tisa 2007 · pdf file• principle 10: “ a firm must ... – cass 7: client...

TRANSCRIPT

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

1

UK / 73024502.1

Beware of CASS - a briefing on client money & asset rules, lessons from our recent enforcement work and the Lehmans decision

Ash Saluja, Simon Morris and Rita Lowe21 June 2012

UK / 73024502.1

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

2

What we will cover this morning

– CASS in a nutshellCASS in a nutshell

– FSA’s recent approach to CASS

– Issues raised by the Lehman Brothers (LBIE) cases around client money and insolvency

UK / 73024502.1

CASS in a nutshell

UK / 73024502.1

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

3

The foundations of CASS

– Important to understand the basic concepts, most breaches flow from a p p ,misunderstanding on these

– Remember the policy drivers behind CASS

• Aimed at achieving the FSA’s statutory objectives, including market confidence, financial stability and consumer protection

• Protection against insolvency (highlighted by the financial crisis)

– If a firm is holding a customer’s investments or money, it should not treat those investments or money as its own (unless agreed)

– Those investments or money belong to the customer at all times – the firm is just

UK / 73024502.1

safeguarding them

– If the firm becomes insolvent, it should be clear to the administrator which investments/money belong to the firm (and therefore the firm’s creditors) and which investments/money belong to the firm’s clients

– The administrator should be able to return the investments/money belonging to the customers promptly

The regulatory principles underlying CASS

– FSA’s Principles for Businesses, in particular:• Principle 10: “A firm must arrange adequate protection for clients' assets when it is responsible

for them.”

• Principle 3: “A firm must take reasonable care to organise and control its affairs responsibly and effectively, with adequate risk management systems.”

• Principle 6: “A firm must pay due regard to the interests of its customers and treat them fairly.”

– MiFID (investment firms only)• Article 13(7) for client assets: “An investment firm shall, when holding financial instruments

belonging to clients, make adequate arrangements so as to safeguard clients' ownership rights, especially in the event of the investment firm's insolvency, and to prevent the use of a client's instruments on own account except with the client's express consent.”

UK / 73024502.1

• Article 13(8) for client money: “An investment firm shall, when holding funds belonging to clients, make adequate arrangements to safeguard the clients' rights and, except in the case of credit institutions, prevent the use of client funds for its own account.”

– IMD Article 4 for client money (insurance intermediation business):• “Member States shall take all necessary measures to protect customers against the inability of

the insurance intermediary to transfer the premium to the insurance undertaking or to transfer the amount of claim or return premium to the insured.”

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

4

The CASS regimes

– CASS 5: client money rules (general insurance intermediaries)

• Money – protection against insolvency

– CASS 6: custody rules

• Investments – protection against insolvency

– CASS 7: client money rules (investment firms)

• Money – protection against insolvency

– CASS 8: mandate rules

• Money – protection against misuse of authority

– CASS 9: additional rules for prime brokers

UK / 73024502.1

CASS 9: additional rules for prime brokers

• Disclosure and reporting requirements for prime brokers

– In each case, the rules only apply to firms and not to unauthorised persons (e.g. bare trustees, nominees)

The legal fundamentals of client money– Every firm that holds client money is a trustee

• The firm needs to not only know when the rules risk being breached but should also understand• The firm needs to not only know when the rules risk being breached, but should also understand when the firm’s trustee obligations risk being breached (e.g. on transfers of business)

– Why is this so?

• European directives impose harmonised organisational requirements but member states can impose additional measures where these organisational requirements insufficient to safeguard ownership rights

• In the UK, the client money trust provides the ‘legal safety net’ in theory

• The trust takes effect by virtue of the client money rules and can take effect automatically (without a trust deed)

• Insurance brokers can also use a non-statutory trust

– What is a trust?

UK / 73024502.1

• Separation of legal and beneficial ownership of property

• Client money does not ‘belong’ to the firm, it ‘belongs’ to the client

• The firm should not secretly profit from the trust, and the firm’s creditors on insolvency should not profit from the trust

• Client money loses trust protection only in certain circumstances (e.g. CASS 7.2.15R)

• On the firm’s insolvency, client money is only available to creditors once the costs of meeting client claims to the money have been met, and the client claims themselves have been satisfied (CASS 7.7.2R/5.3.2R)

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

5

Risks that the client money rules seek to mitigate

– Misappropriation by the firm (who is required to comply with the rules)pp p y ( q p y )

• But in practice this may be difficult to identify until it is too late (e.g. Lehmans)

