town of ramapo rockland county, new york · in the opinion of pannone lopes devereaux & west...

TRANSCRIPT

OHSUSA:753803561.6

NEW ISSUE NOT RATED BOOK-ENTRY-ONLY

In the opinion of Pannone Lopes Devereaux & West LLC, Bond Counsel, based upon an analysis of existing laws, regulations, rulings and court decisions, and assuming among other matters, the accuracy of certain representations and compliance with certain covenants, interest on the Notes is excluded from gross income for federal income tax purposes under Section 103 of the Internal Revenue Code of 1986. In the further opinion of Bond Counsel, interest on the Notes is not a specific preference item for purposes of the federal individual or corporate alternative minimum taxes, although it is included in adjusted current earnings when calculating corporate alternative minimum taxable income. Bond Counsel is also of the opinion that interest on the Notes is exempt from personal income taxes imposed by the State of New York or any political subdivision thereof (including The City of New York). Bond Counsel expresses no opinion regarding any other tax consequences related to the ownership or disposition of, or the accrual or receipt of interest on, the Notes. See “TAX MATTERS” herein.

The Notes will not be designated by the Town as “qualified tax-exempt obligations” pursuant to Section 265(b)(3) of the Code.

TOWN OF RAMAPO ROCKLAND COUNTY, NEW YORK

GENERAL OBLIGATION NOTES

$31,200,000 BOND ANTICIPATION NOTES - 2013 SERIES A

DATED: Date of Delivery INTEREST RATE: 4.70% YIELD: 3.50% DUE: May 28, 2014 CUSIP*: 751396 2N1

The $31,200,000 Bond Anticipation Notes – 2013 Series A (the “Notes”) are general obligations of the Town of Ramapo, Rockland County, New York (the “Town”) within which all taxable real property is subject to the levy of ad valorem taxes to pay the Notes and interest thereon, subject to applicable statutory limitations.

The Notes will be issued in registered form and, when issued, will be registered in the name of Cede & Co., as nominee of The Depository Trust Company (“DTC”), New York, New York, which will act as securities depository. Individual purchases will be made in book-entry form only, in the principal amount of $100,000 or any integral multiple of $5,000 in excess thereof. Purchasers will not receive certificates representing their ownership interest in the Notes. Principal and interest will be paid by the Town to DTC, which will in turn remit such principal and interest to its Participants, for subsequent distribution to the Beneficial Owners of the Notes, as described herein.

This cover page contains certain information for quick reference only. It is not a summary of this issue. Investors must read this entire Placement Memorandum to obtain information essential to making an informed decision.

The purchase and ownership of the Notes involve certain investment risks. See “MARKET AND RISK FACTORS” and “FEDERAL INVESTIGATION” herein.

The Notes are being offered only to purchasers who are “qualified institutional buyers” within the meaning of Rule 144A under the Securities Act of 1933.

The Notes are offered for delivery when, as and if issued and received by the Placement Agent, subject to the receipt of the approving legal opinion of Pannone Lopes Devereaux & West LLC, Bond Counsel, White Plains, New York. Certain other legal matters will be passed upon on behalf of the Town by Michael L. Klein, Esq., Town Attorney. Environmental Capital LLC, New York, New York is serving as Financial Advisor to the Town with respect to the Notes. Certain legal matters in connection with the preparation of this Placement Memorandum will be passed upon for the Town by Orrick, Herrington & Sutcliffe LLP, New York, Special Disclosure Counsel to the Town. Certain legal matters with respect to the Notes will be passed upon for the Placement Agent by its counsel, Bracewell & Giuliani LLP, New York, New York. It is anticipated that the Notes will be available for delivery through the facilities of DTC in New York, New York on or about May 28, 2013.

Jefferies (Placement Agent)

Dated: May 24, 2013

* Copyright 1999-2013, Standard & Poor’s, a Division of The McGraw-Hill Companies, Inc. CUSIP is a registered trademark of the American Bankers Association. CUSIP data herein are provided by Standard & Poor’s CUSIP Service Bureau, a division of The McGraw-Hill Companies, Inc. The CUSIP number has been assigned by an independent company not affiliated with the Town and is included solely for the convenience of the owners of the Notes. The Town is not responsible for the selection or uses of the CUSIP number, and no representation is made as to its correctness on the Notes or as indicated above. The CUSIP number is subject to being changed after the issuance of the Notes as a result of various subsequent actions including, but not limited to, a refunding in whole or in part of the Notes or as a result of the procurement of secondary market portfolio insurance or other similar enhancement by investors that is applicable to all or a portion of the Notes.

OHSUSA:753803561.6

TOWN OF RAMAPO, NEW YORK

CHRISTOPHER P. ST. LAWRENCE Supervisor

PATRICK WITHERS Deputy Supervisor

Town Council DANIEL FRIEDMAN BRENDEL LOGAN

YITZCHOK ULLMAN PATRICK WITHERS

MICHAEL L. KLEIN Town Attorney

CHRISTOPHER P. ST. LAWRENCE Director of Finance

Bond Counsel Pannone Lopes Devereaux & West LLC

White Plains, NY

Financial Advisor Environmental Capital LLC

New York, NY

OHSUSA:753803561.6

No dealer, broker, salesman or other person has been authorized by the Town of Ramapo (the “Town”) to give any information or to make any representations, other than those contained in this Placement Memorandum and if given or made, such information or representations must not be relied upon as having been authorized. This Placement Memorandum does not constitute an offer to sell or solicitation of an offer to buy any of the Notes in any jurisdiction to any person to whom it is unlawful to make such offer or solicitation in such jurisdiction. The information, estimates and expressions of opinion herein are subject to change without notice, and neither the delivery of this Placement Memorandum nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the affairs of the Town since the date hereof.

The information set forth herein has been furnished by the Town, The Depository Trust Company (as to itself and the book-entry only system) and other sources which are believed to be reliable, but such information is not guaranteed as to accuracy or completeness by, and is not to be construed as a representation of the Placement Agent.

CERTAIN STATEMENTS CONTAINED IN THIS PLACEMENT MEMORANDUM REFLECT NOT HISTORICAL FACTS BUT FORECASTS AND “FORWARD-LOOKING STATEMENTS.” IN THIS RESPECT, THE WORDS “ESTIMATE,” “PROJECT,” “ANTICIPATE,” “EXPECT,” “INTEND,” “BELIEVE” AND SIMILAR EXPRESSIONS ARE INTENDED TO IDENTIFY FORWARD-LOOKING STATEMENTS. ALL PROJECTIONS, FORECASTS, ASSUMPTIONS, EXPRESSIONS OF OPINIONS, ESTIMATES AND OTHER FORWARD-LOOKING STATEMENTS ARE EXPRESSLY QUALIFIED IN THEIR ENTIRETY BY THE CAUTIONARY STATEMENTS SET FORTH IN THIS PLACEMENT MEMORANDUM.

THE NOTES HAVE NOT BEEN REGISTERED WITH THE SECURITIES AND EXCHANGE COMMISSION UNDER THE SECURITIES ACT OF 1933, AS AMENDED, NOR HAVE THE AUTHORIZING RESOLUTIONS BEEN QUALIFIED UNDER THE TRUST INDENTURE ACT OF 1939, AS AMENDED, IN RELIANCE UPON EXEMPTIONS CONTAINED IN SUCH ACTS. THE REGISTRATION OR QUALIFICATION OF THE NOTES IN ACCORDANCE WITH APPLICABLE PROVISIONS OF THE SECURITIES LAWS OF THE STATES, IF ANY, IN WHICH THE NOTES HAVE BEEN REGISTERED OR QUALIFIED AND THE EXEMPTION FROM REGISTRATION OR QUALIFICATION IN CERTAIN OTHER STATES CANNOT BE REGARDED AS A RECOMMENDATION THEREOF. NEITHER THESE STATES NOR ANY OF THEIR AGENCIES HAVE PASSED UPON THE MERITS OF THE NOTES OR THE ACCURACY OR COMPLETENESS OF THIS PLACEMENT MEMORANDUM. ANY REPRESENTATIONS TO THE CONTRARY MAY BE A CRIMINAL OFFENSE.

References herein to laws, rules, regulations, resolutions, agreements, reports and other documents do not purport to be comprehensive or definitive. All references to such documents are qualified in their entirety by reference to the particular document, the full text of which may contain qualifications of and exceptions to statements made herein. Where full texts have not been included as appendices to this Placement Memorandum they may be obtained from the Town, upon prepayment of reproduction costs, postage and handling expenses.

(The Remainder of this page intentionally left blank.)

