three essays on an emerging financial market

TRANSCRIPT

Clemson UniversityTigerPrints

All Dissertations Dissertations

5-2018

Three Essays on an Emerging Financial MarketYuekai ChengClemson University, [email protected]

Follow this and additional works at: https://tigerprints.clemson.edu/all_dissertations

This Dissertation is brought to you for free and open access by the Dissertations at TigerPrints. It has been accepted for inclusion in All Dissertations byan authorized administrator of TigerPrints. For more information, please contact [email protected].

Recommended CitationCheng, Yuekai, "Three Essays on an Emerging Financial Market" (2018). All Dissertations. 2160.https://tigerprints.clemson.edu/all_dissertations/2160

Three Essays on an Emerging Financial Market

A DissertationPresented to

the Graduate School of Clemson University

In Partial Fulfillmentof the Requirements for the Degree

Doctor of PhilosophyEconomics

Accepted by:Dr. Gerald P. Dwyer, Jr., Committee Chair

Dr. Michal M. JerzmanowskiDr. Sergey MityakovDr. Robert F. Tamura

byYuekai Cheng

May 2018

Abstract

This dissertation examines the impact of retail trading, price limit rule and market

opening on the Chinese stock market. The Chinese stock market is the second largest

in the world based on market capital. In addition, it has a daily average turnover

eight times of the US stock market. It also has a price limit rule which limits its

daily fluctuation. Furthermore, retail investors play an important role in the Chinese

stock market, meaning its investor structure is different from that of developed stock

markets.

In the first chapter, I explore the impact of the breadth of ownership on stock

returns and turnovers in the Chinese A share market. Using data in the period of

2002-2017, I find that firms with a higher breadth of ownership and a higher change

in the breadth of ownership have lower returns and higher average daily turnovers

in the subsequent quarter. Furthermore, firms with a higher breadth of ownership

have a stronger reversal effect in returns and a stronger negative relationship be-

tween turnovers and subsequent returns. Moreover, adding the breadth and the

change of breadth factors to a six-factor model improves the explanatory power of

excess returns, this improvement is mainly provided by the change of breadth factor.

These findings are consistent with the hypothesis that retail investors are attention-

motivated traders and their trading behavior causes overreaction and mispricing in

the Chinese stock market.

In the second chapter, I explore the impact of the Chinese price limit policy on

ii

long-term stock performance using IPOs on the A share market and HKEx market

from 2006 to 2015. I use a difference-in-differences method to investigate whether

a new IPO policy for the A share market causing consecutive limit-ups on the first

several trading days after the IPO has a long-term effect on stock return, turnover,

volatility and β coefficient. The empirical results are consistent with the hypothesis

that this price limit policy causes the IPO firms on the A share market to have higher

stock returns, turnovers, volatility and β coefficients over a 2-years period after the

IPO.

In the last chapter, I explore the influence of Hong Kong investors on stock returns

and turnovers of stocks involved in the Shanghai-Hong Kong Stock Connect policy.

Using data from 2014-2016 in the Chinese stock market, I find that stocks dual-listed

in Shanghai and Hong Kong have higher monthly stock returns than stocks involved

in the Shanghai-Hong Kong stock connect but listed only in Shanghai; however, the

difference in stock returns between the dual-listed and other Shanghai Hong Kong

stock connect involved stocks decreases gradually. Moreover, stocks dual-listed in

Shanghai and Hong Kong have higher daily average turnovers than stocks involved

in the Shanghai-Hong Kong stock connect but listed only in Shanghai, and the dif-

ference in daily average turnover between dual-listed and other Shanghai-Hong Kong

stock connect involved stocks decreases gradually. These empirical results are consis-

tent with the hypothesis that Hong Kong investors were initially more likely to buy

Shanghai-Hong Kong dual-listed stocks through the stock connect channel; however,

iii

they extended their investment target to stocks involved in the stock connect but

listed only in Shanghai after they gained experience and became familiar with the

Shanghai stock market.

iv

Acknowledgement

I own many more debts than I can possibly acknowledge. I thank my advicer, Gerald

P. Dwyer, Jr., for his guidance on my research and comments on my dissertation.

I also thank my committee members, Michal M. Jerzmanowski, Sergey Mityakov,

Robert F. Tamura, for the comments and advice on my research. Thanks are also

due to Aspen Gorry, whose comments in macro workshop led me to write an essay

on stock market opening. I am grateful to my master advicer, Yao Zheng for his

guidance and support on my research and career development. I thank my teacher,

Xu Weidong for his advice on my research and his help in providing data. I am

grateful to Barbara J. Ramirez for helping me in English writing. I thank my room-

mates, Wu Xiaosong, Zhou Jian and Zou Pengfei, and my classmates, Fan Haobin,

He Qiwei, Tian Chuan, Wang Chen, Wei Qing and Huang Yiheng, who are all my

good friends. Five years study with you are wonderful and unforgettable experience

for me. Thanks also go to my foreign friends, Madeleine Nelson, Jonathan Ernest,

Kelsey Roberts, Leah Kitashima, Smriti Bhargava, Maria Droganova, Richard Sessa

and Corbin Fuller. We have so much fun together. I thank Zhao Liping for every-

thing we have experienced together in the last seven years, including applying for

Economics PhD, doing research, exploring trading strategies, learning programming

languages. Last, certainly not least, I owe more than I can say to the support and

love of my parents.

v

Contents

1 The Breadth of ownership, turnovers and stock returns in the Chi-

nese stock market 1

1.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.2 The Hypotheses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

