the value of trademarks brand strategy and impact on financial reporting - brand valuation in a...

TRANSCRIPT

The Value of Trademarks

Brand Strategy and Impact on Financial Reporting - Brand Valuation in a Regulated Environment

Andreas MackenstedtCopenhagen, 7 June 2007

*

*connectedthinking

Agenda

1 IFRS financial reporting requirements

2 Brand valuation methodologies for financial reporting

3 Financial statements impact

Slide 3 PricewaterhouseCoopers

7 June 2007

Mergers & Acquisitions (M&A):impact on purchase price considerations, individual disposal of patents, brands etc.

Tax Purposes:change of ownership, licensing in/out, transfer pricing

Value Based Management:intellectual asset management, management reporting, investor communication

Valuation of Intangible Assets impacting Financial Reporting

Financing and Securitization:rating (Basel II), start-up financing, sale & lease back, collateralisation

Financial Accounting:acquisition accounting: purchase price allocation, impairment testing

PricewaterhouseCoopers

7 June 2007

Relevant standards for international financial accounting

GoodwillSFAS 142

Goodwill and other intangible assets

IAS 36Impairment of assets

Intangible assets

IAS 38Intangible assets

IFRS 5Assets held for sale

IAS 36

SFAS 142 Indefinite lives

SFAS 144Definite lives

Tangible assets

IAS 16Property, plant &

equipmentIFRS 5IAS 36

SFAS 144Impairment or disposal

of long-lived assets

Business combinations

SFAS 141Business

combinations

IFRS 3Business

combinations

US GAAP IFRS

Post- acquisitionaccounting

Acquisition accounting

Joint exposure

draft issued by

FASB and IASB

Fair value measurements Paper SFAS 157 Discussion Paper

In principle: no capitalisation of self-generated / self-developed intangibles

PricewaterhouseCoopers

7 June 2007

Fair Value

Valuation Concepts and MethodsDefinition of Fair Value

Liquidation Value (net realisable value) including Forced Sale

Value In Use (Going Concern)

Book Value

= Investment Value

Source: IFRS 3 Appendix A

Purchase Price

Willing buyer & willing seller Hypothetical buyer concept Stand-alone valuation

“Fair Value is the amount for which an asset could be exchanged, or a liability settled between knowledgeable, willing parties in an arm’s length transaction.“

PricewaterhouseCoopers

7 June 2007

Market Approach Cost ApproachIncome Approach

Excess Earnings Method

Relief from Royalty Method

Incremental Cash Flow Method

Most recent comparable transactions / Multiples

Current price on active market

Replacement Cost Method

Reproduction Cost Method

Intangible Asset Valuation Valuation techniques for Financial Reporting - Overview

Valuation Techniques

PricewaterhouseCoopers

7 June 2007

“Prices from previous transactions provide empirical evidence for the value of an intangible asset”

Market approachPremise of value

PricewaterhouseCoopers

7 June 2007

Represents one specific transaction only!

Adjustments to derivefair value necessary!

Price Fair value

• Changes in market conditions and legislation

• Marketplace conditions

• Participant-specific influences & motivations

• Deal-specific issues, e.g. financing terms, tax issues

Market approach

Active market for brands: not existing

Comparable transactions / multiples

Key value drivers:

• Future economic benefits

• Asset-specific risk

• Remaining useful life

PricewaterhouseCoopers

7 June 2007

“An intangible asset is worth what it can earn!”

Income approach Premise of value

PricewaterhouseCoopers

7 June 2007

Income Approach - Valuation principles

1. Isolate the future cash flows an investor would expect the subject intangible asset to generate

2. Discount future cash flows with an appropriate discount rate

FV =Cash Flow t

(1 + Discount Rate)t∑ t=1

T

PricewaterhouseCoopers

7 June 2007

2007 2008 2009 2010 2011 .... Terminal Value

Asset-specific cash flows:

Step 2Determination

of asset specific discount rate

Step 1:Expected future

Cash Flows

Asset-specific Weighted Average Cost of Capital (WACC)

PresentValue

Step 3:If applicable: calculation of

terminal value*

Step4:Present value

calculation

Income Approach - Valuation principles

* for indefinite lived intangibles only

PricewaterhouseCoopers

7 June 2007

Relief-from-royalty methodConcept

relieves owner

The royalty savings are the expected cash flows for the subject intangible asset!

from paying royalty rateOwnership of the asset

e.g. trademark

PricewaterhouseCoopers

7 June 2007

Relief-from-royalty method Valuation steps

Determine royalty rate for comparable asset1.

