theroadtobasel3-jan2012

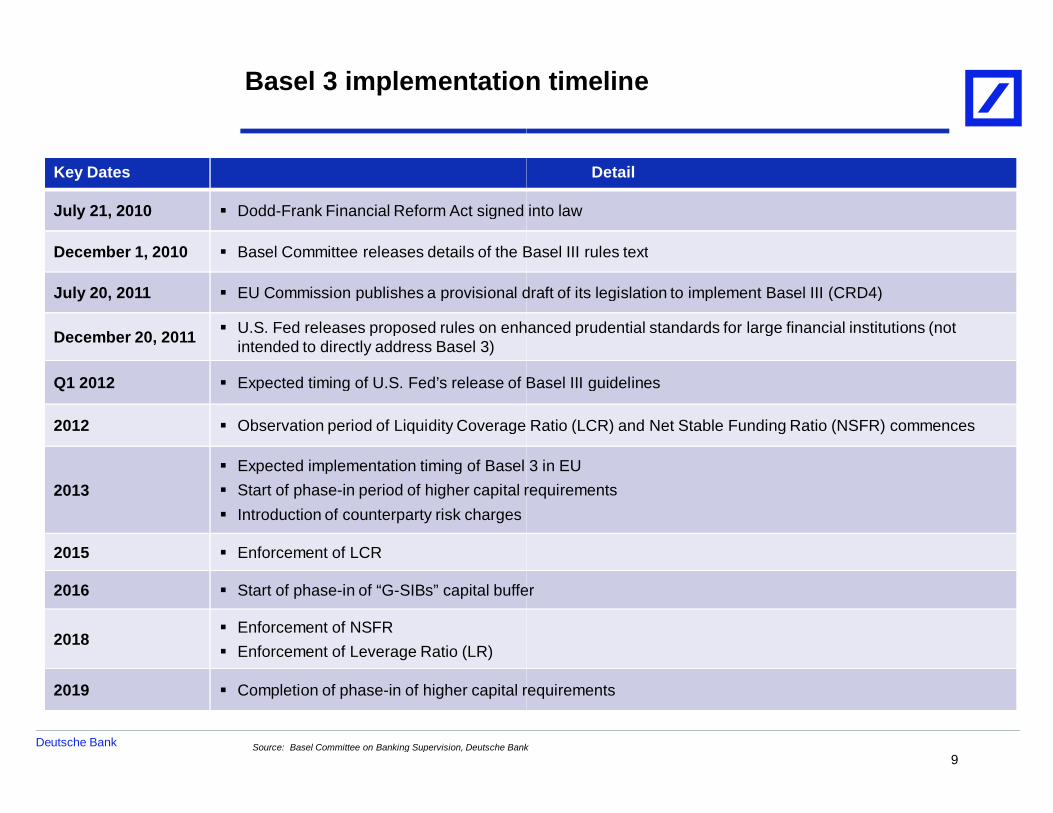

TRANSCRIPT

Deutsche Bank

Deutsche Bank Securities Inc., a subsidiary of Deutsche Bank AG, conducts investment banking andsecurities activities in the United States.

Deutsche BankCapital Markets and Treasury Solutions

January 2012

The Road to Basel 3Implications for Credit, Derivatives & the Economy

Deutsche Bank Securities Inc., a subsidiary of Deutsche Bank AG, conducts investment banking andsecurities activities in the United States. Corporate Solutions & Strategy

Tom Joyce(212) 250-8754 / [email protected]

Michael Dyadyuk(212) 250-0470 / [email protected]

Javier Guzman(212) 250-3464 / [email protected]

Implications for Credit, Derivatives & the Economy

Deutsche Bank

Contents

Section

1 Executive Summary

2 Impact on Credit Facilities and Bond Markets

3 Impact on Derivatives Markets

4 Impact on the Global Economy

5 Positioning for Basel 3: Funding Strategies and Solutions for Corporates

Appendix

I Additional Basel 3 Information

II Glossary of Terms

on Credit Facilities and Bond Markets

Positioning for Basel 3: Funding Strategies and Solutions for Corporates

2

Deutsche Bank

Appendix I

Deutsche Bank Americas

Dean BellissimoHead of Derivative Products

Matthias BergnerHead of GTP Asset & Liability Management Americas

Esperanza CerdanRisk & Capital

Scott FliegerCOO CMTS North America

Marc FratepietroHead of Debt and Solutions Coverage - Corporates

Andreas NeumeierHead of Corporate Banking North America

Paul PuleoHead of Debt and Solutions Coverage – Financial Institutions

Adam RaucherCMTS – Debt & Solutions Coverage

Matthew TiloveCMTS – Derivative Products

James VolkweinHead of Structured Finance and Advisory

Notable contributors

Deutsche Bank Europe

Andreas BoegerCo-Head of Capital Solutions Europe & CEEMEA

Caitriona OkellyHead of Prudential Policy

Vatsal ParikhCredit Products Group

Shamil ShahCross Product Structuring

Neil TranterCore Rates Trading

Daniel TrinderGlobal Head of Regulatory Policy

3

Deutsche BankDeutsche BankCapital Markets and Treasury Solutions

Appendix II

1. Executive Summary

Deutsche BankCapital Markets and Treasury Solutions

Deutsche Bank

Four key components of Basel 3

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Common Equity Tier 1 Total Capital

Minimal Capital Requirement Conservation Buffer = 2.5%Countercyclical Buffer = 0.0% - 2.5% G-SIBs Buffer = 1.0% -3.5%

(1) New capital requirements to be phased in between 2013-2019G-SIB: Global systemically important banks; Currently, no banks fall under highest GSource: Deutsche Bank, BCBS Press Release

New Capital Requirements (1)

4.5%

7.0%

9.5%

13.0%

6.0%

8.5%

11.0%

14.5%

8.0%

10.5%

13.0%

16.5%

Basel 3 focuses on four key regulatory components:1) Capital: Increases minimum regulatory capital ratios (Common Equity Tier 1, Tier 1, Total Capital) and

tightens definitions of eligible capital

2) Liquidity: Introduces two new liquidity ratios

3) Risk Weighted Assets (RWA): Introduces additional risk charges to account for counterparty credit risk intrading book and derivatives exposures

4) Leverage: Introduces global leverage limitations (Basel 3 goes beyond existing requirements in the U.S.)

LiquidityCoverage Ratio(LCR)

Tests an institution's ability to surviveacute short-term stress (30-dayperiod)Objective: Increase banks’ holdingsof highly liquid assets

Net StableFunding Ratio(NSFR)

Requires longer-term funding ofbanks’ assets (1-year time horizon)Objective: Promote better matchingof banks’ assets and liabilities; reducebanks’ liquidity-constraining activities

Four key components of Basel 3

Global systemically important banks; Currently, no banks fall under highest G-SIB bucket (buffer of 3.5%)

New Liquidity Ratios

Basel 3 focuses on four key regulatory components:Increases minimum regulatory capital ratios (Common Equity Tier 1, Tier 1, Total Capital) and

tightens definitions of eligible capital

Introduces two new liquidity ratios

Introduces additional risk charges to account for counterparty credit risk intrading book and derivatives exposures

Introduces global leverage limitations (Basel 3 goes beyond existing requirements in the U.S.)

5

Deutsche Bank

Transmission channels from Basel 3 to the economy

Basel 3 Key Components Availability / Pricing of Credit

1. Higher capital ratios

2. Increased liquidityrequirements (LCR, NSFR)

3. Additional capital charges(CVA, etc.)

4. Leverage constraints (LR)

Impact on credit facilities– Increased internal charges to be

passed through to borrowers (viahigher spreads) and/or investorsin bank shares (via lower ROEs)

– Curtailment of certain lendingproducts (e.g. liquidity facilities,long-term cash lending)

– Resource allocation to top tierclient relationships

Impact on derivatives markets– Increased credit charges on

derivatives transactions

Impact on bond markets– Shift in supply / demand dynamics

Transmission channels from Basel 3 to the economy

Availability / Pricing of Credit Impact on the Global EconomyImpact on credit facilities

Increased internal charges to bepassed through to borrowers (viahigher spreads) and/or investorsin bank shares (via lower ROEs)Curtailment of certain lendingproducts (e.g. liquidity facilities,

term cash lending)Resource allocation to top tierclient relationships

Impact on derivatives marketsIncreased credit charges onderivatives transactions

Impact on bond marketsShift in supply / demand dynamics

Reduced business cycle volatility

Reduced perception of systemicrisks in financial system

× Increased funding costs for privatesector

× Reduced access to certain types ofcredit

× Reduced global output andemployment

6

Deutsche Bank

Summary of Basel 3 impact on markets

Expected Impact

CreditFacilities

New liquidity and leverage requirements to lead to reand re-allocation of credit commitments– Undrawn commitments (particularly liquidity back

facilities) to be acutely affectedImpact studies project wide range of lending spreadincreases (from 15 bps to 500+ bps)

BondMarkets

Banks to decrease reliance on short-term (1-3 yr) fundingin favor of longer-term ( 5 yr) issuance

Increased demand by bank investors for highly-rated (AAand higher) non-financial corporate debt– Banks currently represent only ~5% of the investor buyer

base

DerivativesMarkets

Increased capital charges related to Counterparty CreditRisk– S&P estimates a 4–6x increase in credit-related chargesNew Credit Valuation Adjustment (CVA) capital chargeall OTC derivatives transactions will have greatest impact on:– Corporates with higher and more volatile CDS spreads– Corporates with no observable CDS– Lower-rated corporates– Longer-dated and/or highly complex transactions– High threshold margining agreements

Source: BIS, OECD, Fed, IIF, McKinsey Global Institute, Deutsche Bank

Summary of Basel 3 impact on markets

Potential Responses

d to re-pricing

back-stop

lending spread

New capital charges may force banks to:– Increase rates and/or reduce availability of liquidity

back-stop facilities– Focus on bifurcating revolving facilities (where

possible) between “GCP” and “CP back-stop”uses

– Shift to shorter tenors, particularly <1 year

3 yr) funding

rated (AA-

Banks currently represent only ~5% of the investor buyer

Corporates should explore alternative fundingstrategies:– Short-dated capital markets issuance to fill

potential market void

– CDS-based funding commitments (for short-termfinancing needs of lower-rated corporates)

capital charges related to Counterparty Credit

related chargesCredit Valuation Adjustment (CVA) capital charge on

all OTC derivatives transactions will have greatest impact on:Corporates with higher and more volatile CDS spreads

dated and/or highly complex transactions

Impact can be mitigated through:

– Use of CSAs with daily re-margining(provides nearly full relief)

– Use of master netting agreements(provides partial relief)