OHSUSA:753803561.6

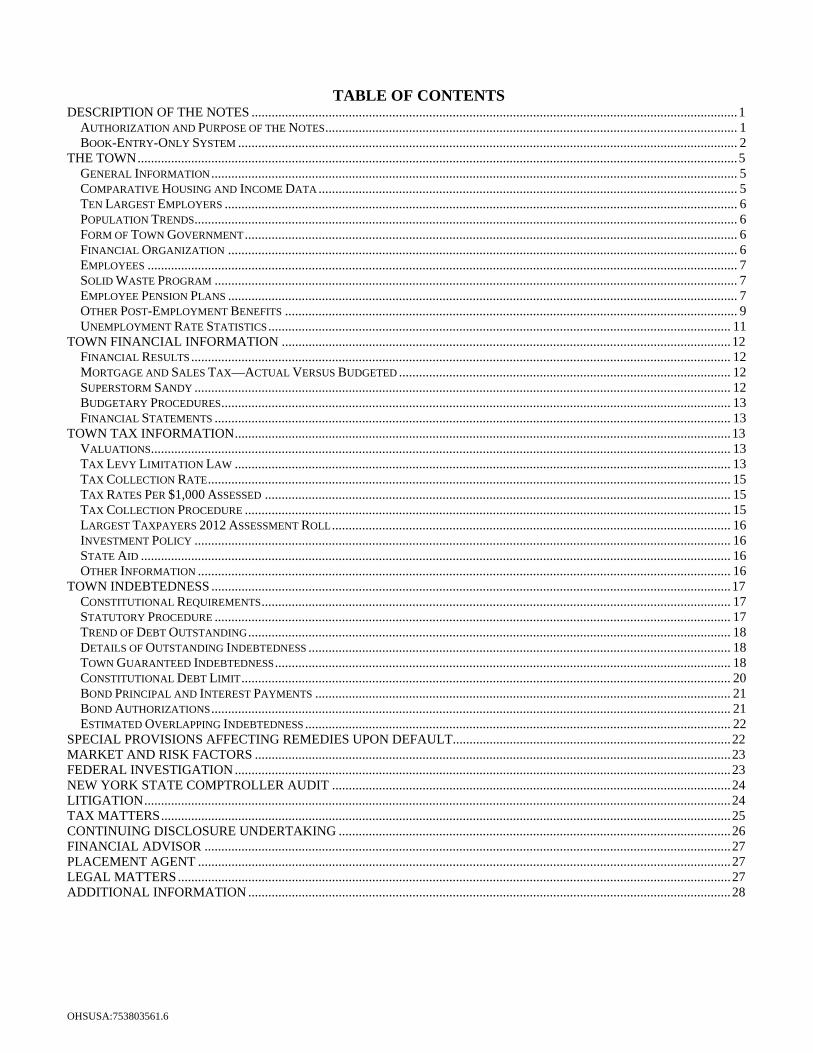

TABLE OF CONTENTS DESCRIPTION OF THE NOTES ................................................................................................................................................. 1

AUTHORIZATION AND PURPOSE OF THE NOTES ........................................................................................................................... 1 BOOK-ENTRY-ONLY SYSTEM ..................................................................................................................................................... 2

THE TOWN ................................................................................................................................................................................... 5 GENERAL INFORMATION ............................................................................................................................................................. 5 COMPARATIVE HOUSING AND INCOME DATA ............................................................................................................................. 5 TEN LARGEST EMPLOYERS ......................................................................................................................................................... 6 POPULATION TRENDS .................................................................................................................................................................. 6 FORM OF TOWN GOVERNMENT ................................................................................................................................................... 6 FINANCIAL ORGANIZATION ........................................................................................................................................................ 6 EMPLOYEES ................................................................................................................................................................................ 7 SOLID WASTE PROGRAM ............................................................................................................................................................ 7 EMPLOYEE PENSION PLANS ........................................................................................................................................................ 7 OTHER POST-EMPLOYMENT BENEFITS ....................................................................................................................................... 9 UNEMPLOYMENT RATE STATISTICS .......................................................................................................................................... 11

TOWN FINANCIAL INFORMATION ...................................................................................................................................... 12 FINANCIAL RESULTS ................................................................................................................................................................. 12 MORTGAGE AND SALES TAX—ACTUAL VERSUS BUDGETED ................................................................................................... 12 SUPERSTORM SANDY ................................................................................................................................................................ 12 BUDGETARY PROCEDURES ........................................................................................................................................................ 13 FINANCIAL STATEMENTS .......................................................................................................................................................... 13

TOWN TAX INFORMATION .................................................................................................................................................... 13 VALUATIONS............................................................................................................................................................................. 13 TAX LEVY LIMITATION LAW .................................................................................................................................................... 13 TAX COLLECTION RATE ............................................................................................................................................................ 15 TAX RATES PER $1,000 ASSESSED ........................................................................................................................................... 15 TAX COLLECTION PROCEDURE ................................................................................................................................................. 15 LARGEST TAXPAYERS 2012 ASSESSMENT ROLL ....................................................................................................................... 16 INVESTMENT POLICY ................................................................................................................................................................ 16 STATE AID ................................................................................................................................................................................ 16 OTHER INFORMATION ............................................................................................................................................................... 16

TOWN INDEBTEDNESS ........................................................................................................................................................... 17 CONSTITUTIONAL REQUIREMENTS ............................................................................................................................................ 17 STATUTORY PROCEDURE .......................................................................................................................................................... 17 TREND OF DEBT OUTSTANDING ................................................................................................................................................ 18 DETAILS OF OUTSTANDING INDEBTEDNESS .............................................................................................................................. 18 TOWN GUARANTEED INDEBTEDNESS ........................................................................................................................................ 18 CONSTITUTIONAL DEBT LIMIT .................................................................................................................................................. 20 BOND PRINCIPAL AND INTEREST PAYMENTS ............................................................................................................................ 21 BOND AUTHORIZATIONS ........................................................................................................................................................... 21 ESTIMATED OVERLAPPING INDEBTEDNESS ............................................................................................................................... 22

SPECIAL PROVISIONS AFFECTING REMEDIES UPON DEFAULT................................................................................... 22 MARKET AND RISK FACTORS .............................................................................................................................................. 23 FEDERAL INVESTIGATION .................................................................................................................................................... 23 NEW YORK STATE COMPTROLLER AUDIT ....................................................................................................................... 24 LITIGATION ............................................................................................................................................................................... 24 TAX MATTERS .......................................................................................................................................................................... 25 CONTINUING DISCLOSURE UNDERTAKING ..................................................................................................................... 26 FINANCIAL ADVISOR ............................................................................................................................................................. 27 PLACEMENT AGENT ............................................................................................................................................................... 27 LEGAL MATTERS ..................................................................................................................................................................... 27 ADDITIONAL INFORMATION ................................................................................................................................................ 28

OHSUSA:753803561.6

REVENUES, EXPENDITURES AND FUND BALANCE - GENERAL FUND ................................................ APPENDIX A-1 BUDGET RESULTS - GENERAL FUND ........................................................................................................... APPENDIX A-2 BALANCE SHEETS - GENERAL FUND ........................................................................................................... APPENDIX A-3 CHANGES IN FUND BALANCES - OTHER FUNDS ...................................................................................... APPENDIX A-4 AUDITED FINANCIAL STATEMENTS FISCAL YEAR ENDING DECEMBER 31, 2011 ................................ APPENDIX B FORM OF BOND COUNSEL OPINION ................................................................................................................ APPENDIX C

1OHSUSA:753803561.6

PLACEMENT MEMORANDUM

of the

TOWN OF RAMAPO, ROCKLAND COUNTY, NEW YORK

Relating to

$31,200,000 Bond Anticipation Notes – 2013 Series A

This Placement Memorandum, which includes the cover page and appendices hereto, presents certain information relating to the Town of Ramapo, in the County of Rockland, in the State of New York (the “Town”, “County”, and “State”, respectively) in connection with the sale of its $31,200,000 Bond Anticipation Notes – 2013 Series A (the “Notes”).

The factors affecting the Town’s financial condition and the Notes are described throughout this Placement Memorandum. Inasmuch as many of these factors, including economic and demographic factors, are complex and may influence the Town tax base, revenues, and expenditures, this Placement Memorandum should be read in its entirety, and no one factor should be considered more or less important than any other by reason of its relative position in this Placement Memorandum. For information relating to a federal investigation involving the Town, see “FEDERAL INVESTIGATION” herein.

DESCRIPTION OF THE NOTES

The Notes are general obligations of the Town, and will contain a pledge of its faith and credit for the payment of the principal thereof and interest thereon as required by the Constitution and laws of the State of New York (State Constitution, Art. VIII, Section 2: Local Finance Law, Section 100.00). All the taxable real property within the Town is subject to the levy of ad valorem taxes to pay the Notes and interest thereon, subject to applicable statutory limitations.

