tplace on main odeo y agon finals ating club ars 69th ... 2013...the organizations we invested in...

TRANSCRIPT

69th Annual Report

Building Our Community In Its Centennial YearWe are proud to have been a major community sponsor thoughout 2013

Air Show

Marketplace on Main

Chuckwagon Finals

STARS

Rocky Pro Rodeo

Relay for Life

Cattlemen’s Day

Speed Skating Club

2013 Annual Report

Table of ContentsRocky Credit Union Profile ............................................. 2Message from the Board President .............................. 3Message from the CEO .................................................. 4VP, Member Services Report ......................................... 7VP, Financial Services Report ........................................ 8VP, Credit & Risk Report ................................................ 9VP, Finance Report .......................................................10Building Expansion .......................................................13Board of Directors for 2013 ........................................14Management and Staff ................................................14RCU Wealth Management ...........................................16Commercial Financing, Special Projects .................... 17Investing in our Community .........................................18Financial Statements ...................................................20

Pro Rodeo and Chuckwagon photos by Shellie Scott Photography

Airshow photo by Rob Ironside

Community Investment

Rocky Credit Union has always contributed to the well-being of our community beyond the standard role of financial services and advice that financial institutions play.

Rocky Credit Union regularly invests capital and time in the Rocky Mountain House region to help create a healthy and prosperous community. Throughout this report we are proud to show pictures of some of the organizations we invested in this past year.

75th ALBERTA CREDIT UNIONSCELEBRATING YEARS1938 - 2013

75 RCU Staff celebrating Rocky Mountain House’s Centennial in front

of the Credit Union’s expansion

2

Girl Guides, Brownies & Sparks

Cookie Jar Preschool

Rocky Credit Union Profile

OUR VISION:

Helping members succeed. Building our community.

Who We Are:

Rocky Credit Union was founded in 1944 by people who wanted a bank that would help local people have the opportunity to grow and prosper by providing good financial service and sound financial advice while sharing the profits in the local community rather than sending them somewhere else.

Since then Rocky Credit Union has evolved into a full service financial institution with:

Lending services and expertise for consumer mortgages and loans, • and the commercial/agriculture industry.

Investing and Wealth Management services for those looking to grow • and protect their savings and retirement funds.

Convenient online and mobile banking services along with a secure • online loan application.

Over $330 million in assets and 11% equity, providing a strong • financial foundation to serve the community for years to come.

With 45 staff to serve the community, and a real dedication to improving the lives of our members through community investment support, Rocky Credit Union is the place to go to get financial services and feel good about it at the same time.

3

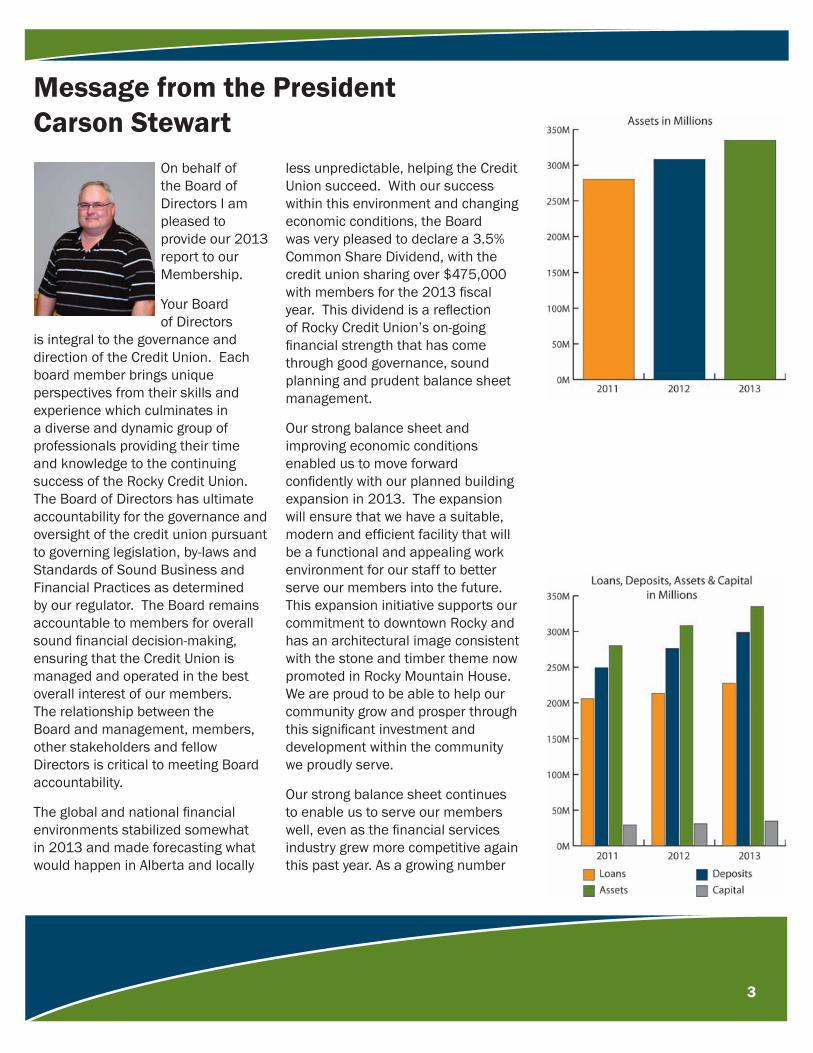

Message from the PresidentCarson Stewart

On behalf of the Board of Directors I am pleased to provide our 2013 report to our Membership.

