thee competitiveness of south african manufacturing and the role of technology strategic...

TRANSCRIPT

Thee Competitiveness of South African Manufacturing and the Role of Technology

Strategic Communications

5th CSIR Annual Conference9 September 2015

Outline of Presentation

2

Introduction to FTI Consulting

Inroductory Remarks

Recent Economic Outcomes in SA & Manufacturing

Changing Global Manufacturing Landscape

Policy & Strategic Agenda for Manufacturing

Section 1

3

Introduction to FTI Consulting

FTI Consulting: Who We Are

FCNPublicly traded

$1.58BLNMarket capitalization(1)

1982Year founded

4,400+Total employees worldwide

440+Senior Managing Directors

2 Nobel Laureates

10/10Advisor to the world’s top 10 bank holding companies

94/100Advisor to 94 of the world’s top 100 law firms

47/10047 of Global100 corporations are clients

16Experts in 16 industry specialties

79Offices in 79 cities around the globe

(1)Total Shares outstanding times the closing share price as of December 31, 2014.4

We Advise Across A Global Economy

Asia Pacific

AustraliaBrisbaneGold CoastMelbournePerthSydney

ChinaBeijingGuangzhouHong Kong Shanghai

IndiaMumbaiNew Delhi

IndonesiaJakarta

JapanTokyo

Singapore

Europe, Middle East, Africa

BelgiumBrussels

DenmarkCopenhagen

FranceParis

GermanyBerlinFrankfurt

IrelandDublin

QatarDoha

RussiaMoscow

South AfricaCape TownJohannesburg

SpainMadrid

United Arab EmiratesAbu DhabiDubai

United KingdomLondonStirling

Latin America

ArgentinaBuenos Aires

BrazilRio de Janeiro São Paulo

CaribbeanBritish Virgin IslandsCayman Islands

ColombiaBogotá

MexicoMexico City

PanamaPanama City

North America

CanadaCalgaryTorontoVancouver

United StatesAnnapolisAtlantaBaltimoreBostonBrentwoodCharlotteChicagoCoral GablesDallas

Denver

Great Neck

Houston

Indianapolis

Los Angeles

McLean

Miami

Mountain View

New York

Oakland

Pasadena

Philadelphia

Phoenix

PittsburghPortland

Princeton

Red Bank

Rockville

RoselandSaddle Brook

San Francisco

Santa Barbara

Seattle

Tucson

Walnut Creek

Washington, D.C.

Wayne

West Palm Beach

Winston-Salem5

3,300+ ProfessionalsDeployed in 26 Countries

With offices in every major financial centre and every corner of the globe, we successfully serve our clients wherever challenges and opportunities arise.

