themes > chapter: fx divergence implications for 4q and

TRANSCRIPT

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: FX Divergence Implications for 4Q and 2016 >> Exhibit 1 of 12

Currency Divergence to Impact Earnings Across Regions, SectorsAnalyst: Tim CraigheadDec 14, 2015Currency volatility remains a keyfactor for 4Q earnings as it has beenthroughout 2015. The dollar remainsa pillar of strength, along with thepound sterling. The euro has beenweak, lagging even the yen. Inemerging markets, trade-weighteddeclines are pervasive along withfalling energy and material pricesacross many commodity-producingeconomies. The yuan appears tobe at an inflection point and maytransition from 10 years of strengthto a period of managed weakening.

Key Points:* Dollar, Pound Dominate as Yuan Changes Course With PBOCAction* Emerging Currencies' Drop is Due to More Than Dollar Strength* Real Emerging Currency Weakness Extends Beyond ModestChina Dip* EM Currency Weakness Portends Mixed Blessings forMultinationals* PBOC's Yuan Shift Belongs in the Context of Longer 10-YearClimb

China TeamBloomberg Intelligence

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: FX Divergence Implications for 4Q and 2016 >> Exhibit 2 of 12

Dollar, Pound Dominate as Yuan Changes Course With PBOC ActionAnalyst: Tim CraigheadDec 11, 2015The dollar's 8.9% trade-weightedgain so far this year dominates thecurrency landscape. In Europe, theBritish pound is up relative to thecontinent, and Israel's shekel hassurged through the year. Companiesin these countries may benefitfrom lower import costs, yet facestiffer global competition on pricing.The yuan has changed coursesince the PBOC's August policyaction, though it's still up 3.8%.Singapore's trade-weighted currencyis also strong relative to many closeregional trading partners.

The Few, the Proud, the Strong Trade-Weighted

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence G BI3 4109<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: FX Divergence Implications for 4Q and 2016 >> Exhibit 3 of 12

Emerging Currencies' Drop is Due to More Than Dollar StrengthAnalyst: Tim CraigheadDec 11, 2015There is more to weakeningexchange rates across emergingmarkets than the dollar's strength.On a trade-weighted basis, manydeveloping-country currencies aredown more than 10% since theend of 2014. Companies in thesemarkets might gain a competitiveedge against foreign rivals as aresult. They also face inflated costson imported inputs, though tumblingprices in energy and metals mayprovide an offset for some. Brazil'sreal is the worst performing amongthe group.

Slip Sliding Away: Weaker Trade-Weighted FX

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence G BI3 4110<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