Your Board of Directors

is integral to the governance and direction of the Credit Union. Each board member brings unique perspectives from their skills and experience which culminates in a diverse and dynamic group of professionals providing their time and knowledge to the continuing success of the Rocky Credit Union. The Board of Directors has ultimate accountability for the governance and oversight of the credit union pursuant to governing legislation, by-laws and Standards of Sound Business and Financial Practices as determined by our regulator. The Board remains accountable to members for overall sound financial decision-making, ensuring that the Credit Union is managed and operated in the best overall interest of our members. The relationship between the Board and management, members, other stakeholders and fellow Directors is critical to meeting Board accountability.

The global and national financial environments stabilized somewhat in 2013 and made forecasting what would happen in Alberta and locally

less unpredictable, helping the Credit Union succeed. With our success within this environment and changing economic conditions, the Board was very pleased to declare a 3.5% Common Share Dividend, with the credit union sharing over $475,000 with members for the 2013 fiscal year. This dividend is a reflection of Rocky Credit Union’s on-going financial strength that has come through good governance, sound planning and prudent balance sheet management.

Our strong balance sheet and improving economic conditions enabled us to move forward confidently with our planned building expansion in 2013. The expansion will ensure that we have a suitable, modern and efficient facility that will be a functional and appealing work environment for our staff to better serve our members into the future. This expansion initiative supports our commitment to downtown Rocky and has an architectural image consistent with the stone and timber theme now promoted in Rocky Mountain House. We are proud to be able to help our community grow and prosper through this significant investment and development within the community we proudly serve.

Our strong balance sheet continues to enable us to serve our members well, even as the financial services industry grew more competitive again this past year. As a growing number

4

Rocky Elementary SchoolDinner & Diamonds Fundraiser

Northern Crossing Music & Drama Society

of our members work non-traditional hours away from Rocky Mountain House, delivering excellent service through technology alternatives is becoming more important every year. To ensure transactional security for our members, security improvements such as Direct Banking Alerts were introduced to help protect our members in an environment that continues to witness the growth of numerous unscrupulous and fraud related activities. The Credit Union is committed to technology solutions that will support product needs, service efficiencies and service reach for our members.

In 2013 we continued to demonstrate our community support by donating capital and staff time to a variety of local community events and organizations. We are a reflection of the communities we serve. We believe that investing in the communities in which we live and work is the right thing to do and makes good business sense. We continue to be extremely proud of our significant community support and highlights of our donations and a list of the community

organizations and events that the credit union supported in 2013 can be found throughout this report.

2014 looks to be an exciting year for us. Jobs in the very important oil and gas industry are returning, and with those jobs will come more local economic development which we are ready to serve and be a part of. As a Board we have confidence in management and staff to achieve Rocky Credit Union’s potential while continuing to “Help Members Succeed” and “Build Our Community”. We appreciate their hard work and commitment to the credit union, and acknowledge the staff’s community commitment with over 1,794 volunteer hours given to the community in 2013. Their great work and service help make Rocky Mountain House and area a better place to live.

The Board would like to thank you, our Members, for continuing to support your Credit Union. We strive to provide the best financial service to our Members and community.

Message from the CEODoug Glessing

I am very proud to be part of an organization that for over 69 years has maintained its fundamental business philosophy of quality personalized

service, financial value and commitment to our community. While these standards are noticeably absent in so many businesses today, these fundamentals have been the catalyst to “help members succeed and build our community”. In an extremely competitive financial services marketplace we believe Rocky Credit Union’s growth and future prosperity

5

will continue to be driven by the quality personalized service, the financial value and the commitment to community that is our tradition and trademark.

2013 was a very successful year due to a sustained focus on prudent balance sheet management, along with deliberate and careful cost management practices. These practices have been instrumental in allowing us the ongoing ability to pay above comparable marketplace dividend rates within this historic low rate economic environment. For 2013 the 3.5% dividend totaled over $475,000, bringing the five year dividend allocation to our member/owners to over $2.2 million dollars and now with $5.5 million dollars in member allocations distributed over the last eight years. In the last five years we also donated over $280,000 in capital and support to community events and organizations in the Rocky Region. More information on other 2013 performance results are provided within the Executive Management Team’s messages within this Annual Report, while community support highlights are featured throughout the report.

Rocky Credit Union is committed to proactively meeting the local economic challenges within the global and Alberta economic environments. As well, Rocky Credit Union is committed to proactively meeting or exceeding the growing regulatory compliance requirements within the increasingly complex dynamics of the financial services industry. Within this environment we remain focused on providing competitive rates and innovative products and

services through in-house expertise, technology and utilizing a unique co-operative partnership approach. While we strive to build on the personal service standards that our members embrace and which identify our Credit Union, we will continue to use technology advancements to add new and improved access channels to extend our service reach for our ever changing and more mobile membership base. We strive to meet all of our Member’s evolving financial service requirements and remain a leader in a fast changing financial services environment.

Rocky Credit Union is very cognizant of the economic impacts to our organization within the economic swings witnessed provincially and internationally. We have worked hard, and will continue to work hard, to proactively create a strong balance sheet and low cost structure, while providing all of the financial products and services that are required by our Members. Our quality member service approach will continue to drive our success in the future. These efforts will continue to allow us to successfully navigate through inconsistent economic times and ever changing financial industry trends.

With proactive planning and successful results in mind, in 2013 we were very comfortable in moving forward with our planned building expansion. The expansion ensures that we have an adequate, up to date, functionally efficient facility with a work environment for our staff that better serves our members into the future. Our due diligence and planning has resulted in a second floor addition design that is very cost

6

Rocky Figure Skating Club

Rocky North & South4H Beef Clubs

effective, space efficient and has an architectural image consistent with the stone and timber theme now promoted in Rocky Mountain House. We are proud to be able to help our community grow and prosper through this development investment and commitment to Rocky Mountain House. Our cautious approach to the building expansion ensures that we remain committed to the financial well-being of our membership and we can continue to offer very competitive rates, quality products and superb service in a modern, convenient, and very efficient work environment.

