towards better transport

DESCRIPTION

According to Towards Better Transport, produced in cooperation with Serco and Bevan Brittan LLP, traffic congestion is now endemic, affecting not just large cities but also the core motorway network and small towns. It currently costs the UK economy in the region of £20bn per year, a figure set to rise significantly in the coming years, harming our future economic competitiveness and growth. The report’s authors, Richard Wellings and Briar Lipson, argue new roads have also tended to be built for political reasons rather than to tackle congestion as transport infrastructure in Britain has become not fit for purpose and detached from consumer demand.TRANSCRIPT

Towards bettertransportFunding new infrastructure with future road pricing revenue

Richard Wellings and Briar Lipson

edited by Oliver Marc Hartwich

Policy Exchange is an independent think tank whose mission is to develop and promote new policy ideas which willfoster a free society based on strong communities, personal freedom, limited government, national self-confidence andan enterprise culture. Registered charity no: 1096300.

Policy Exchange is committed to an evidence-based approach to policy development. We work in partnership with aca-demics and other experts and commission major studies involving thorough empirical research of alternative policy out-comes. We believe that the policy experience of other countries offers important lessons for government in the UK. Wealso believe that government has much to learn from business and the voluntary sector.

Trustees

Charles Moore (Chairman of the Board), Theodore Agnew, Richard Briance, Camilla Cavendish, Richard Ehrman,Robin Edwards, George Robinson, Andrew Sells, Tim Steel, Alice Thomson, Rachel Whetstone.

About the authors

Dr Richard WellingsDeputy Editorial Director, Institute ofEconomic AffairsDr Richard Wellings is the DeputyEditorial Director at the Institute ofEconomic Affairs. He is a deputy editor ofthe journal Economic Affairs and works onthe production of the IEA’s monographseries. After graduating from OxfordUniversity, he undertook a PhD on trans-port policy at the London School ofEconomics, which he completed in 2004.Subsequently, he worked as a researcher forA & F Consulting Engineers, before join-ing the IEA in August 2006. He con-tributed two papers to The Railways, theMarket and the Government (IEA, 2006)and is co-authoring a forthcoming bookon road privatisation.

Briar LipsonResearch Fellow, Policy ExchangeBriar Lipson is a Research Fellow at PolicyExchange specialising in EconomicCompetitiveness. After graduating with anMA in Economics from the University of

Edinburgh, she worked as a ParliamentaryResearcher for Grant Shapps MP.

Dr Oliver Marc HartwichChief Economist, Policy ExchangeDr Oliver Marc Hartwich is Policy Exch-ange’s Chief Economist. He was born in1975 and studied Business Administrationand Economics at Bochum University (Ger-many). After graduating with a Master’sDegree, he completed a PhD in Law at theuniversities of Bochum and Sydney (Aus-tralia) while working as a Researcher at theInstitute of Commercial Law of Bonn Uni-versity (Germany). Having published hisaward-winning thesis with Herbert UtzVerlag (Munich) in March 2004, he movedto London to support Lord Matthew Oak-eshott of Seagrove Bay during the process ofthe Pensions Bill. He is the UK Represent-ative for the German think tank the Institutefor Free Enterprise. He is the co-author ofUnaffordable Housing: Fables and Myths,Bigger Better Faster More, Better Homes,Greener Cities and The Best Laid Plans. Hejoined Policy Exchange in January 2005.

2

© Policy Exchange 2008

Published byPolicy Exchange, Clutha House, 10 Storey’s Gate, London SW1P 3AYwww.policyexchange.org.uk

ISBN: 978-1-906097-12-7

Printed by Heron, Dawson and SawyerDesigned by SoapBox, www.soapboxcommunications.co.uk

Contents

Acknowledgements 4Executive summary 5

1 A competitive disadvantage: Britain’s transport infrastructure 82 The case for road pricing 143 Harnessing private finance 204 The institutional framework 325 Taxation and investment 466 Additional policy options 577 Conclusions and recommendations 65

www.policyexchange.org.uk • 3

Acknowledgements

Policy Exchange would like to thank Serco,Bevan Brittan and an anonymous charita-ble donor for their financial support. Theauthors would like to thank all those whomet with them to discuss aspects of theresearch, as well as Nick Boles, DavidWorskett and two anonymous referees fortheir advice and comments. In addition wewould like to thank Philippa Ingram forproof-reading and Oliver Marc Hartwichfor his insight, expertise and ongoing edi-torial support.

4

Executive summary

Transport has become one of the keyrestraints on Britain’s economic growthand quality of life. Successive governmentshave failed to provide the standard of infra-structure necessary to keep up with anincreasingly mobile and dynamic econo-my. Traffic congestion is now endemic,affecting not just large cities but also thecore motorway network and small towns.It currently costs our economy in theregion of £20bn per year, a figure set to risesignificantly in the coming years. This willharm our future economic competitivenessand growth.

International comparisons suggest thatthe UK is close to the bottom of the tablewhen it comes to transport infrastructure.Among the world’s leading economies, theUK has the most crowded and congestedroads, and the fewest motorways. Eachyear more than 1.6 million passenger kilo-metres are travelled on each kilometre ofBritain’s road network: more than twicethe European average. The UK also per-forms poorly in terms of the quality of itspublic transport.

Clearly a step change is needed in thequality of Britain’s infrastructure. Not onlywould this improve our global competi-tiveness – it would also improve the day today lives of the travelling public.

The deficiencies of UK transport infra-structure do not reflect a shortage of taxrevenues from transport. In 2006 privateroad users paid around £32bn in trans-port-related taxes. Of this £32bn, just£8bn was spent on the road network. Andof this £8bn – which is enough in theoryto construct at least 400 miles of six-lanemotorway – a large proportion was spenton repairing damage to the roads (causedprimarily by good vehicles) and anothersignificant portion on anti-traffic and safe-ty measures. New roads have also tended tobe built for political reasons rather than to

tackle congestion. Inefficiency of govern-ment transport spending is a serious prob-lem. Just 6 per cent of passenger travel isundertaken by train, compared with 84 percent by car, yet the railways receive annualsubsidies totalling almost £6.5 billion –nearly as much as the government spendson roads. The apparent misallocation ofresources reflects the fact that transportinfrastructure investment has becomedetached from consumer demand. Theabsence of price signals means it is difficultfor government planners to allocate expen-diture efficiently.

As a method of allocating a scarceresource, to ration roads without employ-ing road user charges is comparable onlywith the Soviet system of queuing: some-thing so discredited as to be consideredridiculous in almost every sphere of life butmotoring. The waste and inefficiency ofsuch a system is painfully obvious to anyonewho has sat in congestion and traffic jams.

But the greatest barrier to pricing – pub-lic opinion – has arisen not because thepublic cannot appreciate the need for it. Itis instead because, having endured decadesof special taxation for the benefit of gener-al spending, motorists do not trust govern-ments to introduce pricing from whichthey will benefit.

One solution, as proposed in this report,is to upgrade transport infrastructure now,and then, once users have began to experi-ence substantial benefits, introduce theroad user charges necessary to cover the

www.policyexchange.org.uk • 5

“ As a method of allocating a scarce resource, toration roads without employing road user charges iscomparable only with the Soviet system of queuing:something so discredited as to be consideredridiculous in almost every sphere of life but motoring”

costs. There is, of course, the problem ofhow to finance the gap between the start ofconstruction and collection of the revenuestream. The answer to this lies in privatefinance. The Private Finance Initiative(PFI) has a largely successful track recordin the transport sector. The PFI was usedin the Design, Build, Finance and Operate(DBFO) road contracts first employed inthe early 1990s. Cost savings compared topublic sector estimates were between 14per cent and 22 per cent for the first eightsuch projects (depending on the discountrate used). The M6 Toll is another exampleof PFI in transport. Despite traffic projec-tions failing to live up to expectations, ulti-mately it has provided a brand new road ina highly congested area at very minimalcost to the taxpayer. Similarly, PFI hasenabled cities such as Nottingham to buildand operate better public transport servic-es.

One of the greatest problems for the pri-vate financing of transport infrastructure ispolitical risk compounded by a lack of longterm stability and accountability in trans-port governance. The Treasury,Department for Transport, HighwaysAgency, Network Rail, RegionalAssemblies, Passenger Transport Executivesand Authorities, not to mention the EU,all have some influence over policy in thisarea; and these are just the public sectorbodies. With so many layers of governanceand such diverse needs in different parts ofthe country we advocate a significantlymore devolved approach to transport, pos-sibly supported by a strategic road networkmanager, Network Road (by analogy withNetwork Rail). Simplifying the system andimproving accountability would maketransport investment considerably moreattractive to potential investors, therebylowering financing costs and raising thequality of affordable schemes.

