tne 1 tele norte leste participaÇÕes s.a. morgan stanley dean witter global communications...

TRANSCRIPT

1

TNE

TELE NORTE LESTE TELE NORTE LESTE PARTICIPAÇÕES S.A.PARTICIPAÇÕES S.A.

Morgan Stanley Dean Witter Morgan Stanley Dean Witter Global Communications ConferenceGlobal Communications Conference

March, 2001March, 2001

The information included herein has already been filed with SEC and CVM (Brazil) and is also available at www.telemar.com.br

2

TNE

Largest Brazilian Company*

Second Largest Telco in Latin America

Heaviest Weight on IBOVESPA (Jan/01)

First Brazilian Company ADR Volume (Jan/01)

Shareholders’ Equity: US$ 5.1 billion

Market Value: US$ 9.2 billion (Jan/01)

Free Float: 82% of Total Shares

OverviewOverview

* Privately owned

3

TNE

Covers 65% of Brazilian Territory

Reaches 93 million people

Over 20 million households

12.2 million Fixed Lines in Service (Feb/01)

13% Penetration Rate (Brazil: 21%)

560 Lines in Service/Employee

OverviewOverview

4

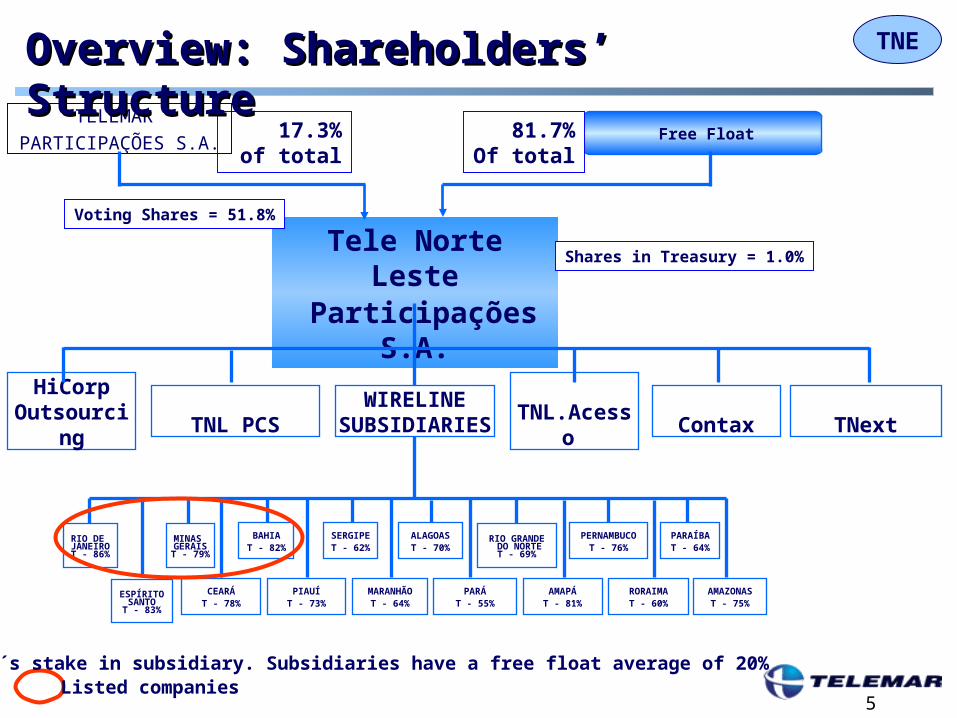

TNEOverview: Shareholders’ StructureOverview: Shareholders’ Structure

Tele Norte Leste Participações S.A.