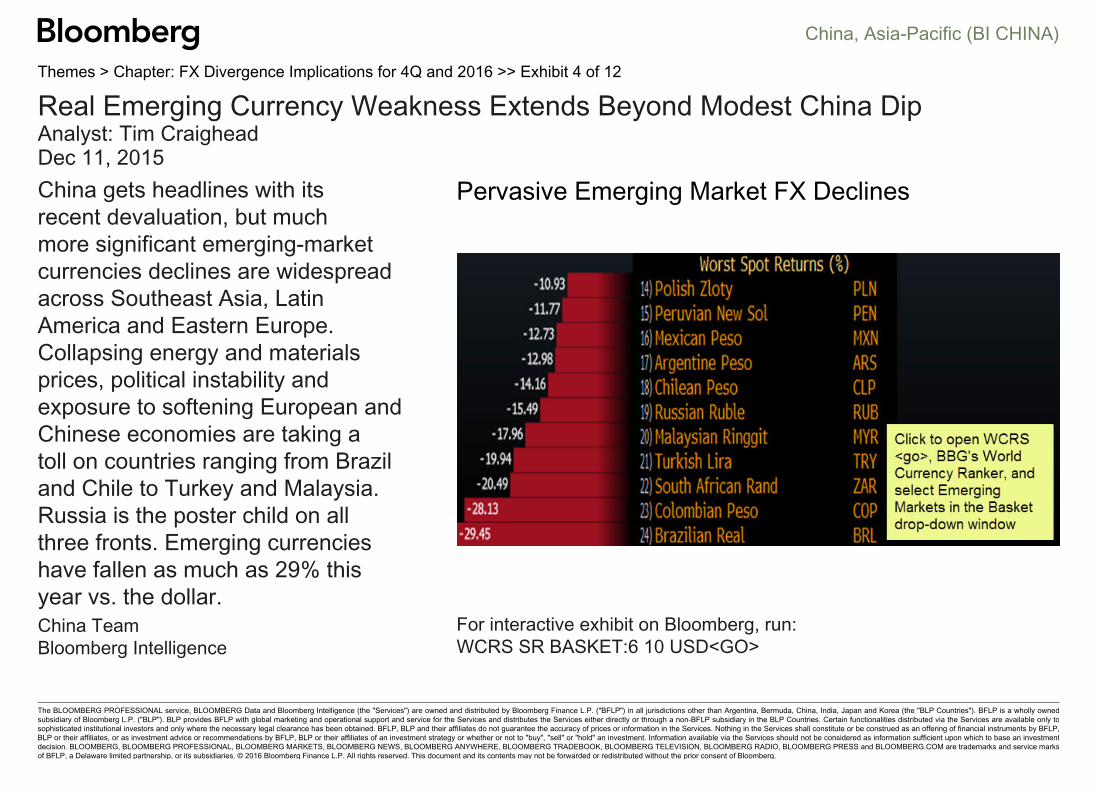

Themes > Chapter: FX Divergence Implications for 4Q and 2016 >> Exhibit 4 of 12

Real Emerging Currency Weakness Extends Beyond Modest China DipAnalyst: Tim CraigheadDec 11, 2015China gets headlines with itsrecent devaluation, but muchmore significant emerging-marketcurrencies declines are widespreadacross Southeast Asia, LatinAmerica and Eastern Europe.Collapsing energy and materialsprices, political instability andexposure to softening European andChinese economies are taking atoll on countries ranging from Braziland Chile to Turkey and Malaysia.Russia is the poster child on allthree fronts. Emerging currencieshave fallen as much as 29% thisyear vs. the dollar.

Pervasive Emerging Market FX Declines

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence WCRS SR BASKET:6 10 USD<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: FX Divergence Implications for 4Q and 2016 >> Exhibit 5 of 12

EM Currency Weakness Portends Mixed Blessings for MultinationalsAnalyst: Tim CraigheadDec 11, 2015Declining currencies in emergingmarkets across Asia, Latin Americaand Eastern Europe are a swordcutting both ways for multinationalcompanies. Their products willbe costlier for buyers in thesemarkets, and their revenue willshrink when it's translated backfrom weaker currencies. Their profitmargins, however, may benefitfrom lower local manufacturing andSG&A costs. Input sourcing andhedging muddy the picture. Clickon the links for interactive screensof multinationals with EM salesexposure.

Key Points:* S.E. Asia: Developed Market Firms Selling to S.E. Asia IncludeJardine Matheson and AIA* LatAm: Companies With Latin American Sales Exposure IncludeMillicom, Ternium, AES* U.K.: British Multinationals With Significant Weak-Currency SalesInclude Old Mutual, Kingfisher and Vodafone* U.S.: Many American Companies Have Emerging-Market and EUSales Including Priceline, Mosaic and Colgate-Palmolive

China TeamBloomberg Intelligence

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: FX Divergence Implications for 4Q and 2016 >> Exhibit 6 of 12

PBOC's Yuan Shift Belongs in the Context of Longer 10-Year ClimbAnalyst: Tim CraigheadDec 10, 2015This year's PBOC's yuan policychange needs to be viewed in along-term context. Weakeningthe yuan by 1.9% in August wasthe largest one-off adjustment onrecord. And it probably also marksa clear shift in stance from years ofpromoting yuan strength. Yet yuanmovements tend to be gradual andlong-term in nature. The 52% gain inthe trade-weighted yuan since 2005was significant, yet it took place over10 years. Other factors have drivenshort-term cycles and will likely doso in the future.

Trade-Weighted Yuan Long & Strong

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence g bi3 2286<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: FX Divergence Implications for 4Q and 2016 >> Exhibit 7 of 12

Yuan Strength May Turn to Weakness in New Era for China CurrencyAnalyst: Tim CraigheadDec 10, 2015The yuan is plateauing on a trade-weighted basis and will probablyshow an annualized decline in 1Q2016. On this basis, its 3% gain in4Q is the smallest since early 2014.It's still up the yen and euro, butdown against the dollar followingthe PBOC's policy shift in August.Ongoing export declines also pointto a need to negate a growingcompetitive headwind for many ofChina's regional trading partnerswith relatively weak currencies. IMFSpecial Drawing Rights approvalthis month may limit depreciation.

Yuan Hits Plateau, New Direction Possible

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence g bi3 2287<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: FX Divergence Implications for 4Q and 2016 >> Exhibit 8 of 12

Weaker Yuan May Stoke Competition, Lower Costs For Global FirmsAnalyst: Tim CraigheadDec 10, 2015Companies around the world mayhave to alter their global strategiesif the PBOC's yuan reset starts anew trajectory. Even if weakening isgradual, China's manufacturing andgrowing services capability wouldbe more competitive. Currencytranslations on exports to China, amajor source of revenue for sellersof everything from tech gadgets toautos, fried chicken to handbags,would be reduced. While importsfrom mainland China would becheaper, growth in its outboundtravel could slow.

