time series analysis - lecture 3 forecasting using arima-models step 1. assess the stationarity of...

Post on 19-Dec-2015

216 views

TRANSCRIPT

Time series analysis - lecture 3

Forecasting using ARIMA-models

Step 1. Assess the stationarity of the given time series of data and form differences if necessary

Step 2. Estimate auto-correlations and partial auto-correlations, and select a suitable ARMA-model

Step 3. Compute forecasts according to the estimated model

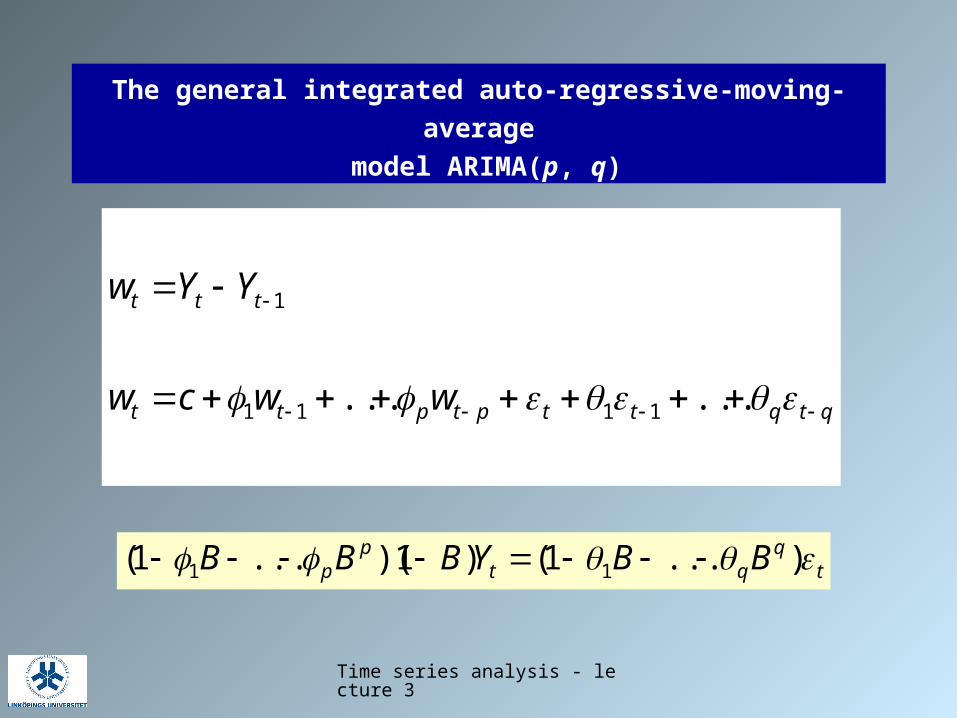

Time series analysis - lecture 3

The general integrated auto-regressive-moving-average

model ARIMA(p, q)