OECD, Fed, IIF, McKinsey Global Institute, Deutsche Bank7

Deutsche Bank

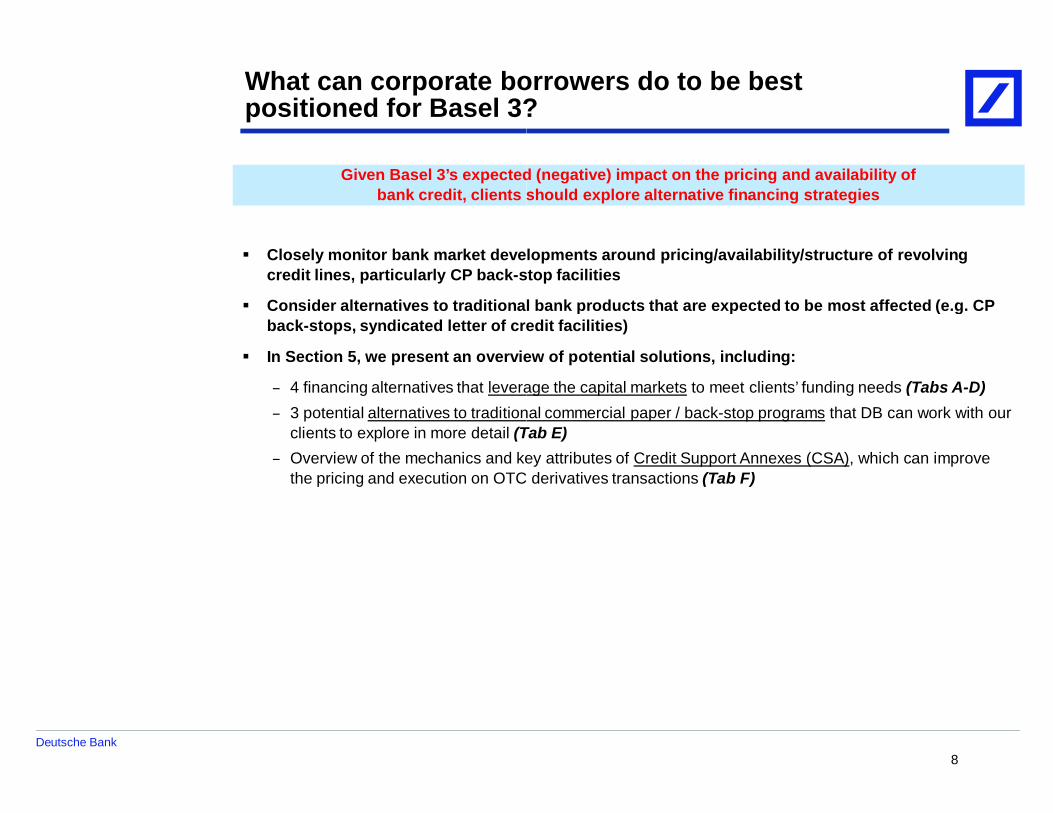

What can corporate borrowers do to be bestpositioned for Basel 3?

Given Basel 3’s expected (negative) impact on the pricing and availability ofbank credit, clients should explore alternative financing strategies

Closely monitor bank market developments around pricing/availability/structure of revolvingcredit lines, particularly CP back-stop facilities

Consider alternatives to traditional bank products that are expected to be most affected (e.g. CPback-stops, syndicated letter of credit facilities)

In Section 5, we present an overview of potential solutions, including:

– 4 financing alternatives that leverage the capital markets– 3 potential alternatives to traditional commercial paper / back

clients to explore in more detail (Tab E)– Overview of the mechanics and key attributes of

the pricing and execution on OTC derivatives transactions

What can corporate borrowers do to be bestpositioned for Basel 3?

Given Basel 3’s expected (negative) impact on the pricing and availability ofbank credit, clients should explore alternative financing strategies

Closely monitor bank market developments around pricing/availability/structure of revolvingstop facilities

Consider alternatives to traditional bank products that are expected to be most affected (e.g. CPstops, syndicated letter of credit facilities)

In Section 5, we present an overview of potential solutions, including:

leverage the capital markets to meet clients’ funding needs (Tabs A-D)alternatives to traditional commercial paper / back-stop programs that DB can work with our

(Tab E)Overview of the mechanics and key attributes of Credit Support Annexes (CSA), which can improvethe pricing and execution on OTC derivatives transactions (Tab F)

8

Deutsche Bank

Basel 3 implementation timeline

Key Dates

July 21, 2010 Dodd-Frank Financial Reform Act signed into law

December 1, 2010 Basel Committee releases details of the Basel III rules text

July 20, 2011 EU Commission publishes a provisional draft of its legislation to implement Basel III (CRD4)

December 20, 2011 U.S. Fed releases proposed rules on enhanced prudential standards for large financial institutions (notintended to directly address Basel 3)

Q1 2012 Expected timing of U.S. Fed’s release of Basel III guidelines

2012 Observation period of Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio

2013Expected implementation timing of Basel 3 in EUStart of phase-in period of higher capital requirementsIntroduction of counterparty risk charges

2015 Enforcement of LCR

2016 Start of phase-in of “G-SIBs” capital buffer

2018Enforcement of NSFREnforcement of Leverage Ratio (LR)

2019 Completion of phase-in of higher capital requirements

Source: Basel Committee on Banking Supervision, Deutsche Bank

Basel 3 implementation timeline

Detail

Frank Financial Reform Act signed into law

Basel Committee releases details of the Basel III rules text

EU Commission publishes a provisional draft of its legislation to implement Basel III (CRD4)

proposed rules on enhanced prudential standards for large financial institutions (not

Expected timing of U.S. Fed’s release of Basel III guidelines

Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) commences

Expected implementation timing of Basel 3 in EUin period of higher capital requirements

SIBs” capital buffer

of higher capital requirements

Basel Committee on Banking Supervision, Deutsche Bank9

Deutsche BankDeutsche BankCapital Markets and Treasury Solutions

Appendix III

2. Impact on Credit Facilities and Bond Markets

Deutsche BankCapital Markets and Treasury Solutions

2. Impact on Credit Facilities and Bond Markets

Deutsche Bank

Overview of Basel 3 regulatory changes

Liquidity Coverage Ratio(LCR)

New ratio to test an institution's ability to survive acute shortAssumes various “outflow factors” for undrawn commitments to nonperiodBanks must retain High Quality Liquid Assets (HQLA) to offset s

Net Stable Funding Ratio(NSFR)

New ratio designed to promote longerAssigns various funding factors depending on the nature and maturity of corporate loan exposuresBanks must retain sufficient Available Stable Funding (ASF) to satisfy ratio requirements

Leverage Ratio(LR)

New ratio focused on gross exposure (i.e. no risk weighting)Includes 100% of unutilized commitments

Intended as a back-stop to the risk

Risk Weighted Assets(RWA)

No change under Basel 3 to banking

Source: BIS, OECD, Fed, IIF, McKinsey Global Institute, Deutsche Bank

Overview of Basel 3 regulatory changes

Description

New ratio to test an institution's ability to survive acute short-term stress (30 day period)Assumes various “outflow factors” for undrawn commitments to non-financial corporates during a stress

must retain High Quality Liquid Assets (HQLA) to offset such potential outflows

to promote longer-term funding of banks’ assetsvarious funding factors depending on the nature and maturity of corporate loan exposures

sufficient Available Stable Funding (ASF) to satisfy ratio requirements

ed on gross exposure (i.e. no risk weighting)Includes 100% of unutilized commitments

risk-based capital requirements

banking book treatment of non-financial loan exposures

OECD, Fed, IIF, McKinsey Global Institute, Deutsche Bank11

Deutsche Bank

Key Basel 3 ratios

HQLA - characterized by low credit/market risk, high liquidity, low correlation to risky assets– Level 1 Assets (e.g. cash, central bank reserves) and Level 2 Assets (e.g. highly

Net Cash Outflows - defined as expected cash outflows minus expected cash inflows– Complex formula for weighting cash inflows and outflows

Stress scenarios:– Partial loss of deposits; significant reduction of unsecured funding; increase in haircuts for secured

funding; out flows due to rating downgrade; collateral requirements for derivatives; drawings oncommitments

Ratio assumes the following outflow factors related to– 10% for Credit Facilities (1)

– 100% for Liquidity Facilities (2)

Any loan commitments to financial institutions

Banks to avoid granting large un-utilized facilities to corporates due to higher outflow factorsEnsure facilities are documented as “General Corporate Purpose and Working Capital” (vs.Liquidity Back-stop)

Details

Definition

Stock of High Quality Liquid Assets(HQLA)

Net Cash Outflows Over a 30-Day TimePeriod

100%

(1) “Credit Facility”: explicit contractual agreements and/or obligations to extend funds at a future date to retail or wholesale counterparties , awhich do not fall under the “Liquidity Facility” definition(2) “Liquidity Facility”: any back-up facility put in place expressly for the purpose of refinancing the debt of a customer in situations where such acustomer is unable to obtain its ordinary course of business funding requirements in the financial marketsSource: BIS Publications, Deutsche Bank

Key Implications

Relevant Metrics forCorporates

Liquidity Coverage Ratio (LCR)

characterized by low credit/market risk, high liquidity, low correlation to risky assetsLevel 1 Assets (e.g. cash, central bank reserves) and Level 2 Assets (e.g. highly-rated corporate bonds)

defined as expected cash outflows minus expected cash inflowsComplex formula for weighting cash inflows and outflows

Partial loss of deposits; significant reduction of unsecured funding; increase in haircuts for securedfunding; out flows due to rating downgrade; collateral requirements for derivatives; drawings on

Ratio assumes the following outflow factors related to corporate loan exposures (i.e. LCR denominator):

financial institutions are subject to a 100% outflow factor

utilized facilities to corporates due to higher outflow factorsEnsure facilities are documented as “General Corporate Purpose and Working Capital” (vs.