Free Float

CEARÁ

T - 78%

PIAUÍ

T - 73%

MARANHÃO

T - 64%

AMAPÁ

T - 81%

AMAZONAS

T - 75%

RORAIMA

T - 60%

PARÁ

T - 55%

ALAGOAS

T - 70%

PERNAMBUCO

T - 76%

PARAÍBA

T - 64%

RIO GRANDE DO NORTE

T - 69%

RIO DE JANEIROT - 86%

ESPÍRITOSANTOT - 83%

MINAS GERAIST - 79%

BAHIA

T - 82%

SERGIPE

T - 62%

Preferred Shares -----99.5% Brazil ------ 52% ADR ------- 48%

Common Shares ------- 46.0%

81.7%17.3%

Common Shares = 51.8%

TELEMAR PARTICIPAÇÕES S.A.

Total Shares: 373,577 millionPreferred: 249,051 millionCommon: 124,526 million

Shares in Treasury = 1.0%

T= TNE´s stake in subsidiary. Subsidiaries have a free float average of 20%

Listed companies

TOTAL CAPITALBNDESParFiagoAG TelecomASSECA ParticipaçõesLexpart Part.L. F. Tel BrasilCapBrasilVeículos

25.0%19.9%11.3%11.3%11.3%11.3%

5.0%5.0%

5

TNE

Tele Norte Leste Participações S.A.

Free Float 81.7%Of total

17.3% of total

Voting Shares = 51.8%

TELEMAR

PARTICIPAÇÕES S.A.

T= TNE´s stake in subsidiary. Subsidiaries have a free float average of 20%Listed companies

CEARÁT - 78%

PIAUÍT - 73%

MARANHÃOT - 64%

AMAPÁT - 81%

AMAZONAST - 75%

RORAIMAT - 60%

PARÁT - 55%

ALAGOAST - 70%

PERNAMBUCOT - 76%

PARAÍBAT - 64%

RIO GRANDE DO NORTE

T - 69%

RIO DE JANEIROT - 86%

ESPÍRITOSANTOT - 83%

MINAS GERAIST - 79%

BAHIAT - 82%

SERGIPET - 62%

WIRELINESUBSIDIARIES

HiCorpOutsourcing TNL PCS Contax TNext

Shares in Treasury = 1.0%

TNL.Acesso

Overview: Shareholders’ StructureOverview: Shareholders’ Structure

6

TNERecent Developments: HighlightsRecent Developments: Highlights

Main Drivers (Revenues) – Dec/00

Line growth: 2.1 million in 2000

Fixed-to-Mobile traffic

Tariff increase – July/00

•14% Local Service/Interconnection

•11.9% DLD

•9.5% Fixed-tp-Mobile (VC1) – Feb/01

Revenue Growth: 31% (00/99)

EBITDA Margin: 49.6% (12M00)

+21.7%

over65%

7

TNERecent Developments: HighlightsRecent Developments: Highlights

Main Drivers (Costs)

Cost Savings (R$ 113 million YoY/Ex-interconnection)

•Integration (Data Processing, Network Management

and Call Centers)

•Shared Services Center (Back Office Functions: SAP

and PeopleSoft)

Improving Efficiencies (network upgrade, systems and

processes)

Revenue Growth: 31% (00/99)

EBITDA Margin: 49.6% (12M00)

8

TNE

15.8

11.811.1

10.410.09.7

18.0

12.812.0

11.310.810.5

95.089.687.9

84.982.180.7

4Q99 1Q00 2Q00 3Q00 4Q00 4Q01E

Lines in Service Lines Installed Digitalization Rate

(million) (%)

Recent Developments:Recent Developments:Plant & Digitalization GrowthPlant & Digitalization Growth