qtqttptptt

ttt

wwcw

YYw

...... 1111

1

tq

qtp

p BBYBBB )...1()1)(...1( 11

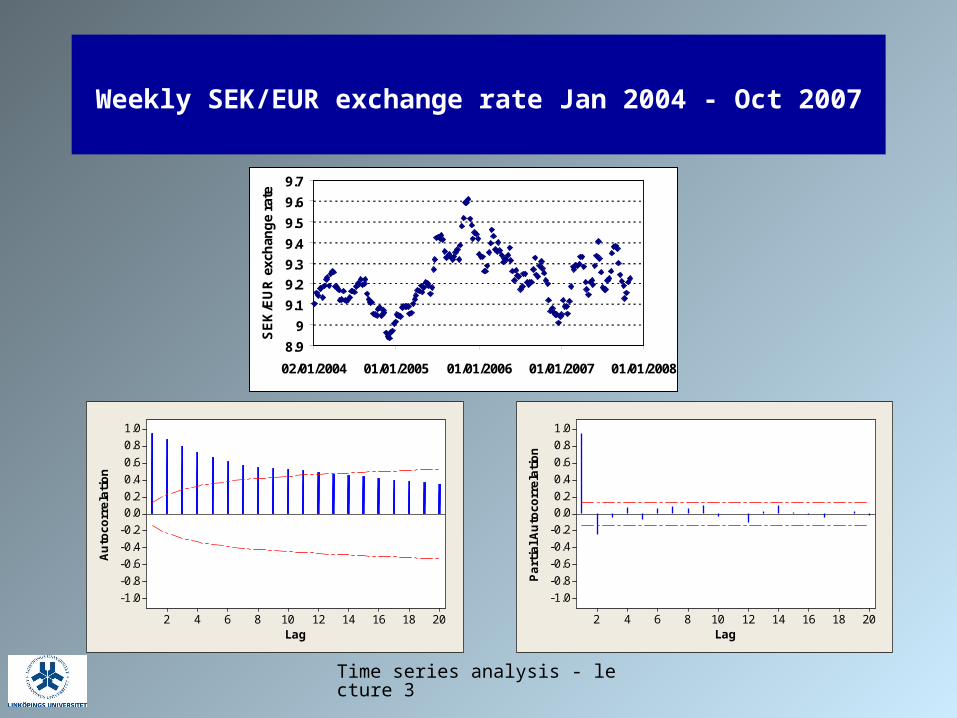

Time series analysis - lecture 3

Weekly SEK/EUR exchange rate Jan 2004 - Oct 2007

8.9

9

9.1

9.2

9.3

9.4

9.5

9.6

9.7

02/01/2004 01/01/2005 01/01/2006 01/01/2007 01/01/2008

SE

K/E

UR

exc

han

ge

rate

2018161412108642

1.00.80.60.40.20.0

-0.2-0.4-0.6-0.8-1.0

Lag

Auto

corr

ela

tion

2018161412108642

1.00.80.60.40.20.0

-0.2-0.4-0.6-0.8-1.0

Lag

Part

ial A

uto

corr

ela

tion

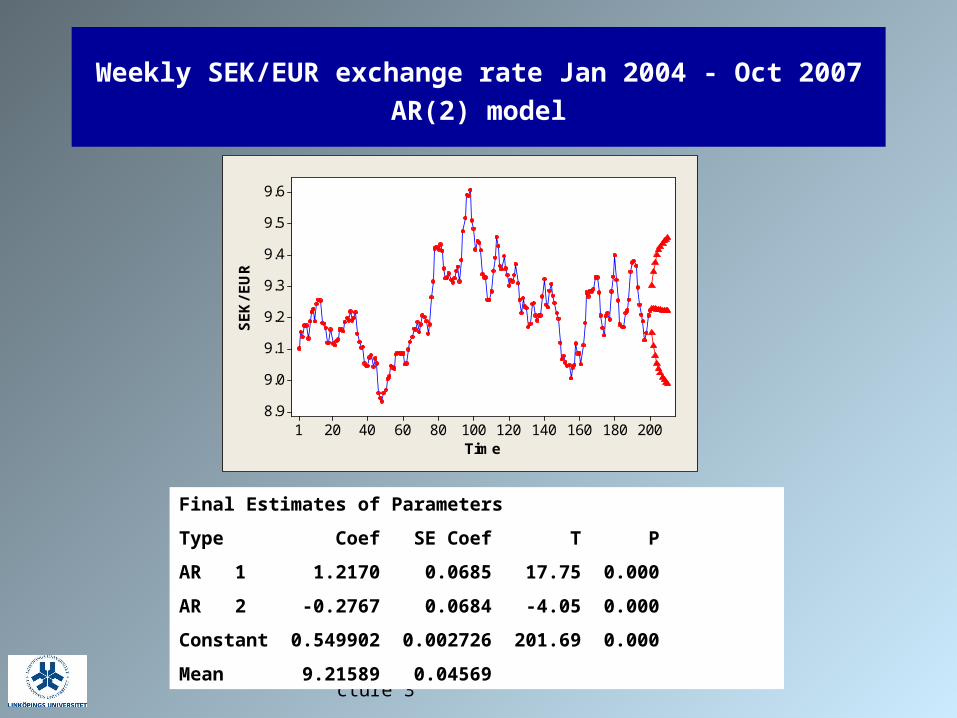

Time series analysis - lecture 3

Weekly SEK/EUR exchange rate Jan 2004 - Oct 2007

AR(2) model

Final Estimates of Parameters

Type Coef SE Coef T P

AR 1 1.2170 0.0685 17.75 0.000

AR 2 -0.2767 0.0684 -4.05 0.000

Constant 0.549902 0.002726 201.69 0.000

Mean 9.21589 0.04569

