tower cameron ambulance service … cameron ambulance service district financial report december 31...

TRANSCRIPT

3

IC 3

It- ' c n UK

tOWER CAMERON AMBULANCE SERVICE DISTRICT

FINANCIAL REPORT

December 31 2008

Jnder provisions of std .. i w this report is a public document A copy of the report has been submitted to 'he entity and other appropnate public officiais The report IS available for public inspection at the Baton ^ouge office of the LegislativeAuditor and where ^opropnate at the office of the parish clerk of court

^p|P3se Date ^ l / 5 ^ / 0 ' T

C O N T E N T S

Page

INDEPENDENT AUDITORS REPORT land 2 ON THE BASIC FINANCIAL STATEMENTS

BASIC FINANCIAL STATEMENTS

Balance sheets 3 Statements of revenues expenses and changes in net assets 4 Statements of cash flows 5 and 6 Notes to financial statements 7 13

SUPPLEMENTARY INFORMATION

Schedules of net patient service revenues 16 Schedules of board fees 17

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCLAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS 19 and 20

Schedule of findings and responses 21 Schedule of prior year findings 22

BROUSSARD, FOCHE, LEWIS & BREAUX, L L P C E R T I F I E D P U B L I C A C C O U N T A N T S

4112 West Congrest

P C Box61400 Lafayette I^oiusiana 70596-1400 p h o n e (337) 988-4930 fax (337)994-4574 www bplb Com

INDEPENDENT AUDITORS REPORT

Other Offices

Crowley L \

(337) 783-5693

O p d o i u a j LA

(337) 942 5 ^ 7

AbbeviUe l A

(337) 898 1497

New Ibena, LA

(337) 364-4S54

Church Point l A

(337) 684-2S55

Frank A Stagno CPA'*'

Scott J Broussard CPA*

L. Charles Abshire CPA*

P John Blanchtt, lU CPA*

Martha B Wyati CPA*

MaiyACastif lc CPA*

JoeyL Breaux CPA*

Craig J Vmtor CPA*

Stacey E Singleton CPA*

John L l8t*e CPA*

T n c i a D Lyoni CPA*

M a r y T Mjlef CPA*

EhzabethJ Moreau, CPA*

Frank D Bergeron CPA*

R e t i r e d

S dney L Broussard CPA 1925 2005

L e o n K . P o t h i CPA 1984

James H Breaux CPA 1987

Erma R Walton, CPA 1988

George A Lewu CPA 1992

GeraldmeJ Wimbcrfcy CPA 1995

Lawrence A Cramer CPA 1999

Ralph Fno^d CPA 2002

D o n a U W KcBey CPA 2005

George J Tnippey IH CPA 2007

Tcrrel P Dreitel, CPA 2007

Herbert Lcmomc n CPA 2008

To the Board of Commissioners Lower Cameron Ambulance Service Distnct Creole Louisiana

Wc have audited the accompanying basic financial statements of Lower Cameron Ambulance Service Distnct a component unit of the Cameron Pansh Police Jury as of and for the years ended December 31 2008 and 2007 as listed in the table of contents These financial statements are the responsibility ofthe Ambulance Distnct s management Our responsibility is to express an opinion on these financial statements based on our audits

We conducted our audits m accordance with auditing standards generally accepted in the United States of Amenca and the standards applicable to financial audits contained in Government Auditmg Standards issued by the Comptroller General of the United States Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of matenal misstatement An audit mcludes exammmg on a test basis evidence supporting the amounts and disclosures in the financial statements An audit also includes assessmg the accounting prmciples used and significant estimates made by management as well as evaluating the overall financial statement presentation We believe that our audits provide a reasonable basis for our opinion

In our opmion the financial statements referred to above present feirly in all matenal respects the financial position of Lower Cameron Ambulance Service Distnct as of December 31 2008 and 2007 and the results of its operations and cash flows for the years then ended in conformity with accounting pnnciples generally accepted in the United States of Amenca

In accordance with Government Auditmg Standards we have also issued our report dated June 30 2009 on our consideration of Lower Cameron Ambulance Service Distnct s intemal control over financial reportmg and our tests of its compliance with certain provisions of laws regulations contracts and grant agreements and other matters The purpose of that report is to descnbe the scope of our testing of intemal cono-ol over financial reportmg and compliance and the results of that testing, and not to provide an opinion on the interna! control over financial reporting or on comphance That report is an integral part of an audit performed m accordance with Govemment Auditmg Standards and should be considered in assessing the results of our audits

The Lower Cameron Ambulance Service Distnct has not presented management s discussion and analysis that accounting pnnciples generally accepted in the United States has determined is necessary to supplement although not required to be part of the basic financial statements

W b /Am Inst i C n r d Publ A nl ni S tvofLa s n Ce tif d F bl A I nc

A P f lal A ting C rp

Our audits were conducted for the purposes of forming an opmion on the basic financial statements taken as a whole The supplementary mformation listed in the table of contents is presented for purposes of additional analysis and is not a required part ofthe basic financial statements Such information has been subjected to the auditmg procedures applied in the audit of the basic financial statements and m our opmion is fairly stated in all matenal respects m relation to the basic financial statements taken as a whole