The Notes will be issued in registered form, and, when issued, will be registered in the name of Cede & Co., as nominee of The Depository Trust Company (“DTC”), which will act as securities depository for the Notes. Individual purchases will be made in book-entry form only, in the principal amount of $100,000 or any integral multiple of $5,000 in excess thereof. Purchasers will not receive certificates representing their ownership interest in the Notes. Principal and interest will be paid by the Town to DTC, which will in turn remit such principal and interest to its Participants for subsequent distribution to the Beneficial Owners of the Notes and as described herein. Interest on the Notes will be payable at maturity. The record date for the Notes is the fifteenth day of the calendar month preceding the interest payment date.

The Notes are being offered only to purchasers who are “qualified institutional buyers” within the meaning of Rule 144A under the Securities Act of 1933.

Authorization and Purpose of the Notes

The Notes are issued pursuant to the Constitution and the laws of the State, including among others, the Town Law and the Local Finance Law, and a series bond resolution duly adopted by the Town Board on the date set forth below authorizing the issuance of the bonds for the purpose set forth below. Each of such bond resolutions was adopted subject to permissive referendum. The period of time to submit a petition requesting a referendum thereon expired without a petition being filed. In addition, the Town has satisfied the procedure for the validation of the obligations authorized under each bond resolution (including the Notes) as set forth in Section 81.00 of the Local Finance Law.

2OHSUSA:753803561.6

Date of Bond Resolution Project Amount November 12, 2008 Pay a portion of the costs of construction, reconstruction, widening and

resurfacing roads in the Town $500,000

November 12, 2008 Pay a portion of the costs of the acquisition, construction and reconstruction of bridges in the Town

$500,000

December 22, 2008 Pay a portion of the cost of construction, reconstruction, widening and resurfacing roads in the Town

$1,000,000

August 10, 2009 Pay a portion of the cost of construction, reconstruction, widening and resurfacing roads in the Town

$1,200,000

September 13, 2010, amended April 17, 2012

Various improvements and embellishments of various parks and pools owned by the Town.

$5,200,000

February 9, 2011, amended October 5, 2012

Payment of a portion of the costs of construction, reconstruction, widening and resurfacing roads, streets, and parking lots in the Town

$5,000,000

April 14, 2011, amended October 5, 2012

Payment of a portion of the costs of construction, reconstruction, widening and resurfacing of roads, streets and parking lots, embellishing parks, playgrounds and recreational areas, acquiring or constructing buildings, and construction or reconstruction of curbs, sidewalks and gutters in the Town

$10,000,000

June 6, 2011, amended October 5, 2012

Payment of a portion of the costs of construction, reconstruction, widening and resurfacing of highways, streets and roads and construction or reconstruction of sidewalks, curbs, and gutters

$3,000,000

July 29, 2011, amended October 5, 2012

Payment of a portion of the costs of installation of drainage improvements in the Town

$2,000,000

July 29, 2011, amended October 5, 2012

Pay the cost of original improvement and embellishment of various parks and pools in the Town

$2,000,000

July 29, 2011, amended October 5, 2012

Purchase vehicles for the Town Highway Department $1,200,000

July 29, 2011, amended October 5, 2012

Payment of a portion of the cost of construction, reconstruction, paving of roads, streets and sidewalks at various locations in the Town

$2,000,000

October 5, 2012

Pay the cost of the construction and reconstruction, widening or resurfacing of highway, road and streets in the Pascack Brook area of Town

$1,000,000

October 5, 2012 Pay the cost of various sewer improvement projects in the Town $3,000,000

A portion of the proceeds of the Notes, together with other funds of $1,845,000 provided by the Town, will be used to pay the Town’s $15,000,000 Bond Anticipation Notes – 2012 Series A (Renewal), which mature on May 29, 2013, and $18,045,000 Bond Anticipation Notes – 2012 Series B (Renewal), which mature on July 1, 2013.

Book-Entry-Only System

The information in this Section concerning DTC and DTC’s book-entry only system has been obtained from DTC. Neither the Town nor the Placement Agent makes any representation or warranty regarding the accuracy or completeness thereof or to the absence of material adverse changes in such information subsequent to the date hereof.

3OHSUSA:753803561.6

The Depository Trust Company (“DTC”), New York, New York, will act as securities depository for the Notes. The Notes will be issued as fully-registered securities registered in the name of Cede & Co. (DTC’s partnership nominee) or such other nominee as may be requested by an authorized representative of DTC. One fully-registered note certificate will be issued for each the Notes and will be deposited with DTC.

DTC, is a limited-purpose trust company organized under the New York Banking Law, a “banking organization” within the meaning of the New York Banking Law, a member of the Federal Reserve System, a “clearing corporation” within the meaning of the New York Uniform Commercial Code, and a “clearing agency” registered pursuant to the provisions of Section 17A of the Securities Exchange Act of 1934. DTC holds and provides asset servicing for over 3.5 million issues of U.S. and non-equity issues, corporate and municipal debt issues, and money market instruments from over 100 countries that DTC’s participants (“Direct Participants”) deposit with DTC. DTC also facilitates the post-trade settlement among Direct Participants of sales and other securities transactions in deposited securities, through electronic computerized book-entry transfers and pledges between Direct Participants’ accounts. This eliminates the need for physical movement of securities certificates. Direct Participants include both U.S. and non-U.S. securities brokers and dealers, banks, trust companies, clearing corporations, and certain other organizations. DTC is a wholly-owned subsidiary of The Depository Trust & Clearing Corporation (“DTCC”). DTCC is the holding company for DTC, National Securities Clearing Corporation and Fixed Income Clearing Corporation, all of which are registered clearing agencies. DTCC is owned by the users of its regulated subsidiaries. Access to the DTC system is also available to others such as both U.S. and non-U.S. securities brokers and dealers, banks, trust companies, and clearing corporations that clear through or maintain a custodial relationship with a Direct Participant, either directly or indirectly (“Indirect Participants”). The DTC rules applicable to Participants are on file with the Securities and Exchange Commission. More information about DTC can be found at www.dtcc.com and www.dtc.org.

Purchases of the Notes under the DTC system must be made by or through Direct Participants, which will receive a credit for the Notes on DTC’s records. The ownership interest of each actual purchaser of the Notes (“Beneficial Owner”) is in turn to be recorded on the Direct and Indirect Participants’ records. Beneficial Owners will not receive written confirmation from DTC of their purchase. Beneficial Owners are, however, expected to receive written confirmations providing details of the transaction, as well as periodic statements of their holdings, from the Direct or Indirect Participant through which the Beneficial Owner entered into the transaction. Transfers of ownership interests in the Notes are to be accomplished by entries made on the books of Direct and Indirect Participants acting on behalf of Beneficial Owners. Beneficial Owners will not receive note certificates representing their ownership interests in the Notes, except in the event that the use of the book-entry system for the Notes is discontinued.

To facilitate subsequent transfers, all Notes deposited by Direct Participants with DTC are registered in the name of DTC’s partnership nominee, Cede & Co., or such other name as may be requested by an authorized representative of DTC. The deposit of the Notes with DTC and their registration in the name of Cede & Co. or such other nominee does not affect any change in beneficial ownership. DTC has no knowledge of the actual Beneficial Owners of the Notes; DTC’s records reflect only the identity of the Direct Participants to whose accounts such Notes are credited, which may or may not be the Beneficial Owners. The Direct and Indirect Participants will remain responsible for keeping account of their holdings on behalf of their customers.

Conveyance of notices and other communications by DTC to Direct Participants, by Direct Participants to Indirect Participants, and by Direct Participants and Indirect Participants to Beneficial Owners will be governed by arrangements among them, subject to any statutory or regulatory requirements as may be in effect from time to time. Beneficial Owners of the Notes may wish to take certain steps to augment the transmission to them of notices of significant events with respect to the Notes, such as redemptions, tenders, defaults and proposed amendments to the Note documents. For example, Beneficial Owners of the Notes may wish to ascertain that the nominee holding the Notes for their benefit has agreed to obtain and transmit notices to Beneficial Owners. In the alternative, Beneficial Owners may wish to provide their names and addresses to the registrar and request that copies of notices be provided directly to them.

Redemption notices shall be sent to DTC. If less than all of the Notes within a maturity are being redeemed, DTC’s practice is to determine by lot the amount of the interest of each Direct Participant in such maturity to be redeemed.

Neither DTC nor Cede & Co. (nor any other DTC nominee) will consent or vote with respect to the Notes unless authorized by a Direct Participant in accordance with DTC’s procedures. Under its usual procedures, DTC mails an Omnibus Proxy to the Town as soon as possible after the record date. The Omnibus Proxy assigns Cede & Co.’s consenting or voting rights to those Direct Participants to whose accounts the Notes are credited on the record date (identified in a listing attached to the Omnibus Proxy).

