the world bankdocuments.worldbank.org/curated/en/679381468144890689/pdf/34912.pdfthe world bank...

TRANSCRIPT

Document of The World Bank

Report No: 34912

IMPLEMENTATION COMPLETION REPORT(IDA-40310 FSLT-72700)

ON A

LOAN AND CREDIT

IN THE AMOUNT OF US$ 300 MILLION

TO THE

PAKISTAN

FOR A

BANKING SECTOR DEVELOPMENT POLICY PROGRAM

JANUARY 17, 2006

Finance and Private Sector Development UnitSouth Asia Region

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective January 17, 2006)

Currency Unit = Pakistani Rupees (Rs) Rs. 1 = US$ 0.0167

US$ US$ 1 = Rs. 59.94

FISCAL YEARJuly 1 June 30

ABBREVIATIONS AND ACRONYMS

ABL Allied Bank LimitedADB Asian Development BankAML Anti-Money LaunderingBCO Banking Companies Ordinance of 1962BSAL Banking Sector Adjustment LoanBSAL Banking Sector Adjustment LoanBSDP Banking Sector Development ProgramCAR Capital Adequacy RequirementCAS Country Assistance StrategyCIRC Corporate and Industrial Restructuring CorporationDFI Development Finance InstitutionFA Financial AdvisorFCD Foreign Currency DepositFSAP Financial Sector Assessment ProgramFSDIP Financial Sector Deepening and Intermediation ProjectGOP Government of PakistanHBFC Housing Building Finance CorporationHBL Habib Bank LimitedICP Investment Corporation of PakistanIDBP Industrial Development Bank of PakistanIRAF Institutional Risk Assessment FrameworkMCB Muslim Commercial BankMOF Ministry of FinanceNAB National Accountability BureauNBP National Bank of PakistanNCB Nationalized Commercial BankNDFC National Development Finance CorporationNIT National Investment TrustNSS National Savings SchemeOAEM Other Assets Especially MentionedPC Privatization CommissionPRSC Poverty Reduction Strategy PaperSBP State Bank of PakistanSMEB SME Bank LimitedUBL United Limited ABLZTBL Zari Taraqiati Bank Limited

Vice President: Praful C. PatelCountry Director John W. WallSector Manager Simon C. Bell

Task Team Leader/Task Manager: Kiatchai Sophastienphong

PAKISTANPakistan Banking Sector Development Policy Program

CONTENTS

Page No.1. Project Data2. Principal Performance Ratings3. Assessment of Development Objective and Design, and of Quality at Entry4. Achievement of Objective and Outputs5. Major Factors Affecting Implementation and Outcome6. Sustainability7. Bank and Borrower Performance8. Lessons Learned9. Partner Comments10. Additional InformationAnnex 1. Key Performance Indicators/Log Frame MatrixAnnex 2. Project Costs and FinancingAnnex 3. Economic Costs and BenefitsAnnex 4. Bank InputsAnnex 5. Ratings for Achievement of Objectives/Outputs of ComponentsAnnex 6. Ratings of Bank and Borrower PerformanceAnnex 7. List of Supporting DocumentsAnnex 8. Borrower's Assessment of the Project

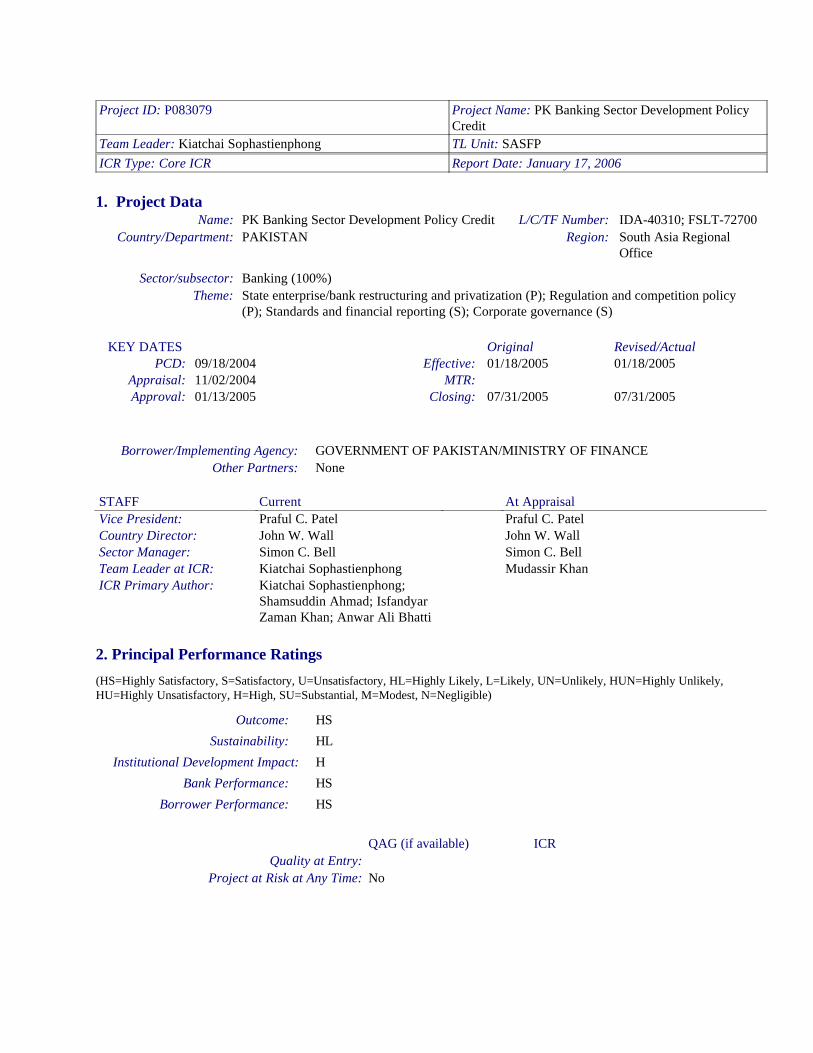

Project ID: P083079 Project Name: PK Banking Sector Development Policy Credit

Team Leader: Kiatchai Sophastienphong TL Unit: SASFPICR Type: Core ICR Report Date: January 17, 2006

1. Project DataName: PK Banking Sector Development Policy Credit L/C/TF Number: IDA-40310; FSLT-72700

Country/Department: PAKISTAN Region: South Asia Regional Office

Sector/subsector: Banking (100%)Theme: State enterprise/bank restructuring and privatization (P); Regulation and competition policy

(P); Standards and financial reporting (S); Corporate governance (S)

KEY DATES Original Revised/ActualPCD: 09/18/2004 Effective: 01/18/2005 01/18/2005

Appraisal: 11/02/2004 MTR:Approval: 01/13/2005 Closing: 07/31/2005 07/31/2005

Borrower/Implementing Agency: GOVERNMENT OF PAKISTAN/MINISTRY OF FINANCEOther Partners: None

STAFF Current At AppraisalVice President: Praful C. Patel Praful C. PatelCountry Director: John W. Wall John W. WallSector Manager: Simon C. Bell Simon C. BellTeam Leader at ICR: Kiatchai Sophastienphong Mudassir KhanICR Primary Author: Kiatchai Sophastienphong;

Shamsuddin Ahmad; Isfandyar Zaman Khan; Anwar Ali Bhatti

2. Principal Performance Ratings

(HS=Highly Satisfactory, S=Satisfactory, U=Unsatisfactory, HL=Highly Likely, L=Likely, UN=Unlikely, HUN=Highly Unlikely, HU=Highly Unsatisfactory, H=High, SU=Substantial, M=Modest, N=Negligible)

Outcome: HS

Sustainability: HL

Institutional Development Impact: H

Bank Performance: HS

Borrower Performance: HS

QAG (if available) ICRQuality at Entry:

Project at Risk at Any Time: No

3. Assessment of Development Objective and Design, and of Quality at Entry

3.1 Original Objective:

The objective of the Project, which remained unchanged throughout the project life, was to support Phase III of the banking reforms. These reforms were aligned with Financial Sector Assessment Program (FSAP) recommendations and the Government's Poverty Reduction Strategy Paper (PRSP) and included: (i) improving sector governance through privatization of United Bank Limited (UBL), Habib Bank Limited (HBL) and resolution of Allied Bank Limited (ABL); (ii) further strengthening the regulatory and supervisory environment for banking; (iii) improving transparency and disclosure; and (iv) preventing possible use of the banking system for money laundering. An assessment of the objective and design of this operation needs to be seen against the background of Pakistan's reform experience and in the context of the Bank's Country Assistance Strategy.