1.3 The Data and Variables . . . . . . . . . . . . . . . . . . . . . . . . . 11

1.4 Empirical Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

1.4.1 Determinants of the Breadth of Ownership . . . . . . . . . . . 21

1.4.2 Breadth of Ownership and Stock Returns . . . . . . . . . . . . 25

1.4.3 Breadth of Ownership and Turnovers . . . . . . . . . . . . . . 36

1.4.4 Breadth of Ownership and the Reversal Effect . . . . . . . . . 42

1.4.5 Breadth of Ownership and Turnover–Return Relation . . . . . 44

1.4.6 Breadth of ownership and factor model . . . . . . . . . . . . . 46

1.5 Summary and Conclusions . . . . . . . . . . . . . . . . . . . . . . . . 56

1.6 Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

1.6.1 A Model of the Breadth of Ownership, Turnover and Stock

Returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 56

1.6.2 Comparison of the Breadth of Ownership Among Feature Groups 60

1.6.3 Test of Reversal Effect . . . . . . . . . . . . . . . . . . . . . . 63

1.6.4 Test of Turnover–Return Relationship . . . . . . . . . . . . . . 65

vi

2 Price Limit Rule and Long-term Performance of IPO in the Chinese

Stock Market 67

2.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 67

2.2 the Hypothesis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 70

2.3 The Data and Variables . . . . . . . . . . . . . . . . . . . . . . . . . 72

2.4 Long-Term Performance of the IPO . . . . . . . . . . . . . . . . . . . 83

2.4.1 Performance by month . . . . . . . . . . . . . . . . . . . . . . 83

2.4.2 Long-term performance by IPO year . . . . . . . . . . . . . . 103

2.4.3 Regression Analysis . . . . . . . . . . . . . . . . . . . . . . . . 112

2.5 Summary and Conclusions . . . . . . . . . . . . . . . . . . . . . . . . 123

3 Do Investors Invest in Familiarity? Evidence from the Shanghai-

Hong Kong Stock Connect 125

3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 125

3.2 the Hypotheses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

3.3 The Data and Variables . . . . . . . . . . . . . . . . . . . . . . . . . 130

3.4 Empirical Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 137

3.5 Summary and Conclusions . . . . . . . . . . . . . . . . . . . . . . . . 147

vii

List of Tables

1 Descriptive Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

2 Correlation Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

3 Determinants of Breadth of Ownership . . . . . . . . . . . . . . . . . 23

4 Return Comparison for Stocks with Different Breadth of Ownerships 29

5 Return Comparison for Stocks with Different Change of Breadth of

Ownership . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

6 Regression Results of Subsequent Returns on Breadth of Ownership . 34

7 Turnover Comparison for Stocks with Different Breadth of Ownership 37

8 Regression Results of Subsequent Turnovers on Breadth of Ownership 40

9 Reversal Effect, Turnover-Return Relation and Breadth of Ownership 43

10 Descriptive Statistics and Correlation Analysis of Factors . . . . . . . 48

11 Regression of Factors on Other Factors (Equally Weighted Factor Re-

turns) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

12 Regression of Factors on Other Factors (Value Weighted Factor Returns) 50

13 Test of Factor Models . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

14 Test of Factor Models . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

15 Comparison of Breadth of Ownership for Different Feature Groups . . 61

16 Comparison of Change of Breadth of Ownership for Different Feature

Groups . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

17 Return Comparison for Stocks with Different Current Returns . . . . 64

viii

18 Return Comparison for Stocks with Different Current Turnovers . . . 65

19 The Distribution of Sectors for the IPO firms . . . . . . . . . . . . . 73

20 Descriptive Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . 75

21 Long term performance of IPO . . . . . . . . . . . . . . . . . . . . . 80

22 Mean of cumulative abnormal return after IPO (Composite index) . . 84

23 Median of cumulative abnormal return after IPO (Composite index) . 86

24 Mean of cumulative abnormal return after IPO (SmallCap index) . . 87

25 Median of cumulative abnormal return after IPO (SmallCap index) . 89

26 Mean of adjusted turnover after IPO (Composite index) . . . . . . . . 91

27 Median of adjusted turnover after IPO (Composite index) . . . . . . 93

28 Mean of adjusted volatility after IPO (Composite index) . . . . . . . 95

29 Median of adjusted volatility after IPO (Composite index) . . . . . . 98

30 Mean of adjusted volatility after IPO (SmallCap index) . . . . . . . . 100

31 Median of adjusted volatility after IPO (SmallCap index) . . . . . . . 101

32 Two-year cumulative adjusted stock return after the IPO (Composite

index) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 103

33 Two year cumulative adjusted stock return after IPO (SmallCap index) 105

34 Two year average adjusted daily turnover after IPO (Composite index) 106

35 Two year adjusted daily volatility after IPO (Composite index) . . . 107

36 Two year adjusted daily volatility after IPO (SmallCap index) . . . . 108

37 Two year β coefficient after IPO (Composite index) . . . . . . . . . . 109

ix

38 Two year β coefficient after IPO (SmallCap index) . . . . . . . . . . 111

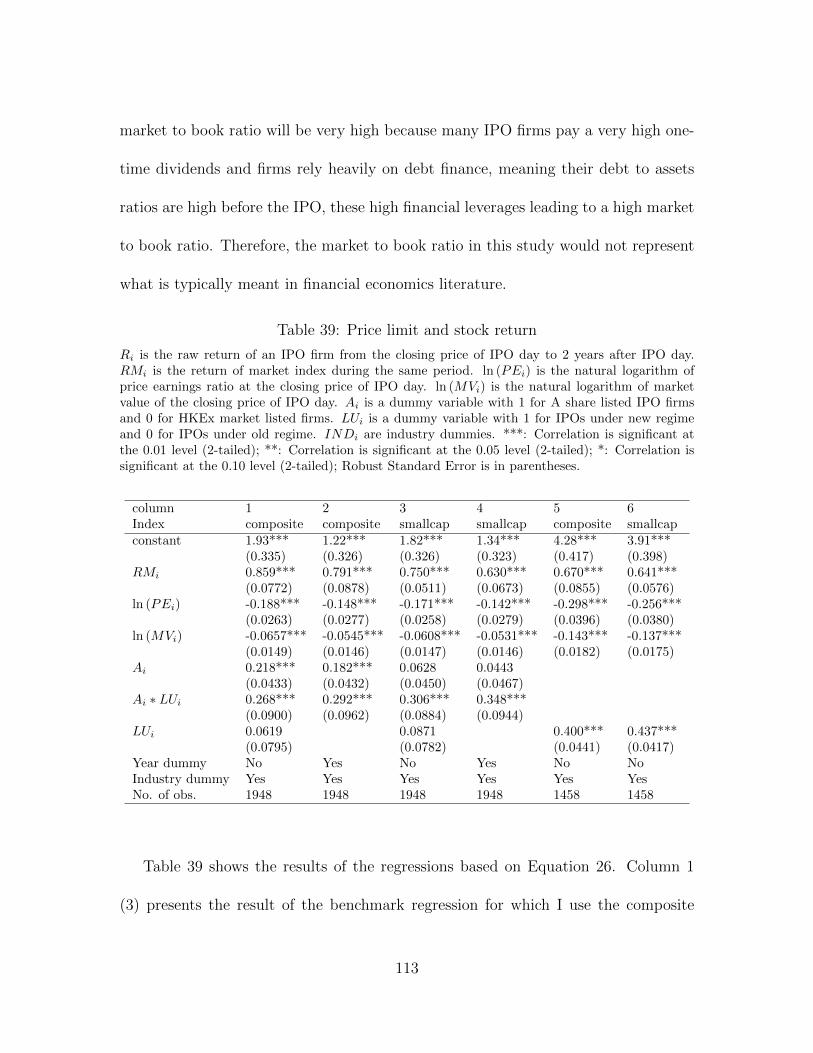

39 Price limit and stock return . . . . . . . . . . . . . . . . . . . . . . . 113

40 Price limit and β coefficient . . . . . . . . . . . . . . . . . . . . . . . 116

41 Price limit and daily volatility . . . . . . . . . . . . . . . . . . . . . . 118

42 Price limit and daily turnover . . . . . . . . . . . . . . . . . . . . . . 121

43 Descriptive Statistics Before Winsorizing . . . . . . . . . . . . . . . . 134

44 Descriptive Statistics After Winsorizing . . . . . . . . . . . . . . . . . 136

45 Impact of Shanghai Hong Kong Stock Connect on Stock Returns and

Turnovers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 138

46 Mean of monthly returns after enactment of Shanghai Hong Kong

Stock Connect . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 142

47 Mean of 5 month returns after enactment of Shanghai Hong Kong

Stock Connect . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 144

48 Mean of monthly turnovers after enactment of Shanghai Hong Kong

Stock Connect . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 146

49 Mean of 5 month turnovers after enactment of Shanghai Hong Kong

Stock Connect . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 148

x

List of Figures

1 Mean of cumulative abnormal return after IPO (Composite index) . . 83

2 Median of cumulative abnormal return after IPO (Composite index) . 85

3 Mean of cumulative abnormal return after IPO (SmallCap index) . . 88

4 Median of cumulative abnormal return after IPO (SmallCap index) . 88

5 Mean of adjusted turnover after IPO (Composite index) . . . . . . . . 90

6 Median of adjusted turnover after IPO (Composite index) . . . . . . 94

7 Mean of adjusted volatility after IPO (Composite index) . . . . . . . 96

8 Median of adjusted volatility after IPO (Composite index) . . . . . . 99

9 Mean of adjusted volatility after IPO (SmallCap index) . . . . . . . . 99

10 Median of adjusted volatility after IPO (SmallCap index) . . . . . . . 102

11 Two year cumulative adjusted stock return after IPO (Composite index)103

12 Two year cumulative adjusted stock return after IPO (SmallCap index) 104

13 Two year average adjusted daily turnover after IPO (Composite index) 105

14 Two year adjusted daily volatility after IPO (Composite index) . . . 107

15 Two year adjusted daily volatility after IPO (SmallCap index) . . . . 109

16 Two year β coefficient after IPO (Composite index) . . . . . . . . . . 110

17 Two year β coefficient after IPO (SmallCap index) . . . . . . . . . . 111

18 Mean of monthly returns after enactment of Shanghai Hong Kong

Stock Connect . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 143

xi

19 Mean of 5 month returns after enactment of Shanghai Hong Kong

Stock Connect . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 144

20 Mean of monthly turnovers after enactment of Shanghai Hong Kong

Stock Connect . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 147

21 Mean of 5 month turnovers after enactment of Shanghai Hong Kong

Stock Connect . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 148

xii

1 The Breadth of ownership, turnovers and stock

returns in the Chinese stock market

1.1 Introduction

An emerging market, the Chinese stock market is the second largest in the world

based on its market value, with a transaction volume in 2015 38% of the total volume

of the world stock market. From December 1990, the day the Chinese stock market

was founded, to November 2017, the Shanghai Composite index increased by 3271%,

and the average annual return is 13.98%. During the same period, the Dow Jones

Industry Average increased by 795%, with an average annual return of 8.50%. The

daily average turnover of the Chinese stock market is about 8 times of the US stock

market.

An important reason that the Chinese stock market has different patterns in stock

returns and turnovers than the developed markets is the high fraction of retail traders

in the Chinese stock market. In contrast to developed markets in which institutional

investors play a major role, the Chinese stock market is significantly affected by the

behavior of retail investors. For example, at the end of the third quarter of 2014,

households and institutional investors, held 33% and 44%, respectively, of the shares

in the US stock market, while at the end of the third quarter of 2015 in the Chinese

A share market, by contrast, retail investors and institutional investors held 42% and

7%, respectively, of the tradable shares.

