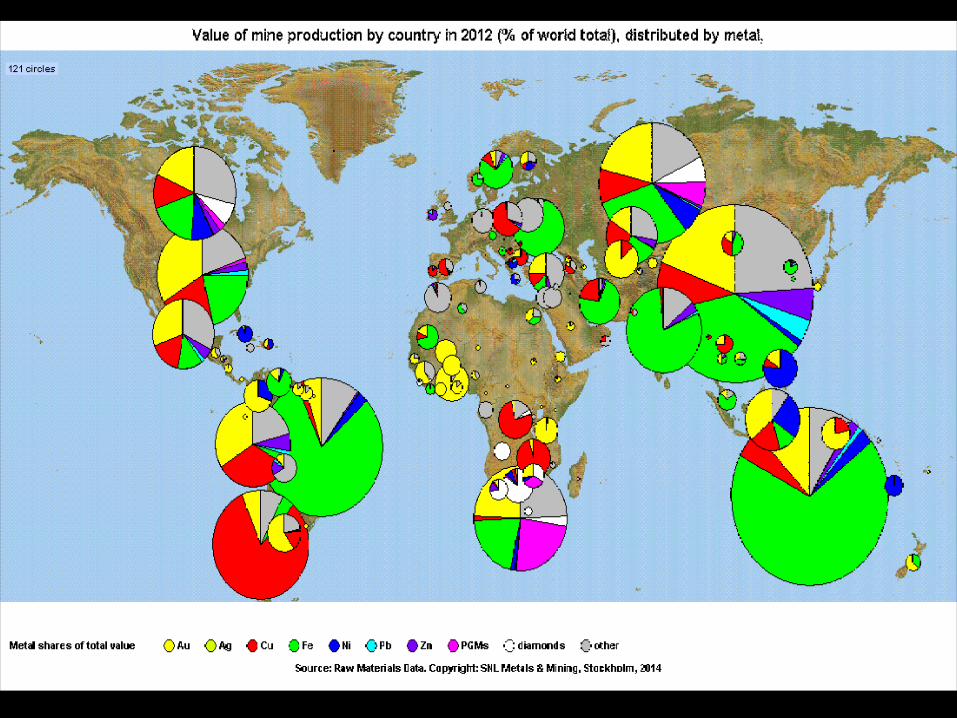

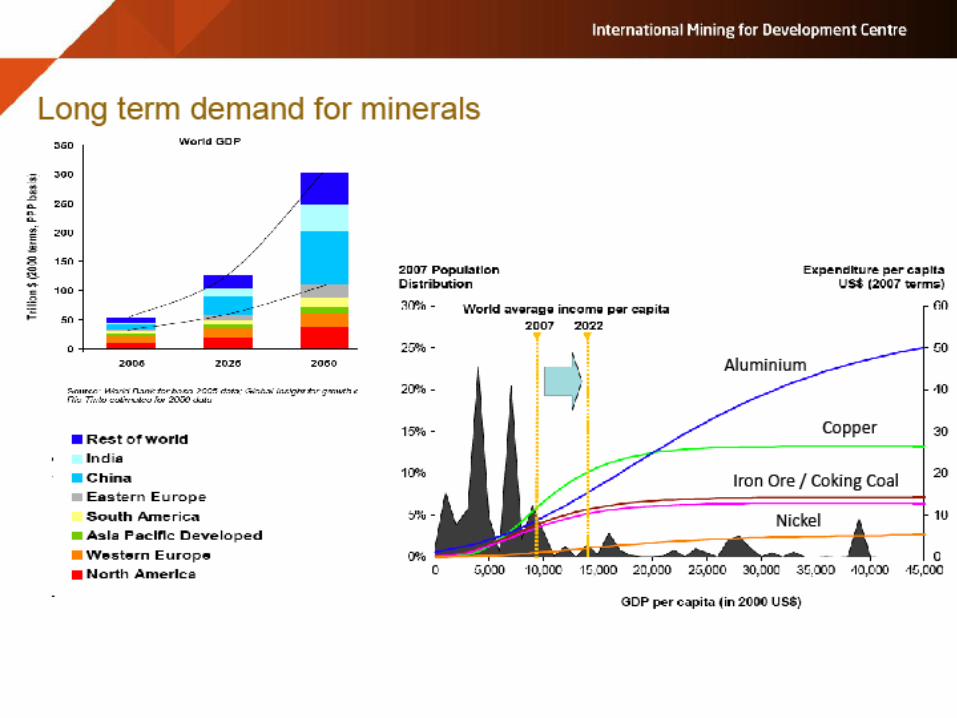

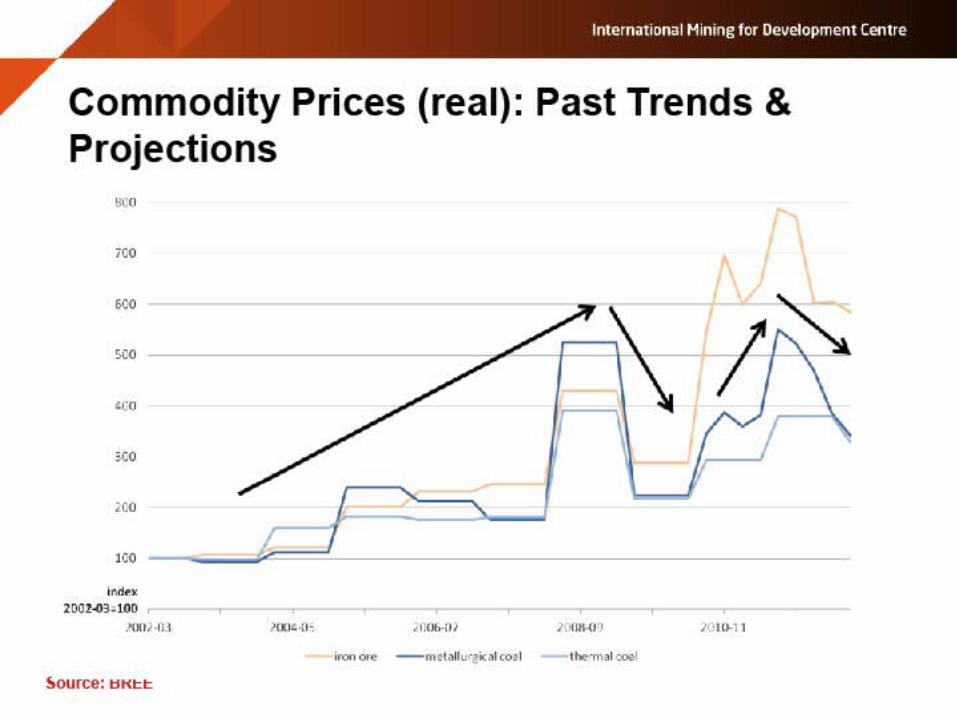

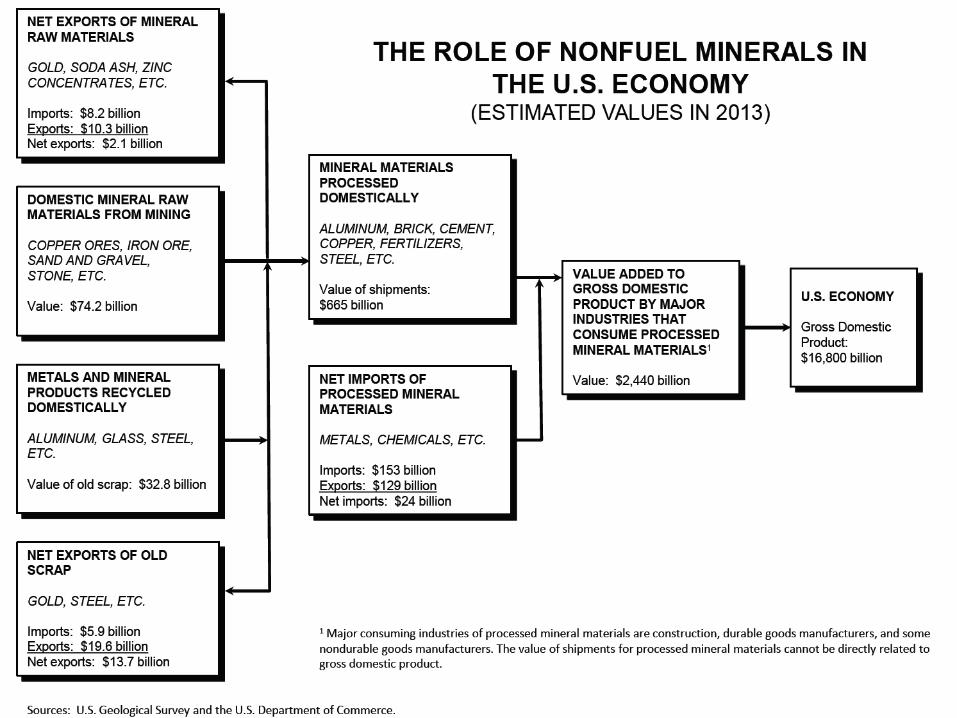

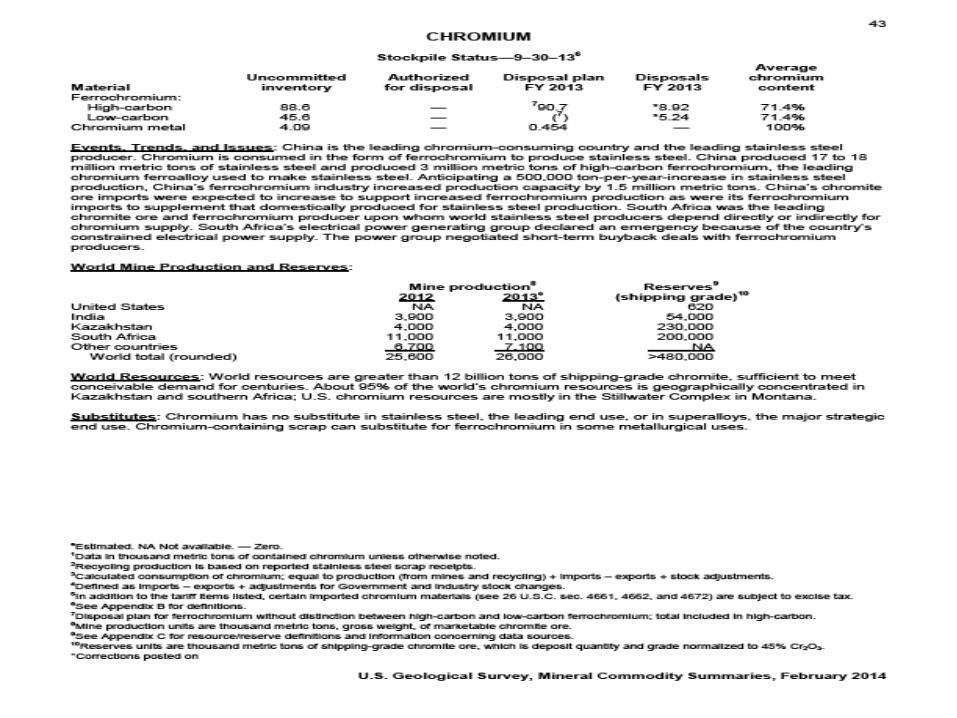

