time value of money - john wiley & · pdf file1052 appendix b appendix b time value of...

TRANSCRIPT

1052 Appendix B

appendix B

Time valueof money

Would you rather receive $1000 today or a year from now? You should prefer to receivethe $1000 today because you can invest the $1000 and earn interest on it. As a result,you will have more than $1000 a year from now. What this example illustrates is theconcept of the time value of money. Everyone prefers to receive money today ratherthan in the future because of the interest factor.

NATURE OF INTERESTInterest is payment for the use of another person’s money. It is the difference betweenthe amount borrowed or invested (called the principal) and the amount repaid or col-lected. The amount of interest to be paid or collected is usually stated as a rate over aspecific period of time. The rate of interest is generally stated as an annual rate.

The amount of interest involved in any financing transaction is based on three elements:1. Principal (p): the original amount borrowed or invested.2. Interest rate (i): an annual percentage of the principal.3. Time (n): the number of years that the principal is borrowed or invested.

SIMPLE INTERESTSimple interest is calculated on the principal amount only. It is the return on theprincipal for one period. Simple interest is usually expressed as shown in figure B.1.

After studying this appendix, you should be able to:

1 Distinguish between simple and compound interest.

2 Solve for future value of a single amount.

3 Solve for future value of an annuity.

4 Identify the variables fundamental to solving presentvalue problems.

5 Solve for present value of a single amount.

6 Solve for present value of an annuity.

7 Calculate the present values in capital budgeting situations.

L E A R N I N G O B J E C T I V E S

LEARNING OBJECT IVE

Distinguish between simple and compound interest.

1

InterestPrincipal

p

Rate

i

Time

n××=

For example, if you borrowed $5000 for 2 years at a simple interest rate of 12%

annually, you would pay $1200 in total interest calculated as follows:

Interest= p × i × n

= $5000 × 0.12 × 2

= $1200Figure B.1 Interest

calculation

Appendix B 1053

COMPOUND INTERESTCompound interest is calculated on principal and on any interest earned that has notbeen paid or withdrawn. It is the return on (or growth of) the principal for two or moretime periods. Compounding calculates interest not only on the principal but also on theinterest earned to date on that principal, assuming the interest is left on deposit.

To illustrate the difference between simple and compound interest, assume that youdeposit $1000 in Bank One, where it will earn simple interest of 9% per year, and youdeposit another $1000 in CityCorp, where it will earn compound interest of 9% per yearcompounded annually. Also assume that in both cases you will not withdraw anyinterest until 3 years from the date of deposit. The calculation of interest to be receivedand the accumulated year-end balances are indicated in figure B.2.

Note in figure B.2 that simple interest uses the initial principal of $1000 to calculatethe interest in all 3 years. Compound interest uses the accumulated balance (principalplus interest to date) at each year-end to calculate interest in the succeeding year —which explains why your compound interest account is larger.

Obviously, if you had a choice between investing your money at simple interest or atcompound interest, you would choose compound interest, all other things — especiallyrisk — being equal. In the example, compounding provides $25.03 of additional interestrevenue. For practical purposes, compounding assumes that unpaid interest earnedbecomes a part of the principal, and the accumulated balance at the end of each yearbecomes the new principal on which interest is earned during the next year.

As can be seen in figure B.2, you should invest your money at CityCorp, which com-pounds interest annually. Compound interest is used in most business situations. Simpleinterest is generally applicable only to short-term situations of 1 year or less.

FUTURE VALUE CONCEPTSFUTURE VALUE OF A SINGLE AMOUNTThe future value of a single amount is the value at a future date of a given amountinvested assuming compound interest. For example, in figure B.2, $1295.03 is the futurevalue of the $1000 at the end of 3 years. The $1295.03 could be determined more easilyby using the following formula:

FV = p × (1 + i )n

where:FV = future value of a single amount

p = principal (or present value)i = interest rate for one period

n = number of periods

Simple interestcalculation

Year 1

Year 2

Year 3

$1000.00 × 9%

$1000.00 × 9%

$1000.00 × 9%

$

$

90.00

90.00

90.00

270.00

$1090.00

$1180.00

$1270.00

$25.03Difference

Simpleinterest

Accumulatedyear-endbalance

Bank One

Compound interestcalculation

Year 1

Year 2

Year 3

$1000.00 × 9%

$1090.00 × 9%

$1188.10 × 9%

$

$

90.00

98.10

106.93

295.03

$1090.00

$1188.10

$1295.03

Compoundinterest

Accumulatedyear-endbalance

City Corp

Figure B.2 Simple vs. compound interest

LEARNING OBJECT IVE

Solve for future value of a single amount.

2

1054 Appendix B

The $1295.03 is calculated as follows:

FV = p × (1 + i )n

= $1000 × (1 + i )3

= $1000 × 1.29503 = $1295.03

The 1.29503 is calculated by multiplying (1.09 × 1.09 × 1.09). The amounts in thisexample can be depicted in the time diagram in figure B.3.

Another method that may be used to calculate the future value of a single amountinvolves the use of a compound interest table, which shows the future value of 1 forn periods. Table 1, shown below, is such a table.