In this paper, I explore the impact of the breadth of ownership (the number of

1

shareholders per 1 million Chinese Yuan of market value) and the change of the

breadth of ownership (the quarterly percentage change of the number of sharehold-

ers) on stock returns and turnovers, obtaining implications of the asset pricing in the

Chinese stock market. Using data from the period 2002-2017, I find that firms with a

higher breadth of ownership and a higher percentage change of the breadth of owner-

ship have lower returns and higher average daily turnovers in the subsequent quarter.

Furthermore, firms with a higher breadth of ownership have a stronger reversal effect

in returns and a stronger negative relationship between turnovers and subsequent re-

turns. Moreover, adding the breadth and the change of breadth factors to a six-factor

model improves the explanatory power of excess returns, this improvement mainly

being provided by the change of breadth factor. These findings are consistent with

the hypothesis that retail investors are attention-motivated traders and their trading

behavior results in overreactions and mispricings in the Chinese stock market.

Factor pricing models assume that the stock market is efficient, so stock returns

covary with factors which proxy for common risks. After both Sharpe (1964) and

Lintner (1965) found that excess market return is a factor in asset pricing, addi-

tional research found book to market equity ratio and size (Fama and French, 1993),

momentum (Carhart, 1994), liquidity (Pastor, Stambaugh, 2003), investment and

profitability (Hou, Xue, and Zhang, 2012; Fama and French, 2015) were documented

as new pricing factors.

The impact of retail trading, which leads to market inefficiency, is ignored in

2

the traditional assets pricing models. Empirical evidence in this paper shows that

adding two factors mimicking portfolios formed by the breadth of ownership and

the change of the breadth of ownership to a six-factor model (Fama, French five

factors and momentum factor) improves the explanatory power of excess returns, an

improvement primarily provided by the change of breadth factor.

Currently, research is simultaneously identifying new factors and discovering anoma-

lies. While size (Banz, 1981), price earnings ratio (Basu, 1977), leverage (Bhandari,

1988), book market ratio (Fama and French, 1992), profitability (Novy-Marx, 2013)

and cash flow (Sloan, 1996) have been proposed as anomalies that challenge the

CAPM and other factor models, there is evidence that improved multi-factor models

can explain these characteristics (Fama and French,1996; Fama and French, 2016).

In this paper, I find that firms with a higher breadth of ownership and a higher

change of the breadth of ownership have lower subsequent returns after controlling

for other firm characteristics for cross-sectional stock returns, and the influence of

the breadth of ownership and the change of the breadth of ownership on future stock

returns cannot be explained by a six-factor model including Fama and French’s five

factors and the momentum factor.

The interplay between market factors and anomalies reflects the inconsistent re-

sults found for market efficiency. There is evidence that factors like book market ratio

(Chen, 2017) cannot proxy for common risk, meaning stock returns reflect firms’ dif-

ferent characteristics (Daniel and Titman, 1997). Additionally, behavioral factors,

3

for instance, irrational expectations (Lakonishok, Shleifer and Vishny, 1994; Brun-

nermeier and Nagel, 2004; Kogan, Ross, Wang and Westerfield, 2006), institutional

trading behavior (O’Brien and Bhushan, 1990; Keim and Madhavan, 1995; Sias and

Starks, 1997; Hotchkiss and Strickland, 2003; Sias, Starks and Titman, 2006), asym-

metric information (Meulbroek, 1992, Coval and Moskowitz, 1999), sentiment (Baker

and Wurgler, 2006; Baker and Wurgler, 2007; Tetlock, 2007), difference in opinion

(Yu, 2001; Diether, Malloy and Scherbina, 2002), and institution factors such as the

short sale constraint (Miller, 1977; Asquith, Patak and Ritter, 2005; Nagel, 2005;

Boehmer, Huszar and Jordan, 2010) are linked to stock returns.

To be specific, there is much research on the behavior of retail investors. Retail

investor ownership (Brandt, Brav, Graham and Kumar, 2010), sentiment (Kaniel,

Saar and Titman, 2008), overconfidence (Barber and Odean, 2000), attention (Bar-

ber and Odean, 2008), disposition effect (Shapira and Venezia, 2001) and visibility

(Gervais, Kaniel and Mingelgrin, 2001) have an impact on stock performance and on

the return of the retail investors themselves.

In this paper, I examine the breadth of ownership of retail investors and treat

the breadth of ownership as a proxy for overreaction and, thus, overpricing given

that there is a strong short sale constraint and retail investors play a significant

role in the Chinese stock market. The negative breadth-return relationship is, thus,

consistent with the hypothesis that irrational retail trading causes overreactions and

overpricings, both of which will be corrected in the future.

4

A firm’s visibility to investors measured by advertising expenditures is positively

related with the breadth of ownership of both individual and institutional investors

(Grullon, Kanatas and Weston, 2004). An increase in the breadth of ownership of

individual investors resulting from a reduction in the minimum trading unit improves

liquidity and is positively related with future stock returns (Amihud, Mendelson and

Uno, 1999). There is also contradicting evidence that an increase in the ownership

breadth of retail investors is a signal of overpricing and a predictor of low returns

(Choi, Jin and Yan, 2013).

The breadth of ownership among institutional investors is negatively related with

differences in opinion and a short sale constraint, meaning that the breadth of own-

ership of institutional investors is positively related with future stock returns (Chen,

Hong and Stein, 2002); Choi, Jin and Yan, 2013). However, the breadth of owner-

ship of institutional investors is positively related to investor recognition; therefore,

the breadth of ownership is negatively related with future stock returns (Lehavy and

Sloan, 2008). The compromising view suggests that the relationship between the

ownership breadth of institutional investors and return can be either positive or neg-

ative depending on the relative strength of the two offsetting forces of disagreement

and sentiment (Cen, Lu and Yang, 2013).

There is significant disagreement among the empirical results on the breadth-

return relationship. The results in this paper are consistent with those of Choi, Jin

and Yan (2013) which also use the Chinese stock market for their data.

5

There is a long-term negative relationship (De Bondt and Thaler, 1985) and a

short-term positive relationship (Jegadeesh and Titman, 1993) between current stock

returns and future stock returns. This paper provides evidence that there is a strong

reversal effect on quarterly stock returns, results that are consistent with De Bondt

and Thaler (1985). Furthermore, I find that firms with a higher breadth of ownership

have a stronger reversal effect. A potential explanation for this result is that firms

with higher ownership breadth have higher retail holdings and, thus, more intense

overreactions to news, meaning that there will be a higher correction in the stock

price.

Stock returns and turnovers are determined by the same firm characteristics in

the same direction (Rouwenhorst, 1999), correlate contemporaneously (Morgan, 1976;

Rogalski, 1978) and react to announcements in the same direction (Bamber and

Cheon, 1995). Dispersion of expectations (Comiskey, Walkling and Weeks, 1987),

risk, size, price, trading costs and S&P 500 membership (Lo and Wang, 2000) affect

turnovers.

After controlling for other potential determinants of cross-sectional turnovers, I

find that firms with a higher breadth of ownership and a higher change of the breadth

of ownership have higher average daily turnovers in the subsequent quarter. Firms

with a higher breadth of ownership are more intensively held by retail investors.

Therefore, the positive breadth-turnover relationship indicates that retail investors

have a higher trading frequency.

6

There is a negative relationship between turnovers and subsequent stock returns

(Datar, Naik and Radcliffe, 1998; Hu, 1997), but other evidence such as a positive

relationship (Claessens et al, 1998) and no relationship (Rouwenhorst, 1999) have also

been documented. This paper shows that there is a negative relationship between

turnovers and subsequent stock returns, a finding which consistent with Datar, Naik

and Radcliffe (1998) and Hu (1997). Firms with a higher breadth of ownership have a

stronger negative relationship between returns and prior turnovers, providing evidence

that irrational retail tradings cause higher turnovers and overpricing.

In conclusion, the findings in this paper are consistent with the hypothesis that

retail investors are attention-motivated traders and their trading behavior leads to

overreaction and overpricing in the Chinese stock market.

Section 2 presents the hypothesis, Section 3 the descriptive statistics of the data

and the variables, while Section 4 examines the impact of the breadth of ownership

on stock returns and turnovers, and Section 5 concludes.