100%

explicit contractual agreements and/or obligations to extend funds at a future date to retail or wholesale counterparties , and

up facility put in place expressly for the purpose of refinancing the debt of a customer in situations where such ato obtain its ordinary course of business funding requirements in the financial markets

Liquidity Coverage Ratio (LCR)

12

Deutsche Bank

Key Basel 3 ratios

Available Stable Funding (ASF)– Different weightings applied to different forms of funding– Focuses on Liability side of balance sheet

Required Stable Funding (RSF)– All balance sheet assets and off-balance sheet commitments multiplied by an RSF factor that varies

based on asset type– Focuses on Asset side of balance sheet

Ratio applies the following factors to corporate loan exposures to calculate RSF (i.e. denominator):– 50% for <1 yr maturities– 100% for >1 yr maturities– 5% for undrawn commitments (same for Credit and Liquidity Facilities)

Increased focus on short-term loans (<1 yr) due to favorable RSF factor

Details

Definition

Source: BIS Publications, Deutsche Bank

Key Implications

Relevant Metrics forCorporates

Available Amount of Stable Funding(ASF)

Required Amount of Stable Funding(RSF)

100%

Net Stable Funding Ratio (NSFR)

Different weightings applied to different forms of fundingside of balance sheet

balance sheet commitments multiplied by an RSF factor that varies

side of balance sheet

Ratio applies the following factors to corporate loan exposures to calculate RSF (i.e. denominator):

5% for undrawn commitments (same for Credit and Liquidity Facilities)

term loans (<1 yr) due to favorable RSF factor

100%

Net Stable Funding Ratio (NSFR)

13

Deutsche Bank

Key Basel 3 ratios

Capital: Tier 1 Capital (i.e. Core / Additional Tier 1 Capital) after deductions

Assets:– On-balance sheet items based on accounting value– Collateral, guarantees and other risk mitigations not subtracted from assets– Derivatives: accounting measure of exposure plus add

Off Balance Sheet Items: Includes 100% of all Commitments, Guarantees, LCs

Ratio includes the following in calculation of total assets (i.e. denominator):– 100% of utilized and undrawn commitments– 100% of contingencies and guarantees

Gross leverage measure to constrain overall size of bank balance sheets, including loan portfolios

Details

Definition

Source: BIS Publications, Deutsche Bank

Key Implications

Relevant Metrics forCorporates

New Definition of Tier 1 Capital

Total On and Off-Balance Sheet Assets

Leverage Ratio (LR)

: Tier 1 Capital (i.e. Core / Additional Tier 1 Capital) after deductions

balance sheet items based on accounting valueCollateral, guarantees and other risk mitigations not subtracted from assetsDerivatives: accounting measure of exposure plus add-on (exposure can be netted)

: Includes 100% of all Commitments, Guarantees, LCs

Ratio includes the following in calculation of total assets (i.e. denominator):100% of utilized and undrawn commitments100% of contingencies and guarantees

Gross leverage measure to constrain overall size of bank balance sheets, including loan portfolios

3%

Leverage Ratio (LR)

14

Deutsche Bank

$100mn, 5yr RCL (Liquidity Facility treatment)

Banks’ Funding Cost L + 75 bps L + 150 bps L + 225 bpsNegative Carry on Liquidity Buffer (a) 75 bps 150 bps 225 bpsLCR Factor 100% 100%Annual Liquidity Charge (bps) 75 bps 150 bps 225 bpsAnnual Liquidity Charge ($) $750,000 $1,500,000 $2,250,000

Incremental Tier 1 Capital Required (b) $3,003,003 $3,003,003 $ 3,003,003

Annual Leverage Charge ($) (c) $600,601 $600,601 $600,601

Annual Leverage Charge (bps) 60 bps 60 bps

Total Annual Capital Charge ($) $1,350,601 $2,100,601 $2,850,601

Total Annual Capital Charge (bps) 135 bps 210 bps 285 bps

Estimating Basel 3 impact on undrawn commitments

Revolving credit facilities may be acutely impacted under Basel 3 as a result of the new LiquidityCoverage Ratio (and to a lesser extent, Leverage Ratio) requirements

The impact may be significantly mitigated if revolving credit facilities (or subas “Credit Facilities” as opposed to “Liquidity Facilities”

(a) (i) Banks' Funding Cost, less (ii) return on re-investment of liquidity buffer (assumed to be Libor flat)(b) Based on 33.3x LR limit(c) Assumes 20% target Return on Equity (ROE)Source: BIS, Deutsche Bank

For Illustrative Purposes Only

LCR/LR Impact on Banks’ Internal Capital Charges

Facility treatment) $100mm, 5yr RCL (Credit Facility treatment)

L + 225 bps L + 75 bps L + 150 bps L + 225 bps225 bps 75 bps 150 bps 225 bps100% 10% 10% 10%

225 bps 8 bps 15 bps 23 bps$2,250,000 $75,000 $150,000 $225,000

3,003,003 $300,300 $300,300 $300,300

$600,601 $60,060 $60,060 $60,060

60 bps 6 bps 6 bps 6 bps

$2,850,601 $135,060 $210,060 $285,060

285 bps 14 bps 21 bps 29 bps

Estimating Basel 3 impact on undrawn commitments

Revolving credit facilities may be acutely impacted under Basel 3 as a result of the new LiquidityCoverage Ratio (and to a lesser extent, Leverage Ratio) requirements

The impact may be significantly mitigated if revolving credit facilities (or sub-limits thereof) qualifyas “Credit Facilities” as opposed to “Liquidity Facilities”

investment of liquidity buffer (assumed to be Libor flat)

For Illustrative Purposes Only

LR impact(currently lessvisible due tolater enforce-ment date)

LCR/LR Impact on Banks’ Internal Capital Charges

LCR impact

Cumulativeimpact

15

Deutsche Bank

Estimating Basel 3 impact on drawn spreads

0 50 100 150 200 250 300

IIF

S&P *

McKinsey

OECD

BIS

Regulator and industry impact studies forecast an increase in lending spreads ranging from 15 bps toover 500 bps; this wide range is indicative of the remaining uncertainty around the implementation

40 568

25 75

35 64

Spectrum of Estimated Lending Spread Increases (bps)

(a) Basel 3 impact on lending spreads assumes a 3% increase in regulatory Tier 1 capital ratio(b) Linear extrapolation used (where applicable) for comparison purposes* Assumes a 9.5% CT1R and 10.5% Tier 1 RatioSource: McKinsey Global Institute, BIS, OECD, IIF, S&P

20 164

15 20

Estimating Basel 3 impact on drawn spreads

Regulator and industry impact studies forecast an increase in lending spreads ranging from 15 bps toover 500 bps; this wide range is indicative of the remaining uncertainty around the implementation

and impact of Basel 3

Spectrum of Estimated Lending Spread Increases (bps)

Basel 3 impact on lending spreads assumes a 3% increase in regulatory Tier 1 capital ratio

Key Questions:1. Will banks’ ROE targets remain unchanged or

be forced to decrease?

2. Will banks be able and/or willing to fully pass-through increased Basel 3 compliance coststo clients?

3. Or, will competitive landscape restrict banks’ability to pass through higher costs?

16

Deutsche Bank

Impact on bond market supply

Historical FI New Issue Volumes Divided by Tenor

Net Stable Funding Ratio (NSFR) to have biggest impact on banks’ issuance patternsNSFR incentivizes banks to shift to longer– For ASF, only senior debt with >1

– Since 2008, banks’ issuance of <3regulatory guidelines

Expected Impact:– Banks to decrease

reliance on short-term(1-3 yr) funding infavor of longer-term

5 yr) issuance– IG investors may face

potential market voidfor shorter-termmaturities if banks shiftto longer-term funding

Potential Opportunity:Corporates shouldseek to fill marketvoid by issuing short-term (up to 3-yr) fixedand/or floating-ratepaper

0

100

200

300

400

500

600

700

800

2000 2001 2002 2003

US

$ B

n<1 Year 1-3 Yrs

(1) Excludes government-guaranteed issuanceSource: Thomson Reuters

Impact on bond market supply

Historical FI New Issue Volumes Divided by Tenor (1)

Net Stable Funding Ratio (NSFR) to have biggest impact on banks’ issuance patternsbanks to shift to longer-term funding

For ASF, only senior debt with >1-year maturities can be included

Since 2008, banks’ issuance of <3-year debt has decreased substantially, partly in anticipation of new

2004 2005 2006 2007 2008 2009 2010 2011

3 Yrs 3-5 Yrs 5-7 Yrs 7-8 Yrs > 10 Yrs

17

Deutsche Bank

Impact on bond market demand

Breakdown of 2011 IG Credit by Rating

Liquidity Coverage Ratio (LCR) to havebiggest impact on banks’ demand for IGcredit– Only non-financial corporate debt rated “AA”

and higher can be included as High QualityLiquid Assets (HQLA)

Such highly rated corporate debtrepresents ~7% ($~40 bn) of the IG marketQuantitative Impact Study (QIS)(1)

conducted by BIS estimated potentialshortfall of EUR 1.73 trillion due to LCR

AA- andHigher

Corporates,6.6%

AA

Financials,

OtherCorporates,

55.7%

OtherFinancials,

23.4%

(1) QIS results based on YE2009 figures across a global sample of 223 banksSource: Deutsche Bank CMTS Syndicate, BIS

Expected Impact:– Increased bank

demand for highly-rated (AA- and higher)non-financial corporatedebt

– Decreased bankdemand for unsecureddebt of other financials

Potential Opportunity:Highly-ratedcorporates shouldseek to capitalize onincreased bankdemand during orderbook building

Impact on bond market demand

Breakdown of 2011 IG Credit by Rating

Liquidity Coverage Ratio (LCR) to havebiggest impact on banks’ demand for IG

financial corporate debt rated “AA”High Quality

represents ~7% ($~40 bn) of the IG market

conducted by BIS estimated potentialshortfall of EUR 1.73 trillion due to LCR

Breakdown of Investors in IG Credit

Banks currently represent < 5 % of IGdemandHistorically, banks’ demand has favoredother FI debt over corporate debt– However, unsecured FI debt is ineligible as

HQLAExpect shift in banks’ buying patterns fromFI to non-financial corporate debt

AA- andHigher

Financials,14.3%

Real moneyfunds /

insurance,~90%

Hedgefunds, ~5%

Banks andother,~5%

a global sample of 223 banks

18

Deutsche BankDeutsche BankCapital Markets and Treasury Solutions

Appendix IV

3. Impact on Derivatives Markets

Deutsche BankCapital Markets and Treasury Solutions

3. Impact on Derivatives Markets

Deutsche Bank

1. Credit ValuationAdjustment (CVA)

New capital charge introduced on derivatives exposures to cover markcounterparty credit spreads

2. Margin Periodof Risk (MPR) Increased margin period of risk for OTC derivative transactions

3. StressedParameters

Expected exposures on OTC derivatives calculated using stressed assumptions, includingincreased charges for “wrong

4. CorrelationAssumptions Multiplier applied to exposures to large or unregulated financial institutions

Basel 3’s focus on Counterparty Credit Risk

S&P estimates a 4–6x average increase in risk weightings / capital charges as a resultof new capital charges and revisions to existing RWA rules under Basel 3