As the second floor addition to the existing building had proven to be the most prudent approach to a necessary expansion, we worked hard to ensure that the service interruptions to our Members would be minimized throughout the project. We would like to sincerely thank the Members, staff and community for their patience, cooperation and understanding through the disruptions and inconvenience and we trust that the great results will bring added pride in our Credit Union and atonement for any sacrifices required throughout the project timeline.

Rocky Credit Union will continue to “build our community” by building on both the ongoing financial investment initiatives that we are known for within the community and through the ongoing support and encouragement we provide towards wide-ranging volunteer efforts from our very community minded employees.

Along with our loyal Membership, we would not be successful without our

great employees. Rocky Credit Union has worked very hard to attract and retain top-quality people and I cannot say enough about their dedication and skills. Just as we invest in products and services, technologies and facilities, we also must invest in our people. We continue to invest significant dollars in employee training and development intended to enhance the quality financial services culture within the Credit Union. Our evolving “FOCUS” (Finding Opportunities – Creating Unlimited Success) culture helps identify and offer financial service opportunities to our members, strengthening proven trust relationships to “help members succeed and build our community”. In 2014 we will continue to support our employees with a comprehensive Human Resource solutions review project that will ensure competitive job profiles with matched compensation, updated comprehensive personnel policies, along with appropriate training and development policies to allow employee success within a clear performance management rewards and motivation system.

Our success really speaks to the commitment of our Board and Staff to make Rocky Credit Union the best place around to do all of your banking business. I feel very fortunate to be a part of such a successful credit union with a loyal membership and staffed with an array of great people and I proudly look forward to the continued success of the Credit Union and community.

7

Relay For LifeFight Against Cancer Event

Leslieville Elementary School Penny Carnival

Message from the VP, OperationsTammy Young

2013 was a very busy year for us at Rocky Credit Union.

Direct Banking Alerts

Rocky Credit Union has implemented an

additional security feature for online banking. The Direct Banking Alerts feature allows our members to receive security notifications about account access events that have occurred on their accounts. They will receive these alerts either by email or mobile text message. In total there are 5 different types of alerts a member can choose. i.e.: a new bill payment vendor has been added to their account, or Online PAC has been changed, or that a security question was answered incorrectly.

Bank of Canada

The Bank of Canada continued to release the new polymer notes in 2013 with the 10’s, and 5’s being introduced into circulation. The new polymer notes are expected to remain cleaner, and to last at least 2.5 times longer than the current cotton-paper bank notes, thereby improving machine handling.

After the Mint ceases distribution of the penny in February, businesses will be asked to return pennies through their financial institutions to the Mint

for melting and recycling of the metal content. The Government of Canada has indicated it will work closely with financial institutions to coordinate this penny redemption program.

Country Blocking and Travel Notification Services

The Cooperative Network Services Committee (CNSC) has been closely monitoring this trend and in an attempt to help credit unions better manage this type of fraud has approved the development of the Country Blocking and Travel Notification services. The purpose of these services is to provide an additional layer of security to prevent debit card fraud and reduce losses typically arising from a number of unsecure foreign countries that have not implemented CHIP technology. The services will be piloted by five credit unions targeted for Q4 2013 and rolled out to the rest of the Cooperative Node participating credit unions in early 2014.

2014 will continue to have technology enhancements as the Credit Union remains committed to technology solutions that will support product needs, service efficiencies and service reach for our members. We look forward to serving our current and future members.

8

Small Town Smack DownBull Riding in Caroline

St. Matthew Catholic School Breakfast Program

Message from the VP, Financial ServicesAngie French

I am pleased to report that 2013 was a successful year for Rocky Credit Union, and our members, assisted by the local healthy economic activity. Our consumer and

mortgage portfolios overall increased by close to 9% ($13,850,000+/-) in spite of Canada posting its lowest year over year increase in mortgage credit in 12 years. Strong activity in the oil and gas industry translated into positive results for our community as well as that of our commercial members, which translates into increasing disposable income for their employees and robust consumer spending. In addition, our local hospitality industry maintained an average occupancy of over 90% throughout the year with some expansions planned for 2014 as a result of the continuous demand for accommodations.

Rocky Credit Union assisted with construction financing during the year for a new apartment complex known as “Edgewater Terrace” (refer to picture on page 16) which was the first development of its kind in over 25 years in our community. We also participated in commercial loan syndication opportunities with Alberta Central and other Credit Unions which resulted in 29% growth in this category (year over year) of quality loans.

In October 2013 Canadian Real Estate Wealth published an article that read “Rocky Mountain House is listed in the

coveted Top 100 Neighbourhoods to invest”. With so much domestic and international demand for property, investors are being advised to think locally, not provincially. This is particularly true in towns with a smaller and less diverse economy, employment base, and rental market. In order to determine the Top 100, such exclusive data as media price, cash flow projections, local economic barometers, cap rate and vacancy rate are included in neighbourhood evaluations.

Our wealth management offering continues to be successful for our members and Rocky Credit Union, as well as our partner Eckville Credit Union and their members. Elaine Kautz, our Wealth Consultant is a Certified Financial Planner who is licensed to provide insurance, investment & financial planning solutions tailored to Rocky and Eckville Credit Union’s members. In spite of ongoing market volatility we are pleased with the results since inception and encourage our members to book an appointment with Elaine for a free consultation (or second opinion). Our new Wealth Management Office is now located in a much more visible and accessible location on the main floor of our building.