Subtract tax expenses3.

Multiply with matching valuation base2.

Calculate present value of royalty savings4.

Compute the tax amortisation benefit (TAB*)5.

* Tax amortisation benefit due to tax deductible amortisation of respective intangible as element to finally calculate fair value

PricewaterhouseCoopers

7 June 2007

Relief-from-royalty methodExample

Brand valuation fromFair value 2007

Brand-specific sales 2000Royalty Rate @ 4%Pre-tax royalty savings 80.0Corporate Taxes @ 40% 32.0After-tax royalty savings 48.0Discount rate @ 10%Growth rate @ 2%Residual multiple 11.918Discount factorPresent value after-tax royalty savings 572Tax amortisation benefit 114Fair value 686

Step-up factor TAB 1.2

Valuation date: 1 January 2007Valuation of brand

PricewaterhouseCoopers

7 June 2007

Incremental cash-flow methodConcepts

Cost savings

The intangible asset allows the owner to lower costs

Incremental Cash-Flow Method

Incremental revenue

The intangible asset allows the owner

to earn incremental cash flows, e.g. to charge a

price-premium

PricewaterhouseCoopers

7 June 2007

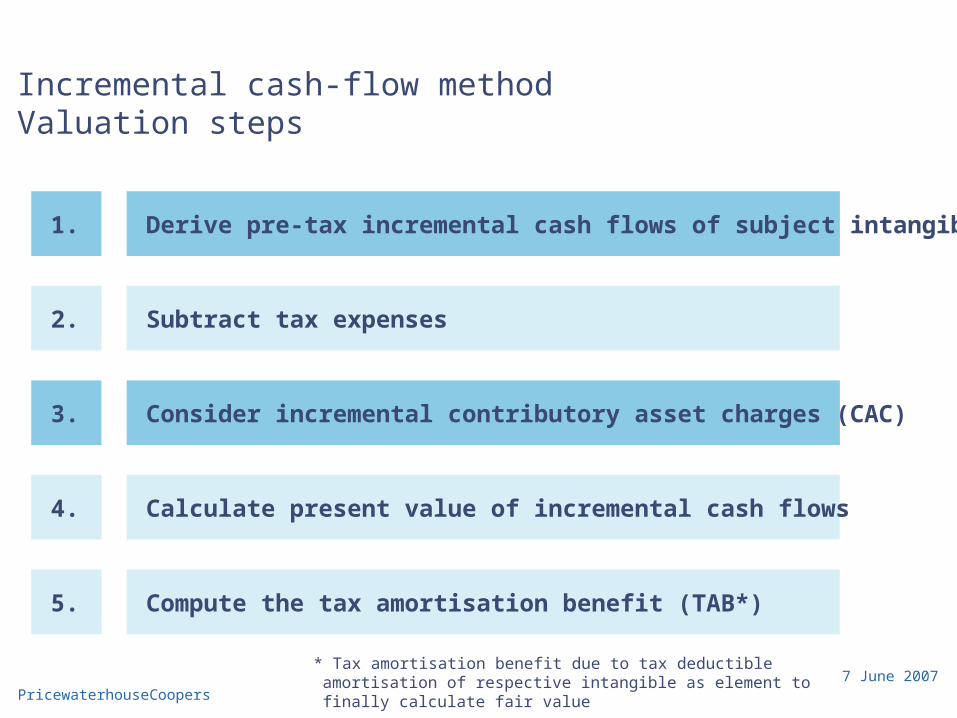

Incremental cash-flow methodValuation steps

Derive pre-tax incremental cash flows of subject intangible1.

Consider incremental contributory asset charges (CAC)3.

Subtract tax expenses2.

Calculate present value of incremental cash flows4.

Compute the tax amortisation benefit (TAB*)5.

* Tax amortisation benefit due to tax deductible amortisation of respective intangible as element to finally calculate fair value

PricewaterhouseCoopers

7 June 2007

Brand Premium

Brand Forecast

BrandRisk

Branded sales

Price effectVolume effect

Consideration of brand specific risks and present value calculation

Volume

Price

Branded Product

Unbranded Product

Price per bottle€ 1,30

Price per bottle€ 1,00

t

R (x)Total revenues

Brand specific revenues

Brand specific contribution to incomeBrand specific costs

C (x)

CP (x)

