towards understanding the structure of islamic economic ... · (muwatta imam malik) ... al-ghazali...

TRANSCRIPT

Journal of Business and Economics, ISSN 2155-7950, USA

April 2013, Volume 4, No. 4, pp. 346-363

Academic Star Publishing Company, 2013

http://www.academicstar.us

346

Towards Understanding the Structure of Islamic Economic System in

Solving the Current Economics and Financial Crisis

Magda Ismail A. Mohsin

(International Center for Education in Islamic Finance INCEIF, the Global University of Islamic Finance, Kuala Lumpur, Malaysia)

Abstract: Islam is not just a religion of worship; it is a comprehensive discipline that includes all aspect of

sciences including economics. It provides many institutions that have to function in parallel in order to meet a just

and a welfare society for all. The current global economics and financial crises urged economists to search for

alternative institutions to solve these crises. This brings in the question of whether the Islamic economic system is

capable of solving such crises or not. The main objective of this paper is to present the different Islamic

institutions within the structure of the Islamic economic system, and to show their roles in handling the current

economics and financial crisis. This research uses both primary and secondary sources. Data collected from

primary sources includes text from the Quran and ahadith from the Sunnah (saying of the Prophet (pbuh), while

data collected from secondary sources includes books, articles, journals besides websites and e-books. The

expected finding of this research is to give a comprehensive structure of the Islamic economic system, as provided

in Quran and Sunnah. This in turn will open the door wider from more researchers to study and to examine the

different institutions within the structure of the Islamic economic system in depth which God/Allah (swt) provided

to serve all mankind in the best way.

Key words: economics; crises; Islamic financial institutions; remedies

JEL code: P4

1. Introduction

The current global economic and financial crises together with the Arab Spring or the Arab Awakening in the

21st century is a good chance for Muslim to revisit the structure of their Islamic economic system not only to

solve their current problems but also to revive the best and the perfect system that the Creator send to serve all

mankind in the best form as mentioned in His Holy Book al-Quran and as come in the following verse.

This day have I Perfected your religion For you, completed My favour upon you, And have chosen for you Islam as your

religion. (Surat al-Maidah 5:3)

And as advised by the Prophet (pbuh) as come in his following hadith:

“…I have left two things behind me for you (the Ummah). You will never go astray as long as you follow these two

things. One of these two things is Allah’s Holy Book and the other is the Sunnah of his Most Beloved Prophet.”

(Muwatta Imam Malik)

The study at hand tries to highlight the role of some of the Islamic institutions from within the structure of the

Magda Ismail Abdel Mohsin, Ph.D., Associate Professor, INCEIF; research areas: Islamic economics and finance. E-mail:

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

347

Islamic economic system, and to provide guidance to how these institutions can assist in solving the current

economics and financial crisis. The main focus of this paper will be limited to three crisis, debt problem, unjust

distribution of wealth and the wide spread of poverty. To achieve this, the paper is divided into four sections,

including the introduction. Section two discusses the literature review; section three develops the blueprints of the

structure of Islamic economic system and section four provides the remedies for three current economics and

financial crises from Islamic perspective, this is followed by the recommendations and conclusion.

2. Literature Review

To come up with a comprehensive structure of the Islamic economics system more references will be

provided from the primary sources Quran and Sunnah, besides the work of early and contemporary Muslim

scholars. From the work of early Muslim scholars we realized that they addressed the economic issues from

different perspectives in response to the needs of their time while holding important government offices, such as

through their writing in tafsir/exegesis, fiqh/Islamic jurisprudence and akhlaq/ethics. For this paper references had

been made to five prominent Muslim scholars, al-Ghazali1, ibn Khaldun

2, al-Shaibani

3, Abu Yusuf

4 and ibn

Taymiyah5. Al-Ghazali in his work Ihya’ Ulum al-Din classified economics as one of the sciences connected with

religion along with metaphysics, ethics, and psychology. One of his main concerns before starting any economic

activity is the behaviour of an individual (i.e. man’s khulq). His ideas on economic activity are numerous such as;

economic achievement is a means to the end, wealth is for a test in this world and a means to success in the eternal

life. His philosophy of life is: the unity of Allah/tawhid, the hereafter/akhirah and the institution of

Prophethood/risalah. His understanding of earning has been encouraged for food; maintain good health, moral

obligations and seeking of knowledge. His idea about money is that it serves as a measure of value and medium of

exchange and as an entity is “sterile”. Furthermore to him trading money with money to generate profit would

result in injustice and is not beneficial to the public interest. On the other hand, Abu Yusuf in his work Kitab

al-Kharaj put a lot of emphasis on the economic responsibilities of the rulers towards providing the basic need

fulfilment of their people besides spreading justice and being equitable in taxation, such as fairness in zakah, ushr,

jiziah and kharaj. Al-Shaibani in his work al- Kasb highlighted the way to earn a decent living through different

ways of distribution of wealth such as through wages, renting, trading though selling agricultural and industrial

products and profit. Ibn Taymiyah in his work al-Hisbah fi al-Islam focused on the society, just and fair price. He

highlighted the importance of the role of the government in regulating and in monitoring the market through the

institution of al-Hisbah for a just and equitable distribution of wealth. Ibn Khaldun in his work al-Muqaddima

noted that growth and development positively stimulate both supply and demand, and that the forces of supply and

demand are the main determinant of the prices of goods and services.

References for contemporary Muslim scholars have been made to four scholars, Chapra, Zubair, Ayub and

1 Abu Hamid Muhammad ibn Muhammad al-Ghazali (451AH-505AH) known as al Ghazali. One of his famous works is known as Ihya’ ulum al-din/ Revival of religious sciences. 2 Abu Zayd Abdu r-Rahman bin Muhmmad bin Khaldun Al-Hadrami known as Ibn Khaldun (732-808 H/1332-1404 AD). He isconsidered as the father of modern economics. One of his famous works is Muqaddimah /Prolegomena/Introduction.3 Muhammad bin al-Hasan al-Shaibani (132AH-189AH), known as al-Shaibani, has many works. The famous one is Kitab al Iktisab

fi’l Rizq al Mustahab/book on earning a decent living. 4 Yaqub ibn Ibrahim al-Ansari, known as Abu Yusuf (113AH-182AH). He was the first jurist to devote a treatise exclusively to economic policy known as Kitab al Kharaj/Book of taxation, which was later followed by a number of similar works by other jurists. 5 Shaykh al-Islam Taqi ud-Din Abu’l-Abbas Ahmad Ibn al-Halim ibn Abd al-Salam Ibn Taymiyah al-Hanbali known as Ibn Taymiyah (661AH-728H) has many works. The famous one is al-Hisbah fi al-Islam/Public duties in Islam.