I look forward to Rocky Credit Union’s new and improved environment for our members and staff and continued success in 2014. Our success is truly the result of our members as well as our knowledgeable and professional team of staff, so, I thank everyone for their contribution in this regard.

9

Rocky Credit Union Red Dogs Baseball Team

Rocky Rebels Boys & Girls Rugby Teams

Message from the VP, Financial ServicesAngie French

Message from the VP, Credit & RiskKen Peterson

Alberta continued to be a great place to do business in 2013, and the performance results in relation to managing the Rocky Credit Union loan

portfolio are reflective of this. Credit quality metrics (loan delinquency and net impaired loans) continue to be at satisfactory levels, and were at five year bests. A strong provincial economy and the communities in which Rocky Credit Union operate supported the sound credit quality witnessed in 2013.

As a result of the strong economic environment and RCU continued efforts in managing our loan portfolio risk, loan delinquency continued to be maintained at satisfactory levels. At the end of 2013, loan delinquency greater than 60 days as a percentage of total loans was 0.45%, far below our credit union target of 0.73%, which is based on the average Alberta credit union system delinquency ratio. Anticipated loan losses are well within the allowances that have been established by the credit union.

Rocky Credit Union’s granting of credit includes analysis, pricing, terms and quality documentation of lending. Effective credit risk management begins with our experienced and skilled professional lending account managers and personal lenders. Lenders have

demonstrated experience, education and clearly documented decision-making authority, and operate within approval processes that include a Management Credit Committee. Consistent lending documentation is used by all Rocky Credit Union lending staff.

The Credit Union employs and is committed to a number of important principles to manage credit risk exposure as follows:• Credit risk assessment includes policies related to credit risk analysis, risk rating and risk scoring;• Credit risk mitigation includes credit structuring, collateral and guarantees;• Credit risk approval limits includes credit risk limits and exceptions;• Credit risk documentation focuses on documentation and administration; and• Credit review and credit deterioration detection includes monitoring and review.

Tolerances and lending practices are approved by the Board. Executive Management is responsible to ensure operating policy and procedure are maintained and adhered to. Review and revision of lending policy and procedures is done on an ongoing basis with regular reviews and updates. The Audit Committee and the Board committee meet on a regular basis and review loan performance indicators.

The internal audit department carries out credit reviews as part of its regular, ongoing audit plan. Members

10

Rocky Knights Soccer Teams

Parade of Lights

can be assured that our present portfolio is sufficiently monitored for acceptable credit quality.

2014 will continue to present a challenge for good quality, profitable lending opportunities as increased competition will continue to make quality credit opportunities scarce. The current lending environment has become even more competitive, and many financial institutions have liberalized their credit policies and while we will have to be competitive with our credit policies, we will also ensure sound practices for the safety

of our member assets. As such, opportunities for solid loan growth will remain constrained for our Credit Union in 2014. Even with the increased liberalized competition for loans, our management and staff are prepared to provide alternative sound quality advice regarding member loan requests.

As a member of the Rocky Credit Union you can be assured that our loan portfolio is healthy, strong and profitable and RCU loan policies will continue to attract our projected growth target for the coming year.

Message from the VP, Finance Randall Sugden

2013 Financial Performance Review

The financial position review provides an analysis of our major statement of financial

position categories, and a review of our balance sheet, liquidity, capital and profitability positions. The review is based on the Audited Financial Statements, as at October 31st, 2013.

Balance Sheet

On-balance sheet assets at the end of 2013 were close to $335.0 million compared to $308.1 million in 2012, an increase of $26.9 million, which equates to growth of 8.8%. The primary driver for RCU’s growth was

deposits, as all of our assets are funded by member deposits. Cash equivalents and investments grew $11.4 million or 12.4%. Similar to many financial institutions, Rocky Credit Union experienced a surge in deposits as members wait for stock markets and interest rate trends to normalize. Deposits that are not lent out locally are strategically invested within the credit union system. Member deposits closed 2013 at $298.7 million, up $22.3 million or 8.1% over 2012.

Total loans increased to $227.4 million from $213.4 million in 2012, or a 6.6% increase. Rocky Credit Union’s loan book continues to be comprised largely of stable, low risk, residential mortgage loans (47% of the total loan portfolio). The total portfolio is further broken down to 24% consumer term loans and

11

Rocky High School Rodeo Association

Rocky Band Parents Association

overdrafts while commercial and agriculture portfolios make up the rest, at 29%. Rocky Credit Union promotes a healthy balance sheet addressing problem loans as they arise.

Liquidity

Liquidity is defined as the ability to generate or obtain sufficient cash/equivalents to meet commitments as they come due. A critical area of focus, Rocky Credit Union continues to manage liquidity not only using traditional financial ratios but also looks forward, anticipating demands and other outside factors that could potentially stress our liquidity levels.

Targeted deposit levels and increased allocation to liquid investments (as a percentage of assets) led to an overall efficient liquidity position. The demand for loans has continued to be funded by deposits from Rocky Credit Union members. These deposits (including interest) are 100% guaranteed by the regulator of credit unions in Alberta, Credit Union Deposit Guarantee Corporation (CUDGC).

Under the Credit Union Act of Alberta the Credit Union must maintain a minimum liquidity ratio of 6% of total assets. The Credit Union’s liquidity ratio was 8.32% at October 31, 2013 (2012 – 8.15%).