Hand in hand with reforming anddevolving the institutional structuresmust be consideration of both the fiscalframework around transport and thecharges to be set. At least to begin with,the scheme we advocate will be revenueadditional, but further investigationreveals two very striking facts. First, rela-tively small charges on congestion hot-spots will soon pay for improvements. Forexample, a six-hour peak time weekdaycharge of 10p/km on a six-lane motorwaypriced to run close to capacity could in ayear raise around £1.5 million per km –sufficient to pay for widening to eightlanes or indeed, to construct a brand newsix-lane motorway in parallel. Second, thedynamic effects of pricing and improvedtransport infrastructure on the economywill increase overall tax yields, which intime could facilitate cuts in fuel and vehi-cle taxes.

The issue of transport taxation has beencomplicated in recent years by environ-mental justifications for high fuel taxes.Although both are externalities of roadtransport, congestion and carbon emis-sions are separate problems with differentsolutions. Fuel consumption is a muchmore accurate proxy for carbon emissionsthan distance travelled, and should remainthe preferred tool. That said, even accord-ing to the high-end estimates of the cost ofcarbon emissions detailed in the Sternreport, the carbon tax on a litre of petrolshould be around 11 pence, which is muchless than the current petrol tax rate ofaround 50 pence per litre.

The British economy is suffering fromits reliance on a centrally planned model oftransport governance. It has left the coun-try crying out for an injection of invest-ment which is simply not available fromthe Treasury. In a relatively small countrysuch as Britain with tightly centralised

Towards better transport

6

www.policyexchange.org.uk • 7

Executive summary

planning laws and an affluent car-lovingpopulation, roads are – and will undoubt-edly remain – a scarce resource for whichrationing by queuing and congestion isinefficient. By combining investment with

pricing, and in that order, Britain’s sub-standard transport infrastructure can beupgraded, thereby improving economiccompetitiveness and the quality of life ofthe British public.

1A competitivedisadvantage:Britain’s transportinfrastructure

Decades of insufficient and inefficientinvestment in transport have damagedBritain’s international competitiveness.In their Economic Survey of the UnitedKingdom, the OECD stated that:

“The United Kingdom ranks poorly ininternational comparison both on surveybased measures regarding the quality oftransport infrastructure and on measuresof congestion.” 1

In March 2006 the EconomistIntelligence Unit warned us that the UKrisked slipping down the global businessenvironment rankings if its “congestedand unreliable land transport infrastruc-ture” did not improve.2 The Departmentfor Transport has itself admitted that:“The core of our railway network wasestablished well over a hundred years ago.Most of our motorways were built 30 or40 years ago. Successive governmentshave devoted insufficient resources toupgrading and modernising the transportsystem, while travel on our road and railnetworks has increased to levels that werenever anticipated when they were built.”3

The following figures from a 2001report by the Prime Minister’s StrategyUnit illustrate this analysis:

� In no other major country were theroad lengths per person as short as inthe UK, where there were on average

six metres of roads per inhabitant.Even in the Netherlands, which ismuch more densely populated, thefigure was seven metres.4

� We have fewer kilometres of motor-way than other European countries ofcomparable population. Spain, Franceand Germany each have a motorwaynetwork that is more than twice thesize of ours.5

� Only 30 per cent of railway trackswere electrified in the UK, comparedwith more than 70 per cent inBelgium, Sweden and the Nether-lands.6

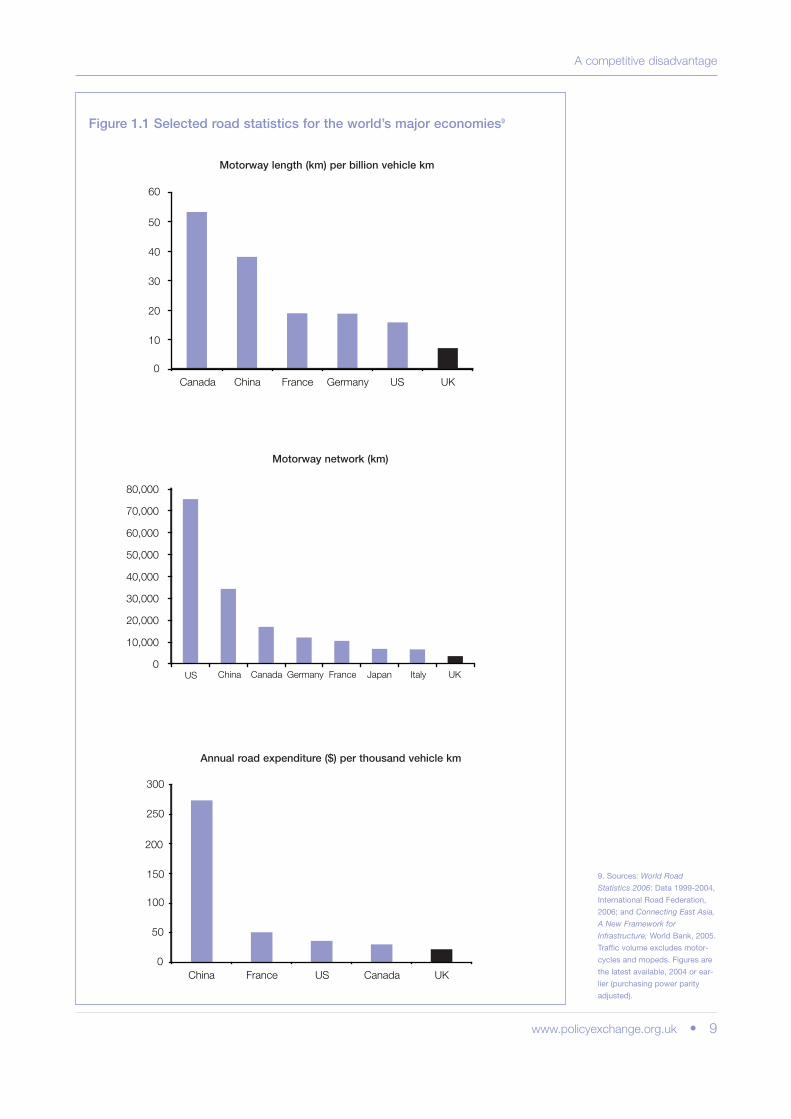

As Figure 1.1 shows, Britain has fallen along way behind its economic competi-tors in the provision of a modern trans-port network, even though it imposes thehighest fuel taxes on road users.7 Alreadyby 2004 China had constructed a motor-way network ten times the size of theUK’s and was investing around thirtytimes the UK figure (adjusted for pur-chasing power parity) in its road net-work. The disparity cannot be explainedby lack of space. Motorways carry 20%of total traffic and 40% of road freight,yet they take up less than one two-thou-sandth of Great Britain’s land area.8

Sir Rod Eddington, who reviewed thelong-term links between transport andthe UK’s productivity, growth and stabil-ity for the Government in 2005-06,

8

1. OECD, Economic Survey of

the United Kingdom 2005:

Public Services and

Infrastructure: Tracking the

Improvements, www.oecd.org

/document/27/0,2340,en_2649

_201185_35461339_1_1_1_1,

00.html

2. The Independent, 28th March

2006, available at: www.findarti-

cles.com/p/articles/mi_qn4158/is

_20060328/ai_n16180583

3. Department for Transport, The

Future of Transport, Stationery

Office, 2004

4. The Strategy Unit, Transport

Strategy Review: Phase One,

Cabinet Office, 2001

5. A large discrepancy remains

even after adjustments are made

for land area and population

density. In fact, densely populat-

ed countries such as the UK

would be expected to have more

motorway km per head of popu-

lation than less densely populat-

ed nations, since there would be

greater demand for high capaci-

ty routes (traffic also declines as

distances increase).

6. Ibid.

7. World Road Statistics 2006,

Tables 8.1 and 8.2, International

Road Federation, 2006

8. Calculated from Department

for Transport, Transport

Statistics Great Britain, Ch. 7,

2006

www.policyexchange.org.uk • 9

A competitive disadvantage

9. Sources: World Road

Statistics 2006: Data 1999-2004,

International Road Federation,

2006; and Connecting East Asia,

A New Framework for

Infrastructure, World Bank, 2005.

Traffic volume excludes motor-

cycles and mopeds. Figures are

the latest available, 2004 or ear-

lier (purchasing power parity

adjusted).

0

10

20

30

40

50

60

Canada China France Germany US UK

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

US China Canada Germany France Japan Italy UK

Figure 1.1 Selected road statistics for the world’s major economies9

Motorway length (km) per billion vehicle km

Motorway network (km)

0

50

100

150

200

250

300

China France US Canada UK

Annual road expenditure ($) per thousand vehicle km

found that air transport performed rela-tively well (although planning delays nowthreatened this competitive advantage),but that land transport was a particularweakness. His study concluded that:“Continued economic success is forecastto lead to rising demands – if leftunchecked 13 per cent of traffic will besubject to stop-start travel conditions by2025.”10

British governments have always had apeculiar reluctance to invest in roads. Inthe 1920s and 1930s, when the firstmotorway networks were being con-structed in Germany, Italy and the US,the Ministry of Transport actually pre-vented entrepreneurs from buildingmotorways in England.11 The UK wouldhave to wait another 30 years, until the1950s, for its first motorway. If such ananti-road building tradition is upheld inthe 21st century, perhaps rationalised onenvironmental grounds, the country willbe unable to fulfil its economic potential.

