the tenants’ guide - nationwide.co.uk/media/mainsite/documents/guides... · chapter 7: moving out...

TRANSCRIPT

The Tenants’ GuideAn independent guide to renting your home

“This Tenants’ Guide from Nationwide will raise tenant awareness further.”Brandon Lewis MP, Minister of State for Housing and Planning

contentsChapter 1: Introduction

Chapter 2: Getting started

Chapter 3: Finding a property

Chapter 4: Becoming a tenant

Chapter 5: Moving in, and your rights

Chapter 6: Day-to-day living

Chapter 7: Moving out

Chapter 8: Glossary and moving home checklist

Click on the chapter links below to jump straight to each section or read the guide from cover to cover:

chapter 1

Click here for contents 3

Introduction

IntroductionIf you are a tenant in the private rental sector then the Tenants’ Guide is for you. It’s been produced by Nationwide Building Society to help make renting your home a smooth and happy experience. Whether you’re renting for the first time, working, retired, or receiving housing benefit, it will help to give you all of the information you need about your rights and responsibilities.

To make it easy to find your way around this guide, we’ve structured it around the different stages of being a tenant – from finding a property to becoming a tenant and moving out. You’ll find a glossary in Chapter 8 that explains all of the key terms featured in the guide, and a list of useful links from each chapter giving more information on important topics. There’s also a handy checklist of who to inform of your change of address when you move home.

Chapter 1 - Introduction

Click here for contents 4

An increasing number of people now rent their home from a private landlord. Empowering tenants to feel confident in their rented home and understand their responsibilities is an important part of this strategy.

Tenancy is changing as the number of people using the private rental sector is growing. More people than ever are opting to rent privately and this includes families, as well as single people. In areas like London, more families are renting than ever before (1.3 million families currently rent across the whole of the UK1).

With increasing numbers of people renting, some financial providers have introduced changes to mortgage policy that make it easier for families to secure longer-term tenancies. This guide will give you the key information you need about any such upcoming changes, and help you to find out more information about renting generally, so you feel more informed and empowered living in your rented home.

Why produce a Tenants’ Guide?A key objective of the Your Home pillar of Nationwide’s Citizenship strategy is to help 750,000 people get into a home of their own.

This is the first time we’ve produced a guide for tenants so we’d really value your feedback. You can contact us at [email protected]

1http://blog.shelter.org.uk/2013/10/the-governments-important-first-steps-towards-better-renting-now-lets-make-it-happen/

“We’re determined to ensure people looking to rent privately are able to do so confident they will get a fair deal.

Our own How to Rent guide will help to create better informed tenants who know their rights and this Tenants’ Guide from Nationwide will raise tenant awareness further.

This, alongside our efforts to encourage private investment from professional landlords, will help deliver a bigger, better private rented sector.”

Brandon Lewis MP, Minister of State for Housing and Planning

Click here for contents 5

Getting started

chapter 2IntroductionWhatever your reasons for renting your home – whether it’s your choice, a stop-gap solution or a result of your current situation – the first question that any letting agent or landlord asks you will always be the same: ‘What can you afford?’ Your answer to this question will have a big influence on the type of property that you live in, but other factors could also influence whether landlords and letting agents consider you a ‘suitable tenant’.

