toba company presentation€¦ · company presentation april 2017 pt toba bara sejahtra tbk ......

TRANSCRIPT

1

PT Toba Bara Sejahtra Tbk (“Toba”)

Company PresentationApril 2017

PT Toba Bara Sejahtra Tbk (“Toba”)

Company PresentationApril 2017

Disclaimer

These materials have been prepared by PT Toba Bara Sejahtra Tbk (the “Company”).

These materials may contain statements that constitute forward-looking statements. These statements include

descriptions regarding the intent, belief or current expectations of the Company or its officers with respect to the

consolidated results of operations and financial condition of the Company. These statements can be recognized by

the use of words such as “expects,” “plan,” “will,” “estimates,” “projects,” “intends,” or words of similar meaning.

Such forward-looking statements are not guarantees of future performance and involve risks and uncertainties, and

actual results may differ from those in the forward-looking statements as a result of various factors and

assumptions. The Company has no obligation and does not undertake to revise forward-looking statements to

reflect future events or circumstances.

These materials are for information purposes only and do not constitute or form part of an offer, solicitation or

invitation of any offer to buy or subscribe for any securities of the Company, in any jurisdiction, nor should it or any

part of it form the basis of, or be relied upon in any connection with, any contract, commitment or investment

decision whatsoever. Any decision to purchase or subscribe for any securities of the Company should be made after

seeking appropriate professional advice.

2

Table of Contents

2

Company Profile

Performance Highlights

3

1

Strategy to Venture into Power

3

4

Performance HighlightsPerformance Highlights2 Company Profile1

Location: Kutai, Kalimantan Timur

Hak Guna Usaha (“HGU”) covers 8,633 ha, where

2,701 ha has been planted

CPO mill ready for operation in 2016, with capacity of

30 tons FFB per hour

GLP and MCL established in February 2016 and March

2017 respectively for development of steam (coal) fired

power plant project (“CFPP") with capacity of 2x50 MW

each

25 year Power Purchase Agreement (“PPA”) through

Independent Power Producer (“IPP”) scheme with PLN

as single offtaker

TBE established in December 2016 for investment in

power generation business 5

Toba Bara Sejahtra In Brief

Location: Kutai Kartanegara, Kalimantan Timur

Total Concession: 7,087 ha

JORC-compliant proved and probable reserves of

147 MM tons and measured, indicated and inferred

resources of 236 MM tons

Coal brands with mid to upper range calorific values

ranging from 4,700-5,800 Kcal/kg GAR

Prime location provides operational cost edge to

grow as a logistical & operational center for the area

Coal Mining Plantation

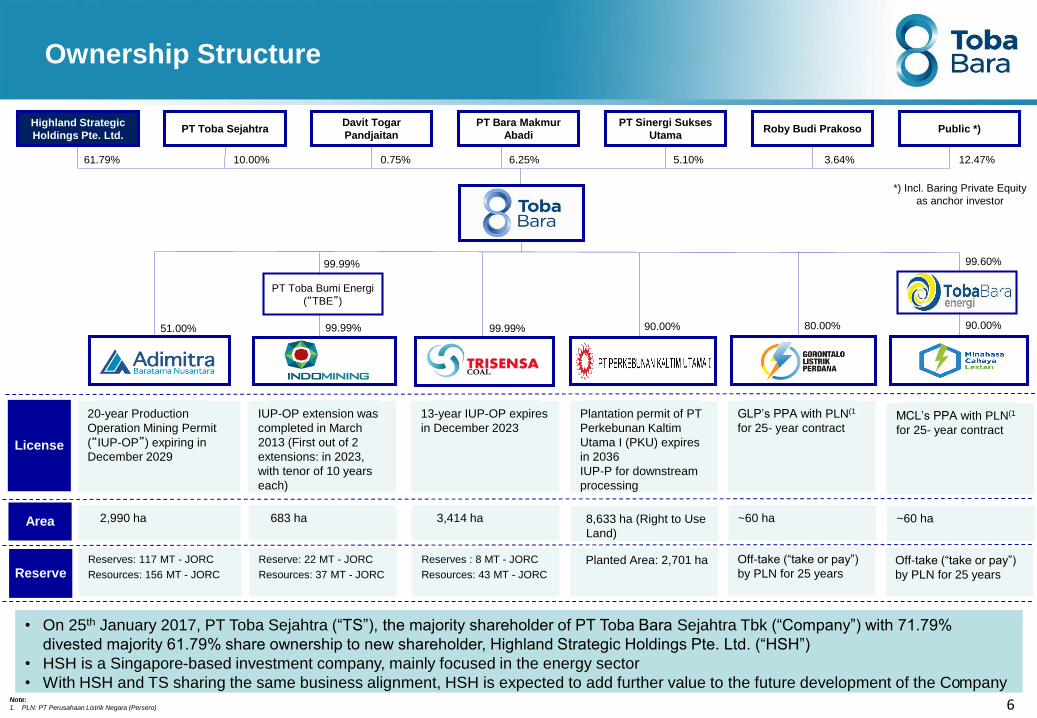

Toba Bara Sejahtra(Toba) has 5 (“five”) subsidiaries engaged in:

Power Generation

Note:

1. PLN: PT Perusahaan Listrik Negara (Persero)

Ownership Structure

License

Area

Davit Togar

Pandjaitan

PT Bara Makmur

AbadiPT Toba Sejahtra Roby Budi Prakoso

PT Sinergi Sukses

Utama

61.79% 10.00% 6.25% 5.10%

PT Toba Bumi Energi

(“TBE”)

99.99%

99.99%

3.64%

51.00% 99.99%

Public *)

12.47%

90.00% 80.00%

Highland Strategic

Holdings Pte. Ltd.

0.75%

• On 25th January 2017, PT Toba Sejahtra (“TS”), the majority shareholder of PT Toba Bara Sejahtra Tbk (“Company”) with 71.79%

divested majority 61.79% share ownership to new shareholder, Highland Strategic Holdings Pte. Ltd. (“HSH”)

• HSH is a Singapore-based investment company, mainly focused in the energy sector

• With HSH and TS sharing the same business alignment, HSH is expected to add further value to the future development of the Company

6

*) Incl. Baring Private Equity

as anchor investor

90.00%

20-year Production

Operation Mining Permit

(“IUP-OP”) expiring in

December 2029

2,990 ha

IUP-OP extension was

completed in March

2013 (First out of 2

extensions: in 2023,

with tenor of 10 years

each)

683 ha

13-year IUP-OP expires

in December 2023

3,414 ha

Plantation permit of PT

Perkebunan Kaltim

Utama I (PKU) expires

in 2036

IUP-P for downstream

processing

8,633 ha (Right to Use

Land)

GLP’s PPA with PLN(1)

for 25- year contract

~60 ha

MCL’s PPA with PLN(1

for 25- year contract

~60 ha

Off-take (“take or pay”)

by PLN for 25 years

Planted Area: 2,701 ha Off-take (“take or pay”)

by PLN for 25 yearsReserveReserves: 117 MT - JORC

Resources: 156 MT - JORC

Reserve: 22 MT - JORC

Resources: 37 MT - JORC

Reserves : 8 MT - JORC

Resources: 43 MT - JORC

99.60%

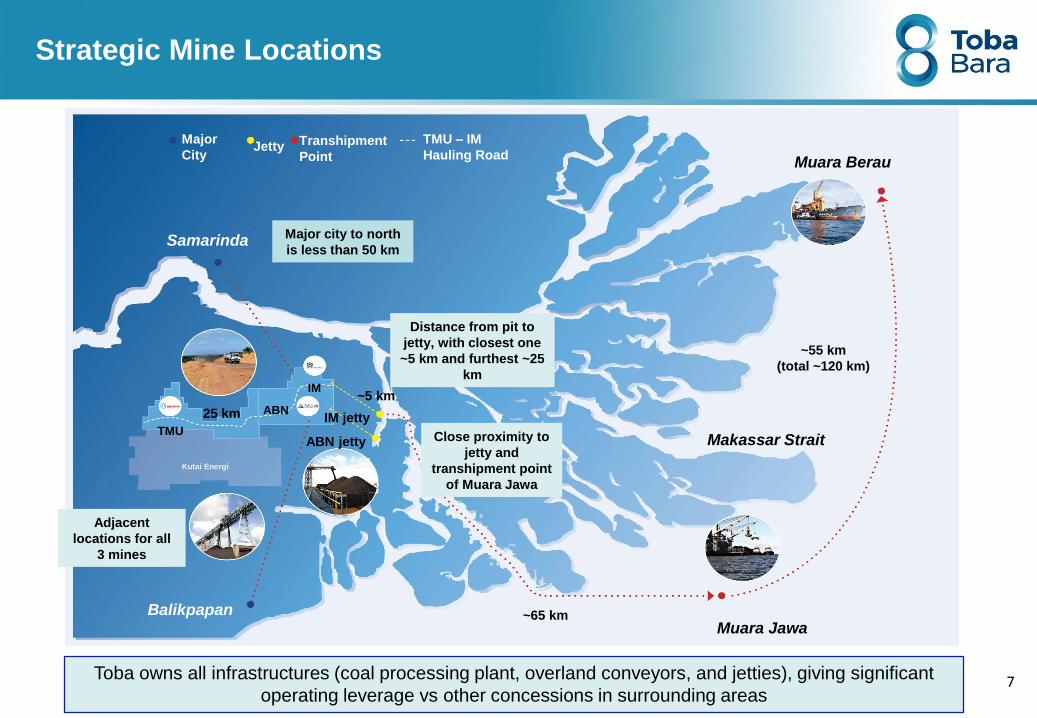

Strategic Mine Locations

Muara Berau

Muara Jawa

Makassar Strait

~55 km

(total ~120 km)

Balikpapan

Samarinda

~65 km

Major

CityJetty Transhipment

Point

TMU – IM

Hauling Road

Kutai Energi

TMU

ABN

IM

Major city to north

is less than 50 km

Adjacent

locations for all

3 mines

Close proximity to

jetty and

transhipment point

of Muara Jawa

Distance from pit to

jetty, with closest one

~5 km and furthest ~25

km

~5 km

IM jetty

ABN jetty

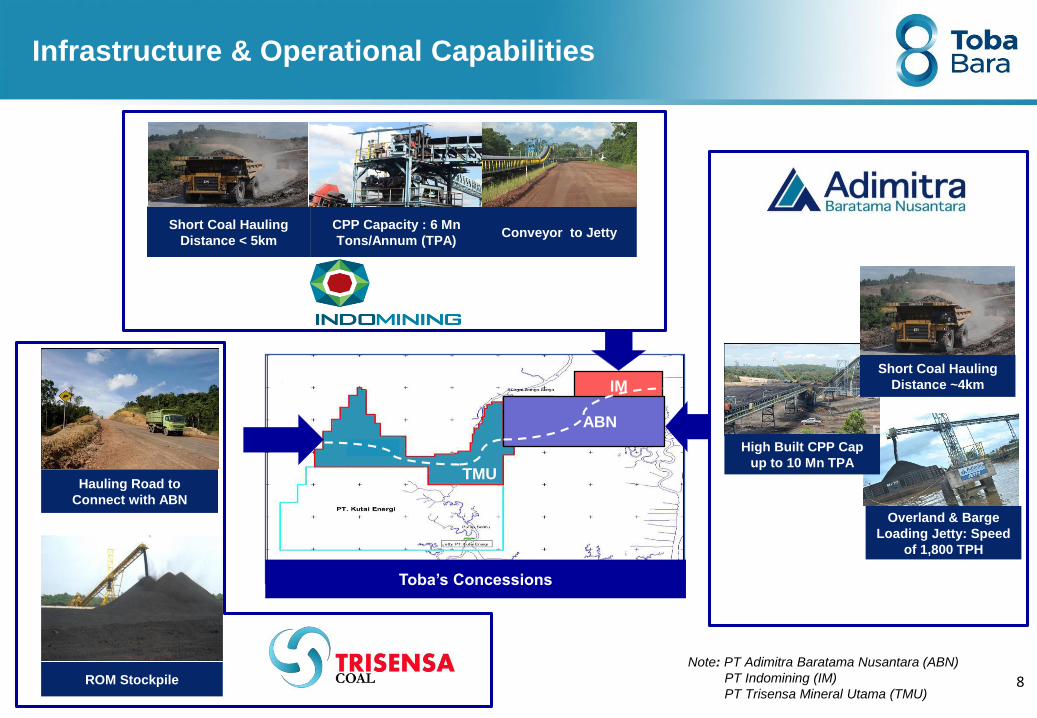

Toba owns all infrastructures (coal processing plant, overland conveyors, and jetties), giving significant

operating leverage vs other concessions in surrounding areas

25 km

7

TMU IM

ABN

TMU

Overland & Barge

Loading Jetty: Speed

of 1,800 TPH

High Built CPP Cap

up to 10 Mn TPA

Short Coal Hauling

Distance < 5km

Hauling Road to

Connect with ABN

CPP Capacity : 6 Mn

Tons/Annum (TPA)Conveyor to Jetty

Short Coal Hauling

Distance ~4km

Infrastructure & Operational Capabilities

Toba’s Concessions

ROM Stockpile 8

Note: PT Adimitra Baratama Nusantara (ABN)