Very little extra capacity has beenadded since 1995, despite rising inter-urban congestion. Existing motorwaysoften take indirect routes that add tojourney times; the M1 heads north westtowards Birmingham before headingnorth to Leeds. There are still obviousgaps in the network; Manchester andSheffield, two of the country’s largestcities and only 30 miles apart, have nodirect motorway connection – travellersmust choose between the tortuous anddangerous Woodhead and Snake Passesor divert 25 miles north to the M62.Motorway provision is also patchy alongthe route of the Great North Roadbetween London and Edinburgh. Thereis no link between Newcastle andEdinburgh or Newcastle and Glasgow,and the current A1 link follows an indi-rect and time-consuming route. The largeconurbations of the North East ofEngland (Teesside and Tyneside) have yetto be linked to the main motorway net-

work, although some progress has beenmade in recent years in upgrading the A1in North Yorkshire. No direct motorwaylink exists between Southampton, one ofBritain’s biggest ports, and the ChannelTunnel.

The misallocation of investmentThe pattern of new roads has borne littlerelation to congestion levels or consumerdemand, with the possible exception ofthe privately built and operated M6 Toll(Birmingham Northern Relief Road).The A74 through southern Scotland didnot suffer from chronic congestion, yetthis road was chosen for upgrading tomotorway standard, probably for politi-cal reasons as it links Scotland (almost) tothe English network. Similarly, theupgrade of the A1 in North Yorkshire wasdriven, at least in part, by regional devel-opment objectives.

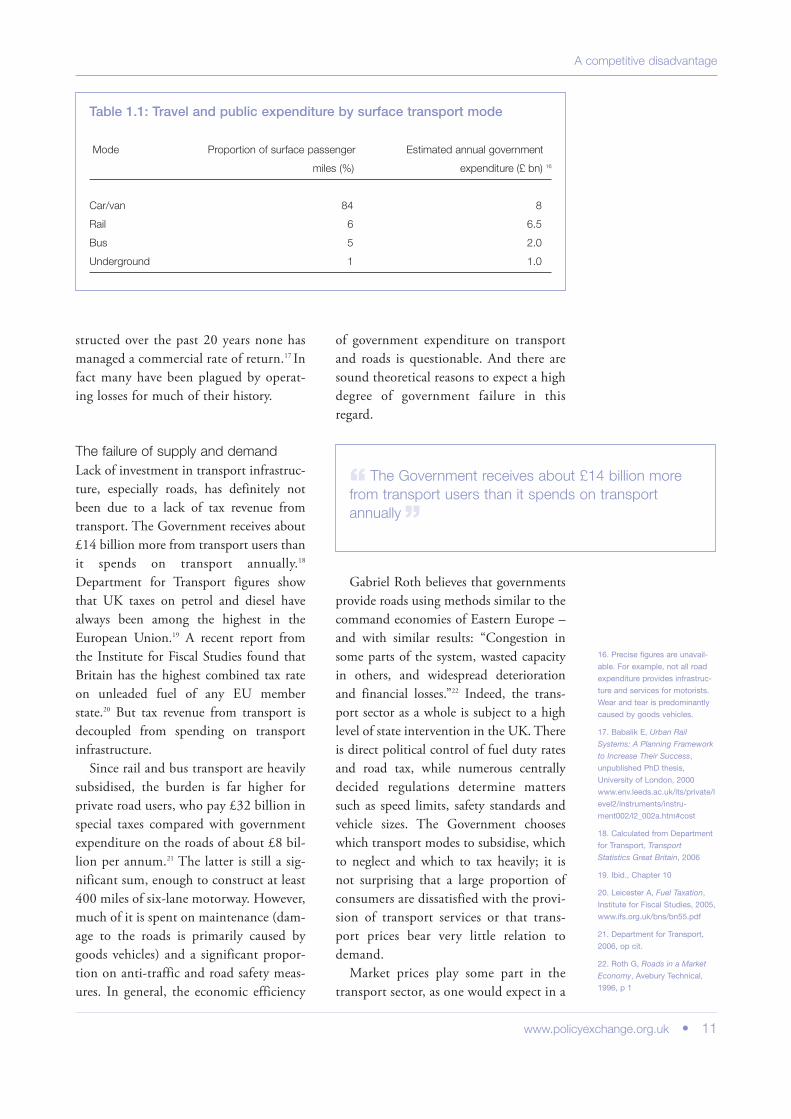

Expenditure on public transport hasalso been driven by political expediencyrather than economic efficiency. Thelevel of government subsidy has risen sig-nificantly over the past 15 years to about£10 billion a year.12 Of this, approximate-ly £6.5 billion per annum is destined forBritain’s railways; even though theyaccount for only 9 per cent of freightmileage and 6 per cent of passengermileage (see Table 1.1).13 Furthermoreoperating subsidies are disproportionate-ly concentrated on poorly used regionalrailways rather than the overcrowdedLondon commuter routes.14

Money has also been lavished on largeinfrastructure projects such as theChannel Tunnel Rail Link and the mod-ernisation of the West Coast Main Line(£5 billion and £7.6 billion respectivelyin 2004 prices). Neither scheme is likelyto achieve a commercial return on invest-ment.15 Local transport schemes have pos-sibly been even worse investments. Ofthe numerous light rail schemes con-

Towards better transport

10

10. The Eddington Transport

Study, the Case for Action: Sir

Rod Eddington’s Advice to

Government, The Stationery

Office, 2006

11. Plowden W, The Motor Car

and Politics, The Bodley Head,

1971

12. Department for Transport,

2006, op. cit.

13. Ibid.

14. Wellings R, ‘Rail in a Market

Economy’ in The Railways, the

Market and the Government,

IEA, 2006, p 225

15. See www.ctrl.co.uk and

Modern Railways, June 2004,

pp 52-4

structed over the past 20 years none hasmanaged a commercial rate of return.17 Infact many have been plagued by operat-ing losses for much of their history.

The failure of supply and demandLack of investment in transport infrastruc-ture, especially roads, has definitely notbeen due to a lack of tax revenue fromtransport. The Government receives about£14 billion more from transport users thanit spends on transport annually.18

Department for Transport figures showthat UK taxes on petrol and diesel havealways been among the highest in theEuropean Union.19 A recent report fromthe Institute for Fiscal Studies found thatBritain has the highest combined tax rateon unleaded fuel of any EU memberstate.20 But tax revenue from transport isdecoupled from spending on transportinfrastructure.

Since rail and bus transport are heavilysubsidised, the burden is far higher forprivate road users, who pay £32 billion inspecial taxes compared with governmentexpenditure on the roads of about £8 bil-lion per annum.21 The latter is still a sig-nificant sum, enough to construct at least400 miles of six-lane motorway. However,much of it is spent on maintenance (dam-age to the roads is primarily caused bygoods vehicles) and a significant propor-tion on anti-traffic and road safety meas-ures. In general, the economic efficiency

of government expenditure on transportand roads is questionable. And there aresound theoretical reasons to expect a highdegree of government failure in thisregard.

Gabriel Roth believes that governmentsprovide roads using methods similar to thecommand economies of Eastern Europe –and with similar results: “Congestion insome parts of the system, wasted capacityin others, and widespread deteriorationand financial losses.”22 Indeed, the trans-port sector as a whole is subject to a highlevel of state intervention in the UK. Thereis direct political control of fuel duty ratesand road tax, while numerous centrallydecided regulations determine matterssuch as speed limits, safety standards andvehicle sizes. The Government chooseswhich transport modes to subsidise, whichto neglect and which to tax heavily; it isnot surprising that a large proportion ofconsumers are dissatisfied with the provi-sion of transport services or that trans-port prices bear very little relation todemand.

Market prices play some part in thetransport sector, as one would expect in a

www.policyexchange.org.uk • 11

A competitive disadvantage

16. Precise figures are unavail-

able. For example, not all road

expenditure provides infrastruc-

ture and services for motorists.

Wear and tear is predominantly

caused by goods vehicles.

17. Babalik E, Urban Rail

Systems: A Planning Framework

to Increase Their Success,

unpublished PhD thesis,

University of London, 2000

www.env.leeds.ac.uk/its/private/l

evel2/instruments/instru-

ment002/l2_002a.htm#cost

18. Calculated from Department

for Transport, Transport

Statistics Great Britain, 2006

19. Ibid., Chapter 10

20. Leicester A, Fuel Taxation,

Institute for Fiscal Studies, 2005,

www.ifs.org.uk/bns/bn55.pdf

21. Department for Transport,

2006, op cit.