UTI%

92.9 92.2 92.1 92.3 92.3 88.0

TNE

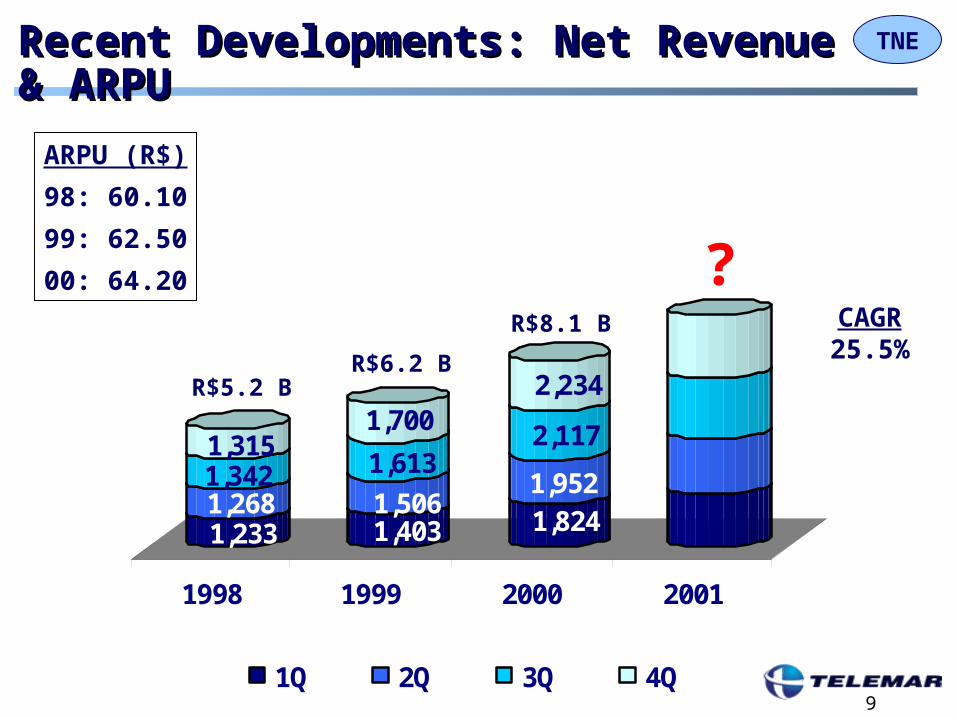

9

1,2331,2681,3421,315

1,4031,506

1,613

1,700

1,8241,952

2,117

2,234

1998 1999 2000 2001

1Q 2Q 3Q 4Q

CAGR25.5%

Recent Developments: Net Revenue & ARPURecent Developments: Net Revenue & ARPU

R$5.2 BR$6.2 B

R$8.1 B

ARPU (R$)

98: 60.10

99: 62.50

00: 64.20 ?

10

TNE

45%

20%

12%

11%

12%

44%

23%

12%

9%

12%

4Q99 4Q00

Recent Developments: Main ServicesRecent Developments: Main Services

Data 5%

DLD

67%

65%

Network Use

Fixed to Mobile

Local

GrossRevenue

R$2,288 mm R$2,996 mm

Other

11

TNERecent Developments: EBITDARecent Developments: EBITDA

1,090

1,149

965

829

599

49%

54%

49%

35%

45%

56%

64%67%

61%

43%

4Q99 1Q00 2Q00 3Q00 4Q00

EBITDA (R$ million) EBITDA Margin (%) Margin ex-interconnection costs (%)

