top accounting and auditing issues for 2019 | cpe...

TRANSCRIPT

Top Accounting and Auditing Issues for 201 9 | CPE COURSE

Top Accounting and Auditing Issues for 2019 CPE COURSE

BONUS CPE COURSE! Earn CPE Credit and stay on top of key accounting and auditing issues. Go to CCHCPELink.com/printcpe

Top Accounting andAuditing Issuesfor 2019 ⏐ CPE Course

Patrick Patterson, CPAKelen Camehl, CPA Scott Taub, CPA

Contributors

Contributing Editor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Patrick Patterson, CPA

Kelen Camehl, CPA

Technical Review . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Kelen Camehl, CPA

Lorraine Zecca, CPA

Production Coordinator . . . . . . . . . . . . . . Mariela de la Torre; Jennifer Schencker;

Vijayalakshmi Suresh

Production . . . . . . . . . . . . . . . . . . . . . . . . . . Sharon Sofinski; Anbarasu Anbumani

This publication is designed to provide accurate and authoritative information in regard to the subject matter covered. It is sold with the understanding that the publisher is not engaged in rendering legal, accounting, or other professional service. If legal advice or other expert assistance is required, the services of a competent professional person should be sought.

© 2018 CCH Incorporated and its affiliates. All rights reserved.2700 Lake Cook RoadRiverwoods, IL 60015800 344 3734CCHCPELink.com

No claim is made to original government works; however, within this Product or Publication, the following are subject to CCH Incorporated’s copyright: (1) the gathering, compilation, and arrangement of such government materials; (2) the magnetic translation and digital conversion of data, if applicable; (3) the historical, statutory and other notes and references; and (4) the commentary and other materials.

iii

IntroductionTop Accounting and Auditing Issues for 2019 CPE Course helps CPAs stay abreast of the mostsignificant new accounting and auditing standards and important projects. It does so byidentifying the events of the past year that have developed into hot issues and reviewing theopportunities and pitfalls presented by these changes. The topics reviewed in this coursewere selected because of their impact on financial reporting and because of the role they playin understanding the accounting landscape in the year ahead.

Module 1 of this course reviews top accounting issues.

Chapter 1 explores the effects of the Tax Cuts and Jobs Act on financial reporting issues.

Chapter 2 discusses the latest developments from the Financial Accounting StandardsBoard (FASB) regarding lease accounting.

Chapter 3 provides an overview of the new revenue recognition standard, AccountingStandards Codification (ASC) Topic 606, Revenue from Contracts with Customers. It explainsthe principles that underlie the new model for revenue recognition and highlights thoseareas that represent the most significant changes between current guidance and the newrequirements.

Chapter 4 discusses the latest releases from the Financial Accounting Standards Board(FASB). Selected accounting standards are highlighted, and the FASB agenda and futurechallenges for the accounting and auditing profession are also discussed.

Chapter 5 discusses the current expected credit loss (CECL) model for losses and/orimpairments as presented in Financial Accounting Standards Board (FASB) AccountingStandards Update (ASU) 2016-13. It also gives an overview of ASU 2016-01, which includessignificant changes in authoritative professional standards concerning financial instruments(financial assets and financial liabilities) and their measurements, impairments, anddisclosures.

Module 2 of this course reviews top auditing issues.

Chapter 6 discusses key information related to Regulation S-K with a particular focus onthe more frequently used sections of the regulation.

Chapter 7 discusses significant changes in the authoritative professional standardsconcerning audit reporting in the area of forming an opinion and reporting on financialstatements. It also identifies future changes to auditor reporting.

Chapter 8 provides an overview of selected preparation, compilation, and review stan-dards and discusses new Statements on Standards for Accounting and Review Services(SSARS) 24, Omnibus Statement on Standards for Accounting and Review Services—2018.

Study Questions. Throughout the course you will find Study Questions to help you testyour knowledge, and comments that are vital to understanding a particular strategy or idea.Answers to the Study Questions with feedback on both correct and incorrect responses areprovided in a special section beginning at ¶10,100.

Final Exam. This course is divided into two Modules. Take your time and review all courseModules. When you feel confident that you thoroughly understand the material, turn to theFinal Exam. Complete one or both Final Exams for continuing professional education credit.

Go to cchcpelink.com/printcpe to complete your Final Exam online for immediate results.My Dashboard provides convenient storage for your CPE course Certificates. Furtherinformation is provided in the CPE Final Exam instructions at ¶10,200. Please note,

iv

manual grading is no longer available for Top Accounting and Auditing Issues. Allanswer sheets must be submitted online for grading and processing.

August 2018

PLEDGE TO QUALITY

Thank you for choosing this CCH® CPELink product. We will continue to produce highquality products that challenge your intellect and give you the best option for your Continu-ing Education requirements. Should you have a concern about this or any other WoltersKluwer product, please call our Customer Service Department at 1-800-344-3734.

COURSE OBJECTIVES

This course provides an overview of important accounting and auditing developments. At thecompletion of this course, the reader will be able to:

• Recognize how the Tax Cuts and Jobs Act affects financial reporting

• Identify the act’s changes to domestic income provisions

• Differentiate requirements for adjustments to deferred tax liabilities and assets for theeffect of a change in tax laws or rates

• Summarize how the act affects the taxation of foreign income

• Identify the FASB pronouncements that may impact entities with leases or that expectto have or enter into leases

• Recognize the major updates to the new Accounting Standards Codifications as pre-scribed by ASU 2016-02

• Understand best practices for starting a lease accounting project under the newstandards

• Understand the principles of ASC Topic 606, Revenue from Contracts with Customers

• Identify the five steps in the new revenue recognition model

• Address key issues in implementing the provisions of ASC Topic 606

• Describe required disclosures for private companies with respect to revenuerecognition

• Identify transition considerations as they relate to business practices

• Identify the latest issuances from the FASB

• Recognize the benefits of the FASB’s proactive outreach with stakeholders

• Summarize the latest implementation guidance for major accounting standards

• Recognize FASB guidance and challenges to expect in the near future

• Recognize the main objectives of ASU 2016-01 and ASU 2016-13

• Identify the steps for implementing the CECL model

• Identify ASU 2016-01 and ASU 2016-13 effective dates, reporting requirements, disclo-sure requirements, and related matters

• Identify key history as it relates to Regulation S-K

• Understand requirements of Regulation S-K that are applicable to common SEC forms

• Identify some of the key guidance throughout Regulation S-K

• Recognize current developments related to Regulation S-K

v

• Understand selected new auditor reporting models

• Identify key audit matters in the independent auditor’s report

• Recognize the new form and content of modifications to the opinion in the independentauditor’s report

• Identify anticipated changes to auditor reporting

• Identify the requirements of revised SSARS 21, 22, and 23

• Recognize the revised compilation and review report requirements of SSARS 24

Additional copies of this course may be downloaded from cchcpelink.com/printcpe.Printed copies of the course are available for $2.99 by calling 1-800-344-3734 (ask for product10024493-0006).

vii

Contents

MODULE 1: TOP ACCOUNTING ISSUES1 Accounting for the Tax Cuts and Jobs Act

Welcome . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶101Learning Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶102Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶103Overview of Changes: Domestic Income . . . . . . . . . . . . . . . . . . ¶104Overview of Changes: Foreign Earnings . . . . . . . . . . . . . . . . . . . ¶105

2 Leases and Impacts: Change to Changes 2018Welcome . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶201Learning Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶202Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶203Five Major Changes to Leases . . . . . . . . . . . . . . . . . . . . . . . . . ¶204ASU 2016-02 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶205Starting A Lease Accounting Implementation Project . . . . . . . . . . ¶206

3 New Revenue Recognition StandardWelcome . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶301Learning Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶302Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶303Five Steps to Revenue Recognition . . . . . . . . . . . . . . . . . . . . . . ¶304Other Items . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶305Contract Costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶306Presentation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶307Disclosures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶308Transition Considerations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶309Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶310

4 FASB OutlookWelcome . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶401Learning Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶402Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶403Implementing New Accounting Standards . . . . . . . . . . . . . . . . . ¶404Conducting Outreach with Stakeholders . . . . . . . . . . . . . . . . . . . ¶405Transition Resource Group . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶406Implementation Guidance for Major Standards . . . . . . . . . . . . . . ¶407Future Guidance and Challenges Ahead . . . . . . . . . . . . . . . . . . ¶408