22. Roth G, Roads in a Market

Economy, Avebury Technical,

1996, p 1

“ The Government receives about £14 billion morefrom transport users than it spends on transportannually”

Table 1.1: Travel and public expenditure by surface transport mode

Mode Proportion of surface passenger Estimated annual government

miles (%) expenditure (£ bn) 16

Car/van 84 8

Rail 6 6.5

Bus 5 2.0

Underground 1 1.0

mixed economy, but their role is subordi-nated to that of political control, prima-rily from central government depart-ments. For example, the provision of newinfrastructure is largely centrally planned.If there is a congested road then it is veryunlikely that capacity will be increased asa response (raising tolls is impossibleunder the present regime). New roads areperhaps more likely to be built in rela-tively uncongested areas as part of regen-eration schemes.

Central planning authorities are lesscapable of making efficient resource allo-cation decisions than free markets operat-ing within relatively unrestrictive regula-tory framework. Because governmentdecision-makers do not personally ownthe capital they are allocating they haveweaker incentives to act responsibly orshow initiative.23 They are further ham-pered because they may not have accessto relevant market prices and thereforecannot accurately calculate costs and out-puts.24 Transport officials have faced thisproblem when planning new roadschemes. In the absence of toll revenuefrom road users, the true value of thefacility to users cannot be known andtherefore the rate of return on the capitalspent cannot be calculated. Vital infor-mation about the best way of allocatingcapital resources is lost.

Although it is impossible to quantifyprecisely the impact of the current misallo-cation of transport sector resources on theBritish economy, the negative effects couldbe of far greater magnitude than those sim-ply relating to congestion. Commentators

have often neglected transport’s integralrole in productivity increases and theresulting production of wealth. Traveltimes are not only dependent on theabsence of congestion but also the patternof infrastructure provision.

One should remember, too, that subsi-dies for public transport are financedfrom taxation, with the associated harm-ful effects on the production of wealth,including reduced incentives and distort-ed decision making. Then there are thecosts of tax collection (and the effortexpended in avoiding taxes) to consider.Some economists have estimated that“deadweight losses” mean every addition-al pound collected by taxation costs theeconomy a further 50p to £1.50.25 Thuspublic transport subsidies inflict substan-tial economic damage for the sake of a rel-atively small proportion of the market formobility.

Transport and wealth creationAs our economy has expanded the need totravel has increased, but investment intransport infrastructure has not kept paceand existing transport networks havebecome increasingly congested. In noother major European country are roads ascongested as in the UK. On every kilome-tre of Britain’s road network more than 1.6million passenger kilometres are travelledevery year – more than twice the Europeanaverage.26 It has been estimated that trafficcongestion costs the UK economy as muchas £21 billion per year.27

Eddington estimated that by 2025,without action, congestion on England’sroads will rise by 30 per cent, increasingcosts to businesses and freight by over £10billion a year, and wasting an extra £12billion worth of time for households.28

As for the opportunity costs (negativeeconomic impacts of the exchanges notundertaken because perceived congestionacts as a deterrent) associated with conges-

Towards better transport

12

23. Mises L, ‘Economic calcula-

tion in the socialist common-

wealth’, in F. A. Hayek (ed.),

Collectivist Economic Planning:

Critical Studies of the

Possibilities of Socialism,

Routledge and Kegan Paul,

1935, pp 87-130

24. See Mises L, Human Action:

A Treatise on Economics,

William Hodge,1949, p 696

25. See, for example, Harrison F,

Wheels of Fortune, London: IEA,

2006, p 165

26. Calculated using data from

Panorama of Transport, Eurostat,

2007

27. Blythe P, ‘Congestion

Charging: technical options for

the delivery of future UK policy’,

Transportation Research Part A,

38; pp 571-87, 2006

28. Eddington R, op. cit., p 30

“ On every kilometre of Britain’s road network more than

1.6 million passenger kilometres are travelled every year –

more than twice the European average”

tion, they are difficult to estimate.Examples include businesses not compet-ing for trade in congested areas, potentialemployees not applying for jobs becausethe travel-to-work time would be too greatand directors not holding a meetingbecause it would waste too much time totravel the distance to convene.

The economic benefits of efficientlydistributed transport capacity could besubstantial. If travel costs allow, morecompanies can locate in one area, increas-ing competition, enabling economies ofscale and thus increasing productivity.For example, new motorways could dra-matically increase the population within,say, two hours’ drive of a particular loca-tion. The new infrastructure could makethe construction of a large and efficientdistribution centre viable where previous-ly only a small centre would have beenprofitable. Reduced transport costs bringsimilar gains in the retail and manufac-

turing sectors. Trade is facilitated thatotherwise would be uneconomic, result-ing in more specialised and productiveeconomic activity. Of course, for the fulleconomic benefits of improvements intransport infrastructure to be realised it isessential that businesses and individualsare free to locate their activities at themost efficient sites. Thus the biggest eco-nomic gains are likely to be achievedwhen efficient transport networks arecombined with a high degree of freedomin land markets.29

The widening gap between supply anddemand for transport in our fast-movingeconomy is threatening our very economiccompetitiveness. Rather than risk slippingdown the international league tables of thebest places to live and do business in theworld, Britain must bring about a stepimprovement in transport. This reportexplores a long-term and politically viablesolution.

www.policyexchange.org.uk • 13

A competitive disadvantage

29. On the economic impact of

planning controls, see Evans A

and Hartwich O, The Best Laid

Plans: How Planning Prevents

Economic Growth, Policy

Exchange, 2007

2The case for roadpricing

The true costs of motoringAt present a significant proportion ofroad user costs such as depreciation,insurance and vehicle excise duty (VED),are fixed. Once paid, they may actuallyencourage motorists – equating marginaljourney costs to the price of fuel – to usetheir cars more than they otherwise wouldin order to justify the sunk payments.Road pricing could help reduce this‘information’ problem by, in relativeterms, reducing the fixed element andincreasing the marginal element of roadtravel costs – for example, by abolishingvehicle excise duty and introducing pay-as-you-go insurance and tolls for usingcongested roads.

Fuel tax, and to a lesser extent VED, arethe only pricing mechanisms currentlyavailable to the government to ration roaduse. Although they undoubtedly do this,they do not accurately reflect the externalcosts of using particular roads. These exter-nal costs vary widely by location, time ofday, type of vehicle and grade of road.Evaluated rationally, they could be incor-porated into road user charges. Thedetails of such a scheme are outlinedbelow.

Congestion costsAt certain times and locations road space isclearly a scarce resource. The evidence iscongestion. But such variations in thescarcity of road space are not reflected incurrent motoring taxes: users pay roughlythe same no matter what kinds of roadthey use, where or at what times.

To put it in blunt economic terms, driv-ers at busy times do not pay the full mar-ginal costs they impose on other road usersthrough resulting congestion. Of course,motorists using congested roads pay a pricein the sense that their time is wasted.However those for whom time has a lowervalue (for example the retired or unem-ployed) are able to impose higher costs onthose for whom time has a greater value(hospital consultants or couriers deliveringexpensive just-in-time products for exam-ple). Any system that fails to account forthe fact that different people value timedifferently is intrinsically inefficient. As amethod of allocating a scarce resource, toration roads without employing roadcharges is comparable only with the Sovietsystem of queuing: something so discredit-ed as to be considered ridiculous in almostevery sphere of life but motoring.

Road pricing would force motorists totake the value of their time into account.People with a high degree of flexibilityabout when they travelled could choose togo at off-peak times when tolls were low.Road operators could even offer specialrates, like saver fares on the railways, toencourage travel at the quietest periods.Such variations in price would even outtraffic levels over time and space, poten-tially increasing the use of existing roadcapacity.

Track costsIt clearly makes sense for drivers usingextremely expensive urban motorways –perhaps built on expensive land and

14

involving the purchase of hundreds of prop-erties and tunnelling – to pay more than adriver using a neglected rural A-road thathas barely been improved since the 1920s.

However, although this principle caneasily be applied to newly built infrastruc-ture, it is more difficult when it comes toexisting roads. Drivers may feel, with somejustification, that they have already paidthe construction costs through theirmotoring taxes. But it is important that thecurrent capital value of roads is reflected inpricing regimes to ensure an efficient allo-cation of resources. These issues and possi-ble institutional solutions are discussedfurther in Chapters 4 and 5.

Environmental costsThe environmental costs of road use –such as noise and pollution – also varygreatly over the road network and, onceagain, the current taxation regime does notreflect this. The introduction of road pric-ing offers the possibility of more closelyrelating vehicle charging to differences inenvironmental impact. For example, noiseand local air pollution costs might be neg-ligible in many sparsely populated ruralareas but considerable in densely populat-ed urban areas. Any attempt to includeenvironmental charging within a road pric-ing scheme would undoubtedly be compli-cated by disagreements over valuationmethodologies.30

Another subject for debate would bewhether revenues from environmentalcharges should be appropriated by govern-ment for general expenditure, as with cur-rent fuel duty revenues or whether theyshould be used directly to reduce environ-mental costs (or perhaps compensateaffected individuals). If these problemscan be overcome then pricing could createincentives for road users to reduce theenvironmental impact of their journeys by,for example, using quieter and less-pollut-ing vehicles or driving less in urban resi-dential areas.