Incremental Cash Flow MethodPrice Premium Method

PricewaterhouseCoopers

7 June 2007

Incremental Cash Flow Method Example

fromFair value 2007

mill. EUR

Price effect 0.15 x 300,000 45.000

Quantity effect 1.65 x 50,000 82.500EBITDA-margin (after CAC) @ 55% 45.375

Pre-tax incremental cash flows 90.375Corporate taxes @ 35% 31.631After-tax incremental cash flows 58.744Discount Rate @ 10% 0,9Present value after-tax incremental cash flows 53.403Tax amortisation benefit 16.021Fair value 69.424

Step-up Factor TAB 1,3

Company xyzValuation of brand

Valuation Date: January 1, 2007Incremental cash flows

PricewaterhouseCoopers

7 June 2007

“An investor will pay no more for an asset than the cost to purchase or construct an asset of equal utility!“

Cost approachPremise of value

PricewaterhouseCoopers

7 June 2007

Cost approach methods

Replacement cost methodReproduction cost method

Using same materials, production standards, design ...

Using modern materials, production standards, design ...

“cost to construct an exact duplicate”

“cost to construct equivalent utility”

Cost Approach

PricewaterhouseCoopers

7 June 2007

Valuation Concepts and MethodsRemaining Useful Lifetime and Nature of Analysis (IAS 38.90)

• Expected usage of the asset

• Typical product life cycle for the asset

• Technical, technological, commercial or other types of obsolescence

• Changes in the market demand for the outputs from the asset

• Expected actions by competitors

• Level of maintenance expenditure required to obtain expected future economic benefits from the asset

• Legal factors (limitations)

• Period of control over the asset

• Dependence on the useful lifetime of other assets

. . . if no foreseeable limit: apply indefinite useful life

PricewaterhouseCoopers

7 June 2007

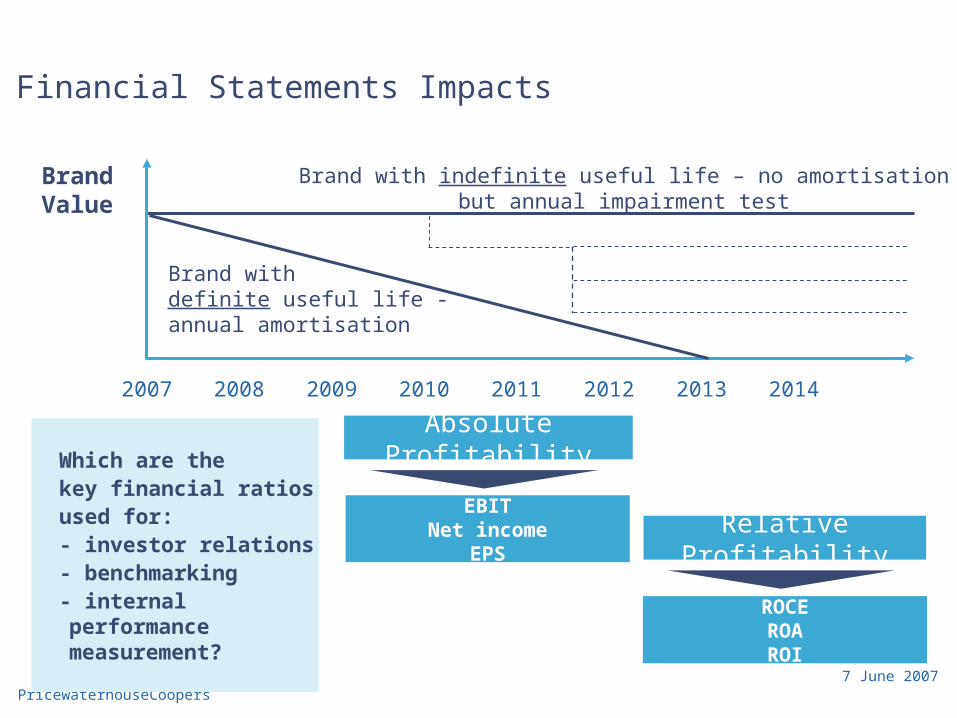

Brand with indefinite useful life – no amortisationbut annual impairment test

Brand Value

Financial Statements Impacts

2007 2008 2009 2010 2011 2012 2013 2014

Brand with definite useful life -annual amortisation

EBITNet income

EPS

ROCEROAROI

Absolute Profitability

Relative Profitability

Which are the key financial ratios used for:- investor relations- benchmarking- internal performance measurement?