5 CECL ModelWelcome . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶501Learning Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶502Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶503ASU 2016-01 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶504ASU 2016-13 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶505

viii

MODULE 2: TOP AUDITING ISSUES6 Regulation S-K

Welcome . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶601Learning Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶602Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶603Form S-1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶604Form 10-Q . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶605Form 8-K . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶606Subpart 229.1: General . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶607Subpart 229.100: Business . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶608Subpart 229.200: Securities of the Registrant . . . . . . . . . . . . . . . ¶609Subpart 229.300: Financial Information . . . . . . . . . . . . . . . . . . . ¶610Subpart 229.400: Management and Certain Security Holders . . . . ¶611Subpart 229.500: Registration Statement and ProspectusProvisions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶612Subpart 229.600: Exhibits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶613Other Key Parts of Regulation S-K . . . . . . . . . . . . . . . . . . . . . . . ¶614Recent Developments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶615

7 Auditor Reporting ModelsWelcome . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶701Learning Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶702Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶703Proposed Changes in Auditor Reporting . . . . . . . . . . . . . . . . . . . ¶704Other Projects Related to Auditor Reporting . . . . . . . . . . . . . . . . ¶705Significant Proposed Amendments to Existing Auditor ReportingStandards . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶706Illustrations of Auditor’s Reports on Financial Statements . . . . . . . ¶707Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶708

8 SSARS 24Welcome . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶801Learning Objectives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶802SSARS 21, SSARS 22, and SSARS 23 . . . . . . . . . . . . . . . . . . . ¶803SSARS 24 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶804Illustrations of Accountant’s Compilation and Review Reports onFinancial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶805

Answers to Study Questions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶10,100Module 1—Chapter 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶10,101Module 1—Chapter 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶10,102Module 1—Chapter 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶10,103Module 1—Chapter 4 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶10,104Module 1—Chapter 5 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶10,105Module 2—Chapter 6 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶10,106Module 2—Chapter 7 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶10,107Module 2—Chapter 8 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶10,108

ix

Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Page143

Final Exam Instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶10,200Final Exam Questions: Module 1 . . . . . . . . . . . . . . . . . . . . . . . . ¶10,301Final Exam Questions: Module 2 . . . . . . . . . . . . . . . . . . . . . . . . ¶10,302

Answer Sheets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶10,400Module 1 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶10,401Module 2 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶10,402

Evaluation Form . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ¶10,500

1

MODULE 1: TOP ACCOUNTING ISSUES—CHAPTER 1: Accounting for the Tax Cuts andJobs Act¶101 WELCOMEThis chapter explores the effects of the Tax Cuts and Jobs Act on financial reportingissues.

¶102 LEARNING OBJECTIVES

Upon completion of this chapter, you will be able to:

• Recognize how the Tax Cuts and Jobs Act affects financial reporting

• Identify the Act’s changes to domestic income provisions

• Differentiate requirements for adjustments to deferred tax liabilities and assetsfor the effect of a change in tax laws or rates

• Summarize how the Act affects the taxation of foreign income

¶103 INTRODUCTIONOn December 22, 2017, H.R. 1, An Act to Provide for Reconciliation Pursuant to Titles IIand V of the Concurrent Resolution on the Budget for Fiscal Year 2018 (the Tax Cutsand Jobs Act), was signed into law. U.S. generally accepted accounting principles(GAAP) requires that the pervasive changes resulting from the Act must be accountedfor in the period that includes the enactment date. Financial statements will be signifi-cantly affected as companies adjust their deferred tax balances, valuation allowances,tax planning strategies, and income tax expense.

In addition to questions and answers (Q&As) on several aspects of the Act, theFinancial Accounting Standards Board (FASB) has issued a new standard on incometaxes recorded in accumulated other comprehensive income. The FASB’s guidanceapplies equally to public and private companies. The U.S. Securities and ExchangeCommission (SEC) staff and FASB staff have provided public and private companieswith some relief by allowing up to a year to finalize financial statement adjustmentsarising from the tax law changes.

This chapter addresses FASB staff guidance and other accounting questionsrelated to provisions of the Act. It presents very condensed summaries of changesbrought about by new tax law. In no case should these condensed summaries besubstituted for a full reading of the new law, nor should they be used to make tax oraccounting decisions. Given the complexity and timing of the new law, consultation withknowledgeable tax professionals should be considered when determining the effect ofthe tax law changes on a company’s tax situation.

¶104 OVERVIEW OF CHANGES: DOMESTIC INCOMEThe U.S. federal tax law changes resulting from the Act affect companies in allindustries, regardless of whether they are large or small, domestic or multinational,publicly traded or privately held. Changes to domestic income provisions may be lesscomplex for many companies, but the effects are still likely to be significant, both in

¶104

2 TOP ACCOUNTING AND AUDITING ISSUES FOR 2019 CPE COURSE

terms of the amount of taxes paid as well as the measurement of deferred taxes on thebalance sheet.

Changes in corporate tax rules affecting the taxation of domestic income rangefrom the headliners that make front-page news, such as reducing corporate income taxrates and eliminating the alternative minimum tax, to the extras that are in the fineprint, such as limiting deductions for interest expense and disallowing all entertainmentexpenses. Although not every company is affected by every change, there is somethingfor everyone in this law.

Examples of changes in the domestic provisions of corporate tax law include thefollowing:

• Reducing the corporate income tax rate from 35 percent to 21 percent, effectiveJanuary 1, 2018. In the transition, blended rates apply to companies with fiscalyear-ends.

• Eliminating the corporate alternative minimum tax (AMT). Existing AMT cred-its can be used or refunded in the future.

• Eliminating the two-year carryback period and making indefinite the carryfor-ward period for a net operating loss (NOL). However, unlike prior law, NOLcarryforwards are now limited to 80 percent of taxable income for the year.

• Allowing the full expensing of the cost of qualified property in the year it isplaced in service. This provision phases out beginning in 2023.

• Modifying the tax deductibility of certain types of compensation to highly paidemployees. The new law expands the limitation to include more companies andpotentially more employees. In addition, commissions and performance-basedcompensation are no longer excluded from the computation of the employee’scompensation that is subject to the limitation.

• Limiting the deduction for net interest expense. While smaller companies areexempt from this provision, the net interest expense deduction for other compa-nies is limited to 30 percent of adjusted taxable income.

• Disallowing the deduction of 100 percent of entertainment expenses. Underprior law, the deduction of qualifying entertainment expenses was limited to 50percent. The new rule is effective for expenses incurred or paid after December31, 2017. Meals continue to be 50 percent deductible.

STUDY QUESTIONS

1. The domestic provisions of the Tax Cuts and Jobs Act:

a. Allow organizations to deduct 100 percent of entertainment expenses

b. Retain the two-year carryback period for net operating losses

c. Retain the corporate alternative minimum tax

d. Reduce the corporate income tax rate

2. Which of the following statements is true regarding tax law changes resulting fromthe Act?

a. The changes will impact all industries.

b. The changes specifically target certain financial services entities.

c. The changes will affect only companies that have more than 1,000 employees.

d. The changes will affect privately held companies only.

¶104

3MODULE 1 - CHAPTER 1 - Accounting for the Tax Cuts and Jobs Act

Accounting for Income Taxes (ASC Topic 740)U.S. GAAP requires recording an income tax provision not only for taxes that are due asa result of the current year’s taxable income (“current tax expense or benefit�), but alsofor the future tax consequences of transactions that have been reported in the financialstatements or tax returns (“deferred tax expense or benefit.�)

The future tax consequences are recorded based on tax law enacted at the date ofthe financial statements. Therefore, deferred tax assets and liabilities are recorded onthe balance sheet at the corporate tax rate in effect at the balance sheet date (e.g., 35percent at November 30, 2017). Changes in tax law cannot be anticipated, regardless ofthe likelihood of the change being signed into law.

The most common examples of items that give rise to deferred tax liabilities aredepreciation of buildings, machinery, and equipment and the amortization of intangibleassets. The costs of those assets generally are expensed more rapidly for tax purposesthan for U.S. GAAP purposes, creating a basis difference in the asset.