Lafayette Louisiana June 30 2009

LOWER CAMERON AMBULANCE SERVICE DISTRICT

BALANCE SHEETS December 31 2008 and 2007

ASSETS 2008 2007

CURRENT ASSETS Cash and cash equivalents Certificates of deposits Patient accounts receivable net of allowance for estunated uncollectibles of

$6 429 and $25 105 for 2008 and 2007 respectively Ad valorem tax receivable net of estimated uncollectibles of

$45 496 and $45 526 for 2008 and 2007 respectively Due from other govemmental agencies Other receivables Prepaid expenses Inventones

$ 421156 $ 113 688 2 981774 2 650 000

9 134 16 004

469 404 1012 796

34 274 39 084 5,585

200 596 999 320 60 814 35 878 13 294

Total current assets $ 4 973 207 $ 4 0S9 594

CAPITAL ASSETS Property plant and equipment at cost less accumulated

depreciation of $407 317 and $403 846 for 2008 and 2007 respectively 59,216 153 990

Total assets $ 5 032 423 $ 4 243 584

LIABILITIES AND NET ASSETS

CURRENT LLABILITIES Accounts payable Accmed liabilities

27 315 $ 19 548 42,165 30,757

Total current liabilities 69,480 $ 50 305

NETASSETS Invested m capitai assets net of related debt Unrestncted

$ 59 216 $ 153 990 4 903 727 4 039 289

Total net assets

Total liabilities and net assets

$ 4 962,943 $ 4.193 279

$ 5 032 423 $ 4 243 584

See Notes to Financial Statements

LOWER CAMERON AMBULANCE SERVICE DISTRICT

STATEMENTS OF REVENUES EXPENSES AND CHANGES IN NET ASSETS Years Ended December 31 2008 and 2007

2008 2007

Operatmg revenues Net patient service revenues net of provision of bad debts of

$8 003 and $47 920 for 2008 and 2007 respectively Other operatmg revenues

Total operatmg revenues

Operatmg expenses Salanes and payroll taxes Depreciation expense Dispatch services Education and travel Employee benefits Fuel expense Insurance expense Medical director Professional fees Rent Repau^ and mamtenance Retirement expense Supplies Telephone Utilities Other expenses

Total operatmg expenses

Operatmg loss

Non operatmg revenues Ad valorem taxes Investment mcome Non capitai grants Gam on mvoluntary conversion of capitai assets

Total non-operatmg revenues

$

$

$

$

$

$

L_

98 980 14 179

113 159

663 646 17 975 20 000 3 839

106 670 12 861 63 018

11200 5 002 17 329 12 143 45 248 8 499 15 194 10.322

1012 946

(899 787)

1 508 541 116 967 2 137 31,903

1 659 548

$

—

S_

$

$

$

$

$

75 112 9

75 121

613 869 42 744 20 000 1031

82 383 10 877 52 775 3 000 9 285 600

15 949 11399 62 424 10 388 12 794 8 814

958,332

(883 211)

1 186 379 146 670 49 706

1,382,755

Excess of revenues over expenses before capital grants

Capitai grants

Increase m net assets

Net assets beginnmg of year

Net assets end of year

See Notes to Fmancial Statements

759 761 $ 499 544

9,903 10,036

$ 769 664 $ 509 580

4 193 279 3 683 699

$ 4 962,943 $ 4 193 279

LOWER CAMERON AMBULANCE SERVICE DISTRICT

STATEMENTS OF CASH FLOWS Years Ended December 31 2008 and 2007

2008 2007

CASH FLOWS FROM OPERATING ACTIVITIES Receipts from and on behalf of patients Payments to employees Payments to suppliers and contractors Other receipts and payments net

Net cash used m operating activities

CASH FLOWS FROM NON CAPITAL FINANCING ACTIVITIES Ad valorem taxes Non capitai grants

Net cash provided by non capital financing activities

CASH FLOWS FROM CAPITAL AND RELATED FINANCING ACTIVITIES Purchase of capital assets Capitai grant mcome Insurance proceeds from mvoluntary conversion of capital assets

Net cash provided by (used in) capitai and financmg activities

CASH FLOWS FROM INVESTING ACTIVITIES Interest mcome Purchase of certificates of deposit net of renewals

Net cash used in mvestmg activities

Net mcrease (decrease) m cash and cash equivalents

Cash and cash equivalents beginnmg of year

Cash and cash equivalents end of year

$ 105 850 $ 77 611 (652 238) (611974) (319 055) (368 367)

14 179 9

$

$

$

(851264) $

1 226 257 $ 2,137

1 228 394 $

(902 721)

933 925 49,706

983 631

(12 386) $ (16 056) 9 903 10 036

121088

$

$

$

$

118 605

143 507 (331,774)

(188 267)

307 468

113 688

$

$

$

S

(6 020)

120 943 (909 831)

(788 888)

(713 998)

827 686

421,156 $ 113 688

(contmued)