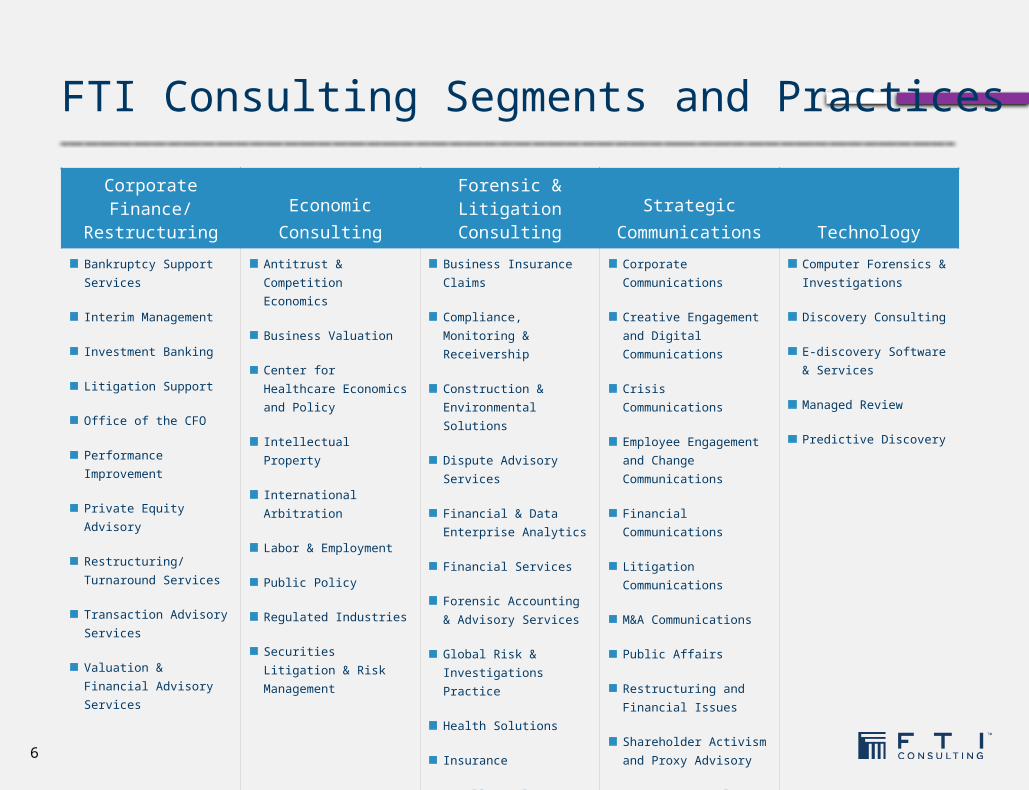

FTI Consulting Segments and Practices

Corporate Finance/

RestructuringEconomicConsulting

Forensic &Litigation

ConsultingStrategic

Communications Technology

Bankruptcy Support Services

Interim Management

Investment Banking

Litigation Support

Office of the CFO

Performance Improvement

Private Equity Advisory

Restructuring/Turnaround Services

Transaction Advisory Services

Valuation & Financial Advisory Services

Antitrust & Competition Economics

Business Valuation

Center for Healthcare Economics and Policy

Intellectual Property

International Arbitration

Labor & Employment

Public Policy

Regulated Industries

Securities Litigation & Risk Management

Business Insurance Claims

Compliance, Monitoring & Receivership

Construction & Environmental Solutions

Dispute Advisory Services

Financial & Data Enterprise Analytics

Financial Services

Forensic Accounting & Advisory Services

Global Risk & Investigations Practice

Health Solutions

Insurance

Intellectual Property

Trial Services

Corporate Communications

Creative Engagement and Digital Communications

Crisis Communications

Employee Engagement and Change Communications

Financial Communications

Litigation Communications

M&A Communications

Public Affairs

Restructuring and Financial Issues

Shareholder Activism and Proxy Advisory

Strategy Consulting & Research

Computer Forensics & Investigations

Discovery Consulting

E-discovery Software & Services

Managed Review

Predictive Discovery

6

FTI Consulting South Africa

7

Majority-owned by FTI Consulting – New York-listed firm

SA offices in Johannesburg and Cape Town

Heavyweight and medium-weight resourcing approach

BEE Level 2 certification – July 2015

SEC compliance and regulatory standards in everything we do!

Section 2

8

Inroductory Remarks

In recent decades SA has been experiencing a gradual

de-industrialization, driven by a cocktail of factors

A Schematic History of SA Manufacturing

Source: Adapted from GIBS

1. The nature of global manufacturing business model is changing, with implications for competitiveness of SA industries.

2. Manufacturing stakeholders in the public and private sectors as well as civil society need to rethink revival strategies for the sector accordingly.

3. Technically, speaking of “manufacturing” is somehow misleading; we need to focus on ‘industries’ as each has its own technical, market-structure and geographic dynamics.

4. The pace of change creates inordinate complexity for industrial policy making- old style policy formulation is a waste of opportunity!

Introductory remarks

Section 3

11

Recent Economic Outcomes in SA & Manufacturing

The performance of SA’s economy remains tied to that of its manufacturing sector

Annual growth in GDP and manufacturing production, South Africa, 1974 - 2014

Source: SARB and PAIRS

-10.0

-7.5

-5.0

-2.5

0.0

2.5

5.0

7.5

10.0

GDP at market prices

Pe

r ce

nt

-4 -2 0 2 4 6 8-15

-10

-5

0

5

10

15

GDP at market pricesM

an

ufa

ctu

rin

g o

utp

ut

Manufacturing contribution to GDP typically rises as the

economy develops but SA has been an exception

Source: McKinsey Global Institute and PAIRSNote: 1 1990 International dollars

1995-2014 SA Average =

15.3%

Manufacturing share in an economy

2013 SA per capita GDPUSD6886.3 (World Bank)

In addition to falling short by standards, SA manufacturing contribution to GDP has gradually

been declining

Manufacturing contribution to GDP, South Africa, 1963 - 2014

Source: SARB and PAIRS

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

2014

0

5

10

15

20

Pe

r ce

nt

Commodities still dominate in terms of the share of total SA exports

Source: IMF, Haver , SARS and PAIRS

SA export products (% of total exports, average 2010 – 2013)