200180160140120100806040201

9.6

9.5

9.4

9.3

9.2

9.1

9.0

8.9

Time

SEK

/EU

R

Time series analysis - lecture 3

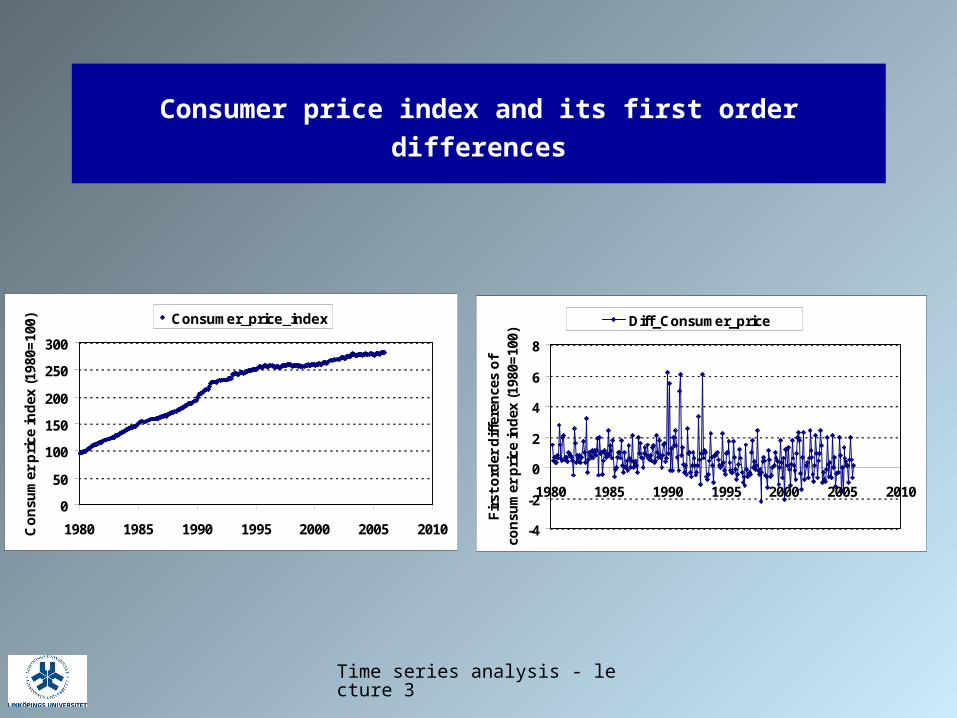

Consumer price index and its first order differences

0

50

100

150

200

250

300

1980 1985 1990 1995 2000 2005 2010Co

nsu

mer

pri

ce in

dex

(19

80=

100) Consumer_price_index

-4

-2

0

2

4

6

8

1980 1985 1990 1995 2000 2005 2010F

irst

ord

er d

iffe

ren

ces

of

con

sum

er p

rice

ind

ex (

1980

=10

0)

Diff_Consumer_price

Time series analysis - lecture 3

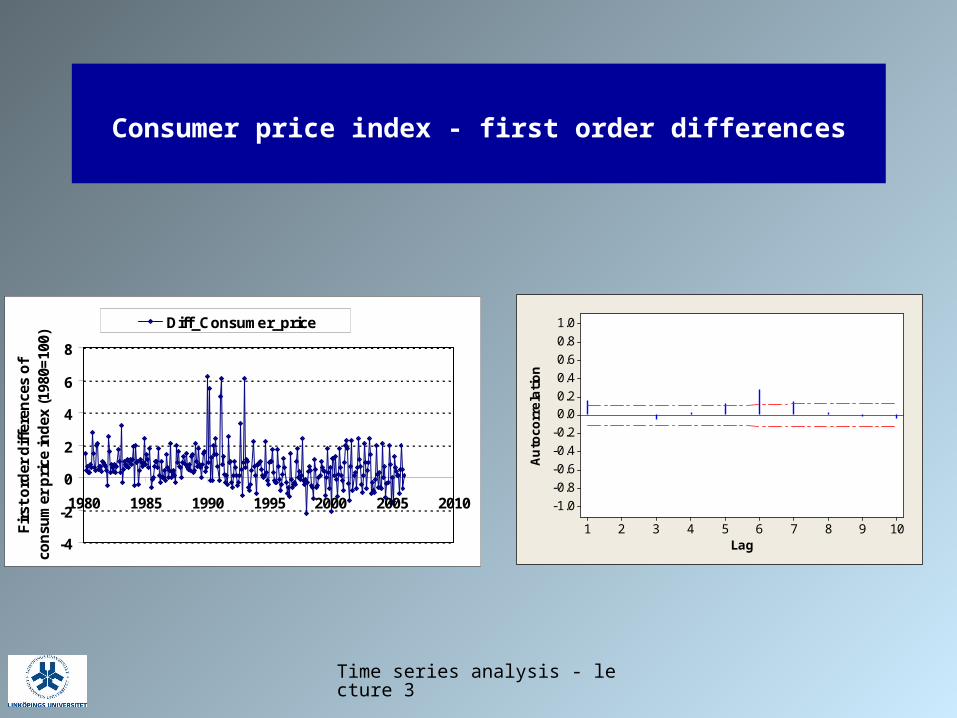

Consumer price index - first order differences

10987654321

1.00.80.60.40.20.0

-0.2-0.4-0.6-0.8-1.0

LagAuto

corr

ela

tion

-4

-2

0

2

4

6

8

1980 1985 1990 1995 2000 2005 2010

Fir

st o

rder

dif

fere

nce

s o

f co

nsu

mer

pri

ce in

dex

(19

80=

100)