LOWER CAMERON AMBULANCE SERVICE DISTRICT

STATEMENTS OF CASH FLOWS (CONTINUED) Years Ended December 31 2008 and 2007

2008 2007

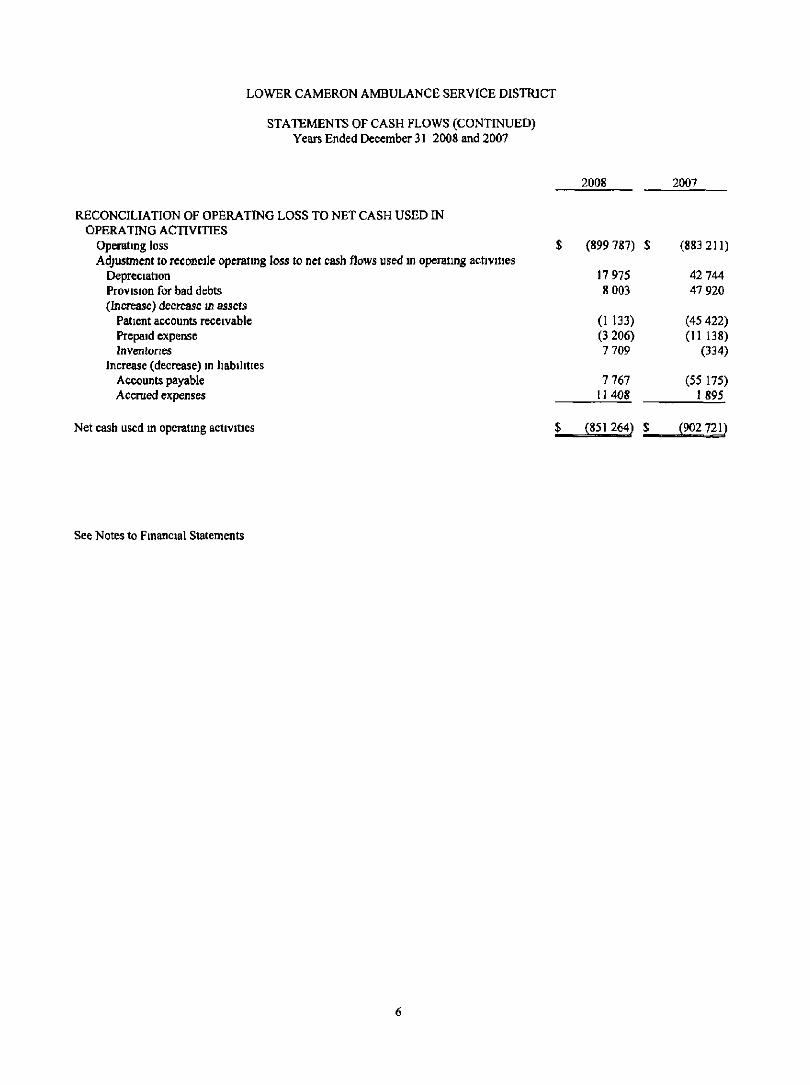

RECONCILLATION OF OPERATING LOSS TO NET CASH USED IN OPERATING ACl IVITIES

Operatmg loss Adjustment to reconcile operatmg loss to net cash flows used m operatmg activities

Depreciation Provision for bad debts (Increase) decrease m assets

Patient accounts receivable Prepaid expense Inventones

Increase (decrease) in liabilities Accounts payable Accmed expenses

$ (899 787) $

17 975 8 003

(I 133) (3 206) 7 709

7 767 11408

(883 211)

42 744 47 920

(45 422) (11 138)

(334)

(55 175) 1895

Nel cash used m operatmg activities

See Notes to Financial Statements

LOWER CAMERON AMBULANCE SERVICE DISTRICT

NOTES TO FINANCIAL STATEMENTS

Note 1 Descnption of Organization and Summary of Significant Accounting Policies

Lower Cameron Ambulance Service Distnct (the Ambulance Distnct ) was established by the Cameron Pansh Policy Jury by vutue of the authonty of R S 33 9053 et seq The purpose of the Ambulance District is to provide ambulance services to Lower Cameron Pansh The board is appomtcd by the Cameron Pansh Police Jury

As the govemmg authonty ofthe Pansh for reportmg purposes the Cameron Pansh Police Jury is the financial reportmg entity for the Ambulance Distnct Accordingly the Ambulance District was determmed to be a component unit ofthe Cameron Pansh Police Jury based on GASB Statement No 14 The Fmancial Reportmg Entity The accompanymg financial statements present only the Ambulance Distnct

The accompanying basic financial statements ofthe Ambulance Distnct have been prepared m conformity with generally accepted accountmg pnnciples (GAAP) in the United States of America as applicable to govemmental entities The Govemmental Accounting Standards Board (GASB) is the accepted standard setting body for establishing govenunental accountmg and financial reporting principles In June 1999 the GASB unanimously approved Statement No 34 Basic Financial Statements and Management s Discussion and Analysis for State and Local Governments GASB 34 established standards for extemal fmancial reporting for all state and local govemmental entities which included a balance sheet or statement of net assets a statement of revenues expenditures and changes in net assets and a statement of cash flows utilizing the duect method of presentation The Statement requires the classification of net assets into four components invested in capitai assets net of related debt restncted expendable net assets restncted nonexpendable net assets and unrestncted net assets Net assets invested m capitai assets net of related debt consist of capitai assets net of accumulated depreciation and reduced by the current balances of any outstanding borrowings used to finance the purchase or construction of those assets Restricted expendable net assets are non capitai net assets that must be used for a particular purpose as specified by creditors grantors or contnbutors extemal to the Ambulance District Restricted nonexpendable net assets equal the prmcipal portion of permanent endowments Unrestricted net assets are remaining net assets that do not meet the definition of invested in capitai assets net of related debt or restricted These and other changes are reflected m the accompanying basic financial statements (including the notes to the financial statements)