Background

Pakistan has implemented far-reaching reforms in the financial sector during the last decade with the help of the Bank. The banking sector has undergone fundamental changes through a three phased reform program. The first phase of reforms initiated in 1997, was supported by the Banking Sector Adjustment Loan (BSAL). The reforms managed to address the root cause of sector's problems and achieved a complete turnaround in the environment for banking in the country. The reforms involved controlling abuse of the public sector banks by vested interests through changes in laws and governance; strengthening the regulatory framework and institutions; rationalization of interest rates through reforms in the National Savings Scheme (NSS), improving the environment for enforcement of financial contracts, bringing greater transparency and disclosure of information, and operational restructuring of public sector banks. While these reforms managed to improve the environment, the sector remained government dominated and privatization efforts stalled. Realizing the need, the Government initiated a second phase of reforms with further restructuring. These reforms were supported by the Banking Sector Restructuring and Privatization Support Project (BSRPP) in 2001. Under this program public sector, banks further downsized their work force and rationalized their branch networks, reducing their overall cost structure and improving profitability. The program also managed to liberalize bank branching, and rationalized the tax structure. Together, these reforms paved the way for third phase of reforms which covered privatization of two out of the three largest commercial banks i.e., UBL and HBL and the sale of 75 percent shares of Allied Bank Limited to local investors. With the privatization of two of the three NCBs which accounted for nearly 25 percent of the system and sale of Allied Bank Limited (ABL), nearly 80 percent of country’s banking sector assets are now in private hands. As National Bank of Pakistan (NBP) is planned to be privatized only in the medium term, the bank was listed on the stock exchange. The government has so far divested 23.2 percent of the bank’s shares through public offerings. This has also brought the first generation reforms commenced in the late 1980s to near a conclusion. The Banking Sector Development Policy Program (BSDP) supports the completion of the third phase and helps with financing the costs incurred by the government in re-capitalizing these banks prior to privatization. The Government and SBP have now initiated second-generation reforms which aimed to further develop the financial markets infrastructure by improving the policy and regulatory environment and expanding access to financial services for all segments of the society and sectors of the economy.

World Bank Group Assistance Strategy

Based on the Government’s strong progress in implementing reforms, Pakistan CAS fully recognizes and supports the banking sector reforms and is aligned with the Government’s Poverty

- 2 -

Reduction Strategy. The Government regards the financial sector reforms as central to its poverty reduction and growth strategy and the PRSP clearly states the Government’s medium term strategy on the financial sector - the vision being of a financial sector that intermediates effectively and caters to all segments of the society thereby contributing to increased growth and reduced poverty in the long run.

The broad PRSP objective for the financial sector is to improve governance through restructuring, privatization, and strengthening banking supervision. Specific areas of importance within the sector include: integration of NSS rates with rates of comparable market instruments; rationalization of taxation on banking; privatization of NBP; bringing the three restructured DFIs to the point of sale or closure; restructuring of SME Bank and Zari Taraqiati Bank Limited (ZTBL); implementing Anti Money Laundering legislation and preparing bankruptcy legislation, further developing the pension and insurance systems and improving the overall framework for contractual savings.

In line with CAS and PRSP, the Bank has continued its support to Pakistan’s financial sector reforms through FSDIP, BSAL, and BSRPP. The Banking Sector Technical Assistance Project, approved in July 2002, supports further strengthening of the SBP and the SECP. The recently approved Second Poverty Alleviation Project also aims to enhance access to finance for the poor. Future assistance will focus on consolidation of existing reforms and further deepening of the financial sector. Both the PRSP and CAS recognize the importance of financial sector reforms for accelerating economic growth and reducing poverty.

3.2 Revised Objective:

None

3.3 Original Components:

Improving sector governance through privatization of UBL, HBL and resolution of ABL,lFurther strengthening the regulatory and supervisory environment for banking,lImproving transparency and disclosure, preventing possible use of the banking system for money l

laundering.

3.4 Revised Components:

None

3.5 Quality at Entry:

The project was not subjected to GAG assessment of Quality at Entry

4. Achievement of Objective and Outputs

4.1 Outcome/achievement of objective:

All the major development objectives of BSDP, namely improving sector governance through privatization of UBL, HBL and resolution of ABL, further strengthening the regulatory and supervisory environment for banking, improving transparency and disclosure and preventing possible use of the banking system for money laundering have been fully realized. The successful implementation of BSAL, BSRPP & BSDP improved the overall performance of the banking system. The divestiture of state-owned banks

- 3 -

substantially changed the structure of the banking sector and nearly 80% of sector assets is now controlled by private banks. The overall banking sector has become considerably more competitive and responsive to customers' needs.

4.2 Outputs by components:

Sector Governance Through Privatization

This component was designed to achieve better governance in the banking sector. In order to reach that goal the government carried out extensive operational restructuring of HBL and UBL to enable the eventual privatization of these banks. Restructuring measures included but were not limited to equity injections, advances against rights issue, issuance of government bonds, tax refunds and transfer of NPLs. For HBL the cost of balance sheet restructuring amounted to US$ 667 million and $ 816 million for UBL including the cost of voluntary schemes (VRS) in the two banks. With the successful privatization and adequate capitalization of these banks this component was considered successfully completed. In the case of ABL, given its precarious financial position with a negative equity of Rs. 3.97 billion (US$66 million), SBP structured a sale of additional shares of 75.35 percent of its combined paid-in capital through a limited public offering. Five investor groups were pre-qualified for bidding and ABL was sold to the highest bidder meeting the SBP’s “fit and proper” test for strategic investors at a price of Rs. 14.2 billion (US$237 million) . The price showed a high premium of Rs. 33.7 per share - reflecting the competitive banking environment, better sector governance, and the fact that the equity will stay within ABL. With the eventual transfer of the bank to a fit private investor, ABL's financial and governance issues were resolved and this part of the component was also considered successful. As for NBP , the only remaining NCB, the Government has already divested 23.2% of its shareholding in the bank through stock exchange, and it is in the process of amending the Banks Nationalization Act of 1974 to grant minority shareholders voting rights and continue further divestments. Furthermore, the Government has started the process of restructuring of ZTBL, SMEB, HBFC, IDBP, ICP and NIT- the largest open-end mutual fund – with the end game of privatization.

