thursday, march 3, 2016 houston, tx 12:30 – 1:45 p.m. it’s

TRANSCRIPT

CIn

Thursday, March 3, 2016Houston, TX

12:30 – 1:45 p.m.

IT’S A MAD WORLD:DUE DILIGENCE AND REPS AND WARRANTIES INSURANCE

Presented by

Bernard P. (Bernie) BellPartner

Jones Day

The state of the energy industry is driving more mergers, acquisitions, and divestitures. In-accuracies in representations and warranties made by the seller or the target company inconnection with a merger or acquisition can result in costly liabilities. Buyers can be leftwithout the ability to recover losses, and sellers can be forced to hand back a portion ofthe purchase price. Representations and warranties insurance helps protect both buyersand sellers involved in these transactions from financial loss in the event inaccuracies inrepresentations and warranties are made. This session will look at the risks arising fromsuch activities and how reps and warranties coverage can help protect all parties.

1

opyright © 2016 International Risk Management stitute, Inc.

www.IRMI.com

Notes

This file is set up for duplexed printing. Therefore, there are pages that are intentionally leftblank. If you print this file, we suggest that you set your printer to duplex.

2

Bernard P. (Bernie) BellPartner

Jones Day

Bernie Bell has decades of experience as a trial lawyer in civil litigation, and he has concentratedhis practice for the last 18 years on obtaining insurance recoveries for corporate policyholdersand their individual directors and officers. His practice covers the full range of insurance claims,from property damage and business interruption losses to claims arising from alleged directors’and officers’ liabilities, as well as employment, environmental, fiduciary (ERISA), product, profes-sional, and toxic tort liabilities.

His recent representations include several engagements to recover property damage and busi-ness interruption losses caused by catastrophic failures at industrial facilities, including refiner-ies, petroleum chemical plants, and oil and gas pipelines.

Mr. Bell also is an experienced environmental litigator. He spent five years as a trial attorney withthe U.S. Department of Justice, representing the U.S. in environmental enforcement lawsuits un-der Superfund (CERCLA), the Clean Air Act, and the Clean Water Act. He has handled complex en-vironmental matters in private practice, including Clean Air Act and Superfund litigation and FI-FRA pesticide data compensation arbitrations.

A frequent author and speaker on insurance coverage issues, he received his juris doctorate fromFordham University, where he was editor of Fordham Law Review. He received his A.B. cumlaude from Colgate University.

3

Notes

This file is set up for duplexed printing. Therefore, there are pages that are intentionally leftblank. If you print this file, we suggest that you set your printer to duplex.

4

Representations and WarrantiesInsurance

Presented By:

BERNARD BELLPartnerJONES DAY

#IRMI2016 1500819400v2

5

AGENDA• Representations & Warranties Insurance

• Who is insured• Buy-Side• Sell-Side

• What is covered• What is not covered

• Purchasing Process• Claims History• Other Transactional Risk Products

3

M&A overview

• Representations and warranties in the contract address risks (known and unknown) in the transaction

• Buyers want protection and recourse; Sellers want clean exit from investment or business

• Buyer may wish to offer seller greater finality as a means to distinguish among competing offers

• Buyer may have limited recourse to Seller, or strategic reasons to avoid future adversity

4

6

Representations & Warranties Insurance• Representations and Warranties (“R&W”) insurance

protects insured party from losses resulting from breach of representations and warranties regarding the acquired company, business or assets

• Financial statements; tax treatment; accounts receivable; inventories; intellectual property

• Take-or-pay or forward sale contracts• Gathering systems “in compliance with laws”• Assets in working order & operating condition

5

Representations & Warranties Insurance• Some standard form policies but manuscript is

common to meet specific needs of each deal• Terms vary significantly from policy to policy

• First underwritten in US market ~1998• Underwriters claim significant increase in volume of

placements since 2013/14• Conventional wisdom:

• Driven by private equity and seller-friendly market• Best suited for middle market (<$1B) transactions

6

7

Who is “Insured”?