Typical examples of items that lead to deferred tax assets include accrued ex-penses and allowances for bad debts. For these items, U.S. GAAP expense oftenexceeds the amount that is deductible in the current year’s tax return under the taxrules, also creating a basis difference in the asset or liability.

These differences between the amounts reported for tax purposes and U.S. GAAPpurposes, whether they create deferred tax assets or liabilities, are referred to in theaccounting literature as “temporary differences.� By contrast, a transaction reported inthe financial statements that is never deductible (or taxable) for income tax purposes iscommonly called a “permanent difference.� Permanent differences create an effectivetax rate that differs from the statutory rate.

U.S. GAAP requires that all companies, both public and private, recognize theeffects of tax law changes on the date of enactment. Such effects are charged to incomeas part of the income tax expense or benefit for the period. Companies will record theconsequences of the Act on their deferred tax balances (as well as any effect on currenttax expense) in the income statement for the reporting period that includes December22, 2017.

Recent FASB GuidanceThe FASB staff has issued five Q&A documents that address a number of implementa-tion issues raised by companies as a result of the new tax law. Those five Q&Asaddress:

• Whether private companies can follow SEC staff guidance on the measurementperiod for tax adjustments

• Whether to discount AMT credits that become refundable

• Whether to discount the one-time transition liability related to certain foreignearnings

• How to account for the base erosion anti-abuse tax (BEAT)

• How to account to the effects of the global intangible low-taxed income (GILTI)provisions of the Act

In addition, the FASB issued a standard to address stranded tax effects embeddedin accumulated other comprehensive income. While the topic is very narrow and has noeffect on reported income, this issue is particularly important to financial institutionsbecause of the effect on regulatory capital.

¶104

4 TOP ACCOUNTING AND AUDITING ISSUES FOR 2019 CPE COURSE

The following Q&As address the accounting and financial reporting changesresulting from the Act and the relevant guidance provided by the FASB.

STUDY QUESTION

3. Under the new Act, deferred tax liabilities are recorded on the balance sheet atwhich rate?

a. 35 percent

b. 21 percent

c. The corporate tax rate in effect at the balance sheet date

d. The corporate tax rate in effect on December 22, 2017

Q&AsCorporate tax rate. Under the Act, the corporate tax rate is reduced from 35 percent toa flat rate of 21 percent. The new rate is effective January 1, 2018. For companies withfiscal year-ends, a blended rate applies to the fiscal year that includes the effective dateof the change in tax rates.

EXAMPLE: A company with a June 30 year-end would apply a blended rate of28 percent (six months at 35 percent and six months at 21 percent) to its taxableincome for the fiscal year ending June 30, 2018. Subsequent fiscal years’ incomewill be taxed at the 21 percent rate.

Remeasurement of deferred tax assets and liabilitiesQuestion: How does the change in tax rate affect existing deferred tax balances for acompany with a December 31, 2017 year-end?

Answer: Deferred tax assets and liabilities for temporary differences as of the enact-ment date that are expected to reverse after January 1, 2018 should be remeasured at 21percent. The debit or credit resulting from that remeasurement is reported in incomefor the fourth quarter of 2017. Any deferred taxes for temporary differences that areexpected to reverse in 2017 should continue to be measured at the old tax rate (i.e., therate in effect for the 2017 tax return). For example, a temporary difference for a bonusaccrual that resulted in a deferred tax asset at December 31, 2016 and is expected toreverse in 2017 would continue to be measured at 35 percent.

Question: How does the change in tax rate affect existing deferred tax balances for acompany with a fiscal year-end?

Answer: Deferred tax assets and liabilities for temporary differences as of the enact-ment date that are expected to reverse in the current fiscal year should be remeasuredat the blended rate that applies to that year’s tax return. If a temporary difference isexpected to reverse in subsequent years, the existing deferred tax should beremeasured at 21 percent. The remeasurement adjustments are reported in income forperiod that includes December 22, 2017 (enactment date).

EXAMPLE: Company A has a June 30 year-end. In its second quarter endedDecember 31, 2017, it remeasures the deferred taxes for temporary differences asof the enactment date that are expected to reverse in its June 30, 2018 tax return atthat fiscal year’s blended rate of 28 percent. The deferred taxes for temporarydifferences that will reverse after June 30, 2018 are remeasured at 21 percent.

¶104

5MODULE 1 - CHAPTER 1 - Accounting for the Tax Cuts and Jobs Act

If Company A has an existing deferred tax for a temporary difference that willreverse and be replaced by a new, similar temporary difference, the existingdeferred tax at the enactment date should be remeasured at the 28 percentblended rate. The deferred tax for the new (replacement) temporary difference ismeasured at 21 percent. An example would be Company A’s temporary differencefor a bonus accrual at June 30, 2017 that will reverse in fiscal 2018. The deferredtax asset for that temporary difference was initially recorded at 35 percent. In thesecond quarter of fiscal 2018, the deferred tax asset for that temporary difference isremeasured at 28 percent. When the new temporary difference for the fiscal 2018bonus accrual is recorded, it will be measured at 21 percent.

Question: Do carryforwards need to be remeasured at the new corporate tax rate?

Answer: Income tax credit carryforwards such as R&D and AMT do not represent taxdeductions. For that reason, they are not affected by the change in corporate tax rates.In contrast, NOL carryforwards are used to reduce taxable income in a future periodand thus should be measured at the new rate of 21 percent.

Setting aside tax rates, the Act makes important changes to AMT and NOLcarryforwards that must be considered in determining what adjustments are necessaryto the deferred tax assets generated by those items. Those considerations are discussedfurther later in this chapter.

Income statement classificationQuestion: Where is the adjustment to remeasure deferred tax assets and liabilitiesreported?

Answer: Under U.S. GAAP, the adjustment to remeasure deferred tax assets andliabilities as a result of a change in tax law is reported in income from continuingoperations as part of income tax expense in the period in which the new law is enacted.

Question: As mentioned earlier, adjustments to remeasure deferred tax assets andliabilities are included in income tax expense within income from continuing operations.But what if some of the deferred tax balances being adjusted to the new tax rate arerelated to discontinued operations, other comprehensive income, or items charged orcredited directly to equity?

Answer: The answer is still the same: adjustments arising from a change in tax law areincluded in income tax expense within income from continuing operations. It does notmatter where the item was initially recorded in the financial statements. U.S. GAAPdoes not require or permit “backwards tracing.� Irrespective of the initial classificationof the item that gave rise to the deferred tax asset or liability, the effects of changes intax law are recorded in income from continuing operations.

For example, a company may have recognized deferred tax benefits or deferred taxexpense through other comprehensive income (OCI). The effect of the tax rate changeon those deferred taxes is recognized in income tax expense from continuingoperations.

Question: Adjustments to remeasure deferred tax assets and liabilities are included inincome tax expense within income from continuing operations. But what about deferredtaxes recognized through goodwill due to an acquisition earlier in the year? Can theremeasurement of acquisition related deferred taxes based on the new corporate taxrate be made through an adjustment to goodwill?

Answer: No.

Question: U.S. GAAP requires all the effects of changes in tax laws or rates on deferredtax assets and liabilities to be recorded in income from continuing operations. No

¶104

6 TOP ACCOUNTING AND AUDITING ISSUES FOR 2019 CPE COURSE

“backwards tracing� is allowed, even for the tax effects of items that were originallyrecognized in other comprehensive income.

However, the result is that the tax effects of items within accumulated othercomprehensive income (AOCI) do not reflect the appropriate tax rate. The differentialbetween the old and new tax rates is effectively stranded in accumulated other compre-hensive income and will almost never be reclassified into retained earnings. This couldbe confusing to investors. But more importantly, this accounting could significantlyaffect the regulatory capital of certain banks. Has the FASB addressed this issue?

Answer: Yes, but only as it applies to the tax effects of the Act. On February 14, 2018,the FASB issued Accounting Standards Update No. 2018-02—Income Statement—Re-porting Comprehensive Income (Topic 220)—Reclassification of Certain Tax Effects fromAccumulated Other Comprehensive Income (ASU 2018-02). ASU 2018-02 permits, butdoes not require, companies to reclassify stranded tax effects arising from the Act fromaccumulated other comprehensive income to retained earnings. This is a narrow-scopestandard and does not address the broader question of “backwards tracing.�

Under ASU 2018-02, the amount reclassified should include the effect of the changein the federal corporate income tax rate related to items remaining in accumulated othercomprehensive income. Because the standard does not specify what constitutes astranded tax effect, a company has the flexibility to determine what other stranded taxeffects resulted from the Act. Thus a company can reclassify other income tax effects(beyond the effect of the change in the federal corporate tax rate) of the Act on itemsremaining in accumulated other comprehensive income along with disclosure of thosereclassified effects.