1.2 The Hypotheses

This research tests eight hypotheses. Since institutional investors and retail investors

are the major players in the Chinese stock market, their trading behavior has an

impact on stock prices. In this paper, I assume that institutional investors have

an information advantage and better analytical skills than the retail investors. As

they are information-motivated traders, they buy undervalued stocks, holding them

for an extended period of time. As a result, institutional trading can increase the

7

information content in the stock price. In contrast, because retail investors do not

have an information advantage nor sufficient analytical skills, they are attention-

motivated traders, buying popular stocks which they hold for a short period. As a

result, these retail traders add noise to stock prices. These investors create pricing

errors in the market which are corrected by institutional investors. If a firm has a

larger number of retail investors, then the stock price is likely to be overvalued, and

it will see a lower return. Thus, I hypothesize that

H1: The level of the breadth of ownership is negatively related to subsequent stock

returns.

For the purpose of this research, the breadth of ownership is considered as a metric

of the number of retail investors. Since the Chinese stock market is highly short sale

constrained, most investors can only hold long positions. Only a small fraction of

stocks are allowed to be short sold and only investors with more than 500 thousand

Chinese Yuan of assets in their stock accounts can short sell stocks. As a result, the

total market value of short sold stocks is only 0.008% of the total market value of

the Chinese stock market. An increase in the number of retail investors results in

overreaction to good news, meaning the stock becomes overvalued. In contrast, a

decrease in the number of retail investors indicates that shares are flowing from retail

investors to institutional investors, meaning the stock might be undervalued. There-

fore, the prices of overvalued or undervalued stocks will return to the fundamental in

the future due to institutional tradings. Therefore, I hypothesize that

8

H2: The change in the breadth of ownership is negatively correlated to subsequent

stock returns.

If a firm has a large number of retail investors, then the stock tends to overreact

to both good and bad news. Since this overreaction to information will be corrected

in the future, I hypothesize that

H3: The level of the breadth of ownership is positively correlated to the reversal

effect in stock returns.

The trading behavior of retail investors is more speculative than that of institu-

tional investors. Thus, it is likely that institutional investors exhibit longer holding

periods than retail investors. Therefore, the fraction of shares held by retail investors

affects turnover. Hence, I hypothesize that

H4: Stocks with a higher breadth of ownership have higher subsequent turnovers.

Further, because retail trading is motivated by the attention to popular stocks,

these investors tend to sell their holdings quickly. Consequently, an increase in retail

holdings causes pressure on future stock prices. In contrast, institutional trading is

based on information, and institutional investors often change their positions gradu-

ally, holding them for a long time. Because the increase in institutional holdings is

indicative of less selling pressure and more buying pressure in the future, I hypothesize

that

H5: Stocks with a higher change of the breadth of ownership have higher turnovers.

Past research has found a negative relationship between turnovers and subsequent

9

stock returns. Stocks with higher retail holdings are subject to more irrational trad-

ing behavior, and have higher turnovers due to the higher trading frequency of retail

investors than institutional investors. If the negative relationship between turnovers

and subsequent stock returns is primarily driven by overpricing caused by irrational

retail trading, retail holdings will affect the relationship between turnovers and sub-

sequent stock returns. Hence, I hypothesize that

H6: Stocks with a higher breadth of ownership have a stronger negative relation-

ship between turnovers and subsequent stock returns.

In their more recent research, Fama and French (2015) proposed a five-factor

model, with more accurate explanatory power than the three-factor model they pro-

posed earlier. The reason that factor pricing models can explain stock returns is that

pricing factors capture the premium for common risks, and their associated factor

loadings, i.e., the coefficients of the factors capture the exposure of securities to com-

mon risks. If the stock market is efficient, the expected excess return is determined

by the risk exposure and the risk premiums of the pricing factors. If the market is ef-

ficient and the factors include all relevant risks, the intercept of a factor pricing model

is not significantly different from zero. If market is inefficient, then the intercept of a

factor model should be significantly different from zero. The breadth of ownership is

a measurement of retail holdings. If the overreaction caused by retail trading is the

main reason for the market inefficiency in the Chinese stock market, adding factors

related to the breadth of ownership and its change to a factor pricing model may be

10

helpful in explaining excess stock returns and may reduce the intercept of a factor

model. Thus, I hypothesis that

H7: Adding a factor which captures the premium of the breadth of ownership will

lower the intercept of the factor pricing model.

H8: Adding a factor which captures the premium of the change in the breadth of

ownership will lower the intercept of the factor pricing model.

1.3 The Data and Variables

This research used the quarterly data from stocks listed in the Chinese A share stock

market (Shanghai Stock Exchange and Shenzhen Stock Exchange) from the fourth

quarter of 2002 to the second quarter of 2017. The data from the first and second

quarters of 2003 are deleted because of their unavailability for key variables. As a

result, this study includes 85,550 observations from this 57-quarter period. These

data are from the WIND Database, a major reporter of data on the Chinese financial

market.

Since this paper focuses on the Chinese A share market, if a firm is listed on

additional exchanges, key variables such as the number of its shareholders and its

institutional shareholding in the A share market are unavailable. For example, if

a firm has B shares (shares listed in China and traded in foreign currencies), H

shares (shares listed in Hong Kong), and/or S shares (shares listed in Singapore)

in a quarter, the observations from this firm for this quarter are excluded. I also

excluded an observation if a stock was not traded for the entire prior quarter, current

11

quarter, or subsequent quarter for its return and turnover cannot be compared with

the remaining firms. In addition, I deleted observations of stocks with initial public

offerings (IPO) with two years or less because I needed 2 years’ data to compute β

coefficients. According to past research, firms exhibit poor performance for two to

three years after going public (Ritter,1991; Loughran and Ritter, 1995; Teoh, Welch

and Wong, 1998), this deletion, thus, eliminates the IPO impact on stock returns.

Rit is the return for stock i in quarter t. I use quarterly stock returns because the

data of the number of shareholders are released quarterly for most firms. A second

impact on stock returns is the breadth of ownership which is defined as the number

of shareholders in a listed company. However, assuming that the average capital that

retail investors invest in a single company is equal across all listed companies, then

the number of shareholders is proportional to the market value of a listed company

given that the institutional holdings percentage is fixed.

To make the breadth of ownership comparable across firms of different sizes, I

scale the definition of the breadth of ownership as follows:

BR∗it =(SHit

SHt)

(TVitTVt

)(1)

where SHit is the number of shareholders in firm i at the end of quarter t; SHt is

the number of investors in the Chinese stock market at the end of quarter t; TVit is

the market value of tradable shares of firm i at the end of quarter t; and TVt is the

market value of tradable shares in the Chinese stock market. The total number of

12

stock investors in China and the market value of the Chinese stock market as a whole

are fixed at a given time. Because this research uses quarterly cross-sectional data, I

simplify the breadth of ownership of firm i in quarter t using the following formula:

BRit =SHit

TVit(2)

The change in the breadth of ownership of firm i in quarter t CHit is measured

using quarterly percentage change of the number of shareholders:

CHit =SHit

SHit−1− 1 (3)

The size of firm i is measured using the market value of tradable shares, which

is the product of the stock price of firm i, multiplied by the freely tradable shares

of firm i. These freely tradable shares are A shares excluding 1) shares of large

shareholders who own more than 5% of the firm and their related shareholders; 2)

shares of shareholders who own less than 5% of the firm but are related to the large

shareholders or with their related parties hold more than 5% of the firm; 3) 75% of

shares of senior managers who are the top ten shareholders of firm i.

The China Securities Regulatory Commission has strict restrictions on the sale of

shares of major shareholders and insiders. In the A share market, senior managers

and large shareholders can sell only 25% of their shares per year and 1% of the total

equity of a listed company per quarter. And shares of large shareholders are held

for controlling power, not for capital gains or dividend proceeds. These shares have

13

much lower liquidity, meaning the behavior of these large shareholders in the stock

market is different from that of small shareholders including institutional and retail

shareholders.

The institutional holding ISit is the fraction of shares of firm i held by institutional

investors at the end of quarter t. Institutional investors include financial institutions

such as mutual funds, private equity funds, insurance companies, investment banks,

national social security funds, qualified foreign institutional investors and commercial

banks. Non-financial companies are not considered as institutional investors.

Additional variables used in this paper include:

• brit = ln (BRit);

• chit = ln (1 + CHit);

• isit = ln (1 + ISit);

• tvit = ln (TVit);

• CLit is the closing price of firm i at the end of period t;

• clit = ln (CLit); βit is the β coefficient of firm i at the end of quarter t calculated

using monthly returns in the prior 24 months;

• BMit is the book to market ratio at the end of period t; if the book value is

negative, then I assign a very small value for book to market ratio to this firm

which will be winsorized;

14

• bmit = ln (BMit); ROEit is the return on equity of firm i in the recent four

consecutive quarters before quarter t; I use earnings before abnormal terms as

the numerator and the book equity at the end of the period as the denominator

to calculate the return on equity;

• AGit is the year over year percentage growth of total assets for firm i at the end

of the recent quarter before quarter t;

• agit = ln (1 + AGit);

• V Lit is the daily average volatility for firm i in quarter t; the volatility is derived

from the standard deviation of daily stock returns in a quarter;

• TOit is the daily average turnover rate for firm i in quarter t; the turnover is

the ratio of the transaction volume to tradable shares.