Chapter 2 - Getting started

Click here for contents 6

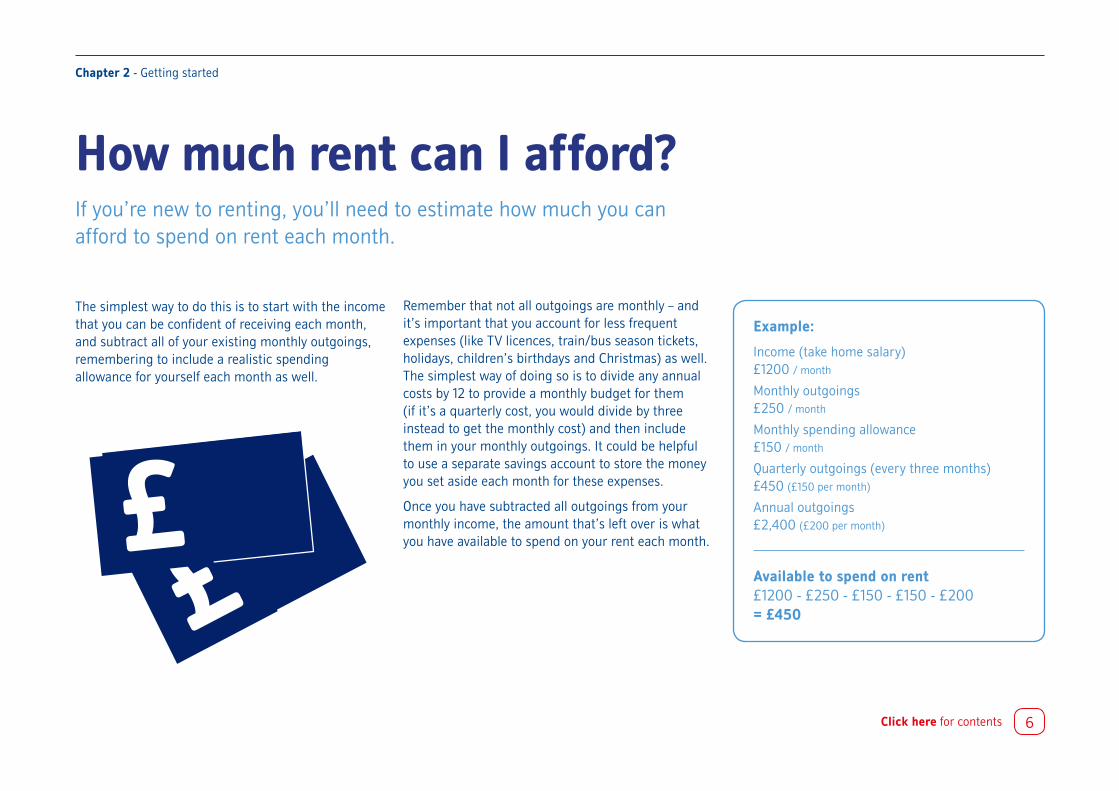

The simplest way to do this is to start with the income that you can be confident of receiving each month, and subtract all of your existing monthly outgoings, remembering to include a realistic spending allowance for yourself each month as well.

Remember that not all outgoings are monthly – and it’s important that you account for less frequent expenses (like TV licences, train/bus season tickets, holidays, children’s birthdays and Christmas) as well. The simplest way of doing so is to divide any annual costs by 12 to provide a monthly budget for them (if it’s a quarterly cost, you would divide by three instead to get the monthly cost) and then include them in your monthly outgoings. It could be helpful to use a separate savings account to store the money you set aside each month for these expenses.

Once you have subtracted all outgoings from your monthly income, the amount that’s left over is what you have available to spend on your rent each month.

How much rent can I afford?If you’re new to renting, you’ll need to estimate how much you can afford to spend on rent each month.

Example:

Income (take home salary) £1200 / month

Monthly outgoings £250 / month

Monthly spending allowance £150 / month

Quarterly outgoings (every three months) £450 (£150 per month)

Annual outgoings £2,400 (£200 per month)

Available to spend on rent £1200 - £250 - £150 - £150 - £200 = £450£

£

Chapter 2 - Getting started

Click here for contents 7

Your monthly outgoings should include all of the following that apply to you: ▪ Council tax (calculated as a monthly cost if you pay quarterly)

▪ Utilities (gas, electricity and water) – you could call a utility company to ask for typical costs, and you can also ask a letting agent

▪ Phone and/or broadband (include connection cost)

▪ TV licence (as well as cable or satellite TV services)

▪ Contents insurance (you’ll be responsible for covering the cost of your belongings)

▪ Any day-to-day costs (such as loan repayments, travel costs, mobile phone, food, and childcare).

BudgetingSpending less on rent than your maximum limit will help to cover unexpected costs or loss of earnings. Make sure you have also accounted for all possible outgoings related to the cost of living, as well as one-off costs that you need to save for throughout the year, and any upfront costs associated with moving (see page 8).

Proof of income When they run their reference checks, most landlords and letting agents will ask to see proof of your income.

They will often require that you earn a particular multiple of the monthly rent you will be paying. So if your rent is £400 per month, you may be required

to earn 2.5 times that. The annual rental cost in this case is £4,800 and you will need an annual salary of £12,000 to cover this.

GuarantorIf you can’t provide proof of income, another option is to find a rent guarantor. This is a person who will cover the cost of any rent arrears or damage to the property if you don’t pay (and if the damage isn’t covered by your deposit). Due to the financial commitment required, most guarantors are family members (your parents, for example). They will need to undergo the same reference checks as you and provide proof of their income to cover the rent.

Budgeting and proof of income Beware of overstretching yourself when working out how much you can afford, to avoid getting into debt.

Chapter 2 - Getting started

Click here for contents 8

DepositThis is the biggest cost you’ll have to allow for and it’s usually four to six weeks’ rent (although the landlord or agent can decide how much). You’re unlikely to find a landlord who doesn’t need a deposit, as this provides important protection if you leave without paying or any damage is caused to the property or its contents. If there aren’t any problems during your tenancy, you should receive it back in full on moving out. The landlord must follow strict rules to protect your deposit (see Chapter 4).

Holding depositA landlord or letting agent might ask for a holding deposit to ‘reserve’ a rental property and take it off the market. This is unlikely to be the full deposit amount but it will be deducted from the deposit that you have to pay when you move in. Be aware,

however, that like many letting fees (see right) it is usually non-refundable. So if you decide not to rent the property or fail any reference or credit checks, you may not get it back.

Pet depositIf you’re allowed to keep a pet, you will normally be asked to pay a pet deposit. Remember, it’s important to be honest with your landlord or agent and inform them of any pets that you may move into the property.

Rent in advanceRent in the private rental sector is normally paid at the start of the month, so you’ll need to pay this upfront when you take up a new tenancy. If you receive housing benefit, you will be paid in arrears, so you’ll need to make arrangements to cover the cost of paying the rent in advance.

Upfront costs Moving home isn’t cheap and there are several costs you need to factor in when you first start renting a new home:

Letting feesLetting agents may charge you a range of fees under different names: a ‘reservation fee’ or ‘application fee’, for instance, to secure the property while the tenancy application is completed. Like the holding deposit this can be used towards the first month’s rent if the tenancy goes ahead (but you may lose it if the application is denied).