Effective Regulation and Supervisory Capacity at SBP

The SBP has introduced a new system of monitoring, surveillance and supervision called the Institutional Risk Assessment Framework (IRAF). IRAF is an institution specific risk rating designed to make banks and DFIs pay greater attention to their risk management regimes. Although the minimum capital adequacy ratio continues to be 8 percent, the existing uniform CAR requirement has been replaced with the variable CAR which will be based on the IRAF rating assigned to individual banks. Furthermore, the SBP has tightened further the loan loss provisioning requirements to bring them in line with international best practices. The OAEM category has been eliminated and the aging criteria have been revised whereby the loans overdue by 90 days will be classified substandard, 180 days doubtful, and one year or more as loss effective from November 2005. Furthermore, the required minimum paid-in capital has been raised to Rs 6 billion (about US$100 million) to be achieved in a phased manner over the next four years. The SBP has adopted and is implementing a new Strategic Plan for 2005-10 to ensure that the reforms will continue regardless of the change in the leadership of the institution. The strategic planning process was participative, consultative, and result-oriented. The overall direction, objectives, vision and mission of the SBP were provided by senior management and spelt out in the document "Pakistan's Financial Sector: A Roadmap for 2005-2010" and the Concept Paper for Strategic Plan 2005-10.

- 4 -

Promote Transparency and Disclosure

The SBP's image as a responsible central bank and regulator of the financial system has been made possible by the increased focus on transparency, openness, policy formulation through consultative process, and information dissemination. The number of economic and statistical publications has been increased and a medium-term (2005-10) Strategic Plan was unveiled to apprise market players about the SBP's plans for the financial sector during the next five years. Furthermore, the internal and external stakeholders' surveys were conducted for the second consecutive year to assess the approval rating of various change initiatives as well as stakeholders' satisfaction with SBP's performance in a number of areas. SBP has started publishing its annual Performance Review since FY03. The performance review takes stock of SBP initiatives achieve progress towards strategic objectives as well as build and enhance its institutional capacity to align it with the strategic direction. The Banking System Review, now a regular quarterly activity, is another initiative to keep stakeholders abreast of the developments in the banking system and provides them an assessment of the overall health, stability, and resilience of the banking system. The MPS (Monetary Policy Statement), issued biannually, is one of the most significant SBP initiatives to make the monetary formulation and implementation process more objective, predictable and transparent. SBP has taken a number of steps towards adopting international standards for data collection, compilation, and dissemination. With the implementation of the IMF's Balance of Payments Manual, Pakistan was accepted as a member of General Data Dissemination System. The SBP has taken a number of steps to ensure adequate disclosure by banks and DFIs about key activities, financial condition, and business performance, to protect the interest of customers of these institutions. At the end of each accounting year, all banks and DFIs are required to prepare their annual financial statements based on IAS formats. In addition, they have been asked to publish an abridged version of their half-yearly financial statements in the newspapers. The quarterly financial statements will also be circulated to the shareholders and an abridged version thereof will be published in the newspapers. Furthermore, effective from December 2005, all banks and DFIs are required to include a comprehensive paragraph under the heading "Risk Management Framework" and a Statement on Internal Controls in the Directors' Report in their annual audited accounts.

Prevent Use of Banking System for Money Laundering

Pakistan has taken several measures to prevent banking channels being used for money laundering. It is an active member of Asia Pacific Group on Anti-Money Laundering. It participates in its programs and meetings for implementation of Anti-Money Laundering (AML) regime in the country. SBP has held awareness and capacity building programs, workshops, and seminars to sensitize the banks' management and staff about the importance of AML initiatives. It has established AML unit and issued prudential regulations dealing with AML. The unit is entrusted with the responsibility of bringing rules and regulations in line with international best practices and developing an effective regulatory system that minimizes the possibility of money laundering.

The draft AML law has been approved by the Cabinet and is currently under consideration in the Ministry of Law, Justice and Human Rights. Pending the enactment of the AML law, SBP has taken steps to set up a Financial Intelligence Unit (FIU) and to intensify the contacts with the new Economic Crime Wing under the National Accountability Bureau (NAB). It is also in the process of laying down rules of engagement to prevent, detect, and prosecute banking crimes. To ensure consolidated supervision, SBP plans to intensify cooperation with other regulatory bodies (both foreign and local) in enhanced off-site monitoring and targeted on-site inspections of cross border branches.

- 5 -

4.3 Net Present Value/Economic rate of return:

Not applicable

4.4 Financial rate of return:

Not applicable

4.5 Institutional development impact:

The institutional impact has been substantial. Learning from the experience of resolving troubled NCBs, SBP plans to formulate more pro-active banking crisis resolution mechanism through implementation of the Prompt Corrective Action (PCA) regime and reinforce it with modification in the Banking Companies Ordinance of 1962. Drawing lessons from its experience with privatization of NCBs, SBP is in the process of developing appropriate strategies to facilitate the GOP in privatization and divestment of the public sector banks including IDBP, SME Bank and ZTBL, divestment of the remaining shares in the already privatized banks. The strategy is to proactively play its role as an advisor and facilitator of the privatization process by bringing improvements in the selection of strategic investors, due diligence, and successful completion of the transactions. Last but not the least, SBP is taking steps to further strengthen the financial sector through introduction of a Deposit Insurance Scheme, a phased increase in the regulatory capital requirement, and acting as catalyst in the development of an enabling legal framework for private sector credit bureaus.

5. Major Factors Affecting Implementation and Outcome

5.1 Factors outside the control of government or implementing agency:

The implementation of this project was aided by several outside factors that had a generally positive influence. The first was the interest shown by many reputed investors who bid for the strategic shares of HBL, UBL and ABL. Though there were initial setbacks with the sale of UBL, the extent of interest shown by investors in HBL and ABL was remarkable, contributing to the success of GOP's bank privatizations. The second was the positive and enterprising behavior of the buyers of these banks in subsequently turning them around. The third was speed with which the Bank came forward to support all the three phases of the reform program, thereby facilitating implementation. Finally, the fourth was the absence of resistance and opposition from the vested interests, such as the employee unions and defaulters of these banks towards privatization, and from the financial institutions for greater transparency and disclosure.

On the negative side, the increased liquidity in the system has led to a rapid expansion of credit to the consumer sector that could be problematic if corrective measures were not taken. Banks will need to strengthen their credit appraisal systems and risk management since much of the credit growth is in areas where banks are relatively inexperienced. There is also a need for close monitoring by the regulator to ensure that the rapid credit growth does not compromise credit quality and undermine the banks' balance sheets. SBP has already issued risk management guidelines, restricted financing for purchase of plots alone unless they are accompanied by construction of house to control speculation of land prices, and increased the provisioning of banks including a 5 percent general reserves for unsecured and 1 percent for secured consumer lending.

- 6 -

5.2 Factors generally subject to government control:

The major factor that affected implementation and outcome substantially was the government’s full and unstained support for the reform program. This coupled with the vision and commitment of successive Governors of the State Bank ensured that implementation was timely and effective to achieve the desired outcomes. The reforms supported under this project were a part of the broader “home-grown” banking reform program designed by the Ministry of Finance with the active participation of the State Bank of Pakistan (SBP) since the early 1997, and effectively implemented by the SBP. The “home-grown” banking reform program, as spelled out in their Letter of Development Policy, was implemented in three phases over the period 1997 to 2004, supported by three IDA Credits and a Bank Loan. The Government’s commitment to the broader “home-grown” reform program remained strong over the entire implementation period and substantially helped to achieve the project outcomes, especially the objective to improve sector governance through the privatization of UBL, HBL and ABL. The reform of corporate governance in the financial sector was the most critical for sustainability and irreversibility of the complete reform program could not have been achieved without the firm, full and continued support of the Government.