As an added measure of safety, Alberta credit unions are required to maintain 9% of their liabilities on deposit with Credit Union Central of Alberta (CUCA) who manages the Provincial Liquidity Program. Throughout 2013, Rocky Credit Union held the required amount

of investments with CUCA for the purpose of maintaining its obligation. Among other reasons, these liquidity investments provide a safety net of liquid resources to satisfy payment obligations and protect against unforeseen liquidity events. In addition to the statutory liquidity investments on deposit with CUCA, Rocky Credit Union maintains a reserve of liquid assets, as well as access to borrowings to meet daily and medium-term liquidity requirements.

Profitability

Income before tax for the year was $4.2 million, up from $2.2 million in the prior year. For 2013 our total annualized return on assets (ROA) before dividend allocation and income tax was 1.25% compared to 0.72% in 2012.

Net Interest Margin – is total interest revenue less total interest expenses while factoring in any provisions for credit and investment losses. For 2013, net interest margin was $7.4 million compared to $5.9 million in 2012. Included is $632 thousand in patronage distributions from Credit Union Central in 2013.

Non-Interest Revenue – includes fixed asset revenue, commissions and charges. Non-interest revenue was down marginally to $1.5 million in 2013 versus $1.6 million in 2012.

During the year RCU received insurance proceeds of $785 thousand relating to previously written off loan losses.

Non-Interest Expense – includes various operating costs such as

12

personnel, occupancy, security, governance, community development and general business. Non-interest expense increased marginally to $5.5 million (1.6% of average assets) from $5.3 million in 2012 (1.8% of average assets).

Capital

Total eligible capital as a percentage of risk weighted assets and total eligible capital as a percentage of total assets (capital adequacy) are primary measures of Rocky Credit Union’s financial strength. Our capital management framework is designed to maintain an optimal level of capital. Accordingly, our capital policies are designed to ensure that: we meet our regulatory capital requirements; we meet our internal assessment of required capital; and we build long-term membership value. Rocky Credit Union retains a portion of its annual earnings in order to meet these capital objectives. Once these capital objectives are met, additional earnings are allocated to members through our profit sharing program. The program allocates earnings to members’ equity accounts based on dividends and/or the usage of services, approved annually by the Board.

Capital adequacy for Alberta credit unions is set and measured in accordance to guidelines issued by CUDGC. The guideline requires that at a minimum the credit union maintain capital that is the greater of 8% of

Risk Weighted Assets (RWA) or 4% of total assets. For the year-ending 2013, our total capital (including dividend payable) expressed as a percentage of risk weighted assets was 19.8% (2012 – 18.5%). As well, total eligible capital expressed as a percentage of total assets was 10.3% (2012 - 10.0%).

For RCU, the application of Basel III, international capital adequacy standards, means an additional regulatory requirement of capital will be required, equal to 2.5% of RWA by the end of 2015. Presently, Rocky Credit Union has met and surpassed these more rigorous capital standards.

Total Members’ Equity of Rocky Credit Union consists of:

Amounts held in member common 1. share accounts (registered and non-registered): $14.2 million ($13.4 million in 2012),Retained Earnings: $19.9 million 2. ($17.1 million in 2012),Allocation distributable (dividends 3. paid in November, 2013)

Profit Sharing

In 2013, Rocky Credit Union allocated approximately $477,000 of earnings to members through the profit share program (Dividends of $435,000 in 2012). Members, in accordance with the profit sharing program, received all of the 2013 allocation as a dividend distribution to members’ equity accounts.

Rocky Stars Girls Fastball Team

The Lord’s Food Bank

Our Vision: Helping Members Succeed. Building Our Community.

13

Building Expansion and RenovationThe building expansion was announced In October, 2012. The official building work started in May of 2013.

Rocky Credit Union would like to thank all our members and staff who have been very patient and flexible throughout the expansion. When the building is completed it will serve our members very well for many years to come, and demonstrate Rocky Credit Union’s commitment to being a strong presence in our community.

The expansion started with the removal of the metal cladding and brick around the building. (Pictured right and far right)

While the work went on outside, the basement was also being prepared with new support concrete and beams put in place. (Pictured far left and left) The elevator shaft was dug out and poured at the same time. (Pictured right)

We closed for one day while the support beam was installed in the ceiling of the MSR desks. Then the second storey really got going. (Pictured right and far right)

As the second storey was built, the staff room was also redone. (Pictured left)

To be continued in 2014...

14

Executive Management and AdministrationBack Row: Randall Sugden, Doug Glessing, Ken Peterson, Jerry PrattFront Row: Joann Thompson, Angie French, Tammy Young, Kim Kadyk, Kyla Logan

2013 Board of DirectorsThe Board of Directors’ role is to oversee the Credit Union and provide direction on long-range objectives, set policy, and monitor Rocky Credit Union’s progress. They work with management to establish and evaluate strategic objectives.

Directors are elected for a three-year term. Duties include establishing corporate objectives, approving corporate strategies and plans, approving financial statements and major financial decisions, and evaluating how well the credit union is achieving the Board’s objectives. Carson Stewart

PresidentDonna Beagle

1st Vice President

Dan ArychukDirector

Elizabeth Kariatsumari Director

Alan Marshall2nd Vice President

Robert BrooksDirector

Tom ClarkDirector

15

Member ServicesBack Row: Pam Burrington, Carolyn Jameson, Michelle Cech, Colleen Peterson, Chris Leclerc, Mark Vos, Nicole Schenk, Tanya OpdenDries, Jill Munday, Jodi Meston, Kandis JacksonFront Row: Darlene Morrow, Nancy Laperriere, Jeanie Nile, Lindsey Haupt, Amanda Corace, Avery Erickson Missing: Patrica Mellot, Megan Teskey, Hennie Webster

Commercial and Consumer Lenders and Lending AdministrationBack Row: Dan Burger, Barbara Schooler, Rachelle Evans, Melinda Leslie, Kendra Wandler, Brande Harder, Penny Forster, Stacey SpeightFront Row: Donna Zenert, Robin Montgomery, Vera McLeod, Judi Tetley, Stephanie McLean, Gloria CollicuttMissing: Lyn Robertson,

16

Rocky Credit Union teamed up with Credential Financial Services in 2010 in response to members’ requests for full financial services. RCU Wealth Management offers financial planning, investment and insurance services to our members and to the general public, for both individuals and businesses.