In table 1, n is the number of compounding periods, the percentages are the periodicinterest rates, and the 6-digit decimal numbers in the respective columns are the futurevalue of 1 factors. In using table 1, the principal amount is multiplied by the futurevalue factor for the specified number of periods and interest rate. For example, thefuture value factor for 2 periods at 9% is 1.18810. Multiplying this factor by $1000 equals

TABLE 1 Future value of 1

(n)

Periods 4% 5% 6% 8% 9% 10% 11% 12% 15%

1 2 3 4 5

1.040001.081601.124861.169861.21665

1.050001.102501.157631.215511.27628

1.060001.123601.191021.262481.33823

1.080001.166401.259711.360491.46933

1.090001.188101.295031.411581.53862

1.100001.210001.331001.464101.61051

1.110001.232101.367631.518071.68506

1.120001.254401.404931.573521.76234

1.150001.322501.520881.749012.01136

6 7 8 910

1.265321.315931.368571.423311.48024

1.340101.407101.477461.551331.62889

1.418521.503631.593851.689481.79085

1.586871.713821.850931.999002.15892

1.677101.828041.992562.171892.36736

1.771561.948722.143592.357952.59374

1.870412.076162.304542.558032.83942

1.973822.210682.475962.773083.10585

2.313062.660023.059023.517884.04556

1112131415

1.539451.601031.665071.731681.80094

1.710341.795861.885651.979932.07893

1.898302.012202.132932.260902.39656

2.331642.518172.719622.937193.17217

2.580432.812673.065813.341733.64248

2.853123.138433.452273.797504.17725

3.151763.498453.883284.310444.78459

3.478553.895984.363494.887115.47357

4.652395.350256.152797.075718.13706

1617181920

1.872981.947902.025822.106852.19112

2.182872.292022.406622.526952.65330

2.540352.692772.854343.025603.20714

3.425943.700023.996024.315704.66096

3.970314.327634.717125.141665.60441

4.594975.054475.559926.115916.72750

5.310895.895096.543557.263348.06231

6.130396.866047.689978.612769.64629

9.3576210.7612612.3754514.2317716.36654

Present value (p)

0$1000

1 2 3$1295.03

i = 9% Futurevalue

n = 3 years

Figure B.3 Time diagram

Appendix B 1055

$1188.10, which is the accumulated balance at the end of year 2 in the CityCorpexample in figure B.2. The $1295.03 accumulated balance at the end of the third yearcan be calculated from table 1 by multiplying the future value factor for 3 periods(1.29503) by the $1000.

The demonstration problem in figure B.4 illustrates how to use table 1.

FUTURE VALUE OF AN ANNUITYThe preceding discussion involved the accumulation of only a single principal sum.Individuals and entities often encounter situations in which a series of equal dollaramounts are to be paid or received periodically, such as loans or lease (rental) con-tracts. Such payments or receipts of equal dollar amounts are referred to as annuities.The future value of an annuity is the sum of all the payments (receipts) plus theaccumulated compound interest on them. In calculating the future value of an annuity,it is necessary to know (1) the interest rate, (2) the number of compounding periods,and (3) the amount of the periodic payments or receipts.

To illustrate the calculation of the future value of an annuity, assume that you invest$2000 at the end of each year for 3 years at 5% interest compounded annually. Thissituation is depicted in the time diagram in figure B.5.

As can be seen in figure B.5, the $2000 invested at the end of year 1 will earn interestfor 2 years (years 2 and 3) and the $2000 invested at the end of year 2 will earn interest

0$20 000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18

i = 6%Future

value = ?Present value (p)

n = 18 years

John and Mary Rich invested $20 000 in a savings account paying 6% interest at the time their son,Matt, was born. On his 18th birthday, Matt withdraws the money from his savings account. How much did Matt withdraw from his account?

Answer: The future value factor from table 1 is 2.85434 (18 periods at 6%). The future value of$20 000 earning 6% per year for 18 years is $57 086.80 ($20 000 × 2.85434).

Figure B.4 Demonstration problem — using table 1 forFV of 1

LEARNING OBJECT IVE

Solve for future value of an annuity.

3

0 1 2 3

$2000Presentvalue $2000 $2000

i = 5% Futurevalue = ?

n = 3 years

Figure B.5 Time diagram for a 3-year annuity

1056 Appendix B

for 1 year (year 3). However, the last $2000 investment (made at the end of year 3) willnot earn any interest. The future value of these periodic payments could be calculatedusing the future value factors from table 1 as shown in figure B.6.

The first $2000 investment is multiplied by the future value factor for 2 periods (1.1025)because 2 years interest will accumulate on it (in years 2 and 3). The second $2000investment will earn only 1 year’s interest (in year 3) and therefore is multiplied by thefuture value factor for 1 year (1.0500). The final $2000 investment is made at the end ofthe third year and will not earn any interest. Consequently, the future value of the last$2000 invested is only $2000 since it does not accumulate any interest.

This method of calculation is required when the periodic payments or receipts are notequal in each period. However, when the periodic payments (receipts) are the same ineach period, the future value can be calculated by using a future value of an annuity of1 table. Table 2, shown below, is such a table.

Table 2 shows the future value of 1 to be received periodically for a given number ofperiods. From table 2 it can be seen that the future value of an annuity of 1 factor for3 periods at 5% is 3.15250. The future value factor is the total of the three individualfuture value factors as shown in figure B.6. Multiplying this amount by the annualinvestment of $2000 produces a future value of $6305.