The more significant policies ofthe Ambulance Distnct are descnbed below

Method of accountmg

The Ambulance Distnct utilizes the propnetary fimd method of accountmg whereby revenues and expenses are recognized on the accmal method The Ambulance Distnct s accountmg and reportmg procedures also conform to the requirements of Louisiana Revised Statute 24 514 and to the guide set forth m the Louisiana Governmental Audit Guide and the Audit and Accountmg Guide - Health Care Organizations published by the Amencan Institute of Certified Public Accountants and standards established by the Govenunental Accounting Standards Board (GASB) which is the accepted standard settmg body for establishmg govemmental accounting and financial reportmg pnnciples

LOWER CAMERON AMBULANCE SERVICE DISTRICT

NOTES TO FINANCIAL STATEMENTS

Accounting standards

Pursuant to the GASB (GASB) Statement No 20 Accountmg and Fmancial Reportmg for Propnetary Funds and Other Governmental Entities That Use Proprietary Fund Accounting the Ambulance District has elected to apply the provisions of all relevant pronouncements ofthe Financial Accounting Standards Board (FASB) mcludmg those issued after November 30 1989 that do not conflict with or contradict GASB pronouncements

Use of estunates

The preparation of financial statements m conformity with generally accepted accounting pnnciples requu^s management to make estimates and assumptions that affect the reported amounts ofassets and liabilities and disclosure of contingent assets and liabilities at the date ofthe financial statements and the reported amounts of revenues and expenses dunng the reporting period Actual results could differ from those estimates

Cash and cash equivalents

For purposes ofthe statements of cash flows the Ambulance Distnct considers all highly liquid mvestments with an original maturity of three months or less when purchased to be cash equivalents Under state law the Ambulance District may deposit fimds in demand deposits mterest bearing demand deposits or tune deposits with state banks organized under Louisiana Law or any other state ofthe United States or under the laws ofthe United States

Trade receivables and allowance for uncollectible accounts

Trade receivables are earned at the onginal billed amount less an estimate made for uncollectible accounts based on a review of all outstandmg amounts on a monthly basis Management determines the allowance for uncollectible accounts by identifying troubled accounts and by usmg histoncal experience applied to an agmg of accounts Trade receivables are wntten off when deemed uncollectible Recovenes of trade receivables previously wntten off are recorded when received

Inventones

Inventones are valued at the latest mvoice pnce which approximates the lower of cost (first m first out method) or market

Capital assets

Capitai assets are stated at cost Depreciation is computed usmg the straight line method over the estimated useful lives of each class of depreciable assets

Ambulances 5 years Buildmg improvements 5 -10 years Equipment 5-10 years Buildmg 25 years

Net patient service revenues

Net patient service revenues are reported at estimated net realizable amounts fixim patients thu d party payors and others for services rendered mcludmg estimated retroactive adjustments under reimbursement agreements with thu-d party payors Retroactive adjustments are accmed on an estimated basis m the penod the related services are rendered and adjusted m future penods as final settlements are determmed

LOWER CAMERON AMBULANCE SERVICE DISTRICT

NOTES TO FINANCIAL STATEMENTS

Grants and donations

Revenues from grants and donations (mcludmg capitai contnbutions of assets) arc recognized when all eligibility requu-ements mcludmg time requirements are met Grants and donations may be restncted for either specific operatmg purposes or for capital purposes Amounts that are unrestncted or that are restncted to a specific operating purpose are reported as non operatmg revenues Amounts restncted to capitai acquisitions are reported after non operatmg revenues and expenses

Operatmg revenues and expenses

The Ambulance Distnct s statements of revenues expenses and changes in net assets distinguishes between operatmg and non operatmg revenues and expenses Operatmg revenues result fix)m exchange transactions associated with providmg health care services the Ambulance Distnct s pnncipal activity Non exchange revenues includmg taxes grants and contributions received for purposes other than capitai asset acquisition are reported as non operatmg revenues Operating expenses are all expenses incurred to provide health care services other than financing costs

Income taxes

The Ambulance Distnct is a political subdivision and exempt from taxes

Restricted resources

When the Ambulance District has both restncted and unrestricted resources available to finance a particular program it is the Ambulance Distnct s policy to use restncted resources before unrestricted resources

Risk management

The Ambulance Distnct is exposed to vanous risks of loss from tort theft of damage to and destmction of assets business intermption errors and omissions employee injunes and illnesses natural disasters and employee health Commercial insurance coverage is purchased for claims ansing from such matters