5.3 Factors generally subject to implementing agency control:

The two implementing agencies were the privatization Commission that sold the strategic shares of HBL and UBL and the SBP that sold ABL. Both the implementing agencies demonstrated strong commitment and were proactive in implementing the program and actions under its control. SBP has continued to develop its regulatory and supervisory capacity, enhanced transparency, introduced anti-money laundering measures, and has recently tightened prudential regulations related to capital adequacy and loan classification and provisioning.

5.4 Costs and financing:

Not applicable

6. Sustainability

6.1 Rationale for sustainability rating:

Overall project sustainability is rated highly likely. While the first and second phases of the overall reform program moved the achievements towards sustainability, the third phase under this project finally ensured sustainability. Thus, the reforms implemented under BSAL were able to stabilize the financial sector and the BSRPP improved the governance and management of the NCBs in preparation for their privatization. The BSDPC completed the first generation of banking reforms by successfully handing over HBL, UBL and ABL to qualified foreign and local investors, thereby ensuring the irreversibility of the reform program. The new investors have already turned around these banks, thereby ensuring that the operations of these banks will no longer impose any fiscal burden on the Government. In reality, the profitability of these banks will contribute to the revenues through higher and higher tax payments. The divestiture of state owned institutions substantially changed the structure of the banking sector and nearly 80% of sector assets are now controlled by the private banks. The overall banking sector has become considerably more competitive and responsive. The initial profitability of these privatized banks has further strengthened the government’s policy to leave a majority share of the banking sector in private hands. Thus given the nature and pace of the reforms, reversal is considered unlikely. In its letter of development policy the government has committed to working actively on the second generation of reforms. It aims to work towards deepening further the financial sector and integrate it into the global economy. Sustainability is

- 7 -

further strengthened by the ongoing process of tightening prudential regulations by SBP to ensure the soundness and stability of the banking sector.

6.2 Transition arrangement to regular operations:

The implementation of this project successfully concluded the first generation reforms that were commenced in the late 1980s. To assist SBP in implementing the second generation reforms, IDA extended a Banking Sector TA (TABS) project, amounting to US$ 26.5 million, to strengthen SBP’s IT capacity and further develop its human resources. The TABS project is expected to close at the end of 2007. In the meantime, SBP and the Government have initiated the design and development of the second generation reforms aimed at expanding access to financial services for all segments of the society and sectors of the economy. These reforms are in line with the recommendations of the joint Bank-Fund Financial Sector Assessment Program conducted in April 2004. The FSAP found the results of the reform efforts in the banking sector manifested in improving financial soundness indicators, greater resiliency to credit, market and liquidity risks, and good compliance with international supervisory standards.

7. Bank and Borrower Performance

Bank7.1 Lending:

Since this was the third in a series of operations designed to support the first generation of banking reforms, the Bank has established good and close dialogue with the Government. The Bank has also acquired an in-depth knowledge of the main issues involved in the reform process. Earlier operations had supported operational restructuring in order to facilitate privatization. The Bank had linked the subsequent recapitalization support to successful privatization. The IDA credit of US $100 million and IBRD of US $200 under the BSDP were released after the privatization of UBL and HBL was complete and the governance and financial problems of ABL had been resolved. Since all these prior actions were successfully carried out, the BSDP was approved in January 2005.

7.2 Supervision:

Due to the nature of the adjustment lending and quick disbursement there was no formal supervision done for BSDP. Since it was in constant touch with the stakeholders throughout the period of implementation of BSRPP, the Bank had a good dialogue with these stakeholders and maintained close oversight over major developments that might have any bearing on project implementation.

7.3 Overall Bank performance:

Borrower7.4 Preparation:

BSDP was a result of a reform program that was primarily led by the borrower. The Bank’s role had been restricted to that of a facilitator. All major decisions and actions were taken by the borrower who was very clear about the strategy regarding reforms in the financial sector. The borrower worked diligently to ensure that the prior actions were met in a timely fashion with no compromise on quality. The borrower led by SBP was convinced that with the successful completion of this program, the phase III of the first generation of financial sector reforms had been brought to a satisfactory conclusion. The government has concurrently started working on the second generation of financial sector reforms to consolidate the gains

- 8 -

realized thus far and to build on the strengths of the financial system for expanding access to financial services. The strategy is aligned with the recommendations of the FSAP and is also discussed in the Government’s LDP.

7.5 Government implementation performance:

The transformation of a largely state-owned and weak banking system into a healthy and privately-owned system could not have been brought about but for the active support and strong commitment of the government to banking reforms. The government has played a proactive role in the process of restructuring the NCBs, on-going consolidation, strengthening of regulatory capacity, and improvements in transparency, corporate governance, and credit culture. As a result, quasi-fiscal responsibility of financial institutions have been reduced sharply. The reform efforts are reflected in improving financial soundness indicators, greater resiliency to credit, market and liquidity risks, and good compliance with international supervisory standards.

7.6 Implementing Agency:

The credit for the success of bank reforms owes in no small measure to the role of SBP in effecting needed reforms throughout the three phases of banking reforms supported by the Bank. Key measures included changes in laws and governance, strengthening the regulatory framework and institutions, rationalization of interest rates through reforms in the National Savings Scheme (NSS), improving the environment for enforcement of financial contracts, bringing greater transparency and disclosure of information, and operational restructuring of public sector banks. To promote scale economies and efficiency and achieve better oversight, SBP also sought to consolidate the banking sector by increasing the minimum capital requirement from Rs. 500 million (US$ 8.3 million) to Rs. 750 million (US$ 12.5 million) as of end-December 2001 and further to Rs. 2 billion (US$ 33.3 million) as of end-December 2005. Most recently, SBP has issued a Circular raising the minimum capital requirements in phases from Rs. 2 billion to Rs. 6 billion (US$100 million) at the end of 2009. It has also shifted from uniform Capital Adequacy Requirement (CAR) to a variable CAR which is linked to the rating of the financial institution under the Institutional Risk Assessment Framework (IRAF).

7.7 Overall Borrower performance:

The government's overall performance is rated as highly satisfactory.

8. Lessons Learned

A number of useful lessons can be learned from Pakistan's experience with banking sector reforms including the following:

1. To ensure that the banking sector privatization runs smoothly, it is very important to have government ownership of the initiative. Setting conditions alone will not serve the purpose as the government can comply with the letter rather than the spirit of the agreement.2. To ensure smooth transition from a nationalized to privatized bank, it is a good practice for public sector banks to undergo cost and operational restructuring before privatization. 3. The cultural change in the organization must be inculcated prior to privatization. The seeds for the new corporate culture should be sown prior to handing over the bank to the new owners.4. It is important that a public sector bank is recapitalized before privatization or at the point of sale

- 9 -

so that it will be able to meet the central bank's minimum capital requirements. Under no circumstances should the supervisory authorities allow regulatory forbearance for the newly privatized bank.5. Government-related business should not convey to the privatized bank as it is important that the bank begins its operations on a level playing field. 6. The government can expect higher bids for the bank sale if the payment for the bank's shares is injected right back into the bank rather than given to the government as consideration for its existing shares in the bank. The privatization of ABL was structured in such a way that the entire proceeds from the bank sale went into the recapitalization and restructuring of the bank’s balance sheet. The shares were sold at a premium of Rs. 33.7 over par value or 337 percent.7. Enhanced regulatory and supervisory capacity in the SBP serves to improve the efficiency of banks and enhances competition among them. Foreign banks and NBP (which is still majority government-owned) should be subject to the same regulations as domestic private banks, creating a level playing field in the banking sector. 8. The benefits to the government in the form of higher value of the shares in a privatized bank and the broader range of financial products at competitive prices - arising from a more healthy and competitive banking sector - usually offset part of the restructuring costs. The banking reforms that were initiated in 1997 had cost the Government about US$2 billion against the proceeds of US$ 590 million from the sale of UBL, HBL and NBP’s 23 percent shares.9. Reforms in the rest of the financial sector should keep pace with those in the banking sector. While the banking sector has gone through beneficial structural transformation, the rest of the financial sector has not been subjected to the reform process to the same extent. Insurance penetration is very low relative to other countries at Pakistan's income level. There is a need for further consolidation and liberalization of the industry. A number of issues in pensions require the authorities' attention including the financial sustainability and regulatory oversight of the present schemes. The SECP, which regulates the capital market, does not appears to have adequate resources and capacity to fulfill its mandate.10. Irrespective of costs, restructuring is necessary to restore the safety and soundness of the financial system since inaction to avoid fiscal costs could result in "meltdown' and huge fiscal costs later.