Reduced by R$135

MM

12

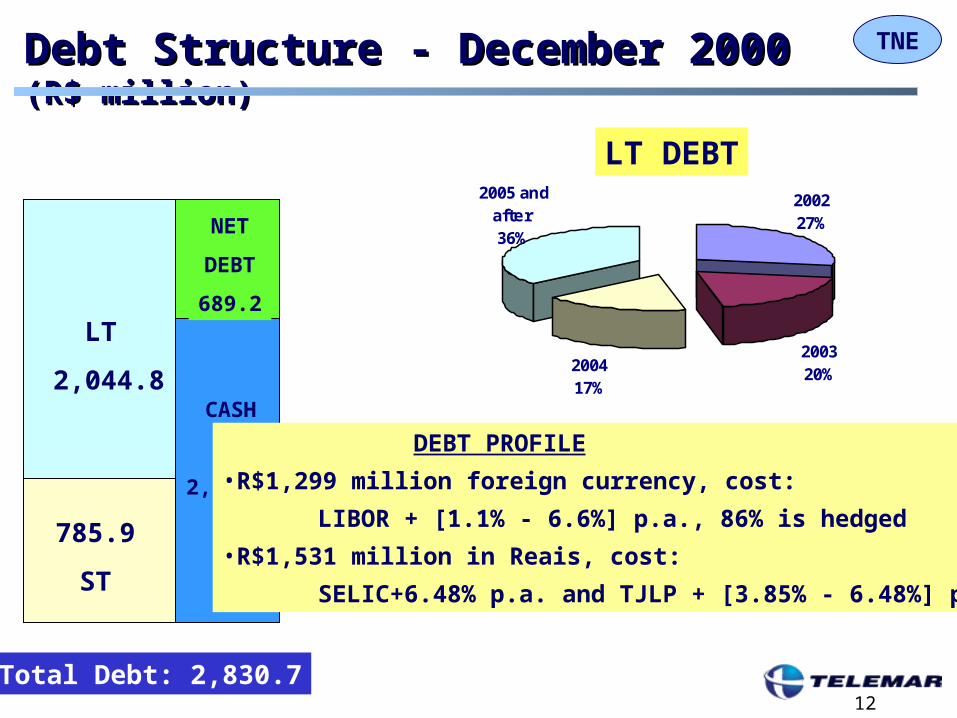

TNE

785.9

ST

LT

2,044.8

NET

DEBT

689.2

CASH

2,141.5

Total Debt: 2,830.7

LT DEBT

Debt Structure - December 2000Debt Structure - December 2000 (R$ million) (R$ million)

200320%2004

17%

200227%

2005 and after36%

DEBT PROFILE

•R$1,299 million foreign currency, cost:

LIBOR + [1.1% - 6.6%] p.a., 86% is hedged

•R$1,531 million in Reais, cost:

SELIC+6.48% p.a. and TJLP + [3.85% - 6.48%] p.a.

13

TNE

World Class - Global Operator

Class A - Mobility

Class B - National Coverage

2000 20022001 2003

Class C - National Corporate Excellence

Class D - Regional Excellence

Steps to Maximize ValueSteps to Maximize Value

Telemar shall increase its value as the company incorporates broader strategies.