4OHSUSA:753803561.6

Principal and interest payments on the Notes will be made to Cede & Co. or such other nominee as may be requested by an authorized representative of DTC. DTC’s practice is to credit Direct Participants’ accounts upon DTC’s receipt of funds and corresponding detail information from the Town on the payable date in accordance with their respective holdings shown on DTC’s records. Payments by Participants to Beneficial Owners will be governed by standing instructions and customary practices, as is the case with securities held for the accounts of customers in bearer form or registered in “street name,” and will be the responsibility of such Participant and not of DTC or the Town, subject to any statutory or regulatory requirements as may be in effect from time to time. Payment of principal and interest payments to Cede & Co. (or such other nominee as may be requested by an authorized representative of DTC) is the responsibility of the Town, disbursement of such payments to Direct Participants shall be the responsibility of DTC, and disbursement of such payments to the Beneficial Owners shall be the responsibility of Direct and Indirect Participants.

DTC may discontinue providing its services as securities depository with respect to the Notes at any time by giving reasonable notice to the Town. Under such circumstances, in the event that a successor securities depository is not obtained, Note certificates are required to be printed and delivered. The Town may decide to discontinue use of the system of book-entry transfers through DTC (or a successor securities depository). In that event, the Note certificates will be printed and delivered.

The information herein concerning DTC and DTC’s book-entry system has been obtained from sources that the Town believes to be reliable, but the Town takes no responsibility for the accuracy thereof.

Source: The Depository Trust Company

THE TOWN CANNOT AND DOES NOT GIVE ASSURANCES THAT DTC, DIRECT PARTICIPANTS OR INDIRECT PARTICIPANTS OF DTC WILL DISTRIBUTE TO THE BENEFICIAL OWNERS OF THE NOTES (1) PAYMENTS OF PRINCIPAL OF OR INTEREST ON THE NOTES (2) CONFIRMATIONS OF THEIR OWNERSHIP INTERESTS IN THE NOTES OR (3) OTHER NOTICES SENT TO DTC OR CEDE & CO., ITS PARTNERSHIP NOMINEE, AS THE REGISTERED OWNER OF THE NOTES, OR THAT THEY WILL DO SO ON A TIMELY BASIS, OR THAT DTC, DIRECT PARTICIPANTS OR INDIRECT PARTICIPANTS WILL SERVE AND ACT IN THE MANNER DESCRIBED IN THIS PLACEMENT MEMORANDUM.

THE TOWN AND PLACEMENT AGENT WILL NOT HAVE ANY RESPONSIBILITY OR OBLIGATIONS TO DTC, THE DIRECT PARTICIPANTS, THE INDIRECT PARTICIPANTS OF DTC OR THE BENEFICIAL OWNERS WITH RESPECT TO (1) THE ACCURACY OF ANY RECORDS MAINTAINED BY DTC OR ANY DIRECT PARTICIPANTS OR INDIRECT PARTICIPANTS OF DTC; (2) THE PAYMENT BY DTC OR ANY DIRECT PARTICIPANTS OR INDIRECT PARTICIPANTS OF DTC OF ANY AMOUNT DUE TO ANY BENEFICIAL OWNER IN RESPECT OF THE PRINCIPAL AMOUNT OF OR INTEREST ON THE NOTES; (3) THE DELIVERY BY DTC OR ANY DIRECT PARTICIPANTS OR INDIRECT PARTICIPANTS OF DTC OF ANY NOTICE TO ANY BENEFICIAL OWNER THAT IS REQUIRED OR PERMITTED TO BE GIVEN TO OWNERS OR (4) ANY CONSENT GIVEN OR OTHER ACTION TAKEN BY DTC AS THE REGISTERED HOLDER OF NOTES.

So long as Cede & Co. is the registered owner of the Notes, as nominee for DTC, references herein to Noteholders or registered owners of the Notes (other than under the heading “TAX MATTERS” herein) shall mean Cede & Co., as aforesaid, and shall not mean the Beneficial Owners of the Notes.

5OHSUSA:753803561.6

THE TOWN

General Information

The Town is a suburban community located in southeastern New York State (the “State”) about 25 miles northwest of New York City. The Town has a land area of approximately 61 square miles and a current population of 128,014 as of the 2011 U.S. Census Bureau’s American Community Survey. The Town includes ten incorporated villages (Airmont, Chestnut Ridge, Hillburn, Kaser, Montebello, New Hempstead, New Square, Sloatsburg, Suffern, and Wesley Hills) and a major portion of the Villages of Pomona and Spring Valley.

The major industrial enterprises in the Town include Novartis Pharmaceuticals Corporation (formerly CIBA-Geigy Corp.), a leading manufacturer of pharmaceuticals, and Avon Products Inc., a manufacturer of cosmetics. Novartis Pharmaceuticals Corporation is one of the world’s largest pharmaceutical manufacturers. Its Suffern site, a 600,000 square foot facility situated on 150 acres, includes manufacturing facilities, administrative offices and testing laboratories and employs approximately 537 people. Avon Products, Inc., also located in Suffern, is located in a new 225,000 square-foot research and development headquarters and employs approximately 339 people. Additionally, Tri-State Health Systems (formerly Good Samaritan Hospital) employs approximately 1,800 people. Tri-State Health Systems will be augmented by the newly constructed 200,000 square-foot Accredited Cardiac Care Unit. The County of Rockland Health and Hospitals, the Fire Training and Social Services Centers and various other County buildings, employing approximately 2,000 people, are also located within the Town.

The Town-operated recreational facilities include a golf course, equestrian center, five swimming pools, pedestrian and greenway trails, a summer camp facility, numerous tennis court facilities, a state-of-the-art sports complex, a riverfront park and a 2,500-acre park system, including the 200,000 square-foot Joseph T. St. Lawrence Sports and Wellness Center with recreational personnel providing year-round activities for all age groups.

The Town is served by a road network which includes Interstate 87 (the New York State Thruway with four interchanges in the Town). It also includes Interstate 287, the Palisades Interstate Parkway, the Garden State Parkway, and New York State Routes 17, 45, 59, 202 and 306. There is Conrail freight service provided by Norfolk Southern. Metro North and New Jersey Transit provide commuter train service within the Town. The Town is also serviced by several commuter bus lines providing bus transportation to surrounding areas as well as Westchester County and New York City. Orange & Rockland Utilities has merged with Consolidated Edison and operates as a subsidiary of Consolidated Edison. The Town of Ramapo has hundreds of acres included in Empire Zones, which are intended to attract new businesses to the Town.

Comparative Housing and Income Data

Housing: Town County State U.S. Median Value Housing $412,100 $426,800 $285,300 $173,600 Median Gross Rent $1,199 $1,330 $1,058 $871 Income: Per Capita Income $24,047 $33,209 $30,679 $26,708 Median Family Income $70,385 $91,254 $66,852 $61,455

Source: U.S. Census Bureau, 2011 American Community Survey 1-Year Estimate

6OHSUSA:753803561.6

Ten Largest Employers

Name Type Number of Employees

Tri-State Health Systems Hospital 1,800 Hamaspik of Rockland County, Inc. Health and Human Services 1,340 Northern Services Group, Inc. Healthcare 1,100 SUNY/Rockland Community College Community College 1026 Rockland County Department of Hospitals Healthcare 675 Novartis Pharmaceuticals Corporation Pharmaceuticals 537 Chestnut Ridge Transportation Inc. Transportation Services 372 Provident Bank Bank 304 Town of Ramapo Municipal 356 Avon Products, Inc. Cosmetics 339

Source: Rockland Economic Development Corporation (as of April, 2013)

Population Trends

Town of Ramapo

Rockland County

New York State

1950 20,584 89,276 14,830,192 1960 35,064 136,803 16,782,304 1970 76,702 229,903 18,241,391 1980 89,060 259,530 17,558,072 1990 93,961 265,475 17,990,445 2000 108,905 286,753 18,976,457 2010 126,595 311,687 19,378,102 2011 128,014 315,158 19,465,197

Source: U.S. Census Bureau, 2011 American Community Survey

Form of Town Government

The chief executive officer of the Town is the Supervisor who is elected for a term of two years and is eligible to succeed himself. He also is a member of the Town Board. In addition to the Supervisor, there are four members of the Town Board who are elected to four-year terms. Each term is staggered so that every two years the Supervisor and two members of the Town Board are elected. There is no limitation as to the number of terms which may be served by members of the Town Board. Both the Supervisor and members of the Town Board are elected at large.

Other elected officials of the Town are the Superintendent of Highways, who is elected to a term of two years, and three Town Justices who are elected to four-year terms.

The Town appoints a Director of Parks and Recreation, Director of Public Works, Town Clerk, Town Attorney, Receiver of Taxes and Director of Finance pursuant to Town Law.