Environmental matters

The Ambulance District is subject to laws and regulations relatmg to the protection ofthe envux)nment The Ambulance Distnct s policy is to accme envu'onmental and cleanup related costs of a non capitai nature when It IS both probable that a liability has been mcurred and when the amount can be reasonably estimated Although It is not possible to quantify with any degree of certamty the potential financial impact of the Ambulance Distnct s contmumg compliance efforts management believes any future remediation or other compliance related costs will not have a matenal adverse effect on the financial condition or reported results of operations ofthe Ambulance Distnct At December 31 2008 management is not aware of any liability resulting from environmental matters

New accountmg pronouncements

In September 2006 the FASB issued Statement No 157 Fau- Value Measiu-ements This Statement defines fair value establishes a fi^mework for measunng fair value and expands disclosuires about fair value measurements This Statement applies to other accounting pronouncements that require or permit fair value measurements

LOWER CAMERON AMBULANCE SERVICE DISTRICT

NOTES TO FINANCLAL STATEMENTS

This Statement is effective for financial statements issued for fiscal years begmnmg after November 15 2007 and mtenm penods within those fiscal years The Ambulance District adopted this Statement as it applies to fair value measurements and m accordance with GASB Statement No 31 Accounting and Fmancial Reportmg for Certam Investments and for Extemal Investment Pools as of January 1 2008 The adoption of this pronouncement had no effect on the financial statements ofthe Ambulance Distnct as the Ambulance Distnct had no such investments However m future years if the Ambulance Distnct does have the investments mcluded above the pronouncements will be followed

Note 2 Net Patient Service Revenues

The Ambulance Distnct has agreements with third party payors that provide for payments to the Ambulance Distnct at amounts different from its established rates A summary of the payment arrangements with major thu-d party payors follows

Medicare - Covered ambulance services are paid based on a fee schedule

Medicaid - Covered ambulance services are paid based on a fee schedule

Dunng the years ended December 31 2008 and 2007 approxunately 37% and 18% ofthe Ambulance Distnct s gross patient services were furnished to Medicare and Medicaid beneficiaries

The Ambulance Distnct also has entered into payment arrangements with certam commercial insurance carriers health maintenance organizations and prefen-ed provider organizations The basis for payment to the Ambulance District under these agreements mcludes prospectively determined rates per ambulance tnp discounts on charges and prospectively determined rates

The Ambulance Distnct also gives a pansh resident discount to any resident ofthe pansh who uses ambulance services The Ambulance District bills pnvate msurance companies Medicare or Medicaid or any other coverage ofthe patient and accepts this as payment m full from the resident

Note 3 Bank Deposits and Investments

The Ambulance Distnct s mvestmg is performed in accordance with mvestment policies complying with state statutes Funds may be mvested m time deposits money market investment accounts or certificates of deposit with financial mstitutions insured by FDIC du"ect obligations ofthe United States Government and its agencies commercial paper issued by United States Corporations with a ratmg of A 1 (Moody s) and P 1 (Standard and Poor s) or higher and goverrunent backed mutual trust funds At December 31 2008 the Ambulance Distnct s funds consisted solely of demand deposits and certificates of deposits These deposits are stated at cost which approxmiates market

Custodial Credit Risk - Deposits Custodial credit nsk is the nsk that in the event of a bank failure the Ambulance Distnct s deposits may not be returned to it State law requu-es collateralization of all deposits with federal depository msurance and other acceptable collateral m specific amounts The Ambulance Distnct s policy requires that all bank balances be insured or collateralized by the financial institution to pledge their own secunties to cover any amount in excess of Federal Depository Insurance Coverage (FDIC) These secunties must be pledged m the Ambulance Distnct s name As of December 31 2008 $ 1 000 000 of the Ambulance Distnct s deposits were secure fiTsm nsk by FDIC coverage and $2 408 881 of securities pledged by the financial institution Accordingly the Ambulance Distnct had no custodial credit risk related to its deposits at December 31 2008

10

LOWER CAMERON AMBULANCE SERVICE DISTRICT

NOTES TO FINANCLAL STATEMENTS

Note 4 Accounts Receivable

Patient accounts receivable reported as current assets by the Ambulance Distnct at December 31 2008 and 2007 consisted of these amounts

Patient Accounts Receivable

Receivable from patients and theu" msurance carriers Receivable from Medicare Receivable from Medicaid

Total patient accounts receivable Less allowance for uncollectible amounts

Patient accounts receivable net

2008 2007

$

$

$

12 721 $ 1667 1,175

15 563 $ (6,429)

9 134 $

37 838 3 143 128

41 109 (25 105)

16 004

Note 5 Concentrations of Credit Risk

The Ambulance Distnct grants credit without collateral to its patients most of whom are local residents and are msured under thu-d party payor agreements The mix of receivables from patients and third party payors at December 31 2008 and 2007 was as follows

2008 Medicaid Medicare Other thu-d party payors/patients

2007

8 % 11 % 81 %

100 %

2 % 8 % 90 %

100 %

Note 6 Ad Valorem Taxes

The Ambulance Distnct s property tax is levied by the parish on the taxable real property in the distnct m late October of each year Bills are sent out m November of each year at which time the Ambulance Distnct records the tax revenue and become a lien m the followmg March The collection period for the Ambulance Distnct s property taxes is from December (at which time they become delmquent) to the succeedmg May