Diff_Consumer_price

Time series analysis - lecture 3

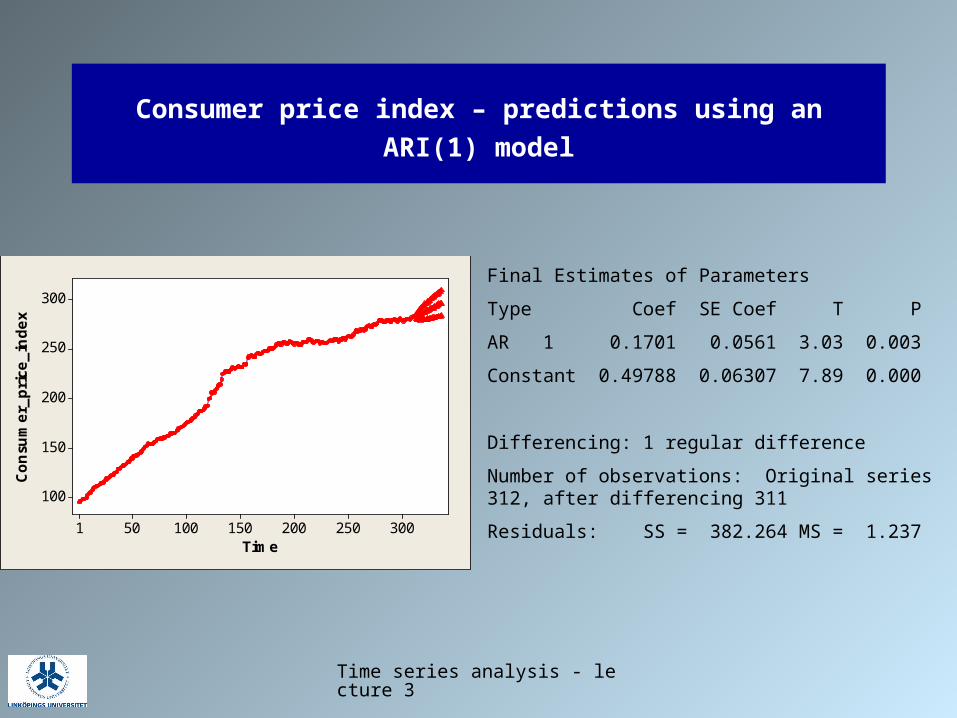

Consumer price index – predictions using an ARI(1) model

300250200150100501

300

250

200

150

100

Time

Consu

mer_

pri

ce_in

dex

Final Estimates of Parameters

Type Coef SE Coef T P

AR 1 0.1701 0.0561 3.03 0.003

Constant 0.49788 0.06307 7.89 0.000

Differencing: 1 regular difference

Number of observations: Original series 312, after differencing 311

Residuals: SS = 382.264 MS = 1.237

Time series analysis - lecture 3

Seasonal differencing

Form

where S depicts the seasonal length

tS

Sttt YBYYw )1(

Time series analysis - lecture 3

Consumer price index and its seasonal differences

-5

0

5

10

15

20

25

30

1980 1985 1990 1995 2000 2005 2010S

easo

nal

dif

fere

nce

s o

f co

nsu

mer

pri

ce in

dex

(19

80=

100)