Financial Organization

Pursuant to Local Law No. 1, 1968, certain of the financial functions of the Town are the responsibility of the Director of Finance. The Supervisor is, however, the chief fiscal officer of the Town. The Director of Finance, who is responsible to the Supervisor, is also designated as the Town Comptroller and Budget Officer of the Town. Christopher St. Lawrence, the current Town Supervisor, also serves the Town as Director of Finance and is the President of the Board of the Ramapo Local Development Corporation.

7OHSUSA:753803561.6

The duties of the Director of Finance include, among others, general supervision of the Department of Finance, including accounting and bookkeeping functions, review and analysis of the operations, financial condition and future financial needs of the Town, and preparation of Town budgets.

Employees

The Town provides services through approximately 332 full-time, 32 part-time and 500 seasonal employees, of which 192 employees are represented by a chapter of the Civil Service Employees Association (“CSEA”) and 98 are represented by the Policemen’s Benevolent Association (“PBA”), and 7 are represented by Ramapo Police Superior Officer’s Association (“RPSOA”). The CSEA contract expires on December 31, 2015. The contracts with the PBA and RPSOA expire on December 31, 2014.

Solid Waste Program

The Town contracts with outside vendors for the collection and disposal of solid waste within the unincorporated areas of the Town. The Town closed and capped its only landfill in November of 1997. The Town sold its solid waste transfer station for $2,000,000 to the Rockland County Solid Waste Management Authority in August of 1998. The Town no longer operates any solid waste or resource recovery facilities.

Employee Pension Plans

Substantially all employees of the Town eligible for pension or retirement benefits under the Retirement and Social Security Law of the State of New York are members of the New York State and Local Employees’ Retirement System (“ERS”) and the Local Police and Fire Retirement System (“PFRS”), collectively referred to as the “System”. The System is a cost sharing, multiple public employers’ retirement system. The obligation of employers and employees to contribute and the benefit to employees are governed by the New York State Retirement and Social Security Law (“NYSRSSL”). The System offers a wide range of plans and benefits which are related to years of service and final average salary, vesting of retirement benefits, death and disability benefits and optional methods of benefit payments. All benefits generally vest after ten years of credited service. The NYSRSSL generally provides that all participating employers in each retirement system are jointly and severally liable for any un-funded amounts. Such amounts are collected through annual billings to all participating employers. Generally, all employees, except certain part-time employees, participate in the System. The System is non-contributory with respect to members hired prior to July 27, 1976. All members hired on or after July 27, 1976 with less than ten years of service must contribute 3% of gross annual salary toward the cost of retirement programs.

On December 12, 2009, a new Tier V was signed into law. The law became effective for new ERS and TRS hires in January, 2010. The legislation created a new Tier V pension level, the most significant reform of the State’s pension system in more than a quarter-century. Key components of Tier V include:

Raising the minimum age at which most civilians can retire without penalty from 55 to 62 and imposing a penalty of up to 38% for any civilian who retires prior to age 62.

Requiring ERS employees to continue contributing 3% of their salaries and TRS employees to continue contributing 3.5% toward pension costs so long as they accumulate additional pension credits.

Increasing the minimum years of service required to draw a pension from 5 years to 10 years. Capping the amount of overtime that can be considered in the calculation of pension benefits for civilians

at $15,000 per year, and for police and firefighters at 15% of non-overtime wages.

On March 16, 2012, the Governor signed into law the new Tier VI pension program, effective for new employees hired after April 1, 2012. The Tier VI legislation provides for increased employee contribution rates of between 3% and 6%, an increase in the retirement age from 62 years to 63 years, a readjustment of the pension multiplier, and a change in the time period for final average salary calculation from 3 years to 5 years. Tier VI employees will vest in the system after ten years of employment and will continue to make employee contributions throughout employment.

8OHSUSA:753803561.6

The Town’s contributions to the ERS and PFRS since 2009 and the 2013 budgeted payments are as follows:

Year Amount 2009 $3,387,563 2010 $3,837,525 20111 $4,647,785 20121

2013 (Budgeted)1 $6,238,696 $6,856,591

1 Pursuant to the Employer Contribution Stabilization Program established pursuant to Chapter 57 of the Laws of 2010, the Town elected to amortize all of its 2011 pension contribution and $1,216,633 of its 2012 pension contribution and $2,647,283 of its 2013 pension contribution.

Pursuant to various laws, the State Legislature authorized local governments to make available certain early retirement incentive programs to its employees. The Town currently does not have any such programs outstanding.

Historically, there has been a State mandate requiring full (100%) funding of the annual actuarially required local governmental contribution out of current budgetary appropriations. With the strong performance of the System in the 1990s, the locally required annual contribution declined to zero. However, with the subsequent decline in the equity markets, the pension system became underfunded. As a result, required contributions increased substantially to 15% to 20% of payroll for the employees’ and the police and fire retirement systems, respectively. Wide swings in the contribution rate resulted in budgetary planning problems for many participating local governments.

Chapter 49 of the Laws of 2003 (“Chapter 49”) amended the NYSRSSL and the Local Finance Law to empower the State Comptroller to implement a comprehensive structural reform program for the System. The reform program requires the Town to make a minimum contribution of 4.5% of payroll every year, including years in which the investment performance of the funds administered by the system would make a lower contribution possible. In addition, the reform program instituted a billing system to match the budget cycle of municipalities and school districts that will advise such employers over one year in advance concerning the actual pension contribution rates for the next annual billing cycle. Under the previous method, the requisite System contributions for a fiscal year could not be determined until after the local budget adoption process was complete. Under the new system, a contribution for a given fiscal year is based on the valuation of the pension fund prior to April 1 of the calendar year preceding the contribution due date instead of the following April 1 in the year of contribution so that the exact amount may now be included in a budget. The Town’s contributions for fiscal year 2010 and 2011 were approximately 18.7% and 16.8% of payroll for PFRS and 9.3% and 11.3% of payroll for ERS, respectively. The 2012 contribution is 20.9% of payroll for PFRS and 15.8% of payroll for ERS.

On July 30, 2004, the Governor signed into law Chapter 260 of the Laws of 2004 (“Chapter 260”) that contains three components which alter the way municipalities and school districts contribute to the State pension system: (1) revision of the payment due date, (2) extension of the period of time for pension debt amortization, and (3) authorization to establish a pension reserve fund. Prior to the effective date of the provisions of Chapter 260, the annual retirement bill sent to municipalities and school districts from the State reflected pension payments due between April 1 and March 31, consistent with the State fiscal year. Chapter 260 requires that the annual payment for each year be paid by February 1 of the following year.

Chapter 260 also amended the Local Finance Law to permit municipalities to issue their own notes or bonds, payable over a period of up to ten years, to finance a portion of such required payments. The Town issued $1,095,000 Public Improvement Serial Bonds 2004 Taxable Series C and $108,000 Retirement Incentive (Serial) Bonds – 2005 Taxable Series B for the purpose of funding an Employees Retirement and Incentive Program.

Although Chapter 49 and Chapter 260 offer temporary relief from the short term actuarial effects of the decline in the value of pension fund investments experienced over the last several years, neither shifts the burden of providing retirement benefits to Town employees away from Town taxpayers.

The investment losses experienced in fiscal year 2009 negatively impacted the value of assets held for the System. The current actuarial smoothing method spreads the impact over a 5-year period, and thus contribution rates increased for fiscal years 2011 through 2014 and a further increase is expected for fiscal year 2015. The amount of such future increase depends, in part, on the value of the pension fund as of each April 1 as well as on the present value of the anticipated benefits to be paid by

9OHSUSA:753803561.6

the pension fund as of each April 1. Final contribution rates for fiscal year 2014 were released in September 2012. The average ERS rate in the State increased from 18.9% of salary in fiscal year 2013 to 20.9% of salary in fiscal year 2014, while the average PFRS rate increased from 25.8% of salary in fiscal year 2013 to 28.9% of salary in fiscal year 2014. The contribution rates for fiscal year 2013 reflect the System’s Actuary’s recommendations, including a reduction in the assumed investment rate of return from 8% to 7.5%, based on the legally required five year review of actuarial assumptions. While the Town is aware of the potential negative impact on its budget and will take the appropriate steps to budget accordingly for the increase, there can be no assurance that its financial position will not be negatively impacted.

The investment of monies and assumptions underlying the System covering the Town’s employees is not subject to the direction of the Town. Thus, it is not possible to predict, control or prepare for future unfunded accrued actuarial liabilities of the System (“UAALs”). The UAAL is the difference between total actuarially accrued liabilities and actuarially calculated assets available for the payment of such benefits. The UAAL is based on assumptions as to retirement age, mortality, projected salary increases attributed to inflation, across-the-board raises and merit raises, increases in retirement benefits, cost-of-living adjustments, valuation of current assets, investment return and other matters. Such UAALs could be substantial in the future, requiring significantly increased contributions from the Town which could affect other budgetary matters. Concerned investors should contact the System administrative staff for further information on the latest actuarial valuations of the System.