Pursuant to Act No 1140 of the 2001 Regular Legislative Session protested ad valorem tax receipts are no longer segregated and held pendmg the outcome ofthe protest lawsuit Instead these payments are remitted to the Ambulance Distnct If the taxpayer successfully wms the protest lawsuit the Ambulance District is liable to pay the taxpayer the protested tax amount plus mterest At December 31 2008 and 2007 the amount of protested ad valorem taxes paid pendmg the outcome of protest lawsuits was $703 266

11

LOWER CAMERON AMBULANCE SERVICE DISTRICT

NOTES TO FINANCIAL STATEMENTS

Note 7 Capitai Assets

Capitai asset additions retirements and balances for the years ended December 31 2008 and 2007 were as follows

Land Equipment Office equipment Buildmgs and improvements Ambulances

Total histoncal cost

December 31 2007

$ 16 000 73 246 23 550

105 980 339,060

Additions

$ 10 192 2 194

Retirements

$ (1419) (7 630)

(94 640)

December 31

$

2008 16 000 82 018 18 114 11340

339,060

$ 557 836 $ 12 386 $ (103 689) S 466 533

Less accumulated depreciation for Equipment Office equipment Buildmgs and improvements Ambulances

Total accumulated depreciation Capitai assets net

$ (40 769) $ (11440) $ (15 396) (9 522)

(338,159)

(I 977) (3 658) (900)

260 $ (51 949) 3 775 10 469

(13 598) (2 711)

(339 059)

$ (403 846) $ (17 975) $ 14,504 $ (407.317)

$ 153 990 $ (5 589) $ (89 186) $ 59 216

Land Equipment Office equipment Buildmgs and improvements Ambulances

Total histoncal cost

December 31 2006

$ 16 000 63 209 26 951

102 230 339 060

Additions

$ 10 037 2 269 3 750

Rel

$

Dei

tu-ements

$

(5 670)

cember 31 2007

16 000 73 246 23 550

105 980 339 060

$ 547 450 S 16.056 $ (5.670) $ 557,836

Less accumulated depreciation for Equipment Office equipment Buildmgs and improvements Ambulances

Total accumulated depreciation C apital assets net

$ (31345) $ (9 424) $ (18 592) (2 474) (4 634) (4 888)

(312 201) (25 958) _ $ (366,772) $ (42,744) $_ S 180 678 $ (26 688) $

5 670 (40 769) (15 396)

(9 522) (338 159)

5 670 $ (403,846) $ 153 990

Depreciation expense for the years ended December 31 2008 and 2007 amounted to $17 975 and $42 744 respectively

12

LOWER CAMERON AMBULANCE SERVICE DISTRICT

NOTES TO FINANCLAL STATEMENTS

Note 8 Compensated Absences

Employees vacation benefits are recognized m the period eamed Accmed compensated absences at December 31 2008 and 2007 totaled $22 147 and $17 038 respectively which is mcluded m accmed liabilities on the balance sheets

Note 9 Simple IRA Plan

The Ambulance Distnct has a Simple IRA Plan covenng all eligible employees as of June 2002 Employees can contribute a maximum of $10 500 for the 2008 and 2007 lax years The Ambulance Distnct contnbutes 2% of compensation to each eligible employee s Simple IRA for the year Total Simple IRA plan expenses for the years ended 2008 and 2007 were $12 143 and $11 399 respectively

13

This page mtentionally left blank

14

SUPPLEMENTARY INFORMATION

15

LOWER CAMERON AMBULANCE SERVICE DISTRICT

SCHEDULES OF NET PATIENT SERVICE REVENUES Years Ended December 31 2008 and 2007

2008 2007

Gross patient service revenues $ 205 021 $ 198 958

Less Medicare and Medicaid contractual adjustments Provision for uncollectible accounts Pansh resident discounts Insurance and other discounts

(29 172) (8 003)

(67 571) (1 295)

(15 603) (47 920) (56 521) (3 802)

Net patient service revenue 98 980 $ 75 112

16

LOWER CAMERON AMBULANCE SERVICE DISTRICT

SCHEDULES OF BOARD FEES Years Ended December 31 2008 and 2007

Board Members

The Ambulance District s board members did not receive any compensation durmg the years ended December 31 2008 and 2007

17

This page mtentionally left blank

18

BROUSSARD, PQCHE, LEWIS & BREAUX, L L P C E R T I F I E D P U B L I C A C C O U N T A N T S

4112 West Congress P O Box 61400 Lafayette Louisiana 70596 1400 p b o n e (337) 9S8-4930 £ix (337)984-4574 www bplb com

Other Offices

Crowley LA

(337) 783-5693

Opelousas LA

(337) 942-5217

AbbeviDc LA

(337) 898 1497

New Ibena LA

(337) 364-4554

Church Pomt, LA

(337) 684-2855

Frank A Stagno CPA*

Scott J BrousBard CPA*

L Cha lea Ahshirc CPA*

P John Blanchct UI CPA*

Martba B Wyatt CPA*

MaryACasttOe CPA*

J o e y L Breaux CPA*

Crate J Vutor CPA*

Stacey E Smgteton CPA*

JohBL Istrc CPA*

T n c i a D Lyons CPA*

M a i y T Miller CPA*

EhzabethJ Moreau,CPA*

Frank D Bergeron, CPA*

R e t i r e d

S dney L Broussa d CPA 1925 2005

LeonK.Pocb* CPA 1984

James H Breaux CPA 1987

E ima R Waltoa, CPA 1988

George A Lewis CPA 1992

GcraldmeJ Wimberiey CPA 1995

Lawrence A Cramer CPA 1999

Ralph Fnend CPA 2002

DonaW "W Kelley CPA 2005

George J Trappcy III CPA 2007

Ter re lP Drcssei, CPA 2007

Herbert Lemoine n CPA 2008

REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF

FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WFTH GOVERNMENT AUDITING STANDARDS