– Failure of the bank

• The firm may make good the shortfall if it is liable (failed to exercise duty of care), or if it is willing to do so (CASS 7A.3.2R/CASS 5.6.15R)

• Otherwise, there is a ‘secondary pooling event’

• Generally, any shortfall is borne by all clients of the firm rateably except clients who requested a ‘designated’ account elsewhere

Failure of the firm a primary pooling event

UK / 73024502.1

– Failure of the firm – a primary pooling event

• Notional pooling of all client money held by the firm

• Any shortfall is borne by all clients of the firm rateably

• The administrator will distribute any remaining money accordingly

• This is the intended purpose of the distribution rules, but Lehmans casts into doubt the effectiveness of the rules...

Is it client money?

– Who is holding it (legal title)?Who is holding it (legal title)?

• Is it the client or another person? (CASS 5/7 does not apply to money held by the client, but CASS 8 might apply)

• Is it held by a firm? (CASS only applies to firms)

– Who does the money belong to (equitable rights)?

• Is it a client of the firm?

– For what purpose are they holding it?

UK / 73024502.1

p p y g

• Is it in the course of or in connection with regulated activity?

– Do any exemptions apply?

• E.g. banking institutions, risk transfer arrangements etc.

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

6

Scope of CASS 7 – client money rules

– CASS 7.1.1R application• Must be a firm (which will require permission from FSA)

• That holds money

• Which belongs to a client (can include a group company)

• In relation to investment/MiFID business (not deposits/general insurance)

– CASS 7 can apply in a wide range of circumstances• Money received from client, received from third parties, and due and payable to client from firm

• Money pending investment or pending return to customer (e.g. uncashed cheque)

• Money on transaction accounts with an exchange/clearing house (CASS 7.5)

TPA ( i li hi d )

UK / 73024502.1

• TPA arrangements (outsourcing client money to a third party)

• Interest earned on client money (unless notified to the customer – CASS 7.4.14R)

• CASS 7 might not apply to money that is a cash component of an investment

– Cash component of a SIPP (rights under personal pension plan) – but is it the trustee’s money?

– Cash component of a life policy (rights under contract of insurance) – but is it the insurer’s money?

• CASS 7 might apply to cash component of some ‘wrappers’

– Cash component of an ISA (because an ISA is not an ‘investment’ in itself)

‘Exemptions’ from CASS 7

– Deposit takers (CAS 7.1.8R)

• Generally hold money under a creditor/debtor arrangement (not a trust)

• But they can choose to treat money as client money (and some do when they carry out investment business)

– Life assurers (CASS 7.1.15A)

• Premiums are considered to be ‘invested’ in the policy

– ‘Trustee firms’ have a lighter regime (CASS 7.1.15ER/FR)

– Separate regime for general insurance: CASS 5

– Title transfer collateral arrangements (CASS 7.2.3R)

UK / 73024502.1

• client transfers to a firm full ownership of money or assets for the purpose of securing or covering existing or future obligations

• Cannot be used now for most retail business

• Prime brokers often use in respect of funds from their clients

– Money due and payable to the firm

• Should not be ‘co-mingled’ with client money

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

7

Main requirements of CASS 7(1)

– Segregation of client money into client bank accounts (CASS 7.4.1R)• The bank(s) must be selected carefully and periodically reviewed (CASS 7.4.7R)

• Each client bank account must have an acknowledgement of trust letter confirming that (CASS 7.8.1R):– The money is held by the firm as a trustee

– The bank cannot use it to set off the firm’s debts to the bank

– The title of the account distinguishes it from the firm’s own money

• A client may request a ‘designated client bank account’ with another bank– If that bank fails, only that client will suffer the secondary pooling event

T h i

UK / 73024502.1

– Two approaches to segregation:• Normal approach: client money is paid directly into client bank account

• Alternative approach: client money is mingled with firm’s house money, and transfers are made between house accounts and client accounts on reconciliation

• Can the alternative approach survive post Lehmans?

Main requirements of CASS 7(2)

– Internal reconciliations

• Does what we (think we) have match what we need?

• Frequency must enable a customer’s money to be identified promptly at any time (CASS 7.6.1R) - FSA generally expects daily

• FSA’s standard method of reconciliation (CASS 7 Annex 1)

• If the firm deviates from this method, auditor opinion required (CASS 7.6.8R)

– External reconciliations

• Does what we (think we) have match what the bank says we have?