Other costs you may be charged for include reference checks or fees for drafting the tenancy agreement, although these can only be charged once your tenancy is agreed. Even if you’re renewing a tenancy and not moving home, the agency may still charge you a fee for doing this. It’s illegal for agencies to charge just for looking for a property for you. In Scotland, it’s illegal for landlords or letting agencies to ask you for any fees.

As a general guide, always ask what your letting agent’s fees are before you commit to anything.

RemovalsYou may be able to move your things yourself, otherwise include any estimates for removal costs in your financial planning.

Chapter 2 - Getting started

Click here for contents 9

Are you a ‘suitable tenant’?The ideal tenant for a landlord or letting agent is somebody who pays their rent on time and doesn’t cause any damage to their property or its contents. It’s why you’ll be asked for references and are likely to have some background checks run on you.

Certain things revealed in your background checks could cause concern for your landlord. If you’ve had trouble with debts, bad credit, a criminal record or if you’ve ever filed for bankruptcy, there’s a risk that you may not be considered a suitable tenant.

Debts and credit historyIf you still have debts, you’ll need to factor the repayments into your monthly outgoings, as it may reduce the amount you can afford to spend on rent, and keep on making regular payments to avoid affecting your credit rating.

If a credit check is run on you, the landlord or letting agent will be able to access publicly available credit information on you, such as whether you have any court judgments (for not paying debts), bankruptcy orders and Individual Voluntary Arrangements (an alternative to bankruptcy that lets you pay back debts over an agreed period of time). This type of credit information is kept on your report for six years.

Criminal recordsIf you have a criminal record you will have to declare it, if asked, for a set number of years (the rehabilitation period) following your conviction. Expect your landlord to ask you, because in many cases it would invalidate their insurance policy on the property if they did not.

What to do if you’re not a ‘suitable tenant’Don’t despair if you have things on your record that could cause you to be considered ‘unsuitable’. There are still ways to make renting work. One option – which many landlords and letting agents will willingly consider – is to use a guarantor. See page 7 for more about how this works.

Don’t forget to register to vote

This is important, as it can affect your credit reference and any loans you are able to take out in the future. You can also now register to vote online. See the useful links in Chapter 8 to find out how to register to vote online.

Chapter 2 - Getting started

Click here for contents 10

Be upfront

Don’t hide anything from a landlord or letting agent – even if it’s about something you don’t think is significant, such as owning a pet or being an occasional smoker. Tell them if they ask, otherwise it could jeopardise your tenancy later on.

Are you a ‘suitable tenant?’, continued.

Information you’ll need to provideA landlord or letting agent will definitely want to see the following information, so make sure you have it available:

▪ The basics: name, date of birth and nationality

▪ Proof that you have the right to be in the country

▪ References from previous landlords – and potentially somebody else who knows you for a character reference

▪ Proof of current address (e.g. bank statement or utility bill)

▪ Details of where you have lived over the last three years

▪ Details of your income / employment (e.g. salary, job title)

▪ Proof of student status (if applicable)

▪ Credit check.

Click here for contents 11

Finding a property

chapter 3IntroductionBefore you start looking for a home to rent, draw up a ‘shopping list’ of requirements such as the location you want, the number of bedrooms you need, and the type of property (whether a detached house, a terrace or a flat, for example). Be aware though that subject to your budget (see Chapter 2) and the supply of properties in your area, you may need to compromise on some of these points. It’s useful to prioritise your requirements at the start, so you know which should take precedence when looking at your rental options.

Chapter 3 - Finding a property

Click here for contents 12

Furnished vs. unfurnishedMany people assume that choosing an unfurnished property will help to reduce their monthly rent. But the truth is that whether a property is furnished or not often has very little impact on the rent that’s charged. If you don’t have any furnishings of your own yet, it’s likely to be cheaper to rent furnished than pay to furnish a property yourself. On the other hand, if you already own a lot of furniture, it is often cheaper to rent unfurnished rather than pay to put your belongings in storage. Your deposit is also less at risk as there is none of the landlord’s furniture to damage.

When renting a furnished property, make sure you check what’s included, that everything works, and that furniture and appliances meet fire safety regulation (see Chapter 6). If you opt for unfurnished, make sure that any furniture belonging to previous tenants has already been removed by the time you move in, otherwise you could end up paying to remove this when you move out.

There are lots of places to seek out your future home: ▪ Online – websites like Primelocation.com, Rightmove.co.uk and Zoopla.co.uk list available properties

▪ Social media – sites like Facebook and Gumtree can be good if you want a spare room or house share

▪ Local newspapers and small ads – these can be useful if you don’t want to deal with a letting agency (or pay their fees) and know your local market

▪ Letting or property management agents – you can find these on the high street or online

▪ Friends and family – although be aware of the pitfalls of renting from those you know!

What are your rental options? It’s important to think about your rental options, as it will influence your property search and what responsibilities your landlord has.

Chapter 3 - Finding a property

Click here for contents 13

Should I rent through a landlord or letting agent? It’s entirely up to you – there are advantages and disadvantages to both options.

Renting directly through a landlord Advantages ▪ Usually cheaper: no letting agent fees

to pay and the rent may be slightly lower (but not always) as the landlord isn’t paying agency fees either.

▪ Some private landlords may not run credit checks, as long as you can show proof of income and references.