The standard does not permit reclassification of the effect of the change in thefederal corporate income tax rate on gross valuation allowances that were originallycharged to income from continuing operations. It also does not permit reclassification ofthe stranded tax effects within accumulated other comprehensive income to retainedearnings for previous changes to other tax rates such as state and local tax rates and forall future tax rate changes.

Disclosure is required for:

• The company’s accounting policy for releasing income tax effects from AOCI(e.g., the portfolio approach or the security-by-security approach);

• Whether the company elected to reclassify to retained earnings from AOCI thestranded income tax effects from the Act; and

• Information about the income tax effects other than the change in the corporatetax rate that are reclassified.

ASU 2018-02 applies to public and private companies in all industries. It is effectivefor fiscal years beginning after December 15, 2018, and interim periods within thoseyears. Early adoption is permitted for financial statements that have not yet been issued.Companies can apply the new standard in the period of adoption or retrospectively toeach period (or periods) in which the effect of the change in corporate tax rates underthe Act is recognized.

The Exposure Draft issued by the FASB in January would have required allcompanies to reclassify stranded tax effects. However, the FASB received feedbackindicating that the cost and complexity of determining the amount to be reclassifiedwould exceed the benefit for some companies. For this reason, the final standardpermits, but does not require, reclassification.

¶104

7MODULE 1 - CHAPTER 1 - Accounting for the Tax Cuts and Jobs Act

STUDY QUESTIONS

4. The five Q&A documents released by the FASB cover all of the following topicsexcept:

a. The measurement period for tax adjustments

b. Stranded tax effects

c. AMT credits

d. The base erosion anti-abuse tax

5. Which of the following statements about ASU 2018-02 is true?

a. It requires that companies reclassify stranded tax effects.

b. It applies to public companies only.

c. It is effective for fiscal years beginning after December 15, 2018.

d. Companies must apply ASU 2018-02 prospectively.

Interim accounting by fiscal year-end companiesQuestion: Under U.S. GAAP, interim tax expense is based on the company’s estimateof its annual effective tax rate for the year. For a fiscal year-end company, should theeffect of the tax rate change on deferred tax assets and liabilities be included as part ofthe annual effective tax rate estimate?

Answer: No. The effect of the tax rate change on deferred taxes represents a discreteitem. In other words, the adjustment to reflect the effect of the change in tax rates ondeferred tax assets and liabilities is recognized in the period of enactment and shouldnot be allocated to later quarters via the annual effective tax rate.

EXAMPLE: Company X, which has a June 30 fiscal year-end, has net deferredtax assets and determines that the net effect of the tax law change on its deferredtaxes is a charge (debit) to income of $200,000. The full amount of that charge isrecorded in income tax expense in the second quarter ended December 31, 2017(i.e., the period that includes the enactment date) and does not affect the computa-tion of Company X’s estimated annual effective tax rate.

Question: The previous question discussed the effect of the tax rate change ondeferred taxes for a company with a fiscal year-end. But the Act also changes the taxrate for the current year by creating blended tax rates for non–calendar year corporatetaxpayers. For a fiscal year-end company, should the reduction in corporate tax rateseffective January 1, 2018, be considered in estimating the annual effective tax rate?

Answer: Yes. U.S. GAAP includes an example of this fact pattern. As a refresher, tocompute income tax expense in an interim period, the company must first estimate theeffective tax rate that will be applicable for the full fiscal year. To make that estimate,each quarter the company considers the applicable statutory tax rate(s) and its bestestimate of tax credits, capital gains rates and usual transactions that have no taxconsequences (typically referred to as “permanent differences.�) The interim tax provi-sion is computed by multiplying the estimated annual effective tax rate against year-to-date pretax income and subtracting income tax expense previously reported. Taxexpense is trued up at the end of the year when the company computes its current anddeferred tax expense following the method described in Subtopic 740-10.

In other words, a company’s estimate of its annual effective tax rate necessarilyconsiders the statutory tax rate for the current year. Therefore, a company with a fiscal

¶104

8 TOP ACCOUNTING AND AUDITING ISSUES FOR 2019 CPE COURSE

year-end will factor the company’s lower, blended tax rate into its estimate when makingits quarterly tax computation for the interim period that includes the enactment date.

EXAMPLE: Company Y has a fiscal year end of June 30. In its first quarterended September 30, 2017, Company Y recorded tax expense of $140,000 based onpretax income of $400,000 and an estimated annual effective tax rate of 35 percent.Pretax income for the six months ending December 31, 2017 is $800,000. Using itsestimated annual effective tax rate of 28 percent as of the end of its second quarter,Company Y will report income tax expense for the quarter is $84,000 ($800,000 x28 percent = $224,000 less $140,000). The $84,000 tax expense related to incomefor the quarter excludes the effect of tax law changes on Company Y’s deferredtaxes.

Effective tax rate reconciliationQuestion: Under U.S. GAAP, a public company is required to present a tax ratereconciliation in the footnotes. What rate should be used as the statutory tax rate for theannual period that includes the enactment date?

Answer: A public company should use 35 percent as its statutory tax rate for the yearended December 31, 2017. A public company with a fiscal year end should use itsblended tax rate, as discussed earlier. For example:

• March 31 year-end companies will reconcile to a 31.55 percent effective tax ratefor the fiscal year ending March 31, 2018.

• June 30 year-end companies will reconcile to a 28.06 percent effective tax rate forthe fiscal year-ending June 30, 2018.

• September 30 year-end companies will reconcile to a 24.53 percent effective taxrate for the fiscal year ending September 30, 2018.

Corporate alternative minimum tax. The Act eliminates the corporate AMT begin-ning with 2018 for calendar year taxpayers. For companies with AMT credits, the Actprovides two mechanisms by which those credits can be realized. Existing AMT creditscan be used against the taxpayer’s regular tax liability.

For taxable years beginning after 2017 and before 2022, existing AMT credits arerefundable. Specifically, the company can obtain a refund in an amount equal to 50percent (100 percent in the case of taxable years beginning in 2021) of the excess of theAMT credit for the taxable year over the amount of the credit allowable for the yearagainst the regular tax liability. In short, companies generally can expect the fullamount of the AMT credit to be used or refunded.

Question: Although prior law permitted a company to carry AMT credits forwardindefinitely, some companies recorded a valuation allowance against the deferred taxasset for AMT credits. Should the valuation allowance be released as a result of the newtax law?

Answer: Generally, yes. Companies that expect to either utilize or receive a refund fortheir AMT credits as a result of the Act should release any previously recordedvaluation allowance related to that deferred tax asset. The release (a credit to income)should be recognized as part of the effect of the change in tax law. In other words, thecredit arising from the reversal of the valuation allowance is recorded in income taxexpense in income from continuing operations in the period the new law is enacted.

Question: How should deferred tax assets for AMT credits be presented on thebalance sheet? In particular, how does a determination that the AMT credit will berefunded affect classification?

¶104

9MODULE 1 - CHAPTER 1 - Accounting for the Tax Cuts and Jobs Act

Answer: U.S. GAAP does not provide a definitive answer. For this reason, it would beacceptable to classify the AMT credit as either a receivable or a deferred tax asset. Ifpresented as a receivable, companies should separate the current and noncurrentportion.

Bifurcation between deferred taxes and receivables is also acceptable. For exam-ple, assume a company expects to use a portion of its existing AMT credit to reduce itsregular tax liability and to receive a portion as a refund. In that case, the company couldpresent the portion that is likely to be reduce its regular tax liability as a deferred taxasset and the portion that is likely to be refunded as a receivable.

Question: To the extent that a company records a receivable for refunds of its AMTcredits, can the noncurrent portion of that receivable be discounted?