UK / 73024502.1

• As regularly as is necessary

– Correcting reconciliation discrepancies

• Making good shortfalls where firm is responsible (CASS 7.6.13R)

• Notifying the FSA (7.6.16R)

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

8

Scope of CASS 5

– CASS 5.1.1RCASS 5.1.1R

• Must be a firm (which will require permission from FSA)

• That holds money

• In relation to general insurance mediation

– Generally applies where a broker (or its appointed representative) is holding premiums money, premium refunds and claims money

– ‘Exemptions’ from CASS 7

RICS b d l fi d t i i t

UK / 73024502.1

• RICS members and law firms under certain circumstances

• Reinsurance money (unless the firm elects to comply)

• Insurers, banks, Lloyds managing agents

• Risk transfer arrangements

What is risk transfer?

– What is the ‘risk’?• If the broker becomes insolvent whilst it is holding client money then…

– Risk that the insurer will not receive the premium

– Risk that the insured will not receive the claims money/premium refund

– How is it transferred?• The intermediary is deemed to be holding the money as the insurer’s agent

• This means that the risk of the broker’s insolvency is transferred from the insured to the insurer

– The requirements are at CASS 5.2• Written risk transfer provisions

if i i / l i / i f d ( ll)

UK / 73024502.1

– specifying premiums/claims/premium refund money (any or all)

– specifying extension of risk transfer to agents (e.g. appointed reps, field agents)

– usually built into ‘TOBA’

• Customer disclosure

– BUT risk transfer money can be client money• If it is co-mingled with client money and

• The insurer consents to its interests being subordinated to the interests of other clients

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

9

Statutory and non-statutory trusts under CASS 5

– Brokers have a choice of what type of trust to useBrokers have a choice of what type of trust to use

– The statutory trust arises automatically and does not require a deed

• But will only be effective if money is segregated into client bank accounts

– The non-statutory trust requires a deed

• Money will also be segregated, but there is more flexibility

• Credit can be given to clients or insurers (but debts are held on trust)

• Letter of credit to make good a shortfall can also be held on trust

UK / 73024502.1

• Letter of credit to make good a shortfall can also be held on trust

• Client money may be placed into investments, also held on trust

– Higher capital resources if using a non-statutory trust for retail customers

Scope of CASS 6 – client assets rules

– Applies to firms who provide custody servicespp p y

• Safeguarding and administering investments

• Arranging the safeguarding and administration of investments

– Very limited ‘exemptions’

• ‘Trustee firms’ have a lighter regime (CASS 6.1.16FR)

• Non-MiFID fund managers (CASS 6.1.16BR)

• …but Principle 10 will still apply!

UK / 73024502.1

p pp y

– Recognition that different assets require different treatment in practice

• But overall objective is to minimise risk of insolvency, fraud, poor administration, inadequate record-keeping and negligence (CASS 6.2.2R)

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

10

Main requirements of CASS 6(1)

– Assets must be registered in the name of: (CASS 6.2.3R)• The client

• A nominee company of the firm, an affiliate, exchange or a sub-custodian or

• Another third party/the firm but only if the asset is subject to non-UK law/market practice, it is in the client’s best interests or not feasible to do otherwise, and the client has consented/been notified

– Distinguish between registration (external), and records (internal)

– Typical scenarios:• Traditional custodian: Registration in the name of the customer (owner)

• Platform: Registration in nominee’s name internal records show customer

UK / 73024502.1

Platform: Registration in nominee s name, internal records show customer

• Sub-custody 1: Registration in sub-custodian nominee’s name, sub-custodian’s internal records show the ‘head-custodian’, and the firm’s internal records show the customer

• Sub-custody 2: Registration in name of head-custodian’s customer (if known)

– FSA’s requires firms to take the best available approach (and avoid registering in the firm’s own name if this is possible)

Main requirements of CASS 6(2)

– Using a sub-custodian (CASS 6.3.1R)• Skill care and due diligence in the appointment, and periodic review

• Ensure customer assets are identifiable separately from custodian’s and sub-custodian’s assets

• Keep records as to selection of sub-custodian

– Internal reconciliations• Various methods available (e.g. ‘total count’, ‘rolling stock’)

• Should not be an external reconciliation

• Frequency must enable a customer’s assets to be identified promptly at any time (CASS 6.5.1R)

UK / 73024502.1

)

– External reconciliations• As regularly as is necessary (CASS 6.5.6R)

– Correcting reconciliation discrepancies• Making good shortfalls where firm is responsible (6.5.10R)

