time : 3 hours maximum marks : 100 note : attempt … papers june... · variable expenses 90 fixed...

TRANSCRIPT

No. of Printed Pages : 8 MCO-05

MASTER OF COMMERCE

Term-End Examination

Uc June, 2010tr)O

MCO-05 : ACCOUNTING FORMANAGERIAL DECISIONS

Time : 3 hours Maximum Marks : 100

Note : Attempt any five questions. All questions carry equal

marks.

What are the objectives of accounting ? Explain 20any four accounting concepts and two accountingconvertions.

What do you mean by analysis of financial 20statements ? Explain briefly the varioustechniques of financial Analysis.

3. Write explanatory notes on : 10+10Performance BudgetingBudgetary Control Ratios.

4. (a) Describe the various methods of transferpricing. 10+10

(b) Elaborate the essentials of success ofresponsibility Accounting.

MCO-05

1 P.T.O.

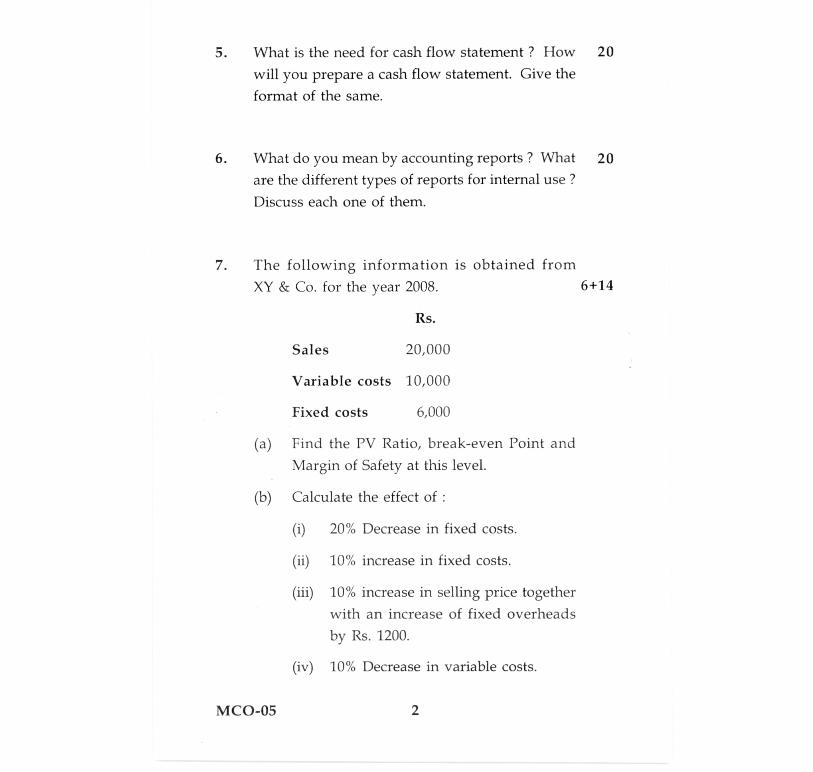

What is the need for cash flow statement ? How 20

will you prepare a cash flow statement. Give theformat of the same.

What do you mean by accounting reports ? What 20are the different types of reports for internal use ?

Discuss each one of them.

7. The following information is obtained fromXY & Co. for the year 2008. 6+14

Rs.

Sales 20,000

Variable costs 10,000

Fixed costs 6,000

Find the PV Ratio, break-even Point andMargin of Safety at this level.

Calculate the effect of :

20% Decrease in fixed costs.

10% increase in fixed costs.

10% increase in selling price togetherwith an increase of fixed overheadsby Rs. 1200.

10% Decrease in variable costs.

MCO-05 2

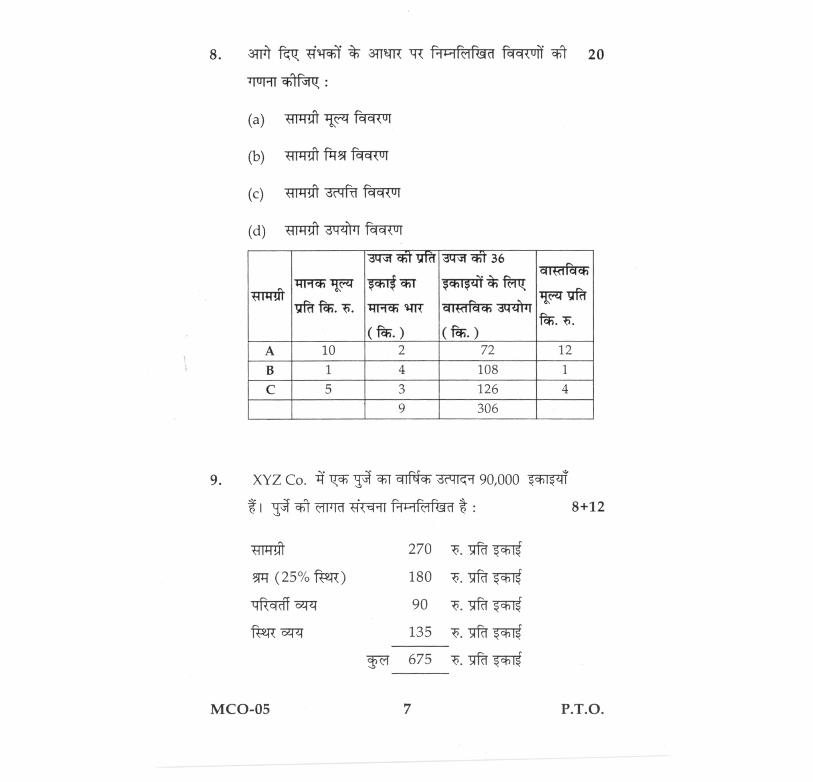

8. Calculate from the following data : 20

Material price variance.