PT Indomining (IM)

PT Trisensa Mineral Utama (TMU)

9

Performance Highlights2

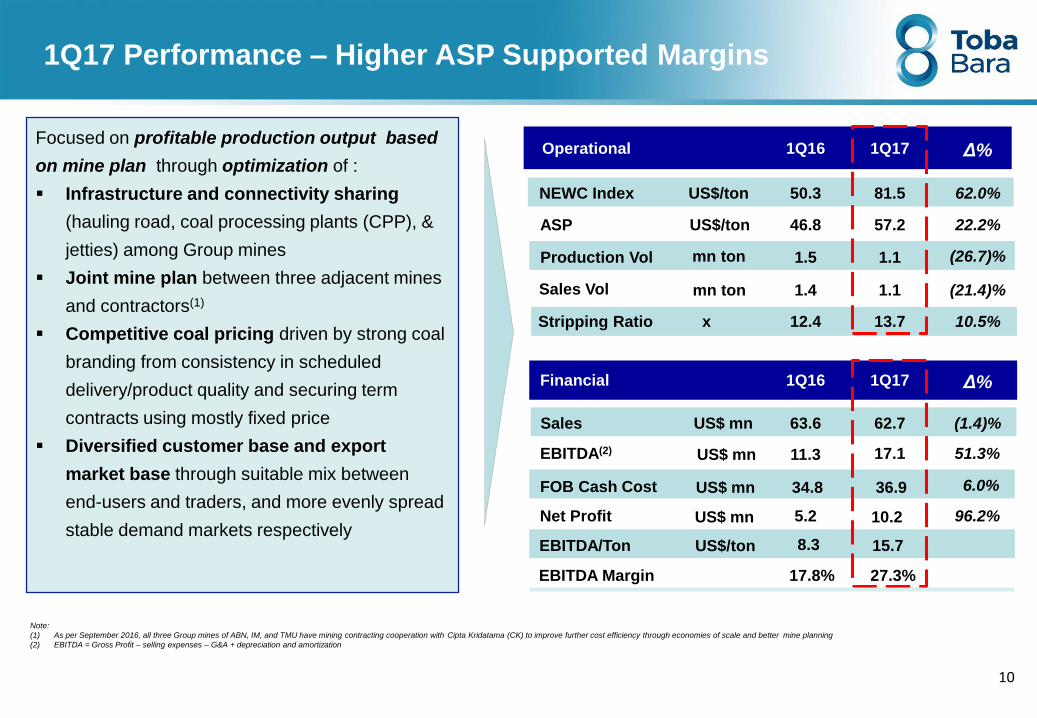

1Q17 Performance – Higher ASP Supported Margins

Operational 1Q16 1Q17 Δ%

Production Vol 1.5 1.1 (26.7)%

Sales Vol 1.4 1.1 (21.4)%

Stripping Ratio x 12.4 13.7 10.5%

Sales 63.6 62.7 (1.4)%

EBITDA(2) 11.3 17.1 51.3%

Net Profit 5.2 10.2 96.2%

Financial 1Q16 1Q17

46.8

NEWC Index 81.5 62.0%50.3

ASP 57.2 22.2%

mn ton

mn ton

US$/ton

US$/ton

US$ mn

US$ mn

US$ mn

Δ%

EBITDA/Ton 8.3 15.7

Focused on profitable production output based

on mine plan through optimization of :

Infrastructure and connectivity sharing

(hauling road, coal processing plants (CPP), &

jetties) among Group mines

Joint mine plan between three adjacent mines

and contractors(1)

Competitive coal pricing driven by strong coal

branding from consistency in scheduled

delivery/product quality and securing term

contracts using mostly fixed price

Diversified customer base and export

market base through suitable mix between

end-users and traders, and more evenly spread

stable demand markets respectively

Note:

(1) As per September 2016, all three Group mines of ABN, IM, and TMU have mining contracting cooperation with Cipta Kridatama (CK) to improve further cost efficiency through economies of scale and better mine planning

(2) EBITDA = Gross Profit – selling expenses – G&A + depreciation and amortization

EBITDA Margin 17.8% 27.3%

US$/ton

FOB Cash Cost US$ mn 34.8 36.9 6.0%

10

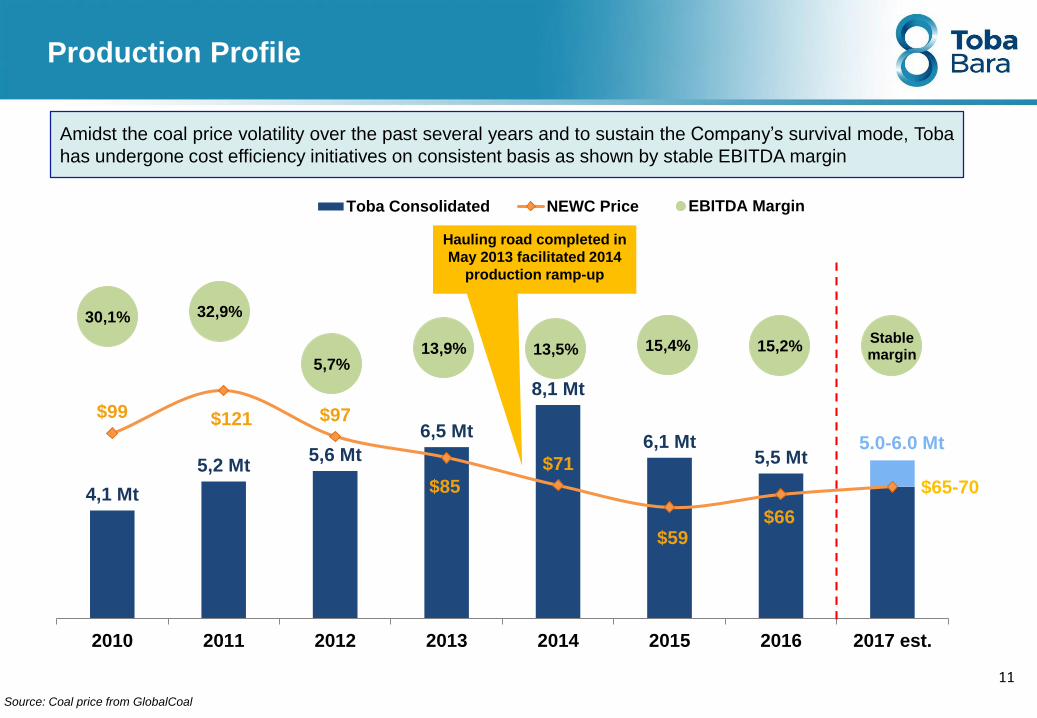

4,1 Mt

5,2 Mt5,6 Mt

6,5 Mt

8,1 Mt

6,1 Mt5,5 Mt

5.0-6.0 Mt

$99 $121 $97

$85

$71

$59$66

$65-70

0

20

40

60

80

100

120

140

0

1

2

3

4

5

6

7

8

9

10

2010 2011 2012 2013 2014 2015 2016 2017 est.

Toba Consolidated NEWC Price

30,1% 32,9%

5,7%13,9% 13,5% 15,4% 15,2%

Stablemargin

EBITDA Margin

Production Profile

11

Hauling road completed in

May 2013 facilitated 2014

production ramp-up

Source: Coal price from GlobalCoal

Amidst the coal price volatility over the past several years and to sustain the Company’s survival mode, Toba

has undergone cost efficiency initiatives on consistent basis as shown by stable EBITDA margin

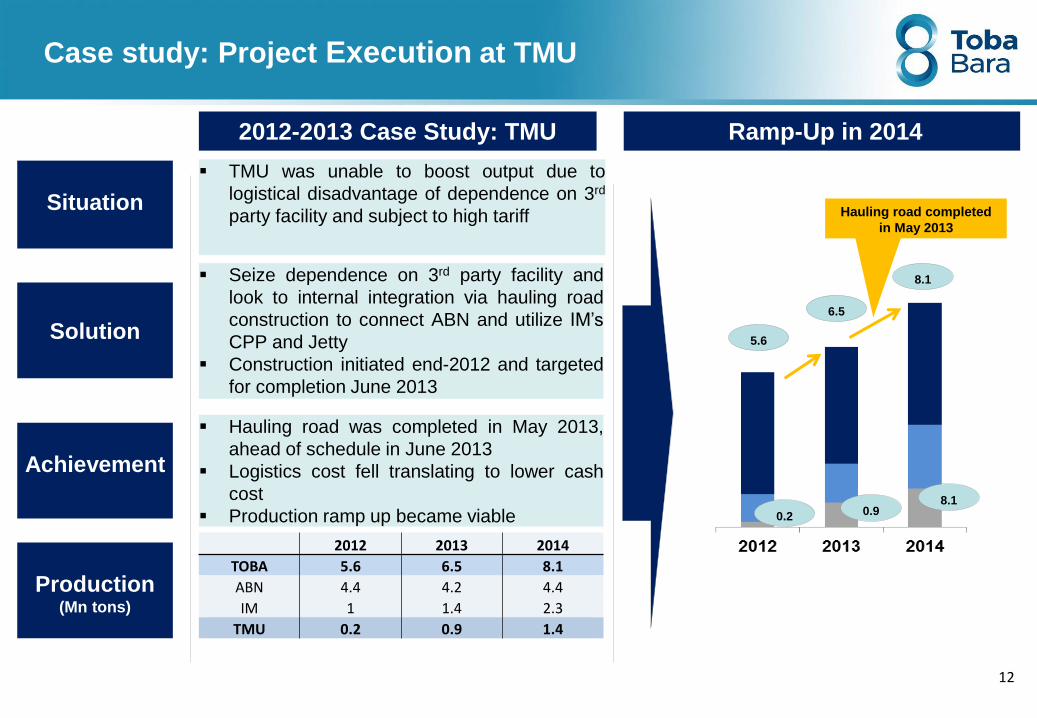

Case study: Project Execution at TMU

Situation

Solution

Seize dependence on 3rd party facility and

look to internal integration via hauling road

construction to connect ABN and utilize IM’s

CPP and Jetty

Construction initiated end-2012 and targeted

for completion June 2013

Achievement

Hauling road was completed in May 2013,

ahead of schedule in June 2013

Logistics cost fell translating to lower cash

cost

Production ramp up became viable

2012-2013 Case Study: TMU Ramp-Up in 2014

TMU was unable to boost output due to

logistical disadvantage of dependence on 3rd

party facility and subject to high tariff

Production(Mn tons)