▪ Direct relationship with your landlord: they may be more flexible on policies like having pets or late payment of rent; and you may be able to get hold of them quicker in an emergency. Having a good relationship could also mean they’re more willing to let you have a longer-term tenancy. Remember though, that relationships can change, and it’s important to secure your tenancy in other ways as well (see Chapter 4).

Disadvantages ▪ More emphasis on you to check

everything is in place: you’ll need to make sure you’ve checked up on all the landlord’s legal obligations (that you’ve seen a gas safety certificate and that he or she has protected your deposit, for example), as there’s nobody else to do it for you.

▪ If you’re worried that your landlord may not meet his obligations, remember, there are legal protections in place to safeguard your rights (see Chapter 6 for more on these).

Renting through a letting agentAdvantages ▪ Find a home faster: they’ll have a list

of properties and can set up multiple viewings on your behalf.

▪ Convenience: they’ll sort out a lot of the paperwork (e.g. tenancy agreement) and know what legal procedures landlords are required to follow.

▪ Regulation: many letting agents are members of a regulated body so you may have more protection by going down this route. Some agents also belong to the SAFEagent scheme or have client money protection insurance, which means your money is protected if they go out of business or dishonestly take it from you.

▪ Availability: an office of several people can be easier to reach than a landlord who isn’t answering his phone.

Disadvantages ▪ More expensive: expect to pay some

letting agent fees – even if you’re just renewing your tenancy agreement.

▪ Less contact with your landlord: communication is likely to always be through your letting agent, which may make it easier or harder to chase the landlord for things like repairs.

Chapter 3 - Finding a property

Click here for contents 14

Test the shower works; flush the toilet; check each light switch; try any electrical appliances; open and shut doors and windows; and make sure everything is in working order before you commit to a property. Be aware that landlords aren’t required to have formal inspections of the electricity or water supply, but are supposed to maintain them to a reasonable standard.

Check the outside of the property: does the building look like it’s been well maintained? Check whether there is water staining from any gutter leaks. Landlords are required to maintain the interior and exterior of the building (including external pipes, drains and guttering). If there’s a garden, how much maintenance is it likely to require and who’s responsible for this? Ask who is responsible for

window cleaning. Be conscious of your potential new home’s safety and security: are there locks on the windows? Have smoke detectors and carbon monoxide detectors been installed, and are they working? See Chapter 6 for your landlord’s fire safety responsibilities.

If you like a property, try to revisit later that day to get a feel for the area. And if you have a smartphone, you could photograph or video each room and its exterior. If you’re not happy with aspects of the property (such as the decor), ask your landlord or letting agent to make any changes before your tenancy starts.

Viewing properties Don’t skimp on the opportunity to properly check a property when you view it because you’ll be renting it ‘as seen’.

Chapter 3 - Finding a property

Click here for contents 15

Some things to find out:

▪ Exactly what’s included in your monthly rent (for example, any bills? Charges for maintaining any communal areas?)

▪ What fees will be charged if you go ahead? (Most landlords / letting agents will charge for an inventory at the start and end of a tenancy.)

▪ How long has the property been available for? (Be aware of unseen pitfalls if it’s too long – or try negotiating on the rent if you want to go ahead.)

▪ What are the council tax and utilities bills likely to be?

▪ Is the electricity on a pre-payment meter? (If it is, you will need to keep the key charged.)

▪ If you are looking at a flat, who is responsible for cleaning communal areas?

▪ When is rubbish collection day and are appropriate recycling bins provided?

▪ Will the property be cleaned (and any repairs completed) prior to moving in?

▪ Are there any shared costs that might be incurred at a later date (e.g. cleaning communal areas in a shared block of flats)?

▪ Does the letting agent and/or landlord belong to an accredited body? (If they do, they’re more likely to be aware of their legal responsibilities towards tenants.)

▪ How soon will the property be available?

What to ask your landlord or letting agent When you meet a letting agent or landlord it’s your opportunity to interview them, as much as it is for them to ‘vet’ you as a possible tenant, so don’t be shy of asking questions.

Click here for contents 16

Chapter 3 - Finding a property

Gas safety certificate

If there are any gas appliances in the property, the landlord has to have an annual gas safety check, which is carried out by a Gas Safe registered engineer. This will ensure that any appliances they provide are in a safe condition. The landlord has to provide a copy of the gas safety certificate, which confirms the checks have been carried out, before you move in. Bear in mind that if you bring any gas appliances into the property, you will be responsible for these working safely.

Record of electrical safety inspections

Under the law, your landlord doesn’t have to have an electrical safety certificate but he or she does have a duty to keep electrical installations in proper working order, and to ensure that any electrical equipment supplied with the property is safe. The Electrical Safety Council

recommends that a registered electrician examines the property every five years or whenever a tenant moves out, whichever comes first. Ask the landlord or letting agent when the checks were last carried out and if they have an Electrical Installation Condition Report, which outlines what was inspected and tested, and whether any action was required.

Energy Performance Certificate

An Energy Performance Certificate (EPC) rates a property’s energy efficiency so you have an idea of how much energy it uses and your likely energy costs. Your landlord needs to obtain an EPC prior to renting the property (it’s then valid for 10 years) and should supply you with this when you move in.