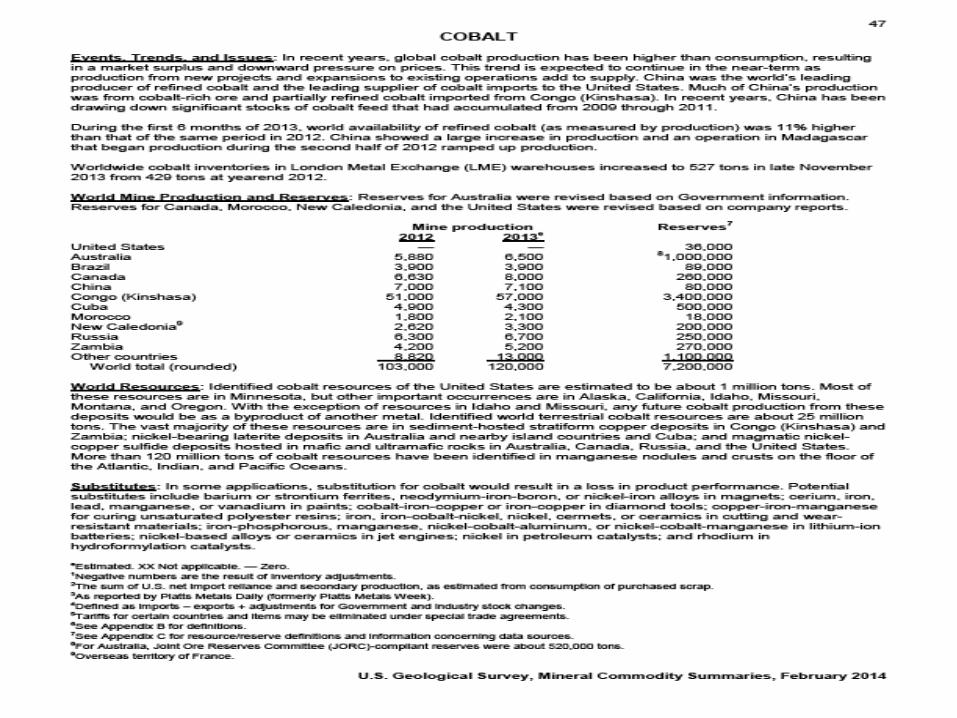

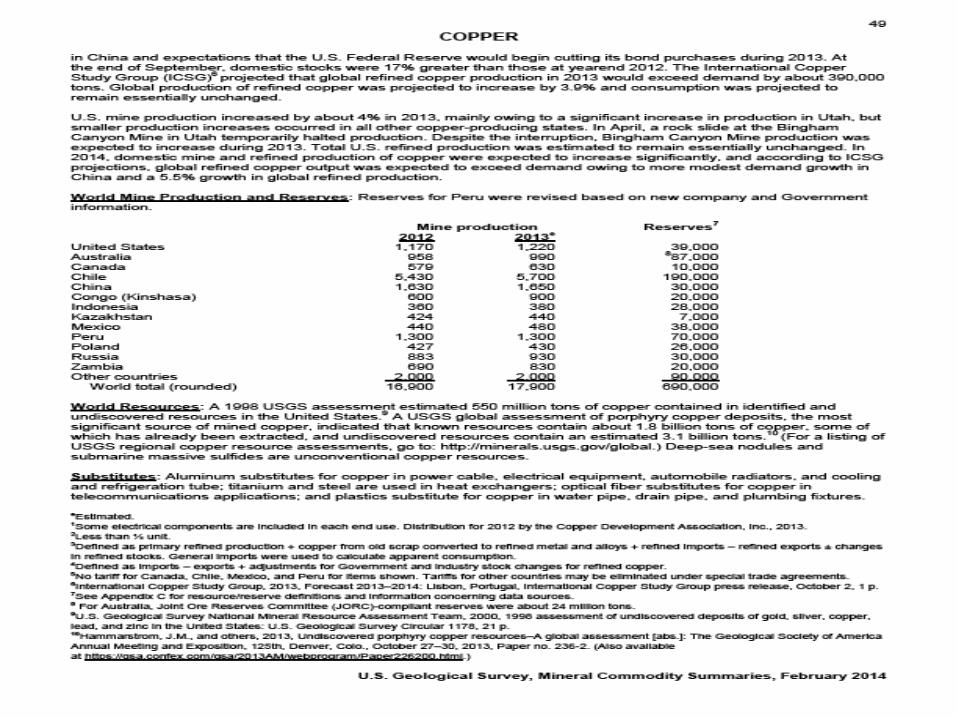

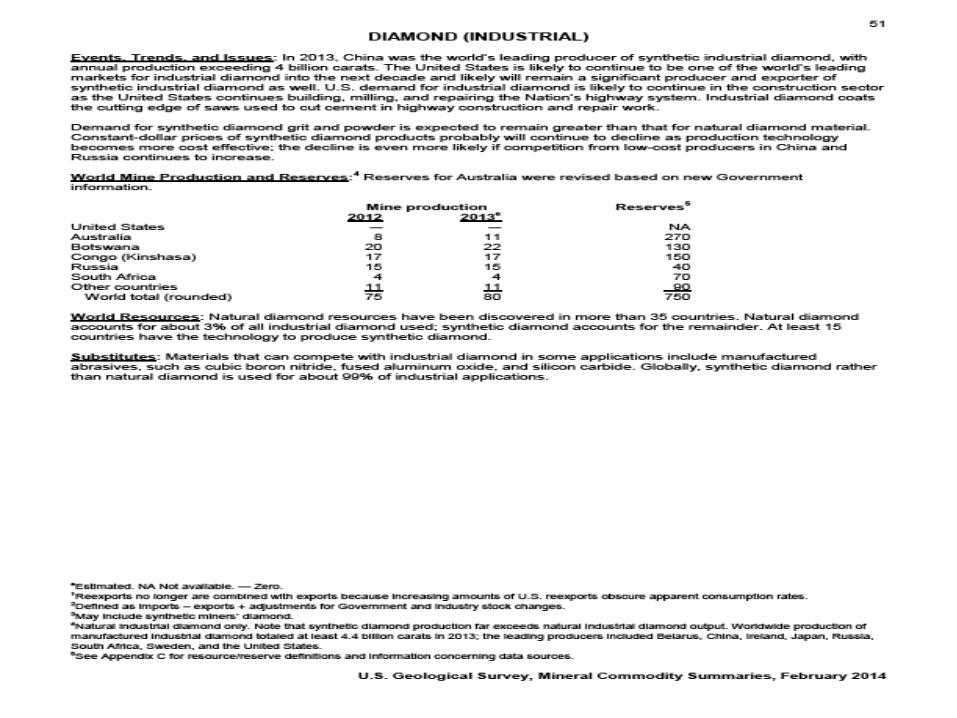

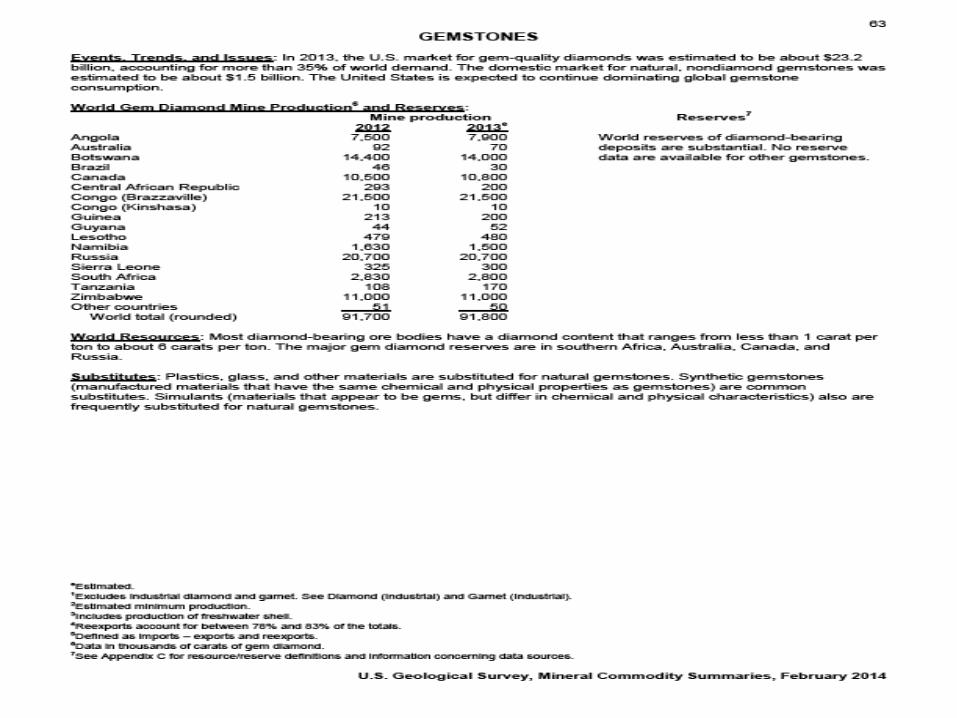

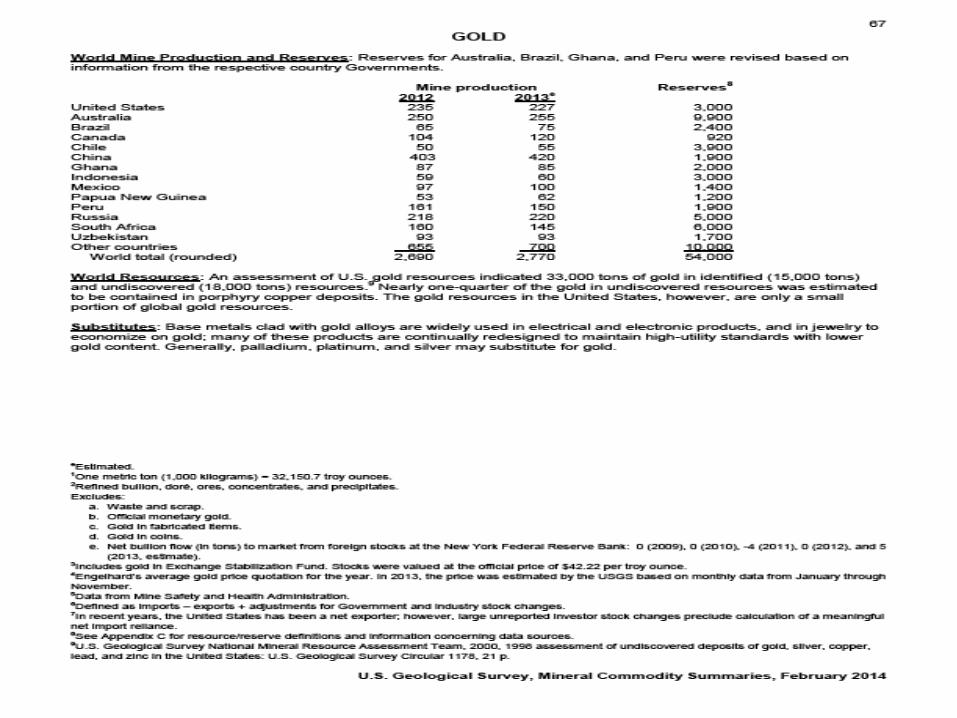

