title / divider screen titlemedia.ifrs.org/2013/projects/conceptual-fr… · ppt file · web...

TRANSCRIPT

The views expressed in this presentation are those of the presenter, not necessarily those of the IASB or IFRS Foundation.

© 2013 IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

International Financial Reporting Standards

Review of the Conceptual Framework

Presentation and disclosure

Kristy RobinsonTechnical Principal

Li Li LianTechnical Manager

Amy BannisterTechnical Associate

Before we start…• You can download the slides by clicking on the button below

the slides window• To ask a question, type into the designated text box on your

screen and click submit• A recording of the webcast will be available after the

presentation at http://go.ifrs.org/Conceptual-Framework• The views expressed are those of the presenters, not

necessarily those of the IASB or IFRS Foundation

2

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Project overview 3

• Not a fundamental re-think• Focus on weaknesses that have given problems in practice• Filling in gaps, and updating and improving existing guidance

Project objectives

• Preliminary views• Starting point for further discussion and consultation• Seeking your views by 14 January 2014

Discussion Paper objectives

• New Conceptual Framework will not override existing IFRSs

Project consequences

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

OverviewObjective of this webinar• Describe and explain the concepts in the Discussion Paper on

presentation and disclosure

What we will cover• What ‘presentation’ and ‘disclosure’ mean• The primary financial statements• The notes to the financial statements• Form of disclosure and presentation requirements

Questions

4

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

What do ‘disclosure’ and ‘presentation’ mean? 5

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Disclosure

Presentation

“the process of providing useful financial information about the reporting entity to users”

“the disclosure of financial information on the face of an entity’s primary financial statements”

Primary financial statements 6

The Discussion Paper identifies the primary financial statements as:

Statement of financial positionStatement(s) of profit or loss and OCIStatement of changes in equityStatement of cash flows

No primary financial statement is more important than the

other primary statements.

They should be looked at together.

Objective of the primary financial statements 7

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Disclosure

“to provide summarised information about recognised assets, liabilities, equity, income, expenses, changes in equity and cash flows that has been classified and aggregated in a manner that is useful to users of financial statements in making decisions about providing resources to the entity”

• recognised economic resources and claims• changes to those resources and claims• how efficiently and effectively the entity’s management and governing

board have discharged their responsibilities to use the entity’s resources

Classification and aggregation 8

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Line items

• Present useful summarised information

Aggregation

• The adding together of individual items within those classifications

Classification

• The sorting of items based on shared qualities

Determined by entity, but IASB

may decide to require a particular

line item to be

presented

Offsetting 9

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Disclosure

• Offsetting will generally not provide the most useful information because it combines dissimilar items, eg:

– assets & liabilities– income & expenses– cash receipt & cash payments

• The IASB may choose to require offsetting when:– provides a faithful representation of items– necessary on cost-benefit grounds

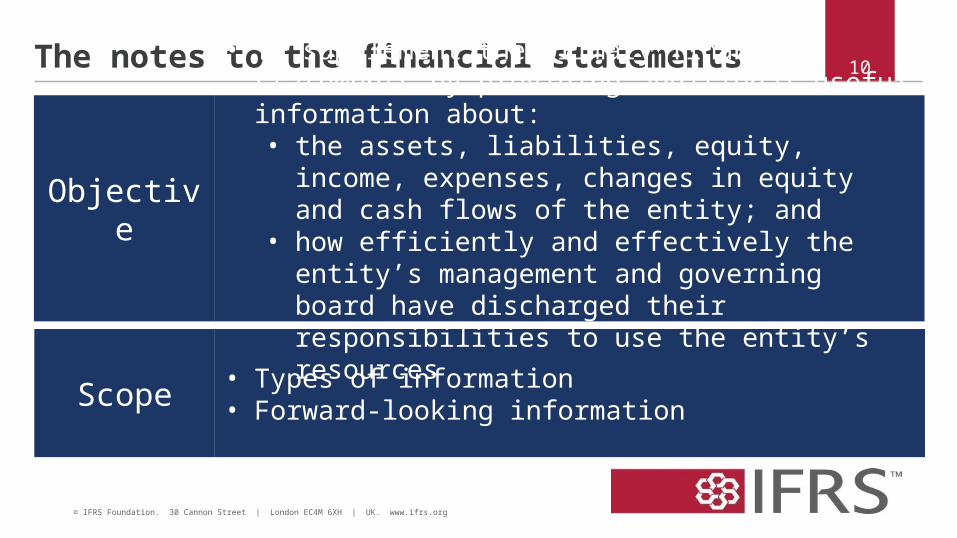

The notes to the financial statements 10

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Disclosure

Scope • Types of information• Forward-looking information

Objective

• To supplement the primary financial statements by providing additional useful information about:• the assets, liabilities, equity, income, expenses,

changes in equity and cash flows of the entity; and• how efficiently and effectively the entity’s

management and governing board have discharged their responsibilities to use the entity’s resources

Scope of the notes to the financial statements 11

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Disclosure

Type of information (scope) ExamplesReporting entity • Information about subsidiaries, associates, parent, etc.

• Business model

Amounts recognised in the primary financial statements

• Disaggregation of line items in primary financials• Relationship between line items

Unrecognised assets or liabilities • Description of unrecognised assets or liabilities and why they have not been recognised

Risks • Types of financial risk• How the entity has managed those risks

Methods, assumptions and judgements

• Accounting policies• Alternative measurements

Materiality

• Existing Conceptual Framework has a materiality concept• The IASB’s preliminary view is that that concept of materiality

is clearly described in the existing Conceptual Framework– not adding to or amending that description

• Another project on the IASB’s agenda looking at how the concept of materiality is applied

12

Form of disclosure and presentation requirements 13

• Each Standard should have a clear disclosure objective• Enables entities to determine whether the specified information is material for that entity

Disclosure objectives

• When developing requirements IASB may need to consider the impact of technology, eg:• Flexibility in order and level of aggregation• Consistent use of terminology, total and subtotals

Electronic format

• Disclosure as a form of communication• See next slide

Communication principles

Communication principles 14

• Seek to promote the disclosure of entity-specific useful information• Result in disclosures that are clear, balanced and understandable• Enable an entity to organise disclosures to highlight important

information• Linked to understand the relationship in the financial statements• Not result in duplication of the same information• Seek to optimise comparability without compromising the

usefulness

15

• Disclosure project in parallel with Conceptual Framework project. Projects inform each other – some overlap

Conceptual Framework

Disclosure Initiative

Materiality

Objective of notes to FS

Communication principles

Form of disclosure requirements

Disclosure Initiative

Questions 16

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

More information

• Discussion Paper http://go.ifrs.org/DP-Conceptual-Framework-July-2013

– Comments to be received by 14 January 2014

• Snapshot http://go.ifrs.org/Snapshot-DP-Conceptual-Framework-2013

• Existing Conceptual Framework http://eifrs.ifrs.org/eifrs/bnstandards/en/2013/conceptualframework.pdf

• Conceptual Framework websitehttp://go.ifrs.org/Conceptual-Framework

17

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

18Other webcasts

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Date Topic Tuesday 3 September 2013 Definitions of assets and liabilities and recognition criteria

Friday 13 September 2013 Profit or loss and other comprehensive income (OCI)

Friday 27 September 2013 Definition of equity and distinction between liability and equity elements

Wednesday 2 October 2013 Measurement

Thursday 10 October 2013 Guidance on liability definition—obligations conditional on entity’s future actions

Tuesday 22 October 2013 Objective and Qualitative CharacteristicsMonday 25 November 2013 Presentation and disclosure