Four Key Changes to

New Definition of Tier 1 Capital

Total On and Off-Balance Sheet Assets

Tier 1 CapitalCredit Risk + Market Risk + Operational Risk

RWA RWA RWA

Credit Risk

Focus of Basel 3

Market Risk

Remains thesame as Basel 2

Will impactOTC

derivativestransactions

Bank’s Capital Ratio Composition

Source: Basel Committee on Banking Supervision, S&P

New capital charge introduced on derivatives exposures to cover mark-to-market volatility inspreads

Increased margin period of risk for OTC derivative transactions

on OTC derivatives calculated using stressed assumptions, includingincreased charges for “wrong-way” risk

exposures to large or unregulated financial institutions

Basel 3’s focus on Counterparty Credit Risk

6x average increase in risk weightings / capital charges as a resultof new capital charges and revisions to existing RWA rules under Basel 3

Four Key Changes to Credit RWA

New Definition of Tier 1 Capital

Balance Sheet Assets

Tier 1 CapitalCredit Risk + Market Risk + Operational Risk

RWA RWA RWA

Market Risk

same as Basel 2

Op. Risk

Remains thesame as Basel 2

= Tier 1 Capital Ratio

Bank’s Capital Ratio Composition

20

Deutsche Bank

Impact on OTC derivatives

Description

Credit ValuationAdjustment

(CVA)(1)Pre-Basel 3: Capital charges only for default risk(and ratings migration)

– No charges required to capture a deterioration ofa counterparty’s credit profile

Basel 3: Introduces explicit capital charge add-onfor Credit Valuation Adjustment (CVA) on all OTCderivatives transactions

– CVA risk charge calculated using normal andstressed market assumptions

– According to BIS, during the financial crisis, ~2/3of banks’ accounting losses attributed tocounterparty credit risk were caused by mark-to-market adjustments from rising credit spreads (i.e.CVA), and only 1/3 were due to actual defaults

Margin Period ofRisk(MPR)

Increase in MPR from 5 – 10 days to 20 days forcomplex and/or illiquid collateralized trades

If daily re-margining, no changes

(1) “CVA” – fair value adjustment to mark-to-market derivatives for counterparty credit riskSource: Basel Committee on Banking Supervision, S&P, Deutsche Bank

Implications for Derivatives Counterparties

1. Pricing of derivatives transactions should nowreflect either:i. Cost of hedging CVA exposure (e.g. CDS); or

ii. Banks’ required hurdle rate on incremental RWAcreated by CVA charge

2. Longer transaction tenors lead to higher CVAcapital charges

3. Higher volatility in CDS leads to higher CVA capitalcharges

4. Expect increased use of master agreements thatpermit regulatory netting

5. Expect shift from uncollateralized trades to mutualCSAs

1. Favor daily re-margining agreements

2. Avoid illiquid collateral and highly complextransactions

Impact on OTC derivatives

deterioration of

credit spreads (i.e.

market derivatives for counterparty credit riskBasel Committee on Banking Supervision, S&P, Deutsche Bank

21

Deutsche Bank

CVA – mitigants and alternatives

CVA Hedges

Dealer hedges CCR in the market

Recognized hedges include:– Single-name / contingent CDS

– Other equivalent instrumentsdirectly referencing counterparty

– Index CDS (only grant partialrelief due to basis risk)

Evolution of client’s credit profileover time (i.e. CVA)

Pricing to reflect level and volatilityof client’s CDS

Pricing also subject to dealer’s costof funds (since dealer likely to facecollateral posting requirements onhedge)

Dealers’ procurement of CDS forcapital charge relief couldmaterially increase CDS levels ofcounterparties

Description

Key Variables

Uncertainty sits with dealer

Implications for Clients

Source: Basel Committee on Banking Supervision, Deutsche Bank

mitigants and alternatives

Client enters into 2-way CreditSupport Annex (CSA) with dealer

CSAs typically only variationmargin (VM) requirements

VM required to be posted by clientover term of transaction

Client’s funding cost for suchrequired collateral

Pricing to reflect reduction/absenceof CVA charge

CSA thresholds matter– Non-zero CSAs still carry CVA

charge (albeit smaller thanuncollateralized trades)

Margin periods matter– Daily re-margining provides

greatest cost relief

Collateral Posting (CSA)

Client faces central clearingcounterparty (CCP) instead ofdealer

Initial Margin (IM) and VM conceptsapply

VM required to be posted by clientover term of transaction

Client’s funding cost for suchrequired collateral

Pricing to reflect absence of CVAcharge

However, banks must capitalizecharge for credit exposure to CCP– Risk weight equal to 2% of

Exposure at Default (EAD) for“qualifying” CCPs

Significant uncertainty remainsregarding timing, implementationand scope of central clearing

Central Clearing

Uncertainty sits with client

22

Deutsche Bank

CVA – illustrative example

Pre-Basel 3 Capital Charge 3 1.5 bps

Basel 3 CVA Capital Charge 3 1.5

Aggregate Capital Charge 4 3 bps

Cost of Funding 0 bps

Variation Margin Does Not Exist

Liquidity Demands Known (Zero)

Direct Costs to Client

(1) Client pays floating rate, receives fixed rate(2) Client pays USD, receives EUR(3) Capital charges based on the following industry metrics:(4) Excludes additional credit charges banks may impose for counterparty default risk(5) Expected cost of funding assuming symmetrical distribution of future potential exposures (i.e. 50/50 probability of clie

collateral)

Indirect Costs to Client

Source: Basel Committee on Banking Supervision, Deutsche Bank

Pricing comparison for “BBB” rated client

Example #1:5y Fixed/Floating IRS

illustrative example

1.5 bps 7 bps < no risk to bank >

1.5 bps 6 bps < no risk to bank >

3 bps 13 bps 0 bps

0 bps 0 bps 0 bps 5

Does Not Exist Does Not Exist Exists

Known (Zero) Known (Zero) Unknown

No CSA 2-way CSA

(3) Capital charges based on the following industry metrics: Return on Capital target of 15% and Tier 1 Capital Ratio target of 10%(4) Excludes additional credit charges banks may impose for counterparty default risk(5) Expected cost of funding assuming symmetrical distribution of future potential exposures (i.e. 50/50 probability of client posting/receiving

Pricing comparison for “BBB” rated client

Collateral PostingExample #2:

5y EUR/USD CCS2Example #1:

5y Fixed/Floating IRS1

23

Deutsche Bank

Margin Period of Risk (MPR) overview

Pre-Basel 3

Margin Period of Risk (MPR) – Time period from (i) the lastexchange of collateral covering a netting set of transactionswith a defaulting counterparty, until (ii) that counterparty isclosed out and the resulting market risk is re-hedged

Supervisory floors (i.e. minimum holding periods)established depending on type of transaction

– Securities Financing Transactions (SFTs) – includes repo-style transactions

– Other collateralized trades

A capital charge is calculated based on the expected mark-to-market movements during the MPR

Current MPR standards:

MPR floor for SFT = 5 daysMPR floor for all other “netting sets” = 10 days

If daily re

MPR floor of

MPR to be adjusted if 2 or more margin call disputes have occurredon a netting set over the previous 2 quarters that have lasted longerthan the set MPR

Source: Basel Committee on Banking Supervision, Deutsche Bank

Margin Period of Risk (MPR) overview

Basel 3

If daily re-margining, no changes

MPR floor of 20 days will apply for the following:

Netting sets where the number of trades exceeds 5,000

Netting sets containing illiquid collateral or OTC derivatives thatare not easily replaced

– Illiquid collateral and OTC derivatives that are not easily replacedto be determined in the context of stressed market conditionswhere multiple price quotations cannot be obtained withoutmoving the market or reflecting a market discount within 2 orfewer days

MPR to be adjusted if 2 or more margin call disputes have occurredon a netting set over the previous 2 quarters that have lasted longerthan the set MPR

24

Deutsche BankDeutsche BankCapital Markets and Treasury Solutions

Appendix V

4. Impact on the Global Economy

Deutsche BankCapital Markets and Treasury Solutions

4. Impact on the Global Economy

Deutsche Bank

Basel 3 economic impact studies

OECD Fed

Date Published February 2011 February 2011

Increase inLending Rates

U.S.: 64 bps

EU: 54 bps

NA

Impact on GDP(annual growth)

U.S.: (-0.6%)

EU: (-1.1%)

Global: (-0.4%)

Numerous Basel 3 impact studies have been published since August 2010 (BIS, OECD, Fed, IIF, etc.),quantifying the potential effects on credit and GDP growth

– While helpful for illustrative purposes, the results of these studies should be viewed as highly preliminaryand inexact given the number of unknown variables involved

The real economy (GDP) is impacted through 3 main channels:1) Reduced lending volumes

2) Increased interest costs

3) Enhanced financial system stability

Linear extrapolation used (where applicable) for comparison purposes(1) Long Run estimates based on August 2010 BIS studySource: BIS, McKinsey Global Institute, OECD, IIF

Basel 3 economic impact studies

IIF BIS

2011 September 2011 October 2011(1)

U.S.: 243 bps

EU: 328 bps

Transition Period: 15-20 bps

Long Run(1): 39 bps

U.S.: (-1.1%)

EU: (-3.9%)

Transition Period: (-0.2%) to(-1.0%) (Global)

Long Run(1): +0.3% (Global)

Numerous Basel 3 impact studies have been published since August 2010 (BIS, OECD, Fed, IIF, etc.),quantifying the potential effects on credit and GDP growth

While helpful for illustrative purposes, the results of these studies should be viewed as highly preliminaryand inexact given the number of unknown variables involved

The real economy (GDP) is impacted through 3 main channels:

Enhanced financial system stability

Linear extrapolation used (where applicable) for comparison purposes

26

Deutsche Bank

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%BIS OECD IIF

Impact on economic growth

Source: Deutsche Bank Global Markets Research, IIF, OECD, BIS

Estimated Negative Impact on GDP Growth

-0.5%

-2.4%

-1.3%

-0.1%

-1.0%

-0.2%

The slowdown in global output growth projected by recent impact studies ranges between 0

According to various impact studies, the economic effects ofBasel 3 can range from marginal to significant– Median estimate (~1% reduction in annual GDP growth) would

have vast ramifications for global economyHowever, the net economic impact of Basel 3 should also takeinto account its potential economic benefits– BIS actually projects a net increase in GDP in the Long Run

(Transition Period)

Impact on economic growth

IIF, OECD, BIS

The slowdown in global output growth projected by recent impact studies ranges between 0 – 2.4%

DB Real GDP Growth Forecast

Basel 3’s impact on growth may create further headwindsto an already-slowing global economy– DB forecasts a slowdown in global economic growth over the

next year (global GDP growth of 3.2% 2012E)

-2%

0%

2%

4%

6%

8%

10%

Asia-ex Japan U.S. UK EU

Ann

ual G

DP

% G

row

th

2010 2011E 2012E

27

Deutsche Bank

Regional economic impact

Size of Banking Systems

$45.8

$12.1

$0$5

$10$15$20$25$30$35$40$45$50

EU U.S.