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

348

Mannan in terms of defining Islamic economics. For example, according to Chapra in his article “Objectives of

the Islamic Order”6 mentioned that:

The Islamic system is unflinchingly dedicated to human brotherhood accompanied by social and economic justice and

equitable distribution of income, and to individual freedom within the context of social welfare.

Moreover7 he added that:

Islam is a universal faith which is simple and easy to understand and rationalize. It is based on three fundamental

principles which are tawhid/unity, khalifah/vicegerent and adalah/justice. These principles not only frame the Islamic world

view, they also constitute the fountain-head of the maqasid and the strategy.

According to Zubair8 he acknowledged the lack of an organisational framework for economic activity at the

present time as he mentioned that:

An organisational framework is needed to conduct the economic activity. The framework is based on some axioms and

fundamental principles having an ideological base. The framework is called an economic system. It is inspired by the world

view of a community.

Ayub9 highlighted the importance of management and wealth distribution in a society as he mentioned that:

An economic system relates to management of wealth distribution in a society that tends to solve economic problems of

various groups by enabling or restricting them from utilizing the means of production and satisfaction.

Mannan10

incorporated both social system and the capitalist system in defining the Islamic concept of society

as he mentioned that:

Islam aims at achieving a social system which is capitalistic in broad outline restricted very largely by socialistic

institutions and ideas. That is, Islamic concept of society is based on five principles. They are Quranic concept of history,

restricted private ownership of the means of production, Universal brotherhood of man, Eternal principle of co-existence and,

Sovereignty of almighty Allah.

Recently western writers wrote criticising the capitalist system. J. K. Gibson- Graham in his book entailed

The End of Capitalism: A Feminist Critique of Political Economy11

mentioned that:

Through a critique of existing conceptions of economy and capitalism, we hoped to make room for new economic

representation ones that would be more friendly and fostering to an innovative and economic politics.

Moreover and recently many you-tube have shown the call to end the capitalism system and to find another

alternatives system that can help overcome those problems. For examples, Occupy Wall Street, End of

Capitalism12

, Capitalism Hits the Fan13

shows the basis for the current financial crisis and while others realized

6 Muhammad Umar Chapra (2005), “Objectives of the Islamic economic order”, in: Sheikh Ghazali, Syed Omar Syed Agil, Aidit Hj. Ghazali (Eds.), An Introduction to Islamic Economics and Finance, CERT Centre for Research and Training, K.L. Malaysia, p. 25. 7 M. Umar Chapra (1992). Islam and the Economic Challenge, Islamic Foundation of the International Institute of Islamic Thought, USA, pp. 201-202. 8 Zubair Hasan, Habibah Lehar, Fundamentals of Microeconomics, pp. 16-20. 9 Ayub Muhammad (2008). Understanding Islamic Finance, Chichester, GBR: Wiley, p. 18, available online at: http://site.ebrary.com/lib/inceif/Doc?id=10233239&ppg=38. 10 M. A. Mannan, Islamic Economics: Theory and Practice — A Comparative Study, p. 56. 11 J. K. Gibson-Graham (1996). The End of Capitalism A Feminist Critique of Political Economy, University of Minnesota, Minneapolis/London. 12 http://www.youtube.com/watch?v=7DQiCwKzKt4. 13 http://www.youtube.com/watch?v=0HTkEBIoxBA.

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

349

the Islamic banking as a way to get out from this financial crisis Islamic Banking System Resists Financial Crisis14

Islamic banks and financial institutions are run according to the principles of shari‘ah law. As a result, they have been

largely protected from the current global financial crisis affecting most banks in the US and Europe. Islamic banks follow

strict ethical guidance on socially responsible investment. They are also prohibited from the buying and selling of debt, risky

market speculation and dealing in interest usury unlike non Islamic banks. The stability that Islamic banks can offer in the

current economic climate positions shari‘ah compliant finance as a viable alternative to the current global economic system

with halal banking set to grow significantly over the next years.

3. Blueprints for the Structure of the Islamic Economic System

Islam provides many institutions that have to function together and in parallel in order to solve the current

economics and financial crises. In this regards, reference can be made to man’s creation. Allah (swt) created man’s

body with different organs each to carry out different functions and different roles in order to form a healthy body.

And if any organ fails to function properly then the whole body will suffer the pain as mentioned by the Prophet

(pbuh) in his following hadith15

:

“Such as the believers in their mutual love, mercy and compassion is like one body if one part complained the whole

body will suffer from fever and pain.”

Similarly, to tackle the current economic and financial crises it is much recommended to revive all Islamic

institutions together and in parallel and to provide their different functions and roles within the structure of the

Islamic economic system for a perfect and a healthy society.

3.1 Islamic Worldview

To have a better understanding of the Islamic economic system it is much recommended to view it within the

context of Islamic worldview. According to Muslim economist, the Islamic worldview is based on three

fundamental concepts which are oneness and unity of God/tawhid, vicegerent/khalifah of human beings and

justice/‘adalah.16

The realization of the Islamic worldview within the Islamic economic system depends on its

integrated principles and values within individuals, institutions, market regualtion and the state which forms the

entire structure of the Islamic economic system as explained below:

3.1.1 Man and His Economic Nature

To understand the economic nature of man as an individual or as a man/khalifah having responsibilities in

this world, let us first know why Allah (swt) created man in the first place. Man has been created for two purposes,

for worshipping Allah (swt) and for developing this earth/i’mar al-ard as mentioned in these Quranic verses:

I have only created Jinns and men, that They may serve Me, (Surat al-Zariyat 51:56)

…It is He Who hath produced you From the earth and settled you Therein…(Surat Hud 11:61)

The immediate question that will follow is; how man can achieve both worshiping his Creator and at the

same time be engaged in the process of economic activities? According to Islam, Allah (swt) guides man

throughout his whole life for achieving success/falah in this world and achieving true happiness/sa’addah

14 http://www.youtube.com/watch?v=D3Trfc5FqYs&feature=relmfu. 15 Sahih al-Jam’I, Narrated by al-Nu’uman ibn Bashir al-Muhadith No. 5849. 16 M. Umar Chapra (1992). Islam and the Economic Challenge, Islamic Foundation of the International Institute of Islamic Thought, USA, p. 201. See also Syed Muhammad al Naquib bin Ali al-Attas (1995), Prolegomena to the Metaphysics of Islam: An Exposition

of the Fundamental Elements of the Worldview of Islam, Kuala Lumpur: International Institute of Islamic Thought and Civilization (ISTAC).

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

350

haqiqiyyah17

in the hereafter. As such, engaging in any economic activity in this world, man must follow the

command of His Creator as highlighted in His last Holy Book, al Quran, and as practiced by His last Messenger,

and which is also a type of worshipping. To explain further, Allah (swt) created man in the best form/ahsan taquim

as mentioned in al Quran (95:4), and bestowed him with mind/‘aql and free will, which is constraint by

responsibility. Hence, man is held accountable for all his deeds including his economic activities. According to the

teaching of Islam man will be held accountable in the next world on three main things; On his time how he spend

it, on his wealth how he acquires it and how he spend it.