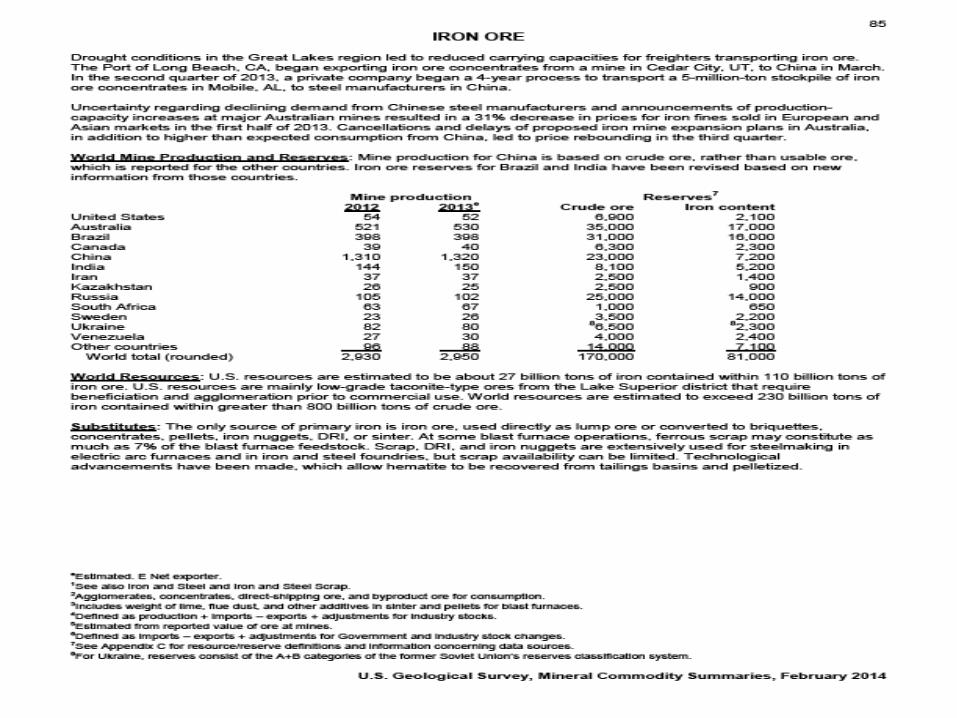

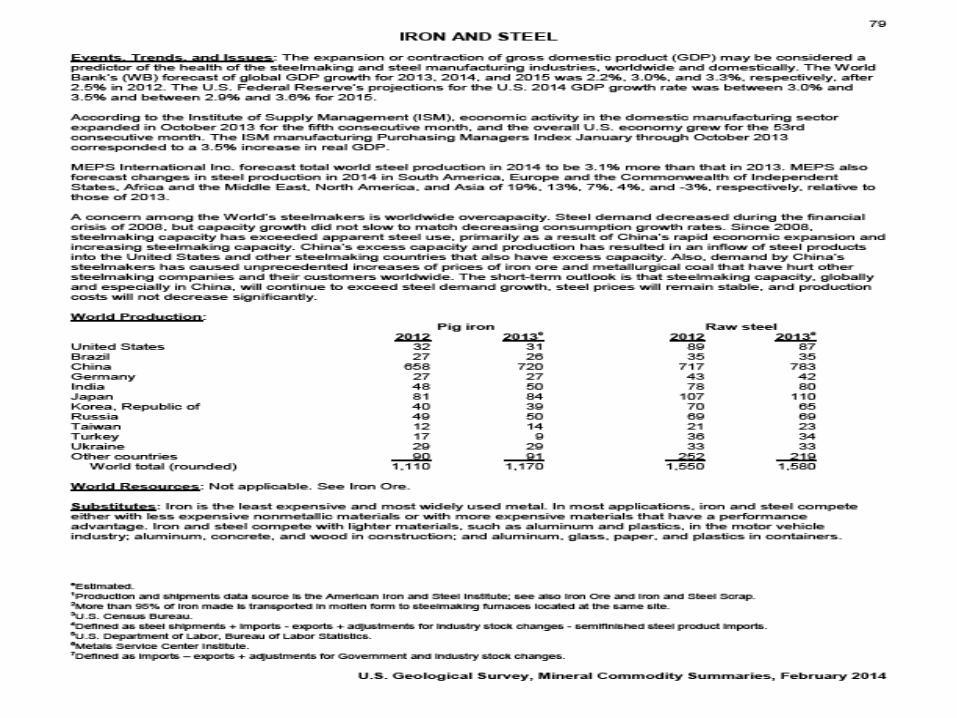

to give you an idea

DESCRIPTION

Markets, value chains and commodity prices of hydrocarbons and minerals by Antonio Pedro, Director UNECA SRO-EA Kigali, Rwanda. To give you an idea. Some other important facts. Measurements. Diamonds and other gemstones: Carats Oil: Barrels Gold, platinum, silver: Oz Coal: Tons - PowerPoint PPT PresentationTRANSCRIPT