Year

invested

Amount

invested ×

Future value of

1 factor at 5%

Future

value

123

$2000$2000$2000

×

×

×

1.10250

1.05000

1.00000

$ 2205

2100

2000

3.15250 $6305

TABLE 2 Future value of an annuity of 1

(n)

Periods 4% 5% 6% 8% 9% 10% 11% 12% 15%

1 2 3 4 5

1.00000 2.04000 3.12160 4.24646 5.41632

1.00000 2.05000 3.15250 4.31013 5.52563

1.00000 2.06000 3.18360 4.37462 5.63709

1.00000 2.08000 3.24640 4.50611 5.86660

1.00000 2.09000 3.27810 4.57313 5.98471

1.00000 2.10000 3.31000 4.64100 6.10510

1.00000 2.11000 3.34210 4.70973 6.22780

1.00000 2.12000 3.37440 4.77933 6.35285

1.00000 2.15000 3.47250 4.99338 6.74238

6 7 8 910

6.63298 7.89829 9.2142310.5828012.00611

6.80191 8.14201 9.5491111.0265612.57789

6.97532 8.39384 9.8974711.4913213.18079

7.33592 8.9228010.6366312.4875614.48656

7.52334 9.2004411.0284713.0210415.19293

7.71561 9.4871711.4358913.5798415.93743

7.91286 9.7832711.8594314.1639716.72201

8.1151910.0890112.2996914.7756617.54874

8.75374 11.06680 13.72682 16.78584 20.30372

1112131415

13.4863515.0258116.6268418.2919120.02359

14.2067915.9171317.7129819.5986321.57856

14.9716416.8699418.8821421.0150723.27597

16.6454918.9771321.4953024.2149227.15211

17.5602920.1407222.9533926.0191929.36092

18.5311721.3842824.5227127.9749831.77248

19.5614322.7131926.2116430.0949234.40536

20.6545824.1331328.0291132.3926037.27972

24.34928 29.00167 34.35192 40.50471 47.58041

1617181920

21.8245323.6975125.6454127.6712329.77808

23.6574925.8403728.1323830.5390033.06595

25.6725328.2128830.9056533.7599936.78559

30.3242833.7502337.4502441.4462645.76196

33.0034036.9735141.3013446.0184651.16012

35.9497340.5447045.5991751.1590957.27500

39.1899544.5008450.3959356.9394964.20283

42.7532848.8836755.7497263.4396872.05244

55.71747 65.07509 75.83636 88.21181102.44358

Figure B.6 Future value ofperiodic payments

Appendix B 1057

The demonstration problem in figure B.7 illustrates how to use table 2.

PRESENT VALUE CONCEPTSPRESENT VALUE VARIABLESThe present value, like the future value, is based on three variables: (1) the dollaramount to be received (future amount), (2) the length of time until the amount isreceived (number of periods), and (3) the interest rate (the discount rate). Theprocess of determining the present value is referred to as discounting the futureamount.

In this book, present value calculations are used in measuring several items. Forexample, capital budgeting and other investment proposals are evaluated using presentvalue calculations. All rate of return and internal rate of return calculations involve pre-sent value techniques.

PRESENT VALUE OF A SINGLE AMOUNTTo illustrate present value concepts, assume that you are willing to invest a sum ofmoney that will yield $1000 at the end of 1 year. In other words, what amount wouldyou need to invest today to have $1000 in a year from now? If you want a 10% rate ofreturn, the investment or present value is $909.09 ($1000 ÷ 1.10). The calculation of thisamount is shown in figure B.8.

The future amount ($1000), the discount rate (10%), and the number of periods (1)are known. The variables in this situation can be depicted in the time diagram infigure B.9.

Present value

PV

PV

PV

=

=

=

=

Future value ÷ (1 + i )n

FV ÷ (1 + 10%)1

$1000 ÷ 1.10

$909.09

0 1 2 3 4

$25 000Presentvalue $25 000 $25 000 $25 000

i = 6% Futurevalue = ?

n = 4 years

Answer: The future value factor from table 2 is 4.37462 (four periods at 6%). The future value of$25 000 invested at the end of each year for 4 years at 6% interest is $109 365.50 ($25 000 × 4.37462).

Henning Printing knows that in 4 years it must replace one of its existing printing presses with a new one. To ensure that some funds are available to replace the machine in 4 years, the business is depositing $25 000 in a savings account at the end of each of the next 4 years (four deposits in total). The savings account will earn 6% interest compounded annually. How much will be in the savings account at the end of 4 years when the new printing press is to be purchased?

Figure B.7 Demonstration problem — using table 2 for FV of an annuity of 1

LEARNING OBJECT IVE

Identify the variables fundamental to solving present value problems.

4

LEARNING OBJECT IVE

Solve for present valueof a single amount.