Mineral products

24%

Precious metals

21%

Base metals13%

Vehicles9%

Machinery9%

Others24%

Sub-Saharan Africa has emerged as a key destination for SA exports

Source: IMF, Haver , SARS and PAIRS

Export markets (% of total exports, average 2010 – 2013)

sub-Saharan Africa26%

Euro area14%

China11%

US8%

Japan6%

ROW35%

Meanwhile, SA’s share of global exports has lagged that of its BRICS peers

South Africa’s share of global trade in context, 2001 - 2013

Source: TradeMap and PAIRS

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

0

2

4

6

8

10

12

14

SA Brazil IndiaChina Russia

Pe

r ce

nt

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

SA Brazil India Russia

Pe

r ce

nt

Rising manufacturing unit labour cost is eroding competitiveness

Manufacturing employment, labour productivity and unit labour cost, South Africa, 2000 - 2013

Source: SARB and PAIRS

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

0

50

100

150

200

250

Employment Labour productivity Unit labour cost

Ind

ex (

20

00

=1

00

)

Onset of widening gap between labour cost and productivity

SA scores below the median of EMEs in many other respects

SA’s competitiveness score in context , 2014/15

Source: WEF, OECD and IMF

Ten most problematic factors for SA exporters in 2013

Technical requirements and standards abroad

rules of origin requirements abroad

Difficulties in meeting qlity/qtity requirements of buyers

Corruption at foreign borders

Access to trade finance

High cost or delays caused by international transporta-tion

Inappropriate production technology and skills

Burdensome procedures at foreign borders

Tariff barriers abroad

Identifying potential markets and buyers

Access to imported inputs at competitive prices

High cost or delays caused by domestic transportation

3.9

3.9

4.6

5.4

5.8

8.7

8.9

8.9

9.3

11.2

12.9

16.6

Sco

re

Section 4

21

Changing Global Manufacturing Landscape

Final product assembly is the most common entry point for African manufacturers into global value

chain

Top activities performed in manufacturing value chains in Africa, 2014

After-sales customer service

Design, research and development

Ancillary services (input retail, equipment services)

Sales and marketing

Intermediate inputs (production of components, modules)

Packaging and shipping

Final product assembly

0% 100%

24%

33%

44%

56%

58%

64%

79%

Share of respondents

Source: 2014 AEO Experts Survey and PAIRS

Note: Based on a survey of AEO country economists.