Tota

l Ass

ets

(US

D T

rillio

ns)

The EU features a substantially higher level of bankintermediation relative to the US– U.S. banking system assets total ~$12 trillion (representing ~

80% of U.S. GDP)– In contrast, EU banking system assets total ~$46 trillion

(~260% of EU GDP), resulting in a significantly morepronounced expected impact from Basel 3 regulations

The EU region is more susceptible to GDP shocks from new Basel 3 requirementsgiven its greater reliance on bank funding relative to the U.S.

Source: Federal Reserve, ECB, IIF, OECD, S&P

0

10

20

30

40

50

60

70

80

90

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

%

Eurozone and UK U.S.

Regional economic impact

Corporate Securities as % of Total Borrowing

Banks play a dominant role in funding European companies,while U.S. corporates rely almost exclusively on capitalmarketsConsequently, Basel 3 impact studies estimate asubstantially greater slowdown in EU GDP growth:– OECD study: -0.59% in the U.S. vs. -1.14% in the EU– IIF study: -1.1% in the U.S. vs. -3.9% in the EU

The EU region is more susceptible to GDP shocks from new Basel 3 requirementsgiven its greater reliance on bank funding relative to the U.S.

28

Deutsche Bank

Potential economic benefits

Reduced probability / frequency of banking crises

The probability and frequency of a banking crisis decreases proportionately to increases in regulatory Tier 1capital ratios– Higher capital buffers improve banking sector resilience to economic instability– Banks better “equipped” to withstand market crashes– BIS’s Basel 3 study suggests that benefits of a more stable financial system outweigh economic costs (projecting

increased annual GDP growth ranging from 0.31% - 1.87%)

0

50

100

150

200

250

300

350

6% 7% 8% 9% 10%

Num

ber

of Y

ears

Bef

ore

Nex

t Cris

is

Tier 1 Capital Ratio

Implied frequency of a banking crisis

More stringent capital and liquidity requirements imposed by the Basel 3 framework are expected todramatically reduce the frequency and probability of future banking crises

Source: IIF, BIS

Potential economic benefits

Reduced probability / frequency of banking crises

The probability and frequency of a banking crisis decreases proportionately to increases in regulatory Tier 1

Higher capital buffers improve banking sector resilience to economic instability

BIS’s Basel 3 study suggests that benefits of a more stable financial system outweigh economic costs (projecting1.87%)

0%

1%

2%

3%

4%

5%

6%

7%

8%

11% 12% 13% 14% 15%

Prob

abilit

y of

a C

risis

Tier 1 Capital Ratio

Implied probability of a banking crisis

More stringent capital and liquidity requirements imposed by the Basel 3 framework are expected todramatically reduce the frequency and probability of future banking crises

29

Deutsche BankDeutsche BankCapital Markets and Treasury Solutions

Appendix VI

5. Positioning for Basel 3Funding Strategies and Solutions for Corporates

Deutsche BankCapital Markets and Treasury Solutions

Funding Strategies and Solutions for Corporates

Deutsche Bank

Spectrum of capital markets

“AA-” and highercorporates

“BBB” categorycorporates

Sub-inv gradecorporates

Rolling Short-Term Notes

(Tab A)

Short-Term(FRN & Fixed)

(Tab B)

In Tabs A-D, we present 4 alternatives that leverage the capital markets to meet clients’ fundingand liquidity needs

An issuer’s credit rating will help determine which alternatives may be feasible and/or priceefficient for that issuer

“A” categorycorporates

Spectrum of capital markets-based solutions

Term Bonds(FRN & Fixed)

(Tab B)

Bilateral CDS-basedFunding(Tab C)

Bilateral CDS-basedLetter of Credit (LC)

(Tab D)

D, we present 4 alternatives that leverage the capital markets to meet clients’ funding

An issuer’s credit rating will help determine which alternatives may be feasible and/or price-

31

Deutsche Bank

Rolling Short-Term (RST) Notes

Tab ATerm (RST) Notes

Deutsche Bank

Overview

Description

Rolling Short Term Notes (“RST-Notes”):at substantially lower short-term rates

Tenor: Final maturity of 5-6 yrs; initial maturity of 13 months

Size: Up to $1+ bn for strong issuers (market limited to highly

Characteristics:– Investors elect periodically (e.g. monthly or quarterly) to extend the initial maturity another 1

– If investors elect not to extend, their RSTmonths from such date

– Coupons on rolled notes step-up annually to a slightly higher pre

– Can be structured to include a par call option, exercisable after 5

Illustrative RST-Note Program (monthly extension example)

13 month LIBOR floater

13 month LIBOR floater

13 month LIBOR floater

0 1 2 3 4 5 6 7

Months from initial issue date

RST-Notes election period “Rolling” 13

RST Notes aredesigned to create alow cost termfunding by targetingmoney market fundinvestors, serving asan alternative to CPfor highly ratedcorporates

Description

Notes”): Designed to create effective long-term funding for an issuer, but

6 yrs; initial maturity of 13 months

Up to $1+ bn for strong issuers (market limited to highly-rated issuers (A1/P1)

Investors elect periodically (e.g. monthly or quarterly) to extend the initial maturity another 1-3 months

If investors elect not to extend, their RST-Notes are exchanged into notes with a final maturity of 10-12

up annually to a slightly higher pre-determined spread to Libor

Can be structured to include a par call option, exercisable after 5th year

Note Program (monthly extension example)

13 month LIBOR floater

13 month LIBOR floater

13 month LIBOR floater

8 9 10 11 12 13 14 15 16

Months from initial issue date

“Rolling” 13-month maturity of RST-Notes

33

Deutsche Bank

Key Considerations

Key Benefits

All-in cost to the final program maturity (5-6 yrs) should besubstantially lower than equivalent term funding rates, as noinvestor term premium is required

Pre-determined coupon step-up schedule significantly flatterthan an issuer’s vanilla floating-rate curve

No incremental back-up liquidity required for rating agencypurposes

A rolling 13-mo. maturity should allow an issuer to classify RSTNotes as long-term debt (assuming monthly extensions)

Allows issuer to access money market investor base

Transaction history dating back to 1998, with a very highhistorical investor extension participation rate

Key Considerations

× Introduces short-term liquidity risk into issuer’s capital structure

×Long-term debt classification less certain if issuer electsquarterly extension periods

34

Deutsche Bank

Legal, accounting and tax considerations

Tax

Legal / Documentation

Accounting

(a) Some 4(2) CP documentation may need to be modified to provide for notes issued with a maturity up to 13 months

Deutsche Bank is not acting and does not purport to act in any way as your advisor. We therefore strongly suggest that you sin relation to any legal, tax, accounting and regulatory issues relating to the merits or otherwise of the products and services discussed.

RST Notes can be issued in a public, 144A or CP offering (using a 4(2) program).Documentation and due diligence is equivalent to a regular term issuanceSubsequent extensions of RST Notes are not considered to be a new issue of securities for SEC purposesOther updated offering materials and/or additional underwriting due diligence are not required for the extension, asinvestors are treated as continuing their initial investment decision

RST Notes with monthly extensions can be recorded as longstatements, given the rolling 13-month maturityRST Notes with quarterly extensions roll into 10No mark-to-market requirements as the RST Notes’ extension feature should not be treated as a separablederivative contract subject to FAS 133, because the “underlying” is an interest rate adjustment and involves no riskto full principal recoveryInterest expense for each period should be accrued on each tranche of RST Notes based on its yield to maturity

RST Notes may be characterized alternatively for tax purposes as either a single longexercise of investors’ extension options) or as a series of 13In either case, extensions of the RST Notes should not trigger taxable gain or loss for the issuer or investorsInterest expense for each period should be accrued on each tranche of RST Notes based on its yield to maturity(same as GAAP)

Legal, accounting and tax considerations

(a) Some 4(2) CP documentation may need to be modified to provide for notes issued with a maturity up to 13 months

Deutsche Bank is not acting and does not purport to act in any way as your advisor. We therefore strongly suggest that you seek your own independent advicetax, accounting and regulatory issues relating to the merits or otherwise of the products and services discussed.

Detail

RST Notes can be issued in a public, 144A or CP offering (using a 4(2) program).Documentation and due diligence is equivalent to a regular term issuance(a)

Subsequent extensions of RST Notes are not considered to be a new issue of securities for SEC purposesOther updated offering materials and/or additional underwriting due diligence are not required for the extension, asinvestors are treated as continuing their initial investment decision

RST Notes with monthly extensions can be recorded as long-term debt on an issuer’s quarterly financialmonth maturity

RST Notes with quarterly extensions roll into 10-month maturities, and may require classification as short-term debtas the RST Notes’ extension feature should not be treated as a separable

derivative contract subject to FAS 133, because the “underlying” is an interest rate adjustment and involves no risk

Interest expense for each period should be accrued on each tranche of RST Notes based on its yield to maturity

RST Notes may be characterized alternatively for tax purposes as either a single long-term security (by assumingexercise of investors’ extension options) or as a series of 13-month securities that are periodically extendedIn either case, extensions of the RST Notes should not trigger taxable gain or loss for the issuer or investorsInterest expense for each period should be accrued on each tranche of RST Notes based on its yield to maturity

35

Deutsche Bank

Short-Term Bonds (FRN & Fixed)

Tab BTerm Bonds (FRN & Fixed)

Deutsche Bank

FRN market overview

Annual IG Corporate (Non-Financial)Issuance Volumes

Recent FRN Corporate (NonIssuer Ratings

A2 / A

A1 / A+

A2 / A

A1/A+

A2/A

A1/A+

A3/BBB+

A3/A-

Source: IFR, Deutsche Bank

Demand for short-term FRNs hasincreased in 2011,providing a goodincremental sourceof 18-month to 3-year liquidity andinvestordiversification

05

1015202530354045

2005 2006 2007 2008 2009

US$

Bn

Financial)Breakdown by Issuer Ratings (2011 Issuance)