Answer: No. The FASB staff addressed this issue in a Q&A. Specifically: “The FASBstaff notes that paragraph 740-10-30-8 prohibits discounting deferred taxes. Accordinglyany AMT credit carryforwards presented as a deferred tax asset would not be dis-counted. Likewise, the FASB staff believes that any AMT credit carryforward presentedas a receivable should not be discounted because the staff does not believe thatSubtopic 835-30 on the imputation of interest applies.�

Net operating loss carryforwards. The Act changed the way in which a NOL can beutilized. While some aspects of the change are more generous than prior law, otheraspects are not.

Prior law permitted a company to carryback a loss generated in a taxable year toeach of the two preceding years, thereby generating a refund of prior taxes paid. Thenew law eliminates the ability to carryback an NOL, effective for taxable years begin-ning after December 31, 2017.

On the other hand, while prior law limited the carryforward period for NOLs to 20years, the Act permits an indefinite carryforward period. This good news is tempered bythe fact that NOL carryforwards are limited to 80 percent of taxable income for the year.Thus, a $100 NOL carryforward will not fully offset $100 of future taxable income. Acompany would need $125 of taxable income to realize $100 of NOLs.

Question: How do these two principal changes—the ability to carry forward an NOLindefinitely and the 80 percent limitation on the utilization of an NOL against taxableincome in any one year—affect the need for a valuation allowance?

Answer: Companies will need to reassess the need for valuation allowances on theirNOLs as a result of the new tax law.

A company that has deferred tax liabilities with indefinite reversal patterns (forexample, a taxable temporary difference related to an indefinite-lived intangible orgoodwill) may have future taxable income that it previously was unable to considerwhen assessing the need for a valuation allowance. Previously, the company may haveconcluded that a full valuation allowance was needed because the future taxable incomeassociated with these indefinite-lived temporary differences would not be available toutilize the NOL during the carryforward period. Therefore, in some circumstances, theability to indefinitely carry forward an NOL may result in the release of a valuationallowance against an NOL carryforward.

However, the 80 percent limitation on the use of NOLs against future taxableincome affects the amount of the NOL that may be realized. As noted above, taxableincome of $125 is needed to realize $100 of NOLs. This limitation not only affects theanalysis in the preceding paragraph, it also affects companies that had partial or novaluation allowances based on the reversal patterns of finite-lived temporary differences.

¶104

10 TOP ACCOUNTING AND AUDITING ISSUES FOR 2019 CPE COURSE

EXAMPLE: Company Z has a $100,000 NOL carryforward that expires in 18years and $110,000 of taxable temporary differences related to depreciable machin-ery and equipment. Under prior law, Company Z concluded that the NOL would befully utilized based on the taxable income generated by the reversal of the taxabletemporary differences. Under the new law, $110,000 of taxable temporary differ-ences would not be sufficient to fully utilize the $100,000 NOL.

To the extent that a company reduces or increases its valuation allowance for itsNOLs as a result of changes in the law, the credit or debit to income is recognized aspart of the effect of the tax law change in the period of enactment.

Deductibility of compensation to highly paid employees. The Act modifies the taxdeductibility of certain types of compensation to highly paid employees in several ways.Prior law limited the tax deduction for compensation for the CEO and the four highestcompensated officers (so-called covered employees). The new law defines coveredemployees as the CEO, the CFO and the three highest paid employees. Further, oncean employee qualifies as a covered person, the limitation applies to that person forfederal tax purposes so long as the company pays compensation to that person or his orher beneficiaries.

Prior law applied to domestic publicly traded companies. Going forward, thelimitation also applies to all foreign companies publicly traded through AmericanDepository Receipts (ADRs) and certain corporations that are not publicly traded.

Exclusions from the computation of compensation for purposes of determining thelimitation have changed. Under prior law, commission-based compensation and quali-fied performance-based compensation were excluded when determining the amount ofcompensation that was not deductible. Said differently, salary in excess of $1 millionwas not deductible but commissions and qualified performance based compensationwere deductible. The Act removes the commission and performance-based compensa-tion exclusions. This change increases the amount of compensation that is notdeductible.

Question: How will these changes affect income tax accounting?

Answer: Compensation that is not deductible represents a permanent difference be-tween book income and taxable income. In all likelihood, these changes in tax law willincrease the amount of nondeductible compensation which, in turn, will result in ahigher effective tax rate.

Permanent differences between book income and taxable income affect a com-pany’s estimate of its annual effective tax rate for interim tax expense computations.Additionally, if material, nondeductible compensation would represent a reconcilingitem in a public company’s effective tax rate reconciliation.

The new law applies to compensation arrangements entered into after November 2,2017. Therefore, a company within the scope of this provision of the new law shoulddetermine whether the compensation arrangements it enters into after that date areaffected by the annual limitation. Deferred income taxes related to compensationarrangements should consider whether the deduction limitation will apply.

Deductibility of net interest expense. Prior tax law included limitations on thedeductibility of interest expense, but those limitations generally only applied to loansfrom foreign related persons when the corporate taxpayer’s debt-to-equity ratio andinterest expense as a percent of adjusted taxable income both exceeded defined limits.Under the Act, net interest expense is limited to 30 percent of the taxpayer’s adjustedtaxable income, a lower threshold than prior law. In addition, the limitation applies toboth related and unrelated-party debt arrangements that include domestic borrowings.Disallowed interest can be carried forward indefinitely.

¶104

11MODULE 1 - CHAPTER 1 - Accounting for the Tax Cuts and Jobs Act

These changes make it more likely that a company with significant amounts ofinterest expense will be faced with a limitation on the deductibility of that expense.

Question: How does this change in tax law affect a company’s accounting for incometaxes?

Answer: Because any amounts that are disallowed in one tax year can be carriedforward indefinitely for use in a later tax year, a company that is subject to a limitationon the deductibility of its interest expense will generate a deductible temporary differ-ence (i.e., it will have a deferred tax asset). As with other deferred tax assets, a companyneeds sufficient positive evidence of book taxable income to demonstrate recoverability.

Deductibility of entertainment expense. The Act disallows 100 percent of entertain-ment expenses. Under prior law, the deduction of qualifying entertainment expenseswas limited to 50 percent. The new rule is effective for expenses incurred or paid afterDecember 31, 2017. Meals continue to be 50 percent deductible.

Question: What effect does the change in the rules regarding deductibility of entertain-ment expenses have on income tax accounting?

Answer: Entertainment expense that is not deductible represents a permanent differ-ence between book income and taxable income. Increasing the nondeductible portion ofentertainment expense from 50 percent to 100 percent will result in a higher effectivetax rate.

Permanent differences between book income and taxable income affect a com-pany’s estimate of its annual effective tax rate for interim tax expense computations. Inaddition, if material, nondeductible entertainment expense would represent a recon-ciling item in a public company’s effective tax rate reconciliation. (Private companies arerequired to provide a narrative discussion of reconciling items but are not required topresent a numerical reconciliation.)

Because the deductibility of meals is not affected, companies will need to insurethat their internal reporting properly separates “meals� from “entertainment.�

¶105 OVERVIEW OF CHANGES: FOREIGN EARNINGSOne area significantly affected by the Act is the taxation of foreign income. The Actreplaces the U.S. tax code’s long-standing worldwide system of taxing foreign earningswith what is being called a partial or quasi territorial system.

Under a worldwide system, earnings generally are subject to taxation based onwhere the taxpayer resides, regardless of where the income is earned. Prior to the Act,a U.S. company paid U.S. federal taxes at the U.S. corporate tax rate on a subsidiary’sforeign earnings when those earnings were repatriated (dividended) to the U.S. parententity. To reduce the effect of double taxation, the U.S. company received credit forforeign taxes paid by the foreign subsidiary. But it meant that the U.S. company waseffectively paying a 35 percent federal tax rate on its global earnings.

Under a territorial system, earnings are generally subject to taxation based onwhere the earnings are generated. The Act’s partial territorial system allows U.S.corporations to receive a 100 percent dividends-received deduction for foreign sourcedividends received from 10 percent or more owned foreign corporations. To implementthis shift to a partial territorial system, the Act mandates a one-time transition tax onpreviously unrepatriated foreign earnings.