The definition of the recent quarter is as follows. For bmit, ROEit, agit, I use

financial data available to investors at the beginning of quarter t if I use the return

of quarter t as the subsequent return. For example, if I use data from the second

quarter of 2017 to calculate the subsequent return, I will use the financial data from

the third quarter report of 2016 to calculate bmit, ROEit, agit. Listed companies are

required to release their annual report for 2016 and the first quarter report for 2017

no later than April 30, 2017.

To avoid the impact of extreme values on the results, I winsorize all the variables

in this paper. For agit,βit, brit, chit, ROEit, Rit, I replace observations in the bottom

15

and top 0.01 quantiles of the variables by the bottom and top 0.01 quantiles value

of the variables, respectively. For bmit, I replace observations in the bottom 0.02

quantile of the variable by the bottom 0.02 quantile value of the variable. For tvit,

clit, isit, TOit, V Lit, I replace observations in the top 0.02 quantiles of the variables

by the top 0.02 quantiles value of the variables. Some variables are winsorized only

in the top or bottom quartiles because extreme values are unlikely to appear in the

other.

Table 1: Descriptive Statistics

CLit is the closing price of firm i at the end of period t; Rit is the return for stock i in quarter t;TVit is the market value of tradable shares of firm i at the end of period t; ISit is the percentage offirm i’s total equity held by institutional investors at the end of quarter t; CHit is percentage changeof the number of shareholders of firm i in quarter t; BRit is the ratio of the number of shareholdersto the market value of tradable shares of firm i at the end of quarter t; ROEit is return on equityof firm i in the recent four consecutive quarters before quarter t; AGit is year over year percentagegrowth of total asset for firm i at the end of recent quarter before quarter t; BMit is the book tomarket equity ratio at the end of period t; βit is the β coefficient of firm i at the end of quarter t;V Lit is the daily average volatility for firm i in quarter t; TOit is the daily average turnover rate forfirm i in quarter t

Variable Min Max Mean Median Std. errorCLit 0.73 386.36 12.12 9.38 11.26

Rit(%) -83.82 638.15 5.94 0.66 29.74TVit (billion cny) 0.021 235.46 3.25 1.90 7.33

ISit(%) 0 67.57 4.37 1.69 6.72CHit(%) -70.68 1456.75 3.17 -1.36 30.55

BRit(per million cny) 0.31 2776.59 28.45 18.21 34.95ROEit(%) -103660.5 651.96 0.99 4.72 486.18AGit(%) -99.98 2530508 19.11 9.75 13865.93

BMit 0.000046 2.17 0.36 0.31 0.24βit -2.61 8.43 1.03 1.03 0.44

V Lit(%) 0.02 50.76 2.85 2.65 1.16TOit(%) 0.0063 279.44 3.46 2.74 3.09

Table 1 presents the descriptive statistics. In order to decrease the impact of

extreme values on the statistics, the means of all variables are calculated with the

16

values obtained after winsorizing, while raw data are used for all other statistics. The

quarterly returns of stocks vary from -83.82% to 638.15%, the mean value is 5.94%

and the median is 0.66%. The stocks in the sample period exhibit good performance

on average though the variation of performances is large. The mean of the market

value of tradable shares is 3.25 billion CNY and the median is 1.90 billion CNY; the

market value of tradable shares vary from 0.021 billion CNY to 235.46 billion CNY.

These statistics indicate that the heterogeneity in size is quite large for Chinese stocks.

The mean of the institutional holding is 4.37% of the total equity while the median

is 1.69%, and the maximum and minimum values are 67.57% and 0, respectively,

indicating that institutional investors hold a very small fraction of the total equity

of companies listed in China. The mean of percentage change of the number of

shareholders is 3.17%, the median is -1.36%, and the maximum and minimum values

are -70.68% and 1456.75%, respectively. The mean and median of the number of

shareholders per million Chinese Yuan of the market value of tradable shares are 28.45

and 18.21, and the maximum and minimum values are 0.31 and 2776.59, respectively.

The breadth of ownership and the change in the breadth of ownership exhibit large

variations in this sample.

Since the purpose of this paper is to explore the cross-sectional variation in stock

returns and turnovers, most of the empirical tests are conducted for each quarter

in the sample period, and then the quarterly average of the results is reported as

the final results for the entire sample period. To examine the correlations among

17

variables, the correlation analysis used here followed the procedure below.

For each quarter in the sample period: (1) I sort the observations equally into five

size groups according to the market value of the tradable shares; (2) I then calculate

the correlation coefficients Rijts between two variables i and j for each size group,

where t denotes the quarter and s denotes the size group; (3) I take equally weighted

averages of the correlation coefficients Rijt for these five size groups as the coefficients

for this quarter, where Rijt = mean(Rijts); (4) I take equally weighted time series

averages of the correlation coefficients Rij for all 57 quarters as the final correlation

coefficients, where Rij = mean(Rijt); (5) I take the time series standard deviation

of the correlation coefficients sd(Rijt) divided by the square root of the number of

quarters in the sample as the standard error of the correlation coefficients se(Rijt),

where se(Rijt) =sd(Rijt)√

57.

The next step invloves conducting a t-test to test the hypothesis that the av-

erage correlation coefficients are zero. If the auto-correlations in the time series of

correlation coefficients are positive (negative), then the standard errors are under-

estimated (overestimated). To adjust the standard errors for the bias caused by

the auto-correlations of the correlation coefficients Rijt, I replace the standard er-

rors by sea(Rijt) = se(Rijt) ∗ Kij as is documented by Fama, French (2002), where

Kij =√

1+ρij1−ρij , and ρij is the estimated one stage auto-correlation coefficients of corre-

lation coefficients Rijt. I conduct the t-test for the correlation coefficients Rij, where

tij = Rij/sea(Rijt) for Rij. However, I do not group observations into size groups

18

before I calculate the correlation coefficient between any variable i and tvit.

Table 2: Correlation Analysis

CLit is the closing price of firm i at the end of period t; clit = ln (CLit); Rit is the return forstock i in quarter t; TVit is the market value of tradable shares of firm i at the end of period t;tvit = ln (TVit); ISit is the percentage of firm i’s total equity held by institutional investors at the endof quarter t;isit = ln (1 + ISit); CHit is percentage change of the number of shareholders of firm i inquarter t;chit = ln (1 + CHit); BRit is the ratio of the number of shareholders to the market valueof tradable shares of firm i at the end of quarter t;brit = ln (BRit); ROEit is return on equity of firmi in the recent four consecutive quarters before quarter t; AGit is year over year percentage growthof total asset for firm i at the end of recent quarter before quarter t;agit = ln (1 +AGit); BMit isthe book to market equity ratio at the end of period t;bmit = ln (BMit); βit is the β coefficient offirm i at the end of quarter t; V Lit is the daily average volatility for firm i in quarter t; TOit is thedaily average turnover rate for firm i in quarter t; ***: Coefficient is significant at the 0.01 level(2-tailed); **: Coefficient is significant at the 0.05 level (2-tailed); *: Coefficient is significant at the0.10 level (2-tailed); Standard errors adjusted for autocorrelation are in parentheses.

Column 1 2 3brit chit Rit+1

chit 0.0399 brit−1 -0.2190*** TOit -0.0870***(0.0267) (0.0138) (0.0114)

isit -0.5167*** isit−1 0.1118*** Rit -0.0488**(0.0518) (0.0165) (0.0193)

bmit 0.3971*** bmit−1 -0.0705*** brit -0.0274(0.0116) (0.0094) (0.0169)

βit 0.2503*** βit−1 -0.0323** chit -0.0717***(0.0452) (0.0129) (0.0106)

tvit -0.4447*** tvit−1 0.0773*** isit 0.0417***(0.0525) (0.0121) (0.0150)

ROEit -0.2083*** ROEit−1 0.0497***(0.0166) (0.0066) TOit+1

agit -0.2054*** agit−1 0.0823*** brit 0.1034*(0.0232) (0.0077) (0.0597)

Rit -0.2120*** Rit−1 0.0650** chit 0.2041***(0.0158) (0.0269) (0.0161)

TOit 0.1156* TOit−1 -0.0023 isit -0.1022**(0.0676) (0.0105) (0.0423)

V Lit -0.0155 V Lit− 1 0.0343*** TOit 0.5976***(0.0508) (0.0111) (0.0150)

clit -0.7439*** clit−1 0.1207*** Rit 0.1295***(0.0194) (0.0162) (0.0280)

Table 2 shows the results of the correlation analysis, with brit being significantly

positively related with bmit and βit, and significantly negatively related with isit, tvit,

ROEit, agit, Rit and clit. Stocks with higher book market ratios and beta coeffi-

19

cients have a higher breadth of ownership, while stocks with smaller sizes, returns

on assets, asset growth rates, and past returns have a higher breadth of ownership.