Following the above teaching man has to struggle in this world in gaining and distributing his wealth

according to the following Quranic verse;

Verily We have created man into toil and struggle. (Surrat al-Balad 90:4)

3.2 Development of Man in Islam

Since man has been created in the best form with mind and free will which is constraint by responsibility as

mentioned above, Islam first mission is to develop man and equip him with all the Islamic principles and values in

order to succeed in handling his responsibilities towards himself and towards his society.

Figure 1 Institutions within the Islamic Economic System18

As such seeking knowledge is the key principles in starting any economic activity in this world and ever

since it has been highlighted in the first revelation as mentioned in the following Quranic verse:

17 For further knowledge please refer to Syed Muhammad al Naquib bin Ali al-Attas (1993) The Meaning and Experience of

Happiness in Islam (Kuala Lumpur: International Institute of Islamic Thought and Civilization (ISTAC). 18

Magda Ismail, Re-Looking at the Structure of Islamic Economic System: Crystal Clear a Just System for All, paper presented at

the Academic Seminar in INCEIF on 28th March 2012.

Self-Monitoring and State Monitoring

Distribution of Wealth How Man acquires his wealth?

Re-Distribution of Wealth

Human Development

(Knowledge + Ethics)

Economic activity/ I’mar al-Ard

Needs Fulfillment

How Man spends his wealth?

E

T

H

I

C

S

K

N

O

W

L

E

D

E

G

E

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

351

Proclaim! (or Read!) In the name Of thy Lord and Cherisher, Who created… (Surat Al-’Alaq 96:1)

This is followed with perfecting ones’ ethics/khuluq according to the ethics of the Prophet (pbuh) as

mentioned in the following Quranic verse:

And thou (standest) On an exalted standard of character (Surat al-Qalam 68:4)

The Prophet (pbuh) also mentioned that he (pbuh) has been send to perfect the ethics of the people19

:

“I have been sent for the purpose of perfecting good morals.”

Following the question of how man can achieve both worshiping his Creator and at the same time be engaged

in the process of economic activities? These will help to provide the blueprints of the structure of the Islamic

economic system starting with a knowledgeable and an ethical man knowing his responsibilities towards himself

and towards his society at large. Hence, these two concepts will form the two pillars of the structure of Islamic

economic system as shown in Figure 1 above.

3.3 Self-monitoring and state Monitoring

As realized in Figure 1 above, the whole process of developing this world must be handled with knowledge

and must be accomplished with ethics according to the teaching of Islam. Having said that, two types of

monitoring is required, self-monitoring and state monitoring.

Self-Monitoring is a state when man is of full conscious of his ethical behaviour throughout his whole life.

i.e., practising Ihsan throughout his whole life. This means that man has to be conscious by strictly following the

Islamic teachings while being engaged in any daily activity. This include all economic activities such as being

involve in trade and business, lending through al-qard al-Hassan, financing the different sectors, paying the

compulsory due or contributing voluntary in developing their societies. In this case self-monitoring can act as a

reminder to remind man as if he can see His Creator and if being unable to see His Creator, he must remember

that His Creator nevertheless sees him as mentioned in the following hadith20

:

“It is to worship Allah as though you see, were not you see Allah sees you”

For state monitoring, we have to remember that development in Islam is the responsibly of every single

individual, since man will be accountable for his time how he utilized it and his wealth how he acquired it and

how spent it. As such the role of the Islamic state is minimized to ensure that every single individual is achieving

his responsibilities. As such the role of the Islamic state is minimized to; ensure the internal and external security

of the country, provide law and order in the market place, facilitate the process of economic development through

the private and the voluntary sector, ensure the provision of the basic needs to all, eradicate poverty, besides close

monitoring the whole market through the institution of al-hisbah of enjoining what is right whenever people start

to neglect it, and forbidding what is wrong whenever people start to engage in it as mentioned in following

Quranic verse:

Let there arise out of you A band of people Inviting to all that is good, Enjoining what is right, And forbidding what is

wrong: They are the ones To attain felicity (Surat al-i-’Imran 3:104).

Hence providing the full guidance for man to handle the process of development according to the teaching of

19 Al-Albani, Narrated by Abu-Hurrairah, No. 45. 20 Sahih al-Bukhari. Narrated by abu-Hurrairah.

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

352

Islam and allowing him to handle his responsibly towards success in this life and true happiness in the hereafter

Man will be motivated to work harder and will spend time and effort to be creative enough in handling this

process in the best way not only for his benefit for the benefit of the whole society.

3.4 Man and His Economic Responsibilities towards I’Mar al-Ard

In Islam, man is the vicegerent/khalifah of Allah (swt) on earth and all resources which are at his disposal are

trust/amanah, he must utilise them according to the will of the Creator as he has been held accountable for any

misuse of these resources. Therefore, these resources are means to attain man’s life in this world and if used

according to the teachings of Islam, a healthy society will be realized in this world and successful gains will be

achieved for man in the hereafter.

For the smooth running of this process, as mentioned above, every individual has to be engaged in the

process of economic activity to gain his lawful means on one hand and to meet his responsibilities towards his

society’s need on the other. To begin with, Islam recognised the need for finance as a function for economic

development. Hence, considering the fact that interest/riba is prohibited in Islam, Islam provides two financial

institutions in order to start any development project that can flourish the economy on one hand and gaining

individual’s wealth on the other. These institutions are the private enterprise and the alternative financial

institutions to riba which will help man to acquire his wealth through lawful means and to re-distribute it

according to the teaching of Islam as seen in Figure 2.

3.5 Distribution of Wealth in Islam

Since man will be answerable during the Day of Judgment on how he acquires his wealth, he should practice

ihsan while earnings a living throughout the whole process of economic activity. Being acquainted with the

knowledge and with all the ethical norms, in accordance to the teachings of Islam, both the owner of the capital

and the entrepreneur know their responsibilities towards developing their society either through the private

enterprise or through the alternative financial institutions to riba which can be explained as follows:

(1) Private Enterprise Institution

Any individual who owns the capital can be engaged in the process of economic development through running

his own lawful business, such as opening his own business, company, grocery store, bakery, barber shop, restaurant,

school and hospital et cetera. In this case, the owner of the capital alone will gain profit or he alone will face the

risk of any loss.21

In this way it is realized that the owner of the capital meets his responsibility towards his society

by providing the lawful goods and services needed by the majority of people on one hand and on the other he

acquires his lawful wealth.