Seasonal diff

0

50

100

150

200

250

300

1980 1985 1990 1995 2000 2005 2010Co

nsu

mer

pri

ce in

dex

(19

80=

100) Consumer_price_index

Time series analysis - lecture 3

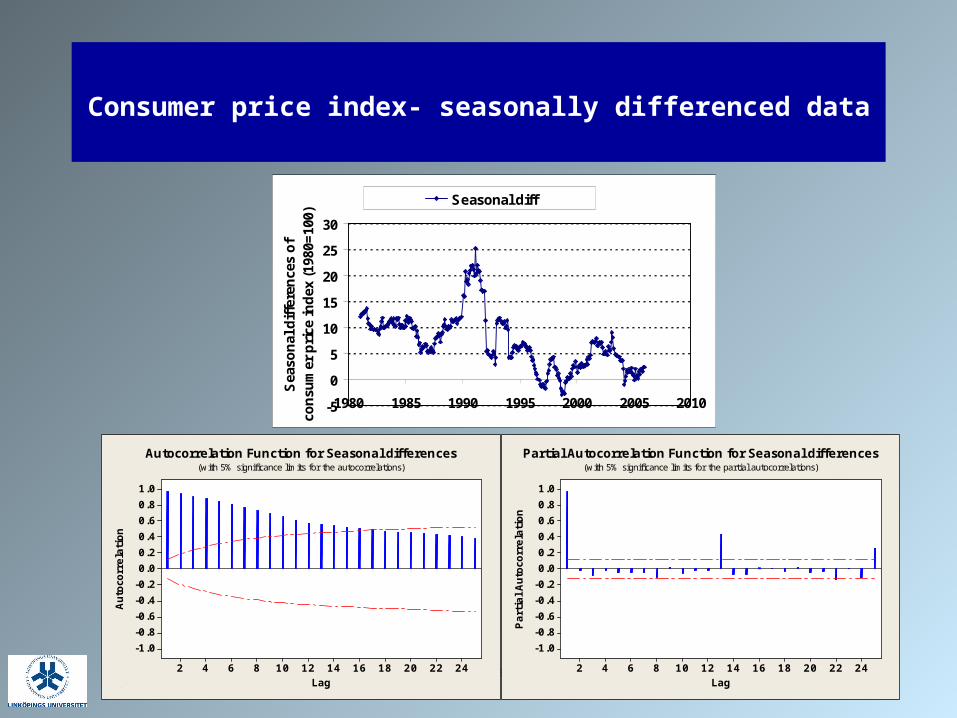

Consumer price index- seasonally differenced data

24222018161412108642

1.0

0.8

0.6

0.4

0.2

0.0

-0.2

-0.4

-0.6

-0.8

-1.0

Lag

Auto

corr

ela

tion

Autocorrelation Function for Seasonal differences(with 5% significance limits for the autocorrelations)

-5

0

5

10

15

20

25

30

1980 1985 1990 1995 2000 2005 2010

Sea

son

al d

iffe

ren

ces

of

con

sum

er p

rice

ind

ex (

1980

=10

0)

Seasonal diff

24222018161412108642

1.0

0.8

0.6

0.4

0.2

0.0

-0.2

-0.4

-0.6

-0.8

-1.0

Lag

Part

ial Auto

corr

ela

tion

Partial Autocorrelation Function for Seasonal differences(with 5% significance limits for the partial autocorrelations)

Time series analysis - lecture 3

Consumer price index- differenced and seasonally differenced data

-8

-6

-4

-2

0

2

4

6

8

1980 1985 1990 1995 2000 2005 2010

Dif

fere

nce

s o

f se

aso

nal

dif

fere

nce

s o

f co

nsu

mer

pri

ce i

nd

ex

(198

0=10

0)

Diff. and seasonally diff.

24222018161412108642

1.0

0.8

0.6

0.4

0.2

0.0

-0.2

-0.4

-0.6

-0.8

-1.0

Lag

Auto

corr

ela

tion

Autocorrelation Function for Diff. of seasonal diff.(with 5% significance limits for the autocorrelations)

24222018161412108642

1.0

0.8

0.6

0.4

0.2

0.0

-0.2

-0.4

-0.6

-0.8

-1.0

Lag

Part

ial Auto

corr

ela

tion

Partial Autocorrelation Function for Diff. of seasonal diff.(with 5% significance limits for the partial autocorrelations)