RCU Wealth Management has access, through its mutual funds dealer, Credential Asset Management Inc. to an extensive list of mutual funds. RCU Wealth Management also has access to segregated funds and life insurance alternatives. We have no affiliation to any single insurance or investment company, as our loyalties are to our members.

Our goal is to provide solid financial services in a comfortable and trustworthy

environment. Whether staff is helping set up an education fund or working on a retirement plan with members, we strive to meet their needs, answer questions and ensure their future is a little brighter.

The RCU Wealth Management’s mutual fund portfolio enjoyed net growth over the past year of 26%. We strive to offer the best solutions in each individual case and truly care about our members’ present and future financial planning needs including investments and insurance. We offer investment products such as RRSP, RRIF, LIRA, TFSA, non registered with tax efficient solutions. The insurance offerings include life, disability, long term care, critical illness and guaranteed investment options. Your success is our success!

RCU Wealth Management

Nancy Laperriere, Mutual Funds Investment SpecialistElaine Kautz, CFP, Manager, Wealth ManagementChris Leclerc, Mutual Funds Investment Specialist

17

Commercial Financing Projects

One of the major projects that Rocky Credit Union financed this past year was the Edgewater Terrace apartments on the western side of Rocky Mountain House.

The apartment complex has 18 rental units and should be finished in the spring of 2014.

18

1st David Thompson Scouts4H Show & SaleAg Society of CarolineAg Society of Rocky Mountain HouseAg TourAlberta Co-operative CampAlfred Von Hollen Christmas Light

DisplayATB FundraiserBrian Mazza Memorial RunCanada Day ActivitiesCaroline Dance WestCaroline ParadeCattleman’s DayCentre for Outdoor EducationChamber of CommerceChamber of Commerce - CarolineChamber of Commerce - RMHClearwater Boys & Girls ClubCommunity Safety DayCOPECows & Creeks Ag EventDavid Thompson Boys & Girls

Basketball teamsDinner and DiamondsFarmerettes’ BonspielFarmers’ BonspielFat Tire FestivalFish & Game AssociationFriends of Lochearn ElementaryGo Girls ConferenceHusky Spring SwingKids CarnivalKinsmen Fundraiser for Rocky

Elementary SchoolLegionLegion Dart ClubLeslieville Elementary SchoolLeslieville Elks ClubLochearn Elementary School Marketplace on MainMiniatures in Motion

Mountain Rose Women’s ShelterNordegg Golf CourseNorthern CrossingOilmen’s BonspielParade of LightsPioneer School Band - Rocky Band

Parents AssociationPrimary Care NetworkRCU Red Dogs Baseball TeamRelay for LifeRocky Air ShowRocky Barracudas Swim ClubRocky Christian SchoolRocky Chuckwagon RacesRocky Community Learning CouncilRocky Curling ClubRocky “Dreams” Dance SchoolRocky Elementary SchoolRocky Figure SkatingRocky Girl GuidesRocky High School Rodeo

AssociationRocky Jr. Rebels FootballRocky Knights SoccerRocky Lions ClubRocky Minor HockeyRocky Mountain House

Centennial CelebrationRocky Mountain House

MuseumRocky ParadeRocky Pro RodeoRocky RABCRocky Rams Junior Forest

WardensRocky Rotary ClubRocky Skating ArenasRocky Stars Girls FastballRocky/Kamikawa Friendship SocietySanta’s Worskshop - Rocky Co-op,

Rotary Club & Rocky Credit UnionSeniors Golf tournmanet

Shred It Day by Rocky Credit UnionSmall Town Smack DownSpeed Skating ClubSpruce Valley VaultersSt. Dominic Catholic High SchoolSt. Dominic Catholic High School

ScholarhsipsSt. Matthew Catholic School

Breakfast ProgramSTARSThe Lord’s Food BankVictim ServicesWest Central Boys & Girls Rugby

TeamsWest Central High SchoolWest Central High School

ScholarshipsWest Country Family Services

Investing In Our CommunityRocky Credit Union invests in our members and our community by providing support to a wide variety of community organizations and events. Our goal with this support is to help keep our community a vibrant place to live and work. We helped the following groups and events this past year:

We are also the proud sponsor of the Positive Ticketing Program that allows RCMP and Peace Officers to reward youth for doing good things like picking up garbage in a neighbourhood or wearing their bike helmets.

Rocky CommunityLearning Council

19

Rural Alberta Business Centre

Rocky Ag. Society Rocky Jr. Rebels Football Teams

Rocky CommunityLearning Council

Rocky Rams Jr. Forest Wardens Rocky “Dreams” Dance School

Nordegg Golf Course

Oilmen’s BonspielCaroline Dance West Rocky Pro Rodeo Brian Mazza Memorial Run

Community Safety Day

Marketplace on Mainstreet

Lochearn Elementary Fundraiser

Mountain Rose Women’s Shelter

Northern Crossing Barracudas Swim Club RCU float in theRodeo Week Parade

Farmerettes’ Bonspiel Husky Spring Swing FatCat out in the community Our cake celebrating Rocky’s Centennial

20

ROCKY CREDIT UNION LTD.