(2) Alternative Institutions to RIBA

In case capital is needed to undertake business activity in the marketplace, both the owner of the capital and the

entrepreneur should undertake their lawful business through any of the four alternative institutions to riba which are:

(a) Institution of Trade and Business

Since the issue of riba and self-interest maximization is not allowed in Islam, Islam provides trade as an

alternative mode of finance to handle the business activities as mentioned in the following Quranic verse:

…Allah hath permitted trade and forbidden usury… (Surat al-Baqarah 2: 276)

21 Muhammad Akram Khan (2005). “Types of business organization in an Islamic economy”, in: Sheikh Ghazali, Syed Omar Syed Agil, Aidit Hj. Ghazali (Eds.), An Introduction to Islamic Economics and Finance, CERT Centre for Research and Training, K. L. Malaysia, p. 269.

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

353

Distribution of Wealth

Figure 2 Distribution of Wealth in Islam22

Hence trade as a financial institution can be divided into four modes of finance such as Musharakah,

Mudarabah, Murabahah and Ijarah in which risk will be spread between the owner(s) of the capital and the

entrepreneur(s). At the present time these modes of finance shows successful cases through Islamic banking system.

Partnership/Profit and Loss Sharing/Musharakah

This mode of finance is meant for two or more partners who are not capable of doing the business

singlehandedly23

, either due lack of capital or lack of knowledge and skills to do the business. Hence, in this case

each party will provide part of the capital, for instance money and machineries to undertake lawful business. In

case the business succeeds, both parties will share the profit according to their agreed ratio. In case of any loss,

they will share this loss in proportion to the amount of capital invested.

Mudarabah/Profit Sharing Principle

This mode of finance is meant for two or more partners in such a way one or more partners supply the capital

22

Magda Ismail, Re-Looking at the Structure of Islamic Economic System: Crystal Clear a Just System for All, paper presented at

the Academic Seminar in INCEIF on 28th March 2012. 23 Muhammad Akram Khan (2005). “Types of business organization in an Islamic economy”, in: Sheikh Ghazali, Syed Omar Syed Agil, Aidit Hj. Ghazali (Eds.), An Introduction to Islamic Economics and Finance, CERT Centre for Research and Training, K. L. Malaysia, p. 270.

Agriculture Sector Industrial Sector Infrastructure Sector Service Sector

Financial Institutions 1. Private enterprise institution 2. Alternative institutions to riba

a. Trade & business (commercial activities) b. Compulsory institutions c. Voluntary institutions d. Free-interest institution (Al-qard hassan)

Income and wealth acquired - Rent- Wages, Salaries - Profit, Dividends, et cetera.

Spending on Man’s need Compulsory and Voluntary spending

Re-Distribution of Wealth (How does Man spend his wealth?)

Distribution of Wealth (How does Man acquire his wealth?)

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

354

and the other run the business on his or their behalf at an agreed rate of profit. Profits will be shared between the

owner of capital and the entrepreneur on the basis of a contractual agreement whereas losses under normal

circumstances would be written on capital in terms of cash and entrepreneur in terms of kinds24

.

Murabahah/Mark-up Principle

This mode of finance is more for financing someone who wants to buy any asset but he cannot afford to pay

immediately. Under this financial mode there are many forms of Permissible Deferred Sales such as, Salam sale,

Mua’jjal sale, Istisna’ sale, Ijarah, Musharakah Mutanaqisah.

(b) Compulsory Institution/Zakah Institution

This is another alternative institution to riba in which Allah (swt) mentioned in the following Quranic verse:

“And that which you give in gift (to others), in other that it may increase (your wealth by expecting to get a better one in

return) from other people’s property, has no increase with Allah; but that which you give in Zakat seeking Allah’s

Countenance, then those they shall have manifold increase.” (Surat al-Rum, 30:39)

Hence, zakah is another financial institution that helps to eliminate riba from Muslim society through

providing cash to support eight categories of people whom usually will be force to borrow with riba to meet the

urgent needs.

(c) Voluntary Institutions (Takaful, Waqf & Sadaqah)

Voluntary institutions are also another alternative institution to riba as mentioned in in the following Quranic

verse:

Allah will deprive usury of all blessing, but will give increase for deeds of charity… (Surat al-Baqarah 2:276)

These voluntary financial institutions include waqf, takaful and sadaqah which are financial institutions

meant to provide many goods and services to the society without burdening the government or resorting to

borrowing with interest.

(d) Interest-Free Institution/Benevolent loan/al-Qard al-Hassan

Al-qard al-hassan is a loan without interest, i.e. debtors of this kind of loan are only required to repay the

amount borrowed. This is the only lending institution which is allowed in Islam in order to assist one’s brother to

find a living. Since it is more to help others who are in crucial needs, the lender must not expect any return but

seeks multiple rewards from His Creator as mentioned in the following Quranic verse:

Who is he that will loan to God A beautiful loan, which God Will double unto his credit And multiply many times? (Surat

al-Baqarah 2:245).

3.5 Re-distribution of Wealth

Once man acquires his wealth as explained in the above mentioned process in terms of rent, wage, salary

profit and dividends, he will be answerable during the Day of Judgment on how he spends this wealth. As such,

man must spend his wealth according to the teachings of Islam through two ways, spending on the hierarchy of

Muslims’ needs and spending on compulsory and voluntary basis which is known as redistribution of wealth.

(1) Hierarchy of Muslim’s Need

Islam recognises that man has certain needs to be fulfilled in this world, some of which are more important

24 Muhammad Akram Khan (2005). “Types of business organization in an Islamic economy”, in: Sheikh Ghazali, Syed Omar Syed Agil, Aidit Hj. Ghazali (Eds.), An Introduction to Islamic Economics and Finance, CERT Centre for Research and Training, K.L. Malaysia, p. 275.

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

355

and others are less important25

. Muslim scholars classified these needs into three hierarchies of needs which are:

Necessities/Daruriyyat: These are the needs that protect man’s physical existence/al-nafs, the provision of

things like food, clothing and shelter; protection of din/ religion; protection of mind/al-’aql, protection of progeny/

al-nasl or pedigree, and property/al-mal.

Conveniences/Hajiyyat: This includes things that improve on the quality of life and remove bearable

hardship and difficulties.

Beautification /Luxury/Tahsiniyyat: This adds beauty and elegance to life without transgressing the limits of

moderation as defined by the Shari‘ah.

Figure 3 Hierarchy of Muslim’s Need

Before man start spending on conveniences and luxury or beautification, he must contribute to his society

through re-distribution of wealth as mentioned in the following Quranic verse:

And those in whose wealth is a recognised right. For the (needy) who asks and him who is prevented (for some reason

from asking) (Surat al-Marij 70:24-25)

(2) Compulsory and Voluntary Spending of Wealth in Islam

As mentioned above and after satisfying man’s need, part of his acquired wealth must be redistributed

through compulsory and voluntary spending in order to ensure a just and equitable distribution of wealth. This is

done through compulsory and voluntary institutions and if implemented according to the teachings of Islam can

circulate the wealth from the rich to the poor in a harmonise manner, thus a just and a more stable economic

system will be realized.