Accident costsSimilar benefits could be forthcoming inroad safety. More than 3,000 people arekilled on Britain’s roads every year, with ahuge human and economic impact.31 Itcould be possible to pay accident-insurancebased on usage, as Norwich Union nowoffers, or even as a component of tolls. Witheither system, insurance companies couldcharge road users more to travel along roadswith a high casualty rate or after midnight,and less to travel along safer roads or at off-peak times during the day. This would givedrivers an obvious financial incentive to usesafer roads and could, if some form of par-tial pricing is introduced, help deter thediversion of motorists from motorways onto minor roads.

At the same time, infrastructure opera-tors would have an incentive to ensurethat their roads were safe in order toattract customers – particularly if theinstitutional framework encouraged adegree of competition between infrastruc-ture providers/ operators. Thus pricingoffers the potential to introduce strongfinancial incentives towards reductions inthe accident rate.

It is also possible that a pricing systemcould reduce the number of untaxed anduninsured drivers using the road network.Research suggests that such individuals aremore likely to be involved in accidentsthan other motorists.32 Thus, dependingon the nature of the scheme(s) implement-ed, there could be an additional road safe-ty effect beyond the incentive structuresdetailed above.

www.policyexchange.org.uk • 15

The case for road pricing

30. See Wellings R, op. cit.

31. Department for Transport,

2006, op. cit.

32. RAC Foundation, News

Release, available at: www.rac-

foundation.org/index.php?option

=com_content&task=view&id=31

8&Itemid=35, 7th November

2005

“ Variations in the scarcity of road space are not

reflected in current motoring taxes: users pay roughly the

same no matter what kinds of road they use, where or at

what times”

Clearer choiceRoad pricing would make it straightfor-ward to compare the total cost of travellingby car or public transport. Distortionsfrom discriminatory taxes and subsidieswould be removed or at least minimised,externalities would be costed and account-ed for and, with congestion reduced,motorists would be able to estimate theirjourney times with far more accuracy thanat present. Britain’s transport infrastructurewould be used more efficiently by all users.

Better investmentRoad pricing is not just about enablingindividuals to make rational transportdecisions, the revenues produced wouldalso provide valuable information aboutconsumer demand for travel and point tothose locations where new infrastructuremay be most profitably provided. Byexploiting the scattered preferences of 30million drivers, road prices would providefar more accurate and dynamic informa-tion about transport preferences than thatcurrently available to planners.

If roads were priced to avoid conges-tion, the highest tolls would be raised atthe biggest bottlenecks, providing a pow-erful incentive for infrastructure operatorsto construct additional capacity. Thiscapacity could be for public transportrather than private road vehicles if itwould harvest more revenue and the insti-tutional framework were sufficiently flexi-ble to allow such cross-modal investment.As Alan Day argues, road pricing shouldnot simply be used to ration existing road

space, but also as “a measure of whether ornot to add to (or, indeed, subtract from)the existing road space: it can and shouldbe used as an investment criterion.”33 Inthe absence of pricing and given the dis-tortions of the taxation system, it is diffi-cult to value our road infrastructure accu-rately. Potential investors struggle to calcu-late future demand and revenue risk ishigh.

Facilitating competitionThe revenue risk problem is well illustratedby the development of the M6 Toll (knownin the planning and construction phase asthe Birmingham Northern Relief Road).Such uncertainties meant that the cost ofthe scheme was inflated by high financingcosts, while traffic projections – and rev-enue forecasts – were overly optimistic.

In the absence of wider pricing the M6Toll suffered from ‘unfair’ competitionfrom the existing M6. In particular, exceptduring severe congestion, speed-limitedhauliers had little to gain by using the tollroute. At the same time, M6 Toll userseffectively paid twice when fuel duty andvehicle excise tax are included. If a nation-al road pricing system had been in placemotorists on the original M6 would alsohave had to pay a toll and, potentially,motoring taxes might have been reducedor abolished. The ‘unfair’ competitioncurrently observed would have been elim-inated.

The implications of this are potentiallygroundbreaking. It would enable privateinvestors to build new links to competewith existing ones in terms of price andquality of service – and bring about a stepchange in the quality of Britain’s infra-structure. However, the level playing fieldnecessary to obtain the greatest economicbenefit from private investment wouldrequire an appropriate institutional and fis-cal framework. As we examine next, thepolitics of transport could make this diffi-cult to achieve.

Towards better transport

16

33. Day A, ‘The Case for Road

Pricing’, Economic Affairs, 18

(4), pp 5-8, 1998

“ If roads were priced to avoid congestion, the highest

tolls would be raised at the biggest bottlenecks, providing

a powerful incentive for infrastructure operators to

construct additional capacity”

What is the case against roadpricing?Road pricing could be a remarkable tool toimprove the efficiency of our transportnetwork, but honest analysis must concedethat it will have some inherent difficultiesto overcome.

Public oppositionAbout 1.8 million people signed a petitionagainst road pricing on the Downing Streetwebsite and surveys show that between halfand three-quarters of the public areopposed to pricing, depending on thedetails of the scheme.34

The same surveys demonstrate thatopposition is reduced when it is madeclear that road pricing revenues will beused to reduce motoring taxes or improvetransport infrastructure.35 Indeed, amajority of the public might support ascheme providing certain conditions aremet. However, there is widespread andunderstandable distrust of governmentmotives and a fear that road pricing couldend up being another tax-raising exercise,just as the road fund was appropriated bythe Treasury and fuel duty is used for gen-eral expenditure rather than improve-ments to transport infrastructure.36 Theway in which the proceeds from roadpricing will be used would have to beattractive and clear in order to build uppublic support.

What rates should be charged?If the primary goal is to reduce congestionand speed up traffic, then prices shouldreflect the scarcity value of sections of roadat various times. Prices would need to beset by trial and error until congestion dis-appeared and traffic flowed freely.37 Butgiven the likely opposition to the introduc-tion of pricing mechanisms, political expe-diency and not scarcity value may deter-mine the charge set. Economic benefitswould then be lost since prices could betoo expensive at certain times (leading to

wasted road space and lost economic activ-ity) and too cheap at others (causing con-gestion).

Although road pricing schemes must besophisticated enough to ensure the effi-cient use of road space, they must also bepredictable and easy for users to under-stand, so that motorists are not surprisedby a sudden rise in rates leading them toseek alternative routes. Unfortunately, it ishard to achieve both features simultane-ously, so a careful balance has to be struckbetween fine-tuning the system and notconfusing drivers. This also means dealingwith “boundary” effects that occur, forexample, when traffic increases just afterthe peak rate charges finish. These are dif-ficult technical questions, but they can beanswered. Over time and with the oppor-tunity to experiment with different charg-ing schemes, what works and what doesnot will become clear.

Competing transport systemsRoad pricing would not operate in a vacu-um because there are other modes of trans-port with which roads have to compete. AsEddington recommended, the Govern-ment needs to get prices right for all formsof transport, especially congestion pricingon roads and environmental pricing acrossall modes.38 For travellers to make efficientdecisions, therefore, price distortionsbetween different modes must be removedas far as possible. If congestion pricing isapplied to the road system then it mustalso be applied to public transport, includ-ing the busy commuter trains running intocentral London. This has, of course,already begun with peak and off-peak pric-ing on the rail and London Undergroundnetwork. Levels of overcrowding on thesetrains suggest that peak fares should beincreased further, although some passen-gers may wish to trade discomfort foraffordability. But on the rail network, sea-son tickets and fares for all journeys within50 miles of London are regulated so fran-

www.policyexchange.org.uk • 17

The case for road pricing

34. See Road User Charging,

RAC Foundation 2006, www.rac-

foundation.org/index.php?option

=com_content&task=view&id=35

0&Itemid=35

35. Ibid.

36. Plowden W, op cit.

37. See Hibbs J, ‘A Radical

Approach’, Economic Affairs, 18

(4), pp 2-4, 1998

38. Eddington R, op. cit., p 50

chisees are not at liberty to raise fares inorder to reduce demand on peak-timecommuter trains. The resulting congestionhas led to demands for expensive capacityincreases on the worst affected routes. Ifthe logic of road pricing were applied topublic transport it would be difficult tojustify the continued regulation of suchfares.

The same reasoning should apply toenvironmental charges. If an environmen-tal charge is included within road prices,public transport users should also pay sucha levy. Under-pricing the environmentalimpact of public transport will encourageinefficient use.

Taxation and subsidiesWhile road users pay taxes such as vehicleexcise duty and fuel tax, buses and trainsreceive substantial government subsidiesand a VAT exemption on their fuel. Thisimbalance should ideally be corrected.