• Notifying the FSA (6.5.13R)

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

11

CASS 8 – mandates

– Applies when firms “control” rather than “hold” client money (e.g. bank account is in the name of client, but the firm has authority to give the bank instructions on making payments and transfers)

– CASS 8 sets out high level rules that requires a firm to “establish and maintain adequate records and internal controls in respect of its use of the mandates” including:• an up-to-date list of the authorities and any conditions placed by the client or the

firm's management on the use of them

• a record of all transactions entered into using the authority and internal controls to ensure that they are within the scope of authority of the person and the firm entering into the transaction

UK / 73024502.1

entering into the transaction

• the details of the procedures and authorities for the giving and receiving of instructions under the authority

• where the firm holds a passbook or similar documents belonging to the client, internal controls for the safeguarding (including against loss, unauthorised destruction, theft, fraud or misuse) of any passbook or similar document belonging to the client held by the firm

Beware of CASS – the FSA approach

UK / 73024502.1

Simon Morris

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

12

The FSA agenda

Our supervisory work shows many firms have inadequate recordsOur supervisory work shows many firms have inadequate records, ineffective segregation of client assets and a low level of awareness of the requirements.

In 2012/13 we will further strengthen our intensive regulatory and supervisory approach for firms holding client money and safe custody assets through visits, thematic projects & desk-based reviews, especially using CMAR.

We will continue to take regulatory action where firm failings are

UK / 73024502.1

We will continue to take regulatory action where firm failings are identified.

FSA Business Plan 2012/13

The FSA initiatives

1 Dear CEO letters1. Dear CEO letters

• Senior management required to confirm CASS position

2. CF10a

• A required function to enhance regulatory oversight in med/large firms ->£1m client money/£10m custody assets

3. CMARs

• Specific focused return filed monthly by all CASS 6/7 firms

UK / 73024502.1

p y y

4. CASS resolution pack (from October 2012)

• Information for speedy return of client money & assets on failure.

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

13

The FSA requirements

PRIN 10PRIN 10

A firm must arrange adequate protection for clients’ assets when it is responsible for them.

The elements of adequate protection:

a) Documented procedures

b) Management oversight

UK / 73024502.1

b) Management oversight

c) Regular testing and reporting

d) Segregation and protection

e) Reconciliations

What goes wrong?

– Inadequate senior management oversightInadequate senior management oversight

– Insufficient MI

– Overcomplicated processes

– Operational & systems changes not thought through

– Banks – cannot find letters or show due diligence

– Poor reconciliations

f

UK / 73024502.1

– Poor oversight of outsourced administrators

FSA Client Money & Asset Report (January 2010)

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

14

And recent Enforcement cases confirm ...

a) Failure to segregate => risk of pooling on insolvencya) Failure to segregate > risk of pooling on insolvency

b) Failure to get acknowledgement of trust letter => risk unprotected

c) Failure to maintain records => cannot tell who owns what

d) Failure to reconcile on timely basis => risk of diminution or loss

e) Failure to account for interest received => breach of duty

f) Failure to work through new system => risk of CASS breaches

)

UK / 73024502.1

g) Failure to have adequate procedures => cannot ensure segregate

h) Failure to perform adequate Compliance monitoring

i) Failure to observe client agreement terms on client money

j) Failure by senior management to oversee client money

Protection against CASS breachesStep 1 – gaining fundamental assurance

1. Review

a. Review every cash flow

b. Review your client agreements

c. Review your outsourcings

2. Consider

a. Are you receiving or holding client money?

i. Consider who is your client

UK / 73024502.1

ii. Who owns the debt?

b. Are you right to rely on any exemption?

c. What have you contracted to do?

d. Does this match what you or your outsourcer does?

3. Remedy as needed

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

15

Protection against CASS breachesStep 2 – validating segregation

1 Are you using a bank1. Are you using a bank

a. Over which you have performed proper due diligence?

b. That has agreed to trust status and you have the letter to hand?

2. Cash in

a. Is it wholly separated from your money?

b. Is it promptly banked on receipt?

c Within one business day (normal approach)?

UK / 73024502.1

c. Within one business day (normal approach)?

d. Or have auditors confirmed the alternative approach?

3. Cash out

a. Is it promptly paid out?

b. To client – 3rd party on instructions – 3rd party exchange – duly to firm?

c. Are client entitlements disbursed within 10 days?