5

Figure B.8 Present value calculation — $1000 discounted at 10% for1 year

1058 Appendix B

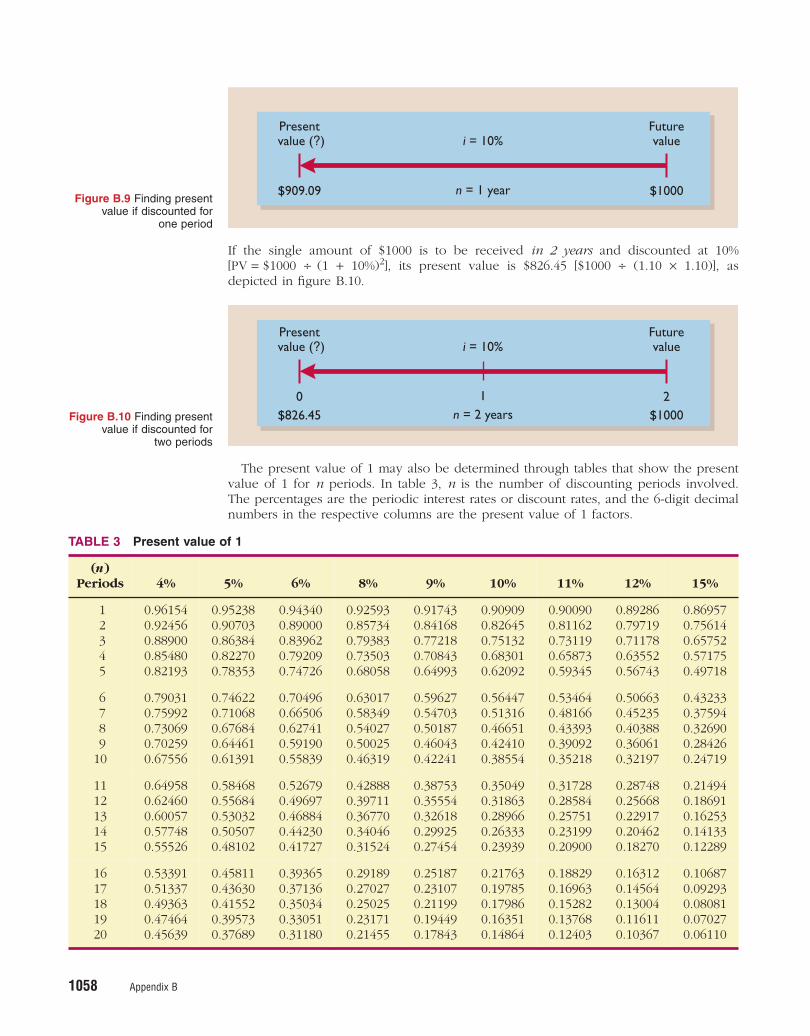

If the single amount of $1000 is to be received in 2 years and discounted at 10%[PV = $1000 ÷ (1 + 10%)2], its present value is $826.45 [$1000 ÷ (1.10 × 1.10)], asdepicted in figure B.10.

The present value of 1 may also be determined through tables that show the presentvalue of 1 for n periods. In table 3, n is the number of discounting periods involved.The percentages are the periodic interest rates or discount rates, and the 6-digit decimalnumbers in the respective columns are the present value of 1 factors.

TABLE 3 Present value of 1

(n)

Periods 4% 5% 6% 8% 9% 10% 11% 12% 15%

1 2 3 4 5

0.961540.924560.889000.854800.82193

0.952380.907030.863840.822700.78353

0.943400.890000.839620.792090.74726

0.925930.857340.793830.735030.68058

0.917430.841680.772180.708430.64993

0.909090.826450.751320.683010.62092

0.900900.811620.731190.658730.59345

0.892860.797190.711780.635520.56743

0.869570.756140.657520.571750.49718

6 7 8 910

0.790310.759920.730690.702590.67556

0.746220.710680.676840.644610.61391

0.704960.665060.627410.591900.55839

0.630170.583490.540270.500250.46319

0.596270.547030.501870.460430.42241

0.564470.513160.466510.424100.38554

0.534640.481660.433930.390920.35218

0.506630.452350.403880.360610.32197

0.432330.375940.326900.284260.24719

1112131415

0.649580.624600.600570.577480.55526

0.584680.556840.530320.505070.48102

0.526790.496970.468840.442300.41727

0.428880.397110.367700.340460.31524

0.387530.355540.326180.299250.27454

0.350490.318630.289660.263330.23939

0.317280.285840.257510.231990.20900

0.287480.256680.229170.204620.18270

0.214940.186910.162530.141330.12289

1617181920

0.533910.513370.493630.474640.45639

0.458110.436300.415520.395730.37689

0.393650.371360.350340.330510.31180

0.291890.270270.250250.231710.21455

0.251870.231070.211990.194490.17843

0.217630.197850.179860.163510.14864

0.188290.169630.152820.137680.12403

0.163120.145640.130040.116110.10367

0.106870.092930.080810.070270.06110

i = 10%

n = 1 year

Present value (?)

$909.09

Futurevalue

$1000Figure B.9 Finding present

value if discounted forone period

i = 10%

1

Present value (?)

0

Futurevalue

2

n = 2 years$826.45 $1000Figure B.10 Finding presentvalue if discounted for

two periods

Appendix B 1059

When table 3 is used, the future value is multiplied by the present value factor speci-fied at the intersection of the number of periods and the discount rate. For example, thepresent value factor for 1 period at a discount rate of 10% is 0.90909, which equals the$909.09 ($1000 × 0.90909) calculated in figure B.8. For 2 periods at a discount rate of10%, the present value factor is 0.82645, which equals the $826.45 ($1000 × 0.82645)calculated previously.

Note that a higher discount rate produces a smaller present value. For example, usinga 15% discount rate, the present value of $1000 due 1 year from now is $869.57 versus$909.09 at 10%. It should also be recognised that the further removed from the presentthe future value is, the smaller the present value. For example, using the same discountrate of 10%, the present value of $1000 due in 5 years is $620.92 versus $1000 due in1 year is $909.09.

The following demonstration problem (figure B.11) illustrates how to use table 3.