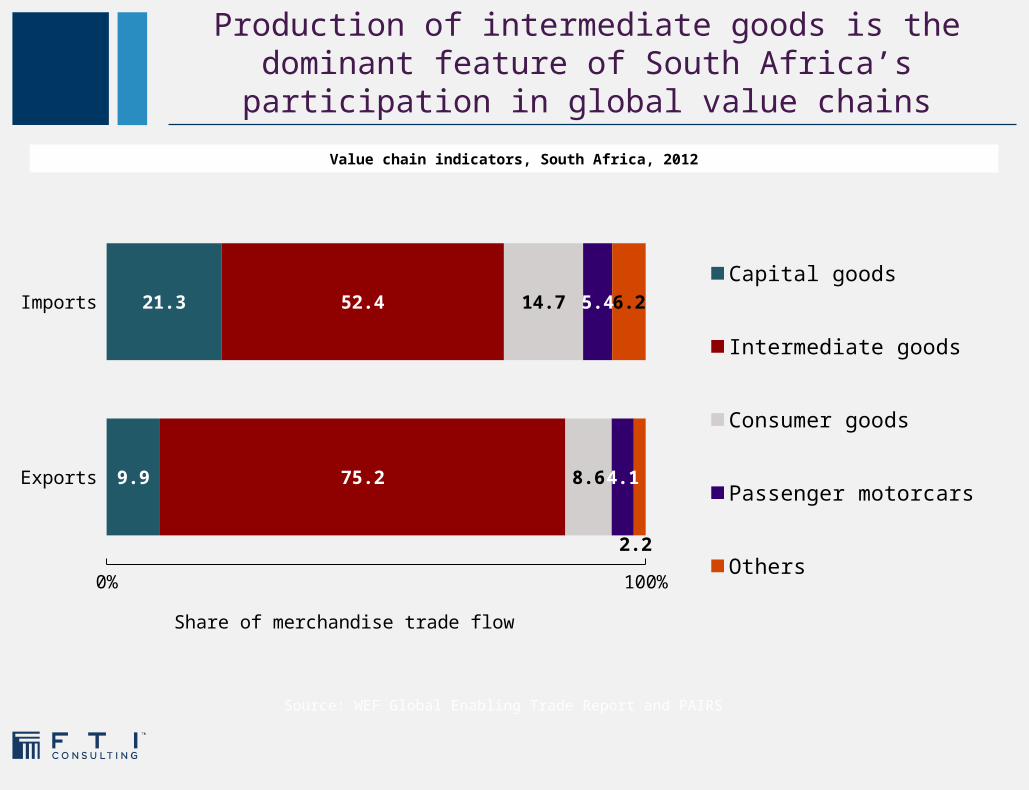

Production of intermediate goods is the dominant feature of South Africa’s participation in global value

chains

Value chain indicators, South Africa, 2012

Exports

Imports

0% 100%

9.9

21.3

75.2

52.4

8.6

14.7

4.1

5.4

2.2

6.2

Capital goods

Intermediate goods

Consumer goods

Passenger motorcars

Others

Share of merchandise trade flow

Source: WEF Global Enabling Trade Report and PAIRS

1. Improvements in ICT and transport infrastructure have contributed to the globalisation of manufacturing value chains.

2. Outsourcing and off-shoring of functions within companies’ manufacturing value chains are rising.

3. The following factors drive this trend:

a. Containing cost and improving productivity;b. Penetrating new markets; andc. Gaining access to strategic assets in other

countries e.g. skilled labour and technological know-how.

Changing global manufacturing practices

Source: Adapted from BIS

1. The concept of “manufacturing” is no longer understood in terms of production alone; it increasingly encompasses varying types of activities:

2. In fact, distinctions between manufacturing and services are no longer clear-cut.

Changing global manufacturing practices

Research Design Production

Logistics &

distribution

Sales & marketing

After sales

services

Illustrative manufacturing value chain

Source: Adapted from BIS

1. “Servitization” refers to the innovation of an organisation’s capabilities and processes to generate greater value via a shift from selling products to selling Product-Service Systems (Neely 2013).

2. As such, addressing SA’s manufacturing competitiveness stalemate and reviving the sector’s performance requires taking into account and embracing the emerging global trends.

3. The servitization of manufacturing is happening during an era characterised by creative destruction and the emergence of disruptive technologies.

More than producing goods:From manufacturing to “manu-services”

Creative destruction and the “age of discontinuity”

Source: McKinsey

Average lifetime of S&P 500 companies

Challenging the status quo:the advent of disruptive technologies

Source: Adapted from McKinsey Global Institute

Some key potentially economically disruptive technologies

Cloud technology

The internet of things

Automation of knowledge work

Mobile internet

Meanwhile, ICT affordability and skills stock in SA falls below the average of peer countries

Source: WEF, Global Information Technology Report (2014)

High score = better

Section 5

30

Policy & Strategic Agenda for Manufacturing

To succeed in repositioning SA manufacturing performance in a changing global environment

requires a concerted effort

Public sector:•Create a positive environment for the sector through strategically coherent policies and institutions•Promoting frank and robust engagement with the private sector

Private sector:•Provide effective on-the-job training and promoting technology-related training•Pro-actively engaging in industrial policy making

Appropriate Infrastructure & Operational Environment:•Critical infrastructure: power, transportation, ...•Industrial relations stability

Source: Adapted from GIBS

Introducing Advanced Manufacturing Technologies will require us to go the Extra Mile

Source: Adapted from GIBS

“A lot of incentives would be required, before a widespread adoption of industry 4.0 applications amongst South African manufacturers will happen.“ “The lack of infrastructure is a key risk for the success of the industrial internet in South Africa. That needs to be overcome first.“ “A lot of South African manufacturers are focused on immediate issues, like labour and electricity. There is a general lack of focus on building for the future and investing in education and training as well as R&D and innovation.“ “A shortage of skills should not stop new investments in technology. Skills will eventually catch-up with industry needs or training will happen.“

Thank you for your attention

[email protected]: 011 214 2400

Content Acknowledgement: Pan African Research and Investment Services and the Manufacturing Circle

Contact Details