9. Partner Comments

(a) Borrower/implementing agency:

SBP advised the Bank that it had adopted the Strategic Plan 2005-10 which would be operationalised through successive annual business plan. The strategic objectives of the plan are to: (i) further strengthen the financial system soundness through consolidation of the banking system by means of merger and acquisitions, introduction of deposit insurance scheme as a safety net, privatization of IDBP, ZTBL, and SME Bank, implementation of Basel II Accord, export of financial services to the Middle East, Central Asia and Africa, further strengthening the supervisory regime, consolidated supervision of banks/DFIS, formulation of a proactive troubled bank resolution mechanism, and achieving full compliance with AML regime; (ii) deepen financial sector and broaden access to finance through broadening access of formal credit to middle and low income groups, promotion and strengthening of Islamic banking, and development of financial derivatives market; (iii) ensure independent and effective monetary policy management through enhanced coverage of monetary aggregates, providing regulatory support for supra-national local currency bonds, and improved quality and dissemination of research, listing of government securities on the stock exchange, introduction of liquidity adjustment facility, and development of Islamic money market; and (iv) achieve efficient and sound payment system through promotion and facilitation of e-banking/commerce within the country, establishment of an electronic clearing house, facilitation in the development of public key infrastructure and digital certificate infrastructure, and development of securities settlement system for secondary market.

- 10 -

(b) Cofinanciers:

None

(c) Other partners (NGOs/private sector):

In addition to government officials, the ICR Mission met with stakeholders in the private sector including senior bankers in private and foreign banks. There was a general consensus that the privatization of the banking sector in Pakistan had been a success. Most stakeholders seemed happy with the way the privatization had panned out and the performance of the banks since. It was generally agreed that SBP had served as an effective supervisory institution. As the financial practices in Pakistan became more complex, there was a consensus that human capital to meet these new higher level needs was not available. The privatization of public sector banks has enhanced the need for effective top management, and as such, created a great deal of competition amongst employers. There is need to enhance the skill set in Pakistan, especially in risk management, particularly in assessing the risk of consumers. There was also a universal recognition of the need to develop the capital market. It was felt that the debt market was currently not very deep and effective. Practitioners expressed the need to develop this market further, especially the corporate bond and commercial paper markets. The views were expressed about the weaknesses of the existing rating companies country and about the need for good equity market analysts. There was also a fear that the sector might not have the sophistication and expertise to conform to Basel II requirements. Furthermore, it was felt that there was limited rationale for having a state-owned commercial bank and that one should work towards removing any unfair advantage in terms of any tied-in business from the government. It was also felt that Pakistan was now in great need of an effective Export Credit Agency.

10. Additional Information

None

- 11 -

Annex 1. Key Performance Indicators/Log Frame Matrix

Prior Action Matrix

Objectives Prior Action Outcome Indicator Status1. Improving sector governance through privatization.

2. Develop effective regulatory and supervisory capacity at SBP.

(a) Privatization and hand over of UBL.

(b) Privatization and hand over of HBL.

(c) Merger/sale and handing over of ABL to a qualified private sector group.

(d) Qualified bankers appointed to board and management of NBP.

(e) Issuance of detailed guidelines under “Fit and Proper Tests (FPT)” for the appointment of Board of Directors, Chief Executive Officers and Senior Management of the banks.

Introduction of a new system of monitoring, surveillance and supervision, Institutional Risk Assessment Framework(IRAF).

Introduction of separate sets of regulations for corporate, SME, consumer finance, and micro-finance

UBL is privately owned and managed and is adequately capitalized compliant with SBP regulations; HBL is privately owned and managed and is adequately capitalized compliant with SBP regulations.

ABL governance issues are resolved with the bank re-privatized and is adequately capitalized.

Autonomy and professionalism assured.

Corporate governance enhanced through hiring of bank managers with professionalism and integrity.

A cohesive andproactive monitoring through preparation of risk profiles of individual institutions and taking prompt corrective action as and when needed. Financial Soundness indicators for the system show an upward trend.

More systematic and risk-focused supervision and regulation of financial institutions. General reserves of 25% introduced for unsecured and 5% for secured consumer lending.

UBL is successfully privatized.

HBL is successfully privatized.

ABL transferred to private sector.

NBP is professionally managed.

Banks have followed these FPT guidelines for appointment of key executives since April 2003.

The IRAF has been put in place since early 2004.

Separate guidelines have been introduced in 2003.

- 12 -

3. Promote transparency and disclosure.

4. Prevent the possible use of the banking system for money laundering, financing for terrorism, and transfer of illegal/ill-gotten money.

Issuance of guidelines on risk management for banks/DFIs.

Issuance of master circular containing consolidated instructions on financial disclosure.

Issuance of guidelines for opening/dealing with the accounts of customers.

A more effective system of risk identification, assessment, measurement, monitoring, and mitigating/controlling all risks inherent in the business of banking has helped ensure that banks are adequately capitalized to assume these risks.

Improved transparency and full compliance with prudential regulations as Banks/DFIs have increased public disclosure.

Money laundering, financing for terrorism, and transfer of ill-gotten wealth through banks will become increasingly difficult.

Banks have started implementing an effective risk management strategy based on these guidelines since August 2003.

The consolidated instructions on financial disclosure have been put in place since January 2004.

Banks have implemented a know-customer policy based on these guidelines since March 2003.