Protection against CASS breachesStep 3 – validating the systems and controls

1 Are the procedures clear & comprehensible?1. Are the procedures clear & comprehensible?

a. When were they last reviewed?

b. And when was the last training?

2. Records

a. Is it entirely clear and up-to-date what each client owns?

3. Reconciliations

a Are internal & external promptly performed?

UK / 73024502.1

a. Are internal & external promptly performed?

b. Are there excessive aged balancing items?

c. Are discrepancies promptly rectified?

4. Outsourcings

a. Are they reviewed and overseen?

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

16

Protection against CASS breachesStep 4 – validating governance

1 Does senior management oversee?1. Does senior management oversee?

a. What MI does it get and how is it acted upon?

2. Client agreements

a. Have you checked that you are doing as promised?

3. Change

a. Is CASS compliance embedded in the new product & project checklists?

UK / 73024502.1

4. Risk

a. Is Compliance oversight adequate?

b. When did GIA last review CASS?

Because in the FSA’s view

– CASS rules apply with strict liabilityCASS rules apply with strict liability

– Viewed as a high-profile theme running for several years

– Self-reporting is no defence

– No loss is no defence

– Fine 1% average balance

– And look closely at role of management

UK / 73024502.1

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

17

Client money – Lehmans and the implications for the buy-side

UK / 73024502.1

Rita Lowe

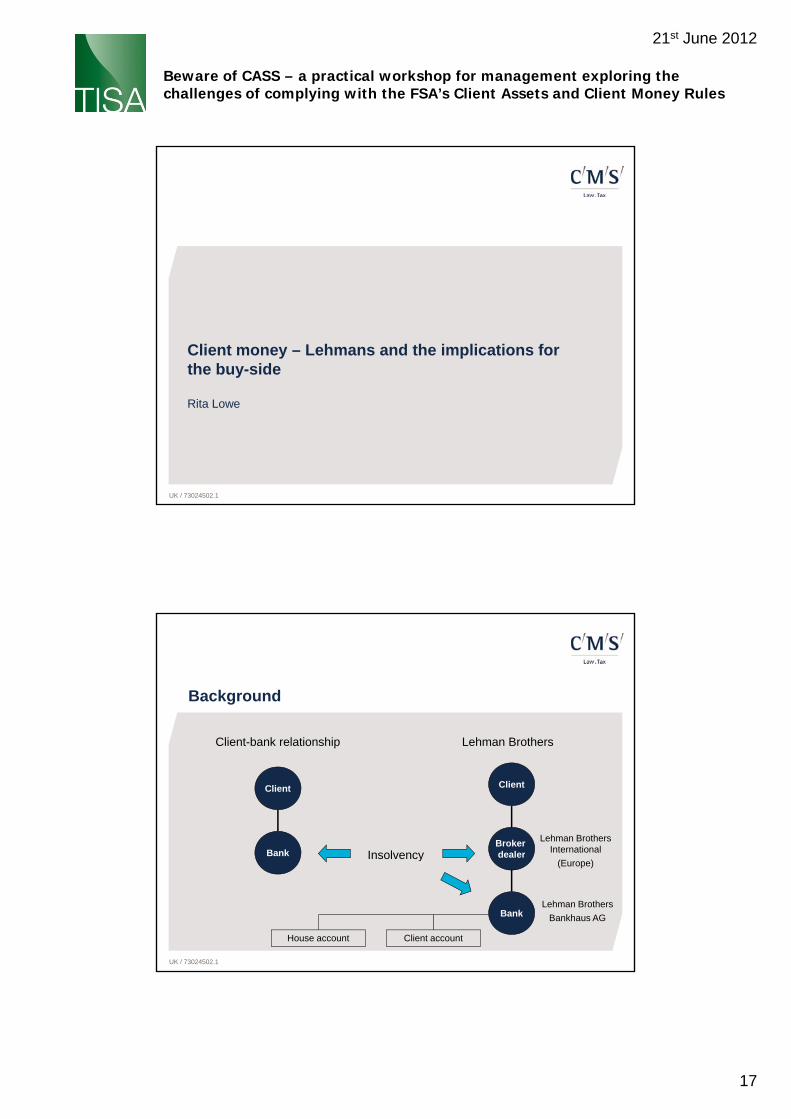

Background

Client

Broker d lBank

Client

Client-bank relationship

I l

Lehman Brothers

Lehman Brothers International

UK / 73024502.1

Bank

dealerBank Insolvency

House account Client account

International

(Europe)

Lehman Brothers

Bankhaus AG

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

18

Background to Lehmans

– LBIE was the primary trading company of Lehmans in Europep y g p y p

• Activities included prime brokerage, investment banking, fixed income/equities dealing and investment management

• Carried out MiFID business and was therefore subject to CASS 7

– LBIE operated the ‘alternative approach’ to segregation

• Client money paid into its house accounts (creating a mixed fund)

• Daily reconciliations between house and segregated accounts

UK / 73024502.1

Daily reconciliations between house and segregated accounts

• Daily transfer from house/segregated accounts to ensure correct amount segregated

• This was permitted, and clients should have adequately protected, except…

So what went wrong?