(a) Compulsory institutions

Regarding compulsory institutions, both Muslims and non-Muslims who are living in an Islamic country,

have to fulfil their responsibility towards their society by paying their compulsory dues to the state to fulfil certain

duties in the country through the following;

Zakah Institution

Zakah is the third pillar of Islam and it is compulsory upon all Muslims to give part of their wealth and assets

(namely livestock, gold, silver, currency, jewellery, commercial assets, agriculture, honey and animal products,

mining and fishing, rented buildings, plants, and fixed capital26

) once it reaches the minimum assigned/ al-nisab

on annual basis or once harvested to the state as mentioned in following Quranic verse:

Of their goods (wealth), take alms, that so thou mightest purify and sanctify them; and pray on their behalf. Verily thy

prayers are a source of security for them: And Allah is One Who heareth and knoweth. (Surah Al-Taubah 9:103)

25 Chapra 1992. Islam and the Economic Challenge, Islamic foundation of the International Institute of Islamic thought, USA, p. 210.26 Ibid, Vol. I, p. 52.

Hierarchy of Muslim’s Need

Daruriyyat (Necessities) Hajiyyat (Conveniences)Tahsiniyyat

(Luxury/Beautification)

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

356

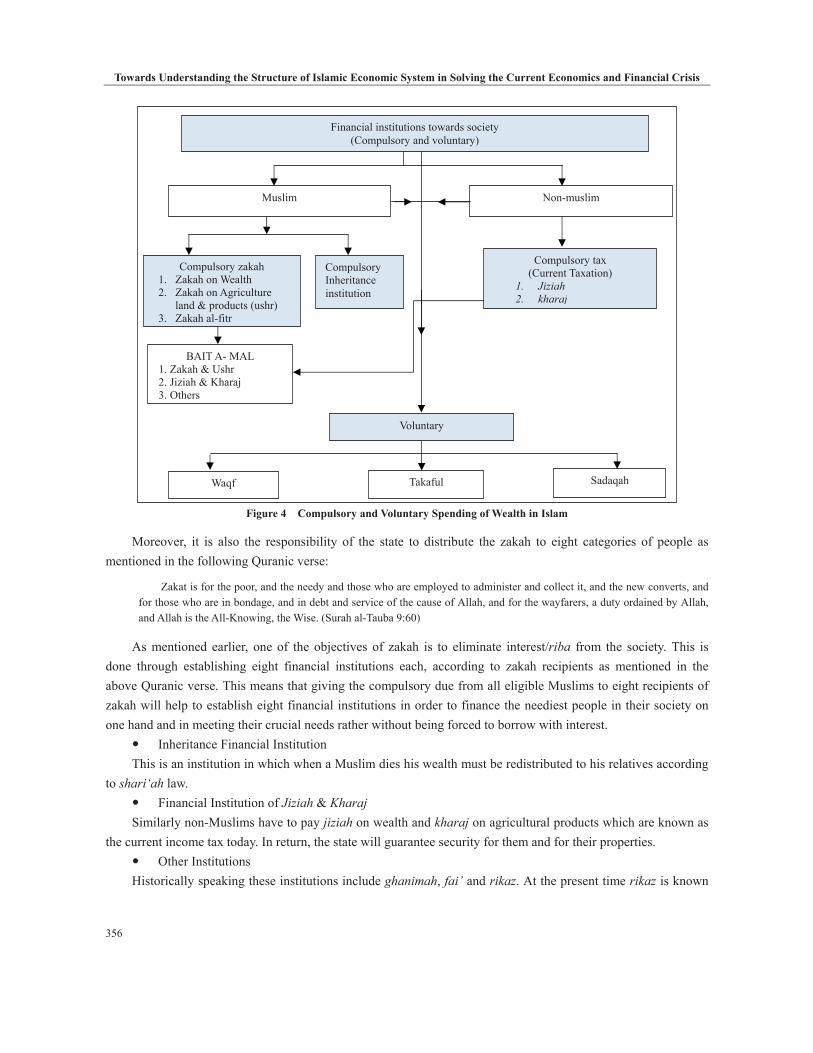

Figure 4 Compulsory and Voluntary Spending of Wealth in Islam

Moreover, it is also the responsibility of the state to distribute the zakah to eight categories of people as

mentioned in the following Quranic verse:

Zakat is for the poor, and the needy and those who are employed to administer and collect it, and the new converts, and

for those who are in bondage, and in debt and service of the cause of Allah, and for the wayfarers, a duty ordained by Allah,

and Allah is the All-Knowing, the Wise. (Surah al-Tauba 9:60)

As mentioned earlier, one of the objectives of zakah is to eliminate interest/riba from the society. This is

done through establishing eight financial institutions each, according to zakah recipients as mentioned in the

above Quranic verse. This means that giving the compulsory due from all eligible Muslims to eight recipients of

zakah will help to establish eight financial institutions in order to finance the neediest people in their society on

one hand and in meeting their crucial needs rather without being forced to borrow with interest.

Inheritance Financial Institution

This is an institution in which when a Muslim dies his wealth must be redistributed to his relatives according

to shari‘ah law.

Financial Institution of Jiziah & Kharaj

Similarly non-Muslims have to pay jiziah on wealth and kharaj on agricultural products which are known as

the current income tax today. In return, the state will guarantee security for them and for their properties.

Other Institutions

Historically speaking these institutions include ghanimah, fai’ and rikaz. At the present time rikaz is known

Financial institutions towards society

(Compulsory and voluntary)

Muslim Non-muslim

Compulsory zakah 1. Zakah on Wealth 2. Zakah on Agriculture

land & products (ushr) 3. Zakah al-fitr

Compulsory tax (Current Taxation)

1. Jiziah

2. kharaj

Voluntary

Waqf Takaful Sadaqah

BAIT A- MAL 1. Zakah & Ushr 2. Jiziah & Kharaj 3. Others

Compulsory Inheritance

institution

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

357

as any hidden natural resources such as oil, gold and silver and all types of minerals hidden on earth.

In summary, revenue generated from compulsory dues, namely from zakah, jiziah and kharaj, et cetera are

income for the state to be placed in State Treasury/Bait al-Mal in order to assist the state in fulfilling its

responsibilities in securing the country, alleviating poverty and in close monitoring the process of economic

development/ i’mar al ard for an equitable distribution of wealth.

(b) Voluntary Financial Institutions

Similarly both Muslims and non-Muslims have to fulfil their responsibilities in contributing voluntarily to

their society through voluntary institutions such as the institution of sadaqah, takaful, and waqf.

Sadaqah Financial Institution

This is a voluntary act of giving alms for the cause of Allah/fisabillilah by individuals who want to contribute

more than the compulsory due. This is a type of a hidden sadaqah which can be given either in cash or in kind to

needy relatives, needy friends or needy neighbours in situation where they face crucial need. The main objective

of this hidden sadaqh is to prevent these people from borrowing with interest when they are in crucial needs.