• Either Buyer or Seller may be the “Insured"• Two types of R&W policies

• “Buy-Side” policy (CW: 90% of market)• “Sell-Side” policy

• Different objectives and coverage triggers• Buyer may purchase coverage for the Seller or vice

versa

7

Buy-Side R&W Insurance• Insured: Buyer• Objective: Cover Buyer for loss from breach of

Seller’s warranties• Written as first party coverage

• Indemnifies Buyer directly for loss resulting from breach

• Buyer’s claim is directly against insurer, not Seller• Seller’s liability is capped; insurance is excess of cap• Covers defense costs and amounts incurred as a

result of third party claims arising out of breaches

8

8

Justifications Offered for Buy-Side Coverage

• Buyer wants to enhance bid in competitive sale• Buyer wants greater or longer indemnification

than Seller is willing to provide• Buyer is concerned about collection risk

– Seller financial status uncertain– Numerous or geographically dispersed Sellers– Seller dissolving; uncertainty of chasing LPs

• Buyer is concerned about ongoing relationships with Seller or valuable employees

• Wants to maintain, may want to avoid 9

Sell-Side R&W Insurance• Insured: Seller• Objective: Coverage for claims by Buyer alleging

Seller breaches of representations and warranties • Written as third party coverage

• Indemnifies Seller for covered loss• Seller retains liability for uncovered breach

• Covers loss and defense costs resulting from claims made against Seller for breach

– Must be a “claim” as defined by policy– Generally no duty to defend, rather reimbursement

of defense costs subject to terms and conditions

10

9

Justifications Offered for Sell-Side R&W• Seller wants clean exit

• PE wants to expedite distribution of sale proceeds to LPs (dissolution or avoid escrow with low rate of return)

• Seller wants to reduce negotiated indemnity obligation and escrow

• Financially distressed Seller wants to use sale proceeds to pay down existing debt

• Seller wants to induce better offers by providing more indemnity

11

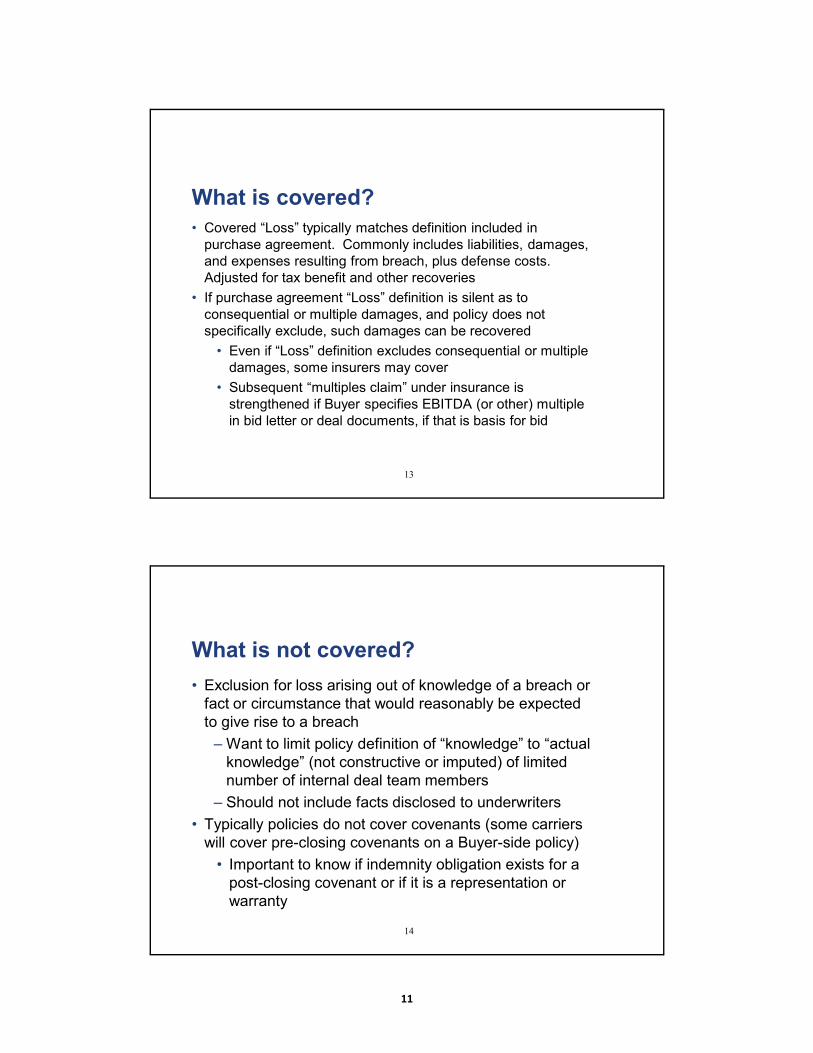

What is covered? • Coverage is determined by Seller’s representations

and warranties in purchase and sale agreement• Agreement is made part of policy application and

incorporated into policy• Insurer’s obligations limited to insured

representations and warranties• Blanket Policies: Cover all representations and

warranties, except as specifically excluded• Single Issue Policies: Cover only specified

representations and warranties

12

10

What is covered? • Covered “Loss” typically matches definition included in

purchase agreement. Commonly includes liabilities, damages, and expenses resulting from breach, plus defense costs. Adjusted for tax benefit and other recoveries