14

TNEMain TargetsMain Targets

Data & Corporate Services

Nationwide Coverage

Mobility

Efficiencyand

Qualityof Services

15

TNE

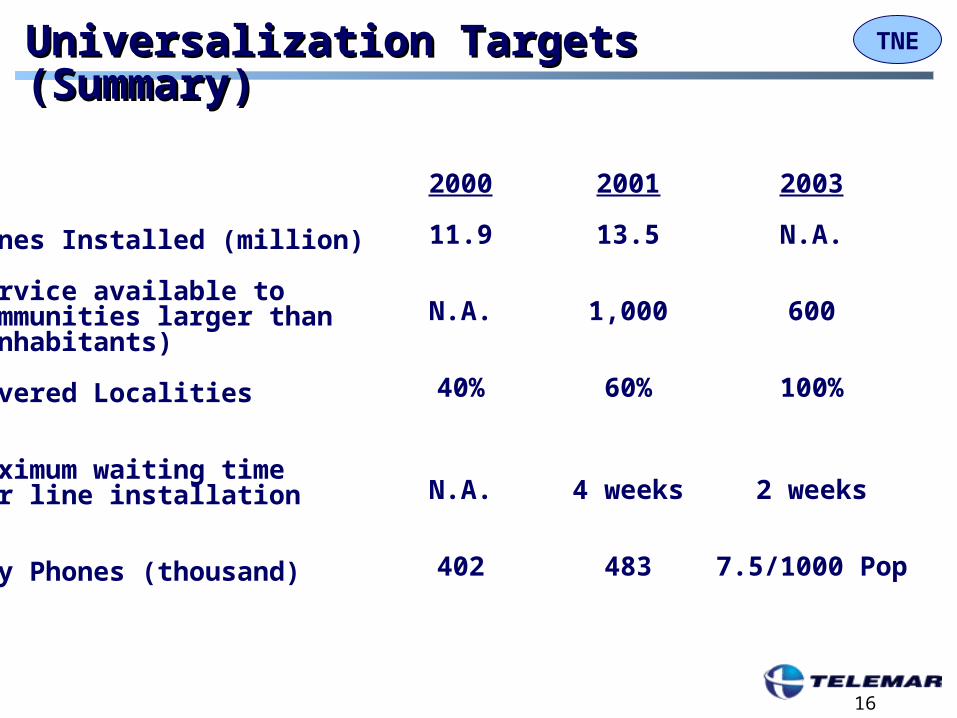

MAIN PRIORITY

Fulfill all 2003 Universalization Targets

Nationwide CoverageNationwide Coverage

16

TNE

Lines Installed (million)

Service available tocommunities larger than(inhabitants)

Covered Localities

Maximum waiting timefor line installation

Pay Phones (thousand)

2000

11.9

N.A.

40%

N.A.

402

2001

13.5

1,000

60%

4 weeks

483

2003

N.A.

600

100%

2 weeks

7.5/1000 Pop

Universalization Targets (Summary)Universalization Targets (Summary)

17

TNENationwide Coverage Nationwide Coverage

DECEMBER 2000

TNE had 12.8 million Lines Installed

DECEMBER 2001TNE will have

18.0 million Lines Installed*

* Including Public Phones and WLL

2001 CAPEX : R$ 8.4 Billion

+5.2 MM

Rio24%

Minas19%

Bahia12%

Ceará12%

Pernambuco11%

Holding22%

Communication Systems

4%

IT Structure2%

Oper./Maint.8%

Universalization Targets

46%

Quality Targets5%

PCS Business18%

Data Transmission

17%

(PCS license included)

18

TNENationwide CoverageNationwide Coverage

Mission

TO BECOME A NATIONAL OPERATOR FROM 2002 ON

DLDData

Services

Challenge

Fulfill and anticipate 2003 Goals

established by Anatel

19

TNENationwide Coverage Nationwide Coverage DLD Traffic Distribution – 2000DLD Traffic Distribution – 2000EE

2% 3%

28%

20%

25%

5%9%

5%

3%

Brazil:40.5 billion

minutes

Region IOriginates 35% Receives 40%

Region IIIOriginates 39% Receives 33%

Region IIOriginates 26%

Receives 27%

Source: Telemar and Mckinsey Co. estimates

20

TNE

151016

34

22

38

2000 2005

3.1

1.9

3.0

4.2

2.7

4.6

2000 2005

Nationwide CoverageNationwide CoverageBrazilian Market Trends (DLD and ILD)Brazilian Market Trends (DLD and ILD)EE

94

41

Region I

Region IIRegion III

Region I

Region II

Region III

Volumebillion minutes/year

RevenueR$ billion/year

8.0

11.5

CAGR18%

CAGR7.5%

Source: Telemar and Mckinsey Co. estimates

21

TNENationwide CoverageNationwide CoverageTelemar LD Market Share – 2005Telemar LD Market Share – 2005EE

47

17

36

23

18.5

58.5

2000 2005

0

100

15

85

2000 2005

National International

Player A

Telemar

Other

Telemar

Other

9441 0.71 1.56

Billion minutesSource: Telemar and Mckinsey Co. estimates

22

TNEData ServicesData Services

Mission

TO BECOME THE LEADER IN NATIONAL DATA MARKET

BY 2005

23

TNEData Services: Market ShareData Services: Market Share

1,973 7,866US$ million

CAGR: 31.9%

2000 2005

16.1%21%

Refers to 3 basic steps of value chain (Traditional and IP Transport and Advanced Services)