To the Board of Commissioners Lower Cameron Ambulance Service Distnct Creole Louisiana

We have audited the basic financial statements of the Lower Cameron Ambulance Service District as of and for the year ended December 31 2008 and have issued our report thereon dated June 30 2009 We conducted our audit in accordance with auditmg standards generally accepted m the United States of America and the standards apphcable to financial audits contamed m Government Auditing Standards issued by the Comptroller General ofthe United States

Intemal Control Over Financial Reporting

In plaiming and performing our audit we considered the Lower Cameron Ambulance Service District s intemal control over financial reportmg as a basis for designmg our auditmg procedures for the purpose of expressing our opinion on the financial statements but not for the purpose of expressing an opmion on the effectiveness of the Lower Cameron Ambulance Service District s mtemal control over financial reportmg Accordmgly we do not express an opmion on the effectiveness of the Lower Cameron Ambulance Service Distnct s mtemal control over financial reporting

Our consideration of intemal control over financial reporting was for the limited purpose descnbed m the preceding paragraph and would not necessarily identify all deficiencies in mtemal control over financial reporting that might be significant deficiencies or material weaknesses However as discussed below we identified a certain deficiency in intemal control over financial reporting that we consider to be a significant deficiency

A control deficiency exists when the design or operation of a control does not allow management or employees in the normal course of performmg their assigned functions to prevent or detect misstatements on a timely basis A significant deficiency is a control deficiency or combination of control deficiencies that adversely affect the entity s ability to initiate authonze record process or report financial data reliably in accordance with generally accepted accounting pnnciples such that there is more than a remote likelihood that a misstatement of the entity s financial statements that is more than inconsequential will not be prevented or detected by the entity s mtemal control We consider the deficiency descnbed m 2008 I ofthe accompanying schedule of findings and responses to be a significant deficiency m mtemal control over financial reportmg

M n b fAm n n Insr tut f C n n d p bi A nt nt S CI ry f l o n C mC d P n A n

A P f otul A trig Corp raoo

19

A matenal weakness is a significant deficiency or combination of significant deficiencies that results in more than a remote likelihood that a matenal misstatement of the financial statements will not be prevented or detected by the entity s intemal control However we consider the significant deficiency descnbed above to be a material weakness

Our consideration ofthe internal control over financial reportmg was for the limited purpose descnbed m the first paragraph of this section and would not necessarily identify all deficiencies in the mtemal control that might be significant deficiencies and accordmgly would not necessanly disclose all significant deficiencies that are also considered to be matenal weaknesses

Compliance and Other Matters

As part of obtammg reasonable assurance about whether the Lower Cameron Ambulance Service District s financial statements are free of matenal misstatement, we performed tests of its compliance with certam provisions of laws regulations contracts and grant agreements noncompliance with which could have a du^ct and matenal effect on the determmation of financial statement amounts However providmg an opmion on compliance with those provisions was not an objective of our audit and accordmgly we do not express such an opinion The results of our tests disclosed no instances of noncompliance that are required to be reported under Government Auditmg Standards

Lower Cameron Ambulance Service Distnct s response to the findmg identified in our audit is descnbed in the accompanying schedule of findings and responses We did not audit the Lower Cameron Ambulance Service Distnct s response and accordmgly we express no opmion on it

This report is intended solely for the information and use of management the Board of Commissioners others withm the entity federal award agencies and pass through entities and is not intended to be and should not be used by anyone other than these specified parties However this report is a matter of public record and its distnbution is not limited

J^A^v^if^^ Yo(tM^ ^e«.rio ^ ^ ^ A ^ a y ^ ^ S ^ f \ Lafayette Louisiana June 30 2009

20

LOWER CAMERON AMBULANCE SERVICE DISTRICT

SCHEDULE OF FINDINGS AND RESPONSES Year Ended December 31 2008

We have audited the basic financial statements of Lower Cameron Ambulance Service Distnct as of and for the year ended December 31 2008 and have issued our report thereon dated June 30 2009 We conducted our audit m accordance with auditmg standards generally accepted m the United States of Amenca and the standards applicable to financial audits contamed m Government Auditmg Standards issued by the Comptroller General ofthe United States Our audit ofthe basic financial statements as of and for the year ended December 31 2008 resulted m an unqualified opmion