• If purchase agreement “Loss” definition is silent as to consequential or multiple damages, and policy does not specifically exclude, such damages can be recovered

• Even if “Loss” definition excludes consequential or multiple damages, some insurers may cover

• Subsequent “multiples claim” under insurance is strengthened if Buyer specifies EBITDA (or other) multiple in bid letter or deal documents, if that is basis for bid

13

What is not covered?• Exclusion for loss arising out of knowledge of a breach or

fact or circumstance that would reasonably be expected to give rise to a breach

– Want to limit policy definition of “knowledge” to “actual knowledge” (not constructive or imputed) of limited number of internal deal team members

– Should not include facts disclosed to underwriters• Typically policies do not cover covenants (some carriers

will cover pre-closing covenants on a Buyer-side policy) • Important to know if indemnity obligation exists for a

post-closing covenant or if it is a representation or warranty

14

11

What is not covered? (Cont’d)• Generally, Sell-side policies exclude coverage for

Seller’s fraud. [These types of breaches are generally covered in Buy-side.]

• Generally do not cover purchase price, net worth or other adjustments

• Deal-specific exclusions (e.g., environmental liabilities)

• May have issues arising out of difference between scope of coverage and indemnity maximum cap and basket

15

What is not covered? (Cont’d)• Exclusions:

• Pollution liabilities• Federal Corrupt Practices Act (FCPA) violations• Certain tax representations

– Market exists for separately insuring tax positions

• Certain securities law violations in respect of acquisition’s publicly-traded securities

16

12

Purchasing Process for R&W InsuranceStep One – Obtaining a Non-Binding Quote (2-5 business

days)• Broker obtains non-binding indication of interest from insurer(s)• Indication letter states general terms of insurance, including

limits, premium and deductible or retention• Enter into non-disclosure agreement before providing any

confidential materials to broker or insurers• Mark material with appropriate legal citations• Understand risk of waiver even with NDA

• Insurers may request offering memorandum, draft purchase-and-sale agreement, recent financial statements

17

Purchasing Process for R&W InsuranceStep Two – Selection of Insurer (1-2 days)

• Review non-binding quotes• Select insurer• Pay non-refundable underwriting fee

• Commonly between $10,000 and $75,000

18

13

Purchasing Process for R&W InsuranceStep Three – Underwriting (5-10 days)• Insurer conducts its own due diligence

• Stated objective: Confirm insured has approached transaction as if it was uninsured; moral hazard

• Independently evaluate Buyer’s advisors’ due diligence (Buy-side) or Seller’s disclosure process (Sell-side)

• Discussion with deal team, including counsel, outside accountants and financial advisors

• Access to legal, financial and tax due diligence or disclosure reports prepared by potential insured (under NDA)

• Access to data room

19

Purchasing Process for R&W Insurance• Step Four – Policy Negotiation

• Not all policy terms and conditions are negotiable• Coverage amount: Deal size? Escrow amount?• Policy period: Match survival period? Fundamental

reps?• Premium: How much does policy cost? Who pays?• Deductible/Retention: Amount? [Typically 2% buy-

side, 1% deductible and 1% paid by Seller] – Eroded by non-covered losses?

20

14

Purchasing Process for R&W Insurance• Step Four – Policy Negotiation (cont’d)

• Definitions: Actual Knowledge, Breach, Claim, Loss, Reps and Warranties

– Minimize insurer’s ability to challenge at time of claim whether insured representations and warranties were adequately disclosed at time of underwriting

• Materiality Scrape: Follow contract?• Dispute Resolution

– Arbitration? Choice of law? – Involve litigation lawyer

21

Purchasing Process for R&W Insurance• Step Four – Policy Negotiation (cont’d)

• Subrogation: Against Sellers “for criminal, deliberately dishonest or fraudulent act, statement or omission.” Defeat “clean exit” purpose of insurance? Frustrate later settlement w/seller?