- 13 -

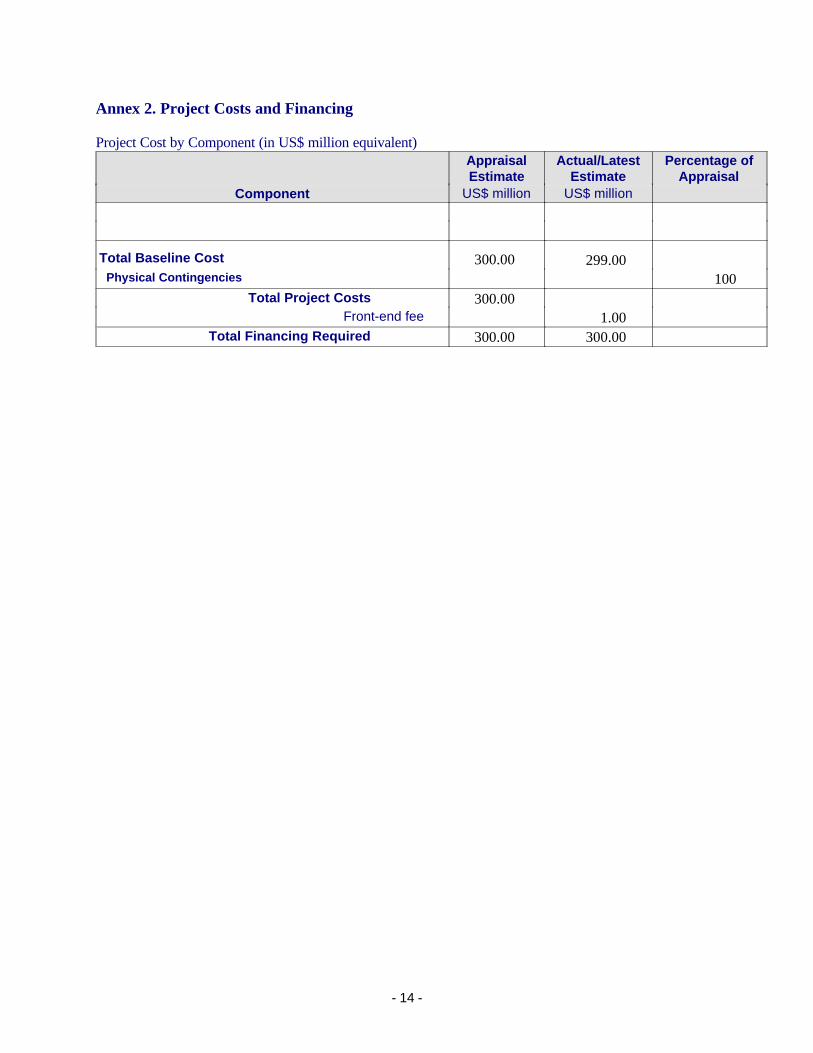

Annex 2. Project Costs and Financing

Project Cost by Component (in US$ million equivalent)AppraisalEstimate

Actual/Latest Estimate

Percentage of Appraisal

Component US$ million US$ million

Total Baseline Cost 300.00 299.00 Physical Contingencies 100

Total Project Costs 300.00Front-end fee 1.00

Total Financing Required 300.00 300.00

- 14 -

Annex 3. Economic Costs and Benefits

Not applicable

- 15 -

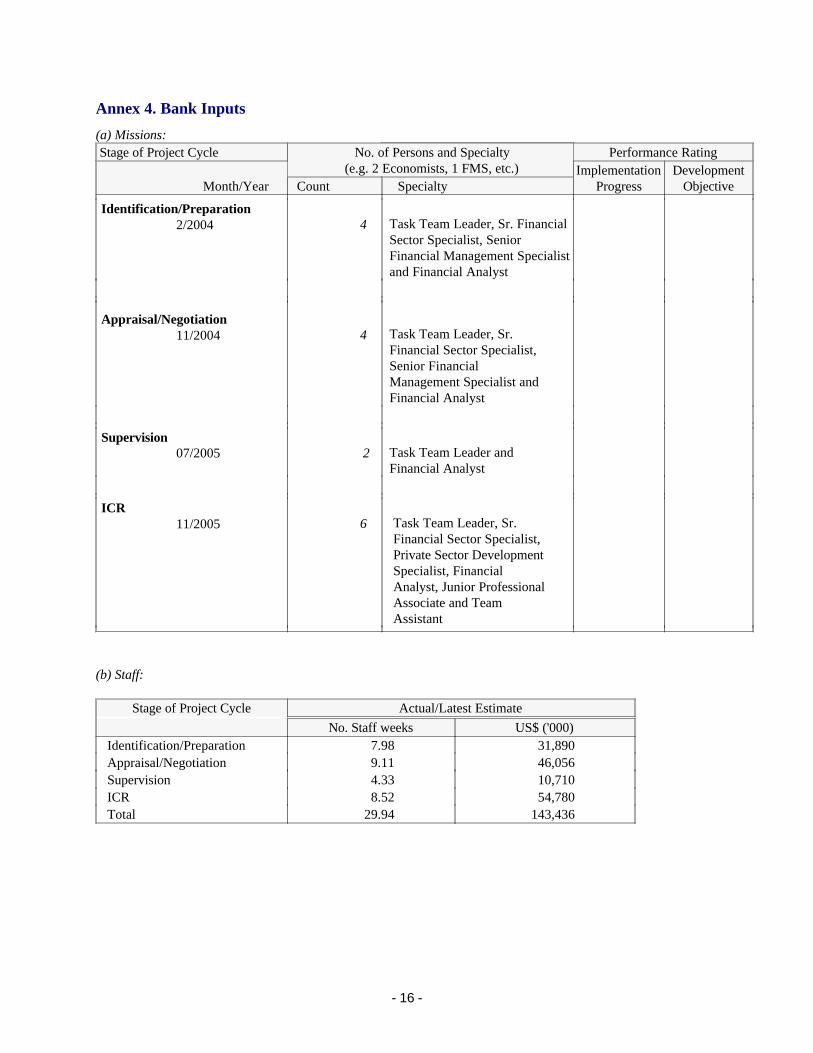

Annex 4. Bank Inputs

(a) Missions:Stage of Project Cycle Performance Rating No. of Persons and Specialty

(e.g. 2 Economists, 1 FMS, etc.)Month/Year Count Specialty

ImplementationProgress

DevelopmentObjective

Identification/Preparation2/2004 4 Task Team Leader, Sr. Financial

Sector Specialist, Senior Financial Management Specialist and Financial Analyst

Appraisal/Negotiation11/2004 4 Task Team Leader, Sr.

Financial Sector Specialist, Senior Financial Management Specialist and Financial Analyst

Supervision07/2005 2 Task Team Leader and

Financial Analyst

ICR11/2005 6 Task Team Leader, Sr.

Financial Sector Specialist, Private Sector Development Specialist, Financial Analyst, Junior Professional Associate and Team Assistant

(b) Staff:

Stage of Project Cycle Actual/Latest EstimateNo. Staff weeks US$ ('000)

Identification/Preparation 7.98 31,890Appraisal/Negotiation 9.11 46,056Supervision 4.33 10,710ICR 8.52 54,780Total 29.94 143,436

- 16 -

Annex 5. Ratings for Achievement of Objectives/Outputs of Components(H=High, SU=Substantial, M=Modest, N=Negligible, NA=Not Applicable)

RatingMacro policies H SU M N NASector Policies H SU M N NAPhysical H SU M N NAFinancial H SU M N NAInstitutional Development H SU M N NAEnvironmental H SU M N NA

SocialPoverty Reduction H SU M N NAGender H SU M N NAOther (Please specify) H SU M N NA

Private sector development H SU M N NAPublic sector management H SU M N NAOther (Please specify) H SU M N NA

Financial stability

- 17 -

Annex 6. Ratings of Bank and Borrower Performance

(HS=Highly Satisfactory, S=Satisfactory, U=Unsatisfactory, HU=Highly Unsatisfactory)

6.1 Bank performance Rating

Lending HS S U HUSupervision HS S U HUOverall HS S U HU

6.2 Borrower performance Rating

Preparation HS S U HUGovernment implementation performance HS S U HUImplementation agency performance HS S U HUOverall HS S U HU

- 18 -

Annex 7. List of Supporting Documents

1. Aide-Memoire of the Implementation Completion Report Mission on BSDP2. Management letter of the ICR Mission for BSDP3. A Project Completion Report prepared by the State Bank of Pakistan4. Project Appraisal Document for the Banking Sector Restructuring and Privatization Project dated October 1, 20015. Program Document for the Banking Sector Development Program dated December 13, 20046. Country Assistance Progress Report for the Islamic Republic of Pakistan dated Marach 26, 2004