8.1

6.5

5.6

0.2 0.98.1

Hauling road completed

in May 2013

2012 2013 2014

TOBA 5.6 6.5 8.1

ABN 4.4 4.2 4.4

IM 1 1.4 2.3

TMU 0.2 0.9 1.4

12

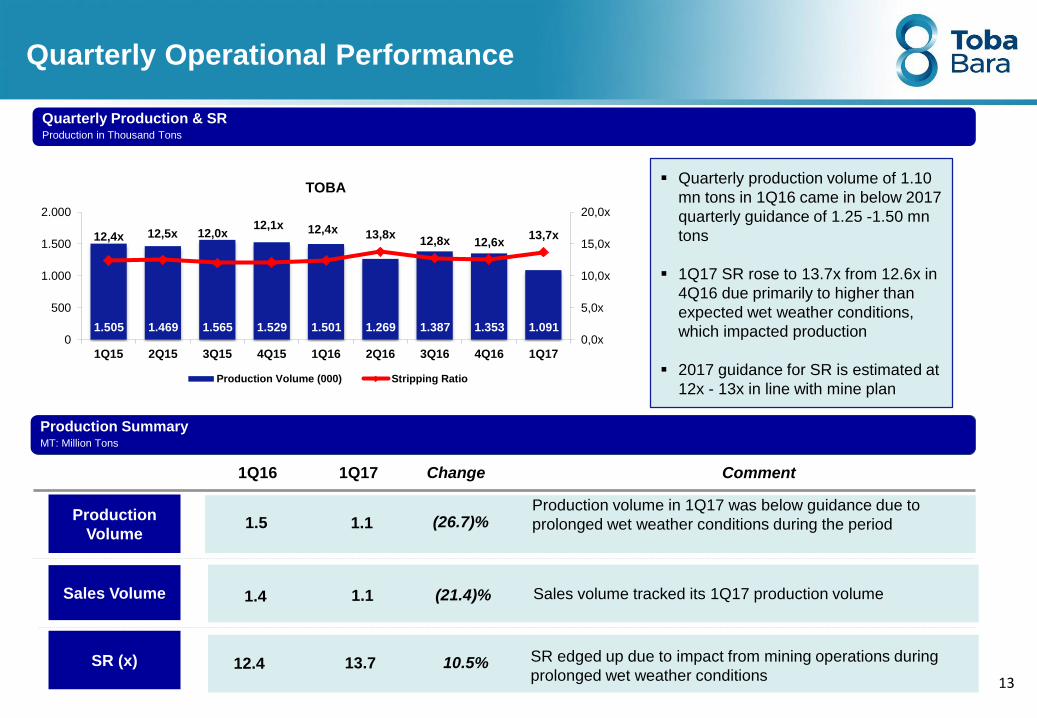

Quarterly Operational Performance

Quarterly Production & SRProduction in Thousand Tons

Production SummaryMT: Million Ton

1Q16 1Q17 Change Comment

Sales Volume

SR (x)

1.4 1.1

12.4 13.7

(21.4)%

10.5%

Sales volume tracked its 1Q17 production volume

SR edged up due to impact from mining operations during

prolonged wet weather conditions

1.5 1.1Production volume in 1Q17 was below guidance due to

prolonged wet weather conditions during the period(26.7)%Production

Volume

Production SummaryMT: Million Tons

Quarterly production volume of 1.10

mn tons in 1Q16 came in below 2017

quarterly guidance of 1.25 -1.50 mn

tons

1Q17 SR rose to 13.7x from 12.6x in

4Q16 due primarily to higher than

expected wet weather conditions,

which impacted production

2017 guidance for SR is estimated at

12x - 13x in line with mine plan

13

1.505 1.469 1.565 1.529 1.501 1.269 1.387 1.353 1.091

12,4x 12,5x 12,0x12,1x 12,4x 13,8x

12,8x 12,6x13,7x

0,0x

5,0x

10,0x

15,0x

20,0x

0

500

1.000

1.500

2.000

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17

TOBA

Production Volume (000) Stripping Ratio

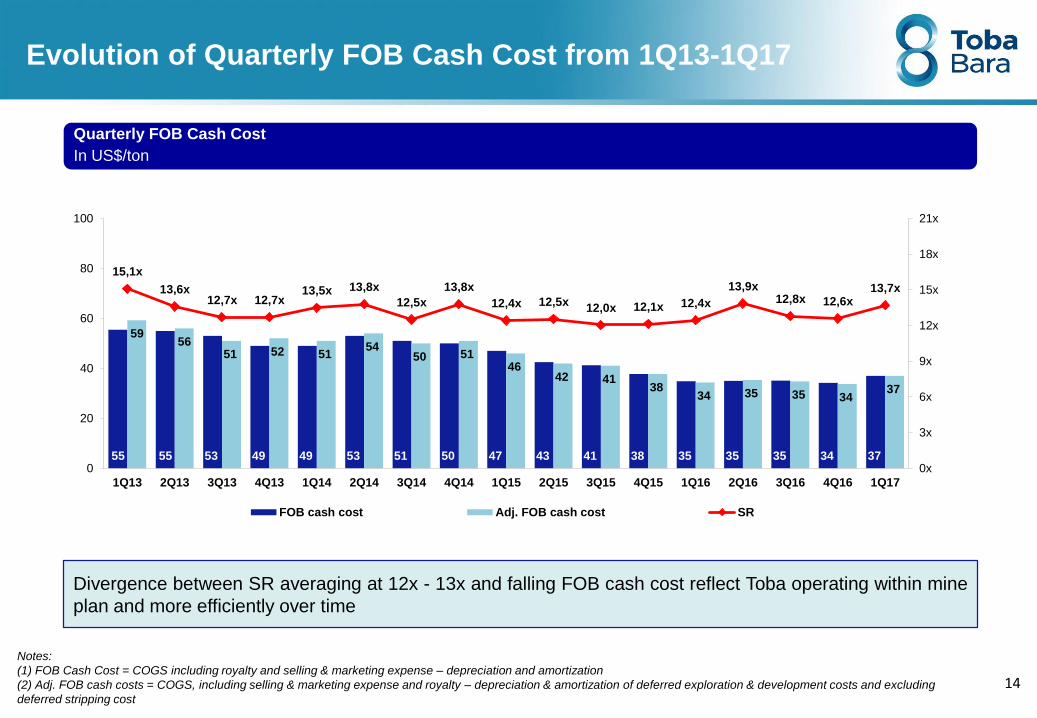

Evolution of Quarterly FOB Cash Cost from 1Q13-1Q17

Quarterly FOB Cash Cost

In US$/ton

Notes:

(1) FOB Cash Cost = COGS including royalty and selling & marketing expense – depreciation and amortization

(2) Adj. FOB cash costs = COGS, including selling & marketing expense and royalty – depreciation & amortization of deferred exploration & development costs and excluding

deferred stripping cost

Divergence between SR averaging at 12x - 13x and falling FOB cash cost reflect Toba operating within mine

plan and more efficiently over time

14

55 55 53 49 49 53 51 50 47 43 41 38 35 35 35 34 37

5956

51 52 51 54

50 51 46

42 41 38

34 35 35 34 37

15,1x

13,6x12,7x 12,7x

13,5x 13,8x

12,5x

13,8x

12,4x 12,5x12,0x 12,1x 12,4x

13,9x12,8x 12,6x

13,7x

0x

3x

6x

9x

12x

15x

18x

21x

0

20

40

60

80

100

1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17

FOB cash cost Adj. FOB cash cost SR

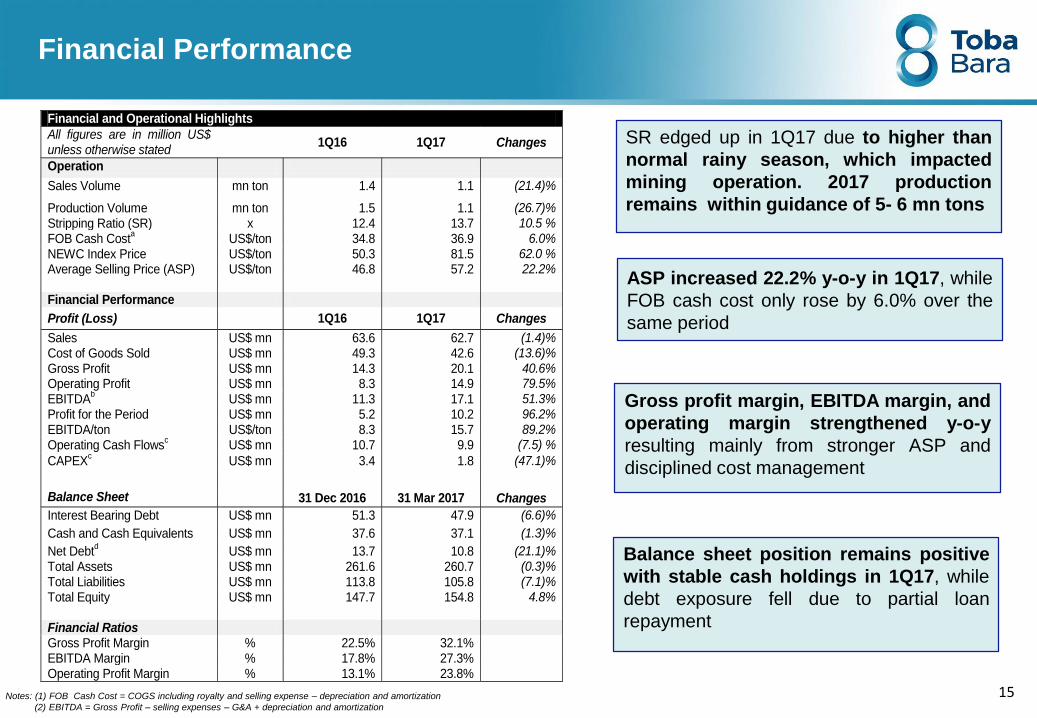

Financial Performance

Notes: (1) FOB Cash Cost = COGS including royalty and selling expense – depreciation and amortization

(2) EBITDA = Gross Profit – selling expenses – G&A + depreciation and amortization

ASP increased 22.2% y-o-y in 1Q17, while

FOB cash cost only rose by 6.0% over the

same period

Balance sheet position remains positive

with stable cash holdings in 1Q17, while

debt exposure fell due to partial loan

repayment

SR edged up in 1Q17 due to higher than

normal rainy season, which impacted

mining operation. 2017 production

remains within guidance of 5- 6 mn tons

15

Gross profit margin, EBITDA margin, and

operating margin strengthened y-o-y

resulting mainly from stronger ASP and

disciplined cost management

Financial and Operational Highlights

All figures are in million US$ unless otherwise stated

1Q16 1Q17 Changes

Operation

Sales Volume mn ton 1.4 1.1 (21.4)%

Production Volume mn ton 1.5 1.1 (26.7)%

Stripping Ratio (SR) x 12.4 13.7 10.5 % FOB Cash Cost

a US$/ton 34.8 36.9 6.0%

NEWC Index Price US$/ton 50.3 81.5 62.0 % Average Selling Price (ASP) US$/ton 46.8 57.2 22.2% Financial Performance

Profit (Loss) 1Q16 1Q17 Changes

Sales US$ mn 63.6 62.7 (1.4)% Cost of Goods Sold US$ mn 49.3 42.6 (13.6)% Gross Profit US$ mn 14.3 20.1 40.6% Operating Profit US$ mn 8.3 14.9 79.5% EBITDA

b US$ mn 11.3 17.1 51.3%

Profit for the Period US$ mn 5.2 10.2 96.2%

EBITDA/ton US$/ton 8.3 15.7 89.2% Operating Cash Flows

c US$ mn 10.7 9.9 (7.5) %

CAPEXc US$ mn 3.4 1.8 (47.1)%

Balance Sheet 31 Dec 2016 31 Mar 2017 Changes

Interest Bearing Debt US$ mn 51.3 47.9 (6.6)%

Cash and Cash Equivalents US$ mn 37.6 37.1 (1.3)%

Net Debtd US$ mn 13.7 10.8 (21.1)%

Total Assets US$ mn 261.6 260.7 (0.3)% Total Liabilities US$ mn 113.8 105.8 (7.1)% Total Equity US$ mn 147.7 154.8 4.8% Financial Ratios Gross Profit Margin % 22.5% 32.1%

