to: mjg capital limited partners from: matt geiger date

TRANSCRIPT

To: MJGCapitalLimitedPartnersFrom: MattGeiger Date: August1,2016Subject: 2016FirstHalfReview BelowissetforthTheMJGCapitalFund,LP’sperformancethroughJune30,2016. 6MonthPerformance:TheMJGCapitalFund,LP(netofallfeesandexpenses) 67.54%S&P500 2.69%S&P/TSXVentureCompositeIndex 38.96%1YearPerformance:TheMJGCapitalFund,LP(netofallfeesandexpenses) 15.15%S&P500 1.74%S&P/TSXVentureCompositeIndex 8.81%3YearPerformance:TheMJGCapitalFund,LP(netofallfeesandexpenses) (19.76)%S&P500 30.67%S&P/TSXVentureCompositeIndex (17.09)%PerformanceSinceInception(9/1/11):TheMJGCapitalFund,LP(netofallfeesandexpenses) (71.75)%S&P500 72.19%S&P/TSXVentureCompositeIndex (59.66)%

Note:AllreturnsforMJGCapitalpartnersareestimatedandsubjecttothecompletionofanauditatafuturedate.Thereturnsforeachlimitedpartnermayvarydependinguponthetimingoftheirindividualcontributionsandwithdrawals.

1

Introduction&PartnershipUpdateThisisTheMJGCapitalFund,LP’stenthsemi-annualletter.ThePartnershipwasformedfifty-eightmonthsagoandtheresultsaredetailedonthepreviouspage.TheS&P500represents“thealternativeinvestmentofchoice”,whiletheTSXVenture(alsoknownasthe“TSXV”)istheclosestproxytotheuniverseofresourceequitiesthatthePartnershipselectsfrom.Whatwe’veseenoverthepastsixmonthshasbeennothingshortofextraordinary,andisyetanotherexampleofthebipolarnatureofthejuniorresourcemarket(andthecyclicalityofresourceextractiveindustriesingeneral).WhowouldhavethoughtduringthebleakdaysofDecember2015that,ameresixmonthslater,hopeandcapitalwouldpourintotheminingspaceinthewaythatithas.Thedevastating,multi-yearbearmarketthatbeganin2011hasfinallyrunitscourse,andwearenow150daysintoanewbullmarketthathassofarbeenverypowerful.Whetherthisuptrendlastsforthreeyearsorsixyearsisanybody’sguess,butIwillsaywithsomeconfidencethattheremainderof2016,thewholeof2017,andthewhole2018willbeatrulygoldenperiodforboththePartnershipandlikemindedinvestors.FocusingspecificallyonthePartnership,Iseethreemainpointsofencouragement:1.WeoutperformedtheTSXVbyroughly75%which,forthetimebeingatleast,indicatesthatour18holdingsareoutperformingthejuniorminingspaceatlarge.2.Overthepastyear,boththePartnershipandtheTSXVhavehandilyoutperformedtheS&P500–whichsupportsmybeliefthatwearewitnessingthebeginningofamassivetransitionintohardassets.3.Itwasabusy6months–weparticipatedin7privateplacementsovertheperiod(Ireviewedroughly40deals).Theadvantageofdoingprivateplacementsisthewarrantsthatcomeattachedwiththedeal.Thesewarrantsprovideyoufreeupsideonyourinvestmentthatyoudon’tgetfrombuyingcommonshares;thekeyisaccesstothedeal.IstatedintheJanuary2016letter:“Theopportunitiescurrentlyavailableinthenaturalresourceindustryareastounding.Inthiscyclicalindustry,whenthingsturn,theydosodramatically.We'retalkingabout300-1000%portfoliogainsover3-5yearperiods.”

2

Evenwiththedramaticgainsseensofarin2016,Istillechothissentiment–weareearlyinthiscycleanditisafantastictimetobeintelligentlyputtingmoneytoworkinpreciousmetal,energymetal,andevenindustrialmetalinvestments.Inthisletter’sMarketOutlook,IdiscusswhyI’mconfidentthatweareinanewbullmarket….andwhyitshouldbeofsimilardurationandmagnitudetothebearmarketwejustendured.ThenIcommentontheperformanceofspecificcommoditiesandhowIexpectthemtobehaveoverthecourseofthisbullmarket. In the Overview of Partnership Holdings, I provide information on how thePartnership is allocating our capital by (1) commodity, (2) jurisdiction, and (3)operationalphase.Keepinmindthatwehave18holdings(allresource-focused)atcurrent.I conclude by presenting twoFeatured Investments (GoldenArrowResources andExcelsiorMining)aswellasupdatesoncompaniesfeaturedinpastletters(AlmadexMinerals,TFSCorporation,NevsunResources,andWesternLithium).MarketOutlookWeAreInANewResourceBullMarketAfterfourgrindingyearsoffallingmetalpricesandvanishingmarketcapitalizations,wehaveseenastunningshiftinmarketsentimentsincemid-January.Multiplephysicalcommoditiesarenowintechnicalbullmarketsandresourceequitiesinparticularhaveenjoyedaspectacular2016thusfar.Itisobvioustomethatweareintheearlystagesofanewbullmarketforthefollowingreasons:1.Metalpricesareagainontherise.Particularstandoutsinclude:silver,lithium,zinc,gold,platinum,andpalladium.Alloftheaforementionedmetalshaveenterednewtechnicalbullmarketsin2016andseemtobebuildingmomentum.Ittookfourpainfulyears,butthisprovesyetagainthatlowpricesarethebestcureforlowprices.Whenthepriceofaparticularcommoditydropsprecipitously,twophenomenoninevitablyoccur:(i)highercostsuppliersofthecommoditycutproductionand(ii)buyersofthecommoditypurchasemoreinrealterms.Thesetwinningeventsmaytakeawhiletoplayout,buttheyinevitablydo.Thestoryofthisbullmarketsofarhasbeensupplydisruption,withproductioncutsoccurringacrossmultiplemetalsforthepast18months.Wehaven’tseensignificantdemandgrowthsofar(asidefromlithiumandafewotheroutliers)butthiscouldchangeoverthecoming24months.

3

2.M&Aactivityhaspickedup,particularlyinQ22016.Notabletransactionsovertheperiodincluded:

• Nevsun’s$500mtakeoverofReservoirMineralsanditsTimokProject• Goldcorp’s$400mtakeoverofKaminakGoldanditsCoffeeProject• Centerra’s$1.1btakeoverofThompsonCreekMetals• Freeport’s$2.7bsaleofTenketoChinaMolybdenum• Anglo’s$1.5bsaleofniobium&phosphatebusinessestoChinaMolybdenum• SilverStandard’s$250mtakeoverofClaudeResources• Tahoe’s$540mtakeoverofLakeShoreGold• Hecla’s$600mtakeoverofAurizonMining

Thispickupindealvolumeisgreatnewsforqualitydevelopmentprojectsnotyetownedbyamajorproducer.Therecentbearmarkethasaleftadearthofnear-termproductioncandidatesandthosestillremainingarethatmuchmorevaluabletoapotentialacquirer. Additionally,ifthisindeedbecomesamulti-yearbullmarket,thenexplorerstoowillreceiveincreasedattention.Withinthepastmonth,mininglegendEricSprottstatedthatitwasanappropriatetimetobebuyingjuniorexplorers.Shareholdersofwell-managedprospectgeneratorsarepoisedtodoverywelloverthecomingfewyears.3.Theincreaseinprivateplacementvolumehasbeenevenmorepronounced.MininginvestorMarinKatusareportedearlierthisyear“thefirst55daysof2016havealreadyseenalmost50%ofthecapitalraisedintheminingsectorduringallof2015.”Sincethen,metalpriceshavecontinuedtoriseandthefinancingpacehasonlyquickened.Iwouldnotbesurprisedtoseemorecapitalraisedthisyearthanin2014and2015combined($7.7bUSD).4.Peoplearemakingseriousmoneyagaininaspacethathasbeenhatedforsolong.Meanwhile,theglobalfinancialmarketisstarvedforyieldinaworldofrealnegativeinterestrates.Thosewhodon’tnormallyinvestinresourcesarejustrecognizingthetremendouswealthcreationthatistakingplace.Theseinvestorswillbetemptedtojointhefray.Inflowsfromgeneralistfundsandretailinvestorswillincreaseinto2017.BullMarketToBeSimilarInDurationAndMagnitudeToThe1200-DayBearMarketWeJustEnduredAsRickRulefamouslysays“bearmarketsaretheauthorsofbullmarkets.”Whatwewitnessedbetween2011-2015leadsmetobelievethattheensuingbullmarketwillbesimilarlylong-livedandsimilarlyviolent.

4

ThebelowchartfromourfriendsatPalisadeResearchdoesagreatjobofillustratingthefollowing:1.Thenaturalresourceindustryisascyclicalasitgets.2.Thebearmarketwejustenduredwasthelongestandmostsevereofthepast25years.3.Longperiodsoflossesareoftenfollowedbylongperiodsofgains,andviceversa.

Anyoneproclaimingtoknowtheexactdurationofanycycleisfoolingyou,foolingthemselves,orboth.However,Idobelieveitisimportanttohavearoughexpectationofwhatwilltranspire–basedonhistory,one’sexperience,andcommonsense.Myexpectationisforthiscurrentcycletolastbetween900and1500days.Operatingunderthisassumption,westillhavetwoyearstofeastourselvesbeforeweneedtoworryaboutcashingin.

5

MusingsOnSpecificCommoditiesPreciousMetalsTheclearwinnersofthisbullmarketsofarhavebeenthepreciousmetals-gold,silver,platinumandpalladium.Miningequitiesassociatedwiththesemetalshavedoneevenbetter,with200%gainsyeartodatenotuncommon.Barchart.comprovidesaYTDchartwith57majorcommodities,currencies,andstockindices.Silver,platinum,palladium,andgoldoccupyfourofthetopsixspots.

Preciousmetalsarelikelytocontinuetheiroutperformanceforatleastanother18months.Afteryearsofpainthereareatleasttwomajortailwinds:1.Theageofnegativerealinterestrateshasinvalidatedoneofthemajorbearcasesagainstpreciousmetals.Fornowatleast,itismoreexpensivetoholdOECDdebtthanitistoholdbullion.WallStreetisrecognizingthisandeverymonthanotherbankseemstoturnpositiveongold.2.Preciousismetalownershipisatahistoriclow.Overthepastthirtyyears,preciousmetalinvestmentshavegenerallyconstituted~2%oftotalassetsundermanagementintheUnitedStates.Asrecentlyasthe1980’sthisnumberwascloserto7%.Todaywe’reat0.3%oftotalinvestmentsbutthetideisquicklyturning.

Outoftheaforementionedpreciousmetals,silverwillbethebiggestbeneficiary.Roughly80%oftheworld’ssilvercomesasaby-productfrombasemetalmines.Thisissignificantbecausethesebasemetalminesarenotassensitivetothepriceofsilver(asitisoftenasmallpercentageoftheoverallrevenuemix),andwon’tnecessarilyrespondtohighersilverpricesbyincreasingproduction.Youdon’tseethisdynamicforgold,platinum,andpalladium,whicharemostlyproducedfromprimarysources.RareEarthsRareearthsseemtobeanicecontrarianbetatthemoment.AfterthemonumentalREEbubbleof2009-2011andtheensuingcollapse,rareearthpriceshavelanguishednearpre-bubblelevels.Whilerealdemanddestructionoccurredwiththe

6

pricessurgewesawfiveyearsago,wecan’tforgetthesignificanceofthesemetalsinourhightechworld.Themarketiscurrentlydiscountingthepossibility,buta20-30%riseinrareearthpricesislikelyoverthenext12-24months.Lowcapexprojectswithashorttimelinetoproductionshouldbeabletobenefitfromthisexpectedrebound.UraniumUraniumisindisputablyTHEcontrarianbetintheresourcesphererightnow.Despitesupply-demanddynamicsoverthenext5-10yearsthatlookmorepromisingthanmostanyothercommodity,uraniumhaslaggedconsiderably–U308pricesaredownbyroughly30%yeartodate.Thiswillreverseand,aslongasyouhavethestomachforit,nowisafantastictimetoputmoneytoworkinselecturaniumequities.Outofconservatism,oneshouldbewillingtowaitatleasttwoyearsbeforewestartseeingasignificantrebound.Uraniumlikelywillbeoneofthebestperformingmetalsinthelaterstagesofthisbullmarket,andtherecentweaknessmeansthatyoucanstillsnapupouncesatdirt-cheapprices.ZincItissafetosaythatindustrialmetalswon’tseesignificantpricemovesforanother12-18months.TheoneexceptionthatIamparticularlyexcitedaboutiszinc–whichhasseensubstantialsupplycutsoverthepastyear.Zincsmeltersarerunningoutoffeed,andthefewneartermproductionstoriesarecurrentlybeinginundatedwithoff-takerequestsforzincconcentrate.