Markets, value chains and commodity prices of hydrocarbons and minerals

by Antonio Pedro,Director UNECA SRO-EA

Kigali, Rwanda

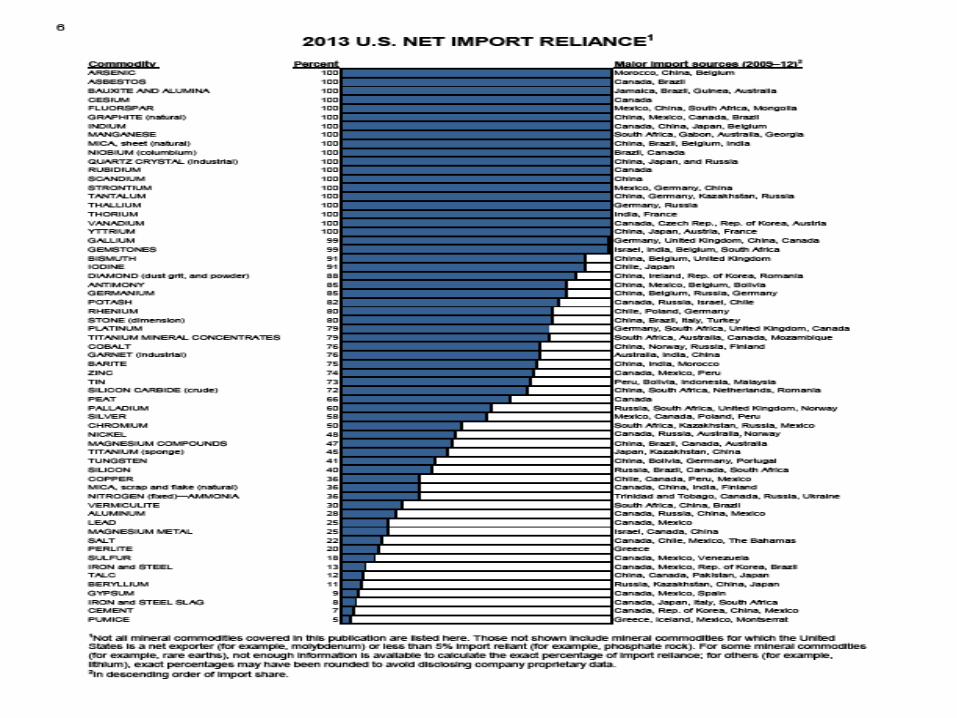

To give you an idea

Some other important facts

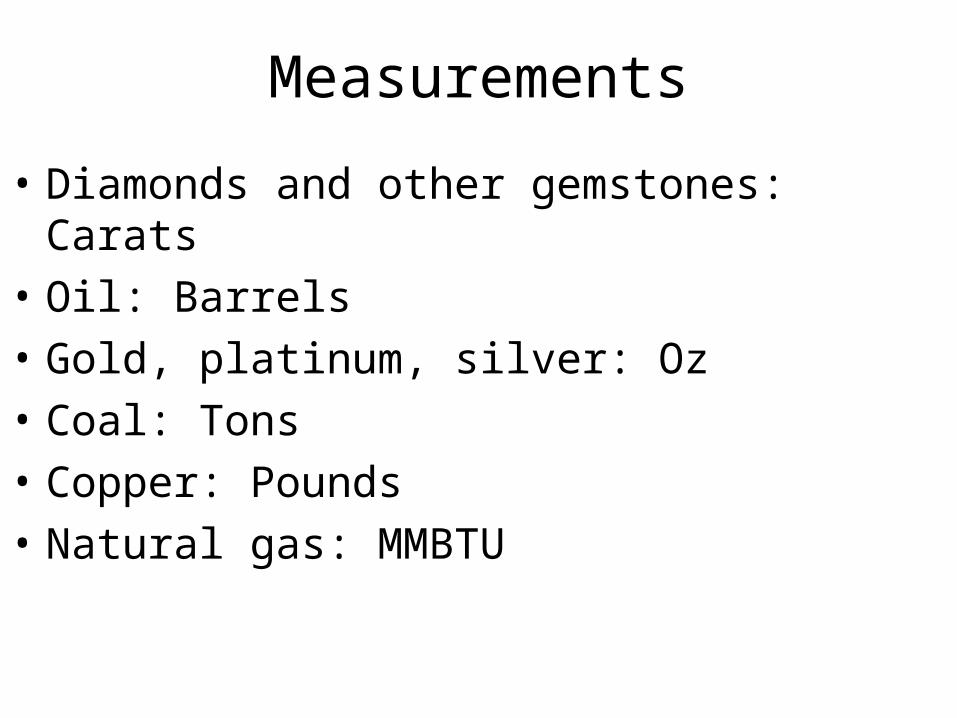

Measurements