24

TNEData Services: Value ChainData Services: Value Chain

B2B commerce through portals and related infrastructure

Complex applications withCustomization and integration

Co-location and hosting services Application and software hosting

Value added servicesVoIP, security, management and other

IP ConnectivityDial-up and broadband connection

Traditional data communication servicesAccess to IP backbone

Description New BusinessesE-market

Place

ASP

Hosting

AdvancedServices

IPTransport

TraditionalTransport

25

TNE

MobilityMobility

26

TNEIntroductionIntroductionMain MessagesMain Messages

Quick DecisionsOpportunities Competitive

Advantages

• Operating synergies

• Commercial Synergies and fixed-to-mobile complement

• Opportunity to buy license at low price

Coverage

• Need for capillarity

• Network quality linked to number of cell sites

• R$ 2 billion CAPEX in 3 years, vendor financing

• Market growing quickly

• High Value Consumers

• New applications due to rapid technological development –GPRS

• Aggressive competitors already established

• Aggressive Targets:

• Subscribers

• Revenue

• Largest roll-out in the world

Cellular telephony operations represent an excellent opportunity for Telemar, and the company is prepared for the challenges involved.

27

TNEThe Cellular Market Opportunity The Cellular Market Opportunity 2.5G/GPRS Advantages and Benefits for the Client2.5G/GPRS Advantages and Benefits for the Client

Larger data transmission capacity 14 - 40 kbps initially: according to the network and equipment transmission, vs. 9.6 GSM

No need to dial-up (packet switching)

Better network utilization, leading to smaller transmission costs than the previous system (circuit-switched).

Open to IP and Internet

Faster access to data

Enables the visualization of complex information (charts, tables, figures, etc.)

Billing connected to effective information transmission

Possibility of permanent connection

GPRS 2.5G Technology Advantages Benefits for the client

Telemar will be able to offer more advanced data transmission than its competitors since the first day of operations, on its way to 3G.

28

TNE

US$ / POP

Note: Total price of 2G licenseSource: Merrill Lynch November 2000, Anatel, DiamondCluster.

Telemar’s Competitive AdvantagesTelemar’s Competitive AdvantagesComparing License PricesComparing License Prices

Telemar: US$ 6/inhabitant

Telemar bought the D Band license at a low cost when compared to other prices paid.

29

TNE

Operating Synergies

Telemar’s Competitive AdvantagesTelemar’s Competitive AdvantagesSynergies between Fixed and Cellular OperationsSynergies between Fixed and Cellular Operations

• Network structure:– Some WLL sites can be shared with PCS

operations– Maintenance costs can be shared

between both operations

• Customer care and billing can be shared with Telemar’s fixed operations

• Backbone

Commercial Synergies

• Sales structure of Telemar Fixed– Own stores– Direct sales force

• Brand recognition– Reduced efforts required to insert a new

brand

• Customer base– 12 million Telemar customers (data

base)

• National “31 code”

Telemar shall take advantage of its significant synergies to leverage its position in the Brazilian telecommunications market.

30

TNE““Safe Harbor” StatementSafe Harbor” Statement

This presentation contains forward-looking statements. Statements that are

not historical facts, including statements about our beliefs and expectations,

are forward-looking statements and involve inherent risks and uncertainties.

These statements are based on current plans, estimates and projections, and

therefore you should not place undue reliance on them. Forward-looking

statements speak only as of the date they are made, and we undertake no

obligation to update publicly any of them in light of new information or future

events.

This presentation contains forward-looking statements. Statements that are

not historical facts, including statements about our beliefs and expectations,

are forward-looking statements and involve inherent risks and uncertainties.

These statements are based on current plans, estimates and projections, and

therefore you should not place undue reliance on them. Forward-looking

statements speak only as of the date they are made, and we undertake no

obligation to update publicly any of them in light of new information or future

events.

31

TNE

Investor Relations

Rua Lauro Müller, 116 / 22º andar - Botafogo

Rio de Janeiro -RJ

Phone: ( 55 21) 279-3220/ 279-3221

Fax: (55 21) 279-3229

E-mail: [email protected]

Visit our website: http://www.telemar.com.br