PRESENT VALUE OF AN ANNUITYThe preceding discussion involved the discounting of only a single future amount.Entities and individuals often engage in transactions in which a series of equal dollaramounts are to be received or paid periodically. Examples of a series of periodicreceipts or payments are loan agreements, instalment sales, notes, lease (rental) con-tracts, and pension obligations. These series of periodic receipts or payments arecalled annuities. In calculating the present value of an annuity, it is necessary toknow (1) the discount rate, (2) the number of discount periods, and (3) the amount ofthe periodic receipts or payments. To illustrate the calculation of the present value ofan annuity, assume that you will receive $1000 cash annually for 3 years at a timewhen the discount rate is 10%. This situation is depicted in the time diagram infigure B.12.

i = 9%

3

PV = ?

Now

$5 000 000

4 years1

Answer: The present value factor from table 3 is 0.70843 (4 periods at 9%). Thus, Metal Fabricators Ltd would need to deposit $3 542 150($5 000 000 × 0.70843) at 9% now in order to receive $5 000 000 in 4 years’ time.

2n = 4

Determine the amount Metal Fabricators Ltd must deposit now in its savings account, paying 9% interest, in order to accumulate $5 000 000in 4 years’ time for an addition to its factory.

Figure B.11 Demonstration problem — using table 3 for PV of 1

LEARNING OBJECT IVE

Solve for present value of an annuity.

6

i = 10%

2Now 3 years

PV = ? $1000 $1000$1000

1n = 3

Figure B.12 Time diagram for a 3-year annuity

1060 Appendix B

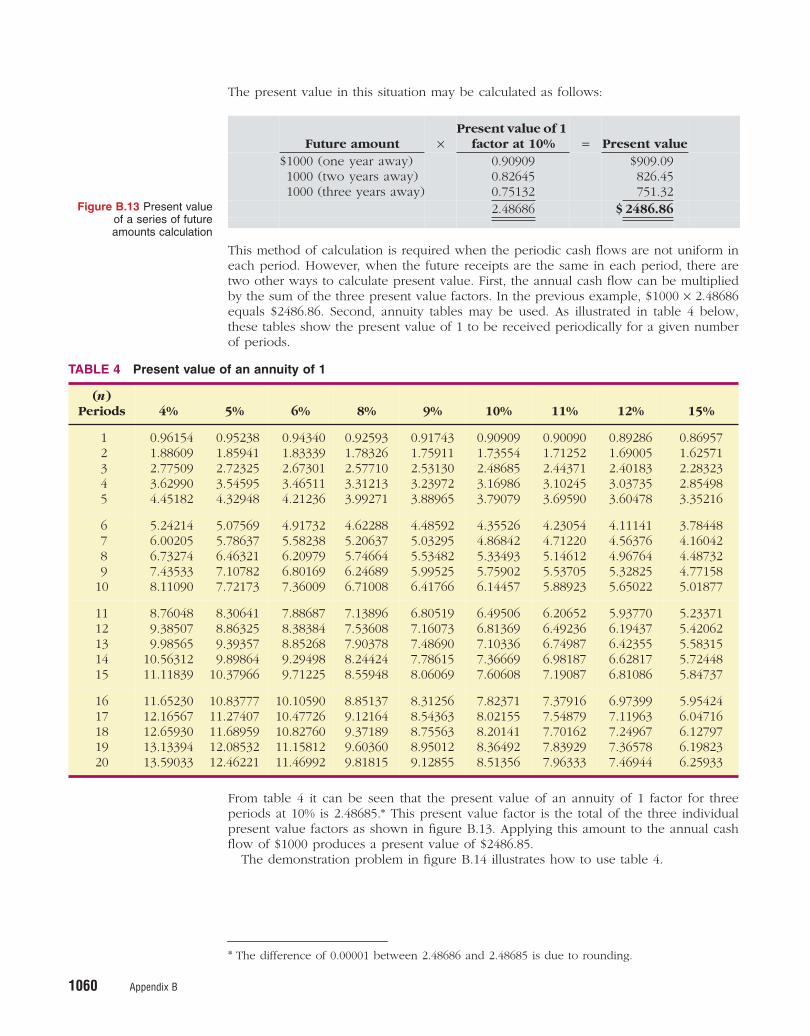

The present value in this situation may be calculated as follows:

This method of calculation is required when the periodic cash flows are not uniform ineach period. However, when the future receipts are the same in each period, there aretwo other ways to calculate present value. First, the annual cash flow can be multipliedby the sum of the three present value factors. In the previous example, $1000 × 2.48686equals $2486.86. Second, annuity tables may be used. As illustrated in table 4 below,these tables show the present value of 1 to be received periodically for a given numberof periods.

From table 4 it can be seen that the present value of an annuity of 1 factor for threeperiods at 10% is 2.48685.* This present value factor is the total of the three individualpresent value factors as shown in figure B.13. Applying this amount to the annual cashflow of $1000 produces a present value of $2486.85.

The demonstration problem in figure B.14 illustrates how to use table 4.