Other Post-Employment Benefits

In addition to providing pension benefits, the Town provides certain health care benefits for retired employees. The various collective bargaining agreements stipulate the employees covered and the percentage of contribution. Contributions by the Town may vary according to length of service. The cost of providing post-employment health care benefits is shared between the Town and the retired employee. Substantially all of the Town’s employees may become eligible for those benefits if they reach normal retirement age while working for the Town. The cost of retiree health care benefits is recognized as an expense/expenditure as claims are paid. The Town recognized revenues of $123,007 for Medicare Part D payments made directly to its health insurance carrier on behalf of its retirees in 2011.

The Town’s annual other post-employment benefit (“OPEB”) cost (expense) is calculated based on the annual required contribution (“ARC”), an amount actuarially determined in accordance with the parameters of GASB Statement No. 45. GASB Statement No. 45 establishes standards for the measurement, recognition and display of the expenses and liabilities for retiree’s medical insurance. The ARC is the sum of (a) the normal cost for the year (the present value of future benefits being earned by current employees) plus (b) amortization of the unfunded accrued liability (benefits already earned by current and former employees but not yet provided for), using an amortization period of not more than 30 years. If a municipality or school district contributes an amount less than the ARC, a net OPEB obligation will result, which is required to be recorded as a liability on the entity’s financial statements. As a result, reporting of expenses and liabilities will no longer be done under the “pay-as-you-go” approach. Instead of expensing the current year premiums paid, a per capita claims cost will be determined, which will be used to determine a “normal cost”, an “actuarial accrued liability”, and ultimately the ARC. The ARC represents a level of funding that, if paid on an ongoing basis, is projected to cover normal costs each year and amortize any unfunded actuarial liabilities over a period not to exceed thirty years. For the calendar year ended December 31, 2011, the Town’s annual OPEB cost of $22,291,009 was equal to the ARC. GASB Statement No. 45 does not require that the unfunded liability actually be amortized nor that it be advance funded, only that the municipality or school district account for its unfunded accrued liability and compliance in meeting its ARC.

Actuarial valuations for OPEB plans involve estimates of the value of reported amounts and assumptions about the probability of events far into the future. These amounts are subject to continual revision as results are compared to past expectations and new estimates are made about the future. Calculations are based on the OPEB benefits provided under the terms of the substantive plan in effect at the time of each valuation and on the pattern of sharing of costs between the employer and plan members to that point. The actuarial calculations of the OPEB plan reflect a long-term perspective.

10OHSUSA:753803561.6

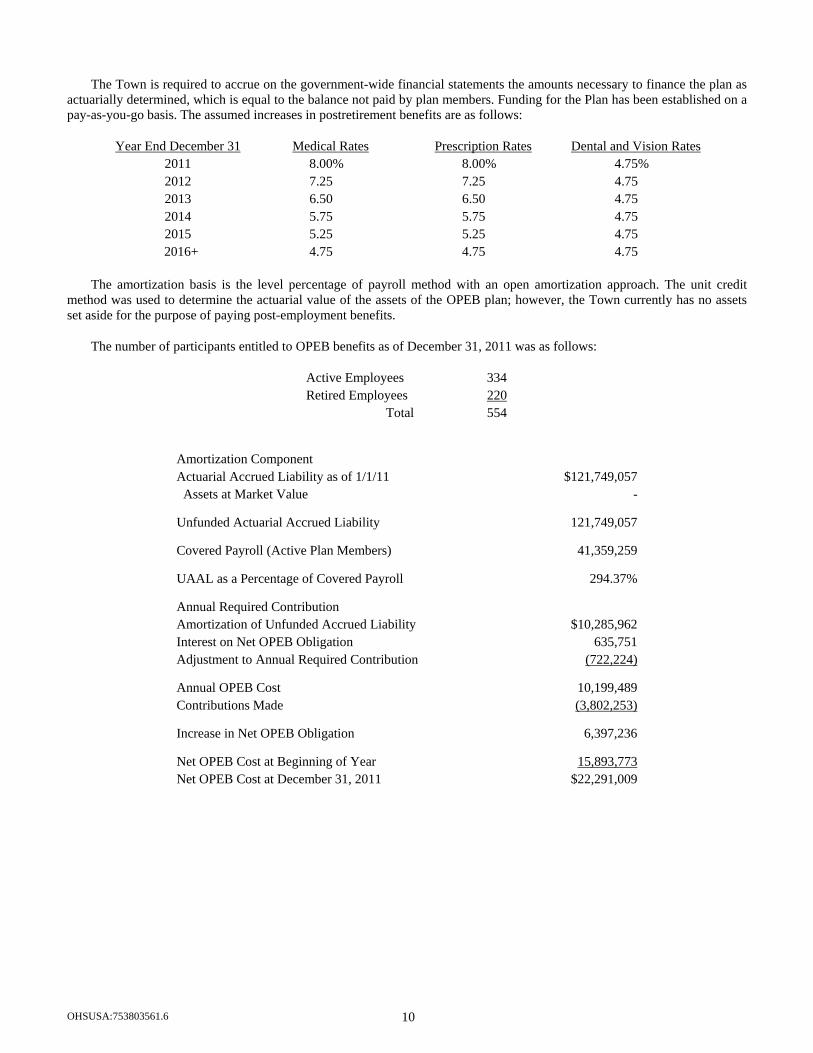

The Town is required to accrue on the government-wide financial statements the amounts necessary to finance the plan as actuarially determined, which is equal to the balance not paid by plan members. Funding for the Plan has been established on a pay-as-you-go basis. The assumed increases in postretirement benefits are as follows:

Year End December 31 Medical Rates Prescription Rates Dental and Vision Rates 2011 8.00% 8.00% 4.75% 2012 7.25 7.25 4.75 2013 6.50 6.50 4.75 2014 5.75 5.75 4.75 2015 5.25 5.25 4.75

2016+ 4.75 4.75 4.75

The amortization basis is the level percentage of payroll method with an open amortization approach. The unit credit method was used to determine the actuarial value of the assets of the OPEB plan; however, the Town currently has no assets set aside for the purpose of paying post-employment benefits.

The number of participants entitled to OPEB benefits as of December 31, 2011 was as follows:

Amortization Component Actuarial Accrued Liability as of 1/1/11 $121,749,057 Assets at Market Value -

Unfunded Actuarial Accrued Liability 121,749,057

Covered Payroll (Active Plan Members) 41,359,259

UAAL as a Percentage of Covered Payroll 294.37%

Annual Required Contribution Amortization of Unfunded Accrued Liability $10,285,962 Interest on Net OPEB Obligation 635,751 Adjustment to Annual Required Contribution (722,224)

Annual OPEB Cost 10,199,489 Contributions Made (3,802,253)

Increase in Net OPEB Obligation 6,397,236

Net OPEB Cost at Beginning of Year 15,893,773 Net OPEB Cost at December 31, 2011 $22,291,009

Active Employees 334 Retired Employees 220

Total 554

11OHSUSA:753803561.6

Unemployment Rate Statistics

AVERAGE UNEMPLOYMENT RATE (%)

Year Town of Ramapo

Rockland County

New York State

United States

2004 4.40% 4.40% 5.80% 5.50% 2005 3.90% 4.00% 5.00% 5.10% 2006 3.60% 3.80% 4.60% 4.60% 2007 3.80% 3.90% 4.60% 4.60% 2008 4.60% 4.80% 5.40% 5.80% 2009 6.60% 7.00% 8.40% 9.30% 2010 6.50% 7.10% 8.60% 9.60% 2011 6.20% 6.70% 8.30% 8.90% 2012 6.50% 6.90% 8.50% 8.10%

Source: U.S. Department of Labor and State Department of Labor.

2013 MONTHLY UNEMPLOYMENT RATE (%)

Jan Feb Mar Apr United States 7.90% 7.70% 7.60% 7.50% New York State 9.30% 8.80% 8.10% 7.30% Rockland County 7.50% 7.10% 6.40% 5.80% Town of Ramapo 6.80% 6.40% 5.70% 5.30%

Source: U.S. Department of Labor and State Department of Labor.

12OHSUSA:753803561.6

TOWN FINANCIAL INFORMATION

Financial Results

The table below includes ending balances for each of the Town’s main funds as of the end of fiscal year 2011 and estimated ending balances as of the end of fiscal year 2012. There has been no material adverse change in the financial condition of the Town since December 31, 2012.