• Parties’ agreement is reflected in binder– Binding cover is commonly a condition of closing– Issues if there is a gap between signing and closing

22

15

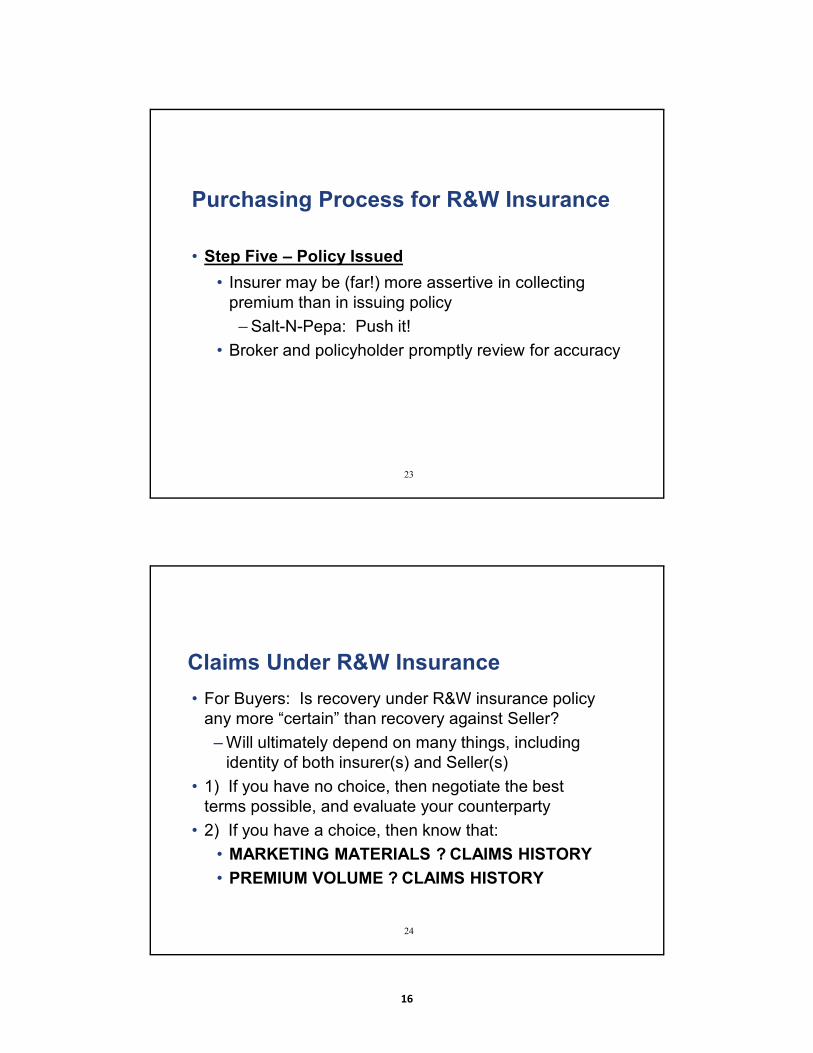

Purchasing Process for R&W Insurance

• Step Five – Policy Issued• Insurer may be (far!) more assertive in collecting

premium than in issuing policy– Salt-N-Pepa: Push it!

• Broker and policyholder promptly review for accuracy

23

Claims Under R&W Insurance• For Buyers: Is recovery under R&W insurance policy

any more “certain” than recovery against Seller?– Will ultimately depend on many things, including

identity of both insurer(s) and Seller(s)• 1) If you have no choice, then negotiate the best

terms possible, and evaluate your counterparty• 2) If you have a choice, then know that:

• MARKETING MATERIALS ? CLAIMS HISTORY• PREMIUM VOLUME ? CLAIMS HISTORY

24

16

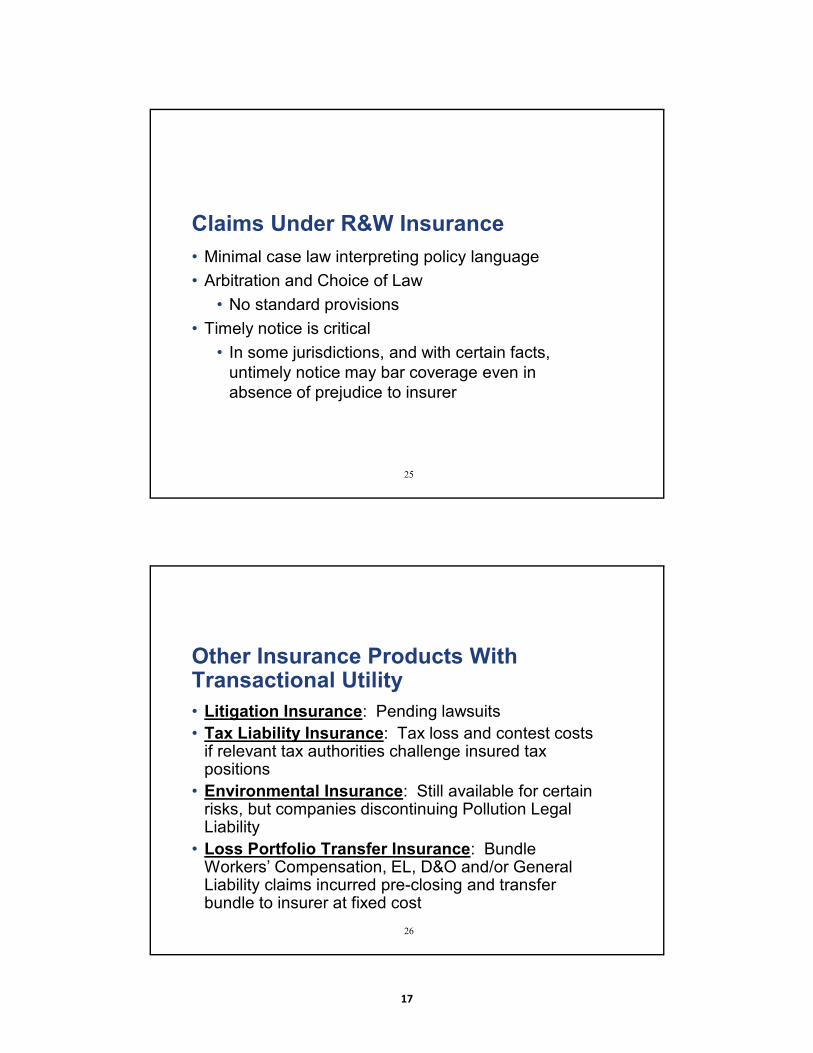

Claims Under R&W Insurance• Minimal case law interpreting policy language• Arbitration and Choice of Law

• No standard provisions• Timely notice is critical

• In some jurisdictions, and with certain facts, untimely notice may bar coverage even in absence of prejudice to insurer

25

Other Insurance Products With Transactional Utility• Litigation Insurance: Pending lawsuits• Tax Liability Insurance: Tax loss and contest costs

if relevant tax authorities challenge insured tax positions

• Environmental Insurance: Still available for certain risks, but companies discontinuing Pollution Legal Liability

• Loss Portfolio Transfer Insurance: Bundle Workers’ Compensation, EL, D&O and/or General Liability claims incurred pre-closing and transfer bundle to insurer at fixed cost

26

17

Thank you!

27

• Questions?

• This presentation should not be considered or construed as legal advice on any individual matter or circumstance. The contents of this document are intended for general information purposes only and may not be quoted or referred to in any other presentation, publication or proceeding without the prior written consent of Jones Day, which may be given or withheld at Jones Day's discretion. The distribution of this presentation or its content is not intended to create, and receipt of it does not constitute, an attorney-client relationship. The views set forth herein are the personal views of the author and do not necessarily reflect those of Jones Day.

1500819400v2

18

H5. IT’S A MAD WORLD: DUE DILIGENCE AND REPS AND WARRANTIES INSURANCE

Rating scale for all questions:

4 = Excellent 3 = Very Good 2 = Average 1 = Somewhat Disappointing 0 = Very Disappointing

Overall rating for this workshop? 4 3 2 1 0 Bernard P. Bell Preparation and quality of information 4 3 2 1 0

Energy and enthusiasm of delivery 4 3 2 1 0

Educational focus (not a sales pitch) 4 3 2 1 0

Comments: _____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

_____________________________________________________________________________________________

To enter the drawing for a cash prize, affix your personal bar code label here or complete this evaluation online.