Takaful Financial Institution

Takaful is another voluntary institution for financial assistance and a kind of protection based upon the

principles of mutual cooperation/ ta’awun,. In this case, a group of people can be formed and any needy

participant within that group is eligible to receive financial assistance in case of need. The main objective of this

institution is also to finance one’s brother in a serious situation rather than letting him borrow with interest to

solve his critical needs.

Waqf Institution

Waqf is another voluntary institution which is much recommended in Islam as mentioned in the following

Quranic verse:

By no means shall ye Attain righteousness unless Ye give (freely) of that Which ye love (Surah Al-i-Imran 3:92)

This institution finances perpetual goods and services needed in every society such as education, healthcare,

national security, different kinds of agricultural and industrial products, transportation facilities and basic

infrastructure without any cost to the government. Furthermore, it will provide continuous rewards to its founder

as mentioned by the Prophet (pbuh) in his following hadith27

:

“The Prophet (s) said: When a man dies his acts come to an end, except three things, recurring charity, knowledge (by

which people benefit), and pious offspring, who pray for him”

The beauty of this institution is that once a property is created as waqf it becomes perpetual, explicitly it must

not be sold or inherited or given away as a gift. This will ensure the continual benefits provided by this institution

within the society for many generations to come without burdening the government or resorting to borrowing with

interest to provide these goods and services.

4. Remedies for the Current Economics and Financial Crises: Islamic Perspective

As realized above, the Islamic economic system provides many institutions that have to function together and

in parallel for an equitable distribution of wealth and a just society. Hence in this section three cases on the current

economics and financial crises will be presented, (the issue of borrowing with interest/riba which led to the

27 Sahih Muslim, narrated by Abu-Hurraira, No. 1631.

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

358

current financial crisis, the unjust distribution of wealth and the wide spread of poverty, and the unwise global

spending), and the remedies from Islamic perspective.

4.1 Borrowing with Interest/Riba & the Current Financial Crisis

At the present time and with the current economic situation, individuals will be forced to borrow from

conventional banks with interest in order to own their basis needs in terms of shelter, the means of transport and

even getting quality education. On the other hand we realized that governments in the different countries are also

forced to borrow with interest for the sake of financing big projects and developing their societies.

With regard to borrow with interest for the sake of development, governments in countries poor realized after

years, that they were fostering persistence poverty in their countries and for generations to come. For example in

2010 the external debt of Pakistan reach $57.2 billion, Indonesia $196 billion, Bangladesh $24.4 billion, Sudan

$38 billion, Egypt $30.6 billion and Nigeria $44 billion. According to Obasanjo the Ex-President of Nigeria and

during the G8 regarding the external borrowing for the sake of developing his country said that:

“All that we had borrowed up to 1985 or 1986 was around $5 billion and we have paid about $16 billion yet we are still

being told that we owe about $28 billion. That $28 billion came about because of the injustice in the foreign creditors’ interest

rates. If you ask me what is the worst thing in the world, I will say it is compound interest.”28

This financial crisis does not only affect the poor countries alone but it affected the developed countries too.

For example the recent financial crises of 2007-2008, affected USA, UK, Canada, Japan, France, Italy, France,

China, Russia, Brazil and India badly in which their total debt reached $40.839 trillion in 2012 and which will be

reflected on their coming generations.

Table 1 Total Debt $40.839 Trillion-2012

Russia $Billion

Canada$Billion

China$Billion

India$Billion

Brazil $Billion

UK $Billion

France $Billion

Italy$Billion

Germany $Billion

Japan$Billion

USA $Billion

Interest 9 14 41 39 31 67 54 72 45 117 212

Repayment 13 221 121 57 169 165 367 438 285 3000 2783

Standing Debt

23 298 907 1115 873 1379 1772 2000 2304 9324 12532

Total Debt Trillion

45 533 1069 1211 1073 1611 2193 2500 2634 12441 15527

Source: Adopted from: http://demonocracy.info/infographics/usa/world_debt/world_debt.html.

In this case one may ask how the Islamic approach can solve this financial crisis. The teaching of Islam

shows that Islam provides guidance in preventing such crisis before it start. As mentioned above, Islam equips

man with the knowledge from the Quran and Sunnah and provides the principles for good ethics in handling

development. Hence through self-monitoring, man knows that it is his responsibility to develop this world and to

be engaged in the process of economic activities according to the principles of Islam. In this case man will be

responsible in developing his society and at the same time he will be carful in gaining his lawful wealth. This

development can either be through the private enterprise institution, or through any of alternative institutions to

riba. In this case through any means of trade man can buy his own house, do his business, get the means of

transport through, for example, the Islamic banks rather than borrowing with interest. In addition through close

monitoring from the state of enjoining what is right whenever people start to neglect it, and forbidding what is

28 http://www.youtube.com/watch?v=SaeRum-GJMY.

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

359

wrong whenever people start to engage in it, will stop borrowing with interest and will engaging all citizens in the

process of development through the alternative institutions to interest/riba. Subsequently this will prevent the

government from borrowing with interest for the sake of developing the country since the process of development

will be handled by well-educated and well behaved people each knows his responsibilities towards developing his

society according to the teaching of Islam.

4.2 Unjust Distribution

In 2008 the World Bank Development statistics29

shows the unjust distribution of wealth as shown in the

following chart in which the share of the world’s private consumptions is divided as follows; 76.6% of the total

wealth of the world consumed by 20% of the world’s richest population, while 21.9% of its wealth consumed by

60% of the world’s middle class population and only 1.5% of its wealth consumed by 20% world’s poorest.

Figure 5 Unjust Distribution of Wealth Around the World

Adopted from the World Bank Development Indicator 2008.

Website: http://www.globalissues.org/article/26/poverty-facts-and-stats.

This can further be explained through the following Table 2.

Table 2 Global Priorities in Spending

Global Priority $ Billions

Military spending in the world 780

Narcotics drugs in the world 400

Alcoholic drinks in Europe 105

Cigarettes in Europe 50

Business entertainment in Japan 35

Pet foods in Europe and the United States 17

Basic health and nutrition 13

Perfumes in Europe and the United States 12

Reproductive health for all women 12

Ice cream in Europe 11

Water and sanitation for all 9

Cosmetics in the United States 8

Basic education for all 6

1458.00

Source: Adopted from the World Bank Development Indicator 2008.

Website: http://www.globalissues.org/article/26/poverty-facts-and-stats.

29 World Bank Development Indicator 2008, available online at: http://www.globalissues.org/article/26/poverty-facts-and-stats.