The Act also creates certain incentives and disincentives that can affect a com-pany’s tax strategies. It encourages generating foreign earnings using U.S.-based assetsby creating a special deduction for foreign-derived intangible income (FDII). It discour-ages shifting certain assets and income to very low tax jurisdictions by creating a new

¶105

12 TOP ACCOUNTING AND AUDITING ISSUES FOR 2019 CPE COURSE

tax on low-taxed foreign income deemed to have been generated by intangible assets(so-called global intangible low-taxed income, or GILTI).

A new alternative minimum tax (the Base Erosion and Anti-abuse Tax, or BEAT)addresses the tax base erosion created by the ability to deduct certain payments torelated foreign parties. While the goal of BEAT is to address potential base erosioncreated by certain tax strategies, it may have broader consequences, potentially func-tioning as a “backdoor� alternative minimum tax in some cases. These changes in theforeign earnings provisions of corporate tax law can be summarized as follows:

• Mandating a one-time tax payment on post-1986 undistributed earnings andprofits. The tax rate on these earnings ranges from 8 percent to 15.5 percent andis thus substantially lower than both the prior corporate tax rate of 35 percentand the new 21 percent tax rate.

• Creating a new tax on GILTI. Excluding any foreign tax considerations, theeffective tax rate on GILTI ranges from 10.5 percent (tax years 2018–2025) to13.125 percent (tax years after 2025).

• Creating a deduction for FDII. The mechanics of this provision result in aneffective tax rate ranging from 13.125 percent (tax years 2018–2025) to 16.406percent (tax years after 2025) on FDII, substantially less than the overallcorporate rate of 21 percent.

• Creating an alternative taxation model, called the Base Erosion and Anti-abuseTax (BEAT). The base erosion tax rate begins at 5 percent for 2018, increases to10 percent for tax years 2019–2025, and increases to 12.5 percent thereafter. Forcertain banks and registered securities dealers, as well as their affiliates, BEATis computed at a slightly higher rate.

Accounting for Income Taxes (ASC Topic 740)U.S. GAAP requires recording an income tax provision not only for taxes that are due asa result of the current year’s taxable income (“current tax expense or benefit�), but alsofor the future tax consequences of transactions that have been reported in the financialstatements or tax returns (“deferred tax expense or benefit.�)

The most common examples of items that give rise to deferred tax liabilities aredepreciation of buildings, machinery and equipment and the amortization of intangibleassets. The costs of those assets generally are expensed more rapidly for tax purposesthan for U.S. GAAP purposes, creating a basis difference in the asset. Typical examplesof items that lead to deferred tax assets include accrued expenses and allowances forbad debts. For these items, the U.S. GAAP expense often exceeds the amount that isdeductible in the current year’s tax return under the tax rules, also creating a basisdifference in the asset or liability.

These differences between the amounts reported for tax purposes and U.S. GAAPpurposes, whether they result in deferred tax assets or liabilities, are referred to assimply “temporary differences.�

However, U.S. GAAP exempts certain temporary differences from deferred taxaccounting. The most significant (and most common) is the exemption related toundistributed earnings of foreign subsidiaries and the related basis difference in theparent’s investment in its subsidiary. Although U.S. GAAP presumes that all undistrib-uted earnings will be transferred to the parent, if there is sufficient evidence that foreignearnings will be reinvested by the subsidiary, that is, evidence that remittance to theparent is postponed indefinitely, then no deferred taxes are provided.

This provision in U.S. GAAP, commonly referred to as the “APB 23 exception,�reflects the long-standing U.S. tax system under which foreign earnings were not

¶105

13MODULE 1 - CHAPTER 1 - Accounting for the Tax Cuts and Jobs Act

subject to U.S. tax until the earnings were remitted. By changing the tax rules forforeign earnings, the Act requires companies to revisit their prior accounting conclu-sions regarding deferred taxes on this temporary difference.

Future tax consequences arising from temporary differences are recorded basedon tax law enacted at the date of the financial statements. U.S. GAAP requires that allcompanies, both public and private, recognize the effects of tax law changes on the dateof enactment. Such effects are charged to income as part of the income tax expense orbenefit for the period.

Companies will record the consequences of the Act on their deferred tax balances(as well as any effect on current tax expense) in the income statement for the reportingperiod that includes December 22, 2017.

Q&AsTransition tax: deemed repatriation of foreign earnings. One of the central featuresof the Act is the imposition of a one-time tax on the undistributed, previously untaxedforeign earnings and profits that have accrued since 1986. This transition tax applies to10 percent or more owned foreign corporations.

Under prior law, foreign earnings could be held outside the U.S. indefinitely, thusavoiding payment of U.S. tax at the then corporate tax rate of 35 percent. Under the Act,the one-time tax must be paid regardless of whether the company repatriates theearnings. However, the tax rate applied to those earnings is substantially reduced: 15.5percent tax rate for earnings and profits that have been retained in cash and other liquidassets and 8 percent for remaining earnings. Foreign tax credit and net operating losscarryforwards may be available to offset the transition tax liability.

Companies can elect to pay the one-time transition tax over eight years on aninterest free basis. Under this election, payments are due without regard to any futuretaxable income or losses and are made in the following amounts: 8 percent per year forthe first five years, 15 percent in the sixth year, 20 percent in the seventh year, and 25percent in the eighth year.

Question: To the extent that a company elects to pay the transition tax in installmentsover eight years, can the noncurrent portion of that tax obligation be discounted?

Answer: No. The FASB staff addressed this issue in a Q&A. Specifically: “The FASBstaff notes that paragraph 740-10-30-8 prohibits discounting deferred tax amounts. Dueto the unique nature of the tax on the deemed repatriation of foreign earnings, the staffbelieves that the guidance in paragraph 740-10-30-8 should be applied by analogy to thepayable recognized for this tax. Further, the FASB staff does not believe that Subtopic835-30 on the imputation of interest applies to the unique circumstances related to thisliability.�

In its guidance, the FASB staff also notes that the transition tax may be subject toestimation and the future resolution of uncertain tax positions. Examples of thoseuncertain tax positions include the amount of earnings and profits from foreign subsidi-aries, the availability and amount of foreign tax credits that can be used to reduce thetransition tax and determining the amount of earnings held in cash and other liquidassets. Because any uncertain tax positions related to the deemed repatriation of foreignearnings cannot be discounted, it would be inappropriate to discount the related taxliability.

Question: How should the transition tax be classified on the balance sheet?

Answer: In general, the obligation to pay the transition tax should not be classified as adeferred tax liability because it does not represent the tax effect of a temporary

¶105

14 TOP ACCOUNTING AND AUDITING ISSUES FOR 2019 CPE COURSE

difference. It represents a tax determined based on a company’s accumulated earningsand profits for tax purposes and thus is unlikely to represent the outside basisdifference in the company’s investment in its subsidiary.

This conclusion is consistent with the manner in which the FASB staff answeredthe question on discounting. Note that the FASB staff refers to the obligation as a“payable� and references U.S. GAAP’s prohibition on the discounting of a deferred taxliability as being applicable by analogy. Companies with a classified balance sheet thatelect to remit the payment over eight years should distinguish between the current andnoncurrent portions of the tax obligation.

Question: Assuming sufficient evidence of indefinite reinvestment exists, U.S. GAAPallows a company to exempt the undistributed earnings of foreign subsidiaries and therelated basis difference in the parent’s investment in its subsidiary from deferred taxaccounting. Does the transition tax eliminate the need to consider whether foreignearnings are indefinitely reinvested?

Answer: No, for two reasons. First, the U.S. GAAP exception applies to the outsidebasis difference in the investment. Basis differences arise for many reasons and maycontinue to exist irrespective of this change in the tax law. Second, the one-timetransition tax does not require that the earnings be repatriated. The liability must bepaid regardless of where the accumulated earnings reside or are invested. Companieswill separately evaluate the repatriation decision because that can trigger other taxconsequences, such as state taxes and/or foreign withholding taxes. For these reasons,companies need to continue to assess how the outside basis difference in foreignsubsidiaries will reverse, including whether foreign earnings are indefinitely reinvested.

Some companies may continue to leave the earnings in the existing foreign taxjurisdiction and make no changes to their legal structures or tax strategies. Others maychange their tax strategies as a result of this change in tax law. For example, a U.S.parent may direct its foreign subsidiaries to remit dividends in order to provide theliquidity needed to pay the transition tax or to reduce debt so as to avoid the newinterest expense deduction limitation.