7

Thezincpricehasalreadyhadasignificantrunin2016,butIwouldn’tbesurprisedtoseeanothermoveof20%overthenext12months.Thesupply-demanddynamicsforthismetalhavebeenskewedfortoolong,anditappearsasifthemarketisbeginningtorecognizethatthecurrentpriceisn’tsustainable.Thereareplentyofsignspointingtoanewequilibriumabove$1.20USDperpound.Oneimplicitassumptionintheabovestatementsonpreciousmetals,rareearths,uranium,andzincisthateachcommoditywilltradeonitsownmeritforatleastthenexttwoyears.(Rememberthisisnotalwaysthecase–we’veseenwithinthepastdecademultipleinstanceswhereALLcommoditieshavetradedinunisonforrelativelylongperiodsoftime.)Howeveradecouplingofcommoditypriceshasbeenapparentthroughoutthewholeof2016,andIexpectsupply-demandfundamentalstocontinuewinoutforsometime.Idon’tbelievewewillseeextremecorrelationbetweencommoditiesreturnuntilthemanicstagesofthiscurrentbullmarket,wheneverthatmaybe.Insummary,wearejustenteringthesecondinningofamajormetalbullmarket.Nowisthetimetogetgreedy-aslongasyoucanstanda20%correctioninthenext6monthswithoutpanicselling.Therearestillexcellentmanagementteamsouttheretradingatinsultingvaluations,andthereareplentyofopportunitiesbeyondthemetalsIdiscussedabove.Wecanworryabouttakingprofitsinthesixthinningorso–butfornowlet’sfeast!

8

OverviewofPartnershipHoldingsBelowisabreakdownofthePartnership’sholdingsasofJuly15,2016.ThePartnershipisexposedtodifferentcommodities,differentjurisdictions,anddifferentstagesofthedevelopmentcycle.ThePartnershipcontinuestoaccumulate“AlternativeResourceHoldings”,indicatedinthebelowchartwithasterisks.Theseholdingsareresource-focusedyetminimallycorrelatedtotheminingcycle.Mytargetisforaminimumof30%ofourweightedholdingstofallintothiscategory,whichshouldreducethevolatilityoftheoverallportfolio.

Allocation By Commodity Food & Water Sulphate of Potash (SOP) 5% Agriculture* 4% Phosphate 4% Forestry Sandalwood* 5% Energy Metals Uranium 10% Scandium 6% Lithium 3% Industrial Metals Zinc 11% Copper 6% Precious Metals Silver 26% Gold 10% Cash (USD) 10%

*Signifiesminimalcorrelationtothe“MiningCycle”

9

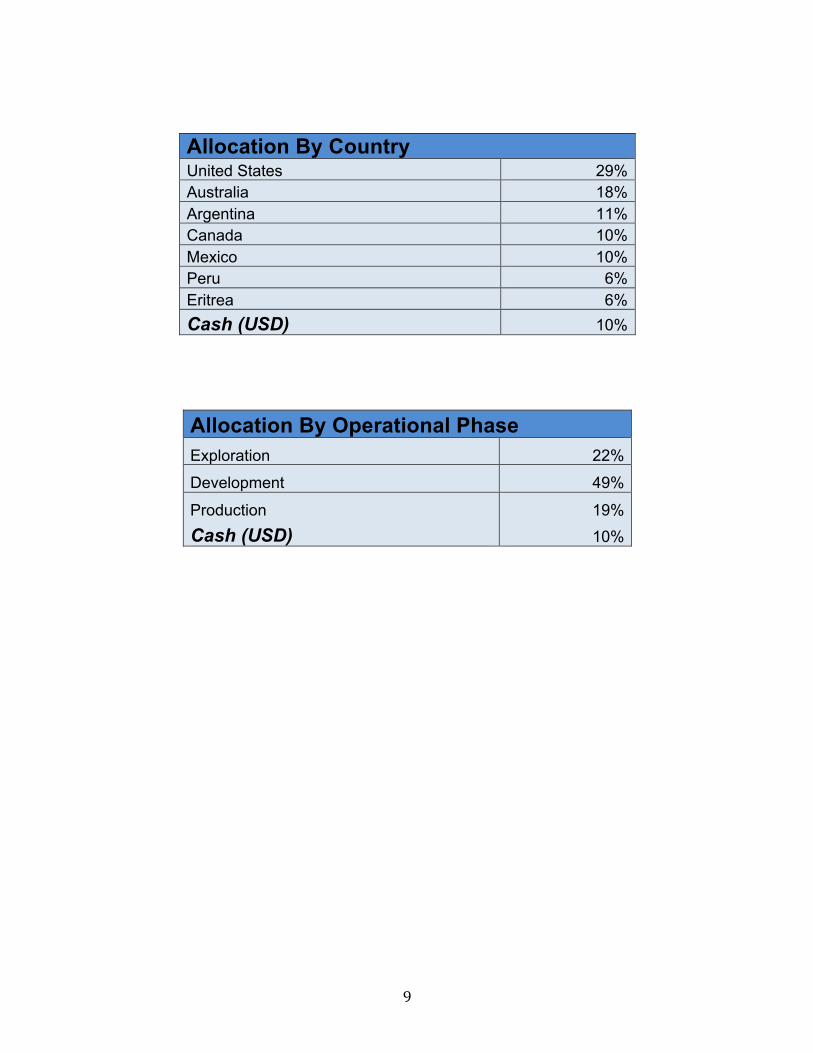

Allocation By Country United States 29% Australia 18% Argentina 11% Canada 10% Mexico 10% Peru 6% Eritrea 6% Cash (USD) 10%

Allocation By Operational Phase Exploration 22%

Development 49%

Production 19% Cash (USD) 10%

10

FeaturedInvestment#1:GoldenArrowResourcesOfour17currentholdings,GoldenArrowResources(CVE:GRG)hasbeenthesinglestrongestperformerin2016.Thecompany,foundedbytheexperiencedJoeGrosso,hasbeenexploringanddevelopingpreciousmetalprojectsinArgentinaforovertwodecades.GRG’sflagshipasset,theChinchillasProjectinJujuyProvince,looksincreasinglylikelytoreachproductionbytheendof2017thankstoaJVwithsilverheavyweightSilverStandard.OncetheChinchillasjointventurebeginsgeneratingcashflow(orconverselyisboughtoutrightbySilverStandard),thecompanywillreturntoitsrootsasaprospectgeneratorfocusedsolelyonArgentina.Atacurrentnetenterprisevalueof~$85mCAD,GoldenArrowismoderatelyundervalued,providesexcellentleveragetocontinuedoutperformanceinthepriceofsilver,andoffersexposuretoanArgentineanminingboomthatisjustinitsinfancy.Thesepointswillbedemonstratedlaterinthispiece.GRGshareshavebeenonanabsolutetearthisyear–withagainof~515%YTD.Clearlythecompanyisnotascheapaswhensharesweretradingbelow$0.20CADasrecentlyasJanuary,butthereisplentyofroomforthestocktorunoverthecomingfewyears.ThemarkethasrewardedGRGsofarin2016forthefollowingreasons:(1)Chinchillasoffersnear-termproductionpotentialwithaveryaffordableinitialcapex(thankstosynergieswithJVpartnerSilverStandardandtheirproducingPirquitasasset)(2)Duetoitsmassivesizeandrelativelylowgrade,Chinchillas’isaclassic“optionalityplay”withsignificantleveragetothepriceofsilver(whichhasbeenthebestperformingcommoditysofarin2016)(3)Argentina’selectionofpro-businessPresidentMauricioMacrihasopportunisticmininginvestorsstreamingintothecountryThePartnershiphasbeenshareholdersofGRGsinceFebruary2014,withanaveragecostof$0.24CADpershare.AsofJuly29th,GRGwastradingat$1.23CAD.Afteryearsofwaiting,ourpatiencehasbeenrewardedoverthepast6months.Inthisfeaturedinvestmentpiece,IwillbeprovidingcoloronwhyGRGhasgrabbedheadlinesthisyear.ThencomestheinvestmentthesisforGRG-coveringthecompany’sbackground,managementteam,andothercompanyessentials.

11

IwillthendetermineafairvalueperGRGshareusingreasonablyoptimisticsilverpricesandassumingthatSilverStandardexercisestheiroptionfor75%ofChinchillasbyyearend.Next,Idiscusshowthecompany’sotherArgentinaprospectscurrentlyareNOTreflectedinthecompany’scurrentshareprice,andhowGRGmanagementhopestofindanotherChinchillasinthenext2years(whichwouldbetheGrossoGroup’s4thmajordiscoveryinArgentina).Weconcludewiththecompany’sexpectedmilestonesoverthecoming24months,sothatfellowshareholderscantrackprogressalongsideme.Near-TermProductionwithLowInitialCapexOnOctober1st2015,GoldenArrow(whichthenhadamarketcapofonly~$10mCAD)enteredintoanagreementwithmulti-billiondollarsilverminerSilverStandard.Themarketbarelybattedaneye;atthattimewewereinthefinalthroesofamulti-yearbearmarket.HerearethedealtermsstraightfromGRG’snewsrelease:“Subjecttoan18-monthperiodofpre-developmentactivities(the"PreliminaryPeriod"),SilverStandardwillhavetherighttocommenceabusinessarrangementthatwillseethePirquitasMineandtheChinchillasprojectcombinedintoa75%(SilverStandard)25%(GoldenArrow)jointlyownedminingbusiness,withSilverStandardassumingtheroleofoperator.DuringthePreliminaryPeriod,SilverStandardwillpayGoldenArrowuptoC$2Moncompletionofcertainmilestones,andinvestuptoanestimatedUS$12.6M,withaminimumexpenditurecommitmentofUS$4M,atChinchillastoadvancetheprojectandevaluatethefeasibilityofdevelopingacombinedminingbusinesswithitsexistingPirquitasoperation.GoldenArrowwillassistinthepre-developmentactivitiesandevaluationprocess.Furthermore,GoldenArrowwillbepaidanamountequalto25%ofthePirquitasmine'scashequivalentearningsduringthePreliminaryPeriod,lesscertainexpendituresforexploration(includingpre-developmentexpenditures),capitalinvestmentandclosurecostsincurredduringthePreliminaryPeriod,basedonapre-definedformula,payableonclosingofthebusinesscombination.”Tosummarize,thedealgoesasfollows:

• SilverStandardhastheoptiontoacquirea75%interestintheChinchillasProject

• SilverStandardmustpay$2mCADtoGRG(infourseparateinstallments)

• SilverStandardmustcomplete$4mUSDof“pre-developmentwork”on

ChinchillasbetweenOct1st2015andApril1st2017

12

• ByApril1st2017,SilverStandardmustpay“anamountequalto25%ofthe

Pirquitasmine’scashequivalentearnings”(lesscertainexpenditures)toexercisetheoption.Otherwise,100%controlofChinchillasreturnstoGoldenArrow.