EBITDA Margin % 17.8% 27.3% Operating Profit Margin % 13.1% 23.8%

Balance Sheet

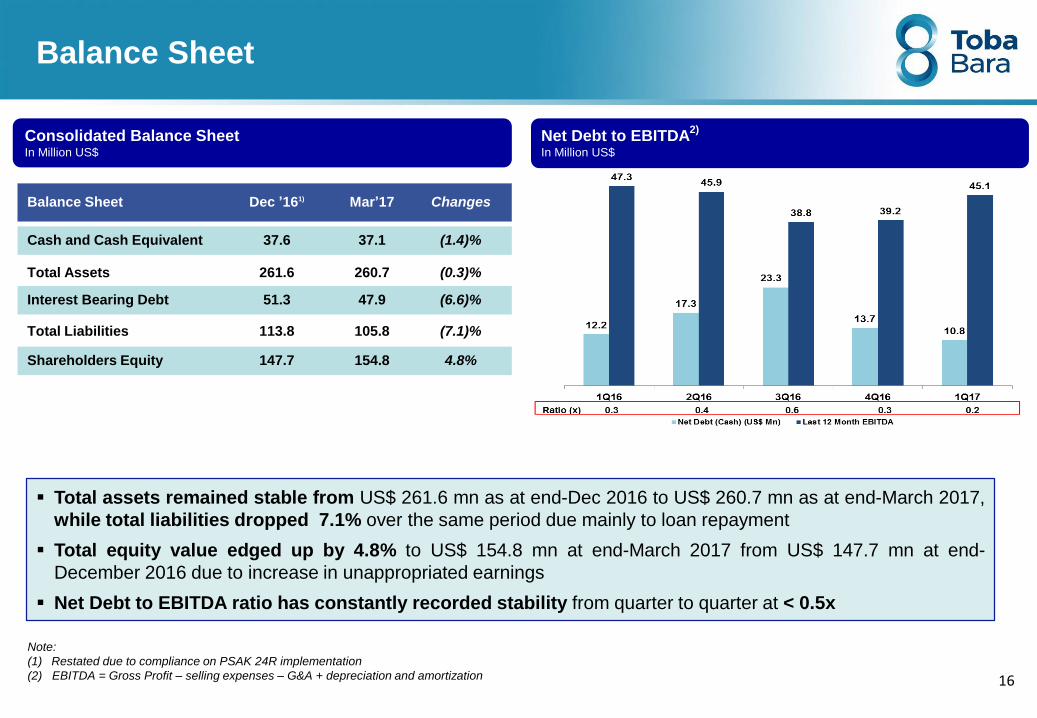

Consolidated Balance SheetIn Million US$

Net Debt to EBITDA2)

In Million US$

Total assets remained stable from US$ 261.6 mn as at end-Dec 2016 to US$ 260.7 mn as at end-March 2017,

while total liabilities dropped 7.1% over the same period due mainly to loan repayment

Total equity value edged up by 4.8% to US$ 154.8 mn at end-March 2017 from US$ 147.7 mn at end-

December 2016 due to increase in unappropriated earnings

Net Debt to EBITDA ratio has constantly recorded stability from quarter to quarter at < 0.5x

Note:

(1) Restated due to compliance on PSAK 24R implementation

(2) EBITDA = Gross Profit – selling expenses – G&A + depreciation and amortization 16

260.7Total Assets 261.6 (0.3)%

Interest Bearing Debt 47.951.3 (6.6)%

Total Liabilities 105.8113.8 (7.1)%

Shareholders Equity 154.8147.7 4.8%

Balance Sheet Dec ’161) ChangesMar’17

Cash and Cash Equivalent 37.6 (1.4)%37.1

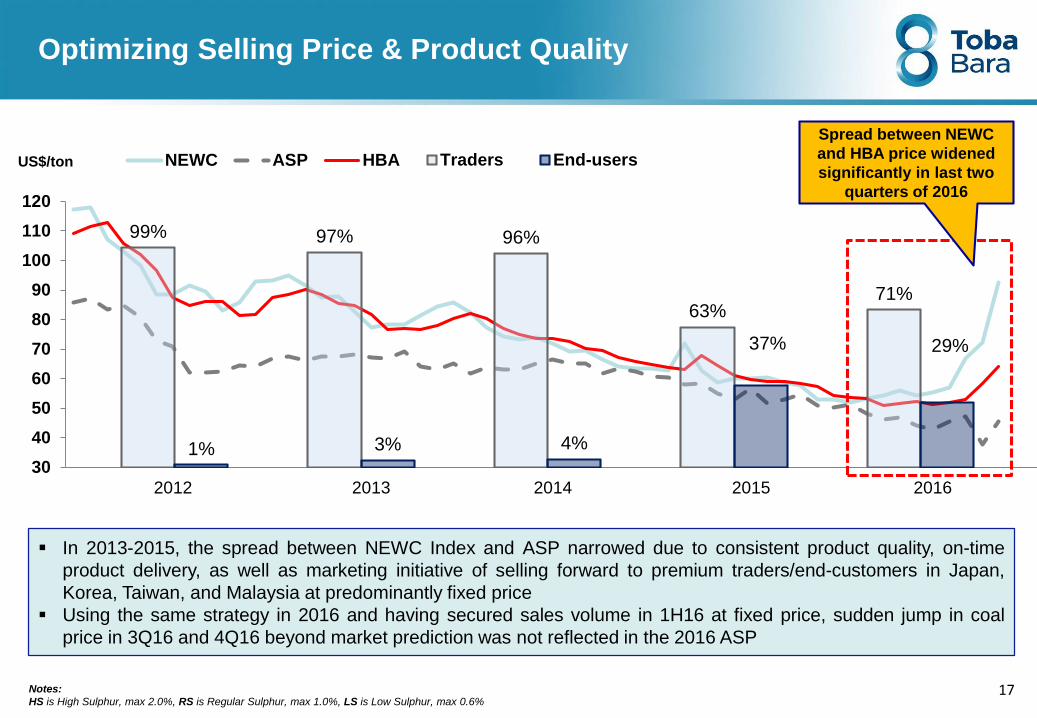

Optimizing Selling Price & Product Quality

30

40

50

60

70

80

90

100

110

120

2012 2013 2014 2015 2016

NEWC ASP HBA

99% 97% 96%

63%71%

1% 3% 4%

37% 29%

Traders End-users

In 2013-2015, the spread between NEWC Index and ASP narrowed due to consistent product quality, on-time

product delivery, as well as marketing initiative of selling forward to premium traders/end-customers in Japan,

Korea, Taiwan, and Malaysia at predominantly fixed price

Using the same strategy in 2016 and having secured sales volume in 1H16 at fixed price, sudden jump in coal

price in 3Q16 and 4Q16 beyond market prediction was not reflected in the 2016 ASP

17Notes:

HS is High Sulphur, max 2.0%, RS is Regular Sulphur, max 1.0%, LS is Low Sulphur, max 0.6%

US$/ton

Spread between NEWC

and HBA price widened

significantly in last two

quarters of 2016

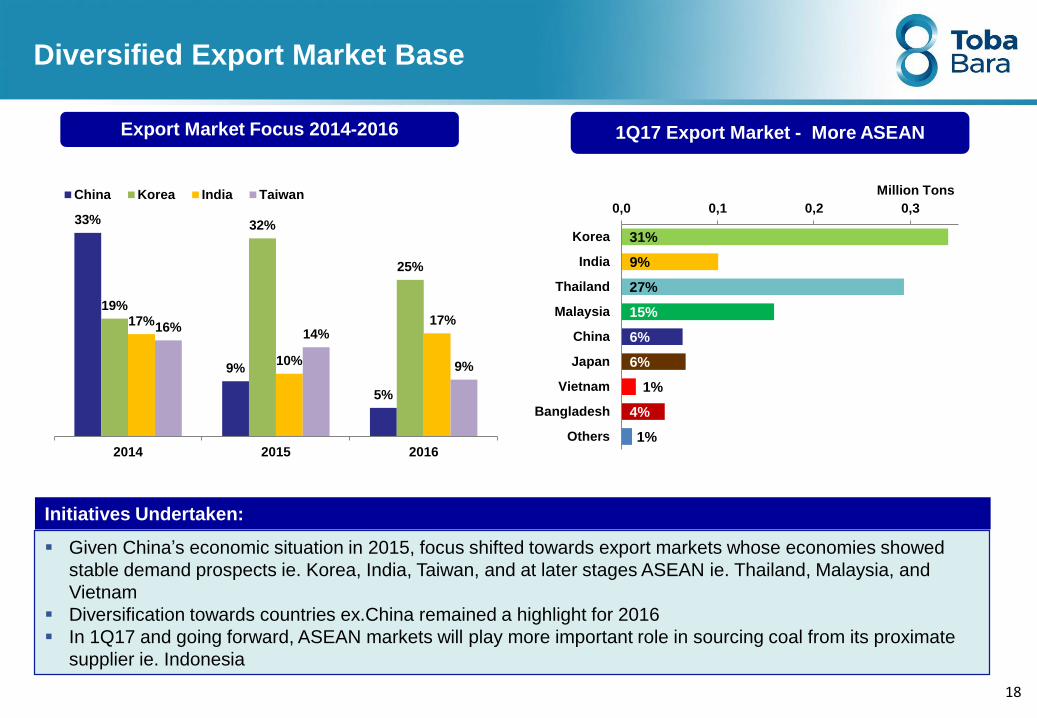

Diversified Export Market Base

Initiatives Undertaken:

Export Market Focus 2014-2016

Given China’s economic situation in 2015, focus shifted towards export markets whose economies showed

stable demand prospects ie. Korea, India, Taiwan, and at later stages ASEAN ie. Thailand, Malaysia, and

Vietnam

Diversification towards countries ex.China remained a highlight for 2016

In 1Q17 and going forward, ASEAN markets will play more important role in sourcing coal from its proximate

supplier ie. Indonesia

18

1Q17 Export Market - More ASEAN

33%

9%

5%

19%

32%

25%

17%

10%

17%16%

14%

9%

2014 2015 2016

China Korea India Taiwan

31%

9%

27%

15%

6%

6%

1%

4%

1%

0,0 0,1 0,2 0,3

Korea

India

Thailand

Malaysia

China

Japan

Vietnam

Bangladesh

Others

Million Tons

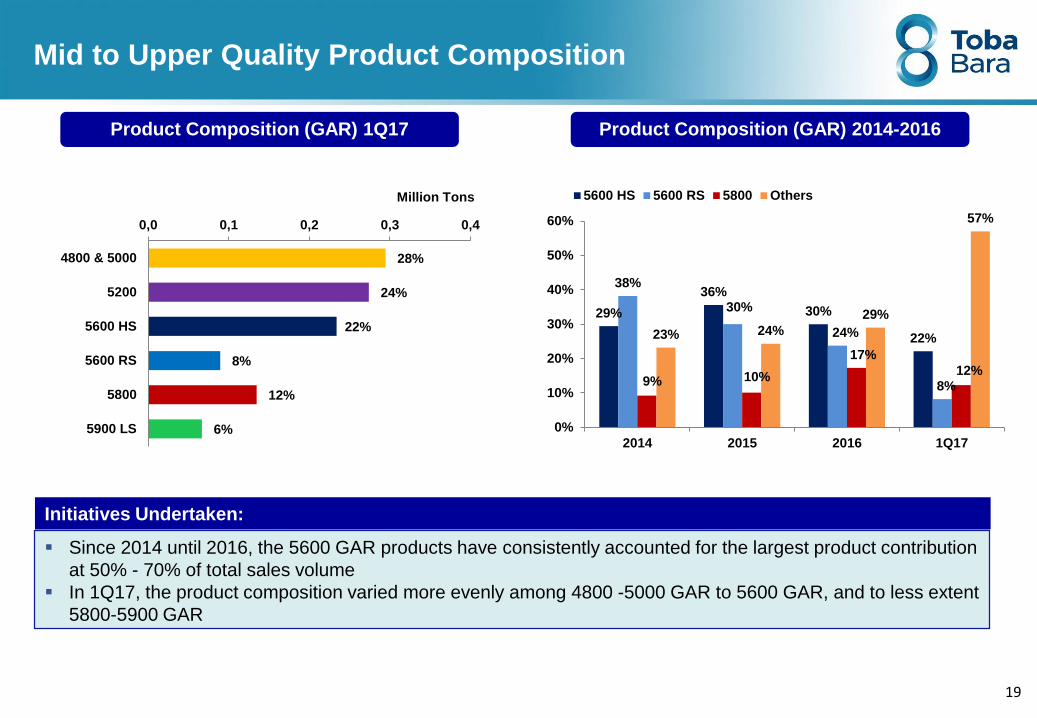

Mid to Upper Quality Product Composition

Initiatives Undertaken:

Product Composition (GAR) 1Q17

Since 2014 until 2016, the 5600 GAR products have consistently accounted for the largest product contribution

at 50% - 70% of total sales volume

In 1Q17, the product composition varied more evenly among 4800 -5000 GAR to 5600 GAR, and to less extent

5800-5900 GAR

19

Product Composition (GAR) 2014-2016

29%

36%

30%

22%

38%

30%

24%

8%9% 10%

17%

12%

23% 24%

29%

57%

0%

10%

20%

30%

40%

50%

60%

2014 2015 2016 1Q17

5600 HS 5600 RS 5800 Others

28%

24%

22%

8%

12%

6%

0,0 0,1 0,2 0,3 0,4

4800 & 5000

5200

5600 HS

5600 RS

5800

5900 LS

Million Tons

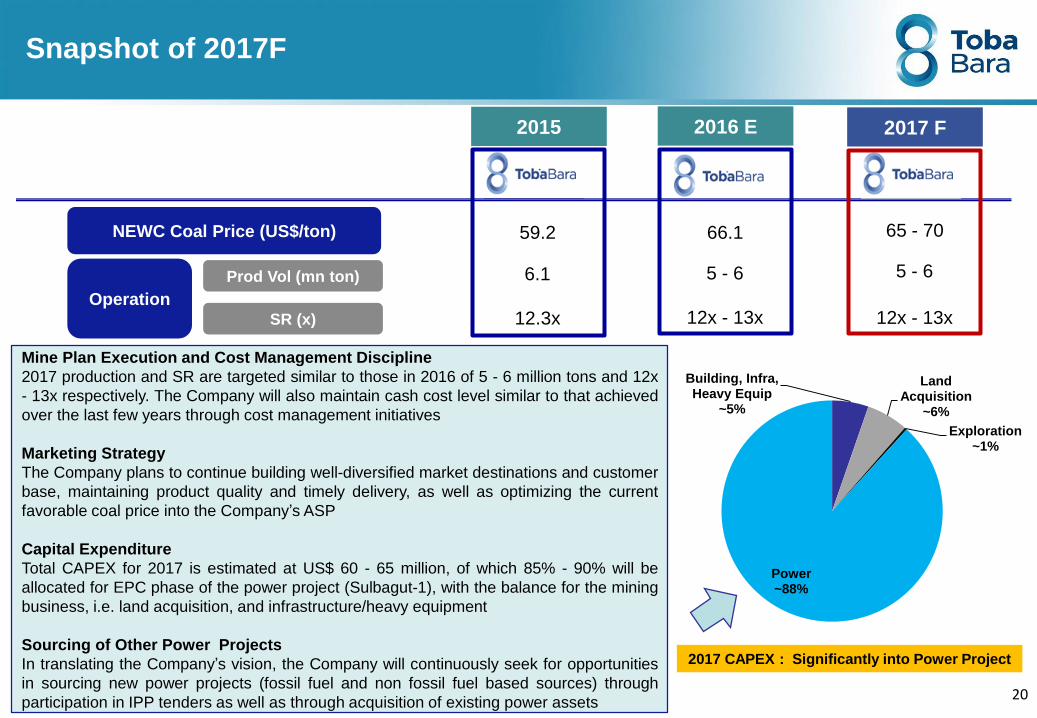

Snapshot of 2017F

Operation

Prod Vol (mn ton)

SR (x) 12x - 13x

5 - 6

2015

12.3x

6.1

NEWC Coal Price (US$/ton) 66.159.2

Mine Plan Execution and Cost Management Discipline

2017 production and SR are targeted similar to those in 2016 of 5 - 6 million tons and 12x

- 13x respectively. The Company will also maintain cash cost level similar to that achieved

over the last few years through cost management initiatives

Marketing Strategy

The Company plans to continue building well-diversified market destinations and customer

base, maintaining product quality and timely delivery, as well as optimizing the current

favorable coal price into the Company’s ASP

Capital Expenditure

Total CAPEX for 2017 is estimated at US$ 60 - 65 million, of which 85% - 90% will be

allocated for EPC phase of the power project (Sulbagut-1), with the balance for the mining

business, i.e. land acquisition, and infrastructure/heavy equipment

Sourcing of Other Power Projects

In translating the Company’s vision, the Company will continuously seek for opportunities

in sourcing new power projects (fossil fuel and non fossil fuel based sources) through

participation in IPP tenders as well as through acquisition of existing power assets20

12x - 13x

5 - 6

2017 F

65 - 70

2016 E

Building, Infra, Heavy Equip

~5%

Land Acquisition

~6%

Exploration~1%

Power~88%

2017 CAPEX : Significantly into Power Project

21

Performance HighlightsPerformance Highlights2Strategy to Venture into Power3

Expansion Strategy for Sustainable Growth & Value

22

2. Forward-Looking Expansion

Upstream Expansion

INTEGRATED MINING AND ENERGY COMPANY

Participate in PLN Open

Tender Projects 1

Identify opportunity to

develop captive Power

Plant in Industrial Estate

2

Evaluate opportunity to

enter Renewable-based

Power Business

3

Continuous

Operational

Efficiency

Improvement to

Sustain Margins

1. Existing Mines

Sustainability

Midstream Business

Diversification

Target coal mining

company that can create

synergy with TOBA coal

mining assets

1

Target coal mining

company with prospects

to supply coal-fired mine-

mouth power plant

2

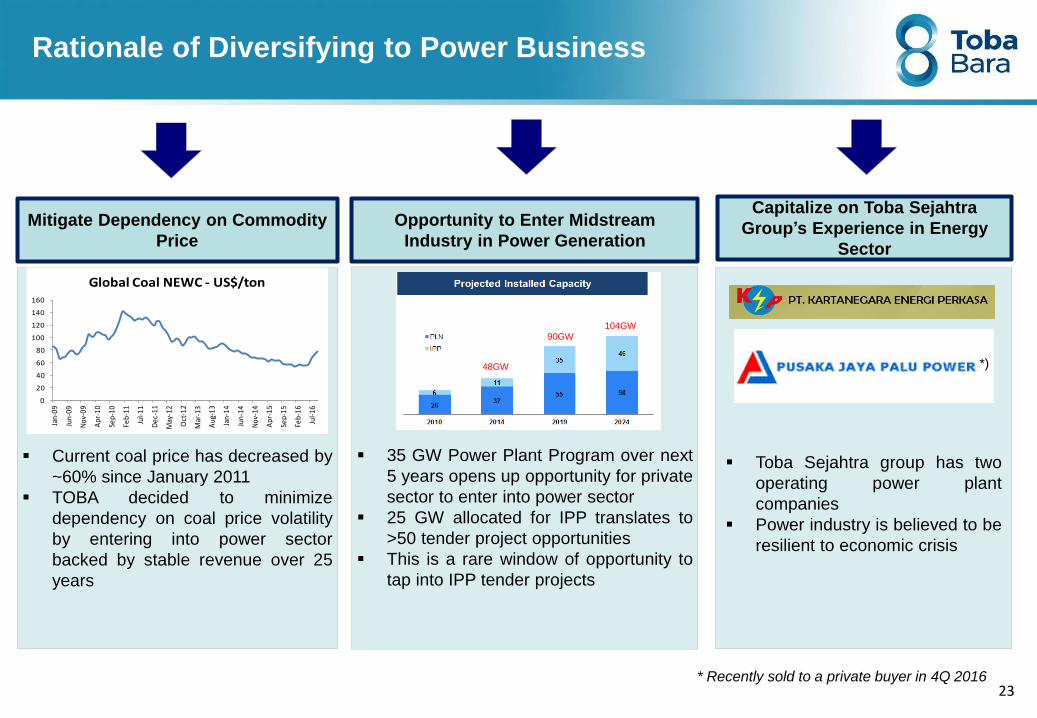

Rationale of Diversifying to Power Business

Mitigate Dependency on Commodity

Price

Opportunity to Enter Midstream

Industry in Power Generation

Capitalize on Toba Sejahtra

Group’s Experience in Energy

Sector

Current coal price has decreased by

~60% since January 2011

TOBA decided to minimize

dependency on coal price volatility

by entering into power sector

backed by stable revenue over 25

years

35 GW Power Plant Program over next

5 years opens up opportunity for private

sector to enter into power sector

25 GW allocated for IPP translates to

>50 tender project opportunities

This is a rare window of opportunity to

tap into IPP tender projects

Toba Sejahtra group has two

operating power plant

companies

Power industry is believed to be

resilient to economic crisis

48GW

90GW104GW

23

0

20

40

60

80

100

120

140

160

Jan-

09

Jun

-09

Nov

-09

Apr

-10

Sep-

10

Feb-

11

Jul-1

1

Dec

-11

May

-12

Oct

-12

Mar

-13

Aug

-13

Jan-

14

Jun

-14

Nov

-14

Apr

-15

Sep-

15

Feb-

16

Jul-1

6

Global Coal NEWC - US$/ton

* Recently sold to a private buyer in 4Q 2016

*)

24

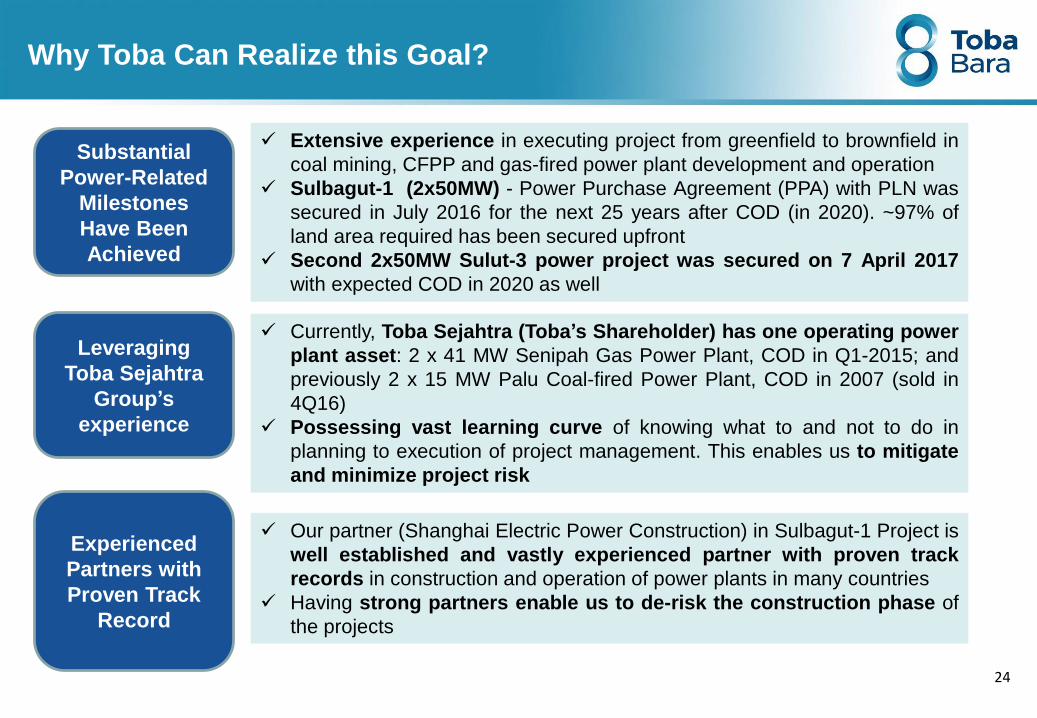

Why Toba Can Realize this Goal?