• Diamonds and other gemstones: Carats• Oil: Barrels • Gold, platinum, silver: Oz• Coal: Tons• Copper: Pounds• Natural gas: MMBTU

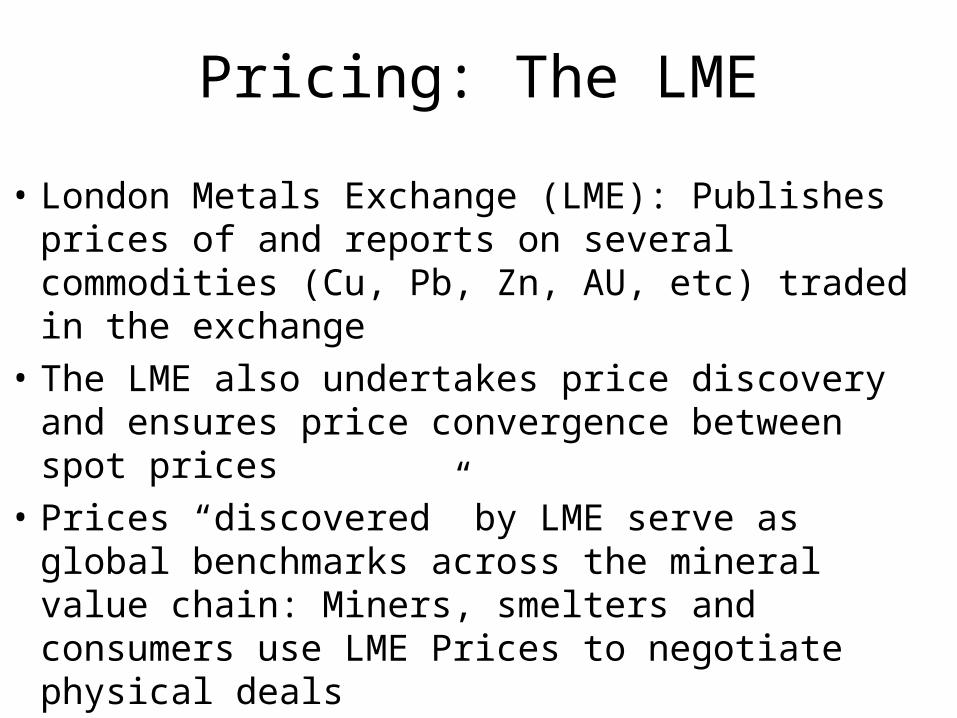

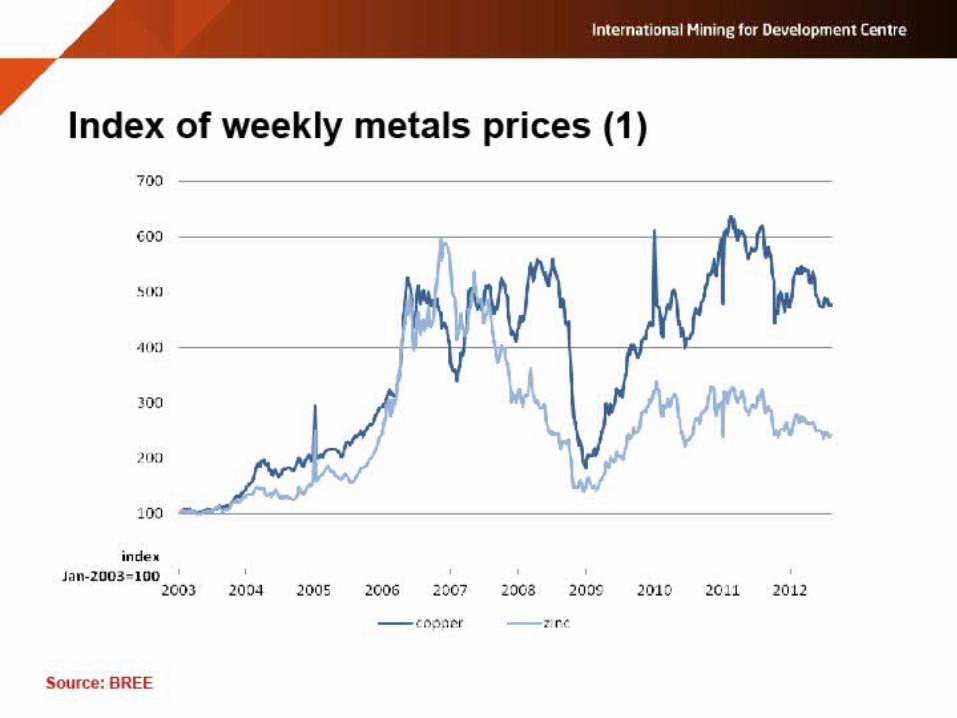

Pricing: The LME

• London Metals Exchange (LME): Publishes prices of and reports on several commodities (Cu, Pb, Zn, AU, etc) traded in the exchange