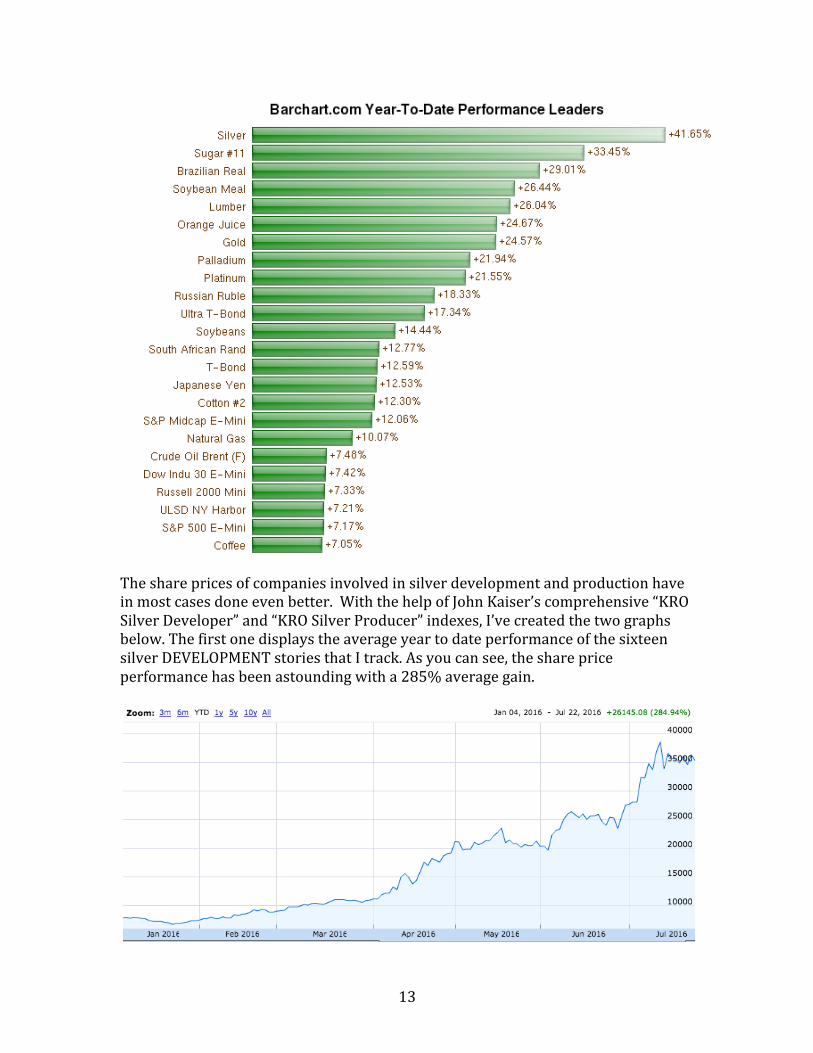

GoldenArrowCEOJosephGrossoprovidedtherationaleforthedealinthesamenewsrelease:"CombiningthesetwoneighboringassetsofferscompellingbenefitsandallowsustoacceleratethedevelopmentofChinchillaswhilebenefitingfromtheexistinginfrastructureandcashflowbeinggeneratedattheproducingPirquitasMine"statedJosephGrosso,ExecutiveChairman,PresidentandChiefExecutiveOfficerofGoldenArrow."WiththispartnershipwehavethepotentialtodeliverattractivereturnstoourshareholderswhileensuringtheChinchillasprojectisadvanced,creatingimmediateandlastingbenefitsforresidentsandcommunitiesintheregion."ThePirquitasMinereachedcommercialproductioninDecember2009.Theoperationcost$146mUSDtogetupandrunning,andhasgeneratedexcellentcashflowforSilverStandardoverthepastsevenyears.Unfortunatelyforthecompany,feedfromtheopenpitisexpectedtorunoutwithinthenext6months.SilverStandardthenhasroughlytwelvemonthsoforestockpiledbut,ifthecompanydoesnothaveanewsourceoffeedbyQ12018,thentheoperationwillhavetocometoahalt.Understandingtheimportanceofmaintainingcashflowandnotlettingexistinginfrastructuregotowaste,SilverStandardhasidentifiedChinchillasasthebestoptionforthisnewmillfeed.Thetwodepositshavesimilarmetallurgyandareonlylocated35kilometersapartinJujuyProvince,Argentina.ItisimportanttonotethatSilverStandardhasnotyetpaidGoldenArrowtoformallyinitiatethe75%/25%jointventure.However,sincetheagreementwassignedinOctober2015,silverhashadapowerful38%moveinpriceandSilverStandardhasspentmostifnotallofthe$12.6mspecifiedintheJVagreementondrillingandmetallurgicalwork.Thechancesoftheagreementcomingtofruitionarehigh,andSilverStandard’shandwillbeforcedsoon–pertheagreement,adecisionontheChinchillasJVmustoccurbeforeApril1,2017.OptionalityPlayforThisYear’sBestPerformingAssetSilverhasbeenkingthusfarin2016.Asyoucanseeinthefollowingchart,themetalitselfhasoutperformedvirtuallyeveryinvestableassetoutthere.

13

Thesharepricesofcompaniesinvolvedinsilverdevelopmentandproductionhaveinmostcasesdoneevenbetter.WiththehelpofJohnKaiser’scomprehensive“KROSilverDeveloper”and“KROSilverProducer”indexes,I’vecreatedthetwographsbelow.ThefirstonedisplaystheaverageyeartodateperformanceofthesixteensilverDEVELOPMENTstoriesthatItrack.Asyoucansee,thesharepriceperformancehasbeenastoundingwitha285%averagegain.

14

ThissecondchartdisplaystheaverageYTDperformanceforthethirteensilverPRODUCERSonmyradar.Theaverageperformancehereissimilarat225%.

Thesenumbersareundoubtedlyimpressive,butGoldenArrowhasperformedevenbetterthatitspeers–withGRGshareshavingappreciated515%sofarin2016.WhathasbeenthekeytoGoldenArrow’srelativeoutperformance?Theanswerissimple:optionality.Themainpremiseof“optionality”isthat,inanenvironmentofRISINGmetalprices,marginalprojectswillseethelargestgainsinvalue.Inpractice,thismeansacoupleofthings,whichmayatfirstseemcounter-intuitive:1.Large,low-gradedevelopmentprojectswillgenerallyseegreaterincreasesinvaluethansmall,high-gradedeposits.2.Highercostproducerswillgenerallyseegreatersharepriceappreciationthanlowercostproducers.Todemonstratethisconcept,Iwillusetwohypotheticalsilverminesasanexample.SilverMineAisabletoproducesilveratanallincostof$5perounce.SilverMineB,whichisonthehigherendofthecostcurve,hastosettleforanallincostof$11perounce.Tokeepthingsimple,let’sassumethetwocompaniesareeachproducing1millionouncesofsilverperyear.At$14silver(whichwesawasrecentlyasJanuary2016),SilverMineAwouldreasonablyexpecttogenerate$9minprofitsoverthecomingyear.Thisequatestoaprofitmarginof64%.

15

SilverMineBontheotherhandwillhavetosettleforonly$3moverthenext12months,foraprofitmargin21%.Nowlet’sassumethatsilverunexpectedlyjumpsto$20inveryshortorder.RevisitingSilverMineA,thenewexpectationwouldbe$15minprofitsoverthecomingyear(ahealthy66%jumpfromthe$14scenario).Logicallythegrossmarginwouldalsoincrease(to75%,elevenpercentagepointshigherthanbefore).At$20silver,SilverMineBcannowexpect$9minprofitsoverthenext12months(amassive200%jumpfromthepreviousscenario).Additionally,thegrossmarginofthecompany’soperationwouldmorethandoubleto45%.Notbad!ThereisnodoubtthatSilverMineAdisplayssuperioreconomicsinbothscenarios.Allthingsequal,thenetpresentvalueofSilverMineAisstillsignificantlyhigherthanSilverMineB.However,itisalsoevidentthatshareholdersofSilverMineBreceivedmorebenefitfromsilver’sriseinpricethantheircounterparts.Allthingsequal,theymademoremoneyinthisscenario.I’llskipthehypotheticalthistime,butthesameconceptoccurstodevelopmentstageprojects.Toputitsimply,developmentstageprojectsthatareanticipatingfuturelow-costproductionhaveLESStogainfromspikesinthepriceoftheunderlyingcommodity.Meanwhile,projectsthatmayhavebeenworthlessatsay$14silvercouldbeworthhundredsofmillionsat$20silver.GoldenArrow’sChinchillasprojectisatextbookoptionalityplay–arelativelylow-gradedepositthatcontainsover200msilver-equivalentounces.I’veprovidedbelowthemostrecentMineralResourceEstimateforChinchillas,whichwasreleasedApril2016).

Onekeytakeawayisthatthisisamassiveproject,particularlywhenyouconsiderthatatleast50%ofthelandpackagehasyettobeexplored.Anultimateresourceof500msilver-equivalentouncesisoptimisticbutnotimpossible.

16

Secondly,thegradeofChinchillasislowbyglobalproductionstandards.Thebelowchart,generouslyprovidedbyMAGSilver,suggeststhattheaveragesilver-equivalentgradeofprimarysilverproducersisroughly295g/t.

Meanwhile,Chinchillassportsagradeofroughly140g/tsilverequivalent(orlessthanhalfoftheproducingaverage).Thismakesthecompany’ssharepriceparticularlysensitivetothepriceofsilverand,loandbehold,silver’srunfrom$14to$20hastransformedtheprojectfromanuneconomicpropositiontoamulti-hundredmillion-dollarproject(atleastintheeyesofthemarket).Ifwesee$30silverandthedepositcontinuestogrowinsize,Iwouldn’tbesurprisedtoseethemarketvaluingChinchillasatover$1b.ItislargelyforthisreasonthatsilverbullshavebeenattractedtotheGoldenArrowstorysofarthisyear.ArgentinaIsOpenForBusinessAgainWiththesurpriseelectionofMauricioMacriinNovember2015,Argentinaovernightbecametheemergingmarketdarlingfortheglobalinvestmentcommunity.Foryears,doingbusinessinArgentinahadbeenenormouslyfrustrating,with30percentinflation,currencycontrolsthatmakeitcostlytogetmoneyoutofthecountry,sub-pareconomicgrowthandunpredictablegovernmentpolicies.Macri’sdefeatofDanielScioli(aperonistapromisingtomaintainthestatusquo)gavehopetoinvestorsthatArgentinawouldbemorereceptivetotheirinvolvementinthecountry.Sofar,Macrihasyettodisappointashiscenter-rightgovernmenthasaccomplishedthefollowinginlessthanayear:

17

• December2015-FinanceMinisterAlfonsoPrat-Grayscrapsmostofthe

country’scurrencycontrolsandallowedthepesotobegintradingfreely.

• December2015-Macri’sgovernmenteliminatesexporttarrifsonbeef,corn,andwheat.

• January2016–Argentineangovernmentagreesto$5bloandealwithHSBC,

JPMorgan,GoldmanSachs,DeutscheBank,Citibank,SantanderandBBVAtobolsterforeign-currencyreserves.

• April2016–Argentinasettlesa15-yeardisputewithahigh-profilegroupof

bondholders,mostnotablyElliottManagementfromNewYork.

• June2016–MacriliftsthestatisticalblackoutofINDEC–theagencyresponsibleforcollectingandprocessingeconomicdata.ThisindicatesarenewedconfidenceintheaccuracyofINDEC’snumbers.

Investorshaverespondedtothesetangiblemilestones,withforeigndirectinvestmentpouringintoArgentineanagriculture,livestock,mining,banking,andconsumerproducts.Within60daysofMacrireachingoffice,thecountryhadalreadyreceiveda“$1binvestmentpledge”fromCocaColaand“hundredsofmillionsofdollarseach”fromTotalSA,RoyalDutchShell,DowChemical,andBP.Macrioptimisticallyanticipates$20binFDIinflowsin2016alone.Evenifheisoffby50%,thisresultwilldwarfArgentina’s2015FDInumber–whichwasameasly$1.2b.Argentina’sfragileeconomicsituationhasyettobefullyresolved,andthere’snowayitwillbeduringMacri’sfirstterm.However,thingsarecertainlymovingintherightdirectionandforeigninvestorsarerewardingthecountrywithmassivecapitalinflows.ThismacroeconomictailwindshouldcontinuetodrawinvestorstotheGRGstoryoverthecomingyears.InvestmentThesisforGoldenArrowGoldenArrowisasilverdevelopmentcompanythathasbeenexclusivelyfocusedonArgentinasince1993,withCEOJosephGrossoinvolvedtheentiretime.Thecompanyhasmadethreemajordiscoveriesoveritshistory:

• Navidad-adevelopmentstageprojectnowinthehandsofPanAmericanSilver(a$3.5bCADsilverproducer)

• Gualcamayo-aproducingassetownedbyYamanaGold(a$6.4bgoldproducer)

• Chinchillas

18

Afterfourextremelyleanyears,therecentexcitementaroundbothArgentinaandsilverhaverevitalizedthecompany’streasury.GoldenArrowcurrentlyhasaworkingcapitalpositionof~$9mCAD,asthecompanyjustannouncedtheclosingofa$6.7mCADplacementwhichincludedahandfulofnotableinstitutionalinvestors.Thisgivesthecompanya5-yearrunwayatthecurrentmonthlyburnof$150kCAD.However,Iexpectthecompany’sburntodoubleortripleinshortorderconsideringtheimminentfinancingandGRG’sambitiousplansbeyondChinchillas.UltimatelytherearetwopartstotheGoldenArrowstory:1.GoldenArrow’ssoontobe25%stakeintheChinchillas/PirquitasJVwithSilverStandard.2.GRG’sprospectgeneratoreffortselsewhereinArgentina,whichwillrampuptremendouslyoverthenext3years.Firstlet’sdetermineafairvalueperGRGfocusingsolelyonChinchillas.I’veprovidedsomemathbelowthatdemonstratesthatGoldenArrowsharesaremoderatelyundervaluedforthisprojectalone.KeepinmindthatI’veusedthreekeyassumptionshere:(a)thefactthatSilverStandardexercisesits75%optiononChinchillasbytheendofthisyear,(b)Iassume$20silverfortheremainderof2016,and(c)Iassume$25silverbythetimeChinchillasreachesproduction-whichis25%abovecurrentspotprices.Asmentionedearlierinthispiece,inordertoexerciseits75%optionatChinchillas,SilverStandardmustpayGoldenArrow25%ofPirquitias’cashearnings(minusafewadjustments)sincetheagreementwassignedOctober1,2015.ThispaymentmustbemadebyApril1,2017butisverylikelytooccurin2016.Giventhesignificantjumpinsilverprices(andthesubstantialreductionstoopexatPirquitas)sincetheagreementwassigned,thisoptionpaymentislikelytobeasubstantialsumofmoney.AssumingthedealissignedinDecember2016,IexpectGRGtobepaidforthefollowingfivequartersofPirquitasproduction:Q42015AverageSilverPrice=$14.80USDQ42015AllInSustainingCost@Pirquitas=~$12USDQ42015SilverProduction@Pirquitas=2.6mouncesofsilver-equivalentQ42015Cashflow@Pirquitas=$7.3mUSDQ12016AverageSilverPrice=$14.50USDQ12016AllInSustainingCost@Pirquitas=~$10USDQ12016SilverProduction@Pirquitas=2.6mouncesofsilver-equivalentQ12016Cashflow@Pirquitas=$11.7mUSD