Recent FRN Corporate (Non-Financial) IssuanceDate Size ($mm) Maturity Spread

12/12 /11 200 12/11/13 3mL+30

12/01/11 500 06/06/13 3mL+45

9/19/11 350 9/22/14 3mL+53

9/26/11 100 9/29/14 3mL+92

9/13/11 350 9/19/14 3mL+155

9/07/11 300 9/12/14 3mL+55

9/07/11 600 9/13/13 3mL+120

8/17/11 400 8/23/13 3mL+75

AAA4%

AA15%

A62%

BBB19%

2010 2011

37

Deutsche Bank

Fixed-rate, short-term bond market overview

Annual IG Corporate (Non-Financial)Issuance Volumes

01020304050607080

2005 2006 2007 2008 2009 2010

US$

Bn

Issuer Ratings

A2/A

Baa1/A-

A2/BBB+

Baa1/BBB+

A2/A

A2/A

A2/A

A3/A-

Source: IFR, Deutsche Bank

Issuance of short-term (~3-yr), fixed-rate notes hasincreasedsubstantially overthe past 3 years ascompanies seek tocapitalize onhistorically lowshort-term rates

Recent Fixed-Rate, Short

term bond market overview

Financial)Breakdown by Issuer Ratings (2011 Issuance)

2010 2011

Date Size ($mm) Maturity Coupon

12/12/11 400 12/15/14 1.125%

12/06/11 750 12/01/14 2.400%

12/06/11 650 12/09/14 2.625%

12/05/11 500 12/08/14 2.375%

12/01/11 650 12/05/14 1.700%

11/29/11 1000 12/01/14 0.875%

11/29/11 600 12/02/14 1.250%

11/29/11 575 12/15/14 1.400%

AAA3% AA

8%

A45%

BBB44%

Rate, Short-Term Corporate (Non-Financial) Issuance

38

Deutsche Bank

Bilateral CDS-based Funding Alternative

Tab Cbased Funding Alternative

Deutsche Bank

Overview

Description

Alternative funding source to traditional bank loan andbond markets

Available in funded and unfunded (i.e. revolver) forms– Unfunded structure provides incremental source of guaranteed

liquidity

Floating-rate term funding structure with pricing linked to acompany’s 1-year CDS credit spread– Up to 10-year maturity, with annual coupon reset based on

then-current 1y CDS level– Can elect longer tenor (e.g. 3-year) at time of drawdown– Prepayable at par on each annual coupon reset date

DB can provide a bilateral, CDSsources of funding/liquidity; Companies can elect funded or undrawn structures

Source: DB Credit Solutions and Credit Structuring

Illustrative CDS Curve

0

50

100

150

200

250

1 2 3 4 5 7 10

CDS

Spre

ad (b

ps)

Tenor (yrs)

DB can provide a bilateral, CDS-based credit facility to companies seeking alternativesources of funding/liquidity; Companies can elect funded or undrawn structures

40

Deutsche Bank

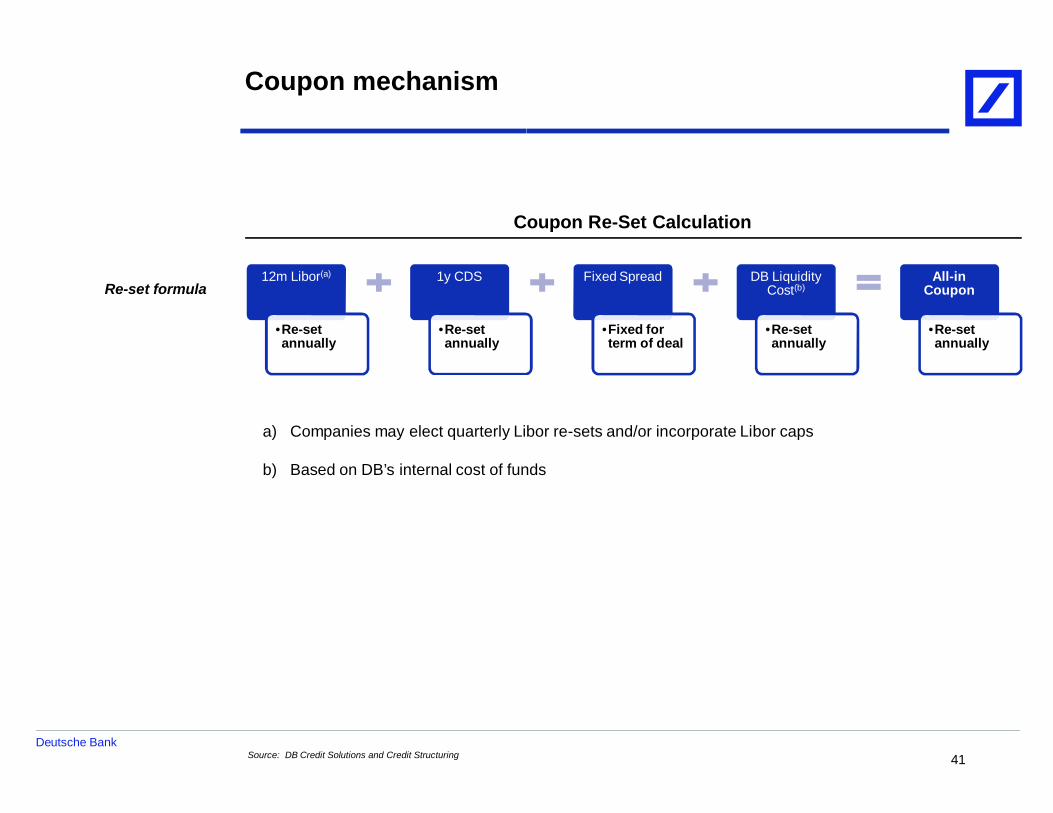

Coupon mechanism

Coupon Re

12m Libor(a)

•Re-setannually

1y CDS

•Re-setannually

Re-set formula

a) Companies may elect quarterly Libor re

b) Based on DB’s internal cost of funds

Source: DB Credit Solutions and Credit Structuring

Coupon Re-Set Calculation

Fixed Spread

•Fixed forterm of deal

DB LiquidityCost(b)

•Re-setannually

All-inCoupon

•Re-setannually

may elect quarterly Libor re-sets and/or incorporate Libor caps

Based on DB’s internal cost of funds

41

Deutsche Bank

Key considerations

Key Benefits

Short-term funding that does not use relationship bank capacity

Competitive pricing vs. long-term funding

– Take advantage of steepness of companies’ CDS curves

– Forward CDS spreads typically exceed realized credit spreads

No financial covenants required

Pre-payable at par annually

Enables a company to express bullish view on its own credit

Precedent transaction history

Private transaction limits disclosure requirements

Avoid potentially negative signal to market if incremental liquidityis needed

May not require bifurcation under US GAAP due to “closelyrelated” nature of linking cost of funding to a company’s owncredit spreads

Source: DB Credit Solutions and Credit Structuring

Key Considerations

Company exposed to potential widening of 1y CDS spreads ateach annual coupon re-set date

FMV termination payment if prepaid intra-year

– Company to pay if CDS tightens; DB to pay if CDS widens

For unfunded (revolver) structure, [3]-day advance noticerequired as Condition Precedent to each draw to enable DB toprocure CDS in the market

Rating agencies may not give 100% liquidity credit to unfundedstructure (i.e. may impose haircuts)

DB has option to terminate following a Succession Event (perISDA definition)

42

Deutsche Bank

Summary of indicative terms

(a) Staggering of issuances dependent on liquidity constraints for 1y CDS and other applicable market conditions

Source: DB Credit Solutions and Credit Structuring

FundedBorrower [Company’s CDS-referenced entity]

Size / Tranches(a) Up to $[1]bn, depending on CDS liquidityStaggered issuances may be required

Structure /Documentation

Senior Unsecured Notes (the “Notes”)– Standalone / Eurobond (MTN) documentation

Listing Not applicable

Initial Maturity 1 year from issuance, with Extension Option until Maximum MaturityDate

Upfront Fees [0.50]%

Interest Rate [ ]m Libor + 1y Borrower CDS Spread + 1.50% + DB Liquidity Cost

Undrawn Fee Not applicable

Minimum / MaximumDraw

Not applicable

Coupon Reset Date /Extension Option

[3] Business Days before Initial Maturity;– On each Coupon Reset Date, Calculation Agent (DB AG) will

provide an Interest Rate quote, and Borrower can decide toextend Notes for 1 year

Maximum Maturity Date Up to 10 yrs

DB Put Option DB will have right to put Notes back to Borrower in circumstanceswhere a Succession Event has occurred or is about to occur andwhere CDS is envisaged to be split into a different or more than onesuccessor

Prepayment At par on each Coupon Reset Date;Subject to unwind costs if prepaid at any other time

Summary of indicative terms

Overview of Structural Alternatives

Unfunded[Company’s CDS-referenced entity]

Up to $[1]bn, depending on CDS liquidity

Senior Unsecured Credit Facility

Not applicable

with Extension Option until Maximum Maturity Each drawn tranche will mature 1 year from draw date, with Extension Optionuntil Maximum Maturity Date

[0.50]%

]m Libor + 1y Borrower CDS Spread + 1.50% + DB Liquidity Cost [ ]m Libor + 1y Borrower CDS Spread + 1.50% + DB Liquidity Cost– Individually set for each draw

[0.375]% per annum

Minimum: $[20]mn / Maximum: $[250]mn– On each potential draw date, Calculation Agent will provide an Interest Rate

quote, and Borrower can decide whether to draw at such rate– Draw amounts may affect pricing due to CDS liquidity constraints

On each Coupon Reset Date, Calculation Agent (DB AG) willprovide an Interest Rate quote, and Borrower can decide to

[3] Business Days before Initial Maturity of each drawn tranche;– On each Coupon Reset Date, Calculation Agent will provide an Interest

Rate quote, and Borrower can decide to extend each drawn tranche for 1year

Up to 10 yrs

DB will have right to put Notes back to Borrower in circumstanceswhere a Succession Event has occurred or is about to occur andwhere CDS is envisaged to be split into a different or more than one

DB will have right to demand repayment of drawn amounts in circumstanceswhere a Succession Event has occurred or is about to occur and where CDS isenvisaged to be split into a different or more than one successor

At par on each Coupon Reset Date;Subject to unwind costs if prepaid at any other time