Global Firms With Notable China Sales

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence EQS /SAMPLE 12701435 /RESULTS<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: FX Divergence Implications for 4Q and 2016 >> Exhibit 9 of 12

Yuan Shift May Stimulate Exporters from China, Vex ImportersAnalyst: Tim CraigheadDec 10, 2015A sustained yuan weakeningwould have both positive andnegative implications for Chinesecompanies. It could boost exportcompetitiveness or translatedrevenue or both, reversing a trendthat has been in place with fewexceptions since 2005. For thosethat import into China, costs couldgo up. Servicing dollar debt will bemore expensive. These effects willtake time to play out, especiallywith the trade-weighted yuan still upabout 3% vs. the 4Q 2014 average.

China Firms With Big International Sales

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence EQS /SAMPLE 12701449 /RESULTS<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: FX Divergence Implications for 4Q and 2016 >> Exhibit 10 of 12

Impact of Yen's Second Slide Is Fading, Could Disappear SoonAnalysts: Tim Craighead & Elaine TungDec 14, 2015The dollar and other currenciescontinued to strengthen vs. theyen so far in 4Q, but the effectis waning. The dollar is up about6% from a year ago vs. about20% earlier this year. Challengesposed by rising import prices areeasing for companies that sell inJapan. The negative translationeffect on revenue generated in yenis diminishing as well. Japanesecompanies' overseas sales, on theother hand, have been magnified bythe weaker yen, while import costsinflated. This effect, too, is fading.

Dollar Gains vs. Yen

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence G BI3 4107<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: FX Divergence Implications for 4Q and 2016 >> Exhibit 11 of 12

Euro Weakness Persists in 4Q vs. Dollar, Major Asia CurrenciesAnalysts: Tim Craighead & Elaine TungDec 14, 2015Europe's slowing economy andinitiation of quantitative easing havepushed the euro down vs. mostmajor currencies. The yuan hasjumped 10% vs. the euro, on ayear-on-year basis, so far in 4Q,and many Asian currencies aretied to the U.S. dollar, up 14%against the euro. The yen trailsafter Japan's aggressive policyeasing, but it's still up 7% vs. theeuro. Asian companies' exportrevenue to Europe may be hurt bytheir stronger relative currencies,and their products are at risk ofbecoming less competitive.

Yuan, Dollar Outpace Yen Against Weak Euro

China Team For interactive exhibit on Bloomberg, run:Bloomberg Intelligence g BI3 4108<GO>

China, Asia-Pacific (BI CHINA)

The BLOOMBERG PROFESSIONAL service, BLOOMBERG Data and Bloomberg Intelligence (the "Services") are owned and distributed by Bloomberg Finance L.P. ("BFLP") in all jurisdictions other than Argentina, Bermuda, China, India, Japan and Korea (the "BLP Countries"). BFLP is a wholly ownedsubsidiary of Bloomberg L.P. ("BLP"). BLP provides BFLP with global marketing and operational support and service for the Services and distributes the Services either directly or through a non-BFLP subsidiary in the BLP Countries. Certain functionalities distributed via the Services are available only tosophisticated institutional investors and only where the necessary legal clearance has been obtained. BFLP, BLP and their affiliates do not guarantee the accuracy of prices or information in the Services. Nothing in the Services shall constitute or be construed as an offering of financial instruments by BFLP,BLP or their affiliates, or as investment advice or recommendations by BFLP, BLP or their affiliates of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. Information available via the Services should not be considered as information sufficient upon which to base an investmentdecision. BLOOMBERG, BLOOMBERG PROFESSIONAL, BLOOMBERG MARKETS, BLOOMBERG NEWS, BLOOMBERG ANYWHERE, BLOOMBERG TRADEBOOK, BLOOMBERG TELEVISION, BLOOMBERG RADIO, BLOOMBERG PRESS and BLOOMBERG.COM are trademarks and service marksof BFLP, a Delaware limited partnership, or its subsidiaries. © 2016 Bloomberg Finance L.P. All rights reserved. This document and its contents may not be forwarded or redistributed without the prior consent of Bloomberg.

Themes > Chapter: FX Divergence Implications for 4Q and 2016 >> Exhibit 12 of 12

Euro, Yen, Dollar Shifts Top Corporate Considerations Into 2016Analyst: Tim CraigheadDec 14, 2015Cross-rate shifts between theeuro, yen, yuan and dollar will be adriver of operational and financialperformance across regions in 4Qand into 2016. Regional exposureswill determine whether companiesgain or lose. Japanese firms withinternational sales, for example,may get a sales boost, whilecompanies in other parts of Asiawith European businesses will facerevenue headwinds. Click on thebullet points to analyze specificEuropean and Japanese companies'geographic exposures.

Key Points:* Asia to Europe: Must Deal With Slowing Economy, WeakeningEuro* Japan Exporters: Firms Selling Abroad Will Have Fading SecondBoost From Weak Yen* Global to Japan: Firms Trading With Japan Suffer DecreasingCompetitive, Currency-Translation Obstacles

China TeamBloomberg Intelligence