Extensive experience in executing project from greenfield to brownfield in

coal mining, CFPP and gas-fired power plant development and operation

Sulbagut-1 (2x50MW) - Power Purchase Agreement (PPA) with PLN was

secured in July 2016 for the next 25 years after COD (in 2020). ~97% of

land area required has been secured upfront

Second 2x50MW Sulut-3 power project was secured on 7 April 2017

with expected COD in 2020 as well

Our partner (Shanghai Electric Power Construction) in Sulbagut-1 Project is

well established and vastly experienced partner with proven track

records in construction and operation of power plants in many countries

Having strong partners enable us to de-risk the construction phase of

the projects

Substantial

Power-Related

Milestones

Have Been

Achieved

Experienced

Partners with

Proven Track

Record

Currently, Toba Sejahtra (Toba’s Shareholder) has one operating power

plant asset: 2 x 41 MW Senipah Gas Power Plant, COD in Q1-2015; and

previously 2 x 15 MW Palu Coal-fired Power Plant, COD in 2007 (sold in

4Q16)

Possessing vast learning curve of knowing what to and not to do in

planning to execution of project management. This enables us to mitigate

and minimize project risk

Leveraging

Toba Sejahtra

Group’s

experience

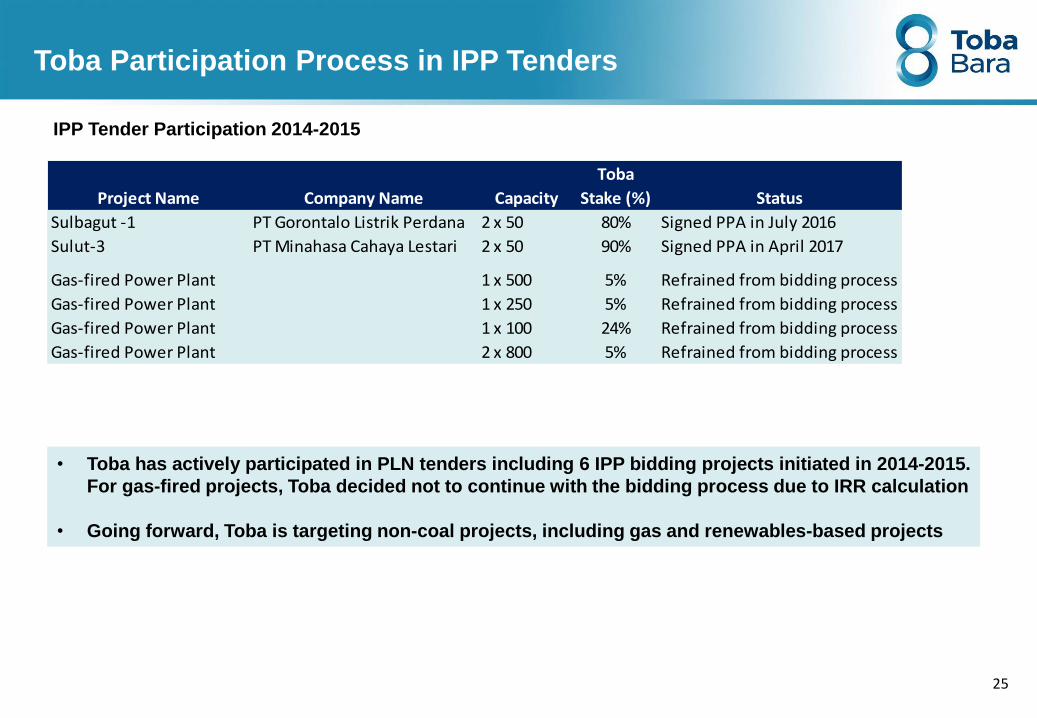

Toba Participation Process in IPP Tenders

IPP Tender Participation 2014-2015

• Toba has actively participated in PLN tenders including 6 IPP bidding projects initiated in 2014-2015.

For gas-fired projects, Toba decided not to continue with the bidding process due to IRR calculation

• Going forward, Toba is targeting non-coal projects, including gas and renewables-based projects

25

Project Name Company Name Capacity

Toba

Stake (%) Status

Sulbagut -1 PT Gorontalo Listrik Perdana 2 x 50 80% Signed PPA in July 2016

Sulut-3 PT Minahasa Cahaya Lestari 2 x 50 90% Signed PPA in April 2017

Gas-fired Power Plant 1 x 500 5% Refrained from bidding process

Gas-fired Power Plant 1 x 250 5% Refrained from bidding process

Gas-fired Power Plant 1 x 100 24% Refrained from bidding process

Gas-fired Power Plant 2 x 800 5% Refrained from bidding process

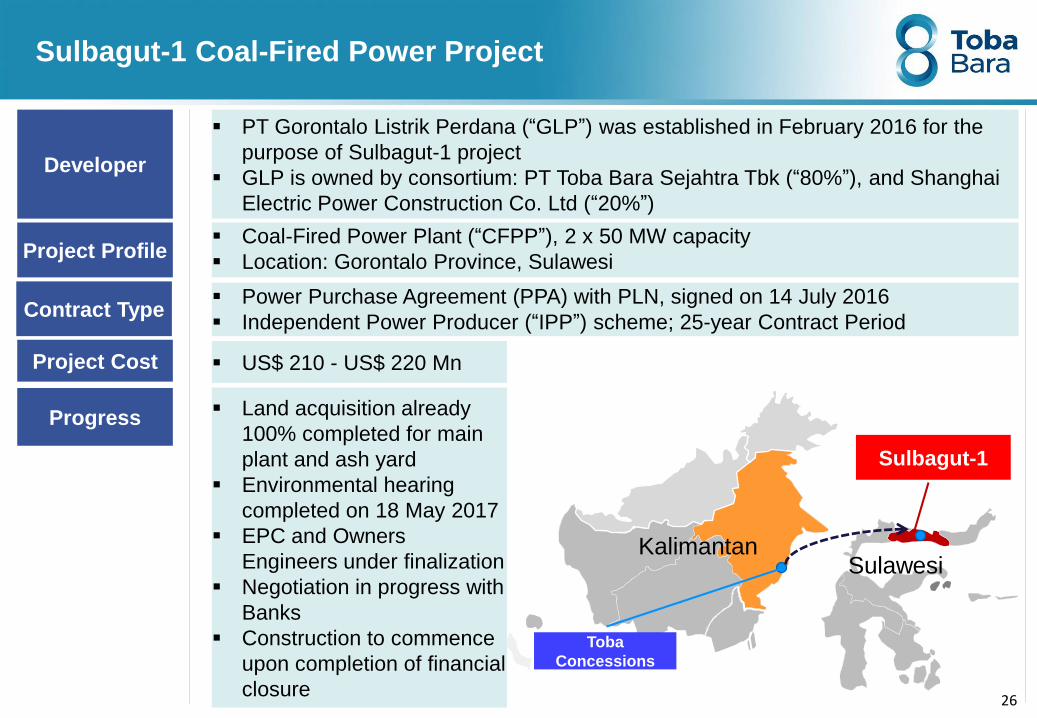

PT Gorontalo Listrik Perdana (“GLP”) was established in February 2016 for the

purpose of Sulbagut-1 project

GLP is owned by consortium: PT Toba Bara Sejahtra Tbk (“80%”), and Shanghai

Electric Power Construction Co. Ltd (“20%”)

Sulbagut-1 Coal-Fired Power Project

Developer

Contract Type Power Purchase Agreement (PPA) with PLN, signed on 14 July 2016

Independent Power Producer (“IPP”) scheme; 25-year Contract Period

Project Cost US$ 210 - US$ 220 Mn

Progress

Project Profile Coal-Fired Power Plant (“CFPP”), 2 x 50 MW capacity

Location: Gorontalo Province, Sulawesi

KalimantanSulawesi

Sulbagut-1

Toba

Concessions

26

Land acquisition already

100% completed for main

plant and ash yard

Environmental hearing

completed on 18 May 2017

EPC and Owners

Engineers under finalization

Negotiation in progress with

Banks

Construction to commence

upon completion of financial

closure

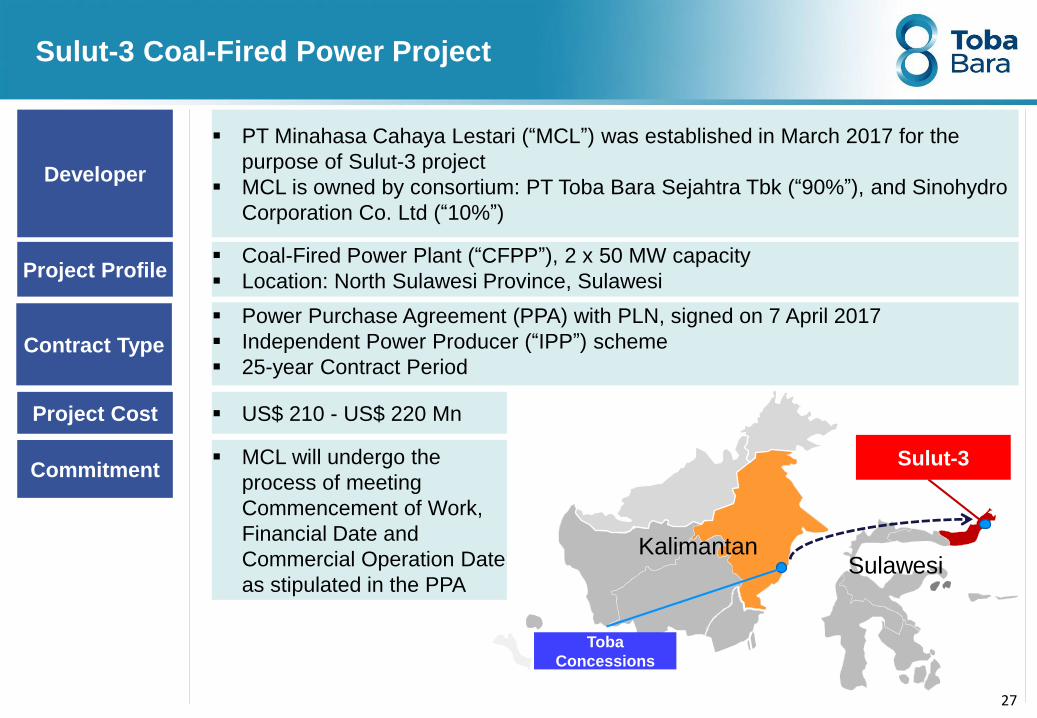

PT Minahasa Cahaya Lestari (“MCL”) was established in March 2017 for the

purpose of Sulut-3 project

MCL is owned by consortium: PT Toba Bara Sejahtra Tbk (“90%”), and Sinohydro

Corporation Co. Ltd (“10%”)