Future amount ×

Present value of 1

factor at 10% = Present value

$1000 (one year away)1000 (two years away)1000 (three years away)

0.909090.826450.75132

$909.09826.45751.32

2.48686 $ 2486.86

TABLE 4 Present value of an annuity of 1

(n)

Periods 4% 5% 6% 8% 9% 10% 11% 12% 15%

1 2 3 4 5

0.961541.886092.775093.629904.45182

0.952381.859412.723253.545954.32948

0.943401.833392.673013.465114.21236

0.925931.783262.577103.312133.99271

0.917431.759112.531303.239723.88965

0.909091.735542.486853.169863.79079

0.900901.712522.443713.102453.69590

0.892861.690052.401833.037353.60478

0.869571.625712.283232.854983.35216

6 7 8 910

5.242146.002056.732747.435338.11090

5.075695.786376.463217.107827.72173

4.917325.582386.209796.801697.36009

4.622885.206375.746646.246896.71008

4.485925.032955.534825.995256.41766

4.355264.868425.334935.759026.14457

4.230544.712205.146125.537055.88923

4.111414.563764.967645.328255.65022

3.784484.160424.487324.771585.01877

1112131415

8.760489.385079.98565

10.5631211.11839

8.306418.863259.393579.89864

10.37966

7.886878.383848.852689.294989.71225

7.138967.536087.903788.244248.55948

6.805197.160737.486907.786158.06069

6.495066.813697.103367.366697.60608

6.206526.492366.749876.981877.19087

5.937706.194376.423556.628176.81086

5.233715.420625.583155.724485.84737

1617181920

11.6523012.1656712.6593013.1339413.59033

10.8377711.2740711.6895912.0853212.46221

10.1059010.4772610.8276011.1581211.46992

8.851379.121649.371899.603609.81815

8.312568.543638.755638.950129.12855

7.823718.021558.201418.364928.51356

7.379167.548797.701627.839297.96333

6.973997.119637.249677.365787.46944

5.954246.047166.127976.198236.25933

* The difference of 0.00001 between 2.48686 and 2.48685 is due to rounding.

Figure B.13 Present value

of a series of future

amounts calculation

Appendix B 1061

TIME PERIODS AND DISCOUNTINGIn the preceding calculations, the discounting has been done on an annual basis usingan annual interest rate. Discounting may also be done over shorter periods of time suchas monthly, quarterly or half-yearly. When the time frame is less than 1 year, it is necess-ary to convert the annual interest rate to the applicable time frame. Assume, forexample, that the investor in figure B.13 received $500 every 6 months for 3 yearsinstead of $1000 annually. In this case, the number of periods becomes 6 (3 × 2), thediscount rate is 5% (10% ÷ 2), the present value factor from table 4 is 5.07569, and thepresent value of the future cash flows is $2537.85 (5.07569 × $500). This amount isslightly higher than the $2486.86 calculated in figure B.13 because interest is calculatedtwice during the same year; therefore interest is earned on the first 6 months’ interest.

CALCULATING THE PRESENT VALUES IN A CAPITAL BUDGETING DECISIONThe decision to make long-term capital investments is best evaluated using discountingtechniques that recognise the time value of money, i.e the present value of the cashflows involved in a capital investment. The evaluation must reduce all cash inflows andoutflows to a common comparable amount. That can be accomplished by either futurevaluing to some future date all the cash flows, or present valuing (discounting) to thepresent date all cash flows. Although both are useful for evaluating the investment, thepresent value (discounting) technique is more appealing and universally used.

Nagel Ltd is considering adding another truck to its fleet because of a purchasingopportunity. Navistar Ltd, Nagel Ltd’s main supplier of trucks, is overstocked and offersto sell its biggest truck for $154 000 cash payable on delivery. Nagel Ltd knows that thetruck will produce a net cash flow per year of $40 000 for 5 years (received at the endof each year), at which time it will be sold for an estimated residual value of $35 000.Nagel Ltd’s discount rate in evaluating capital expenditures is 10%. Should Nagel Ltdcommit to the purchase of this truck?

The cash flows that must be discounted to present value by Nagel Ltd are as follows:

Cash payable on delivery (now): $154 000.Net cash flow from operating the rig: $40 000 for 5 years (at the end of each year).Cash received from sale of truck at the end of 5 years: $35 000.

The time diagrams for the latter two cash flows are shown in figure B.15.

i = 12%

4

PV = ?

Now

$6000

5 years1

$6000 $6000

2 3

$6000 $6000

n = 5

Steel Products Ltd has just signed an agreement to purchase equipment for instalment payments of $6000 each, to be paid at the end of each of the next 5 years. In setting the amount of the payments, the seller used a discount rate of 12%. What is the present value of the instalment payments — i.e. how much is Steel Products Ltd paying for the equipment and how much is it paying in total interest over the term of the instalment contract?

Answer: The present value factor from table 4 is 3.60478 (5 periods at 12%). The present value of 5 payments of $6000 each discounted at 12% is $21 628.6 8 ($6000 × 3.60478). Therefore, the cost of the equipment to Steel Products Ltd is $21 628.68 and the interest is $8371.32 [($6000 × 5) – $21 628.68]. Figure B.14 Demonstration

problem — using table 4 for PV of an annuity of 1

LEARNING OBJECT IVE

Calculate the present values in capital budgeting situations.

7

1062 Appendix B

Note from the diagrams that calculating the present value of the net operating cash flows($40 000 at the end of each year) is discounting an annuity (table 4) whereas calculatingthe present value of the $35 000 residual value is discounting a single sum (table 3).

The calculation of these present values is shown in figure B.16.

Because the present value of the cash receipts (inflows) of $173 363.80($151 631.60 + $21 732.20) exceeds the present value of the cash payments (outflows) of$154 000.00, the net present value of $19 363.80 is positive and the decision to investshould be accepted.