- 19 -

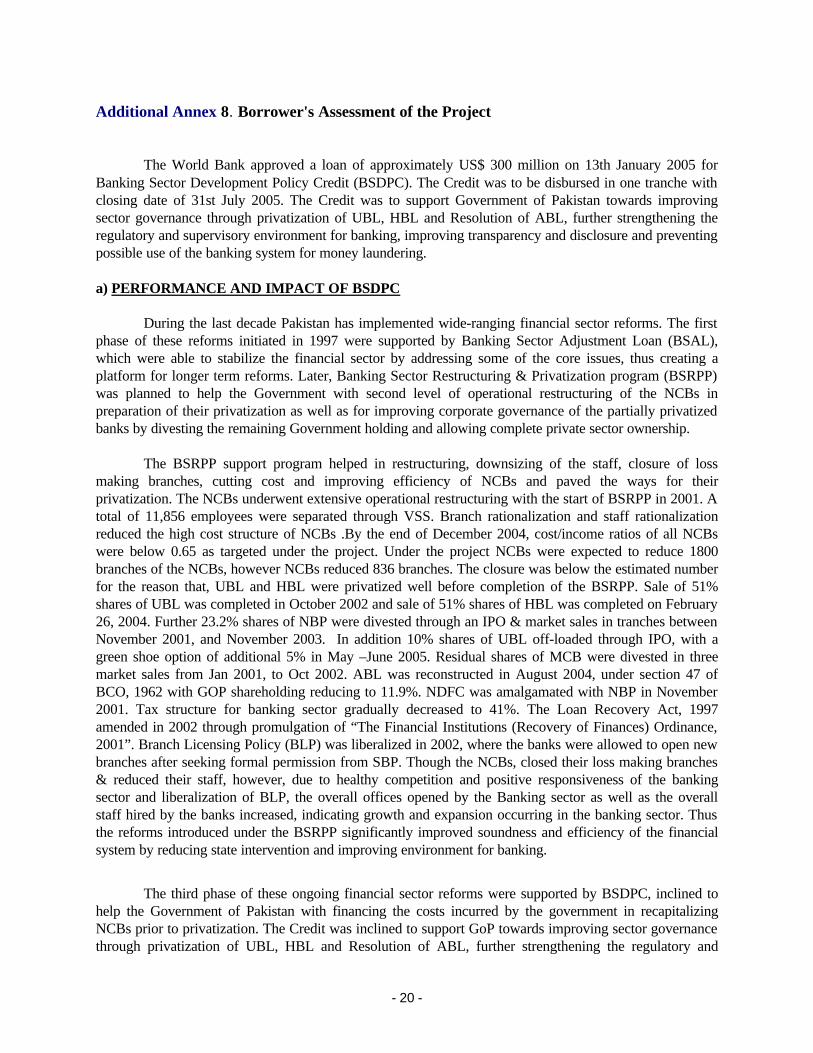

Additional Annex 8. Borrower's Assessment of the Project

The World Bank approved a loan of approximately US$ 300 million on 13th January 2005 for Banking Sector Development Policy Credit (BSDPC). The Credit was to be disbursed in one tranche with closing date of 31st July 2005. The Credit was to support Government of Pakistan towards improving sector governance through privatization of UBL, HBL and Resolution of ABL, further strengthening the regulatory and supervisory environment for banking, improving transparency and disclosure and preventing possible use of the banking system for money laundering.

a) PERFORMANCE AND IMPACT OF BSDPC

During the last decade Pakistan has implemented wide-ranging financial sector reforms. The first phase of these reforms initiated in 1997 were supported by Banking Sector Adjustment Loan (BSAL), which were able to stabilize the financial sector by addressing some of the core issues, thus creating a platform for longer term reforms. Later, Banking Sector Restructuring & Privatization program (BSRPP) was planned to help the Government with second level of operational restructuring of the NCBs in preparation of their privatization as well as for improving corporate governance of the partially privatized banks by divesting the remaining Government holding and allowing complete private sector ownership.

The BSRPP support program helped in restructuring, downsizing of the staff, closure of loss making branches, cutting cost and improving efficiency of NCBs and paved the ways for their privatization. The NCBs underwent extensive operational restructuring with the start of BSRPP in 2001. A total of 11,856 employees were separated through VSS. Branch rationalization and staff rationalization reduced the high cost structure of NCBs .By the end of December 2004, cost/income ratios of all NCBs were below 0.65 as targeted under the project. Under the project NCBs were expected to reduce 1800 branches of the NCBs, however NCBs reduced 836 branches. The closure was below the estimated number for the reason that, UBL and HBL were privatized well before completion of the BSRPP. Sale of 51% shares of UBL was completed in October 2002 and sale of 51% shares of HBL was completed on February 26, 2004. Further 23.2% shares of NBP were divested through an IPO & market sales in tranches between November 2001, and November 2003. In addition 10% shares of UBL off-loaded through IPO, with a green shoe option of additional 5% in May –June 2005. Residual shares of MCB were divested in three market sales from Jan 2001, to Oct 2002. ABL was reconstructed in August 2004, under section 47 of BCO, 1962 with GOP shareholding reducing to 11.9%. NDFC was amalgamated with NBP in November 2001. Tax structure for banking sector gradually decreased to 41%. The Loan Recovery Act, 1997 amended in 2002 through promulgation of “The Financial Institutions (Recovery of Finances) Ordinance, 2001”. Branch Licensing Policy (BLP) was liberalized in 2002, where the banks were allowed to open new branches after seeking formal permission from SBP. Though the NCBs, closed their loss making branches & reduced their staff, however, due to healthy competition and positive responsiveness of the banking sector and liberalization of BLP, the overall offices opened by the Banking sector as well as the overall staff hired by the banks increased, indicating growth and expansion occurring in the banking sector. Thus the reforms introduced under the BSRPP significantly improved soundness and efficiency of the financial system by reducing state intervention and improving environment for banking.

The third phase of these ongoing financial sector reforms were supported by BSDPC, inclined to help the Government of Pakistan with financing the costs incurred by the government in recapitalizing NCBs prior to privatization. The Credit was inclined to support GoP towards improving sector governance through privatization of UBL, HBL and Resolution of ABL, further strengthening the regulatory and

- 20 -

supervisory environment for banking, improving transparency and disclosure and preventing possible use of the banking system for money laundering.

The SBP took a number of steps to promote transparency and disclosure through a master circular containing consolidated instructions on financial disclosure. Several measures were taken by SBP to prevent banking channels for the purpose of money laundering. The measures included the establishment of AML unit, and issuance of prudential regulations, the unit is entrusted with the responsibility of bringing rules and regulations in line with international best practices and developing an effective regulatory system that minimizes the possibility of money laundering. Introduction of a new system of monitoring, surveillance and supervision, Institutional Assessment Framework (IRAF), aimed to bring more systematic and risk-focused supervision. ABL governance issues resolved with the bank being adequately re-capitalized and management transferred to private sector.

The successful implementation of BSAL, BSRPP & BSDPC program improved the overall performance of the banking system. The divestiture of state owned institutions substantially changed the structure of the banking sector and nearly 80% of sector assets are now controlled by the private banks. The overall banking sector has become considerably more competitive and responsive. Thus continuous restructuring has reduced the burden on the government and has left it with few minor areas to concentrate.