Retail investors hold stocks with low valuation and low quality, which is defined as a

low growth rate and low profitability. The strong negative relationship between the

breadth of ownership and institutional holdings is not surprising as the breadth of

ownership is an indicator of retail holdings. The negative relationship between the

stock price and the breadth of ownership is attributable to the fact that low price

stocks are more available for retail investors.

The variable chit is significantly positively correlated with isit−1, tvit−1, ROEit−1,

agit−1, Rit−1, V Lit−1, clit−1, and significantly negatively correlated with brit−1, bmit−1,

βit−1. The stocks with higher institutional holdings, larger sizes, higher returns on

assets, higher past returns, higher volatilities, and higher prices have a higher in-

crease in the breadth of ownership in the subsequent quarter. These relationships are

consistent with the hypothesis that retail investors tend to buy stocks with good re-

cent fundamental and technical performances. The negative relationship between the

breadth of ownership and the subsequent change in the breadth of ownership shows a

mean reversion pattern in the breadth of ownership. Stocks with lower book market

ratios and beta coefficients have a higher increase in the breadth of ownership. Retail

investors tend to buy stocks with a higher valuation level and that seem to be less

risky. These results are consistent with the belief that retail investors buy stocks that

seem good and are not cheap.

20

High turnovers, stock returns and change in the breadth of ownership all predict

poor returns in the subsequent quarter, while institutional holdings are positively

correlated with subsequent returns. The relationship between the breadth of own-

ership and subsequent returns is negative but insignificant. High turnovers, stock

returns, breadth of ownership, change in the breadth of ownership all predict larger

subsequent turnovers, while institutional holdings are negatively correlated with sub-

sequent turnovers. These results are consistent with the hypotheses in this paper,

which will be tested further with regression analysis to control for other variables.

1.4 Empirical Results

1.4.1 Determinants of the Breadth of Ownership

Because in this paper, I explore the influence of the breadth of ownership on stock

returns and turnovers, it is worth while to investigate the determinants of the breadth

of ownership. Specifically, I investigate the kinds of stocks that have a higher breadth

of ownership and what determines the change in the breadth of ownership in this

section.

I apply multivariate regressions to investigate the factors determining the breadth

of ownership using two specifications, one for the level of the breadth of ownership,

the other for the change in the breadth of ownership. I take the logarithms for

several variables because they vary largely for different stocks, meaning their standard

deviations also vary. The models are as follows:

21

brit = a0 + a1isit + a2Rit + a3clit + a4βit + a5bmit

+a6V Lit + a7TOit + a8tvit + a9ROEit + a10agit + eit

(4)

chit = a0 + a1brit−1 + a2isit−1 + a3Rit−1 + a4clit−1 + a5βit−1 + a6bmit−1

+a7V Lit−1 + a8TOit−1 + a9tvit−1 + a10ROEit−1 + a11agit−1 + eit

(5)

The variable chit is not included on the right hand side of Equation 4 because

it captures the difference between brit and brit−1. Thus adding chit to the model

will cause an endogenous problem. I use the Fama-MecBeth procedure to run the

cross-sectional regressions for each of the 57 quarters for each of the five size groups

and obtain the final coefficients by averaging the coefficients first by size groups and

then by quarters, using the same sorting and averaging method as for the correlation

analysis. Then, I adjust the standard errors for auto-correlation of the coefficients

using the method proposed in Fama, French (2002) and conduct t-test.

I sort the sample by size for the Fama-MacBeth regressions because the volatilities

of major variables vary with firm size. Simply pooling all observations in a single

Fama-MacBeth regression would cause the coefficients to be identified by firms with

a particular size. Running the Fama-MacBeth regressions for each size quintile and

taking the average of the coefficients prevents the results from being dominated by a

specific size quintile.

Column 1 of Table 3 shows the regression results of the determinants of the level

of the breadth of ownership. As this table shows, the breadth of ownership is sig-

22

Table 3: Determinants of Breadth of Ownership

CLit is the closing price of firm i at the end of period t; clit = ln (CLit); Rit is the return forstock i in quarter t; TVit is the market value of tradable shares of firm i at the end of period t;tvit = ln (TVit); ISit is the percentage of firm i’s total equity held by institutional investors at the endof quarter t;isit = ln (1 + ISit); CHit is percentage change of the number of shareholders of firm i inquarter t;chit = ln (1 + CHit); BRit is the ratio of the number of shareholders to the market valueof tradable shares of firm i at the end of quarter t;brit = ln (BRit); ROEit is return on equity of firmi in the recent four consecutive quarters before quarter t; AGit is year over year percentage growthof total asset for firm i at the end of recent quarter before quarter t;agit = ln (1 +AGit); BMit isthe book to market equity ratio at the end of period t;bmit = ln (BMit); βit is the β coefficient offirm i at the end of quarter t; V Lit is the daily average volatility for firm i in quarter t; TOit is thedaily average turnover rate for firm i in quarter t; ***: Coefficient is significant at the 0.01 level(2-tailed); **: Coefficient is significant at the 0.05 level (2-tailed); *: Coefficient is significant at the0.10 level (2-tailed); Standard errors adjusted for autocorrelation are in parentheses.

Column 1 2Dependent brit chitconstant -6.547*** constant -1.827***

(0.344) (0.315)brit−1 -0.090***

(0.015)isit -3.424*** isit−1 0.009

(0.629) (0.062)Rit -0.271*** Rit−1 0.027

(0.099) (0.021)clit -0.728*** clit−1 -0.050***

(0.022) (0.012)βit 0.170*** βit−1 0.012**

(0.062) (0.005)bmit 0.146*** bmit−1 -0.003

(0.049) (0.004)V Lit -2.910 V Lit−1 -0.209

(2.244) (0.176)TOit 6.139*** TOit−1 0.369***

(2.710) (0.108)tvit -0.116*** tvit−1 0.044***

(0.010) (0.013)ROEit -0.171*** ROEit−1 -0.008

(0.065) (0.006)agit -0.094*** agit−1 0.036***

(0.036) (0.005)

23

nificantly and negatively related with institutional holdings. A larger proportion of

the stocks with a higher breadth of ownership are held by retail investors, meaning

institutional investors hold a smaller proportion of the total equity. Stocks with a

poor performance have a higher breadth of ownership, indicating that retail investors

tend to hold such stocks. Stocks with lower prices have a higher breadth of ownership

as they are more available to retail investors. Stocks with higher β coefficients have

a higher breadth of ownership. If the β coefficient is an indicator of risk, then retail

investors hold stocks with higher risks. Stocks with a higher book market ratio have

a higher breadth of ownership. Retail investors hold these stocks which are cheap

but may have higher risks. Stocks with higher turnovers have a higher breadth of

ownership, consistent with the hypothesis that retail investors have a higher trad-

ing frequency and prefer stocks with higher trading volumes. Stocks from smaller

firms and with lower profitabilities and lower growth rates have a higher breadth of

ownership. These stocks seem to have a poor business performance.

These results show that retail investors hold stocks with lower valuations, higher

risks, and poorer business and stock market performances, consistent with the hy-

pothesis that retail investors do not use value strategies. The stocks typically held by

retail investors exhibit poor performances but have high turnovers, indicating that

retail investors lose money in the stock market though they trade frequently.

Column 2 of Table 3 shows the result of the determinants of the change in the

breadth of ownership. Stocks with a higher breadth of ownership tend to see a

24

decrease in the breadth of ownership in the subsequent quarter, reflecting a mean

reversion in the breadth of ownership. Stocks with lower prices, higher β coefficients,

higher turnover, larger firm sizes and higher growth rates have a higher change in

the breadth of ownership in the subsequent quarter. These features capture the

attention of retail investors who do not consider profitability in their stock purchases.

Though retail investors will buy stocks with lower prices, a higher book market ratio

is attractive to them.

Column 1 of Table 3 shows the features of stocks typically held by retail investors,

while Column 2 of Table 3 shows the features of stocks that will increase the position

of retail investors in the next quarter. Results in Table 3 provide evidence that

retail investors do not use value strategies as they hold stocks with poor qualities,

low valuations and high risks, and they buy stocks that look attractive but are not

particularly profitable or cheap. For these reasons, though retail investors trade

frequently, they do not see a profit from their investment.