FUND 2011 (Audited) 2012 (Unaudited)*

General Fund $2,004,151 $ 1,495,034† Town Outside Villages 357,122 1,449,278 Police Fund 1,835,887 2,623,788 Highway 187,890 427,827

Town Wide 130,986 241,428 Town Outside Villages 56,904 186,399

Special Districts Water 178,091 445,528 Sewer 66,294 (139,977) Refuse 1,154 55,232 Lighting 324,693 309,421 Ambulance 494,178 552,017

Mortgage and Sales Tax—Actual Versus Budgeted

Mortgage Tax 2012 2011 2010 Budgeted Amount $1,377,000 $2,200,000 $2,800,000

Mortgage Revenue Received 1,406,604* 1,319,358 1,321,126

Amount over/(under) $29,604* $(880,642) $(1,478,874)

Sales Tax 2012 2011 2010

Budgeted Amount $1,860,413 $1,929,250 $2,000,000

Sales Tax Revenue Received 1,689,620* 1,675,921 1,590,821

Amount over/(under) $(170,793)* $(253,329) $(409,179)

Superstorm Sandy

On Monday, October 29, 2012, Superstorm Sandy hit the New York metropolitan region. The storm caused widespread damage to the region, including substantial damage in the Town to private and public property. The Town has incurred expenses related to the storm and expects to be reimbursed by the Federal Emergency Management Agency and other federal or State agencies, though the Town cannot predict the timing or extent of any reimbursement. The storm did not materially affect the Town’s short-term revenue collections.

* Unaudited. Estimated as of May 2013. † Ending balance includes the following receivables: $3,145,503 to be received as reimbursement from the federal government for expenses of the Town related to Hurricane Irene and Superstorm Sandy, $300,000 from the ambulance fund, $300,000 from the refuse fund, and $250,000 as a community benefit agreement payment from Millennium Pipeline.

13OHSUSA:753803561.6

Budgetary Procedures

The Supervisor, with the assistance of the Deputy Director of Finance (acting in his capacity as Budget Officer), prepares a preliminary budget each year and the Town Board holds a public hearing thereon. Subsequent to the public hearing, revisions (if any) are made and the budget is then adopted by the Town Board as its final budget for the coming fiscal year. The budget is not subject to referendum. The Town is in the process of implementing a multi-year budgeting plan to supplement the normal annual budget cycle. The Town believes that this will give it additional control over its expenses. In addition, the Town is in the process of formally adopting a general fund balance policy under which the general fund balance would be maintained at a level between 15% and 20% of general fund revenues.

Financial Statements

The Town retains O’Connor Davies LLP, independent Certified Public Accountants (the “Auditor”), to conduct audits of its financial affairs. The last audit covers the fiscal year ended December 31, 2011 and is attached hereto as Appendix B. The Auditor was not associated with the preparation of this Placement Memorandum.

Summary statements of the results of operations for various funds, shown in the Appendices of this Placement Memorandum, have been derived from the annual and audited financial reports of the Town and are provided in memorandum form for information only. It is not implied by inclusion of these statements that the individual funds included performed individually in accordance therewith. Reference should be made to the actual audit reports, which are available for inspection at the Town offices.

TOWN TAX INFORMATION Valuations

Tax Levy Limitation Law

On June 24, 2011, Chapter 97 of the Laws of 2011 was signed into law by the Governor (the “Tax Levy Limitation Law”). The Tax Levy Limitation Law applies to all local governments, including school districts (with the exception of New York City, and the counties comprising New York). It also applies to independent special districts and to town and county improvement districts as part of their parent municipalities tax levies.

The Tax Levy Limitation Law restricts, among other things, the amount of real property taxes (including assessments of certain special improvement districts) that may be levied by or on behalf of a municipality in a particular year, beginning with fiscal years commencing on or after January 1, 2012. It expires on June 16, 2016 unless extended. Pursuant to the Tax Levy Limitation Law, the tax levy of a municipality cannot increase by more than the lesser of (i) two percent (2%) or (ii) the annual increase in the consumer price index (“CPI”), over the amount of the prior year’s tax levy. Certain adjustments would be permitted for taxable real property full valuation increases or changes in physical or quantity growth in the real property base as defined in Section 1220 of the Real Property Tax Law. A municipality may exceed the tax levy limitation for the coming fiscal year only if the governing body of such municipality first enacts, by at least a sixty percent vote of the total voting strength of the board, a local law (resolution in the case of fire districts and certain special districts) to override such limitation for such coming fiscal year only. There are exceptions to the tax levy limitation provided in the Tax Levy Limitation Law, including expenditures made on account of certain tort settlements and certain increases in the average actuarial contribution rates of the ERS, the PFRS, and the Teachers’ Retirement System. Municipalities are also permitted to carry forward a certain portion of their unused levy limitation from a prior year. Each municipality prior to adoption of its fiscal year budget must

Taxable Assessed Equalization Full Year Valuation Ratio Valuation 2012 2011

$1,619,398,541 1,622,724,087

14.95% 14.32%

$10,832,097,264 11,331,907,032

2010 1,631,134,215 14.15% 11,527,450,283 2009 1,642,111,085 13.17% 12,468,573,159 2008 1,641,238,403 12.38% 13,257,176,115

Source: Town of Ramapo Assessors’ Office

14OHSUSA:753803561.6

submit for review to the State Comptroller any information that is necessary in the calculation of its tax levy for such fiscal year.

The Tax Levy Limitation Law does not contain an exception from the levy limitation for the payment of debt service on either outstanding general obligation debt of municipalities or such debt incurred after the effective date of the Tax Levy Limitation Law (June 24, 2011).

Article 8 Section 2 of the State Constitution requires every issuer of general obligation notes and bonds in the State to pledge its faith and credit for the payment of the principal thereof and the interest thereon. This has been interpreted by the Court of Appeals, the State’s highest court, in Flushing National Bank v. Municipal Assistance Corporation for the City of New York, 40 N.Y.2d 731 (1976), as follows:

“A pledge of the city’s faith and credit is both a commitment to pay and a commitment of the city’s revenue generating powers to produce the funds to pay. Hence, an obligation containing a pledge of the City’s “faith and credit” is secured by a promise both to pay and to use in good faith the city’s general revenue powers to produce sufficient funds to pay the principal and interest of the obligation as it becomes due. That is why both words, “faith” and “credit”, are used and they are not tautological. That is what the words say and that is what courts have held they mean.”

Article 8 Section 12 of the State Constitution specifically provides as follows:

“It shall be the duty of the legislature, subject to the provisions of this constitution, to restrict the power of taxation, assessment, borrowing money, contracting indebtedness, and loaning the credit of counties, cities, towns and villages, so as to prevent abuses in taxation and assessments and in contracting of indebtedness by them. Nothing in this article shall be construed to prevent the legislature from further restricting the powers herein specified of any county, city, town, village or school district to contract indebtedness or to levy taxes on real estate. The legislature shall not, however, restrict the power to levy taxes on real estate for the payment of interest on or principal of indebtedness theretofore contracted.”

On the relationship of the Article 8 Section 2 requirement to pledge the faith and credit and the Article 8 Section 12 protection of the levy of real property taxes to pay debt service on bonds subject to the general obligation pledge, the Court of Appeals in the Flushing National Bank case stated:

“So, too, although the Legislature is given the duty to restrict municipalities in order to prevent abuses in taxation, assessment, and in contracting of indebtedness, it may not constrict the city’s power to levy taxes on real estate for the payment of interest on or principal of indebtedness previously contracted….While phrased in permissive language, these provisions, when read together with the requirement of the pledge of faith and credit, express a constitutional imperative: debt obligations must be paid, even if tax limits be exceeded”.

In addition, the Court of Appeals in the Flushing National Bank case has held that the payment of debt service on outstanding general obligation bonds and notes takes precedence over fiscal emergencies and the police power of municipalities.

Therefore, while the Tax Levy Limitation Law may constrict an issuer’s power to levy real property taxes for the payment of debt service on debt contracted after the effective date of the Tax Levy Limitation Law, it is clear that no statute is able (1) to limit an issuer’s pledge of its faith and credit to the payment of any of its general obligation indebtedness or (2) to limit an issuer’s levy of real property taxes to pay debt service on general obligation debt contracted prior to the effective date of the Tax Levy Limitation Law. Whether the Constitution grants a municipality authority to treat debt service payments as a constitutional exception to such statutory tax levy limitation is not clear.