19

Q22016AverageSilverPrice=$17.20USDQ22016AllInSustainingCost@Pirquitas=~$10USDQ22016SilverProduction@Pirquitas=2.6mouncesofsilver-equivalentQ22016Cashflow@Pirquitas=$18.7mUSDQ32016AverageSilverPrice=$20USDQ32016AllInSustainingCost@Pirquitas=~$10USDQ32016SilverProduction@Pirquitas=2.5mouncesofsilver-equivalentQ32016Cashflow@Pirquitas=$25mUSDQ42016AverageSilverPrice=$20USDQ42016AllInSustainingCost@Pirquitas=~$10USDQ42016SilverProduction@Pirquitas=2.5mouncesofsilver-equivalentQ42016Cashflow@Pirquitas=$25mUSDThetotalPirquitasearningsforthequarterslistedaboveislikelytobe~$88mUSD,or~$116mCAD.ToestimateGRG’sshare,wemustperformafewadjustments:$116mCADminus$12.5mCAD(GoldenArrow’s25%shareofanticipatedinitialcapexforChinchillas/PirquitasJV)=$103.5CAD$103.5CADminus$2mCAD(GRG’sshareofanticipatedreclamationcosts@PirquitasMine)=$101.5CAD$101.5CADminus$17.4CAD(anticipatedArgentinarepatriationtax)=$84.1mCADToexercisetheoption,SilverStandardwillhavetopayGRG25%oftheabove$84.1mCADnumber,whichresultsina$21mCADanticipatedpaymenttoGoldenArrowlaterthisyear.BecausethispaymentisnotyetinGRG’shands,we’lldiscountthenumberby5%.Thisresultsinapresentpaymentvalueof~$20mCAD.Inadditiontothe$20mvaluefortheexpectedpaymentfromSilverStandard,GoldenArrowshareholderswillalsoown25%oftheChinchillas/Pirquitasjointventure.Usingconservativeparameters,Iestimatethevalueofthis25%stakebelow:InOctober2014GoldenArrowannouncedaPEAforChinchillas,whichresultedina$305mCADafter-taxNPVforastandaloneoperation(at$25silver).Keepinmindthattheinitialcapexforthisoperationwasanticipatedtobe$240mCAD.

20

Fastforwardtothepresentday,inwhichSilverStandardisproposingtoutilizingtheexistinginfrastructureatPirquitas(seebelow)toreduceChinchillas’initialcapextoroughly$50mCADforasimilarlysizedoperation.

WhileaformalestimatehasyettobepublicallyreleasedbySilverStandard,thereisnodoubtthatthis80%reductionininitialcapexwillworkwondersfortheproject’seconomics–perhapsincreasingtheafter-taxNPVby50-100%.SureGoldenArrowwillnowonlyown25%oftheoperation,butthereisnodoubtitwillbeamorevaluableoperationthanChinchillasasastandaloneproject.Despitethisfact,I’mgoingtoassumethatthecombinedoperationisONLYworth$305mafter-taxat$25silver-theexactnumbersGRGusedintheir2014PEA.Somewouldcallthisassumptioncomicallyconservative;otherswouldsaythisisanappropriate(albeitbackoftheenvelope)approachastherehasn’tbeenaNI43-101complianteconomicstudydoneonChinchillassincethe2014PEA.25%ofa$305mCADprojectresultsinaprojectvalueof$77mCADforGoldenArrow.Thisleadstoa~$97mCADvalueforChinchillasalone–whenonefactorsin(1)theoptionpaymentand(2)GRG’s25%stakeinthejointventure.Thecompany’snetenterprisevalueof$85mCADdoesnotfullyreflectthevalueofChinchillas.

21

ThisalsomeansthatGoldenArrow’sotherArgentineanprospectsareNOTreflectedinthecompany’scurrentshareprice,andanyfuturevaluecreationispureupsideforGRGshareholders.IwillnowgiveasummaryofGoldenArrow’sprospectgenerationactivityelsewhereinArgentina,andwhyIthinkthecompanywillfindanotherChinchillaswithinthenextfewyears(thiswouldbetheGRG’s4thmajordiscoveryinthecountry).WemuststartwithAntofallaasitisthecompany’smostexcitingprospectandmostrecentacquisition.Thedeal,whichwasannouncedinaJuly11thnewsrelease,seemslikeasteal.GoldenArrowmustpayamodest$1.5mover5yearstotheseller.Thesellerretainsa1%NSRroyaltythatcanbeboughtbackbyGRGfor$1.5m.Theprojecthasseenasurprisingamountofworkalready.Managementestimatesthat$5mworthofworkhasalreadybeenperformedontheproperty,withapastinterceptreturningahealthy18m@128g/tsilver.Belowisanimageoftheexpansiveproperty.

Inarecentdiscussion,thenormallytight-lippedBrianMcEwencouldhardlyholdbackhisenthusiasmabouttheproperty.(Brianisthecompany’sVPExploration&Development;hewasinstrumentalinthediscoveryanddevelopmentofChinchillas.)BelowisanexcerptfromarecentNorthernMinerinterviewwithBrianwherehediscussedtheAntofallaacquisitionindetail:“It’soneoftheonesthatwe’vehadoureyeonforacoupleofyears,”saysBrianMcEwen,thecompany’svicepresidentofexplorationanddevelopment.“Youcansee

22

thislargeareaofalterationatAntofallaandwestartedlookingatitonGoogleEarthtwoorthreeyearsago.”“Whenwesignedourduediligencedealanddidsomechipchannelsamplingonoutcropswecamebackwithsomespectacularresults,like14.9metresof271gramssilverand1%lead.”“It’sanincredibledealandit’sback-ended,sowe’renotputtingtoomuchupfront,”McEwensays,notingthatthecompany’smanagementteamandthesellerhadcomeupwiththestructureofthedealayearandahalfago.“It’sfairtosaythatifweweregoingtogoinandtrytonegotiateadealtoday,itwouldbedifficulttostrikeonethisattractiveintoday’smarket,giventhepositiveoutlookinArgentina[followingtheelectionofPresidentMacriinlate2015]andtheuptickinthemarketandmetalpricesingeneral.”“PeoplebelievedChinchillaswastoosmallandwewentinandfounditisnot,”hesays.“It’sabigdepositandit’sgettingbigger.AtAntofallaweseeasimilarenvironmentwithyoungerrocksandmineralizingeventsintrudingmucholdersedimentswithabigfootprint.Thepotentialistheretofindsomethingsignificant.”Overtheremainderof2016,GoldenArrowwillspendroughly$500,000atAntofallaongrassrootsexplorationwork.Managementwon’tadmitityet,butanaggressivedrillprogrambeginninginQ1/Q2ofnextyearishighlylikely.Weshouldknowwithinthenext18monthswhetherornotAntofallaisthecompany’snextbigproject.TherearetwomoreprojectsthatmaybedrilledbyGoldenArrowwithinthenext18months:PotrerillosandPescado.Potrerillosisa4000-hectaregold-silverprojectinArgentina’sSanJuanProvince.Theprojectislocatedjust8kilometersawayfromBarrick’sproducingVeladerogoldmine–thegeologyandlocationarecertainlyenticing.In2010-2011GoldenArrowcompletedasignificantexplorationprogram,including:

• Diamonddrilling(508min3holes)• Bulldozerroadsandtrenches(23km)• Surfacerockchipsamples(1,754)• IP/ResistivityandCSAMTResistivitygeophysics(16.5linekm)• Groundmagneticsurveys(54linekm)• Detailedgeologicalmapping(covering3,950ha)

23

TheprojecthasremaineddormantinGRG’sportfolioforthepast5yearsduetothesuccessatChinchillascoupledwiththe2011-2015bearmarket.HoweverIwouldn’tbesurprisedtoseeGoldenArrowrevitalizePotrerillosin2017.Pescadoisalsoaninterestingpreciousmetalsprospect–locatedjust10kmfromGualcamayo,apreviousGoldenArrowdiscovery.Thecompanyperformedanairbornesurveyin2007,whichwasfollowedupbyasoilsamplingcampaigninearly2008.Nodrillinghasbeenperformedontheproperty,however,asfurtherexplorationwasderailedbythe2008-2009bearmarketandafailedJVwithCoronationResources.NowthatGoldenArrowiscashedupandtheprojectis100%intheirhandsagain,IexpecttoseeGRGdrillsturninginthenearfuture.ThreemoreGoldenArrowprojectswarrantamention–MogoteinSanJuanProvince,DonBoscoinLaRiojaProvince,andCaballos(alsoinLaRioja).Eachoftheseisaclassiccopper-goldporphyrytarget,similaringeologytowhatisfoundinChile.GoldenArrowhasconductedpreliminaryworkatallthreeprojects,includingsignificantdrillingatMogotethroughitspreviousjointventurepartnerVale.Despitethepromise,GoldenArrowmanagementwouldratherfarmeachoftheseprojectsouttoalargerentity(versusdrillingouttheprojectsinternally).Massivecopper-goldporphyrytargetsareexpensivetodevelopand,giventhecompany’srecentsuccesswithChinchillas,BrianMcEwenwouldratherfocusonfindingasimilarsilver-zinc-leaddeposit.I’mhopefulthatthecompanycanfindJVpartnersforallthreeofthesewithinthenext18months.Ifsuccessful,thiswouldexposethecompanytonon-dilutivevaluecreation. AsafinalnoteonGoldenArrow’sprojectportfolio,thecompanyislikelyto“addanotherhorsetothestable”oncetheaforementionedprivateplacementcloses.ThisacquisitionwouldlikelybesimilaringeologytoAntofalla,andthegoalwouldbetodiscoveranotherChinchillas-likedeposit.Thecompany’sdeepexperienceinArgentinawillgivethemalegupinanynegotiationsthatmaytakeplace.Toconcludethispiece,I’veprovidedbelowmyexpectationsasaGoldenArrowshareholderforthecomingtwoyears:PurchaseofanotherArgentineanexplorationtargetbyend2016FinalizedJVDealAnnouncedbySilverStandardbyend2016FirstDrillAssaysatAntofallabyendQ22017AdditionalDrillAssaysatPotrerillosandPescadobyend2017JointventuresannouncedatMogote,DonBosco,and/orCaballosbyend2017

24

Ofthesemilestones,themostsignificantissurelySilverStandard’sdecisiononthePirquitas/ChinchillasJV.ThisdecisionmustoccurbyApril1,2017butmostGoldenArrowobserversexpectanannouncementthisyearasPirquitasisrapidlyrunningoutoffeed.AnegativedecisionbySilverStandardseemshighlyunlikelyatthispoint;ifanythingafullontakeoverforGoldenArrowisagreaterprobability.OncetheChinchillassituationisresolvedwithinthecomingmonths,GoldenArrowcanreturnfull-timetowhattheydobest–prospectgenerationinArgentina.AslongasthemarketcontinuestoassignzerovaluebeyondChinchillas,thenIamastrongbuyerofGRGshares.FeaturedInvestment#2:ExcelsiorMining(CVE:MIN)ExcelsiorMiningisacopperdevelopmentcompanywiththePFS-stageGunnisonProjectinArizona.Atthecurrentimpliedprojectvalueof$35mUSD,Excelsiorsharespresentsignificantvaluefromarisk-adjustedNPVperspective.Onecouldmakeaconservativecasethatexpectedfairvaluepershareis100-200%abovecurrentlevels.Risk-adjustedNPVinvestmentsonlysucceedifthecompanyinquestionmakesitintoproductionwithinareasonabletimewindow.Excelsiorseemstohavearealisticchanceofreachingproductioninearly2018,aftertakingintoaccountthefollowing:(1)theexcellentprojectedNPV,IRR,andpaybackperiodannouncedinlastmonth’sUpdatedPrefeasibilityStudy(2)thecompany’sopportunisticDecember2015acquisitionoftheneighboringJohnsonCampMine,significantlyreducinginitialcapexandshorteningexpectedconstructiontime(3)thecurrentmktcaptoinitialcapexratioindicatesthatthecompanycouldbeabletofinancemineconstructionthemselveswithoutseveredilutionInApril2014IwasgivenanextensivetourofExcelsioroperationsbyExecutiveVPRolandGoodgame-wevisitedthecompany’scoreshedandtheGunnisonprojectitself,located65milesSEofTucson.ThePartnershipinitiatedapositionshortlythereafterandwe’veaddedsince,withanaveragecostof$0.24CADpershare.AsofJuly29th,MINsharesweretradingat$0.37CAD.Whilethegainshavebeenmodest,thoseinvolvedinthejuniorresourcespacecantestifythatpositivesharepriceperformersoverthetrailing24monthsarefewandfarinbetween.Onepossibleexplanationforthediscrepancybetweenthecurrentsharepriceandexpectedrisk-adjustedfairvalueismarketskepticismovertheeconomicsof