If a company can no longer assert the ability and intent to indefinitely reinvest, itshould record the resulting deferred tax consequences based on the manner in which itexpects to recover its investment. In some cases, management may conclude that theoutside basis difference will reverse through distributions (repatriation of earnings). Inother cases, it may conclude that it will recover its investment via liquidation or sale.

If management has sufficient evidence to support its conclusion that the earningsare indefinitely reinvested, the disclosure requirements of U.S. GAAP continue to apply.

Question: Where is the adjustment to record the one-time transition tax reported?

Answer: Under U.S. GAAP, the adjustment to remeasure deferred tax assets andliabilities and record any additional tax obligations as a result of a change in tax law isreported in income from continuing operations as part of income tax expense in theperiod in which the new law is enacted.

The transition tax is simply one of the many changes to previously recorded taxesbrought about by the Act. Companies that had previously recorded no taxes onunremitted earnings did so on the basis that tax law permitted them to postponetaxation indefinitely. Alternatively, companies that had provided taxes on some or all oftheir foreign subsidiaries’ unremitted earnings did so based on the tax rates that were ineffect. In both cases, adjustments are required as a result of the Act.

Question: Computing the transition tax requires extensive information gathering, anin-depth analysis of the tax law and, in some cases, judgments regarding the application

¶105

15MODULE 1 - CHAPTER 1 - Accounting for the Tax Cuts and Jobs Act

of the new tax law to a company’s specific facts and circumstances. Must a companyfinalize its measurement of the one-time transition tax in the accounting period thatincludes the December 22, 2017 enactment date of the Act?

Answer: No. Based on the SEC staff guidance in SAB 118 and the FASB staff guidancein its Q&A, public and private companies are permitted up to a year to finalize themeasurement of the effects of the change in tax law. Companies that choose to use therelief provided by this guidance are required to make certain disclosures. Refer to thedisclosures addressed in the domestic earnings section above.

Global intangible low-taxed income. As part of the fundamental change to the U.S.regime for taxing foreign earnings, the Act introduces a new category of income,referred to as global intangible low-taxed income (GILTI). For tax years beginning afterDecember 31, 2017, a company will be subject to tax on GILTI to the extent that thatincome exceeds a safe harbor. While the provisions of GILTI are complex, this new taxwill most likely affect companies that (1) have foreign earnings generated without alarge aggregate foreign fixed asset base (i.e., income generated by intangible assets)and (2) are taxed on those earnings at a low tax rate.

GILTI is the excess of a U.S. shareholder’s total net foreign income over a deemedreturn on tangible assets. If the amount of GILTI for a tax year is a loss, the Act permitsno carryforward or carryback of that loss. If the amount of GILTI for a tax year isincome, the U.S. shareholder is allowed a deduction of 50 percent of that amount, up tothe amount of the U.S. shareholder’s taxable income.

The U.S. shareholder is also allowed a deemed paid foreign tax credit of up to 80percent of foreign taxes attributable to the underlying foreign corporation. However,foreign tax credits associated with global intangible low-taxed income can only be usedto reduce U.S. taxes owed on GILTI and cannot be carried forward. Because of the 50percent deduction, the effective tax rate on GILTI is 10.5 percent through 2025. In 2026,when the deduction is lowered to 37.5 percent, the effective tax rate on GILTI will be13.125 percent.

Question: How should the tax consequences associated with global intangible low-taxed income be accounted for? Specifically, is the tax on GILTI included in tax expensein the year it is incurred? Or should a company recognize deferred taxes for temporarybasis differences that are expected to reverse as global intangible low-taxed income infuture years?

Answer: According to the FASB staff, U.S. GAAP is not clear as to the treatment oftaxes on GILTI. As discussed in a FASB staff Q&A, pending further guidance from theFASB, a company should choose between one of the two following acceptable account-ing policies:

• Alternative Policy 1: The tax on GILTI should be accounted for as a period cost,similar to special deductions. This accounting policy views GILTI as a computa-tion that is not premised on the U.S. taxpayer’s basis in discrete investments orassets and liabilities and is dependent on future, contingent events. BecauseGILTI is based on the aggregate income from all foreign corporations in a year,the unit of account for deferred tax purposes is neither the investment in anindividual foreign corporation or that corporation’s assets and liabilities. U.S.GAAP’s accounting model for income taxes does not address taxes on aggre-gated income across multiple jurisdictions in which basis differences offset suchthat any particular basis difference might never be taxed. Further, GILTI isdependent on contingent or future events, such as the amount of foreignqualified business asset investment in a given year, future foreign tax creditsand future foreign income versus loss. This suggests that taxes on GILTI areperiod costs.

¶105

16 TOP ACCOUNTING AND AUDITING ISSUES FOR 2019 CPE COURSE

• Alternative Policy 2: Deferred tax assets and liabilities should be recognized whenbasis differences exist that are expected to affect the amount of GILTI inclusion uponreversal. This accounting policy views the tax on GILTI as similar to the taximposed on existing Subpart F income. Currently, deferred taxes generally areprovided for basis differences that are expected to result in Subpart F incomeupon reversal. Because GILTI is included in taxable income when earned by aforeign corporation, similar to Subpart F income, it is appropriate to account forit similarly. Companies that elect this second accounting policy are likely to haveadditional implementation questions. More guidance may be forthcoming as theFASB staff receives additional questions and monitors what companies aredoing in practice.

A company should disclose its accounting policy related to GILTI inclusions, as re-quired by U.S. GAAP.

Question: Must a company select its accounting policy for GILTI in the accountingperiod that includes the December 22, 2017, enactment date of the Act?

Answer: The SEC staff guidance in SAB 118 that provides public companies with somerelief regarding the measurement of the effects of the change in tax law does notspecifically address accounting policy issues arising from the new tax law. (Privatecompanies are permitted to follow the guidance in SAB 118.)

While U.S. GAAP does not permit a “temporary� accounting policy election, itwould not be unreasonable for a company to defer its election of an accounting policy tothe period in which it completes its measurement of the effects of the GILTI tax lawprovisions. In other words, so long as the company has not recorded a provisional orfinal amount for the effects of GILTI, it has not adopted an accounting policy. Thus, itwould disclose that its accounting for the effects of GILTI tax law provisions isincomplete and an accounting policy has not been elected.

Once the company records an amount that reflects GILTI provisions of the tax law,however, it has implicitly adopted an accounting policy. Any change to that policy wouldneed to be based on the requirements of U.S. GAAP.

Deduction for foreign-derived intangible income. To encourage certain tax strate-gies, the Act creates a deduction for income earned by a U.S. corporation in connectionwith sales of goods or services to a non-U.S. person for foreign use only (i.e., U.S. exportsales). For taxable years beginning after December 31, 2017, and before January 1,2026, the deduction is equal to the sum of 37.5 percent of FDII plus 50 percent of GILTItax (if any). After that date, the deduction for FDII and the GILTI tax are reduced to21.875 percent and 37.5 percent, respectively. The effect of this specific deduction is tolower the tax rate on this category of income to 13.125 percent for and taxes 2018through 2025 and 16.406 percent thereafter.

The computation of the tax benefit is based on a measure of export sale intangible-derived income that can vary based on any number of factors. It is similar to previoustax benefits such as foreign sales corporations and the extra territorial income exclu-sion, both of which have been repealed.

Question: How should a company account for an FDII deduction?

Answer: U.S. GAAP states that the tax benefits associated with special deductionsshould not be anticipated for purposes of offsetting a deferred tax liability and thusgenerally should be recognized no earlier in the year in which the special deduction isdeductible on the tax return. U.S. GAAP does not define “special deductions.� However,the FDII deduction is similar to prior export-related benefits that were accounted for asspecial deductions.

¶105

17MODULE 1 - CHAPTER 1 - Accounting for the Tax Cuts and Jobs Act

Base Erosion and Anti-abuse Tax. The Act created a new alternative minimum tax(Base Erosion and Anti-abuse Tax, or BEAT) to address the tax base erosion created byother aspects of the tax law. Specifically, the computation of BEAT differs from thecomputation of the regular tax liability in two broad respects: (1) BEAT disallows taxdeductions for certain payments made to related foreign parties, and (2) BEAT imposesa lower tax rate. Specifically, amounts that are not deductible for BEAT (referred to asbase erosion payments) include payments to foreign related parties for items such asroyalty payments or payments to acquire depreciable or amortizable property. The taxrate used to compute the BEAT is 5 percent in 2018 but increases to 10 percent in 2019through 2025 and 12.5 percent thereafter.