ROCKY MOUNTAIN HOUSE, ALBERTA

FINANCIAL STATEMENTS

FOR THE YEAR ENDED OCTOBER 31, 2013

Hawkings Epp Dumont LLP Chartered Accountants

21

REPORT OF THE INDEPENDENT AUDITOR ON THE SUMMARY FINANCIAL STATEMENTS

To the Members of Rocky Credit Union Ltd.

The accompanying summary financial statements, which comprise the statement of financial position as at October 31, 2013 and the statement of net income and comprehensive income, statement of changes in members’ equity, and the statement of cash flows for the year then ended are derived from the audited financial statements of the Rocky Credit Union Ltd. for the year ended October 31, 2013. We expressed an unmodified audit opinion on those financial statements in our report dated January 17, 2014. Those financial statements, and the summary financial statements, do not reflect the effects of events that occurred subsequent to the date of our report on those financial statements.

The summary financial statements do not contain all the disclosures required by International Financial Reporting Standards. Reading the summary financial statements, therefore, is not a substitute for reading the audited financial statements of the Rocky Credit Union Ltd.

Management’s Responsibility for the Financial Statements Management is responsible for the preparation of a summary of the audited financial statements in accordance with International Financial Reporting Standards.

Auditors’ ResponsibilityOur responsibility is to express an opinion on the summary financial statements based on our procedures, which were conducted in accordance with Canadian Auditing Standard 810 Engagements to Report on Summary Financial Statements.

OpinionIn our opinion, the financial statements present fairly, in all material respects, the financial position of Rocky Credit Union Ltd. as at October 31, 2013 and its financial performance and cash flows for the year ended October 31, 2013 in accordance with International Financial Reporting Standards.

Edmonton, Alberta HAWKINGS EPP DUMONT LLPJanuary 17, 2014 Chartered Accountants

22

MANAGEMENT’S RESPONSIBILITY FOR FINANCIAL REPORTING

These financial statements were prepared by the management of Rocky Credit Union Ltd. (the “Credit Union”) who are responsible for their accuracy, completeness and integrity. They were developed in accordance with the requirements of the Credit Union Act of Alberta and conform in all material respects with International Financial Reporting Standards.

Systems of internal control and reporting procedures are designed to provide reasonable assurance that the financial records are complete and accurate so as to safeguard the assets of the Credit Union. These systems include establishment and communication of standards of business conduct throughout all levels of the organization to provide assurance that all transactions are authorized and proper records are maintained. Internal control provides management with the ability to assess the adequacy of these controls. Further, they are reviewed by the Credit Union’s external auditors.

The Board of Directors has approved the financial statements. The Board, comprising seven directors who are not officers or employees of the Credit Union, has reviewed the statements with the external auditors in detail and received regular reports on internal control findings. Hawkings Epp Dumont LLP, the external auditors appointed by the membership, have examined the financial statements of the Credit Union in accordance with Canadian auditing standards. They have had full and free access to the internal audit staff, other management staff, and the Audit and Finance Committee of the Board. Their report appears herein.

Rocky Mountain House, AlbertaJanuary 17, 2014

Doug Glessing Randall SugdenDoug Glessing Randall SugdenChief Executive Officer VP Finance

The following Financial Report is extracted from the Financial Statements of the Rocky Credit Union Ltd. for the year ended October 31st, 2013 which were audited by Hawkings Epp Dumont LLP Chartered Accountants who expressed an unmodified opinion on those statements on January 17th, 2014.

The Report of the Independent Auditor on the Summary Financial Statements does not cover the other information presented in the Annual Report and the auditors have no specific responsibility for determining whether or not the other information is properly stated.

A complete set of Rocky Credit Union Ltd. financial statements and notes can be obtained from the branch or online at www.rockycreditunion.com.

23

ROCKY CREDIT UNION LTD.STATEMENT OF FINANCIAL POSITION

AS AT OCTOBER 31, 2013

2013 2012ASSETS

Cash and cash equivalents $85,636,830 $61,242,887 Investments 17,805,564 30,776,992 Derivative assets 153,703 171,399 Member loans 227,366,253 213,360,307 Property and equipment 3,327,804 1,148,226 Intangible assets 355,724 409,609 Taxes receivable - 37,015 Assets held for sale 149,525 810,953 Other assets 182,550 127,092

$334,977,953 $308,084,480

LIABILITIES

Member deposits $298,693,966 $276,400,020 Derivative liabilities 222,408 283,822 Accounts payable and accrued liabilities operating 551,902 506,370 Accounts payable and accrued liabilities capital 425,649 - Taxes payable 486,614 - Deferred income tax liability 27,520 19,929

300,408,059 277,210,141

MEMBERS’ EQUITY

Dividends distributable 477,439 435,318 Member shares 14,165,185 13,363,132 Retained earnings 19,927,270 17,075,889

34,569,894 30,874,339

$334,977,953 $308,084,480

ON BEHALF OF THE BOARD:

Carson Stewart Donna BeaglePresident, Board of Directors Vice President, Board of Directors

24

ROCKY CREDIT UNION LTD.STATEMENT OF NET INCOME AND COMPREHENSIVE INCOME

FOR THE YEAR ENDED OCTOBER 31, 2013

2013 2012INTEREST INCOMEInterest from member loans $9,041,658 $9,028,454 Investment income 1,802,560 947,321

10,844,218 9,975,775

INTEREST EXPENSEInterest on member deposits 3,245,610 3,819,355 Interest rate swap expense 5,403 17,507 Interest on financing 1,113 1,115