– Shortfall in amount of client money actually segregatedShortfall in amount of client money actually segregated

• LBIE failed to recognise some counterparties as clients, e.g. it did not treat money belonging to affiliates ($3bn) as client money

• LBIE also failed to operate reconciliation/segregation perfectly

– Client money potentially misappropriated

• LBIE operated a liquidity management process whereby it swept surplus h i h t i ht t US t (i l di th t it

UK / 73024502.1

cash in house accounts every night to US parent (including money that it should have segregated)

– Lehman Brothers Bankhaus AG defaulted (whilst holding $1bn of LBIE client money)

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

19

So what went wrong?

– Primary pooling event meant a further shortfall in client money available for di t ib tidistribution

• At 07.56am on Mon 15 Sept 2008, LBIE went into administration; last segregation took place on Fri, based on Thurs night reconciliation

– There was movement in client balances between the final segregation and the point of administration

There was also movement in client balances after the point of administration

UK / 73024502.1

– There was also movement in client balances after the point of administration

• Some client positions were in the money, some lost money, before being closed

• Currency fluctuations have also had an impact

– Failure to spot or act on any weaknesses

• auditor sign offs provided to FSA

Summary of competing interests

– The client money available is insufficient to repay all clients who were meant to y p ybe protected

• Some clients were un/under segregated, but should not have been:- they claim a share in the client money

• Other clients were treated by LBIE as they should have been:- they wish to keep the client money for themselves

– LBIE has unsecured creditors (non-clients)

UK / 73024502.1

• Unsecured creditors are competing for unsegregated money

– CASS 7 is relatively silent/ambiguous on distribution in these circumstances

• LBIE administrators approached the courts for guidance

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

20

Basics of Supreme Court judgment

CASS 7 requires investment banks:q

– To receive and hold client money as trustee

– To segregate client money in designated bank accounts

– To pool client money and to distribute that client money so that each client receives a sum which is rateable to its client money entitlement

The questions for the court

– Does the trust arise on receipt or segregation?

UK / 73024502.1

Does the trust arise on receipt or segregation?

– Do the primary pooling arrangements apply to client money in house accounts or just in the designated accounts?

– Is participation in the client money pool dependent upon segregation of client monies?

Result and Implications of Lehmans

The result

– The statutory trust applies on receipt

– The pooling arrangements apply to any identifiable client money (even if not segregated)

– The money pooled, or treated as pooled, should be grouped and distributed to clients (pro rata to their entitlements), irrespective of whether such monies were segregated for them

The implications

UK / 73024502.1

– Immediately before pooling, segregated client money belonged to the clients for whom the money had been segregated. However, on pooling, clients with segregated client money have to share their segregated money with clients who merely had a contractual entitlement to client money

– Will market rumours, therefore, cause speedier and more damaging runs on client assets?

– Scotland?

Beware of CASS – a practical workshop for management exploring the challenges of complying with the FSA’s Client Assets and Client Money Rules

21st June 2012

21

Actions for clients

– Review contractual arrangements, e.g. to understand the status of money held (title g , g y (transfer arrangements remove the protection of CASS/client money regime)

– Assurance re auditing and systems of broker-dealer client money, and insolvency risk of the bank at which broker-dealer has its client money accounts

– Is broker-dealer using the “normal approach” for holding client money?

UK / 73024502.1

– Ensure that no excess cash is kept with the broker-dealer

– Alternative structures for lawyers to think about? E.g. client money to be held by the bank in separate account either: (i) for the client with the broker-dealer having a mandate under CASS 8, or (ii) for the broker-deal but subject to non-statutory trust in favour of client

The future

– Broker may maintain a buffer to cover client money exposurey y p

– Special purpose bankruptcy remote structure

– Wait and see for new FSA/FCA guidance and rules/ government legislation on CASS, reporting, auditing, and other changes (including, potentially, client preference)

UK / 73024502.1