The documents a landlord should show you Your landlord has legal obligations towards you as a tenant. If you see a property you like, you should request to see the following documents:

Finally...

You should always ask for a landlord’s contact details even if renting through a letting agent. Also, don’t be afraid to ask your landlord or letting agent for references from past tenants.

Click here for contents 17

IntroductionYou’ve seen the property you want to rent, and the landlord or letting agent has agreed to take it off the market. Now you need to complete and sign the paperwork to secure your home.

Becoming a tenant

chapter 4

Click here for contents 18

Chapter 4 - Becoming a tenant

Tenancy agreements A tenancy agreement is a contract between you and your landlord that outlines the rental rights and responsibilities of both parties.

2https://www.gov.uk/private-renting-tenancy-agreements/what-should-be-in-a-tenancy-agreement

It isn’t required by law – legally, you can rent somewhere for up to three years on a verbal agreement alone – but it’s extremely important to have it in case anything goes wrong.

If you are renting a home from a private landlord, then it’s most likely to take the form of an Assured Shorthold Tenancy (AST). This has been the default tenancy in England since the 1996 Housing Act. The equivalent in Scotland is the Short Assured Tenancy.

A tenancy agreement for an Assured Shorthold Tenancy should include the following information: ▪ Your name and the landlord’s name

▪ The rental price and how it’s paid

▪ How the rent will be paid (always ask for a receipt and if you pay weekly, you should get a rent book)

▪ How and when the rent will be reviewed (check for clauses that allow your landlord to increase the rent before the tenancy agreement ends)

▪ The deposit amount and how it will be protected

▪ When the deposit can be fully or partly withheld (e.g. for any damages)

▪ The property address

▪ The start and end date of the tenancy (this is the ‘fixed term’)

▪ Your obligations, and your landlord’s

▪ Which bills you are responsible for.

It can also include information on: ▪ Whether the tenancy can be ended early and how this can be done

▪ Who’s responsible for minor repairs

▪ Whether you can let the property to someone else (sub-let) and whether you can have lodgers

▪ What furniture will be supplied (if any)

▪ Whether there are any other rules (about pets, guests or smoking, for example)

▪ Responsibility for any communal areas including hallways, stairs and outdoor space, such as the garden2.

A tenancy agreement is not allowed to discriminate, so landlords are not allowed to exclude people because they have a disability or because they are pregnant, unless they can give a very good reason. They can exclude tenants on housing benefit though, because some mortgage and insurance providers will make this a condition of their policies.

An agreement also can’t contain anything that’s clearly unfair to you. A clause that allows the landlord to change the terms of the agreement at any time would be unacceptable – and would not be legally enforceable. If you’re unsure of any terms in the tenancy agreement, ask the landlord or letting agent to clarify what they mean, or get legal advice (see Chapter 8) and don’t sign until you’re happy with the contents. Remember to keep a copy of the signed tenancy agreement.

Click here for contents 19

Chapter 4 - Becoming a tenant

Assured Shorthold Tenancies Most tenancies under an AST have a fixed term, which means the start and end date are specified in the tenancy agreement (this is usually six or 12 months).

When the fixed term ends, you don’t have to renew the tenancy agreement but can continue on a rolling month-on-month basis (or week-on-week basis, depending on how often you pay rent). This is called a periodic tenancy and the terms within the tenancy agreement are still valid.

If you want more security, you could ask your landlord to agree another fixed term period when your initial agreement ends but, be aware, that many letting agents will charge you a fee for drafting a renewal tenancy agreement (they won’t be able to if the contract simply continues on a rolling basis or if you live in Scotland).

Break clauses

If you want flexibility on when you move out, make sure there’s a break clause in your tenancy agreement. This enables you to move out and stop paying rent – subject to the legally required notice period – before the end of the fixed term specified in the tenancy agreement.

Click here for contents 20

Chapter 4 - Becoming a tenant

Joint Assured Shorthold Tenancies If you share a property it’s important to know whether you have a joint tenancy (where you all signed the same document) or separate tenancies (where you signed individual agreements). This has implications for your rights.

Joint tenancies in a shared propertyA joint tenancy agreement means that other people you live with share the rights and responsibilities with you.

In a joint tenancy it’s quite common that a single deposit covers the whole tenancy; the advantage of this is you don’t have to fund the entire deposit out of your own pocket. However, you maybe liable if any damage occurs during the tenancy (which will also reduce the amount of deposit you all receive back), and if one person in a joint tenancy doesn’t pay their rent, the others will have to pay it for them.

If you are still within the fixed term of an AST, the tenancy cannot be ended early unless all of the joint tenants agree and either your landlord agrees that the tenancy can end early (this is called a ‘surrender’),

or there is a ‘break clause’ (see page 19) in your tenancy agreement.

If you have passed the end date in your tenancy agreement and one of you gives the landlord notice to end the agreement, it will normally be ended for everyone – even if it’s not a joint decision. However, the landlord must be given a valid written notice and there are special rules about how and when this must be done. Be aware that joint tenancies can be complicated. See Chapter 8 for more advice on these types of tenancy from Shelter, an independent housing charity,

Living with your partnerMany people choose to rent with their partner. Should the worst happen and you split up, there are ways you can continue living in the property on your own –

even if you shared a joint tenancy. If your relationship breaks down violently, there are organisations that can give you support too. See Chapter 8 for advice on this from Shelter and other organisations that might be able to help you.