25

Excelsior’sproposedIn-SituRecovery(ISR)miningmethod.IstartthisFeaturedInvestmentpiecebydiscussingthehistoryofISRcoppermininginArizona–asthestatehasalreadyseenhasalreadyseen40+yearsofproductionbetweenmultipleIRSmines.NextcomesthechiefriskthattheGunnisonProjectfaces:permitting.TasekoMinesownstheotheradvantaged-stageISRcopperdevelopmentprojectinArizona,whichhasstruggledtoreceivepermitsinatimelymanner.I’llhighlightthekeydifferencesbetweentheFlorenceandGunnisonprojects.WeconcludewiththeinvestmentthesisforExcelsior,coveringthecompany’sbackground,managementteam,andothercompanyessentials.IthendiscussthreekeyassumptionsI’mmakingasaninvestor,MIN’supsideasaninvestment,andexpectedcompanymilestonesoverthecomingtwoyears.In-SituCopperMininginArizonaIn-SituRecovery(ISR)isanalternateminingmethodthatdiffersfromtraditional“openpit”or“underground”mines.ISRinvolvesleavingtheorewhereitisintheground,andrecoveringthemineralsfromitbydissolvingthemandpumpingthepregnantsolutiontothesurfacewherethemineralscanberecovered.Consequentlythereislittlesurfacedisturbanceandnotailingsorwasterockgenerated.ISRismuchmoreprevalentintheuraniumindustry–itisestimatedthat30%ofglobaluraniumproductioncomesfromthisstyleofmining.ISRisafarlesssignificantportionofglobalcopperproduction,butithasstillknowntobeacommerciallyviabletechniqueforatleastthreedecades.

26

ArizonaitselfhasarichhistoryinISRcopperproduction.TheSanManuelcoppermine,ownedbyBHPBilliton,wasasuccessfuloperationthatintegratedISRmethodswithopenpitandundergroundminingandproducedapproximately3.25billionpoundsofcopperin14yearsofproduction.AnotherprojectownedbyBHP,PinotValley,alsousedISRtoextractcopper.Excelsior’sproposedISRoperationatGunnisonisnothingoutoftheordinaryforthestateofArizona.Permitting:Gunnisonvs.FlorenceTheGunnisonProjectisoftencomparedwiththeFlorenceProject–anArizona-basedISRcopperprojectthatwasboughtinNovember2014byTasekoMines(a$140mUSDmid-tiercopperproducer).TheFlorenceProjecthasbeenstalledforafewyearsnow–quotingthecompany’swebsite“onlytwooutstandingpermitsrequiredtomoveforwardwiththePhase1TestFacility”.UnfortunatelythosetwopermitshavebeenelusivethusfarforTaseko.ThekeyquestionforExcelsiorshareholdersiswhetherornotGunnisonwillfacethesamepermittingheadwindsthatTaseko’sFlorencehasexperienced.ThisisthekeyriskforExcelsiorcurrently–ifthecompanyisnotabletoreceivepermitsinatimelymanner,thenshareholderswillbeleftdisappointed.MybeliefisthatExcelsiorwillsurprisethemarketwitharelativelysmoothpermittingprocess.Therearesomemassivedifferences(intermsofpermitting)betweenTaseko’sFlorenceandExcelsior’sGunnisonProject.I’vehighlightedafewkeydifferentiatorsbelow:1.TheFlorenceProjectiszonedwithintheFlorencecitylimitsandislocatedtwomilesfromdowntownFlorence,Arizona(pop.25,000).Gunnisonislocatedaboutfourmilesnorthofanunincorporatedtown–Dragoon.ThedifferencehereisthatDragoonhasapopulationthatthatisonly1%ofFlorence’stotal–at209residents.IvisitedtheGunnisoninApril2014andcanattesttotheproject’sremoteness.Thebelowimagesnicelyjuxtaposethesetwoprojects;thefirstisTaseko’sFlorence(noticethetownofFlorenceintheimmediatebackground)followedbyExcelsior’sGunnison.

27

2.ISRoperationsuseasulfuricacidsolutiontoseparatetheeconomicmetalfromitshostrock.Akeyenvironmentalworryisthatthissolutionwillescapethehydraulicbarrierandcontaminatelocalgroundwater.BoththeGunnisonandFlorencedepositsarelocatedneargroundwateraquifers,butwithverydifferentcircumstances.Gunnisonislocatedinabasinwheretheaquiferisnot“activelymanaged”byanycounty,state,orfederalagency.Thisisduetothebasin’sminisculepopulationandlackofeconomicactivity.Inessence,nooneisusingthiswater.Forthisreason,the

28

DragoonWaterCompanyisinfullsupportoftheGunnisonProject–amassivevoteofconfidencegiventhenatureofISRoperations.TheFlorenceProject,ontheotherhand,islocatedinaverypopulousbasin.Theaquiferinthisinstanceisusedforexistingagriculturaloperations,is“activelymanaged”byatleastonegovernmentagency,andislocatednearoneofthemainsourcesofwaterforPhoenix(theGilaRiver).Forthisreason,theFlorenceWaterCompanyisinvehementoppositiontotheconstructionoftheproject.ThisoppositionwillcontinuetoshapepublicopinionandhamperTaseko’scontinuedeffortstoacquiretheremainingtwopermits.3.AfterExcelsior’sopportunisticacquisitionoftheneighboringJohnsonCampMineclosedinDecember2015,theGunnisonprojectinessencebecamea“brownfieldproject”.Thismeansthatthecompanycanutilizeexistingmininginfrastructuretobothreducecapexandtheoperation’senvironmentalfootprint.Indeed,theJohnsonCampincludestheexistingcopperprocessinginfrastructure:“a4,500gallonperminutesolventextractionplant,atankfarm,anelectrowinningplantwith88electrowinningcellswithcapacityfor25millionpoundsofcoppercathodeperannum,solutionstorageponds,atruckshop,corestoragebuilding,offices,warehouse,laboratory,mechanicalshop,aprimaryandsecondarycrusher,andvariousotherequipment.”Allofthisinfrastructurehasalreadybeenbuilt,andcanbeutilizedbeExcelsiorintheirminingplan(versussittingidle,asithassincetheJohnsonCamphaltedoperationsin2010).ThiscontrastswithTaseko’sFlorenceProject,whichwouldfullybeconsidereda“greenfield”operation.ThismeansthattheproposedmineisNOTlocatednearexistingmininginfrastructure,andthecompanywillhavetoconstructtheirminefromscratch.Intuitively,greenfieldoperationscanbedifficulttopermit–localswhoarenotusedtonearbyminingoperationsaremorelikelytobalkatproposedmines.Inconclusion,permittingremainsthekeyriskforExcelsiorshareholders.Additionally,itisclearthatTaseko’sstrugglesatFlorencehaveturnedoffpotentialinvestorsfrombackingExcelsior.ThethreepointsprovidedabovedemonstratethattheGunnisonProjectdiffersinmanywaysfromthebeleagueredFlorenceProject,andIthinkpermittingisfarmorelikelythanthemarketcurrentlyexpects.Excelsiorshareholdersshouldhaveananswertothis“permittingquestion”bymid2017.AccordingtoanApril26thnewsreleasefromthecompany:AdministrativeCompletenessReview(ACR)(“AdministrativeReview”)hasbeenachievedforboththeFederalUndergroundInjectionControl(UIC)PermitandfortheStateAquiferProtectionPermit(APP).TheUICisissuedbytheEnvironmentalProtectionAgency(EPA)undertheSafeDrinkingWaterAct;whereastheAPPisissuedbytheArizonaDepartmentofEnvironmentalQuality(ADEQ)undertheEnvironmentalQualityAct.AdministrativeReviewisthefirststageofthepermitting

29

process.Itconfirmsthatthepermittingapplicationisadministrativelycomplete,meaningthatalltherequireddocumentationandtechnicaldataarepresent.ExcelsiorisworkingcloselywiththeStateandFederalregulatoryagenciestohelpadvancetheissuanceofdraftpermits,whichExcelsiorexpectswilloccurearlynextyear.Excelsiorhasnowenteredthetechnicalreviewcomponentofthepermittingprocess.IexpectthecompanytoreceivetheirAPPandUICpermitsinQ12017,andfinaloperatingpermitsinQ22017.Shouldtheybeabletoacquirethesepermitsinatimelymanner,constructionwouldcommenceinQ32017-aswellasamassivere-ratingofExcelsior’sshareprice.InvestmentThesisforExcelsiorMiningExcelsiorMiningisacopperdevelopmentcompanyfocusedonadvancingtheirPFS-stageGunnisonCopperProject.Theprojecthasbeenthecompany’ssolefocusforoversevenyears,andCEOStephenTwyerouldandExecutiveVPRolandGoodgamehavebeeninvolvedtheentiretime.BothareobsessedwiththeprospectofGunnisonreachingproduction.Thetwohavedoneacommendablejobinproactivelytomitigatingenvironmentalandsocialrisks.Arecentexample:In2014,thecompanycommissionedanindependentstudytodemonstratetheeconomicbenefitstoCochiseCountyiftheproposedGunnisonMineisindeedbuilt.ThestudywasconductedbyresearchersfromArizonaStateUniversity,theSeidmanResearchInstitute,andtheWPCareySchoolofBusiness;furtherdetailscanbefoundhere:http://goo.gl/4JZAiTAtcurrentpricesMINsharespresenttremendousrisk-adjustedexpectedvalue.Whatdoesthismeanexactly?Here’sasimplehypotheticaltodemonstratethepoint…Howmuchwouldyoupayfora50%chancetowin$100?Onfirstglance,aslongasyoudon’tpaymorethan$50inthescenariooutlinedabove,thenyouaren’tgettingrippedoff.Thatisabsolutelycorrect.However,IpresumethatBenjaminGraham(thefatherofvalueinvesting)wouldprovideaslightlymorenuancedanswer-$33orless.GrahamlookedforaMarginofSafetyofatleast33%inallofhisinvestmentstomitigatehumanerror;whileitispossibleforadiscerninginvestortoknowtheapproximatechanceofsomethingoccurring,itdoesn’ttakeageniustounderstandthatreallifeprobabilitiescannotbepredictedwiththesameaccuracyofacoinflip.Hence,Graham’sinsistenceonaMarginofSafety.TheabovehypotheticalisrelevanttoExcelsiorMiningduetothepermittingscenariothatGunnisonfaces.Inessence,thisisabinaryoutcomesimilarinsomewaystoacoinflip–ifExcelsiorgetstheirpermittheninvestorsgettheir$100,ifnotinvestorsget$0.