• The LME also undertakes price discovery and ensures price convergence between spot prices

• Prices “discovered” by LME serve as global benchmarks across the mineral value chain: Miners, smelters and consumers use LME Prices to negotiate physical deals

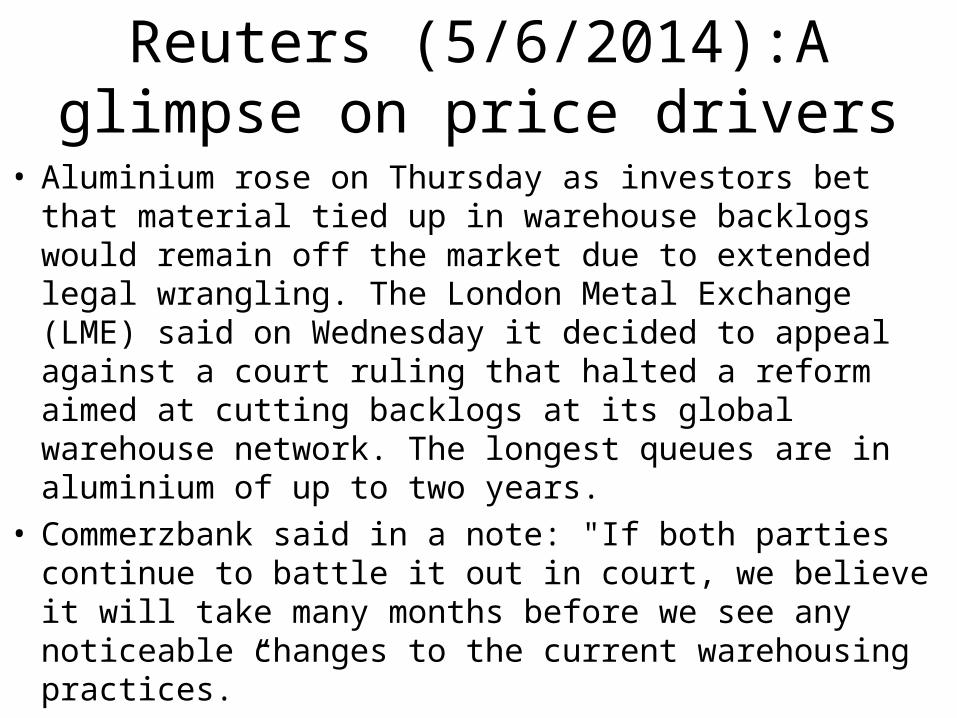

Reuters (5/6/2014):A glimpse on price drivers

• Aluminium rose on Thursday as investors bet that material tied up in warehouse backlogs would remain off the market due to extended legal wrangling. The London Metal Exchange (LME) said on Wednesday it decided to appeal against a court ruling that halted a reform aimed at cutting backlogs at its global warehouse network. The longest queues are in aluminium of up to two years.

• Commerzbank said in a note: "If both parties continue to battle it out in court, we believe it will take many months before we see any noticeable changes to the current warehousing practices.”

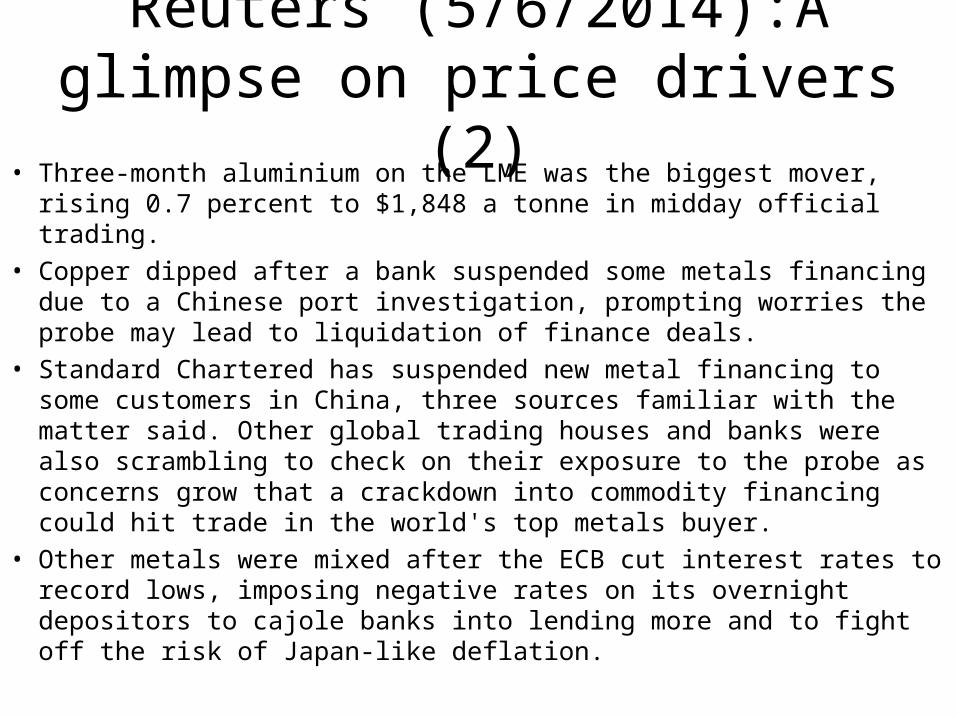

Reuters (5/6/2014):A glimpse on price drivers (2)

• Three-month aluminium on the LME was the biggest mover, rising 0.7 percent to $1,848 a tonne in midday official trading.

• Copper dipped after a bank suspended some metals financing due to a Chinese port investigation, prompting worries the probe may lead to liquidation of finance deals.

• Standard Chartered has suspended new metal financing to some customers in China, three sources familiar with the matter said. Other global trading houses and banks were also scrambling to check on their exposure to the probe as concerns grow that a crackdown into commodity financing could hit trade in the world's top metals buyer.

• Other metals were mixed after the ECB cut interest rates to record lows, imposing negative rates on its overnight depositors to cajole banks into lending more and to fight off the risk of Japan-like deflation.