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

360

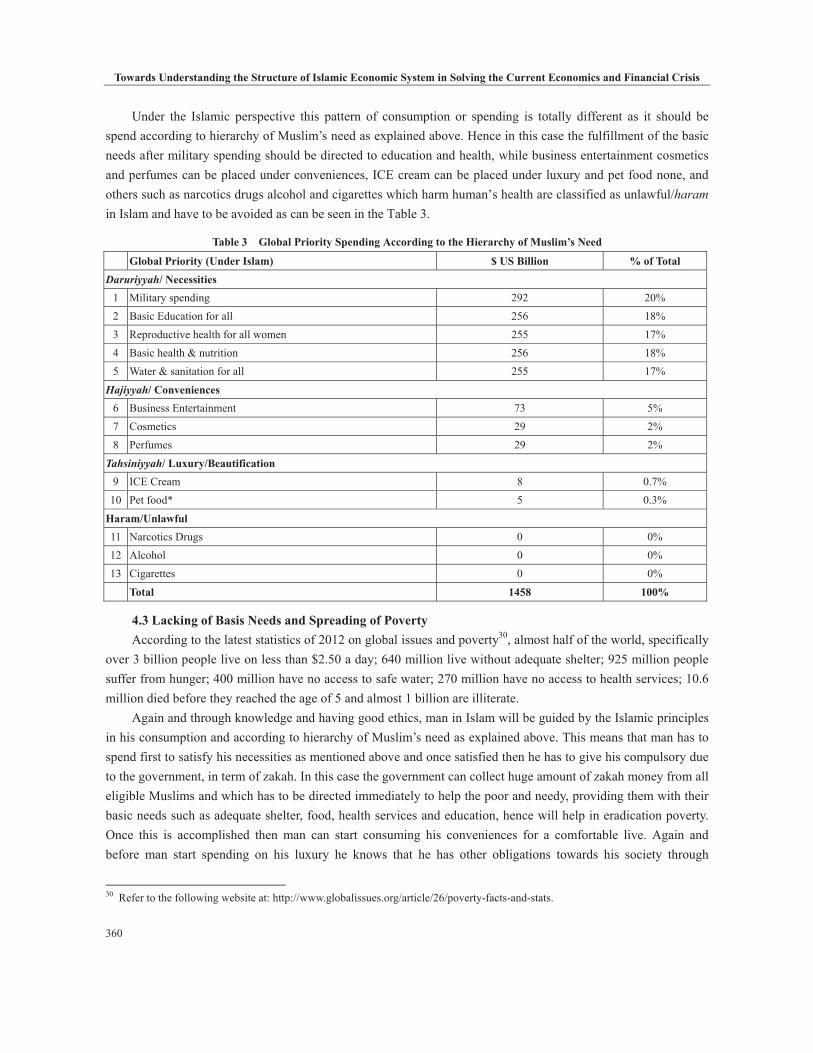

Under the Islamic perspective this pattern of consumption or spending is totally different as it should be

spend according to hierarchy of Muslim’s need as explained above. Hence in this case the fulfillment of the basic

needs after military spending should be directed to education and health, while business entertainment cosmetics

and perfumes can be placed under conveniences, ICE cream can be placed under luxury and pet food none, and

others such as narcotics drugs alcohol and cigarettes which harm human’s health are classified as unlawful/haram

in Islam and have to be avoided as can be seen in the Table 3.

Table 3 Global Priority Spending According to the Hierarchy of Muslim’s Need

Global Priority (Under Islam) $ US Billion % of Total

Daruriyyah/ Necessities

1 Military spending 292 20%

2 Basic Education for all 256 18%

3 Reproductive health for all women 255 17%

4 Basic health & nutrition 256 18%

5 Water & sanitation for all 255 17%

Hajiyyah/ Conveniences

6 Business Entertainment 73 5%

7 Cosmetics 29 2%

8 Perfumes 29 2%

Tahsiniyyah/ Luxury/Beautification

9 ICE Cream 8 0.7%

10 Pet food* 5 0.3%

Haram/Unlawful

11 Narcotics Drugs 0 0%

12 Alcohol 0 0%

13 Cigarettes 0 0%

Total 1458 100%

4.3 Lacking of Basis Needs and Spreading of Poverty

According to the latest statistics of 2012 on global issues and poverty30

, almost half of the world, specifically

over 3 billion people live on less than $2.50 a day; 640 million live without adequate shelter; 925 million people

suffer from hunger; 400 million have no access to safe water; 270 million have no access to health services; 10.6

million died before they reached the age of 5 and almost 1 billion are illiterate.

Again and through knowledge and having good ethics, man in Islam will be guided by the Islamic principles

in his consumption and according to hierarchy of Muslim’s need as explained above. This means that man has to

spend first to satisfy his necessities as mentioned above and once satisfied then he has to give his compulsory due

to the government, in term of zakah. In this case the government can collect huge amount of zakah money from all

eligible Muslims and which has to be directed immediately to help the poor and needy, providing them with their

basic needs such as adequate shelter, food, health services and education, hence will help in eradication poverty.

Once this is accomplished then man can start consuming his conveniences for a comfortable live. Again and

before man start spending on his luxury he knows that he has other obligations towards his society through

30 Refer to the following website at: http://www.globalissues.org/article/26/poverty-facts-and-stats.

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

361

voluntary spending such as, assisting and helping friends and close relative through giving sadaqah, mutual

cooperation through takaful and providing different goods and services at large through waqf such as good health

care, good education, basic infrastructures, agricultural and industrial products. Hence, following the concept of

the hierarch of Muslim’s need in consumption will help in circulating the wealth from the rich to the poor in an

equitable distribution of wealth and in a just way and hence will prevent the concentration of the wealth at the

hands of minority as realized above.

One may asked how much fund can be collected from the re-distribution of wealth within a society compared

to the external borrowing. A recent study conducted by the author shows the following amount of zakah and cash

waqf can be collected31

.

If we assumed Muslim population in a country (X) is 23 million, our assumption in this case is that; out of

this 23 million, 3 million are rich people, 10 million are middle class people and the rest of the population are

unproductive members in the society (young, poor and old age). In the following two cases we tried to show how

much funds can be collected from zakah and cash waqf and which can replace the eternal borrowing.

(1) Zakah Collection

If the zakah of rich people is $1000/year and the middle class people is $100/year then the accumulated

amount of zakah funds will be $ 1billion/year (one billion US dollars).

Rich people 3 million x $1000 = $3.00 billion

Middle class people 10 million x $100 = $1.00 billion

Total $4.00 billion

(2) Cash Waqf Collection

If the same rich people can donate $500/month as cash waqf, and the middle class people can give

$100/month as cash waqf and as to fulfill their responsibilities towards their soceity, the accumulated cash waqf

funds will be $30 billion (thirty billion US dollars) per year.

Rich people 3 million x $500 x 12 mth. = $18.00 billion

Middle class people 10 million x $100 x 12 mth = $12.00 billion

Total $30.00 billion

Hence, a total of $4 billion/year can be collected as zakah to alleviate poverty and $30 billion as cash waqf to

provide the different services needed in their countries. Following the same two cases let us find how much funds

from zakah and cash waqf can be collected within nine listed countries below.