30

Togoabitdeeper,belowarethreeassumptionsthatI’mmakingasanExcelsiorshareholder:1.Ifpermitted,thisminewillbefast-trackedtoproduction,willbeprofitableatcurrentcopperprices,andwillbealowest-quartileproducer.Thisstorywillnotfailduetomanagementineptitudeorprojecteconomics.2.Ifnotpermitted,thecompany’smarketcapwilldropto$0.Thisisnotentirelyaccurate,butoutofconservatismitisworthassumingentirelossofcapitalifthingsdon’tworkout.3.ThechancesofGunnisonbeingpermittedarebetween40-60%,astheamountofmoneyandeffortthathasbeenputintotheprojectsuggeststhatthereisatleastareasonablechanceofasuccessfulpermittingissuance.Outofconservatism,I’llusea40%chanceofSUCCESSfortherestofthispiece.BeforeIaddresstheabovepoints,Iwanttoemphasizesomethingthatshouldbeobviousatthispoint.Duetothenatureofthisinvestment,aninvestmentinExcelsiorshouldonlytakeupasmallpercentageofone’sportfolioandwouldideallybecoupledwith10-15unrelatedinvestmentsthatoffersimilarrisk-adjustedexpectedvalue.Nowontotheassumptions.Ifpermitted,thisminewillbefast-trackedtoproduction,willbeprofitableatcurrentcopperprices,andwillbealowest-quartileproducer.Thisstorywillnotfailduetomanagementineptitudeorprojecteconomics.Asoutlinedintheintroduction,Gunnisonhasthepotentialtobethenextlow-costcopperproducertoreachproductionintheUnitedStates.Permittingworriesaside,theprojecthasatremendousamountgoingforit:(a)ThecompanyreleasedanUpdatedPrefeasibilityStudyinFebruary2016withstellareconomics.ThisPFSwascommissionedprimarilytoillustratethetremendousimpactthattheJohnsonCampacquisitionhasonGunnison’seconomics,andalsotoadjustforthelowercopperpriceswehaveseensinceGunnison’soriginalPFSinFeb2014.Themainhighlightofthestudywasthattheproject’sinitialcapexestimatedroppedfrom$284mto$50m–adecreaseofover80%.Otherheadlinenumbersincludedan$829mpost-taxNPV(using$2.75copperanda7.5%discountrate),anafter-taxIRRof26%at$2copper,andprojectedAll-InCostof$1.24/lb.(b)Thecompany’sopportunisticDecember2015acquisitionoftheneighboringJohnsonCampMineforatotalof$8.4m.Asmentionedabove,thissignificantlyreducescapexandinessenceturnsGunnisonintoabrownfieldoperation.Anotherunderlookedbenefitisthattheconstructiontimenowestimatedbymanagementisamere9months–25%lessthanthe12monthsprojectedintheoriginalPFS.This

31

neartermproductionpotentialimprovesprojectpaybackandisanotherreasonwhyExcelsior’smarketcapshouldbemuchclosertoGunnison’sprojectedNPV.(c)Excelsior’scurrentmarketcapitalizationof$36mUSDisprettyclosetoGunnison’sinitialcapexof$50mUSD.ThisratioindicatesthatthecompanycouldpotentiallyfinanceGunnison’sconstructionthemselveswithoutseveredilution.Asahypothetical,iftheMIN’ssharepricerisesby50%betweennowandconstructionfinancing,thecompanycouldfinanceGunnison50%debt/50%equityandonlydiluteshareholdersby30%.Yes30%dilutionisnotpretty–butthebeautyofthisoptimisticscenarioisthatMINshareholderscankeepGunnison’svaluefullytothemselvesasthemineracestowardsproduction.Ifnotpermitted,thecompany’smarketcapwilldropto$0.Thisisnotentirelyaccurate,butoutofconservatismitisworthassumingentirelossofcapitalifthingsdon’tworkout.Thisassumptionisadmittedlyconservative.Forthesakeofconversation,ifpermitsarenotgrantedforISRproduction,thecompanystilldoeshavealargeamountofcopperinthegroundthatcouldbeminedthroughtraditionalpractices.However,inordertomaketheeconomicswork,significantlyhighercopperpriceswouldbeneededandthevalueplacedonMINsharesinthisscenariowouldbesignificantlylowerthanwheretheyarenow.ThechancesofGunnisonbeingpermittedarebetween40-60%,astheamountofmoneyandeffortthathasbeenputintotheprojectsuggeststhatthereisatleastareasonablechanceofasuccessfulpermittingissuance.Permittingisthebiggestrisktothisinvestment.Therearereasonstodoubtthatpermittingissuanceinatimelymannerwillhappen–theproblemsatFlorence’sISRproject,astricterEPA,andthegeneralstigmasurroundingISRminingallloomlarge.However,ascoveredaboveintheGunnisonvs.Florencediscussion,thereareplentyofreasonstobelievethatExcelsiorcansuccessfullynavigatethepermittingmaze.Thefollowingfactorsarealsorelevant:(i)managementhashadenoughbelieftofocusonthisprojectformorethantenyears,(ii)arespectedminingprivateequityfirmhasinvested$22mintoExcelsioroverthepast18months,(iii)twoprominentArizonans,JimKolbeandStevenLynn,sitonthecompany’sboard,and(iv)thecompanyhasproactivelydemonstratedthatGunnisonhastheabilitytospurtremendouseconomicactivityinarelativelydepressedcounty.Ignoringthepermittingworriesforasecond,howmuchexactlyistheGunnisonprojectworth?TherecentlyreleasedPrefeasibilityStudyprovidesuswithagoodplacetostart.I’veincludedbelowanexcerptstraightoutofExcelsior’sFebruary9thnewsreleasediscussingthePFS’sheadlinenumbers:

32

HighlightsoftheNorthStarGunnisonCopperProjectUpdatedPFS(UnitedStatesdollars)NetPresentValue(“NPV”)of$1.2billionpre-taxand$829millionpost-taxat7.5%discountrateusingalifeofmine(“LOM”)copperpriceof$2.75/lb;InternalRateofReturn(“IRR”)of57.9%pre-taxand45.8%post-tax;Initialconstructioncapitalcostsof$45.9million(includes20%contingency,16%EPCM,freight,mobileequipment,owner’scostsandcapitalspares);Paybackperiodforinitialcapitalof1.8yearspre-taxand2.6yearspost-tax;Averagelife-of-mineoperatingcostsof$0.70/lb;All-InCost(allcapitalplusoperatingcosts)of$1.24/lb;SensitivityanalysisataLOMcopperpriceof$2.00/lbgeneratesanIRRof30.8%pre-taxand26.2%post-tax.Over850millionpoundsofcopperaddedtotheprobablemineralreserve,anincreaseof24%;Minelifeof27years;Stagedproductionprofile:initialproductionrateof25millionpoundsofcoppercathodeperannumusingtheexistingJCMfacilities,followedbyanintermediateexpansionstageto75millionpoundsperannumandfinalexpansionstagetofullproductionof125millionpoundsperannum(includestheconstructionofanacidplantatfullproduction).Thestagedproductionprofilemakespossiblethefundingoffutureexpansionsoutofcashflow;Stagedproductionapproachlowersinitialcapitalcosts,reducesfinancingriskandspeedsthetimelinetofirstproduction.Thesearenodoubtimpressivenumbers,butoutofconservatismtheyneedtobediscounted.Let’sfocusontheproject’safter-taxNPV,asthisnumbertellsuswhatthevalueofGunnisonwouldbeifitwereputintoproductiontoday.Thecompanyestimatesan“$829mUSDpost-taxNPV$829millionpost-taxata7.5%discountrateusingalifeofmine(“LOM”)copperpriceof$2.75/lb”.WhileIdobelievethatthelong-termpriceofcopperwillactuallybeabovethis$2.75numberforthemajorityofthemine’sproducinglife,outofconservatismweneedtoadjust

33

forthecurrentcopperpriceofroughly$2.20perpound.Ascanbeseenbelow,thecompanyincludedasensitivityanalysisintheirPFSthataccountsforlowercopperprices.

Thisadjustmentforcopperpricesthatare20%lowerthanthe$2.75priceassumptionleadsustoanafter-taxNPVof$512mUSD.Additionally,mybeliefisthata10%discountrateshouldbeusedforallminingcompaniesacrosstheboard.Whilesomewouldcallthisharsh,aparticularlytrustedfriendofmineadvocatesfora20%discountratetoaccountfor(a)theuncertaintyinherentinminingand(b)thesignificanceofneartermcashflow.Withthisperspectiveinmind,Ithink10%isprettyreasonable.Excelsiormanagementuseda7.5%discountrateinthePFS,sowe’regoingtochopthe$512mnumberbyanother33%(ourpreferred10%discountrateis33%greaterthanthe7.5%used).Thisisanadmittedlybackoftheenvelopewayofcalculating,andisoverlyharshtoGunnison’svalue.Regardless,let’sdiscountthe$512mby33%toreachanafter-taxNPVof$340m.Next,wediscountthis$340mNPVbyanother60%toreflectthepermittingriskdiscussedinlengthabove(akaonly40%chanceofsuccess).

34

Thisresultsinarisk-adjusted,after-taxNPVof$136mUSD,or$1.07CADperfullydilutedshareofMIN.Despitethefactthatthisis190%aboveExcelsior’scurrentshareprice,Ibelievethis~$1CADnumberisthecompany’sfairvaluepershareatthistime.Let’sexpandouroutcomevisualizationalittlefurtherandspeculateonwhatwouldoccurif/whenthepermitsaresuccessfullyobtainedinH12017.Whilethecompanywon’tbetradingatGunnison’sfullNPVimmediatelyafterpermitapproval,itwouldbereasonableforthecompany’senterprisevaluetoequalthefull$340mUSDbythetimeGunnisonreachesproduction.ThankstotheacceleratedconstructiontimeduetotheJohnsonCampannex,thiscouldhappenasearlyas2018.Ifthecompany’sEVdoesindeedequalthe$340mNPVuponfirstproductionin2018,thiswouldresultina$2.69CADshareprice,ora691%returnovertwenty-fourmonths.Drawingbacktothecoinflipanalogydiscussedearlier,Iviewthisastheequivalentofpaying$34(i.e.MIN’scurrentshareprice)foraroughly50%chancetowin$269(i.e.Gunnison’sadjustedNPVpershare).Aslongasonecanacceptthatanegativeoutcomeisadistinctpossibility,theseareverygoododdsindeed.Beforewegettooexcitedaboutthebest-casescenariooutlinedabove,wehavetotakeintoaccountacouplepoints.Thefirstisthatanyequitydilutionassociatedwithprojectfinancingisnotfactoredintotheabovenumbers.Myviewonthisisthatthepotentialupsidediscussedaboveissolargethatanypotentialequitydilutioninvolvedwithprojectfinancingisavirtuallyanon-issue.Permittingisfarandawaythebiggerriskhere.ThesecondisthatthereisalwaystheriskthatExcelsiorshareholderswillnotbeabletorealizethefullvalueofGunnisonintheeventofatakeoverbyanexistingcopperproducer.Thisisalwaysariskinherentindeeplyundervalueddevelopmentprojects.Myopinionintheeventofatakeoveristhat,aslongasareasonablepremiumisofferedandmanagementactsinthebestinterestofshareholders,it’sworthsmiling,takingthemoney,andmovingontothenextplay.Toconcludethispiece,I’veprovidedbelowmyexpectationsasanExcelsiorshareholderforthecomingtwoyears:$4mFinancing(providessufficientworkingcapitalthroughaproductiondecision)byend2016GunnisonFeasibilityStudyReleasedbyend2016APP,UIC,andOperatingPermitsReceivedbyendQ22017$45mConstructionFinancingRaisedbyendQ22017

35

FirstProductionatGunnisonbyendQ22018Ofthesemilestones,themostsignificantissurelyExcelsior’sexpectationthatAPP,UIC,andOperatingpermitswillbereceivedinH12017.Ifthecompanyhasn’tannouncedapermittingsuccessbyJuly2017,thenitwillbetimetoseriouslyconsiderliquidatingyourinvestment.IfExcelsiordoesinfactdefythemarketandannouncesuccessfulpermitting,thenIexpectthesharepricetodoubleovernight.Timewilltellhere–thegoodnewsisthatwewillknowtheanswertothispermittingquestionwithin1year,whichintheworldofjuniorminingisn’taparticularlylongtime.

36

PastFeaturedInvestmentsAlmadexMinerals(CVE:AMZ) FeaturedIn:July2015PartnershipAverageCostperShare:$0.16CADCurrentMarketPrice(July29,2016):$0.43CADAlmadexMineralswasthePartnership’sfeaturedinvestmentinJanuary2016.Atthetime,thecompany’smarketcapitalizationwasequaltoitsworkingcapitalposition–aludicrouspropositionconsideringmanagement’sdeepmineralexplorationexpertiseandthecompany’suniquecollectionofpreciousmetalassets(royalties+promisingexplorationproperties).ItwasaclassicGraham-Doddvalueinvestmentwithverylimiteddownsideandampleupsidepotential.Whiledeepvalueinvestmentsgenerallytakeyearstopanout,AMZshareshavehadastunning180%gainyeartodate–helpedinalargepartbythenascentmetalsbullmarketthatbeganinFebruary2016.Butcompany-specificnewsalsoplayedabigrole.Ontheprospectgenerationfront,thecompanyreportedmoderatelypositiveresultsoverthefirsthalfofthisyear.InearlyFebruary,thecompanyissuedanewsreleasestatingthatthecompanyhad“commencedexplorationactivitiesonseveralofitsprojectsandworkprogramsarecurrentlyunderway.ThefocusofworktodatehasbeentheCompany’sElCobreandLosVenadosprospectsinMexico.Someregionalexplorationworkhasalsobeeninitiated.”Roughly4monthslater,onJune1st,thecompanyannouncedtheresultsofthreeholesatElCobre.Oneoftheholesshowedpromise(HoleEC-16-008),butthemarketwasunimpressed.ChairmanDuanePoliquin,aprospectgenerationlegend,madesuretopointoutinthenewsreleasethat“thesefirstresultsarefromonlyoneofthetargetsidentified”–indicatingthatmoredrillresultsareimminentfromelsewhereontheElCobreproperty.BeyondElCobre,itseemnearlycertainthatwewillseeresultsfromLosVenadosinthecomingmonths.Thepropertyisatextbook“areaplay”,locatedimmediatelyadjacenttotheoperatingLaIndiaandMulatosgoldmines(ownedbyAgnicoEagleandAlamosGold,respectively).Iamalsohopefulthatwewillseedrillresultsfromthefollowingtwopropertiesbytheendoftheyear:WillowinNevada,USAandCalderainPueblaState,Mexico.Almadex’sfutureasaprospectgeneratorisundoubtedlybright,butthusfarin2016thecompany’sroyaltyandequityholdingshaveprovidedthemostexcitement.Therehavebeenthreemajordevelopments:

37

(1)thematerializationofGoldMountainMining’sElkGoldProjectintoalegitimateBritishColumbiadevelopmentplay(nowsupportedbythelikesofMarinKatusa,DougCasey,andRickRule)(2)therevitalizationoftheIxtacaProject,onwhichAlmadexownsa2%NSRroyalty(3)thesaleofElEncuentrotoMcEwenMiningfor$250kCAD(Almadexretaineda2%NSRroyaltyontheproperty)WhenIfirstwroteaboutAlmadexsixmonthsago,IonlymentionedinpassingAMZ’sexposuretoGoldMountainMiningandtheirElkGoldProject.Almadexdidatthetimeown27mGUMsharesanda2%royaltyonElkGold,butGoldMountainhadasub$2mCADmarketcapandscantworkingcapital.Accordingly,IwrotethisoffasaneartermvaluedriverforAlmadexshares.BoywasIwrong–GoldMountainshareshaveproceededtorallyfrom$0.025to$0.33,astunning1200%YTDgain.Justasimportantly,developmentatElkCreekhasbeenprogressingandfirstproductionby2020isadistinctpossibility.ProductionatElkCreekwouldresultinatleast7yearsofroyaltypaymentstoAlmadex.ThecatalystforthisbreathtakingmovehasbeenheavybuyingfromKCRLLC–agroupcompromisedofmininginvestmentlegendsMarinKatusa,DougCasey,andRickRule.KCRnowowns~44%ofoutstandingGoldMountainsharesandthemarketisslowlybeginningtotakenotice(asevidencedbythespikeinGUMtradingvolumewe’veseeninJuly).Justafewweeksago,CEOMorganPoliquinnegotiatedadealdirectlywithKCRandsold$2mCADinGoldMountainsharestothegroup.Thisisnotaninsignificantamountofmoneyatall;Almadexisaleancompanywithanannualburnof$1.5m.Soinessencethissaleaddedayeartothecompany’srunway.Additionally,Almadexstillowns6.75msharesofGoldMountainforacurrentmarketvalueof~$2.2m.AlmadexshareholdersshouldcontinuetofollowtheGoldMountainstorywithinterest.Almadex’smostsignificantroyaltyassetisnotElkGold,butrathera2%royaltythatcoverstheIxtacaGold-SilverdepositinPueblaStateMexico.MorganPoliquinknowstheIxtacaprojectverywell,ashediscovereditwithhisfatherDuanein2008.AfterdevelopingtheprojectwithinacompanynamedAlmadenMinerals,in2015thefather-sonduospunoutallprospectgenerationactivitiesintoALMADEXandkeptIxtacawithinALMADEN.(Thecompaniesareoftenconfused,hencetheallcaps.)AlmadexshareholdersstillhavealottogainfromsuccessatIxtacaduetothe2%NSRroyalty.

38

Ixtacaisarelativelylargedevelopment-stageasset.AnupdatedPEAreleasedinearly2016envisionsa$100moperationthatismarginallyeconomicat$1150goldand$16silver.However,asmostofusknow,bothgoldandsilveraretradingwellabovetheseprices(17%and27%,respectively),andthemarketiscatchingontothefactthatAlmadenmaybeabletogetIxtacaintoproductionwithin3years.ThecompanyiscurrentlyworkingonaPre-FeasibilityStudythatshouldbereleasedbyyear-end.Athirdnotabletransactionwasthecompany’ssaleofElEncuentrotoMcEwenMiningonMay2nd.Theprojectislocatedjust10kilometersfromMcEwen’soperatingElGallogold-silverprojectinSinaloaState,Mexico.Almadexreceived$250kUSDanda2%NSRroyaltyinexchangeforownershipoftheproperty.

Inthenewsrelease,DuanePoliquindiscussedthedealinfurtherdetail:“Ihavebeeninvolvedwiththisprojectsincetheearly1990sandbelieveverystronglyinitsmineralpotential.ThissaletoMcEwenisbeneficialtoAlmadexasitputsUS$250,000inthetreasuryimmediatelywhilepreservingupsideforshareholdersthroughthecreationofanewNSRroyalty.GivenMcEwen’spresenceinthearea,theyarebestplacedtodeveloptheseassetsinthenearterm”. ItispossiblethatElEncuentrocouldbefast-trackedtoproductionevenmorequicklythanIxtacaorElkGold,duetoMcEwen’sexistingoperationsinthearea.Infact,thedealincludedanuncommonterm:“advanceannualroyaltypaymentsinanamountuptoUS$100,000peryearcommencingJanuary1,2021,intheeventthatcommercialproductiondoesnotoccurpriortothatdate.”ThefactthatMcEwenagreedtothisnon-standardstipulationdemonstratesmanagement’sbeliefthatElEncuentrowillbeginsupplyingmillfeedforElGallowithinthenextfewyears.ThisofcoursewouldresultincashflowtoAlmadexfromthe2%royalty. AlmadexsharesarenotnearlyascheapaswhenIlastwroteaboutthecompany(currentnetenterprisevalueof~$8mCADversus$0justsixmonthsago).Thatsaid,thisisstillaclassicvalueinvestment–thecompany’sprospectgenerationbusinessaloneisworthatleast$25minmyestimation.Thethreeholdingassetsdiscussedaboveonlyprovideadditionalupsidebeyondthecompany’scorebusiness.Toconclude,I’veprovidedbelowtherelevantmilestonesI’mexpectingoverthenext18months:AdditionaldrillresultsatElCobrebyendQ32016AlmadenMineralsannouncesPre-FeasiblityStudyatIxtacabyendQ32016FirstdrillresultsatLosVenadosbyend2016FirstdrillresultsatWillowbyend2016

39

FirstdrillresultsatCalderabyend2016AlmadenMineralsannouncesFeasibilityStudyatIxtacabyendQ22017AlmadenMineralscommencesconstructionatIxtacabyend2017GoldMountaincommencesconstructionatElkGoldbyend2017TFSCorporation(ASX:TFC)FeaturedIn:July2015PartnershipAverageCostperShare:$1.86AUDCurrentMarketPrice(July29,2016):$1.63AUDTFSCorporationwasthePartnership’sfeaturedinvestmentinJuly2015.Thecompanyremainsmyfavoriteforestrypick.Thoughshareshaveremainedvirtuallyflatyeartodate,itwasanotherproductivesixmonthsforthecompanyandTFSinvestorssawconstantnewsflow.Fourcompany-specificdevelopmentsstoodabovetherest:1.InlateFebruary,TFSannouncedintheirmid-yearearningsreportthatnumerousmulti-yearsupplyagreementshadbeensignedwithChineseandIndianwoodbuyers.CEOFrankWilson,whoco-foundedTFSnearlytwodecadesago,commentedonthetransaction:“IamdelightedwehavesignednewagreementswithwoodbuyersinChinaandIndiaatattractivepricesforTFS.WithourexistingcontractswithGaldermaandLushCosmetics,IamverypleasedtoannouncethatwehavenowforwardsoldalloftheTFSownedyieldfromtheforthcomingtwoharvests.WearenowintheenviablepositionofhavingmultiplecustomersacrossmultiplemarketsinfourdifferentcontinentsandthisperfectlyillustratestheglobaldemandforIndiansandalwood.”Notonlydoesthisdealprovideearningsvisibilityforthenext2years,butitalsoconfirmsthatIndianSandalwoodpriceshavebeenentirelyuntouchedbythesoftcommoditiesslumpthatbeganinmid-2014.ThelasttimeTFSpublicallyannouncedthepriceofasupplyagreementwasinAugust2014–whenthecompanysignedanagreementwithGalderma,aNestle-owneddermatologycompany.Thedealwastosellupto20yearsofsandalwoodoilat$4500USDperkilogram.Thisyear’ssupplydealwasalsostruckatprices“broadlyequivalenttoUS$4,500perkgofoil”.Skepticsofthesandalwoodstoryshouldtakenote;therearenowbuyersonmultiplecontinentswillingtopaythispriceforTFS’ssandalwoodoil.Whilesandalwood’spriceincreaseoverthepasttwodecadeshasbeenmonumental,

40

itiscleartomeatleastthatthemarketcanhandletheseprices.ThisbodesverywellforTFSoverthecomingdecade.

2.InApril2016,thecompanyundertooka$60mAUDplacementat$1.55pershare.Whilethedilutionisunfortunate,thecompanyraisedthisplacementforgoodreason-toembarkonaprojectwitha“blendedinternalrateofreturnofapproximately37%overtheperiodofFY17toFY23”.ThistypeofIRRisunheardofintheforestryspaceand,aslongasthecompanygetsreasonablyclosetothis37%goal,theinvestmentseemsverywellwarranted.Whatexactlyisthisproject?RememberthatTFSboth(a)directlyownssandalwoodplantationsand(b)managessandalwoodplantationsownedbylargeinvestors.TFSseesanopportunityto“buyout”someoftheselargerinvestorsearlierthanoriginallyexpected,andwouldthenusethissandalwoodtosatisfythecompany’send-userobligationsoverthecomingyears.ThecompanyprovidedmorespecificsinanApril2016presentation:

• TheCompanywillmakeofferstoacquireupto221hectaresofMISGrowerinterestsinfiveMISProjectsduetobeharvestedbetween2016and2022

• TFS’sofferswillprovidegrowerswithanoptiontosellaheadofharvestata

cashpricebasedinitiallyonthe31December2015bookvalue

41

• TheBuy-Backisexpectedtohaveamaximumcostof$53mAUD

• Theacquiredplantationsareexpectedtoyieldaround600tonnesof

heartwoodwhichTFSintendstosupplytoitsrecentlyannouncedcustomersinChina,IndiaandtheMiddleEast

Amonthlater,thecompanyannouncedthat“thefirstofaseriesofitsbuy-backofferstoinvestorsincertainofTFS’sManagedInvestmentSchemesclosedwitha66%acceptancerate.”Thishighrateofacceptanceshowsthattheprojectisofftoafaststart.Thecompanywillbemakingadditionalbuybackoffersovertherestofthisyear.3.TFShasannouncedpublicallythattheywanttosella$40mloanbookbytheendofthisyeartoraisecashforoperations.Thismakessense–thecompanyisnotafinancialinstitutionandwouldbebetterservedputtingthismoneyintonewcompany-ownedplantations.OnJune28th,TFSannouncedthatithad“enteredintoagreementstosellloansandreceivableswithabookvalueof$25millionforcashproceedsof$24million.”Thisisaverysmalldiscounttotheloanbookvalue,anddemonstratesthatthecompanyshouldbeabletogetanother~$15mbytheendoftheyear.Thisisnotinsignificantmoney,anditcomeswithoutdilution.Additionally,itsetstheprecedentforadditionalloanmonetizationdowntheline.AsstatedbyFrank

42

Wilson:“theestablishmentoftheon-goingfundingprogramsprovidesTFSwithvaluableoptionalitytoreleasecapitalfromfutureloansonpre-arrangedterms.”4.OnJune28th,TFSannouncedyetanotherplantationsaletoanewinstitutionalinvestor.Accordingtothenewsrelease,“ThenewinvestorisaUS-basedglobalinvestmentmanagementfirmwithoverUS$100billionofassetsundermanagementandanestablishedtrackrecordofinvestinginAustralianandNewZealandagriculture.”Thekeytermsoftheinvestmentinclude: •SaleofnewIndiansandalwoodplantations. •SaleofthefreeholdlandintheNorthernTerritory,originallyacquiredby theCompanyin2015. •TFStomanagetheplantationsthroughtoharvest. •TotalFY16revenuefromthesaleofthelandandplantationsofAU$27.0 million. •Cashsettlementscheduledfor29June2016.TFSalreadymanagessandalwoodplantationsforawholehostofinstitutions,includingHarvardandtheChurchofEngland.Managementfeesderivedfromthesepartnershipscompromiseanimportantcomponentofthecompany’searnings.Additionalinstitutionalplantationsalesaretobeexpectedoverthecomingmonths.TFS’smarketcapitalizationisstillbelowthenetvalueofthecompany’sassets–thoughthediscounthasnarrowedfrom10%to5%sinceIlastwroteaboutthecompany.Forthosewithlonger-termtimehorizons,TFSsharesoffercompellingupsidewithminimalrisk.ThemarketclearlydoubtsthecredibilityofTFS’scoreplantationownership/managementbusiness.Continuedoperationalexecutionandconsistentdividendpaymentswillslowlychangethissentimentgoingforward.NevsunResources(NYSE:NSU)FeaturedIn:January2015PartnershipAverageCostperShare:$3.07USDCurrentMarketPrice(July29,2016):$3.32USDNevsunwasthePartnership’sfeaturedinvestmentinJanuary2015andremainsmyfavoritemid-tierbasemetalplay.WhiletheNSUsharepricehaslaggedmanyofits

43

peers,thecompanyhashadasensational2016fromabusinessperspective.Themarketwillsooncatchon.Therehavebeenmultiplepositivedevelopmentsthusfarthisyear,butNevsun’smostsignificantwastheacquisitionofReservoirMineralsanditsworldclassTimokcopper-goldprojectinSerbia.ClosefollowersoftheNevsunstoryknewthatabigdealwaslikelyonthehorizon-IstatedmyselfinJanuary2016: Whilethereisnoharddeadlineforthecompany,Ifullyexpectoneofthefollowingtwooutcomesinthenext12months–(a)anopportunisticacquisitionofalow-costcopperoperationtocomplementBishaor(b)thedistributionofalargespecialdividend.Eitheroftheseeventswouldbeawelcomedevelopmentforshareholders,asit’stimeforthecompanytoputthisoutsizedcashpositiontoworkinoneformoranother. Sureenoughthecompanyhascomethroughontheirpromiseofanopportunisticacquisition,butImustsaythattheresultexceededmyexpectations.AfteritsdiscoverybyReservoirMineralsinmid-2012,Timokhasbecomeoneofthemostsignificantundevelopedbasemetaldepositsintheworld–duetoitshighgrade,massivesize,andproximitytoexistingmininginfrastructure.

