GVCs

• Asymmetrical impact of trade policy measures on firms integrated in GVCs and those outside it.

• Tariffs

• Antidumping / countervailing / safeguard duties

• Rules of origin: value addition norms and cumulation

Issues relevant in GVC negotiations

• Like product (conceptual clarification)

• Tariff reduction / elimination (sectoralinitiative through the backdoor)

• Trade facilitation (Bali decision using GVC)

• Harmonisation of standard

• Trade remedies (conceptual clarity required)

• Rules of origin (conceptual clarity required)

• Services (higher liberlisation in some sectors)

Issues relevant in GVC negotiations

• Investments and competition (re-emergence of some of Singapore issues)

• Labour standards (Lamy panel recommendations)

• IPRs

• Agriculture subsidies (developed countries farm subsidies have squeezed efficient producers from GVCs

Thank You