Now assume that Nagel Ltd uses a discount rate of 15% not 10% because it wants agreater return on its investments in capital assets. The cash receipts and cash paymentsby Nagel Ltd are the same. The present values of these receipts and cash payments dis-counted at 15% are shown in figure B.17.

Present values using a 10% discount rate

Present value of net operating cash flows received annually over 5 years:$40 000 × PV of 1 received annually for 5 years at 10%$40 000 × 3.79079

Present value of residual value (cash) to be received in 5 years:$35 000 × PV of 1 received in 5 years at 10%$35 000 × 0.62092

$151 631.60

21 732.20

Present value of cash inflows

Present value of cash outflows (purchase price due now at 10%):$154 000 × PV of 1 due now$154 000 × 1.00000

173 363.80

154 000.00

Net present value $ 19 363.80

Present values using a 10% discount rate

Present value of net operating cash flows received annuallyover 5 years at 15%:

$40 000 × 3.35216

Present value of residual value (cash) to be received in 5 years at 15%:$35 000 × 0.49718

$134 086.40

17 401.30

Present value of cash inflows

Present value of cash outflows (purchase price due now at 15%):$154 000 × 1.00000

151 487.70

154 000.00

Net present value $ (2 512.30)

i = 10%

1

Presentvalue

?

Now

Net operatingcash flows

5 year

Diagram fornet operating

cash flows

2

$40 000 $40 000 $40 000 $40 000 $40 000

3 4n = 5

i = 10%

1

Presentvalue

?

Now

Cash fromsale

5 year

Diagram forresidualvalue

2

$35 000

3 4n = 5

Figure B.15 Time diagramsfor Nagel Ltd

Figure B.16 Present valuecalculations at 10%

Figure B.17 Present valuecalculations at 15%

Appendix B 1063

Because the present value of the cash payments (outflows) of $154 000 exceeds thepresent value of the cash receipts (inflows) of $151 487.70 ($134 086.40 + $17 401.30),the net present value of $2512.30 is negative and the investment should be rejected.

The above discussion relied on present value tables in solving present value prob-lems. Electronic handheld calculators may also be used to calculate present valueswithout the use of these tables. Some calculators have present value (PV) functions thatallow you to calculate present values by merely identifying the proper amount, discountrate and periods, then pressing the PV key.

SUMMARY OF LEARNING OBJECTIVES1 Distinguish between simple and compound interest. Simple interest is calculated on the principal only whereas compound interest is calculated on the principal and any interest earned that has not been withdrawn.

2 Solve for future value of a single amount. Prepare a time diagram of the problem. Identify the principal amount, the number of compounding periods, and the interest rate. Using the future value of 1 table, multiply the principal amount by the future value factor specified at the intersection of the number of periods and the interest rate.

3 Solve for future value of an annuity. Prepare a time diagram of the problem. Identify the amount of the periodic payments, the number of compounding periods, and the interest rate. Using the future value of an annuity of 1 table, multiply the amount of the payments by the future value factor specified at the intersection of the number of periods and the interest rate.

4 Identify the variables fundamental to solving present value problems. The following three variables are fundamental to solving present value problems:(1) the future amount, (2) the number of periods, and (3) the interest rate (the discount rate).

5 Solve for present value of a single amount. Prepare a time diagram of the problem. Identify the future amount, the number of discounting periods, and the discount (interest) rate. Using the present value of1 table, multiply the future amount by the present value factor specified at the intersection of the number of periods and the discount rate.

6 Solve for present value of an annuity. Prepare a time diagram of the problem. Identify the future amounts (annuities), the number of discounting periods, and the discount (interest) rate. Using the present value of an annuity of 1 table, multiply the amount of the annuity by the present value factor specified at the intersection of the number of periods and the interest rate.

7 Calculate the present values in capital budgeting situations. Calculate the present values of all cash inflows and all cash outflows related to the capital budgeting proposal (an investment-type decision). If the net present value is positive, accept the proposal (make the investment). If the net present value is negative, reject the proposal (do not make the investment).

GLOSSARYAnnuity A series of equal dollar amounts to be paid or received periodically (p. 1055).

Compound interest The interest calculated on the principal and any interest earned that has not been paid or received (p. 1053).

Discounting the future amount(s) The process of determining present value (p. 1057).

Future value of a single amount The value at a future date of a given amount invested assuming compound interest (p. 1053).

Future value of an annuity The sum of all the payments or receipts plus the accumulated compound interest on them (p. 1055).

Interest Payment for the use of another’s money (p. 1052).

Present value The value now of a given amount to be invested or received in the future assuming compound interest (p. 1057).

Present value of an annuity A series of future receipts or payments discounted to their value now assuming compound interest (p. 1059).

Principal The amount borrowed or invested(p. 1052).

Simple interest The interest calculated on the principal only (p. 1052).

1064 Appendix B

BEB.1 Don Smith invested $5000 at 6% annual interest, and left the money invested without withdrawing any of the interest for 10 years. At the end of the 10 years, Don withdrew the accumulated amount of money. (a) What amount did Don withdraw assuming the investment earns simple interest? (b) What amount did Don withdraw assuming the investment earns interest compounded annually?

BEB.2 For each of the following cases, indicate (a) to what interest rate columnsand (b) to what number of periods you would refer in looking up the future value factor.

1. In table 1 (future value of 1):

2. In table 2 (future value of an annuity of 1):

BEB.3 Porter Ltd signed a lease for an office building for a period of 10 years. Under the lease agreement, a security deposit of $10 000 is made. The deposit will be returned at the expiration of the lease with interest compounded at 5% per year. What amount will Porter receive at the time the lease expires?