Sulut-3 Coal-Fired Power Project

Developer

Contract Type

Power Purchase Agreement (PPA) with PLN, signed on 7 April 2017

Independent Power Producer (“IPP”) scheme

25-year Contract Period

Project Cost US$ 210 - US$ 220 Mn

Commitment MCL will undergo the

process of meeting

Commencement of Work,

Financial Date and

Commercial Operation Date

as stipulated in the PPA

Project Profile Coal-Fired Power Plant (“CFPP”), 2 x 50 MW capacity

Location: North Sulawesi Province, Sulawesi

KalimantanSulawesi

Sulut-3

Toba

Concessions

27

28

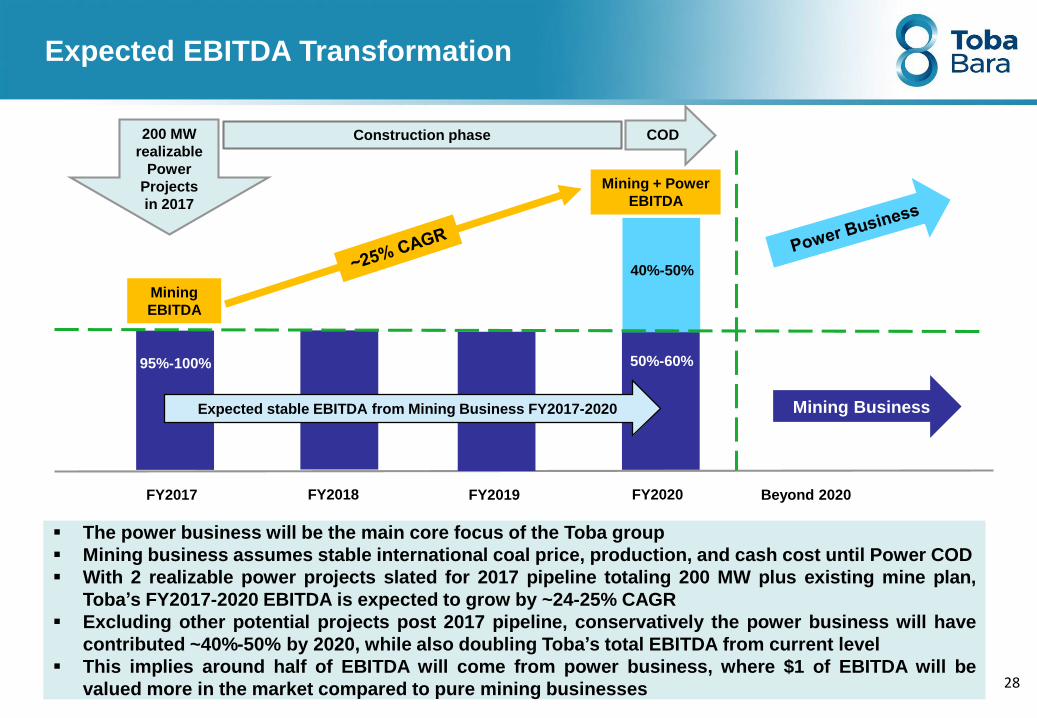

Mining

EBITDA

Expected stable EBITDA from Mining Business FY2017-2020

40%-50%

50%-60%

FY2017 FY2020 FY2019 FY2018

The power business will be the main core focus of the Toba group

Mining business assumes stable international coal price, production, and cash cost until Power COD

With 2 realizable power projects slated for 2017 pipeline totaling 200 MW plus existing mine plan,

Toba’s FY2017-2020 EBITDA is expected to grow by ~24-25% CAGR

Excluding other potential projects post 2017 pipeline, conservatively the power business will have

contributed ~40%-50% by 2020, while also doubling Toba’s total EBITDA from current level

This implies around half of EBITDA will come from power business, where $1 of EBITDA will be

valued more in the market compared to pure mining businesses

Expected EBITDA Transformation

Mining + Power

EBITDA

95%-100%

200 MW

realizable

Power

Projects

in 2017

Construction phase

Mining Business

Beyond 2020

COD

29

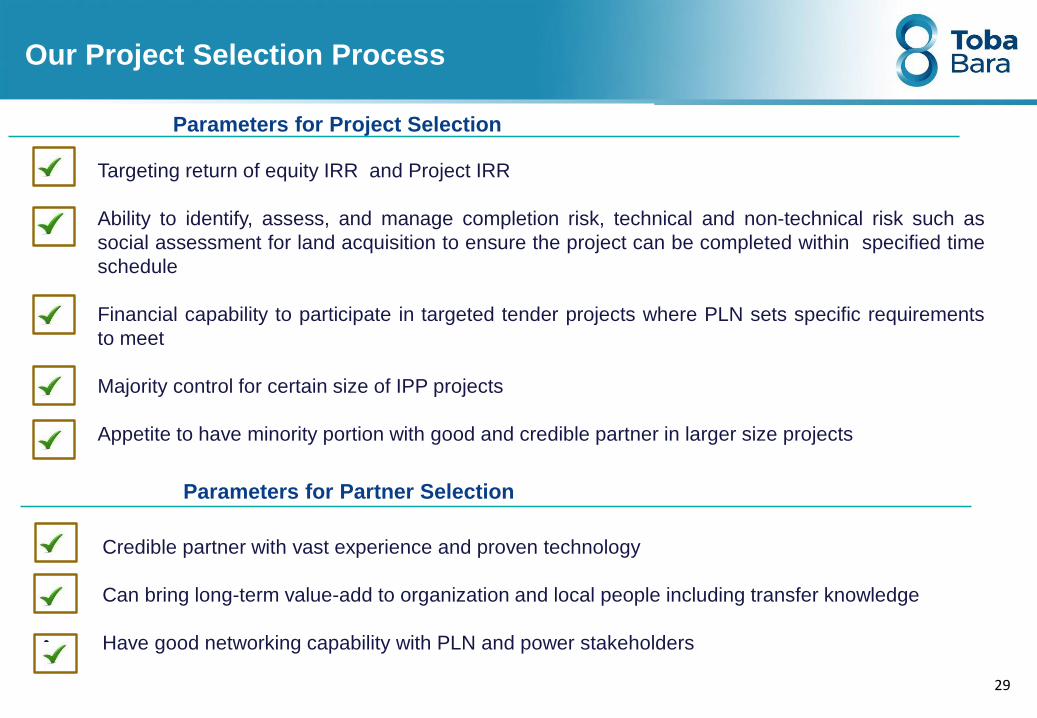

Our Project Selection Process

Targeting return of equity IRR and Project IRR

Ability to identify, assess, and manage completion risk, technical and non-technical risk such as

social assessment for land acquisition to ensure the project can be completed within specified time

schedule

Financial capability to participate in targeted tender projects where PLN sets specific requirements

to meet

Majority control for certain size of IPP projects

Appetite to have minority portion with good and credible partner in larger size projects

• Credible partner with vast experience and proven technology

• Can bring long-term value-add to organization and local people including transfer knowledge

• Have good networking capability with PLN and power stakeholders

Parameters for Project Selection

Parameters for Partner Selection

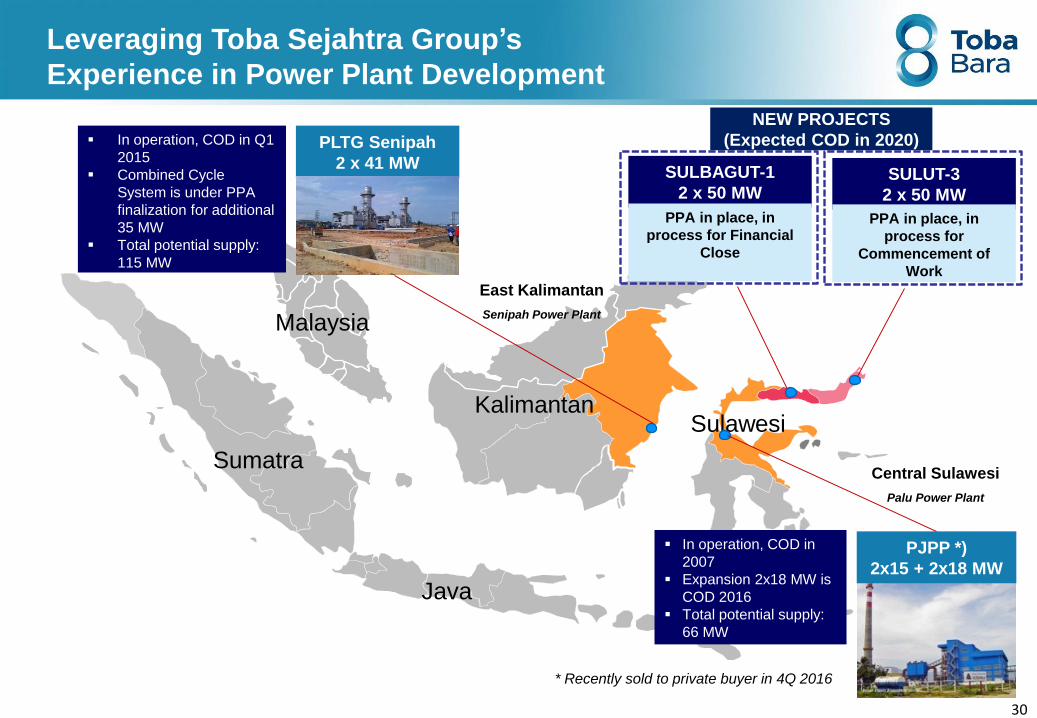

Leveraging Toba Sejahtra Group’s

Experience in Power Plant Development

Sumatra

Kalimantan

Java

Sulawesi

Malaysia

East Kalimantan

Senipah Power Plant

Central Sulawesi

Palu Power Plant

PLTG Senipah

2 x 41 MW

PJPP *)

2x15 + 2x18 MW

In operation, COD in Q1

2015

Combined Cycle

System is under PPA

finalization for additional

35 MW

Total potential supply:

115 MW

In operation, COD in

2007

Expansion 2x18 MW is

COD 2016

Total potential supply:

66 MW

30

SULBAGUT-1

2 x 50 MW

PPA in place, in

process for Financial

Close

NEW PROJECTS

(Expected COD in 2020)

* Recently sold to private buyer in 4Q 2016

SULUT-3

2 x 50 MW

PPA in place, in

process for

Commencement of

Work

THANK YOU

5.5%7.1% 7.5% 8.0%

6.4% 6.4% 6.4% 6.4% 6.4% 6.4%

217244

268292

315340

366394

425

457

0

50

100

150

200

250

300

350

400

450

500

0

0.05

0.1

0.15

0.2

0.25

0.3

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

839932

1,0111,089

1,1621,241

1,3221,409

1,5061,604

6.2% 6.0% 5.6% 5.0% 4.8%

156172

186 196 200

0

50

100

150

200

250

300

350

400

450

500

0

0.05

0.1

0.15

0.2

0.25

0.3

2011 2012 2013 2014 2015

646

702746

779 784

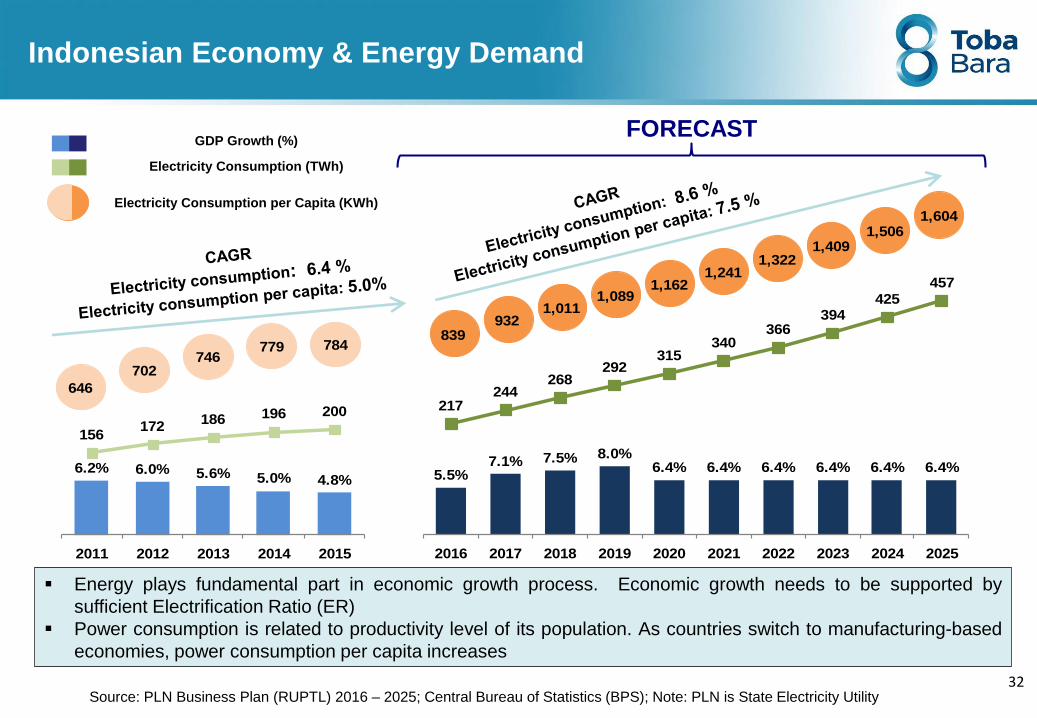

Indonesian Economy & Energy Demand

Source: PLN Business Plan (RUPTL) 2016 – 2025; Central Bureau of Statistics (BPS); Note: PLN is State Electricity Utility