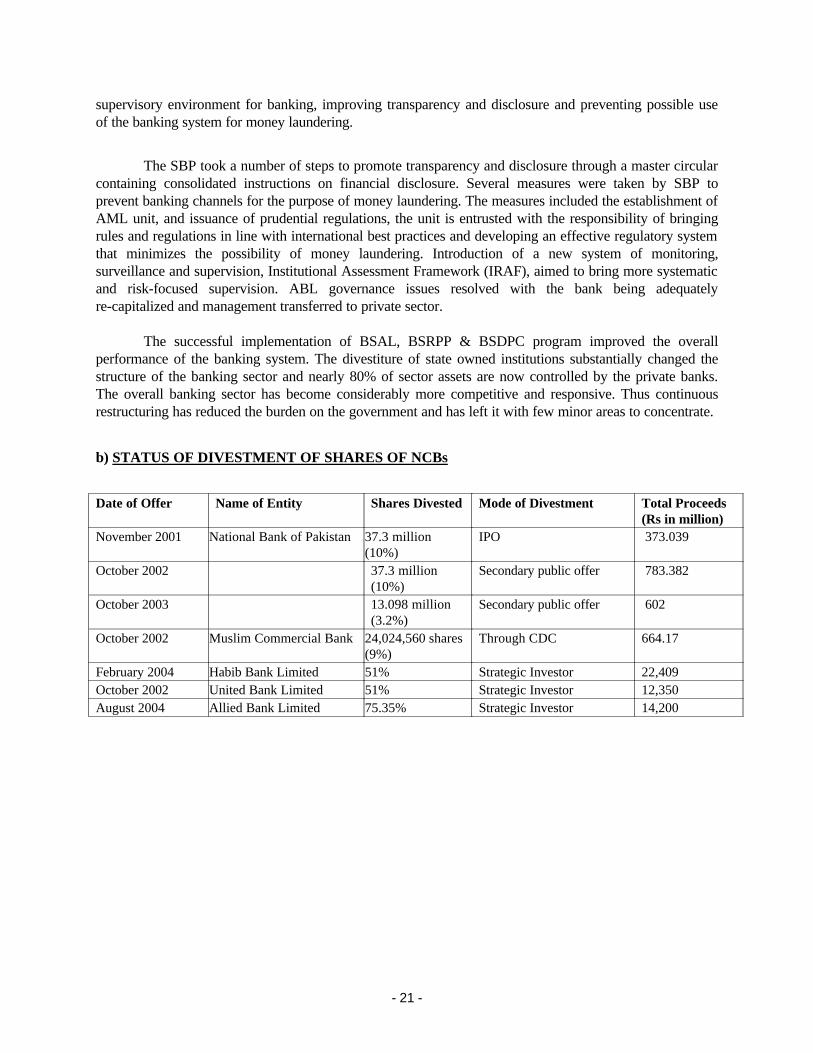

b) STATUS OF DIVESTMENT OF SHARES OF NCBs

Date of Offer Name of Entity Shares Divested Mode of Divestment Total Proceeds (Rs in million)

November 2001 National Bank of Pakistan 37.3 million (10%)

IPO 373.039

October 2002 37.3 million (10%)

Secondary public offer 783.382

October 2003 13.098 million (3.2%)

Secondary public offer 602

October 2002 Muslim Commercial Bank 24,024,560 shares (9%)

Through CDC 664.17

February 2004 Habib Bank Limited 51% Strategic Investor 22,409October 2002 United Bank Limited 51% Strategic Investor 12,350August 2004 Allied Bank Limited 75.35% Strategic Investor 14,200

- 21 -

c) Key Performance Indicators of BSDPC and their outcomes

Key Performance Indicators Outcomea) Improving transparency & Disclosure The SBP has taken a number of steps to promote transparency and

disclosure through a master circular containing consolidated instructions on financial disclosure. At the end of each accounting year, all banks are required to prepare their annual financial statements in the prescribed manner, as on the last working day of that year. These financial statements together with the auditor’s report, as passed in the Annual General Meeting, shall be published and circulated as well as furnished, as returns, to the SBP as prescribed in the BCO, 1962. Further, all DFIs are also required to prepare their annual financial statements at the end of each accounting year as on the last working day of that year. These financial statements together with the auditor’s report, as passed in the Annual General Meeting, shall be circulated to the shareholders and furnished as returns to the SBP within three months of the close of the period to which they relate. Furthermore, an abridged version of the financial statements shall also be published in the newspaper(s) within the stipulated time. For 1st and 3rd quarter, quarterly un-audited financial statements, along with directors’ review, shall be prepared by all banks / DFIs, including the branches of foreign banks, within 45 days of the close of the quarter to which they relate. These quarterly financial statements shall be circulated by domestic banks / DFIs to their shareholders. Furthermore, an abridged version of the quarterly financial statements shall be published in the newspaper(s) by all banks / DFIs, including branches of foreign banks, within the aforesaid time. Half yearly (2nd quarter) financial statements, with limited scope review by the statutory auditors, shall be prepared by all banks / DFIs, including the branches of foreign banks, within two months of the close of the half-year (2nd quarter). These half-yearly statements shall be circulated to the shareholders by domestic banks / DFIs. Furthermore, an abridged version of the half-yearly financial statements shall be published in the newspaper(s) by all banks / DFIs, including branches of foreign banks, within the aforesaid time. All banks and DFIs, including the branches of foreign banks operating in Pakistan, shall prepare their quarterly financial statements within 30 days of the end of the quarter to which they relate. The quarterly financial statements shall also be circulated to the shareholders and an abridged version thereof published in the newspaper(s) within the aforesaid time.

b) Preventing possible use of banking system for money laundering

The SBP has taken several measures to prevent banking channels for the purpose of money laundering. The measures include the establishment of AML unit, and issuance of prudential regulations, the unit is entrusted with the responsibility of bringing rules and regulations in line with international best practices and developing an effective regulatory system that minimizes the possibility of money laundering.

c) Developing effective regulatory capacity at SBP

The SBP has introduced a new system of monitoring, surveillance and supervision, Institutional Assessment Framework (IRAF). The aim is to bring more systematic and risk-focused supervision.

d) Completing the process of restructuring and privatization of the

The Government has already disinvested 23.2% of its shareholding in NBP, the only remaining NCB, through stock exchange and it is in the

- 22 -

remaining state owned financial institutions.

process of amending the Nationalization Act 1974 to allow minority shareholders and to continue further disinvestments. The Government has started operational restructuring of ZTBL, SMEB and HBFC. IDBP, ICP and NIT- the largest open-end mutual fund, are being restructured for privatization.

e) Improving the legal framework and judicial process for enforcement of financial contracts

The Loan Recovery Act 1997 amended in 2002 through promulgation of “The Financial Institutions (Recovery of Finances) Ordinance, 2001. The Government has already initiated the work for review and consolidation of the banking laws through the Banking Law Review Commission. The Commission is basically working on banking laws for implementation of Real Time Gross Settlement System, SBP Act and sharing Credit Information to facilitate private sector.

f) Improving financial markets infrastructure and excess to financial services

The Government and the SBP have taken concrete steps to improve the legal and regulatory framework for improving access to finance for the micro, SMEs and consumers and new Prudential Regulations for these sectors have been introduced. In addition, the Government has initiated operational restructuring of ZTBL, HBFC and SMEB. Apart from this a lot of work is being done on record keeping transparency in operations, promoting expansion of private sector credit information services, equipping financial institutions with necessary tools for a risk based environment, innovation/product development for borrowers and focus on technology.

- 23 -

- 24 -