From an environmental perspective andin certain locations the continued govern-ment subsidy of carbon emissions throughspecial support for public transport is diffi-cult to justify. The introduction of roadpricing – alongside an economy wide car-bon tax (see Chapter 5) – would demon-strate whether existing public transportservices are commercially and environmen-tally viable. This is a further argument infavour of increasing the pricing flexibilityof public transport operators and reducingsubsidy levels.

The introduction of a (non-carbon)environmental component to road pricing– it would probably vary according to theestimated (non-carbon) environmentalimpact of a journey – would, alongside aneconomy wide carbon tax, provide a pow-erful rationale for phasing out existingmotoring taxes. This would also increasethe political acceptability of road pricingand have economic benefits, since distor-tions are likely to occur when taxes arefocused on one sector of the economy

alone. These issues are discussed further inChapter 5.

Operating costsOpponents of road pricing argue that mostof the revenue generated would be spent onadministration. High estimates of the costsof introducing and administering a nationalscheme have been published recently.39 If,for example, the system cost £10 billion ayear to run (about £300 per vehicle), thisamount would constitute around half theannual current cost to the UK economy ofcongestion and, to put the figure in furtherperspective, would be sufficient to constructat least 500 miles of six-lane motorway. Acomplex IT driven road-pricing schemecould suffer from severe cost over-runs anddelays in implementation, as seen with theGerman lorry charging system, and the £6billion National Health Service “choose andbook” computer system, which may end upcosting £50 billion.40

Opinion differs on whether such a sce-nario is probable for road pricing; it hasbeen suggested that the costs of implemen-tation are likely to be concentrated in thetechnology installed in vehicles rather thancomplex computer systems.41 Withoutquestion, though, any proposal willinevitably have to balance the potentialbenefits with the costs and risks associatedwith administration.

Wider economic effectsThus the economic benefits of road pricingcould be lost through a combination ofpolitical interference, modal bias, failure toreform taxation and inflated administrativecosts. It would be foolish to deny that thesedangers exist or to ignore them whenintroducing a road pricing scheme.

If expensive peak-time pricing wereintroduced in major cities to eliminatecongestion, strict government planningcontrols could prevent businesses andhouseholds from moving out of cities toavoid the high charges (a market reaction

Towards better transport

18

39. For example ‘Drivers face

£600 bill for an in-car road pric-

ing black box’, Daily Telegraph,

21 February 2007. www.tele-

graph.co.uk/news/main.jhtml?xml

=/news/2007/02/19/nroads19.xml

40. See Sunday Times, 2 April

2006 www.timesonline.co.uk/tol/

comment/columnists/simon_jenk

ins/article701108.ece

41. Private communication, 19

April 2007

that makes more efficient use of the avail-able road space and cheaper land).Companies could face demands forincreased pay from workers charged todrive into town at peak times.

At the same time, modal bias is likely tomean that public transport users wouldnot be paying the full costs of commutinginto city centres, since services are sub-sidised and environmental costs ignored.Thus significant numbers of commuterswould be displaced on to public transport,which is often already full at peak times.The Government might then think itexpedient to spend significant capitalsums on increasing capacity on publictransport. However, because market pricesare so distorted by the simultaneous use offuel tax, VED, road user charges and pub-lic transport subsidies, and because gov-ernments are notoriously poor at invest-ment, this may well represent a misalloca-tion of resources. A significant proportionof the economic gain from road pricingcould be dissipated on wasteful publictransport schemes. Although in some areaspublic transport schemes will be commer-cially viable, in others journeys cannot eas-ily be transferred to public transport andso businesses and individuals could facesubstantial economic losses, both fromdirect charging costs and opportunitycosts.

This is only one example, but it couldhave wider implications. Public transportreceives around £10 billion in subsidiesevery year.42 If the number of commutersusing public transport doubled as a resultof road pricing, the need for increased sub-sidy would be very significant indeed.

The redistributive effects of road pricingare also far from clear. A negative effect onsome less affluent inner city areas is possi-ble. Pricing could deter middle-incomemotorists from living in such locations,leaving inner cities to low-income publictransport users and increasing social polar-isation. Demands for regeneration subsi-

dies could then rise, dissipating yet more ofthe benefits of road pricing.

Finally, there is the possibility that, driv-en by bureaucratic and industry interests,the road pricing system would suffer fromhigh set up and administration costs, fur-ther undermining its economic case.

A new case for road pricingAll of this leaves transport policy on thehorns of a political dilemma. To realise theadvantages of a market-based solution, roadpricing has to be introduced. Yet on its ownsuch a proposal would be guaranteed tomeet with fierce political resistance, whichin turn could lead to excessive interventionand over-regulation – as happened with railprivatisation. Given budget constraints andthe high level of fuel taxation, it would bedifficult to finance new infrastructurethrough either the general budget or bylevying higher petrol and diesel duties. Oneway to surmount these difficulties would beto combine the introduction of road pric-ing with the provision of new infrastruc-ture. Motorists would not then be payingagain for existing infrastructure, but forvital upgrades to the network.

But unfortunately this would involve atime lag, because new infrastructure cantake years to plan and build. The M6 Toll,for example, was first considered in theearly 1980s but opened only in 2003.Paying the tolls would only be followed bybetter infrastructure at a much later date. Iftransport users were charged throughoutthis time without any visible improvementin the infrastructure, road pricing couldwell fail. That is why this report suggeststaking a different route: introducing roadpricing after the necessary upgrades to ourtransport infrastructure have been made.The obvious question, which the nextchapter explores, is how to finance theinvestment in new infrastructure beforethe revenue stream from user charging haseven begun.

www.policyexchange.org.uk • 19

The case for road pricing

42. Department for Transport,

2006, op cit.

3Harnessing privatefinance

Historical contextIn the 18th century a mixture of publicand private capital funded the develop-ment of an extensive and integrated net-work of toll roads or turnpikes.43 In the19th century, following the commercialdevelopment of the canals, private compa-nies built a vast railway network, support-ed by Acts of Parliament that enabled thecompulsory purchase of land. During the1920s private consortiums proposed aseries of profit-making toll motorwayslinking London with other big cities, usu-ally with the support of the local authori-ties along the route. By this time, however,the political climate had changed and SirHenry Maybury, the Minister of Tran-sport, objected to “the placing of very imp-ortant road traffic arteries in the hands ofprivate capitalist enterprise, to be operatedfor profit”.44 Britain never did get a private-ly built motorway network but, in theright conditions, private investors wereprepared to fund the development of large-scale infrastructure networks.

As the role of the State grew, in trans-port as in other economic sectors, opportu-nities for private investment became morelimited. The Conservative Government ofthe 1980s tried to increase the role of theprivate sector, albeit within a tightly regu-lated framework. The Queen Elizabeth IIBridge at Dartford, opened in 1991, wasthe first notable modern road scheme to beprivately financed; investors were paid backusing toll revenues. It served as a model forseveral projects launched under the PrivateFinance Initiative (PFI) during the 1990s.

The Private Finance InitiativeThe Government officially introducedthe PFI in 1992. It allows the private sec-tor to finance large projects, such as theconstruction of new hospitals, prisonsand roads. The Government lays downspecifications for each project, and theprivate sector – usually a consortium ofcompanies each specialising in a particu-lar aspect of the scheme – is responsiblefor the construction and operation of theinfrastructure. A defining feature of PFIprojects is the transfer of at least someoperational risk from the public to theprivate sector.45 As Roe and Craigexplain, this distinguishes PFI from themore nebulous public private partner-ships (PPP), such as LondonUnderground, that are effectively backedby government guarantees and caninvolve less transfer of risk to the privatesector. They add: “PPPs also tend to beso complex as to obscure any hope oftransparency, are difficult to monitorand have confused lines of accountabili-ty.”46

The advantages of PFI projects47

� They provide an alternative fundingsource for infrastructure schemes. Inthe short term, more capital projectscan be undertaken for a given level ofpublic expenditure and therefore theycan be brought on stream earlier.Private organisations may also havegreater scope to make use of innovativefinancial instruments and financingtechniques.

20

43. Albert W, ‘The Turnpike

Trusts’, in Aldcroft D and

Freeman M (eds), Transport in

the Industrial Revolution,

Manchester University Press,

1983

44. Plowden W, op cit., p 193

45. Roe R and Craig A,

Reforming the Private Finance

Initiative, Centre for Policy

Studies, 2004

46. Ibid.

47. See for example, Poole F,

Roads and Private Finance,

Research Paper 97/85, House of

Commons Library, 1997

� Private sector skills and expertise arebrought into the planning and execu-tion of projects.

� The involvement of private businessand a competitive tendering processshould lead to better value for moneyand greater economies of scale.

� Risk can be transferred from the publicto the private sector, so that taxpayersdo not have to contribute when costover-runs occur. The level of paymentsfor the specified service is set out in thecontract and cannot be increased as aresult of unforeseen costs. The PFI cantherefore deliver improved price cer-tainty for government departments.

� Incentive structures can ensure theclose integration of service needs withdesign and construction. The design,construction and maintenance compa-nies that comprise PFI consortiumshave an incentive to work closelytogether to protect their long termfinancial interests.