Energy plays fundamental part in economic growth process. Economic growth needs to be supported by

sufficient Electrification Ratio (ER)

Power consumption is related to productivity level of its population. As countries switch to manufacturing-based

economies, power consumption per capita increases

GDP Growth (%)

Electricity Consumption (TWh)

Electricity Consumption per Capita (KWh)

FORECAST

32

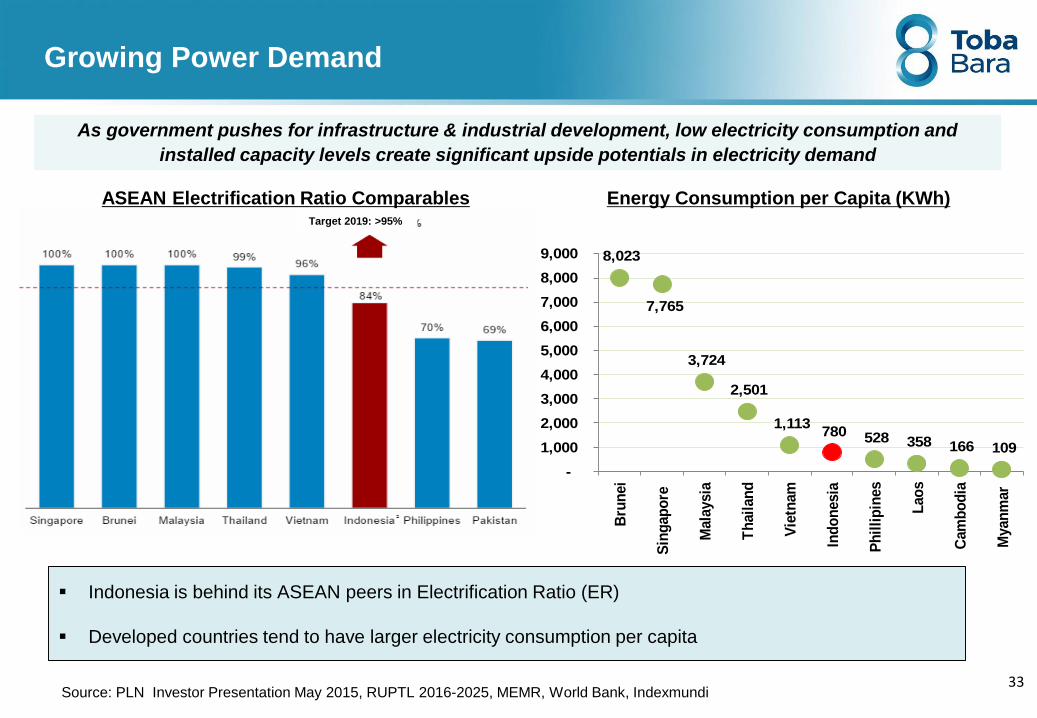

Growing Power Demand

As government pushes for infrastructure & industrial development, low electricity consumption and

installed capacity levels create significant upside potentials in electricity demand

Indonesia is behind its ASEAN peers in Electrification Ratio (ER)

Developed countries tend to have larger electricity consumption per capita

ASEAN Electrification Ratio ComparablesTarget 2019: >95%

Energy Consumption per Capita (KWh)

Source: PLN Investor Presentation May 2015, RUPTL 2016-2025, MEMR, World Bank, Indexmundi

8,023

7,765

3,724

2,501

1,113 780 528 358 166 109

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Bru

nei

Sin

gap

ore

Mala

ysia

Th

ail

an

d

Vie

tnam

Ind

on

esia

Ph

illi

pin

es

Lao

s

Cam

bo

dia

Myan

mar

33

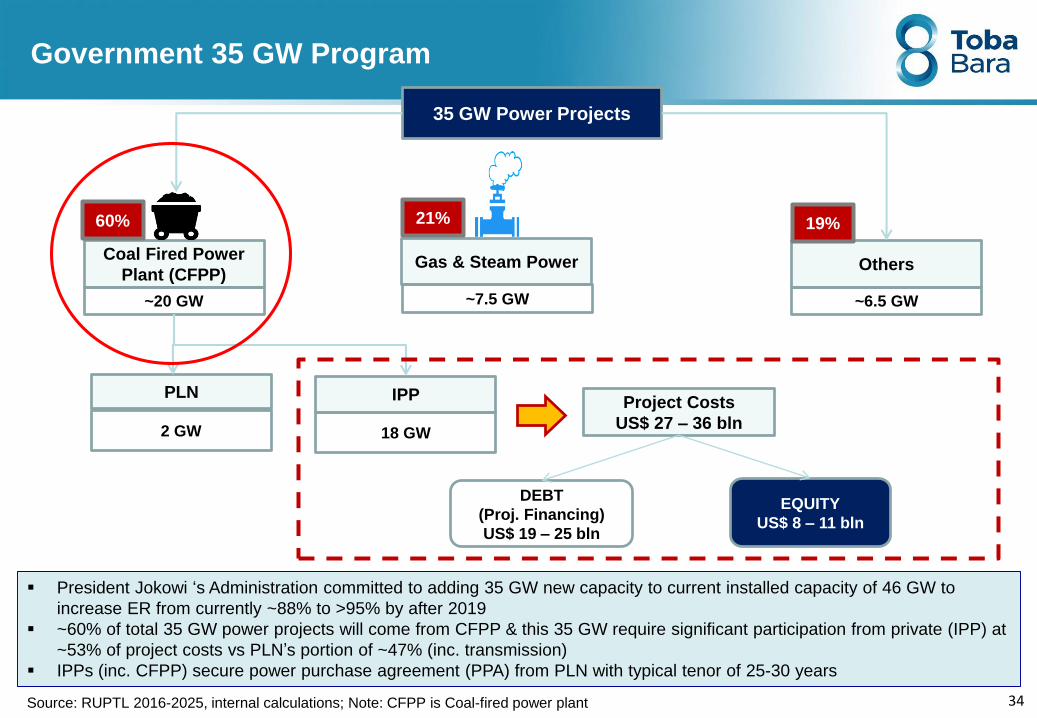

Government 35 GW Program

35 GW Power Projects

Coal Fired Power

Plant (CFPP)Gas & Steam Power Others

~20 GW ~7.5 GW ~6.5 GW

PLN

2 GW

IPP

18 GW

Project Costs

US$ 27 – 36 bln

60% 21% 19%

DEBT

(Proj. Financing)

US$ 19 – 25 bln

EQUITY

US$ 8 – 11 bln

President Jokowi ‘s Administration committed to adding 35 GW new capacity to current installed capacity of 46 GW to

increase ER from currently ~88% to >95% by after 2019

~60% of total 35 GW power projects will come from CFPP & this 35 GW require significant participation from private (IPP) at

~53% of project costs vs PLN’s portion of ~47% (inc. transmission)

IPPs (inc. CFPP) secure power purchase agreement (PPA) from PLN with typical tenor of 25-30 years

Source: RUPTL 2016-2025, internal calculations; Note: CFPP is Coal-fired power plant 34

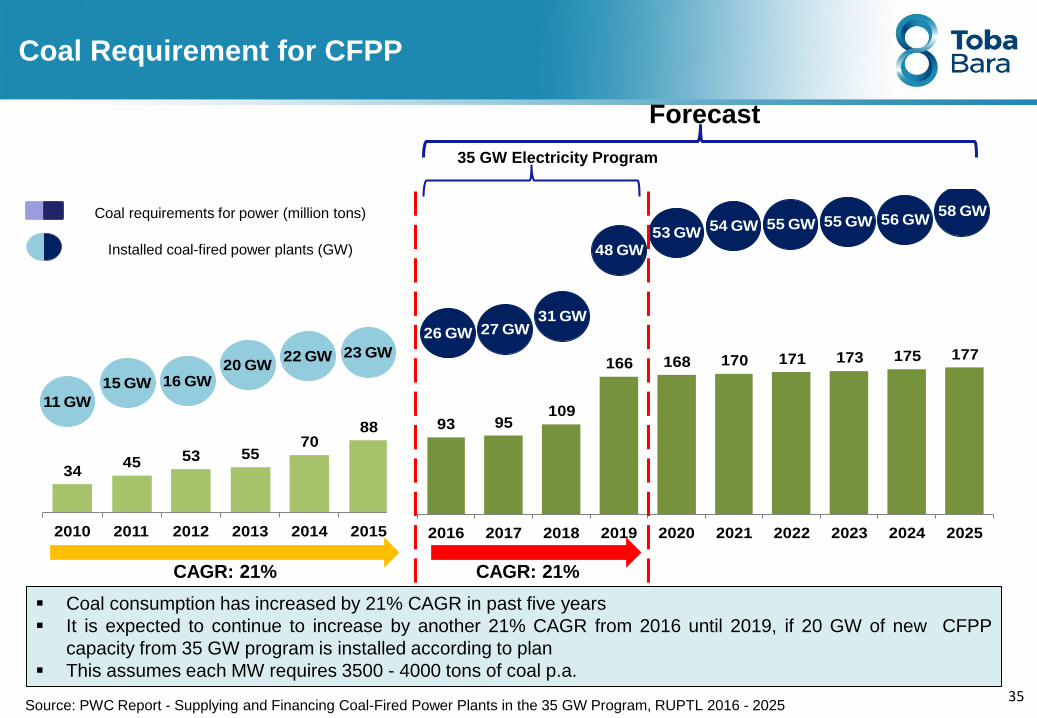

3445 53 55

7088

2010 2011 2012 2013 2014 2015

93 95109

166 168 170 171 173 175 177

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

11 GW

15 GW 16 GW20 GW

22 GW 23 GW

26 GW 27 GW31 GW

48 GW53 GW 54 GW 55 GW 55 GW 56 GW

58 GW

Coal Requirement for CFPP

Coal requirements for power (million tons)

Installed coal-fired power plants (GW)

CAGR: 21%CAGR: 21%

Coal consumption has increased by 21% CAGR in past five years

It is expected to continue to increase by another 21% CAGR from 2016 until 2019, if 20 GW of new CFPP

capacity from 35 GW program is installed according to plan

This assumes each MW requires 3500 - 4000 tons of coal p.a.

35 GW Electricity Program

Source: PWC Report - Supplying and Financing Coal-Fired Power Plants in the 35 GW Program, RUPTL 2016 - 2025

Forecast

35