Material Mix variance.

Material yield variance, and

Material usage variance.

MaterialStandardPriceper kg Rs.

StandardWeight perunit ofout ut kg sp

Actual usagefor output of36 units kgs

Actualpriceper kgRs.

A 10 2 72 12B 1 4 108 1C 5 3 126 4

9 306

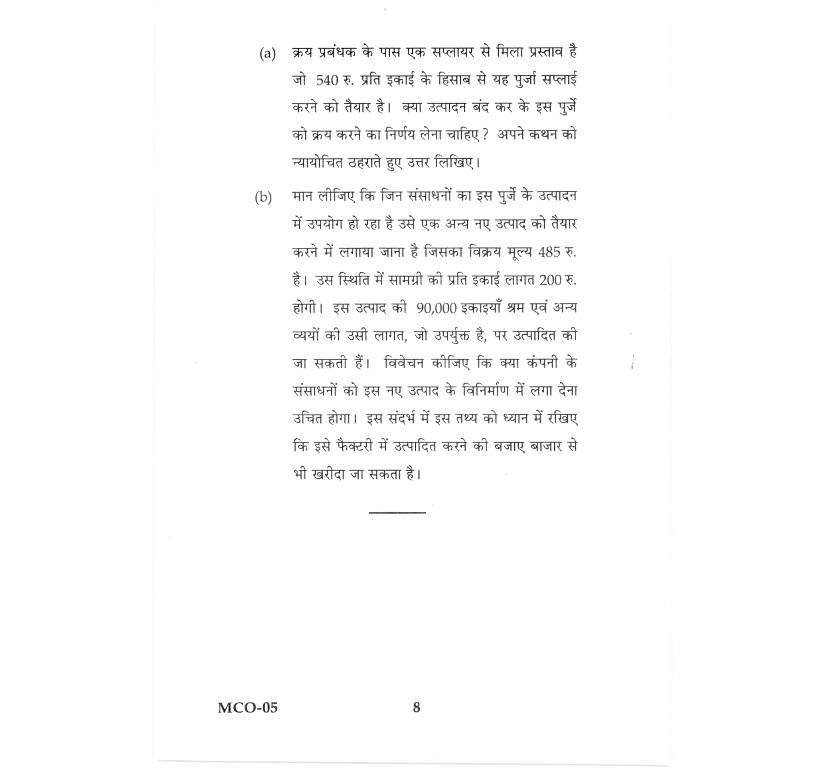

9. XYZ Co. has an annual production of 90,000 unitsfor a component The component cost structureis given below : 8+12

Rs.Material 270

Labour (25% fixed) 180Variable expenses 90Fixed expenses 135

Total 675

per unitper unitper unitper unitper unit

(a) The purchase manager has an offer from asupplier, who is willing to supply thecomponent at Rs. 540. Should thecomponent be purchased and productionstopped ? Give Justifications for youranswer.