Separate tenancies in a shared propertyIt’s not unusual to share a house with other people but have different tenancy agreements. If you have your own tenancy agreement this means you’re responsible only for your own rent and if somebody is evicted it doesn’t affect your tenancy. Just make sure you know what rights and responsibilities your own tenancy agreement gives you.

Click here for contents 21

Chapter 4 - Becoming a tenant

Longer-term lets The standard tenancy term is six to 12 months, and this is usually what’s specified in an Assured Shorthold Tenancy.

However, short-term lets (usually defined as anything under six months), and longer-term lets (tenancies over 12 months, sometimes up to three years) are also available.

Longer-term lets can make a lot of sense for families, particularly those with children at school who value having some certainty over where they will be living. It can also save on moving costs, as you don’t have to relocate as frequently.

If you want a longer-term tenancy, raise it with the landlord or letting agent as early as possible. Be aware that if you take up a longer-term let without a break clause, you are committed to staying – and paying the rent – for the full length of the term. You will need to negotiate with the landlord and get their agreement should you want to end the tenancy early.

Click here for contents 22

Chapter 4 - Becoming a tenant

DepositsWhen you sign your tenancy agreement, you’ll normally be expected to hand over the deposit and your rent in advance at the same time.

Tenancy deposit protection schemesLandlords letting their properties on an AST basis have to register their tenants’ deposits with a Government-approved tenancy deposit protection scheme within 30 days of receiving it. This ensures that you get your deposit back at the end of the tenancy – assuming you have met the terms of your tenancy agreement, not damaged the property and paid your rent and bills during your time living in the property. Even if your parents or a guarantor have paid the cost of the deposit for you, it still needs to be protected in the same way.

3https://www.gov.uk/deposit-protection-schemes-and-landlords/information-you-must-give-to-your-tenants

Bear in mind

Landlords don’t have to protect a ‘holding deposit’ in a tenancy deposit protection scheme until it becomes part of the ‘full deposit’.

Within 30 days of getting your deposit, your landlord has to tell you, in writing, the following:

▪ The address of the rented property

▪ How much deposit you’ve paid

▪ How the deposit is protected

▪ The name and contact details of the tenancy deposit protection scheme and its dispute resolution service

▪ Their (or the letting agency’s) name and contact details

▪ The name and contact details of any third party that’s paid the deposit

▪ Why they would keep some or all of the deposit

▪ How to apply to get the deposit back

▪ What to do if you can’t get hold of the landlord at the end of the tenancy

▪ What to do if there’s a dispute over the deposit3.

What happens if your deposit isn’t protectedYour landlord could be forced to pay you up to three times the deposit. A court may also decide that you won’t have to leave the property when the tenancy ends.

Remember:

Always ask your landlord or letting agent which approved schemes they’ve used.

Click here for contents 23

Chapter 4 - Becoming a tenant

Housing benefitAround one in four private tenants use some form of housing benefit to help pay their rent4.

The benefits market is undergoing significant change, so if you receive benefits it’s important to know how the changes will affect you.

Local Housing AllowanceUnder the current system, most tenants in the private rented sector receive housing benefit through a local housing allowance (LHA), which is determined by the number of bedrooms they have and rental prices in the area. This is paid directly to the tenant unless they fall behind on payments for eight weeks or more, in which case the council pays the LHA direct to the landlord. They can also do this if the tenant has a history of not paying their rent, is considered to be vulnerable, suffers from mental illness, or has a history of substance misuse, which means they could have problems keeping up payments.

Universal creditUnder the incoming system of universal credit, you can still claim housing benefit if you need help paying rent, but this will be rolled into a single lump sum

with any other benefits you receive, rather than paid out separately.

As with local housing allowance, universal credit will usually be paid to the tenant rather than the landlord. However, if you fall behind on your rent, your landlord can be paid directly. You can also ask for the rent element of universal credit to be paid to your landlord, with each case considered on its merit.

To find out about the level of your housing benefit entitlement, you will need to contact the Department for Work and Pensions (see Chapter 8).

4https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/211288/EHS_Headline_Report_2011-2012.pdf

Remember:

If you’re entitled to housing benefit, you might also be entitled to council tax benefit. Speak to your local council to find out.

chapter 5Moving in and your rights

Click here for contents 24

IntroductionWhen you move into your new home, you’ll be taking on certain rights and responsibilities as a tenant. This section will help to ensure that the moving process goes smoothly, and that you have everything you need to protect your rights in the future.

Click here for contents 25

Chapter 5 - Moving in and your rights

Tenant and landlord rightsAs a tenant, the law gives you and your landlord rights to help keep you safe in your home.

Your rights ▪ To live in a property that’s safe and in a good state of repair

▪ To have your deposit returned when the tenancy ends – and to have it protected (if you have an Assured Shorthold Tenancy)

▪ To challenge excessively high charges (see the Glossary in Chapter 8 for who to approach)

▪ To know who your landlord or their representative is

▪ To live in the property undisturbed

▪ To see an Energy Performance Certificate for the property (see Chapter 3)

▪ To be protected from unfair eviction and unfair rent

▪ To have a written agreement if you have a fixed-term tenancy of more than three years

▪ If you do have a tenancy agreement (see Chapter 4), to have a fair one that complies with the law.