43

Deutsche Bank

Bilateral CDS-based Letter of Credit Facility

Tab Dbased Letter of Credit Facility

Deutsche Bank

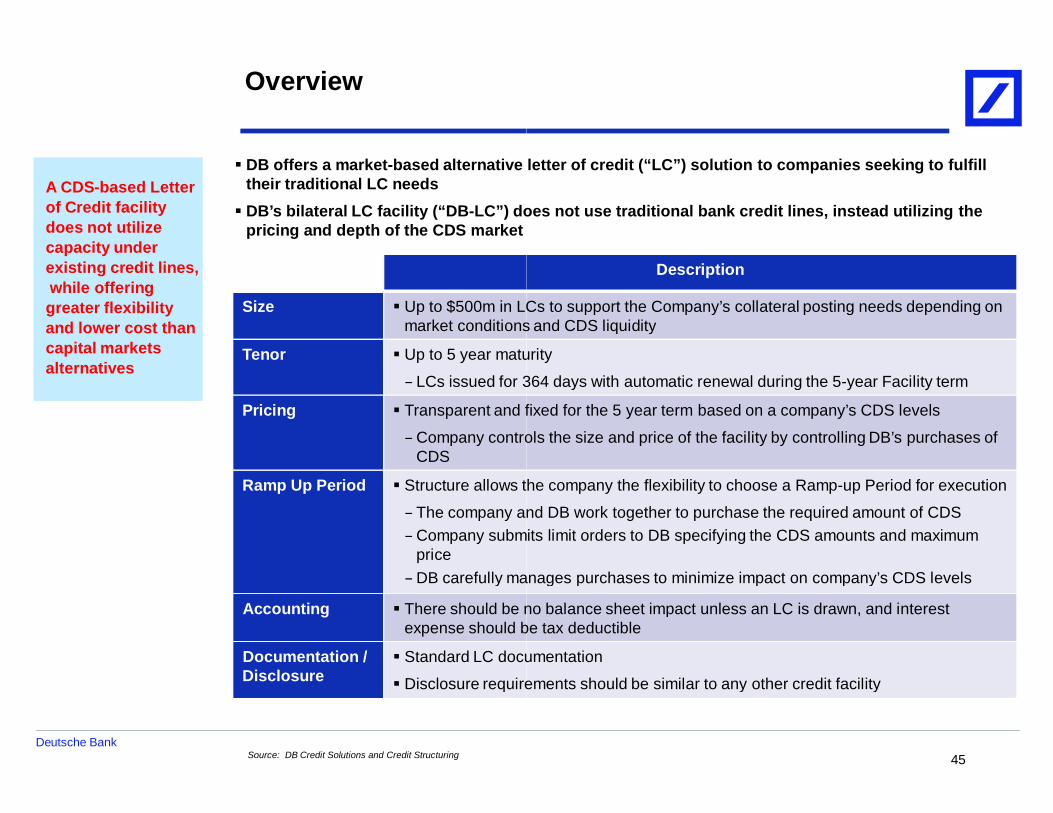

Overview

A CDS-based Letterof Credit facilitydoes not utilizecapacity underexisting credit lines,while offeringgreater flexibilityand lower cost thancapital marketsalternatives

Source: DB Credit Solutions and Credit Structuring

Size Up to $500m in LCs to support the Company’s collateral posting needs depending onmarket conditions and CDS liquidity

Tenor Up to 5 year maturity

– LCs issued for 364 days with automatic renewal during the 5

Pricing Transparent and fixed for the 5 year term based on a company’s CDS levels

– Company controls the size and price of the facility by controlling DB’s purchases ofCDS

Ramp Up Period Structure allows the company the flexibility to choose a Ramp

– The company and DB work together to purchase the required amount of CDS– Company submits limit orders to DB specifying the CDS amounts and maximum

price– DB carefully manages purchases to minimize impact on company’s CDS levels

Accounting There should be no balance sheet impact unless an LC is drawn, and interestexpense should be tax deductible

Documentation /Disclosure

Standard LC documentation

Disclosure requirements should be similar to any other credit facility

DB offers a market-based alternative letter of credit (“LC”) solution to companies seeking to fulfilltheir traditional LC needsDB’s bilateral LC facility (“DB-LC”) does not use traditional bank credit lines, instead utilizing thepricing and depth of the CDS market

Description

Up to $500m in LCs to support the Company’s collateral posting needs depending onmarket conditions and CDS liquidity

Up to 5 year maturity

LCs issued for 364 days with automatic renewal during the 5-year Facility term

Transparent and fixed for the 5 year term based on a company’s CDS levels

Company controls the size and price of the facility by controlling DB’s purchases of

Structure allows the company the flexibility to choose a Ramp-up Period for execution

The company and DB work together to purchase the required amount of CDSCompany submits limit orders to DB specifying the CDS amounts and maximum

DB carefully manages purchases to minimize impact on company’s CDS levels

There should be no balance sheet impact unless an LC is drawn, and interestexpense should be tax deductible

Standard LC documentation

Disclosure requirements should be similar to any other credit facility

based alternative letter of credit (“LC”) solution to companies seeking to fulfill

LC”) does not use traditional bank credit lines, instead utilizing the

45

Deutsche Bank

Structure overview

1. DB enters into a stand-alone bilateral credit facility with the company that allows for the issuance of LCs to specified Beneficsubject to the agreed upon standard terms and conditions

2. The DB-LC issuance capacity is built up through DB’s purchase of CDS during the Ramp– The total outstanding amount of CDS purchased is the amount of LCs available to be issued by DB under the structure– The company may be as active as it wishes during the ramp-

price reports; orders can be started / terminated / amended at any time

3. Company pays a fixed running spread (based on its CDS level) to DB on the available LC amount

4. Company may request DB to issue LCs at any time and is required to promptly (i.e. same day) reimburse DB for amounts drawnunder the LCs

Description

Source: DB Credit Solutions and Credit Structuring

LCbeneficiaries

LCs issued atCompany’s request

Reimbursement of LC draws

LC issuance fees(CDS cost + spread)

DC-LC facility

Client

41

1

3

DB-LC facility

alone bilateral credit facility with the company that allows for the issuance of LCs to specified Beneficiaries,

LC issuance capacity is built up through DB’s purchase of CDS during the Ramp-up Period.The total outstanding amount of CDS purchased is the amount of LCs available to be issued by DB under the structure

-up period, providing daily or weekly limit orders or monitoring dailyprice reports; orders can be started / terminated / amended at any time

Company pays a fixed running spread (based on its CDS level) to DB on the available LC amount

Company may request DB to issue LCs at any time and is required to promptly (i.e. same day) reimburse DB for amounts drawn

Description

CDSmarket

CDS premium

100% hedge of issuedLC exposure

2

46

Deutsche Bank

Sample indicative terms

(a) Term CDS rate is the weighted average of the CDS premium rates for the aggregate CDS purchases executed by Deutsche BankSource: DB Credit Solutions and Credit Structuring

Facility Borrower [Company’s CDS-referenced entity]

Issuing bank Deutsche Bank AG, NY or one of its affiliates

Letter of credit facility Amount: Up to $500 mMaturity: 5.0 yearsIssuance Fee: Term CDS rate + [50-75] bps(a)

LC commitment amount Up to $500m on the Facility closing date

Ramp-up period~2 weeks – 3 months from the Facility closing date, depending on market liquidity.If the Company would like to begin the Ramp-up Period prior to closing, the Company can do so at its option after signing both aCommitment Letter and Fee Pricing Agreement for the transaction

LC availability amountThe LC Availability Amount will be increased as agreed upon by the Borrower and Deutsche Bank during the Rampfollowing the closing date, and the maximum aggregate LC amount will not at any time exceed $500m (“Maximum LC AvailabilityAmount”)

Structuring fees 1.00% of the LC commitment amount

Annual Facility feesAn amount equal to the LC availability amount multiplied by a per annum rate equal to [TBD]% (based on the average expected Ccost + [50-75] bps)

Financial covenants Based on the terms of the Borrower’s existing term bank credit facilities

Reimbursementobligations

If Deutsche Bank funds any drawn amount under an issued LC, the Borrower is obligated to pay that amount (each, a“Reimbursement Obligation”) to the Administrative Agent on the same Business Day on which the Issuer notifies the Borrower ofsuch LC Drawing (the “LC Reimbursement Date”)

Conditions precedentStandard conditions precedent including but not limited to: (a) receipt of all internal approvals including credit, risk, legcompliance, (b) signed binding documentation acceptable to Deutsche Bank, and (c) receipt of all fees and expenses

Sample indicative terms

Term CDS rate is the weighted average of the CDS premium rates for the aggregate CDS purchases executed by Deutsche Bank

3 months from the Facility closing date, depending on market liquidity.Period prior to closing, the Company can do so at its option after signing both a

Fee Pricing Agreement for the transaction

The LC Availability Amount will be increased as agreed upon by the Borrower and Deutsche Bank during the Ramp-up Periodfollowing the closing date, and the maximum aggregate LC amount will not at any time exceed $500m (“Maximum LC Availability

An amount equal to the LC availability amount multiplied by a per annum rate equal to [TBD]% (based on the average expected CDS

Based on the terms of the Borrower’s existing term bank credit facilities

If Deutsche Bank funds any drawn amount under an issued LC, the Borrower is obligated to pay that amount (each, a“Reimbursement Obligation”) to the Administrative Agent on the same Business Day on which the Issuer notifies the Borrower ofsuch LC Drawing (the “LC Reimbursement Date”)

Standard conditions precedent including but not limited to: (a) receipt of all internal approvals including credit, risk, legal, andcompliance, (b) signed binding documentation acceptable to Deutsche Bank, and (c) receipt of all fees and expenses

47

Deutsche Bank

Comparison of DB-LC and alternatives

Key Benefits

Traditional LC Often structured off existing credit facility pricing,availability, and duration

Typically lowest cost alternative

May allow funded loan if underlying agreementprovides for a drawn facility

DB-LC Based on market CDS, not revolver capacity, freeingup liquidity under a company’s traditional revolver

Up to 5 year term with fixed, transparent pricingbased on purchased CDS

LCs may be issued for the benefit of any of thecompany’s affiliates or subsidiaries

No balance sheet impact unless an LC is drawn, andinterest expense should be tax deductible

Documentation based off existing credit facility

Financial strength of issuing bank (DB rated Aa3 / A+)

Proven structure (10+ facilities extended to datetotalling over $7bn)

Source: DB Credit Solutions and Credit Structuring

LC and alternatives

Key Considerations

Often structured off existing credit facility pricing, Difficult to source incremental capacity in current andfuture (Basel 3) environment

Decline in availability and increased pricing on renewedfacilities due to market conditions and overall bank creditappetite

May not provide for funded loan if standalone,bi-lateral LC

Based on market CDS, not revolver capacity, freeingup liquidity under a company’s traditional revolver

Up to 5 year term with fixed, transparent pricing

No balance sheet impact unless an LC is drawn, and

Financial strength of issuing bank (DB rated Aa3 / A+)

Proven structure (10+ facilities extended to date

LCs require beneficiaries to issue standingdraw instructions to be used upon occurrence of aCompany’s Credit Event (i.e. auto-draw)

Likely more expensive due to CDS-based pricing vs.“subsidized” credit facility pricing