AnApril2016PEAonTimok’sUpperZoneoutlinestheproject’sexceptionaleconomics:

• Initialcapexof$213mUSD• Post-taxNPVof$1bUSD(at8%discountrateandspotmetalprices)• Post-taxIRRof86%

44

• Paybackoflessthan1yearForaprojectofthissize,theseeconomicsarevirtuallyunheardof.Additionallytheydon’ttakeintoaccountTimok’sLowerZone,whichmayhaveapotentialproductionlifeof15-20years.We’lllearnmoreabouttheLowerZoneoverthecomingyearasNevsunhasinitiatedanaggressivedrillingprogram.Inabestcasescenario,theLowerZonecoulddoubleortripletheoverallvalueofTimok.NevsunultimatelyboughtReservoirfor$512mUSD,withacombinationofsharesandcash.Onfacevalue,NevsunpaidafairpriceforTimok’sUpperZone–50%ofNPVissteepforaPEAstageprojectbutnotunheardofforworld-classdeposits.(Asarecentexample,Goldcorpoffered60%ofNPVforKaminakGold’sPEAstageCoffeeProjectinMay2016.)However,themarkethasyettoappreciatewhatNevsunacquiredbeyondTimok’sUpperZone:

• ExposuretotheLowerZoneasdiscussedabove

• Participationinamassive$75mJVagreementwithRioTinto(exploringfourprospectivepropertieslocatedincloseproximitytoTimok)

BoththeLowerZoneandtheRioTintoJVhavethepotentialtoaddtremendousvalueoverthecomingyearsandshouldbeviewedasfreeupsideforcurrentNevsunshareholders. DevelopmentsattheBishaMinehavebeenovershadowedbythehigh-profileTimokdeal.However,therehavebeenthreesignificantdevelopmentsthisyearworthnoting:1.OnaJuly29thearningscall,managementconfirmedthatthefinalcostofBisha’szincexpansionwas$77mUSD.Thiscomparestoaguidanceof$100m.Thisisthecompany’sthirdmajorcapitalprojecttobecompletedon-timeandunderbudgetwithinthepast6years–atremendousachievementthatreflectswellonmanagementandbodeswellforthedevelopmentofTimok.2.InaFebruary11thnewrelease,thecompanyreleasedthefollowingcostguidancefor2016:“Remainingsupergeneoreprocessinginthefirsthalfof2016isexpectedtoproduce40to50millionpoundsofcopperincopperconcentrateataC1cashcostof$1.20to$1.40perpayablepoundofcopper.”Sureenough,themarketwassurprisedwhenjustlastweekthecompanyannouncedQ1/Q2supergenecopperproductionof55.8millionpoundsataC1cashcostof$1.04perpayable.NSUshareholderswererewardedwitha10%moveonFridaylargelyduetothisresult.

45

3.ThemostsignificantBishadevelopmentoccurredjustlastweek,whenNevsunannouncedthatithadincreaseditstotallandpackageofexplorationlicensesto814squarekilometersinEritrea’sBishaVMSDistrict.Thisrepresentsa1,891%increasefromthe41squarekilometersthecompanyhadbeforethedeal.Inthenewsrelease,CEOCliffDaviselaboratedontheimportanceofthisdeal:“TheBishaVMSDistrictremainsvastlyunder-explored.ExpandingourexplorationlandpackagehasbeenahighprioritythatrequiredanegotiationwiththeMinistryofEnergyandMinesforextendedandimprovedlicenseterms.BMSCnowhasownershipofalloftheexplorationlandintheBishadistrict.Withgreateraccesstoadditionalhigh-prioritytargetsandincreasedtimetoevaluateresults,wehaveaddedanotherkeyelementtoourstrategytodelivershareholdervaluethroughexplorationinthisprolificminingdistrict.”

ThisacquisitionsolidifiesmybeliefthatNevsunwillfindenoughoretokeeptheBishamineproducingforanotherthreedecades.ThismaybeaVMSdistrictonthesamescaleasManitoba’sFlinFlondistrict,whichhasseen25producingminesinthepastcentury.I’mthrilledtoseewhatthecompanycandiscoverelsewhereinthedistrictoverthecomingyears.

46

Toconclude,I’veprovidedbelowtherelevantmilestonesshareholdersshouldexpectfrombothBishaandTimokoverthenext18months:FirstzincconcentratesaleatBishabyendQ42016 2016copperproductionof80-110mlbsbyend20162016zincproductionof70-100mlbsbyend2016MaidenresourceestimateatAsheliDeposit(locatedtruckingdistancefromBisha)byendQ12017UndergroundexplorationrampcompletedatBishabyend2017Pre-FeasibilityStudyreleasedatTimokbyend2017 TsodiloResourcesLtd(CVE:TSD)–NOLONGERAPARTNERSHIPHOLDINGFeaturedIn:July2014PartnershipAverageCostperShare:$0.86CADExitPrice:$0.71CADLithiumAmericasCorp(TSE:LAC)FeaturedIn:January2014PartnershipAverageCostperShare:$0.24CADCurrentMarketPrice(July29,2016):$0.96CADLithiumAmericas(formerlynamedWesternLithium)wasthePartnership’sfeaturedinvestmentinJanuary2014.WhenIlastprovidedanupdateonLACinJanuary,thecompanywastradingatapproximately$0.40CAD.Thecompany’sfortuneshaveshiftedsignificantlyoverthepast6months,andshareholdershavebeenrewardedwitha140%YTDgain.Whileincreasingbuzzaroundthelithiumspacehasn’thurtmatters,thecatalystforthismovewasthetransformativejointventuredealthatLithiumAmericasreachedwith$7blithiumheavyweightSQM.ThisJVdeal,whichwasannouncedonMarch28th,willbethefocusofthisupdate.TheannouncementoftheSQMjointventurewasasurprisetomostmarketparticipants,consideringLithiumAmericashadjustsigneda“HeadsofAgreement”withindustrialconglomeratePOSCOinAugust2015.POSCOhoweverhaditschance

47

tolockuptheCauchari-Olarozproject,butspenttheremainderof2015bickeringovertermswithLithiumAmericasmanagement.OncetheHOA’sexclusivityclauseexpiredinJanuary2016andnodealhadbeenreached,LithiumAmericasbegantoonceagainconsiderthirdpartyoffers.ThisiswhenSQMsteppeduptotheplate,withthefollowingdealannouncedafter2-3monthsofnegotiations:TheJointVenturewillgointoeffectfollowingacapitalcontributionofUS$25millionbySQMinexchangefora50%ownershipstakeinMineraExarS.A.("MineraExar"),awhollyownedsubsidiaryofLAC.SQM'scontributionincludesUS$15milliontorepayintercompanyloansbetweenMineraExarandLAC;theremainingUS$10millionwillbeallocatedtoprojectdevelopment.SQMandLACintendtoimmediatelyadvanceaworkandengineeringplan,whichcontemplatescompletionofanupdateddefinitivefeasibilitystudybasedonanexistingstudyforCaucharithatwascompletedbyMineraExarin2012.Theupdatedstudywillevaluateeconomicfeasibilityforaprojectwithanameplateproductioncapacityofapproximately40,000metrictonsperyearoflithiumcarbonateequivalent.Dependingontheresultsofthestudy,theprojectmaybeexecutedinstages. Thekeytakeawayshereinclude:1.SQMpaysLithiumAmericas$25mfor50%ofCauchari-Olaroz2.LithiumAmerica’sremaining50%stakeintheJVisNOTfreecarried(meaningthatthecompanywillhavetopayfortheirfairshareoffeasibility-relatedcostsandtheproject’sinitialcapex)3.Afeasibilitystudywillbereleasedbyyear-enddemonstratingtheeconomicsofa40,000tonperyearoperation.Thisistwicethenameplatecapacitythatpreviouseconomicstudieshadenvisioned.JohnKanellitsas,whoisViceChairmanofLithiumAmericas,commented:“LithiumAmericas’boardhasdeterminedthatSQMrepresentsthepremierpartnerintheworldforourproject.Theirunderstandingofbrinechemistries,pondandchemicalplantconstruction,knowledgeofallend-userproductspecificationsandthecollaborativeapproachwithourteamwereimportantcriteriainourselectionprocess.WebelievethatSQMistheworld’slargestandlowestcostproduceroflithiumfrombrinesandourboardhasdeterminedthatajointventurewithSQMinwhichwepursueaproductionpathutilizingaproven,low-costbrineevaporationprocessrepresentstheoptimalcoursetomaximizelongtermvalueforLithiumAmericas’shareholders.”Marketreactiontothedealwasatfirstmuted,assomebelievedthatLithiumAmericashadnotreceivedsufficientcompensationfor50%oftheproject.However,

48

LAC’ssharepricestartedclimbingoncethesheermagnitudeoftheoperation(andthesignificanceofSQM’sinvolvement)begantosinkin.InaMay4thnewsrelease,SQMassuredthemarketoftheirintentionstofast-trackCauchari-Olaroztoproduction:“InMarchofthisyear,SQMandLithiumAmericasannouncedajointventuretodeveloptheCaucharí-OlarozlithiumprojectintheJujuyprovinceofArgentina.Theproject’sproductioncapacityistargetedat40,000tonsperyearoflithiumcarbonateequivalent.Underthecurrentprojecttimeline,thecompaniesexpecttobeginplantcommissioningandproductionby2019.TotalcapitalexpendituresfortheprojectareestimatedtorangebetweenUS$500millionandUS$600million,dependingonfinaldesigncriteriaandprojectstaging.SQMhasbeendiligentlyworkingonthisprojectsincethebeginningofApril2016andhopestobeabletostartconstructionbythefirsthalfof2017.SQMiscommittedtosuccessfullydevelopingtheMineraExarprojectinordertomeettheworld'slithiumneeds,complementingitsexistinglithiumoperationsinChile.”Anotherrecentdevelopmentdemonstratesthetremendousexcitementsurroundingthecompany.InaMay2ndnewsrelease,LithiumAmericasannouncedtheappointmentofDavidDeakasthecompany’sCTO.LithiumAmericasCEOTomHodgsoncommented:

"Davidiswidelyrespectedthroughoutthegloballithiumsupplychain.Hehasthetechnicalinsight,commercialexperience,andindustryrelationshipsrequiredtoadvancetheLithiumAmerica'smission,includingtheNevadaclayproject.WeexpecttobenefitfromDavid'sleadershipinhisroleasthecorporateCTOandcontributionstoourrecently-announcedJointVenturewithSQMfortheCauchari-OlarozprojectinArgentina.WehavealsoaskedDavidtoleadthedevelopmenteffortsforourNevada-basedproject,whichrepresentsoneofthelargestlithiumresourcesinNorthAmerica,andremainsanimportantcorporatepriority."Davidwaspreviouslyahigh-rankingofficeratTeslaworkingonrawmaterialprocurementforthegigafactory.ToaccepttheCTOposition,hehadtoturndownanofferfromApple-presumablytoworkintheirsecretivecardivision,dubbed“ProjectTitan”.David’sinvolvementisfurthervalidationforthesignificanceoftheCauchari-Olarozproject.WhatistheprojectworthtoLACshareholders?Thisisatoughquestion,particularlyasthe40,000tpyFeasibilityStudyisstillinprogress.Additionally,thereismuchcontroversyabouttheappropriatelong-termlithiumcarbonateprice.

49