1.4.2 Breadth of Ownership and Stock Returns

The breadth of ownership of a company is primarily determined by its number of retail

investors. To explore the impact of the behavior of these investors on subsequent stock

returns, I compare stock returns in the next quarter among stocks with different levels

of the breadth of ownership brit at the end of the current quarter using the following

procedure.

For each quarter t in the sample period: (1) I sort the observations equally into

25

five size groups according to the market value of tradable shares; (2) in each size

group, I sort the observations equally into five subgroups according to the breadth of

ownership brit at the end of quarter t, so that each stock belongs to a size group and a

breadth group; thus stocks are split into 25 groups; (3) for each group, I calculate the

equally weighted average of Rst+1 as the subsequent stock return of this group, where s

denotes size quintiles, and Rst+1 = mean(Rist+1); (4) for each breadth quintile, I take

the equally weighted average stock returnRt+1 of the five size groups as the subsequent

stock return of this breadth quintile in quarter t, where Rt+1 = mean(Rst+1); (5) I

take the equally weighted time series average of stock return R for all 57 quarters

as the subsequent stock return of this breadth quintile, where R = mean(Rt+1); (6)I

calculate the difference between subsequent stock returns R of high and low breadth

quintiles.

To test whether the results from this test are robust after considering the assets

pricing factors, I run a time series regression of excess quarterly returns REt on

RMEt, SMBt, HMLt, MOMt, RMWt and CMAt for each breadth of ownership

category, obtaining intercept a0 as the abnormal return after 6 factors:

REt = a0+a1RMEt+a2SMBt+a3HMLt+a4MOMt+a5RMWt+a6CMAt+et (6)

where

• REt = Rt − RFt; Rt is the equally weighted average return of firms in a group

in quarter t and RFt is the three-month risk-free rate divided by four. I use the

26

benchmark deposit rate set by the People’s Bank of China.

• The market excess return RMEt = RMt − RFt; RMt is the equally weighted

average return of all stocks in the sample in quarter t.

• SMBt is the difference in the equally weighted average returns between the

small stock group and the large stock group; the former includes stocks with

the market value of tradable shares below the 0.3 quantile at the end of quarter

t-1, while the large stock group includes stocks with the market value of tradable

shares above the 0.7 quantile at the end of quarter t-1.

• HMLt is the difference in equally weighted average returns between the high

book to market equity ratio (B/M) stock group and the low B/M stock group;

the high B/M stock group includes stocks with the B/M above the 0.7 quantile

at the end of quarter t-1, while the low B/M stock group includes stocks with

the B/M below the 0.3 quantile at the end of quarter t-1;

• MOMt is the difference in equally weighted average returns between the strong

stock group and the weak stock group; the strong stock group includes stocks

with the returns above the 0.7 quantile in quarter t-1, and the weak stock group

includes stocks with the returns below the 0.3 quantile in quarter t-1.

• RMWt is the difference in equally weighted average returns between the robust

profitability stock group and the weak profitability stock group; the robust

profitability stock group includes stocks with the return on equity in the recent

27

four consecutive quarters above the 0.7 quantile in quarter t-1, and the weak

profitability stock group includes stocks with the return on equity below the 0.3

quantile in quarter t-1.

• CMAt is the difference in equally weighted average returns between the con-

servative investment stock group and the aggressive investment stock group;

the conservative investment stock group includes stocks with a year-over-year

growth of the total asset at the end of recent quarter below the 0.3 quantile in

quarter t-1, and the aggressive investment stock group includes stocks with the

growth of total assets above the 0.7 quantile in quarter t-1.

I also calculate the difference of quarterly raw returns of the high and low breadth

of ownership quintiles, obtaining abnormal returns after 6 factors of the return dif-

ference through regression of Equation 6.

To ensure my results are robust, I exclude the profitability factor and the invest-

ment factor from Equation 6 and followed the same procedure to obtain the abnormal

returns after 4 factors including comparing them among the breadth of ownership

quantiles. In addition, I use the value weighted return to calculate the stock returns

and factor returns and then repeat the tests. Table 4 reports the subsequent stock

returns for different breadth of ownership groups.

For both value weighted returns and equally weighted returns, with an increase

in the breadth of ownership, the subsequent stock returns decrease with the stocks

in the highest breadth of ownership quintile having lower subsequent stock returns

28

Table 4: Return Comparison for Stocks with Different Breadth of Ownerships

In Panel A and B, Columns 1-5 present equally weighted and value weighted average raw returnsand abnormal returns after 3 and 6 factors in quintiles of BRit; in Panel C, Columns 1-5 present theresiduals of regressing Rit+1 on the variables on the right side excluding brit; Column 6 shows thedifference between the lowest and highest quintiles; Rit is the return for stock i in quarter t; BRit

is the ratio of the number of shareholders to the market value of tradable shares of firm i at the endof quarter t;brit = ln (BRit).

column 1 2 3 4 5 6Rit+1 brit Low 2 3 4 High Low-High

Panel AEqual W. Raw 0.0611 0.0557 0.0528 0.0515 0.0535 0.0076

3 Factors 0.021 0.006 -0.005 -0.009 -0.014 0.035***6 Factors 0.015 -0.001 -0.010 -0.009 -0.004 0.019***

Panel BValue W. Raw 0.0592 0.0543 0.0515 0.0504 0.0526 0.0065

3 Factors 0.014 0.007 -0.007 -0.010 -0.014 0.028***6 Factors 0.015 0.005 -0.006 -0.006 -0.004 0.019***

Panel CResidual Equal W. 0.0052 0.0017 0.0001 -0.0032 -0.0038 0.0089***

Value W. 0.0045 0.0016 0.0001 -0.0034 -0.0039 0.0082***

*** indicates the coefficient is significant at the 0.01 level (2-tailed).

than the lowest breadth quintile. The results for abnormal returns after both four

factors and six factors are significant at the 1% level. For example, the value weighted

quarterly abnormal stock return after 6 factors of the highest breadth quintile is 1.9%

lower than that of the lowest breadth quintile. These empirical results indicate that

the level of breadth of ownership has an impact on subsequent stock returns, results

support Hypothesis 1.

To test Hypothesis 2, I compare subsequent stock returns among different change

of breadth of ownership groups using the same method as comparing subsequent

returns with different level of breadth of ownership groups. The results can be seen

in Table 5.

29

Table 5: Return Comparison for Stocks with Different Change of Breadth of Owner-ship

In Panel A and B, Columns 1-5 present equally weighted and value weighted average raw returnand abnormal return after 3 and 6 factors in quintiles of CHit; in Panel C, Columns 1-5 presentthe residuals of regressing Rit+1 on the variables on the right side excluding chit; Column 6 showsthe different between lowest and highest quintiles; Rit is the return for stock i in quarter t; CHit ispercentage change of the number of shareholders of firm i in quarter t;chit = ln (1 + CHit).

Column 1 2 3 4 5 6Rit+1 chit Low 2 3 4 High Low-High

Panel AEqual W. Raw 0.0680 0.0658 0.0574 0.0469 0.0367 0.0313***

3 Factors 0.023 0.009 -0.003 -0.013 -0.018 0.041***6 Factors 0.025 0.013 -0.001 -0.014 -0.031 0.056***

Panel BValue W. Raw 0.0668 0.0647 0.0555 0.0464 0.0354 0.0313***

3 Factors 0.019 0.007 -0.003 -0.013 -0.021 0.040***6 Factors 0.026 0.014 -0.002 -0.010 -0.026 0.052***

Panel CResidual Equal W. 0.0112 0.0075 -0.0011 -0.0075 -0.0100 0.0208***

Value W. 0.0108 0.0073 -0.0010 -0.0077 -0.0103 0.0206***

*** indicates the coefficient is significant at the 0.01 level (2-tailed).

For both value weighted returns and equally weighted returns, with the increase

in the change in the breadth of ownership, the subsequent stock returns decrease,

with stocks in the highest change in breadth quintile having lower subsequent returns

than the lowest change of breadth quintile. The results for raw returns and abnormal

returns after both four factors and six factors are significant at the 1% level. For

example, the value weighted quarterly abnormal stock return after six factors of the

highest change of breadth quintile is 5.2% lower than that of the lowest change of

breadth quintile. These results are consistent with Hypothesis 2.

To control for the impact of factors other than breadth of ownership on stock

returns, I run a Fama-MacBeth cross-sectional multivariate regression to explore the

30

relationship between future stock returns and breadth of ownership.