BEB.4 David and Kathy Hatcher invested $5000 in a savings account paying 6% annual interest when their daughter, Sue, was born. They also deposited $1000 on each of her birthdays until she was 18 (including her 18th birthday). How much will be in the savings account on her 18th birthday (after the last deposit)?

BEB.5 Ron Watson borrowed $20 000 on 1 July 2000. This amount plus accrued interest at 6% compounded annually is to be repaid on 1 July 2005. How much will Ron have to repay on 1 July 2005?

BEB.6 For each of the following cases, indicate (a) to what interest rate columns and (b) to what number of periods you would refer in looking up the discount rate.

1. In table 3 (present value of 1):

2. In table 4 (present value of an annuity of 1):

BEB.7 (a) What is the present value of $10 000 due 8 periods from now, discounted at 8%? (b) What is the present value of $10 000 to be received at the end of each of 6 periods, discounted at 9%?

Annual rateNumber of

years invested Compounded

(a)(b)

6%5%

53

AnnuallyHalf-yearly

Annual rateNumber of

years invested Compounded

(a)(b)

5%4%

106

AnnuallyHalf-yearly

Annual rateNumber of

years involvedDiscounts per year

(a)(b)(c)

12%10%8%

6158

AnnuallyAnnuallyHalf-yearly

Annual rateNumber of

years involvedNumber of

payments involvedFrequency of

payments

(a)(b)(c)

12%10%8%

2054

2058

AnnuallyAnnuallyHalf-yearly

BRIEF EXERCISES (USE TABLES TO SOLVE EXERCISES)Calculate the future value of a

single amount.

(LO2)

Using future value tables.

(LO2,3)

Calculate the future value of a

single amount.

(LO2)

Calculate the future value of a

single amount and of an

annuity.

(LO2,3)

Calculate the future value of a

single amount.

(LO2)

Using present value tables.

(LO5,6)

Determining present values.

(LO5,6)

Appendix B 1065

BEB.8 Smolinski Ltd is considering an investment which will return a lump sum of $500 000 in 5 years from now. What amount should Smolinski Ltd pay for this investment to earn a 15% return?

BEB.9 Pizzeria Ltd earns 11% on an investment that will return $875 000 in 8 years from now. What is the amount Pizzeria should invest now to earn this rate of return?

BEB.10 Kilarny Bros is considering investing in an annuity contract that will return $20 000 annually at the end of each year for 15 years. What amount should Kilarny Bros pay for this investment if it earns a 6% return?

BEB.11 Jenna & Co. earns 11% on an investment that pays back $110 000 at the end of each of the next 4 years. What is the amount Zarita & Co. invested to earn the 11% rate of return?

BEB.12 Caledonia Pty Ltd receives a $50 000, 6-year note bearing interest of 11% (paid annually) from a customer at a time when the discount rate is 12%. What is the present value of the note received by Caledonia?

BEB.13 Brian Sands owns a garage and is contemplating purchasing a tyre-retreading machine for $16 280. After estimating costs and revenues, Brian projects a net cash flow from the retreading machine of $2790 annually for 8 years. He hopes to earn a return of 11% on such investments. What is the present value of the retreading operation? Should Brian purchase the retreading machine?

BEB.14 Hung-Chao Yu Ltd issues a 10%, 6-year mortgage note on 1 January 2006 to obtain financing for new equipment. The terms provide for half-yearly instalment payments of $112 825. What were the cash proceeds received from the issue of the note?

BEB.15 Ramy Pty Ltd is considering purchasing equipment. The equipment will produce the following cash flows: Year 1, $30 000; Year 2, $40 000; Year 3, $50 000. Ramy Pty Ltd requires a minimum rate of return of 15%. What is the maximum price Ramy should pay for this equipment?

BEB.16 Kerry Rogers invests $1827 now and will receive $10 000 at the end of 15 years. What annual rate of interest will Kerry earn on her investment? (Hint: Use table 3.)

BEB.17 Michael Cork has been offered the opportunity of investing $24 719 now. The investment will earn 15% per year and at the end of that time will return Michael $100 000. How many years must Michael wait to receive $100 000? (Hint: Use table 3.)

BEB.18 Annie Dublin purchased an investment for $11 469.92. From this investment, she will receive $1000 annually for the next 20 years starting 1 year from now. What rate of interest will Annie’s investment be earning for her? (Hint: Use table 4.)

BEB.19 Dylan Grey invests $8851.37 now for a series of $1000 annual returns beginning one year from now. Dylan will earn a return of 8% on the initial investment. How many annual payments of $1000 will Dylan receive? (Hint: Use table 4.)

Calculate the present value of

a single amount investment.

(LO5)

Calculate the present value of

a single amount investment.

(LO5)

Calculate the present value of

an annuity investment.

(LO6)

Calculate the present value of

an annuity investment.

(LO6)

Calculate the present value of

a note.

(LO5,6)

Calculate the present value of

a machine for purposes of

making a purchase decision.

(LO7)

Calculate the present value of

a note.

(LO5,6)

Calculate the maximum price

to pay for a machine.

(LO7)

Calculate the interest rate on a

single amount.

(LO5)

Calculate the number of

periods of a single amount.

(LO5)

Calculate the interest rate on

an annuity.

(LO6)

Calculate the number of

periods of an annuity.

(LO6)