3,252,126 3,837,977

NET INTEREST INCOME BEFORE PROVISION FOR LOAN IMPAIRMENT 7,592,092 6,137,798

PROVISION FOR LOAN IMPAIRMENT 189,474 218,470

NET INTEREST INCOME AFTER PROVISION FOR LOAN IMPAIRMENT 7,402,618 5,919,328

OTHER INCOME 1,474,938 1,615,976

RECOVERIES FOR INSURANCE SETTLEMENT 784,618 -

NET INTEREST AND OTHER INCOME 9,662,174 7,535,304

OPERATING EXPENSES 5,462,611 5,333,783

INCOME BEFORE INCOME TAXES 4,199,563 2,201,521

INCOME TAXES Current 982,512 374,172 Deferred 7,591 942

990,103 375,114

NET INCOME AND COMPREHENSIVE INCOME $3,209,460 $1,826,407

25

ROCKY CREDIT UNION LTD.STATEMENT OF CHANGES IN MEMBERS’ EQUITY

FOR THE YEAR ENDED OCTOBER 31, 2013

Dividends Member Retained Distributable Shares Earnings Total

Balance, October 31, 2011 $415,283 $13,205,196 $15,593,089 $29,213,568

Net income - - 1,826,407 1,826,407 Dividends paid (415,283) 420,118 - 4,835 Dividends declared 435,318 - (435,318) - Tax recovery on dividends paid - - 91,711 91,711 Issuance of member shares - 799,421 - 799,421 Redemption of member shares - (1,061,603) - (1,061,603)

Balance, October 31, 2012 $435,318 $13,363,132 $17,075,889 $30,874,339

Net income - - 3,209,460 3,209,460 Dividends paid (435,318) 433,260 - (2,058) Dividends declared 477,439 - (477,439) - Tax recovery on dividends paid - - 119,360 119,360 Issuance of member shares - 1,302,029 - 1,302,029 Redemption of member shares - (933,236) - (933,236)

Balance, October 31, 2013 $477,439 $14,165,185 $19,927,270 $34,569,894

26

ROCKY CREDIT UNION LTD.STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED OCTOBER 31, 2013

2013 2012OPERATING ACTIVITIESNet income $3,209,460 $1,826,407 Adjustments for:Depreciation of property and equipment 142,627 86,364 Amortization of intangible assets 76,885 63,048 Deferred income taxes 7,591 942 (Gain)/Loss on disposal of property and equipment (43,893) 4,210 Provision for loan impairment 189,474 218,470 Net interest income (7,592,092) (6,137,798) Interest received 10,857,789 10,097,022 Interest paid (3,177,057) (3,926,923) Income taxes paid (458,883) (341,935) Current income tax expense 982,512 374,172

4,194,413 2,263,979 Changes in non cash working capital:Other assets (55,456) (56,226) Net change in member deposits 22,218,877 26,126,639 Net change in member loans (14,170,538) (7,479,274) Accounts payable and accrued liabilities - operating 45,532 (66,637) Derivative liabilities (43,719) (32,097)

12,189,109 20,756,384

FINANCING ACTIVITIESIssuance of member shares, net 802,052 157,936 Dividends paid (435,318) (415,283) Income tax savings on dividends 119,360 91,711 Net decrease in assets held for sale 661,428 199,258

1,147,522 33,622

INVESTING ACTIVITIESPurchase of property and equipment (2,325,692) (94,372) Proceeds on disposal of property and equipment 47,380 - Purchase of intangible assets (23,000) (32,932) Net change in investments 12,932,975 (14,110,603) Accounts payable and accrued liabilities - capital 425,649 -

11,057,312 (14,237,907)

NET CHANGE IN CASH AND CASH EQUIVALENTS 24,393,943 6,552,099

CASH AND CASH EQUIVALENTS, BEGINNING OF YEAR 61,242,887 54,690,788

CASH AND CASH EQUIVALENTS, END OF YEAR $85,636,830 $61,242,887

27

Notes

28

Other Community InvolvementTop: Halloween DayCentre left: RCU Shred It DayCentre Right: Chuckwagon BBQ with Rocky Co-opBottom: Marketplace on Main

PO Box 1420, Stn Main 5035 49th StRocky Mountain House, AB T4T 1B1Ph. 403.845.2861Fax 403.845.7295

CAD$ Chequing & Saving AccountsUSD Chequing AccountDebit CardsOnline, Mobile (Smart phone) & Text BankingATM usage at CU’s across CanadaAutomatic Transfers, Bill Payments, & DepositsAuthorized Overdraft ProtectionCredit Cards

Personal Banking

Savings Accounts & High Interest Savings AccountsTax Free Savings Accounts (TFSA)Registered Retirement Savings Plans (RRSP)Registered Retirement Income Funds (RRIF)Registered Education Savings Plans (RESP)Term Deposits & Guaranteed Income CertificatesAdditional Variety of Investment OptionsFinancial Planning & Retirement Planning

Investing & RCU Wealth Management

FinancingMortgagesVehicle LoansPersonal LoansPersonal Lines of CreditEducation LoansRRSP LoansLoan Insurance (Life & Disability)Secure Online Loan Application

Agriculture & Business BankingCAD$ Chequing & Saving AccountsUSD Chequing AccountInternet & Telephone BankingAutomatic Transfers & Bill Payments Automatic DepositsAuthorized Overdraft Protection

Agriculture & Business FinancingMortgagesVehicle LoansTerm LoansLines of CreditLoan Insurance

Additional ServicesCoin Counter MachinePersonal ChequesTravelers ChequesSafety Deposit BoxesFund TransfersForeign Exchange ServiceseTransfers

Helping Members Succeed and Building Our Communities Since 1944