MCO-05

3 P.T.O.

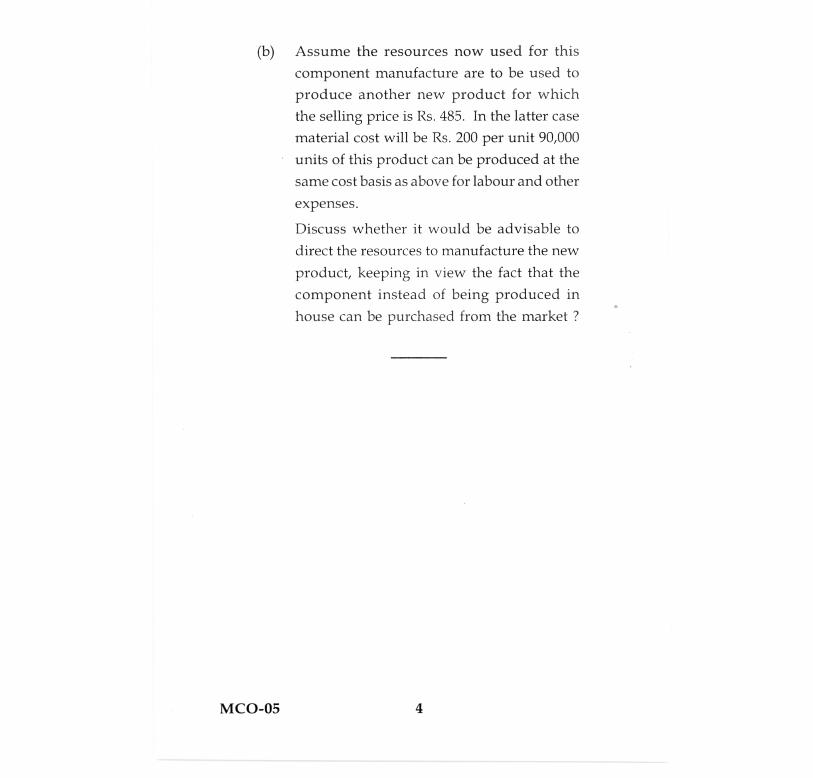

(b) Assume the resources now used for thiscomponent manufacture are to be used toproduce another new product for whichthe selling price is Rs. 485. In the latter casematerial cost will be Rs. 200 per unit 90,000units of this product can be produced at thesame cost basis as above for labour and otherexpenses.

Discuss whether it would be advisable todirect the resources to manufacture the newproduct, keeping in view the fact that thecomponent instead of being produced inhouse can be purchased from the market ?

MCO-05 4

airukr#4 Iriet.;171( 7crrru

IthalT

2010

7r. .art-05 : "Cf4U-4-4 falT1711

Fri=fq :3 74'0- 31fgiwuTt 3-iW : 100

-de : w)-$` drf,c -F-73 7 / F .# vyaTi 37W

;t113-k7z1? ki=n(-,-1113ff 20

HRHirdisi cq i(y-if --If•--A7

fade faat ul faocaa u r qzfr *? facer 20

rcw. a u r rafi r 7F--af974 =411 *17 cws,-ir

3. 14-iri tq d 'TT =iitsq icH ch d u-i 1 44T ffft17 : 10+10

fiWKi

i fl7=NuT aura

4. (a) 1174 f qi-Tur 1.1r faitfzft air qqff

•Af-A7 10+10

(b) dcit6iiq c,4 4)1 31"1-41

fa-9-ff aui-r

MCO-05

5 P.T.O.

-43 31-a7 fT7T chi aziT 311-47177T A-*3- -51-a7 20

fa-a-t-17 3-Ti4 feu M chR *TR ? -9-wq q11-',1

c(.11 ,11-1ft-t4h1 A Ir 4f t? alf-d-r-TT -a-cr?trr 20

111 .-fTft fqr ITI? r{Thq. 171R .1;1 ? oe-iksqf

7. X Y& Co. A 2008 ci ti A A-4Na -1 4--1 od

1;7 : 6+14

T.

fa-T-74 20,000

trfta-d1 cit 4 1 10,000

#.247 e-11 4 1 6,000

. 11-1. Hi* 3-1TITff (PV Ratio), TITI-fd-4 "fq-

(BEP) 7:17 TUT -1=11 (Margin of

Safety) .W1f-4 I

1 4-1 tad t 741.Td oh1 I 1-1[1-r—A7 :

#2.17 ovicif A 20%

f=9-R C1I 1 Ici A 10%

f-R-17 3ZTfti-?4 4 1200T. enl 1f4 Afq

fat -1=r4 -4 10%

(iv) li-r-{4a1 10% ch1-1

MCO-05 6

8. 31-14 R q, TlIT*1 31-KR "Ti F-H-forig d FacR u il a1 20

4 i u mf :

-PTI:ra

3q-7 -1' 1;rfa.

1+TW•

d44 22. 36cm-drach

iiiich Itro-1,, ,.,

ArffTw. T.

.)w.41*.FF7liC`q vrfff- . . T.

Ruch WIT

( ft. )

cii iach d'4 I

( ft. )A 10 2 72 12B 1 4 108 1C 5 3 126 4

9 306

9. XYZ Co. 14 1-) ri4 'TT arrft 90,000

t I rwici +1. (-,411 F-1 4-ifolocr : 8+12

77qt 270 T. "gt

5p4 (25%#27) 180 T. 'At

tift—dt 0q 4 90 T. "5ft

#27 oqq 135 T. sik

mfr 675 T. i;rfff

MCO-05

7 P.T.O.

5414 Slcf 41N i c w-olw R4 fil-ff1 d t

540 T. SI rcf -pi TILTIF

c4-;1 NTT t I °HI dc-41 q -r 741-4

sh q rf9-074 349-4 -T-2

att-r 3r1 f7r-U7

-14N M1I 11 1 fA-r dcyq-1

39 T t 1-) .-1/ dc4-11q 1-4 thlTi

-T4s cd 4 ii1r s=tiir t fqw-4 174 485 T.

t 13ti -FF-24-rd -R1-1:11t obl siFcr 0141c1 200 T.

11 4 1 I 74 z-o=i-r a-)1 90,000 r-14 1 31-4

chl 3# 01 4 1d, 31:FT t, IT{

t I fq-----47 rch ci-q t ttrt

Tfti-rg-91 <4-4 z-r 3c41‹ rar-Hi u r (1 , 1r -i1

ir l 4of -474 2.7:1 1;1 tzrrff fmi7

*--1z-1 dr-iirq d m1 q--ATR al vilt

ut-1---r d t I

MCO-05 8