Time series analysis - lecture 3

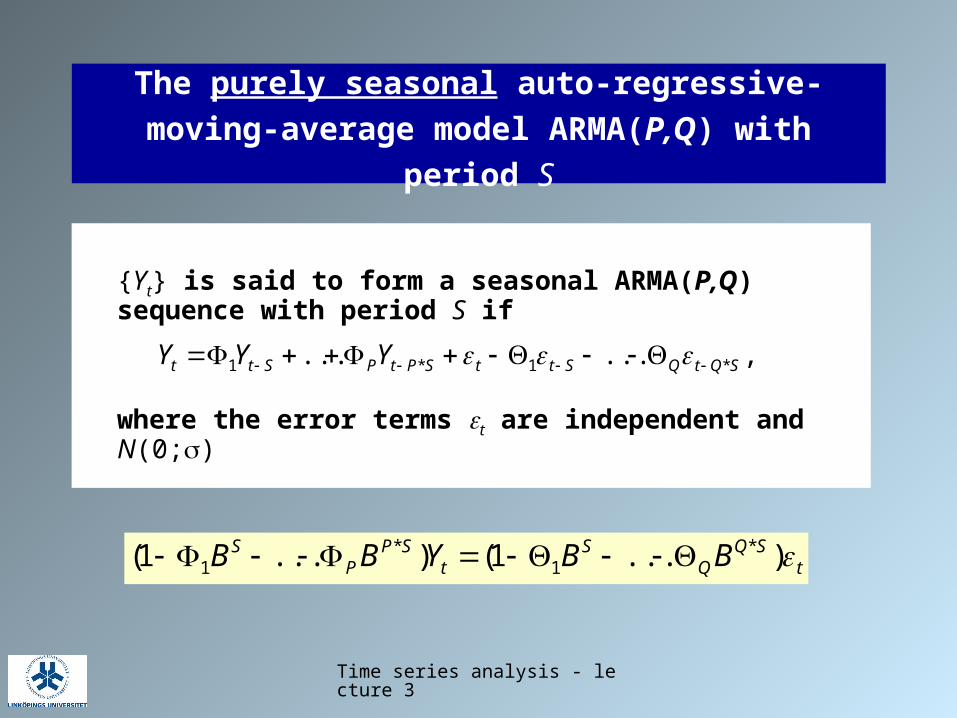

The purely seasonal auto-regressive-moving-

average model ARMA(P,Q) with period S

{Yt} is said to form a seasonal ARMA(P,Q) sequence with period S if

where the error terms t are independent and N(0;)

,...... *1*1 SQtQSttSPtPStt YYY

tSQ

QS

tSP

PS BBYBB )...1()...1( *

1*

1

Time series analysis - lecture 3

Typical auto-correlation functions of purely

seasonal ARMA(P,Q) sequences with period S

Auto-correlations are non-zero only at lags S, 2S, 3S, …

In addition: AR(P): Autocorrelations tail off gradually with increasing time-lags

MA(Q): Auto-correlations are zero for time lags greater than q*S

ARMA(P,Q): Auto-correlations tail off gradually with time-lags greater than q*S

Time series analysis - lecture 3

No. air passengers by week in Sweden

-original series and seasonally differenced data

12.2

12.4

12.6

12.8

13.0

13.2

13.4

13.6

1992 1996 2000 2004No

.pas

sen

ger

s at

Sw

edis

h a

irp

ort

s (t

ho

usa

nd

s)

No. passengers

-0.4

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

1992 1996 2000 2004D

iffe

ren

ce la

g 5

2 (t

ho

usa

nd

s)

Difference lag 52

Time series analysis - lecture 3

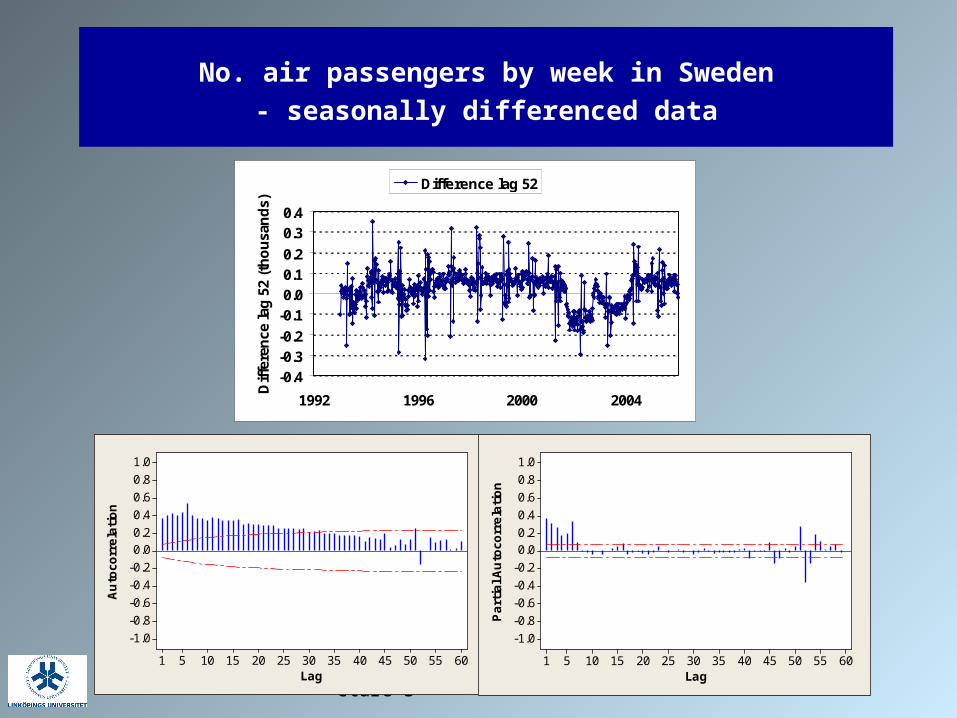

No. air passengers by week in Sweden

- seasonally differenced data

-0.4

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

1992 1996 2000 2004

Dif

fere

nce

lag

52

(th

ou

san

ds)