For the control variables, Rit−1 is used to control for the momentum or reversal

effect. The increase in breadth of ownership is a result of higher retail holdings that

is often accompanied by lower institutional holdings. This change in institutional

holdings can influence stock returns through the corporate governance channel be-

cause institutional investors have a higher motivation and more ability to monitor

the managers. To control for this effect, I add isit to the model. Stocks with lower

prices are more available for retail investors so that they may have a higher number

of shareholders given the same market value of tradable shares. Controlling clit leads

to the breadth of ownership becoming more comparable among stocks with different

prices. To control for this size effect, tvit is added to the model. The five factors in the

pricing model proposed by Fama and French (2015) are represented by the variables

βit, bmit, tvit, ROEit, agit. V Lit and TOit are added to control for the impact of past

volatility and volume on future stock returns, while eit is the error term. First, I run

Equation 7 for each quarter for each of the five size groups to obtain the residuals for

each observation; both brit and chit are not included as right side variables.

Rit+1 = a0 + a1isit + a2Rit + a3clit + a4βit + a5bmit

+a6V Lit + a7TOit + a8tvit + a9ROEit + a10agit + eit

(7)

In each quarter for each size group, I sort observations further into five breadth

of ownership groups based on brit, and calculate equally weighted and value weighted

averages of the residuals rtsb for each breadth group, where t denotes quarter, s denotes

31

size, and b denotes breadth. Then I calculate the equally weighted average by size and

then by quarter to obtain rb, the average residual of a breadth group; these results are

presented in Table 4. The average residual changes from positive to negative as the

breadth of ownership changes from the smallest to the largest quintile, indicating a

variation in stock returns related to breadth of ownership remains unexplained. These

results support the hypothesis that a higher breadth of ownership predicts lower stock

returns.

Then for each size group in each quarter, I sort the observations into five change

in the breadth of ownership groups according to chit and repeat the above procedure

to test how residuals change with a change in the breadth of ownership; These results

are reported in Table 5. The average residual changes from positive to negative when

the change in breadth increases from the smallest to the largest quintile, indicating a

variation in stock returns related to the change in the breadth of ownership which is

unexplained. These results are consistent with the hypothesis that a higher change

in the breadth of ownership predicts lower stock returns. Then I use Equation 8 as

baseline model to examine the impact of breadth of ownership on stock returns.

Rit+1 = a0 + a1chit + a2brit + a3isit + a4Rit + a5clit + a6βit + a7bmit

+a8V Lit + a9TOit + a10tvit + a11ROEit + a12agit + eit

(8)

Because of the high correlations between brit and chit, brit and isit, isit and the

control variables, I use several alternative specifications in addition to the baseline

regression. I use the same Fama-MacBeth procedure as I used to run the regression of

32

determinants of the breadth of ownership; Table 3 shows these results. The coefficients

a1 and a2 are significant at 1% level for all six specifications, meaning the results

are very robust. For the baseline regression shown in Column 1 of Table 3, if the

number of shareholders is twice as large, the quarterly stock return decreases by

1.9%; and when the change in the number of shareholders increases by 10%, the

quarterly stock return decreases by approximately 0.86%. Given that there is no

evidence that breadth of ownership is related to variables representing the cash flow

of the firm such as dividend, profit or investment, the relationship between breadth

of ownership and stock return is economically significant. The results can be seen in

Table 6.

As the regression results in Table 6 show, stocks with a higher breadth of owner-

ship have lower returns in the subsequent quarter, a relationship that is statistically

significant. This result is consistent with Hypothesis 1. Stocks with a higher breadth

of ownership are typically held by retail investors, so their prices are overvalued be-

cause retail investors tend to hold attention-catching stocks. Hence, the stock prices

will return to normal in the subsequent quarter.

The results in Table 6 also show that stocks with a higher change in the breadth

of ownership have lower returns in the subsequent quarter, a finding consistent with

Hypothesis 2. A large increase in the breadth of ownership means the shares are

moving from information-motivated institutional investors to attention-motivated re-

tail investors, a signal that the stock price have overreacted to financial news because

33

Table 6: Regression Results of Subsequent Returns on Breadth of Ownership

CLit is the closing price of firm i at the end of period t; clit = ln (CLit); Rit is the return forstock i in quarter t; TVit is the market value of tradable shares of firm i at the end of period t;tvit = ln (TVit); ISit is the percentage of firm i’s total equity held by institutional investors at theend of quarter t;isit = ln (1 + ISit); CHit is the percentage change of the number of shareholders offirm i in quarter t;chit = ln (1 + CHit); BRit is the ratio of the number of shareholders to the marketvalue of tradable shares of firm i at the end of quarter t;brit = ln (BRit); ROEit is the return onequity of firm i in the four consecutive quarters before quarter t; AGit is year-over-year percentagegrowth of total assets for firm i at the end of the quarter before quarter t;agit = ln (1 +AGit); BMit

is the book to market equity ratio at the end of period t;bmit = ln (BMit); βit is the β coefficient offirm i at the end of quarter t; V Lit is the daily average volatility for firm i in quarter t; TOit is thedaily average turnover rate for firm i in quarter t.

Column 1 2 3 4 5 6

Dependent Rit+1

constant 0.514*** 0.456*** 0.550*** 0.647*** 0.488*** 0.582***(0.143) (0.146) (0.139) (0.155) (0.142) (0.157)

chit -0.086*** -0.086*** -0.083*** -0.083***(0.023) (0.022) (0.022) (0.022)

brit -0.019*** -0.022*** -0.019*** -0.022***(0.004) (0.004) (0.004) (0.004)

isit 0.121* 0.142** 0.184***(0.067) (0.062) (0.061)

Rit -0.053*** -0.055*** -0.032* -0.046** -0.032 -0.047**(0.017) (0.018) (0.019) (0.017) (0.019) (0.018)

clit -0.024*** -0.022*** -0.023*** -0.010 -0.021** -0.004(0.008) (0.008) (0.008) (0.006) (0.008) (0.006)

βit 0.002 0.002 0.003 0.000 0.003 -0.001(0.006) (0.006) (0.006) (0.006) (0.006) (0.007)

bmit -0.033 0.006** -0.033 -0.034 0.006*** 0.003(0.030) (0.002) (0.032) (0.029) (0.002) (0.002)

V Lit -0.445 -0.469 -0.632** -0.369 -0.641** -0.340(0.296) (0.282) (0.289) (0.303) (0.274) (0.295)

TOit -0.243** -0.256** -0.435*** -0.378*** -0.467*** -0.437***(0.117) (0.108) (0.129) (0.125) (0.120) (0.114)

tvit -0.029*** -0.027*** -0.031*** -0.027*** -0.028*** -0.023***(0.007) (0.008) (0.007) (0.007) (0.007) (0.007)

ROEit 0.025*** 0.026*** 0.021*** 0.026*** 0.022*** 0.029***(0.007) (0.007) (0.007) (0.007) (0.007) (0.007)

agit 0.026* 0.009* 0.024 0.028* 0.007 0.012**(0.015) (0.005) (0.015) (0.014) (0.005) (0.005)

*** indicates the coefficient is significant at the 0.01 level (2-tailed);** indicates the coefficient issignificant at the 0.05 level (2-tailed); * indicates the coefficient is significant at the 0.10 level (2-tailed); The standard errors adjusted for autocorrelation are in parentheses.

34

of the irrational trading behavior of retail investors. This situation will lead to a

significant underperformance of the stock in the subsequent quarter.

It is important to differentiate the difference between the impact of change of

breadth of ownership and the level of breadth of ownership on subsequent stock

returns. The regression coefficients a1 and a2 in Table 6 show that subsequent stock

returns are more sensitive to a change in the breadth of ownership than the level of

the breadth of ownership.

The change in the breadth of ownership reflects the pattern of market’s short-

term reaction to information. If this change results in an increase in the breadth of

ownership, it indicates that retail investors have overreacted to information. This

change not only causes an overvaluation of the stock price but will subsequently

induce selling pressure due to the high frequency of retail trading. However, the level

of the breadth of ownership, a firm characteristic, is more stable than the change of

the breadth of ownership. Stocks with higher retail holdings will underperform, a

situation that is a long-term pattern in stock returns.

The coefficients of control variables are informative. As is shown in Columns 1, 3,

4 of Table 6, when I add isit to the right side of the regression, the coefficients of bmit

become negative and insignificant, and the standard errors become large because of

the high correlation between isit and bmit. However, this collinearity problem does

not affect the coefficients of brit and chit, so the results that the level of the breadth of

ownership and the change of the breadth of ownership have a significant and negative

35

impact on subsequent return are robust, after controlling for institutional holdings.

The coefficient a3 is positive and significant in Column 1, 3, 4 of Table 6, indicating a