DB-LC does not provide for funded loans – LCs only

Early cancellation of committed capacity is subject tomake whole prepayment fees

48

Deutsche Bank

Alternatives to Current CP Back

Tab EAlternatives to Current CP Back-stop Programs

Deutsche Bank

Overview of potential alternatives

Solution

1) Bifurcation of RevolvingCredit Facilities(1)

Two documentation alternatives:

a) Establish a sub-limit for “CP Backdrawn to repay CP above the sub

b) Document two distinct facilities

2) Synthetic ContingentLiquidity Facility

An SPV issues term bonds into the capital markets, guaranteed by a corporate sponsor– Bond proceeds are re-invested in UST money market funds

Corporate sponsor enters into an agreement with SPV, whereby it can draw on the cash in exchange fordelivering new senior bonds to the SPV– Corporate sponsor pays a running premium to the SPV, which (together with interest

cover coupon payments on the SPV bonds

SPV bonds remain off-balance sheet (and offproceeds

3) Callable Commercial PaperProgram(2)

(for “A-1/P-1” or better names only)

Establish a new CP program where issuance is limited to CP with a final maturity of 60 daysissuer call option on Day 30-45– If CP is called, company would refinance with new CP under the program

– If CP is not called, company would pay a step

– If company does not call, and cannot refinance, existing CP would mature on final maturity date

A bi-lateral liquidity facility from DB would back

Below we present three potential solutions aimed at mitigating the higher cost / reduced availability of CP backDB can work with our clients to explore these (and other) ideas in more detail

(1) Documentation and administration process around(2) Market and infrastructure (e.g. DTC) will need to develop further to allow for sizable issuanceSource: Deutsche Bank

Overview of potential alternatives

Description

limit for “CP Back-stop” use within existing revolving credit facilities (facility could not bedrawn to repay CP above the sub-limit amount); or

two distinct facilities – one for CP Back-stop, the other for GCP (with distinct pricing for each)

An SPV issues term bonds into the capital markets, guaranteed by a corporate sponsorinvested in UST money market funds

Corporate sponsor enters into an agreement with SPV, whereby it can draw on the cash in exchange fordelivering new senior bonds to the SPV

Corporate sponsor pays a running premium to the SPV, which (together with interest on the collateral)cover coupon payments on the SPV bonds

balance sheet (and off-credit) for the corporate sponsor unless it draws on the

where issuance is limited to CP with a final maturity of 60 days or longer, with

If CP is called, company would refinance with new CP under the program

If CP is not called, company would pay a step-up penalty rate (to incentivize it to call)

If company does not call, and cannot refinance, existing CP would mature on final maturity date

lateral liquidity facility from DB would back-stop the new CP program (requiring >30-day notice to draw)

Below we present three potential solutions aimed at mitigating the higher cost / reduced availability of CP back-stop facilities;DB can work with our clients to explore these (and other) ideas in more detail

Documentation and administration process around sub-limits needs to be developed furtherMarket and infrastructure (e.g. DTC) will need to develop further to allow for sizable issuance 50

Deutsche Bank

Mechanics of a Credit Support Annex (CSA)

Tab FMechanics of a Credit Support Annex (CSA)

Deutsche Bank

(120)(100)

(80)(60)(40)(20)

02040

Feb-06 Jul-06 Nov-06 Mar-07 Jul-07

$m

m

Posting to counterparty under CSA

Mechanics of CSAs

(a) Collateral posting requirement on a $500mm 10y swap executed in FebSource: Deutsche Bank Global Markets

A Credit Support Annex (“CSA”) to an ISDA Master Agreement provides for counterparties to postcollateral (typically cash or Treasuries) against the mark

A party who is out-of-the-money by an amount greater than a predetermined threshold posts to theother party collateral equal to excess of the market value over the threshold

The threshold represents the maximum uncollateralized exposure, and may be zero

In the event of default, the non-defaulting party liquidates collateral to cover the termination cost ofthe ISDA

Basel 3 imposes newcapital charges onbanks for counterpartycredit risk in OTCderivatives, resulting inincreased transactioncosts

Execution of a 2-wayCSA can significantlymitigate such costs

Illustrative Collateral Posting Example (w/Threshold)

Dec-07 Apr-08 Aug-08 Dec-08 Apr-09 Sep-09 Jan-10 May-10 Sep-10 Feb-11

Posting from counterparty under CSA Swap mark-to-market Threshold

Collateral posting requirement on a $500mm 10y swap executed in Feb 2006, assuming a CSA threshold of $15mm

Implementing a CSA

A Credit Support Annex (“CSA”) to an ISDA Master Agreement provides for counterparties to postcollateral (typically cash or Treasuries) against the mark-to-market of the derivatives portfolio

money by an amount greater than a predetermined threshold posts to theother party collateral equal to excess of the market value over the threshold

The threshold represents the maximum uncollateralized exposure, and may be zero

defaulting party liquidates collateral to cover the termination cost of

Illustrative Collateral Posting Example (w/Threshold) (a)

52

Deutsche Bank

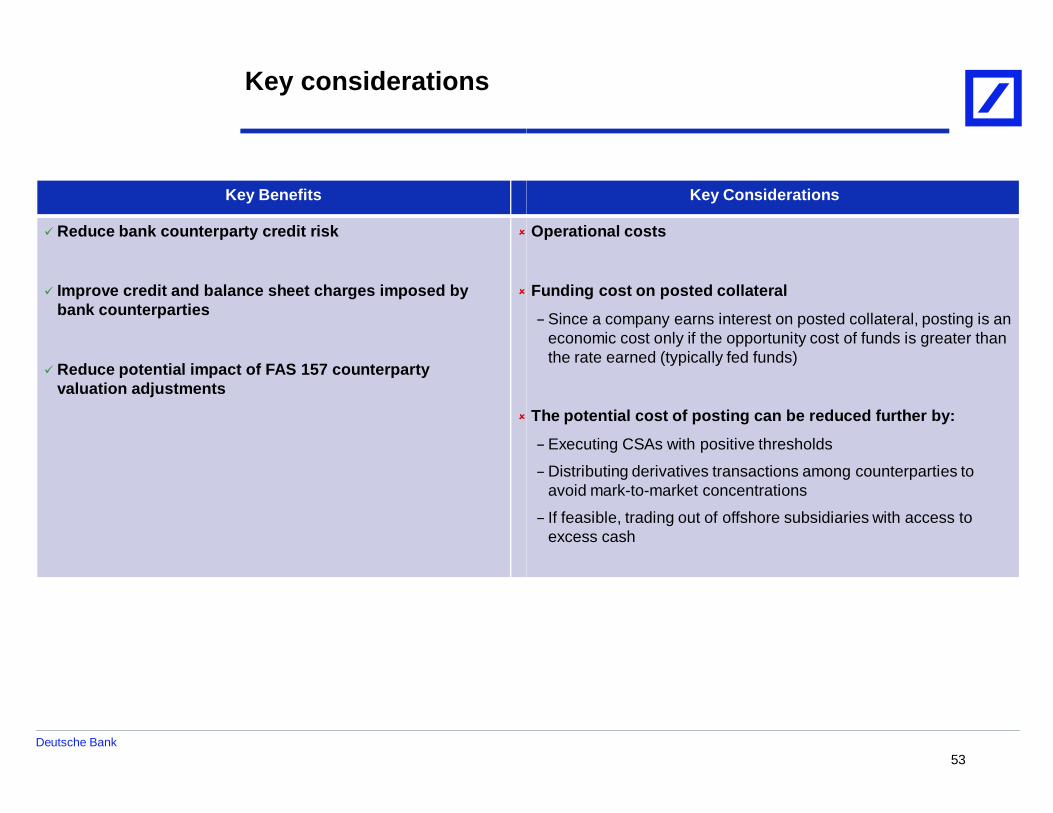

Key considerations

Key Benefits

Reduce bank counterparty credit risk

Improve credit and balance sheet charges imposed bybank counterparties

Reduce potential impact of FAS 157 counterpartyvaluation adjustments

Key Considerations

Operational costs

Funding cost on posted collateral

– Since a company earns interest on posted collateral, posting is aneconomic cost only if the opportunity cost of funds is greater thanthe rate earned (typically fed funds)

The potential cost of posting can be reduced further by:

– Executing CSAs with positive thresholds

– Distributing derivatives transactions among counterparties toavoid mark-to-market concentrations

– If feasible, trading out of offshore subsidiaries with access toexcess cash

53

Deutsche BankDeutsche BankCapital Markets and Treasury Solutions

Appendix VII

Appendix A: Additional Basel 3 Information

Deutsche BankCapital Markets and Treasury Solutions

Appendix A: Additional Basel 3 Information

Deutsche Bank

Implementation timeline

2012

Cap

ital

RiskCoverage Counterparty Risk Introduction

Capital Base

Core Tier 1 Ratio 2.0%Tier 1 Ratio 4.0%Total Capital Ratio 8.0%

Phase-in reg. deductions

Instruments no longer qualify forTier 1/Tier 2

CapitalBuffers

Conservation Buffer

Countercyclical Buffer

G-SIB Buffer

LiquidityLCR ObservationNSFR Observation

Leverage Leverage Ratio Monitoring

(1) G-SIBs will be allocated into 4 buckets based on their scores of systemic importance, with various levels of additionalloss absorbency requirements applied to each bucket

Source: Basel Committee on Banking Supervision, DB GTB Asset and Liability Management

Implementation timeline

Roll Out Fully Effective

2013 2014 2015 2016 2017 2018 2019

Introduction

3.5% 4.0% 4.5% 4.5% 4.5% 4.5% 4.5%4.5% 5.5% 6.0% 6.0% 6.0% 6.0% 6.0%8.0% 8.0% 8.0% 8.0% 8.0% 8.0% 8.0%

20% 40% 60% 80% 100% 100%

90% 80% 70% 60% 50% 40% 30%

0.625% 1.25% 1.875% 2.50%

Phased in at discretion of national regulator

1.0% - 3.5% surcharge introduced in parallelwith conservation and countercyclical buffers (1)

IntroductionIntroduction

Parallel running Disclosure Introduction

scores of systemic importance, with various levels of additional

Basel Committee on Banking Supervision, DB GTB Asset and Liability Management 55

Deutsche Bank

Basel 3 capital requirements

Higher Core Capital Ratio Requirements

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Current Basel III Current

Minimal Capital Requirement Conservation Buffer = 2.5%

Common Equity

2.0%

4.5%

7.0%

9.5%

13.0%

4.0%

G-SIB: Global systemically important banksSource: Deutsche Bank, BCBS Press Release

The new Basel 3 framework substantially increases minimum capital requirements, andredefines Tier 1 capital to exclude hybrid instruments and other securities

Basel 3 capital requirements