If we assume the compulsory due of rich people in those countries is $1000/yr and the middle class people is

$500/yr then the total collected zakah funds in the follow countries will be, Pakistan $42.5 billion, Indonesia $50

billion, Bangladesh $40 billion, Sudan $16 billion, Algeria $15.5 billion, Egypt $30 billion, Nigeria $47 billion,

Turkey $22 billion and Malaysia $10 billion, collected within one year only, an amount which can eradicate total

poverty from this countries within few years.

If we assume the voluntary contribution of rich people in those countries is $100/mth and the middle class

people is $50/mth then the total collected cash waqf funds in the follow countries will be, Pakistan $51 billion,

31 Utilization of Zakah and Waqf as Community Empowerment for Economic Transformation of Muslim Societies, paper presented at the Life-3 INSANIAH International conference Islamic finance and economic, organized by INSANIAH & IRTI, Langhawi, 28-31 October.

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

362

Indonesia $96 billion, Bangladesh $48 billion, Sudan $19.2 billion, Algeria $ 18.6 billion, Egypt $36 billion,

Nigeria $56.4 billion, Turkey $26.4 billion and Malaysia $12 billion, collected within one year only, an amount

which can provide the different goods and services needed in their societies rather than forcing the government to

borrow with riba to provide them as seen in the table below.

Table 4 The Total Collection of Zakah and Cash WAQF per Year

Country Population In 2009

Million

People who live below poverty

%

External Debt*With Riba

$Billion

Rich Muslim Population (Assumption) Z = $1000/yr CW = $100/mthMillion

Mid. Class MuslimWorkingPopulation (Assumption) Z = $500/yr CW = $50/mth Million

Zakah / year

Rich+Mid

$Billion/yr

Cash Waqf/yr

Rich+Mid

$Billion/yr

Pakistan 175 24 57.2 15 55 42.5 51

Indonesia 245 18 196 30 100 50 96

Bangladesh 150 45 24.4 10 60 40 48

Sudan 42 40 38 10 12 16 19.2

Algeria 36 23 4.1 8 15 15.5 18.6

Egypt 82 20 30.6 10 40 30 36

Nigeria 151 70 44 12 70 47 56.4

Turkey 77 20 313 7 30 22 26.4

Malaysia 29 2.3 72 5 10 10 12

5. Conclusion & Recommendations

As realized above the structure of the Islamic economic system provides many institutions that can work

together for a perfect and a just system which deals with all aspects of values starting from developing man as an

individual/khalifa with good ethics and preparing him to handle the process of development according to the

guidance given by His Creator in achieving his responsibilities towards himself and towards a just and equitable

society which will reflect his Happiness in the hereafter.

Some recommendations which can be deduced from this study are as follows:

Integrating all Islamic principles and values within the economic system.

Reviving the role of al-hisbah institution in order to monitor the whole process of economic activities and

development through enjoining what is right whenever people start to neglect it, and forbidding what is wrong

whenever people start to engage in it.

Educating the mass about lawful earnings through injecting the money in trade and business and not through

lending with interest/riba.

Educating the mass on a balance consumption that will not harm the future generation.

Reviving the role of compulsory institutions and activate the eight roles of zakah within Muslim society.

Reviving the role of voluntary institutions and activate their roles in providing the different goods and

services needed in the different societies.

Reviving all Islamic financial institutions, which had been neglected for so long, study them carefully and

find ways and means how to put them in practice today for the benefit of all mankind.

To conclude, Islam provides many economic and financial institutions within the structure of Islamic economic

system which need to be studied in detail in order to avoid the current economic and financial crises in the future.

Towards Understanding the Structure of Islamic Economic System in Solving the Current Economics and Financial Crisis

363

References:

Abdel Mohsin Magda (2011). “Utilization of Zakah and Waqf as community empowerment for economic transformation of Muslim

societies”, in: the Life-3 INSANIAH International Conference Islamic Finance and Economic, organized by INSANIAH & IRTI,

Langhawi, 28-31 October 2011.

Ayub Muhammad (2008). Understanding Islamic Finance, Chichester, GBR: Wiley, available online at:

http://site.ebrary.com/lib/inceif/Doc?id=10233239&ppg=38.

J. K. Gibson-Graham (1996). The End of Capitalism A Feminist Critique of Political Economy, University of Minnesota,

Minneapolis/London.

M. A. Mannan (1983). Islamic Economics: Theory and Practice, SH. Muhammad Ashraf New Anarkai, Labore-7 Pak.

Muhammad Umar Chapra (2005). “Objectives of the Islamic economic order”, in Sheikh Ghazali, Syed Omar Syed Agil, Aidit Hj.

Ghazali (Eds.), An Introduction to Islamic Economics and Finance, CERT Centre for Research and Training, K.L. Malaysia.

Muhammad Umar Chapra (1992). Islam and the Economic Challenge, Islamic Foundation of the International Institute of Islamic

Thought, USA.

Muhammad Akram Khan (2005). “Types of business organization in an Islamic economy”, in: Sheikh Gazali, Syed Omar Syed Agil,

Aidit Hj. Ghazali (Eds.), An Introduction to Islamic Economics and Finance, CERT Centre for Research and Training, K.L.

Malaysia.

Syed Muhammad al Naquib bin Ali al-Attas (1995). Prolegomena to the Metaphysics of Islam: An Exposition of the Fundamental

Elements of the Worldview of Islam, Kuala Lumpur: International Institute of Islamic Thought and Civilization (ISTAC).

Syed Muhammad al Naquib bin Ali al-Attas (1993). The Meaning and Experience of Happiness in Islam, Kuala Lumpur:

International Institute of Islamic Thought and Civilization (ISTAC).

Yusuf al Qardawi, “Fiqh al-Zakah: A comparative study of zakah, regulations and philosophy in the light of Qur’an and Sunnah”,

trans. by Monzer Kahf, Scientific Publishing Centre King Abdulaziz University Jeddah, Saudi Arabia, Vol. II, available online at:

http://monzer.kahf.com/books/english/fiqhalzakah_vol1.pdf.

Zubair Hasan and Habibah Lehar (2011). Fundamentals of Microeconomics: Book Review, Selangor: Oxford Fajar.

“The end of capitalism”, available online at: http://endofcapitalism.com.

“The end of capitalist—So what’s next?”, available online at:

http://www.huffingtonpost.com/klaus-schwab/end-of-capitalism—_b_1423311.html.

Available online at: http://www.globalissues.org/article/26/poverty-facts-and-stats.

World Bank Development Indicator 2008, http://www.globalissues.org/article/26/poverty-facts-and-stats.

Sabahuddin Azmi (2012), “An Islamic approach to business ethics”, available online at:

http://renaissance.com.pk/Mayviewpoint2y5.htm.