� The company responsible for buildinginfrastructure is generally responsiblefor its continued long-term operation,increasing the incentive for consor-tiums to take a longer term approach todesign and construction, and thereforeto deliver high standards. There are alsostrong financial incentives to completeprojects on time.

Private finance has been mobilised in manysectors, with varied success. A paper pub-lished by the Institute for Public PolicyResearch suggests that although significantvalue-for-money gains are made in road andprison PFIs, the improvements in schooland hospital PFIs are more questionable.48

The National Audit Office (NAO) foundthat the price ultimately paid by the publicsector exceeded the one agreed at contract in22 per cent of PFI construction projects.49

Although this may sound like a high pro-portion, the figure for projects implement-ed within the public sector was 73 per cent.

Moreover, the increases in PFI price aftercontract generally resulted from latechanges being made to the project specifica-tions, such as the re-categorisation of pris-ons to take more dangerous offenders. Suchchanges would undoubtedly have led toprice increases under the traditional pro-curement process too.

According to the NAO, only 24 per centof PFI projects were delivered late, comparedto 70 per cent within conventional publicsector procurement. The delay was morethan two months in only 8 per cent of thePFI projects surveyed. These figures showthat the PFI has delivered substantialimprovements in reliability. It would alsoappear that most public sector project man-agers have been satisfied with the perform-ance of their PFI-built infrastructure.50

Criticisms of PFIDespite empirical evidence that the PFIoffers significant advantages over conven-tional procurement, several difficultieshave been identified.

� Critics suggest that PFI investment hasnot in fact brought about a significantincrease in the level of investment incapital projects and that the real moti-vation for employing private finance isto remove investment from theGovernment’s balance sheet in theshort term, in effect creating a mort-gage on the public sector. Roe andCraig estimated in 2004 that theGovernment was already committed topay over £110 billion for PFI projectsbetween 2003-04 and 2028-29.51

www.policyexchange.org.uk • 21

Harnessing private finance

48. Maltby P, ‘Public service

reform in the UK: the PFI experi-

ence’, Institute of Public Policy

Research, 2003 www.ippr.org/

articles/index.asp?id=335

49. PFI: Construction

Performance, Report by the

Comptroller and Auditor

General, National Audit Office,

HC 371 Session 2002-2003, 5th

February 2003

50. Ibid.

51. Roe R and Craig A,

op. cit., p iii

“ Risk can be transferred from the public to the private

sector, so that taxpayers do not have to contribute when

cost over-runs occur”

� The case that the PFI offers better valuefor money has also been questioned.52

The transfer of risk to the private sectormeans that projects have faced higherborrowing costs, as financiers havedemanded a risk premium. In contrast,the Government can borrow at very lowrates since repayment – backed by pow-ers to tax and print money – is all butguaranteed. Yet arguably these low ratescan be achieved only by transferringprojects’ financial risks to taxpayers.Cost over-runs on publicly financedprojects involve either higher tax ratesor extra government borrowing. Thenegative economic impact of suchmeasures, as well as the gains in efficien-cy brought about by the PFI, musttherefore be balanced against higherfinancing costs when assessing the valuefor money offered by PFI schemes.

� The tendering process for PFI contractsis said to be far more protracted thantraditional procurement, inflicting riskand cost on the businesses involved.53

This can deter businesses consideringentering the PFI market and under-mine competition and innovation.There is a danger that a handful oflarge operators, with the resources toenter the expensive bidding process,will come to dominate the market.

� PFI projects have been attacked fortheir lack of flexibility.54 Contracts typ-ically set out detailed specifications fora 20 or 30-year period, thereby limitingthe ability of the public sector to makefuture changes and reducing its scope

for innovation. In defence of detailedcontracts, without them the main ben-efits of the PFI could be lost; uncer-tainty could lead to an increased riskpremium on borrowing and reduce thelong-term incentives for high construc-tion standards.

Arguably, the real trouble has been a mis-match between the long-term planningand investment culture of PFI consortiumsand the often short-term politicised natureof the public sector. In the Second Reviewof the Private Finance Initiative, commis-sioned by the Treasury, Sir Malcolm Batesuncovered systemic deficiencies in themanagement of the PFI process including:a failure to prioritise projects on thegrounds of affordability, service need andcommercial viability; poor preparation ofbids; unrealistic risk allocation in con-tracts; late cancellations due to policychanges; and the appointment of preferredbidders either too early or too late – allleading to excessive bid costs, lengthynegotiations and weak competition.55

According to the review, suppliers werenot impressed with public sector procure-ment in general and felt that “departmentswere still overly risk averse and naïve indealing with them”. There was also “dupli-cated activity, poor use of (and wasted)resources, poor value for money togetherwith uncoordinated and unprofessionaldealing with suppliers”.

The review suggested that there wereparticular skill shortages among localauthority officials, few of whom had solidexperience of leading complex PFI negoti-ations with the private sector or in struc-turing the contractual package underlyingPFI deals and resolving issues of risk allo-cation. “To get real value for money, thepublic sector must acquire and retainfamiliarity with the financial products usedto create PFI funding practices.”

Possible solutions to this skills deficitinclude setting up more specialist PFI

Towards better transport

22

52. Ibid., p 7

53. The Future of the Private

Finance Initiative, Social Market

Foundation, 2004, pp 24-25

54. For example, Unison ‘A

Briefing on the Private Finance

Initiative’, 2004 www.unison-

scotland.org.uk/briefings/pfi-

jnov02.html

55. Bates M, Second Review of

the Private Finance Initiative,

HM Treasury, 1999, p 18

“ Arguably, the real trouble has been a mismatch

between the long-term planning and investment culture of

PFI consortiums and the often short-term politicised

nature of the public sector”

units, perhaps based within the main gov-ernment spending departments rather thanthe Treasury, and making greater use ofindependent private sector consultants.

Quoting a Treasury and Cabinet Officereview, Bates wrote that the politicalimportance of many PFI projects hasmeant that officials in both central andlocal government view the procurementprocess as high risk and potentially careerthreatening. The result is responsibilitysharing and decision-making by commit-tee, leading to delays. The institutionaldeficiencies of the public sector, therefore,have contributed to the high costs of thetendering process, which in turn have lim-ited the number of businesses willing toinvest in PFI projects.

Transport and private financeThere is considerable experience of privatefinance within transport. It has been usedin both the construction of roads and ofpublic transport infrastructure.56 The list ofprojects suggests that both PFI and PPPsin general are flexible tools when it comesto the transport sector. PPPs have helpedto fund very large schemes such as themodernisation of London Undergroundlines and small ones such as the provisionof street lighting in local boroughs.Interestingly, they have involved a varietyof public sector partners including theHighways Agency, London Underground,passenger transport executives and localauthorities.

Some projects have been perceived asmore successful than others, both by spe-cialists and the public at large. It is there-fore essential to identify those schemecharacteristics that appear to best facilitatesuccessful private investment. The nextsection examines recent road and publictransport projects that have included a sig-nificant role for private finance, boththrough PFI and more broadly definedPPPs.

Road projectsDBFO road building schemesThe roads constructed as design, build,finance and operate (DBFO) schemesappear to be among the most successfulapplications of the private finance initia-tive. In the basic model, the consortiumconstructs the new road and then receivesrevenues from the Highways Agency, inthe form of shadow tolls for vehicles thatuse it, for the duration of the concession(generally around 30 years). However, incontrast to the situation with a private tollroad, there is a cap on revenues – beyondcertain traffic levels no more shadow tollsare paid. The Highways Agency thereforeavoids the risk that traffic levels will exceedexpectations, while the risk associated withlower than expected traffic levels is borneentirely by the private consortium. Duringthe bidding process and subject to themmeeting certain quality requirements, con-sortiums compete according to the lowestshadow toll rate they will accept from theHighways Agency.

Shadow tolls are used instead of directones because they have negligible adminis-tration costs, do not divert traffic on toparallel minor roads and can easily beapplied to discrete stretches of road, with-out the need for expensive and disruptivetoll booths or the development of alterna-tive charging technology.57

A penalty points system has been usedto encourage DBFO consortiums to pro-vide a good quality service for drivers.Penalties are applied, for example, whenthe road is taken out of service for repairs.

www.policyexchange.org.uk • 23

Harnessing private finance

56. See HM Treasury ‘PFI

Signed Projects List’, www.hm-

treasury.gov.uk/media/3/6/pfi_sig

neddeals_110707.xls

57. See Poole F, op. cit.

“ PPPs have helped to fund very large schemes such

as the modernisation of London Underground lines and

small ones such as the provision of street lighting in local

boroughs”

Variability charges, which make deduc-tions to payments when congestion occurs,may also be used instead of conventionalshadow tolls.