Difference lag 52

605550454035302520151051

1.00.80.60.40.20.0

-0.2-0.4-0.6-0.8-1.0

Lag

Auto

corr

ela

tion

605550454035302520151051

1.00.80.60.40.20.0

-0.2-0.4-0.6-0.8-1.0

Lag

Part

ial A

uto

corr

ela

tion

Time series analysis - lecture 3

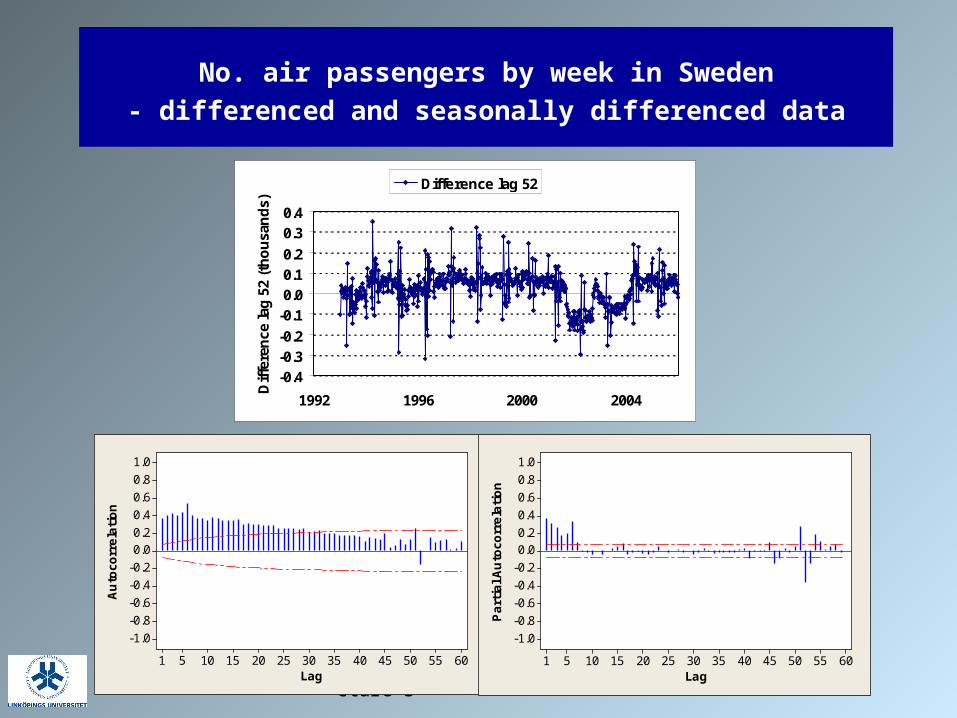

No. air passengers by week in Sweden

- differenced and seasonally differenced data

-0.4

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

1992 1996 2000 2004

Dif

fere

nce

lag

52

(th

ou

san

ds)

Difference lag 52

605550454035302520151051

1.00.80.60.40.20.0

-0.2-0.4-0.6-0.8-1.0

Lag

Auto

corr

ela

tion

605550454035302520151051

1.00.80.60.40.20.0

-0.2-0.4-0.6-0.8-1.0

Lag

Part

ial A

uto

corr

ela

tion

Time series analysis - lecture 3

The general seasonal auto-regressive-moving-

average model ARMA(p, q, P, Q) with period S

{Yt} is said to form a seasonal ARMA(p, q, P, Q) sequence with period S if

where the error terms t are independent and N(0;)

Example: p = P = 0, q = Q = 1, S = 12

.

131112111112

1 )1)(1( tttttt BBY

tq

qSQ

QS

tp

pSP

PS

BBBB

YBBBB

)...1)(...1(

)...1)(...1(

1*

1

1*

1

Time series analysis - lecture 3

The general seasonal integrated auto-regressive-moving-

average model ARMA(p, q, P, Q) with period S

{Yt} is said to form a seasonal ARIMA(p, q, d, P, Q, D) sequence with period S if

where the error terms t are independent and N(0;)

tq

qSQ

QS

tdDSp

pSP

PS

BBBB

YBBBBBB

)...1)(...1(

)1()1)(...1)(...1(

1*

1

1*

1

Time series analysis - lecture 3

Forecasting using Seasonal ARIMA-models

Step 1. Assess the stationarity of the given time series of data and form differences and seasonal differences if necessary

Step 2. Estimate auto-correlations and partial auto-correlations, and select a suitable ARMA-model of the short-term dependence

Step 3. Estimate auto-correlations and partial auto-correlations, and select a suitable seasonal ARMA-model of the variation by season

Step 4. Compute forecasts according to the estimated model

Time series analysis - lecture 3

Consumer price index- differenced and seasonally differenced data

-8

-6

-4

-2

0

2

4

6

8

1980 1985 1990 1995 2000 2005 2010

Dif

fere

nce

s o

f se

aso

nal

dif

fere

nce

s o

f co

nsu

mer

pri

ce i

nd

ex

(198

0=10

0)

Diff. and seasonally diff.