Pricing: Diamond sightholders

• Buying and selling of diamonds depends on agreed standards of size, shape, colour and clarity

• De Beers has 12000 identifiable different types of diamonds

• Sorting is done by experts using traditional loupes or advanced technology for large volumes or small stones

• Sorters classify the diamonds by comparisons with master reference samples

• Each diamond category corresponds to a price in the Global Sightholder Sales Property Price Box

Pricing: Crude oilExtracted from STEVE AUSTIN OIL-PRICE.NET, 2014/05/05

• There are three main global oil price indexes: The West Texas Intermediate (WTI) set by the New York Mercantile Exchange); The Brent Crude Index, set by the Intercontinental Exchange in London; and the OPEC Basket (average of oil prices in all OPEC countries), set in Vienna

• Beyond the indexes, politics and transport networks influence price setting

• Oil refineries buy their oil by the barrel• The index rises and falls depending on how many people

want to buy oil on a particular day

Pricing: Crude oil (2)• Speculators and political tensions (which can disrupt supply routes)

impact commodity prices• Volatility work for speculators: Any price movement would

immediately offer an opportunity for them to sell their inventory at a higher price

• Speculators and the information providers that support them, over-react to world news to try to force dips and peaks so they can buy and sell

• Many who invest in oil never actually intend to take delivery. They just want to buy a contract at a low price and then sell it at a higher price

• State of world economy (e.g. global recession) would also impact prices: Demand for oil would go down and prices would fall

Pricing: Crude oil (3)• Other investor-related factors may also influence the price of crude

oil: The banking crisis of 2008 saw savers looking for places to store their money when it looked like banks might go bust, so they poured money into commodities, including oil. Thus, the price of oil rose despite a general collapse in demand

• Buyers of oil for delivery rarely pay the index price. However, the price of a particular index is a factor in the contract price mechanism

• Not all oil in the world is the same. Some oil is quicker and cheaper to refine than others. Thus, you would likely pay more for oil that is easy to process, than for oil that is expensive to process

• The location of the oil and transport capacity is also a factor• Prices of natural gas used to mirror the behaviour of crude oil prices,

but now they are more in tune with coal price sentiments

Pricing: Industrial minerals

• We are talking of limestone, clays, gypsum, sand and gravel, dimension stones, and silica for the production of cement, bricks, glass, ceramics, and abrasive products

• Mostly high-volume and low cost• Sensitive to distance and transport costs• Specifications are key

Pricing: It can be even very messy and complicated

• In the good old days there was clear correlation between commodity prices and supply/demand ratios

• Now we talk about decoupling and financialisation of commodities: We have hedging, derivates, future markets and many other fancy trade and pricing instruments

• Read this: “In "swap" transactions participants exchange rights to future cash flows based on underlying index prices or delivery obligations or time periods. Participants use these tools to further hedge their financial exposure to the underlying price of natural gas”

• Transfer pricing complicates matters: Berne Declaration and “Treasure Islands”

• ASM: Plugged by smuggling, but hope in fair trading (e.g. “green gold”

The case of China

• Largest producer of coal, gold, cement, stainless steel, refined cobalt, lead, phospate rock, rare earths (96%), zinc

• Number one consumer and importer of most minerals, metals and hydrocarbons

• Since 2002, its economic growth trajectory had major impact on commodity price increases: iron ore prices went up 6X, coking coal 5X and thermal coal 3X

• Slower growth from 2008 onwards dumped prices

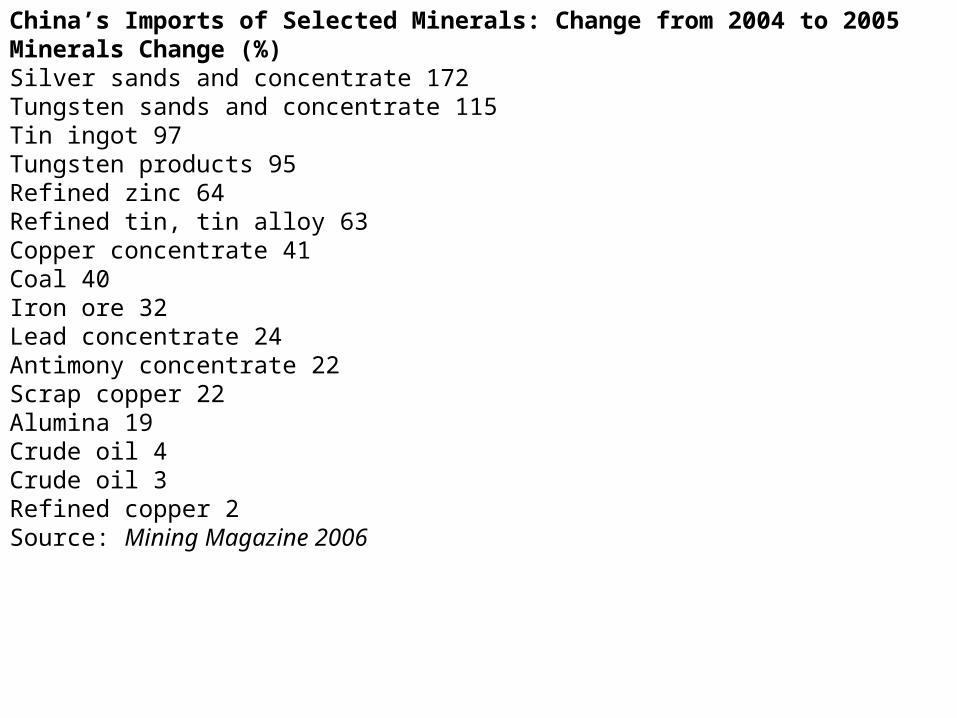

China’s Imports of Selected Minerals: Change from 2004 to 2005Minerals Change (%)Silver sands and concentrate 172Tungsten sands and concentrate 115Tin ingot 97Tungsten products 95Refined zinc 64Refined tin, tin alloy 63Copper concentrate 41Coal 40Iron ore 32Lead concentrate 24Antimony concentrate 22Scrap copper 22Alumina 19Crude oil 4Crude oil 3Refined copper 2Source: Mining Magazine 2006

Many thanks!