If you don’t know who your landlord is, ask the person or company you pay rent to, in writing. They should give you this information within 21 days, otherwise your landlord could be at risk of a fine for not providing the details.

In return, your landlord has some rights too: ▪ To reasonable access to the property for inspection or repairs (but they must give at least 24 hours’ notice and visit at a reasonable time of day, unless it’s an emergency)

▪ To agree the terms of the tenancy (for example, the property cannot be sub-let without their agreement)

▪ To receive rent on time

▪ To receive proper notice of departure

▪ To be able to serve an eviction notice if you don’t pay rent and show no sign of doing so

▪ To increase the rent at certain times and within certain circumstances, as long as the new rent is fair and justifiable

▪ To charge the cost of any repairs to you if you caused them5.

Find out more about your responsibilities as a tenant – and those a landlord has towards you – in the next chapter.

5Visit https://www.gov.uk/government/publications/how-to-rent for a checklist to help tenants renting in England

Click here for contents 26

Chapter 5 - Moving in and your rights

Moving home and checklistHere’s a quick checklist of things to do before moving into your new home – and some important measures to protect yourself on the day.

Ahead of your moving-in dateIf you’re renting already, give the correct notice period for your existing property. You’ll find this in your tenancy agreement.

Make sure all your belongings are packed up. If you’re going to be using a removals firm, book it as far in advance as possible and avoid Fridays, as they’re usually busiest then.

Set up a redirection for your post. See Chapter 8 for a checklist of who to inform).

Remember to insure your contents for your new home and make sure any insurance policy begins on the day you move in.

You may need to set up a standing order for your rent every month if this is how you’ve agreed to pay your landlord or letting agent.

Make sure your TV licence is in place.

Let your council tax department know you are moving house. You may have to complete a change in circumstance form with your new details.

Let your existing utilities providers (water, gas and electricity) know that you’re moving out. They’ll also want you to take meter readings on the day itself. If you’re on a fixed price tariff, be aware you can’t always transfer this to your new home (and may have to pay an early penalty), Speak to your provider to find out what their terms are. Otherwise, now is a good time to seek out a better deal.

On the day of your moveRead your meters at your old rental property and give them your new address for the final bill.

Arrange a time to meet the landlord or letting agent at the property to get your keys and move in.

Read the meters and call the utility companies.

Check all the supplies work (electricity, water and central heating) before accepting the keys.

Take photos of the condition of the property when you move in.

Check everything works that’s listed in the inventory and ask for instruction manuals for all appliances. Make sure you know important basic information like: how the boiler works, the location of the water stop tap and where the fuse box is if the electric trips off. If there’s a security alarm, check this and make sure you have the code. Don’t forget to check smoke alarms at the same time.

Find out who’s going to be your main point of contact: is it the landlord direct or an agent acting on his or her behalf? Make sure you have the right contact details for any emergencies. Ideally, you want two phone numbers, an email address and a postal address (for written communications).

Click here for contents 27

Chapter 5 - Moving in and your rights

The inventoryThis outlines what fittings, furnishings and appliances are provided as part of the rental agreement.

It can include anything from carpets to shower curtains, and light fittings to pots and pans. It should also describe the property condition at the start of the tenancy. This could include details about how clean the property is, as you’ll be expected to leave it the same way when you move out.

Your landlord or letting agent doesn’t have to supply you with an inventory (except in Northern Ireland – where a landlord must provide an inventory of any furniture and furnishings for tenancies since April 2007). If they don’t, you should record one of your own, so that you have signed evidence of the state of the property and its belongings at the start of your tenancy (make sure you send a copy of it to your landlord). Besides a written inventory, you can record video and take photographs of the property as well.

If your landlord is producing an inventory, try to be there when they compile it. If he or she isn’t, make sure you have an independent witness (somebody who’s not going to be living at the property with you) who can sign your version.

Some landlords and letting agents will employ a ‘check in’ specialist to do the inventory, rather than doing it themselves. It’s exactly the same process, however. Clearly check everything that’s listed on the inventory and make a note of the state it is in. This will help you to get your deposit back at the end of the tenancy. If there are any features that you think could be disputed at a later date (e.g. existing damage to the walls) then photograph or video these. If you dispute anything in the inventory at this stage, you need to raise this straightaway. Do not sign if there is something listed on the inventory that’s not present in the property.

Be aware that your landlord or letting agent will also need to agree on the contents of the inventory and the state of the property, and sign and date all inventory documents including photographs. It can help to hold up the day’s newspaper next to the items you are videoing or photographing to date the ‘evidence’.

Wear and tear

It’s inevitable that furniture and fittings will suffer some wear and tear during the rental period. Landlords and letting agents expect this, and it shouldn’t affect your deposit. However your deposit is at risk if there is any damage to the property that isn’t repaired during the tenancy period, or if there is ‘excessive’ wear and tear.

Hold onto important documents

It’s important not to lose any important documents, like the tenancy agreement, inventory and any photographs or video footage. You may need these as evidence if there’s a dispute at the end of it, so store them in a safe place. Also keep hold of any receipts for items you have replaced or had repaired; receipts for rent payments and bills (particularly the final ones to prove you’ve paid up your utility bills); and a copy of any letters to and from your landlord or letting agent.