15OHSUSA:753803561.6

Tax Collection Rate

For the Fiscal Years Ended December 31 2009 2010 2011 2012 2013 General Town and Highway Tax $45,064,427 $47,946,233 $50,418,000 $52,506,979 $57,267,495Special District Taxes and Assessments 32,342,913 36,054,289 38,578,469 41,078,932 44,602,870Relevied Items 1,487,893 1,304,602 1,684,004 1,712,540 1,606,444State and County Charges 18,319,564 18,604,467 20,071,684 26,039,593 29,808,316Reassessed School Taxes 9,150,904 10,582,567 10,040,038 9,713,926 10,120,767Miscellaneous Items 101,631 394,361 161,462 181,894 158,594 Total Tax Levy $106,467,332 $114,886,519 $120,953,657 $131,233,864 $143,564,486 Returned to County as Uncollected: Amount $16,896,132 $17,613,049 $18,481,652 $18,956,413 Percentage 15.87% 15.33% 15.28% 14.45% Uncollected Taxes Due to Town None None None None None

Source: Town of Ramapo

Tax Rates Per $1,000 Assessed

Fiscal Year Ending December 31 2009 2010 2011 2012 2013 General Town $8.94 $9.28 $9.75 $9.94 $10.87 Town Outside Villages 4.95 5.02 5.27 5.36 5.83 Police 21.17 22.49 23.92 24.37 26.70

Source: Town of Ramapo

Tax Collection Procedure

The Town collects County, Town, Highway and Special District Taxes. The Town offers its residents two methods for payment of taxes. With the traditional method, taxes are due January 1 and are payable without penalty until January 31. The penalty for payment during February is 1% and during March is 2%. After March 31 the tax roll is returned to the County and taxes plus penalties are payable to the County Treasurer. Since January 1, 1998, the County of Rockland has offered a quarterly installment payment option. The payments are due on January 31, April 15, July 15, and October 15 of each year. The first payment is payable to the Town Receiver and the subsequent payments are payable to the Commissioner of Finance of the County of Rockland. A service charge of 5% on each installment payment is added to the amount of taxes.

Regardless of the method of payment, the Town retains the total amount of Town, highway and special district levies from total collections it receives and returns the balance plus uncollected items to the County, which assumes collection responsibility and enforcement, and holds annual tax lien foreclosure sales. Thus, the Town is assured of receiving the total amount levied.

The Town provides school tax collection services for the Ramapo Central School District and the East Ramapo Central School District. For this service, the Town receives a fee of 1% of the respective tax collections.

16OHSUSA:753803561.6

Largest Taxpayers 2012 Assessment Roll

Name Type Assessed Valuation Consolidated Edison, Inc. Public Utility $31,637,529 State of New York Government 18,688,632 United Water Public Utility 21,581,591 Novartis Pharmaceuticals Commercial 14,843,400 Consolidated Edison Public Utility 13,987,330 Verizon New York, Inc. Commercial 8,966,883 Millennium Pipeline* Commercial 6,526,975 Dunnigan Realty Inc. Commercial 5,425,000 Four Hundred Rella Blvd Commercial 4,500,000 Algonquin Trans Co. Public Utility 4,340,701 Total: $131,469,741 Source: Town of Ramapo

*Millenium Pipeline Company, LLC (“Millenium”) commenced proceedings challenging its special franchise valuation established by the New York State Board of Real Property Tax Services in connection with gas pipelines located in the Town for certain tax years (the “Tax Certiorari Proceeding”). The Town filed a motion to intervene in the Tax Certiorari Proceeding and Millenium has since entered into a settlement agreement to resolve the dispute (“Settlement”). Pursuant to the Settlement, Millenium has waived its right to collect any refund from the Town and the Ramapo Central School District and has entered into a Community Benefit Agreement with the Town dated as of December 31, 2012 whereby Millenium will pay the Town the following annual fees: $250,000 relating to tax year 2012; $250,000 relating to tax year 2013; and $250,000 relating to tax year 2014. Such Community Benefit Agreement will be effective following approval by the County legislature of the related PILOT Agreement.

Investment Policy

The Town’s investments are governed by a formal written investment policy, which is consistent with the Investment Policies and Procedures guidelines promulgated by the Office of the State Comptroller. The Town’s monies must be deposited in FDIC-insured commercial banks or trust companies authorized to do business in the State of New York and located within the Town. The Town limits its investments to time deposit accounts, certificates of deposit and repurchase agreements that are fully collateralized and retained in segregated accounts.

It is the Town’s policy to require collateral for all deposits not covered by federal deposit insurance. Obligations that may be pledged as collateral are obligations of the United States and its agencies and obligations of the State and its municipalities and school districts.

The Town’s investment policy further provides that all investment obligations must be payable or redeemable at the option of the Town within such time or times as the proceeds will be needed to meet expenditures for the purposes for which monies were provided.

The Town’s investment policy does not permit the Town to invest in derivatives or reverse repurchase agreements and the Town has never invested in derivatives or reverse repurchase agreements.

State Aid

The Town receives financial assistance from the State. In its General Fund budget for the 2013 fiscal year, approximately 3.55% of the operating revenues of the Town are estimated to be received in the form of State aid. The State is not constitutionally obligated to maintain or continue State aid to the Town. No assurance can be given that present State aid levels will be maintained in the future. State budgetary restrictions which eliminate or substantially reduce State aid could have a material adverse effect upon the Town, requiring either a counterbalancing increase in revenues from other sources to the extent available, or a curtailment of expenditures (see also “MARKET AND RISK FACTORS” herein).

Other Information

No principal or interest on any obligation of the Town is past due.

17OHSUSA:753803561.6

The fiscal year of the Town is the calendar year.

This Placement Memorandum does not include the financial data of any political subdivision having power to levy taxes within the Town except to the extent shown in the section entitled “TOWN INDEBTEDNESS -Estimated Overlapping Indebtedness.”

TOWN INDEBTEDNESS

Constitutional Requirements

The New York State Constitution limits the power of the Town (and other municipalities and certain school districts of the State) to issue obligations and to contract indebtedness. Such constitutional limitations include the following, in summary form, and are generally applicable to the Town and its obligations.

Purpose and Pledge. Subject to certain enumerated exceptions, the Town shall not give or loan any money or property to or in aid of any individual or private corporation or private undertaking or give or loan its credit to or in aid of any of the foregoing or any public corporation.

The Town may contract indebtedness only for a Town purpose and shall pledge its faith and credit for the payment of principal of and interest thereon.

Payment and Maturity. Except for certain short-term indebtedness contracted in anticipation of taxes or to be paid within three fiscal year periods, indebtedness shall be paid in annual installments commencing no later than two years after the date such indebtedness shall have been contracted and ending no later than the expiration of the period of probable usefulness of the object or purpose as determined by statute and unless substantially level or declining annual debt service is authorized by the Town Board and utilized, no installment may be more than fifty per centum in excess of the smallest prior installment. The Town is required to provide an annual appropriation for the payment of interest due during the year on its indebtedness and for the amounts required in such year for amortization of its serial bonds and such required annual installments on its bonds.

Debt Limit. The Town has the power to contract indebtedness for any Town purpose so long as the principal amount thereof shall not exceed seven per centum (7%) of the average full valuation of taxable real estate of the Town and subject to certain enumerated exclusions and deductions such as water, electric and certain sewer facilities and cash or appropriations for current debt service. The constitutional method for determining average full valuation is by taking the assessed valuations of taxable real estate as shown upon the latest completed assessment roll and dividing the same by the equalization rate as determined by the State Board of Real Property Services. The State Legislature is required to prescribe the manner by which such ratio shall be determined. Average full valuation is determined by taking the sum of the full valuations of such last completed assessment roll and the four preceding assessment rolls and dividing such sum by five.

Pursuant to Article VIII of the Constitution and Title 8 of Article 2 of the Local Finance Law, the debt limit of the Town is calculated by taking seven per centum (7%) of the latest five-year average of the full valuation of all taxable real property.

Statutory Procedure

In general, the State Legislature has authorized the power and procedure for the Town to borrow and incur indebtedness by enactment of the Local Finance law, subject of course, to the constitutional provisions set forth above. The power to spend money, however, generally derives from other law, including specifically the Town Law and the General Municipal Law.

The adoption of proceedings authorizing the issuance of certain obligations may or may not be subject to permissive referendum. Generally the authorization of obligations having a maximum maturity in excess of five years is subject to permissive referendum subject to certain exceptions. In any event, the Town complies with the permissive referendum requirement whenever it is applicable.

The Local Finance Law also provides that where a bond resolution is published with a statutory form of notice, the validity of the bonds authorized thereby, including bond anticipation notes issued in anticipation of the sale thereof, may be contested only if:

18OHSUSA:753803561.6

(1) Such obligations are authorized for an object or purpose for which the issuer is not authorized to expend money, or

(2) There has not been substantial compliance with the provisions of law which should have been complied with in the authorization of such obligation, and an action contesting such validity is commenced within twenty days after the date of such publication, or

(3) Such obligations are authorized in violation of the provisions of the constitution.

Each bond resolution usually authorizes the construction, acquisition or installation of the object or purpose to be financed, sets forth the plan of financing and specifies the maximum maturity of the Bonds subject to the legal (Constitution, Local Finance law and case law) restrictions relating to the period of probable usefulness with respect thereto.

In general, the Local Finance Law contains provisions providing the Town with power to issue certain other short-term general obligation indebtedness including revenue and tax anticipation notes, deficiency notes, and budget and capital notes.

Trend of Debt Outstanding