Under the Act, if the BEAT is greater than the company’s regular tax liability, thelarger amount must be paid. The payment of BEAT does not result in a tax credit. Whilethe goal of BEAT is to address potential base erosion created by certain tax strategies, itmay have broader consequences, potentially functioning as a “backdoor� alternativeminimum tax in some cases.

BEAT applies to companies that have average annual gross receipts of at least $500million and that have made related party deductible payments totaling 3 percent (2percent for banks and securities dealers) or more of total deductions for the year. BEATis effective for base erosion payments paid or accrued in taxable years beginning afterDecember 31, 2017.

Conceptually, BEAT is similar to the corporate AMT that Congress eliminated viathe Act. Both are alternative tax computations that impose a minimum level of taxationby excluding certain tax deductions to arrive at an alternative amount of taxable incomethat is taxed at an alternative, lower tax rate. However, there is an important distinction:while the payment of AMT resulted in a tax credit that could be carried forward, thepayment of BEAT does not.

Question: If a company reasonably expects to be subject to BEAT, should the companymeasure its deferred tax assets and liabilities at the BEAT tax rate?

Answer: No. The FASB staff addressed this issue in a Q&A. Based on an analogy toU.S. GAAP related to the accounting for AMT, the FASB staff concluded: “[A]n entitythat is subject to BEAT should measure deferred tax assets and liabilities using thestatutory tax rate under the regular tax system. The FASB staff believes that measuringa deferred tax liability at the lower BEAT rate would not reflect the amount an entitywould ultimately pay because the BEAT would exceed the tax under the regular taxsystem using the 21 percent statutory tax rate.�

Question: How should a company that is subject to BEAT account for the incrementaltax incurred?

Answer: The incremental effect of BEAT should be recognized in income tax expensein the year that the BEAT is incurred. This conclusion is consistent with the manner inwhich the FASB staff answered the question on the measurement of deferred taxes for acompany that is subject to BEAT.

Question: Given the interaction between BEAT and certain deferred tax assets such asNOL and AMT credit carryforwards, should a company that is subject to BEAT considerthe effect of BEAT in evaluating the need for a valuation allowance?

Answer: Possibly. In its Q&A addressing BEAT, the FASB staff specifically states that acompany “would not need to evaluate the effect of potentially paying the BEAT in futureyears on the realization of deferred tax assets under the regular tax system.�

¶105

18 TOP ACCOUNTING AND AUDITING ISSUES FOR 2019 CPE COURSE

The FASB staff explains its view by noting that “the realization of the deferred taxasset [such as an NOL carryforward or AMT credit carryforward] would reduce itsregular tax liability, even when an incremental BEAT liability would be owed in thatperiod.� Said differently, because deferred taxes are measured based on the regular taxsystem, as long as the deferred tax asset results in a reduction of the regular taxliability, there is no need for a valuation allowance.

That conclusion is logical. However, it nonetheless seems inconsistent with the factthat a company subject to BEAT may receive no economic benefit from that deferredtax asset. Consider a fact pattern in which a company’s regular tax liability is reduced bya $1,000 AMT credit carryforward. If the company is not subject to BEAT, the $1,000deferred tax asset is economically realized. However, if the company is subject toBEAT, the $1,000 AMT credit carryforward produces no economic benefit. The com-pany’s tax return shows the offset of the AMT credit carryforward against the regulartax liability. However, the company does not pay the regular tax liability because theBEAT is higher. The deferred tax asset is indeed used, but the company does notreceive an equivalent economic benefit.

Although the FASB staff Q&A states that there is no requirement for a company toconsider BEAT when evaluating the need for a valuation allowance against certaindeferred tax assets, it remains to be seen how this area will evolve. Companies that havesignificant NOL and/or AMT credit carryforwards and believe that they are reasonablylikely to be subject to BEAT for the foreseeable future should carefully consider theirspecific facts and circumstances in determining whether a valuation allowance isappropriate.

STUDY QUESTION

6. Which of the following identifies the new alternative minimum tax introduced by theTax Cuts and Jobs Act.

a. BEAT

b. FDII

c. GILTI

d. Corporate AMT

¶105

19

MODULE 1: TOP ACCOUNTING ISSUES—CHAPTER 2: Leases and Impacts: Change toChanges 2018¶201 WELCOMEThis chapter discusses the latest developments from the Financial Accounting Stan-dards Board (FASB) regarding lease accounting.

¶202 LEARNING OBJECTIVES

Upon completion of this chapter, you will be able to:

• Identify the FASB pronouncements that may impact entities with leases or thatexpect to have or enter into leases

• Recognize the major updates to the new Accounting Standards Codifications asprescribed by ASU 2016-02

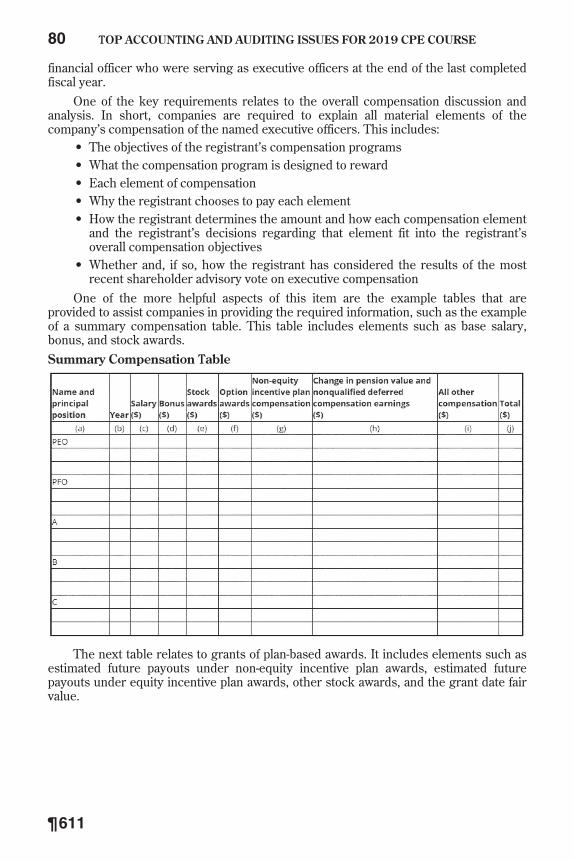

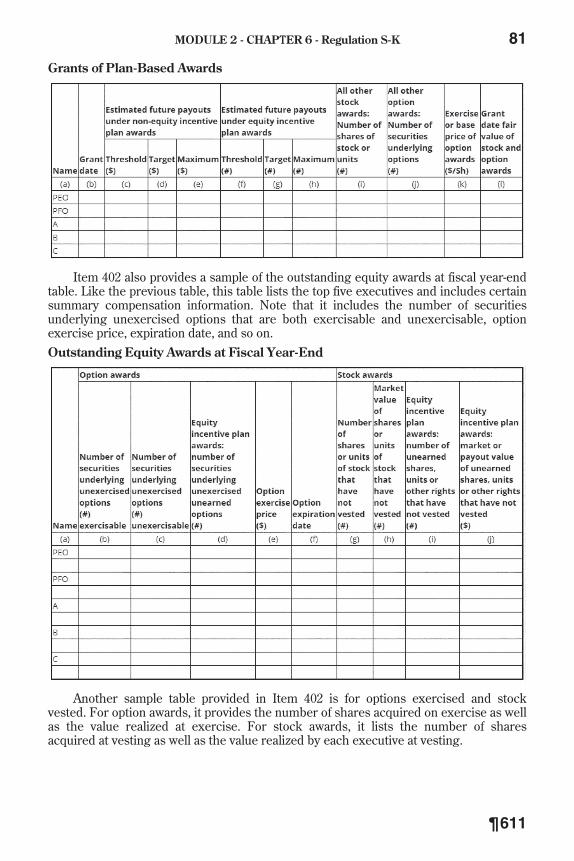

• Understand best practices for starting a lease accounting project under the newstandards