24222018161412108642

1.0

0.8

0.6

0.4

0.2

0.0

-0.2

-0.4

-0.6

-0.8

-1.0

Lag

Auto

corr

ela

tion

Autocorrelation Function for Diff. of seasonal diff.(with 5% significance limits for the autocorrelations)

24222018161412108642

1.0

0.8

0.6

0.4

0.2

0.0

-0.2

-0.4

-0.6

-0.8

-1.0

Lag

Part

ial Auto

corr

ela

tion

Partial Autocorrelation Function for Diff. of seasonal diff.(with 5% significance limits for the partial autocorrelations)

Time series analysis - lecture 3

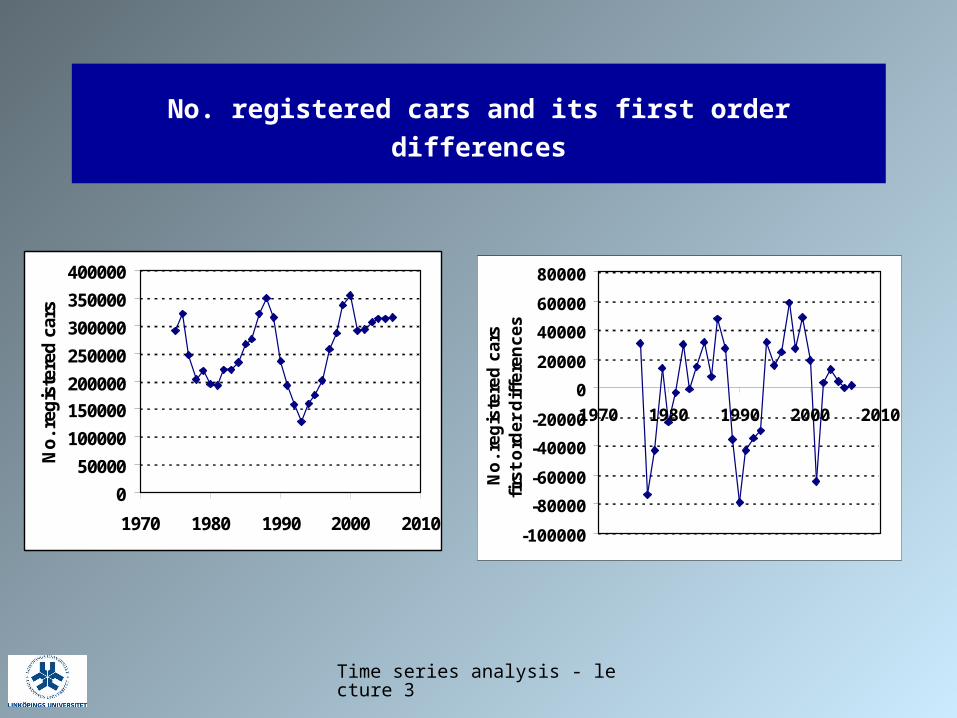

No. registered cars and its first order differences

0

50000

100000

150000

200000

250000

300000

350000

400000

1970 1980 1990 2000 2010

No

. reg

iste

red

car

s

-100000

-80000

-60000

-40000

-20000

0

20000

40000

60000

80000

1970 1980 1990 2000 2010

No

. re

gis

tere

d c

ars

firs

t o

rde

r d

iffe

ren

ce

s

Time series analysis - lecture 3

No. registered cars

- first order differences

-100000

-80000

-60000

-40000

-20000

0

20000

40000

60000

80000

1970 1980 1990 2000 2010

No

. re

gis

tere

d c

ars

firs

t o

rde

r d

iffe

ren

ce

s

10987654321

1.00.80.60.40.20.0

-0.2-0.4-0.6-0.8-1.0

Lag

Auto

corr

ela

tion

30282624222018161412108642

1.00.80.60.40.20.0

-0.2-0.4-0.6-0.8-1.0

Lag

Part

ial A

uto

corr

ela

tion