DBFO schemes are said to have resultedin significant cost savings – between 14and 22 per cent for the first eight suchprojects (depending on the discount rateused).58 However, critics have pointed tothe lengthy, bureaucratic and expensivebidding process. Also, DBFO consortiumshave a vested interest in ensuring a highlevel of road use in order to extract theirmaximum revenue from the shadow tolls(these incentives have been modified to adegree in contracts) and thus cannot, it isargued, be involved fully in a wider trans-port strategy. Contractual arrangementslargely insulate DBFO schemes fromdirect political interference, though thosecommitted to a more top-down model oftransport policy consider this a disadvan-tage. Consortiums still face a degree ofpolitical risk, however. For example, theintroduction of a national road pricingscheme could significantly affect their rev-enues, as could a variety of local transportmeasures.

The M6 TollWith the exception of a small number oftoll bridges, the M6 Toll was the UK’s firstsection of tolled motorway. Designed toalleviate the increasing congestion on theM6 through Birmingham, it connects M6Junction 4, near the National ExhibitionCentre, to M6 Junction 11A north ofWolverhampton with 43km of three-lanemotorway. This, the busiest section of theM6, was previously carrying up to two-and-a-half times as many vehicles per dayas it was designed for.

A private sector company, MidlandExpressway Ltd (MEL), won the 53-yearconcession to build and operate the M6Toll (allowing three years for constructionand fifty for operation). It was to carry outthe design, construction, financing, opera-

tion and maintenance of the road at itsown cost and risk, without recourse to gov-ernment funds or guarantees. A consor-tium of big contractors (Carillion,McAlpine, Balfour Beatty and AMEC)began work in mid-2002 and the road wasopened one month ahead of schedule, inDecember 2003.

MEL was to recoup its costs by collect-ing tolls, which it was entirely free to set.The only cost to government of the M6Toll road was an £18 million contributiontowards rebuilding part of the connectingM42. The motorway cost £485 million tobuild, although Macquarie InfrastructureGroup, the Australian company thatacquired MEL in 2005, put the total proj-ect cost at £900 million. The discrepancyin part reflected high financing costs at thestart of the project related to the politicalrisk that final permission to build the roadwould not be granted, as well as risk asso-ciated with the untested nature of such aproject in the UK.59

MEL reported an operating profit ofaround £16 million in 2005.60 Total rev-enue was £45 million, with staff and otheroperating costs amounting to £11.4 mil-lion and depreciation of £17.4 million.Taking into account net interest costs ofaround £43 million, this left an overall lossof £26.5 million in 2005 – its first fullfinancial year. At this stage long term debtwas £819 million. Since then tolls havebeen raised, interest repayments have beenreduced through refinancing and a numberof large developments, including distribu-tion centres, have been attracted to thevicinity of the route. It is plausible, there-fore, that the motorway will return a prof-it in the medium term.

Although the M6 Toll, in Macquarie’sown description, remains a “premiumquality road that was delivered on budget,ahead of schedule and with minimum useof taxpayer’s funds”,61 it is still too early tojudge its commercial success. A number offactors have contributed to this outcome.

Towards better transport

24

58. Haynes L and Roden N,

‘Commercialising the

Management and Maintenance

of Trunk Roads in the United

Kingdom’, Transportation, 26,

pp 31-54, 1999

59. Private communication

60. Midland Expressway Ltd,

interim financial statements

(unaudited) for the six months

ended 31st December 2005,

www.macquarie.com.au/au/mig/

acrobat/m6toll_financials_end-

dec05.pdf

61. Evidence given by

Macquarie to the Parliamentary

Select Committee on Transport

Road Pricing: The Next Steps,

Seventh Report of Session

2004-5, Volume 1

First there are competing toll-freeroutes, above all the existing M6. Secondly,goods vehicles were originally envisaged tobe a major source of revenue but manyhaulage companies have boycotted the tollroad. Hauliers often charge a fixed rate fora delivery and, given their competitive,low-margin industry, the tolls dent theirprofits – especially where the speed ofdelivery is of low importance.

Thirdly, traffic predictions were over-optimistic: MEL never published its fore-cast traffic volumes, but estimates made bytransport consultants Steer Davies Gleavegroup suggested that about 70,000 vehiclesper day would be using the road within ayear of opening, and 80,000 after threeyears.62 In fact just over three months afteropening, average traffic flows were about47,000 vehicles on a weekday (invariablybusier than weekends), and after a yearthey were still below 50,000 vehicles perweekday.63 Time savings were also over-optimistic. A survey conducted beforecompletion of the road estimated thatusing the new M6 Toll could reduce jour-ney times by up to 45 minutes, howeverthe maximum time saved has been around30 minutes.64 Comparing journey times onthe M6 Toll and on the M6 before theproject opened, average weekday journeytimes are seven minutes shorter south-bound and twelve minutes shorter north-bound. Time savings are not nearly as bigas expected, which may also help to explainwhy traffic has been below the levels fore-cast during the planning stage.

Finally, financing costs were high, bothbecause of the unique nature of the projectand because the consortium had to bearthe planning risk: a significant proportionof the total cost was spent before the con-sortium knew that the project would begranted permission to proceed.

Notwithstanding the project’s disap-pointing financial performance so far, fur-ther criticisms have focused on the Gover-nment’s lack of regulatory power over the

route. Providing certain standards are met,MEL is able to operate the M6 Toll as anentirely independent stretch of road. TheParliamentary Select Committee onTransport has pointed out that, until 2054,the Government’s policies, such as nation-al road pricing, high occupancy vehiclelanes and active traffic management canonly be applied to the M6 Toll road withthe co-operation of the operators. (Theseissues could be resolved by legislation,renegotiation or compensation, or a com-bination of all three.)

Some have suggested that because MELcurrently has an incentive to maximise rev-enue rather than minimise overall conges-tion, a toll-free route – a shadow tollscheme or even a conventionally procuredmotorway – would have made a far greatercontribution to reducing congestion in theM6 corridor and have produced greateroverall benefits for the economy.

Public transport schemesPrivate finance in public transport schemeshas been more controversial than in roadprojects. It has often been characterised bysevere financial problems and persistentcontractual disputes with the commission-ing bodies. Such projects tend to remaindependent on government subsidies andare therefore vulnerable to political risks;they also have to contend with ideologicalopposition to private sector involvementfrom traditionalist public transport admin-istrations. Important lessons can howeverstill be drawn from recent public transport

www.policyexchange.org.uk • 25

Harnessing private finance

62. ‘M6 Toll Birmingham opens

end-2005’, Toll Roads News,

15th July 2003

63. Post Opening Project

Evaluation: M6 Toll One Year

After Study, Highways Agency,

2005

64. Road Pricing: The Next

Steps, Seventh Report of the

Transport Select Committee,

Session 2004-2005

“ DBFO schemes are said to have resulted in

significant cost savings – between 14 and 22 per cent

for the first eight such projects (depending on the

discount rate used)”

projects in terms of funding, contractualarrangements and the limitation of politi-cal risk.

Croydon TramlinkIn 1996 Tramtrack Croydon Ltd (TCL)won a 99-year contract to build and runTramlink (99 years was considered suffi-cient time to enable the private sector toview it as a long-term business rather thana limited period concession). The projectcost £205 million to construct andopened in May 2000. More than half thecapital cost (£125m) was provided as agrant by central government.65 The con-tract was signed by London Transport butin July 2000 its successor body, Transportfor London (TfL) was given responsibili-ty for setting tram and bus fares acrossLondon.

The predicted passenger numbers were20 million a year after 18 months of opera-tion and 25 million a year when the systemreached maturity after five years, but inreality passenger numbers fell about 2 mil-lion short of these figures.66 Having takenon revenue risk the consortium initiallystruggled to cover operating costs, let alonecapital repayments, despite the Govern-ment subsidy for construction costs.

According to TCL one of the main rea-sons for the shortfall in patronage wasTransport for London’s policy of expand-ing bus services in direct competition totram routes.67 The level of bus mileageoperated in Croydon is currently 32 percent higher than at the time when the con-cession was granted, with some routes run-ning directly parallel to trams. Secondly,bus fares on competing routes were origi-nally set at a rate 20-30 per cent lower thantram fares. The company took TfL to courtclaiming that the lower bus fares and com-peting services had lost TCL up to 8 mil-lion passengers and therefore substantialrevenue. The court decided that TCL wasowed compensation. When fares were har-monised in 2004 there was an immediate

12 per cent increase in passengers using thetrams.

TCL made an operating profit of around£2.5 million in the year to March 2005 butits interest payments amounted to £8.3 mil-lion.68 Tramlink now relies heavily on pay-ments from TfL (£5.8 million in 2004-05)to compensate for the introduction of lowerbus fares, competing bus services andOyster cards, as well as to cover conces-sionary fares. The scheme is considered tohave been a far greater financial failurethan the M6 Toll because taxpayers haveeffectively had to subsidise both the con-struction and operation of the route. Morepositively, the use of private financeensured that construction cost over-runsdid not burden the taxpayer. Moreover,the contract was also robust enough todeal with much of the associated politicalrisk and to ensure that insolvency wasavoided.