PricewaterhouseCoopers

7 June 2007

PwC’s deal continuum considers the importance of intangible assets, esp. brands

Deal due diligence

Operations analysis

Deal structuring

Negotiation

Legal services

Tax and human resources issues

Completion accounts

SPA support

Identifying deals

Evaluating deals

Executing deals

Making deals successful

Harvesting deals

Bid support

Investment banking advice

Deal flow

Strategy evaluation

No-access due diligence

Deal strategy validation

Value driver identification

Target evaluation

Synergy assessment

Pre-deal purchase price allocation

Post merger integration

Synergy review

Operational improvements

Purchase price allocation (IFRS / US GAAP)

Sell-side due diligence

Carve-outs

Capital markets

IPO advice

Buyer identification

Investment banking advice

Pre Deal First 100 days Transformation

Intangible Asset DD

Identification

Assessment

Closing

Aspects of further

Segementation

of Intangible Assets

Improvement

Valuation

Structuring

Management

Exit Strategy

Valuation

Value added

© 2006 PricewaterhouseCoopers. All rights reserved. PricewaterhouseCoopers refers to the German firm PricewaterhouseCoopers AG WPG and the other member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity.

Thanks for your attention!

© 2006 PricewaterhouseCoopers. All rights reserved. PricewaterhouseCoopers refers to the German firm PricewaterhouseCoopers AG WPG and the other member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity.

ContactPricewaterhouseCoopers AGWirtschaftsprüfungsgesellschaftAndreas MackenstedtAdvisory PartnerTel: +49 69 9585 [email protected]

PricewaterhouseCoopers

7 June 2007

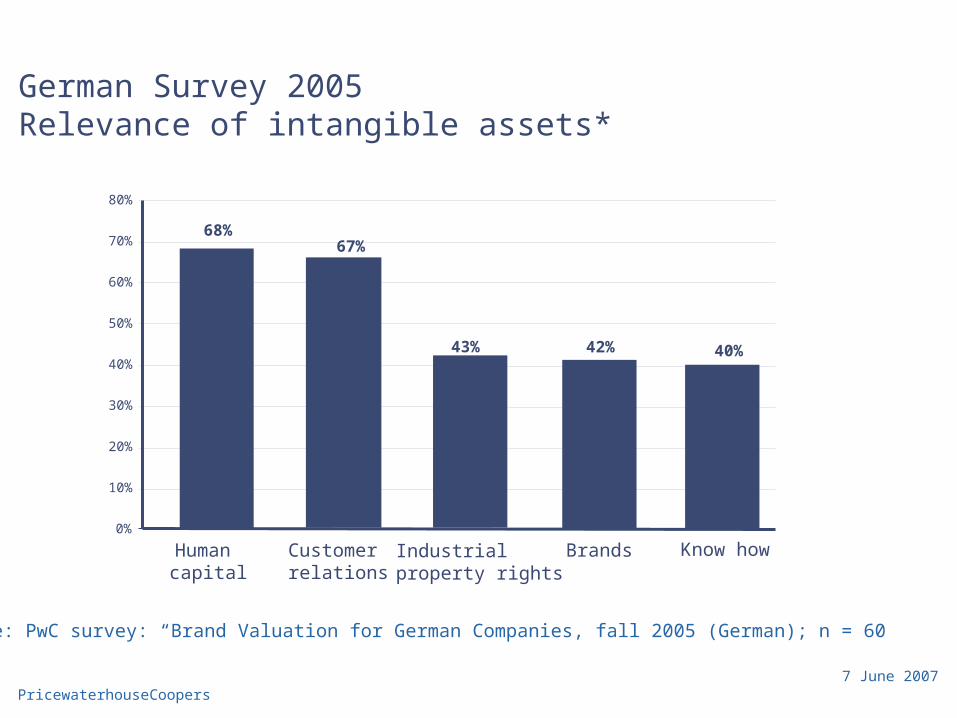

Human capital

Customer relations

Brands Know howIndustrialproperty rights

German Survey 2005Relevance of intangible assets*

68%67%

42% 40%

0%

10%

20%

30%

40%

50%

60%

70%

80%

*source: PwC survey: “Brand Valuation for German Companies, fall 2005 (German); n = 60

43%

PricewaterhouseCoopers

7 June 2007

1999 (n = 100)

German Survey 2005Proportion of brand value compared to business enterpise value*

56%

67%

0%

10%

20%

30%

40%

50%

60%

70%

80%

*source: PwC survey: “Brand Valuation for German Companies, fall 2005 (German)

2005 (n = 60)

Brand strategy and impact on financial reporting

Partner Andreas MackenstedtPrincewaterhouse Coopers

Refreshments

Welcome back at 16.10