Section I Summary of Auditor's Reports

a Report on Intemal Control and Compliance Matenal to the Financial Statements

Intemal Control Matenal Weaknesses identified ^Yes Q No Significant Deficiency identified that is

not considered to be a material weakness []] Yes [3 No

Compliance Noncompliance Matenal to Financial Statements n Yes ^ No

Was a management letter issued'' • Yes ^ No

Section 11 Financial Statement Findings

2008 1 Segregation of Duties

Fmding The Ambulance Distnct does not have adequate segregation of duties A system of mtemal control procedures contemplates a segregation of duties so that no one mdividual handles a transaction from its inception to Its completion While we recognize the Ambulance Distnct may not be large enough to permit such procedures it is important that you be aware of this condition This condition was also included m the 2008 audit as Item 2008 I

Recommendation Keepmg m mind the limited number of personnel to which duties can be assigned the Ambulance Distnct should continue to monitor assignment of duties to assure as much segregation of duties and responsibility as possible and the board should review financial mformation on a timely basis

Response The Ambulance Distnct is aware of and evaluated this problem and concluded that it would not be cost beneficial or possible with the limited resources available to create a segregated accounting envuonment However the Ambulance District will contmue to monitor this issue and the board will review financial mformation on a timely basis

21

LOWER CAMERON AMBULANCE SERVICE DISTRICT

SCHEDULE OF PRIOR YEAR FINDINGS Year Ended December 31 2008

Section I Internal Control and Compliance Matenal to the Financial Statements

2007 1 Segregation of Duties

Recommendation Keepmg in mmd the limited number of personnel to which duties can be assigned the Ambulance Distnct should continue to monitor assignment of duties to assure as much segregation of duties and responsibility as possible and the board should review financial information on a timely basis

Current status NOT RESOLVED The Ambulance Distnct is aware of and has evaluated this issue and concluded that It would not be cost beneficial or possible with the limited resources available to create a segregated accounting environment The Ambulance District will continue to monitor this issue with segregation of duties and continues to review all financial mformation on a tunely basis This findmg is also mcluded m the audit report for the year ended December 31 2008 and descnbed m 2008 1

Section II Internal Control and CompUance Material to the Federal Awards

Not applicable

Section III Management Letter

There were no matters reported m a separate management letter for the year ended December 31 2007

THIS SCHEDULE HAS BEEN PREPARED BY MANAGEMENT

22

^ ^R^ \\^ChVlViH U l h \ Lower Cameron Amhulonce Service District

\ A^ Polish I . L L i ^^- • - ^ - ^ \ \ f ^ - P O H n \ : 4 H C i t o k Louismn i 706J2

f^ , , t - r ( c ^ - " . . T e l 337 542 4926 F a x 337 542 4924 [m^^^^ ;NvC>OimX%^, VlCJt^ , icK^rcimttl rat

• a ^ ^ r m - w » ' i " Miijr-.JU'j«,:.luiiJii'''gcM^a.iMimuai'wiiMiiJuBitt''BBJHTg'BTaL

MANACr! M l M C O K K I C l l M AC HON 11 AN

JiUK 0 2009

I L;,is| l i n t Auditor St Uc o f l ouisnrn I 'O B o \ 9 J j 9 7 l i i to r iRou^t l o i i i s n i n 7()S{)4 9^97

I o u t r Cameron \ in ln i l I I K L Senicc Dist i i t t n,spi.Ltliill\ submits IIIL IO11OV\II1J^ corrunuc iction pi iii lot tht \ i \ \ u i du l Dut-nibt i j l ZOOS

N uiR ind iddiLss ol iiulLpLndirit publit. iLcounlmu lirm

Broubsird I'ocja I tw is & B K u i \ 1 1 i' Ctrt i l icd PublK ALCOuimrus 10! liuicpLiukiiet. I3hd L i l n t t t u 1 ouisi Ul 1 70^06

Audit Period l m u u \ 1 200S t h i o u j i OccLmlKi )1 2008

! ht, rindin-,s from llic 2008 schedule ol liiultnus uid questioned costs iie discussed below Ihe lindinL,s ire numbered consisleiulv with the numbers issiuned in the schedule Section I of the schedule Sii i i inur\ o f Auditor 5 Reports does nol include findin_s uid is nol iddresscd

ScLtinn I I Hin i n i n l Sn tc i i i t n t I indinjis

200S 1 Sc^ieuition ol Duties

Recommend itioii KeepuiL, in mind the Innilcd number ol personnel to which duliLS e ui be issiL,ned the Ambul uicc nislnet should comiiun. lo monitor dssitntiietit ol duties lo assure is nuieli se£,reLUion ol dutiLS uid responsibilit> as possible ind the board should reMcw f in inen i intoninl ion on a timeh basis

Response file Ambul iriee Disincl is iw ue of and e\ ilu lad this p iohLni and concluded ih i l it would no be cost henLtienl or possible with the limited resources n i i l i b l e lo ereate i seutL,ited Kcounlme. en\ironmenl l lowe\er ihe Ambul nice D K U I C I wil l continue to monilor tins issue uid the hoird wi l l rcMcw (ill inei l l in loinnt ion on i l imeK hisis

Responsible pu t ) H\ton Rrouss ird Dircctoi

I OWl R C \ M I RON A M B L L A N C I SI RVIC I D I S I R I C l