Click here for contents 28

IntroductionYou’ve found the property, signed the paperwork and now you’ve moved into your home. But before you start banging picture hooks into the wall or redecorating the bedroom, you should make sure you know what you’re allowed to do and not do in your new home and, importantly, what to do in the event of things going wrong.

Day-to-day living

chapter 6

Click here for contents 29

Chapter 6 - Day-to-day living

Tenant and landlord responsibilitiesYou and your landlord have certain responsibilities towards each other now you’re in your new home.

Being a responsible tenantThere are certain things you need to do, in order to abide by your responsibilities as a tenant:

▪ Give your landlord access to the property to inspect it or carry out repairs (your landlord has to give you at least 24 hours’ notice and visit at a reasonable time of day, unless it’s an emergency)

▪ Take good care of the property (for example, by turning off the water at the mains if you’re away in cold weather)

▪ Pay the agreed rent, even if repairs are needed or you’re in dispute with your landlord

▪ Pay other charges as agreed with the landlord (such as council tax, TV licence and/or utility bills)

▪ Pay for any damage caused by you, your family or friends

▪ Deal with your rubbish properly by putting it into bins and out for collection on the correct day

▪ Heat the property adequately and make sure it’s kept well ventilated, which includes opening the windows to help prevent condensation6

▪ Only sub-let if the tenancy agreement, or your landlord, allows it7.

Abiding by your tenancy agreementAs a tenant you’re expected to live in the property. This means that if you go away for any length of time, you should tell your landlord. And of course, you need to continue paying your rent.

Be aware that anti-social behaviour by you or anybody living at or visiting your address could get you evicted. If your neighbours complain to your landlord about any anti-social behaviour, your landlord is expected to intervene. Anti-social behaviour could be considered

playing music loudly or late at night, leaving rubbish outside your home which has not been collected or visitors making noise when they come to see you. You should also tell your landlord if your neighbours are causing you any problems. If people in a number of houses in an area are behaving anti-socially, your local council can create a ‘selective licensing scheme’. This means that all landlords of properties in that area must have a licence to show they’re meeting minimum standards8.

Smoking is allowed in a rental property unless the tenancy agreement says otherwise; however, you shouldn’t smoke in any parts of the building that are shared with other tenants.

If you’re unsure about anything or your circumstances change, check your tenancy agreement and if you’re still not clear, talk to your landlord. For instance, if you want to set up a business from your home, keep a pet, take in a lodger or pass on the tenancy, ask first.

6http://england.shelter.org.uk/get_advice/renting_and_leasehold/rights_and_responsibilities/tenants_responsibilities7https://www.gov.uk/private-renting8https://www.gov.uk/private-renting/antisocial-behaviour

Click here for contents 30

Chapter 6 - Day-to-day living

Tenant and landlord responsibilities, continued.

You should put everything in writing to your landlord, keep a copy and make sure you receive written permission before you do anything.

Your health and safetyYour landlord is responsible for important aspects of your health and safety in the property:

▪ They must comply with fire safety regulations (for example, by checking you have access to escape routes at all times)

▪ They must make sure any furniture and furnishings that they supply are fire-safe (but be aware that duvets, carpets and curtains are exempt from this requirement)

▪ They must provide fire alarms and extinguishers (depending on the size of the property)

▪ They must properly maintain gas appliances, pipes, flues and ventilation, and provide a certificate confirming this has been done

▪ They must ensure electrical wiring meets safety standards (there are enough circuits and sockets, for example).

Your landlord is also responsible for managing and maintaining the fire safety systems in your home – but it’s a good idea to make your own checks as well. In single household dwellings, it’s recommended that fire detection systems are tested at least once a year, but, for your own safety, you should check alarms more regularly (every week or month, for example). Take sensible fire precautions (not covering electric heaters with wet belongings, for example), and keep escape routes free of storage and clutter.

If your property is part of a shared dwelling (like a block of flats), you will need to provide regular access to your flat for testing central fire alarm systems, or arrange for the landlord or letting agent to enter the property and do this for you.

Click here for contents 31

Chapter 6 - Day-to-day living

House in Multiple OccupationA House in Multiple Occupation (HMO) is a property occupied by at least three tenants, forming more than one household, and sharing toilet, bathroom or kitchen facilities.

An HMO can be anything from a house split into separate bedsits to a shared house (where everyone has separate tenancy agreements) to shared accommodation for students (although many halls of residence aren’t classed as HMOs). If you are living in an HMO, your landlord has some extra responsibilities that you should be aware of:

▪ Ensuring there are smoke detectors in every bedroom and communal area, and that the kitchen has a heat detector

▪ Carrying out annual gas safety checks

▪ Checking the electrics every five years

▪ Making sure the HMO isn’t over-populated

▪ Ensuring there are adequate cooking and washing facilities

▪ Ensuring communal areas and shared facilities are clean and in good repair

▪ Ensuring there are enough rubbish bins for everyone living in the house9.

HMOs with three or more floors, which are occupied by five or more people and two or more households, must have a licence from the council to ensure they meet certain standards. The council can also request other HMOs obtain a licence if they are concerned about the living standards at these properties.

If you’re thinking about moving into a shared place, ask the landlord or letting agent if it counts as an HMO. If it does, ask the council if it currently has a licence.

9http://england.shelter.org.uk/get_advice/renting_and_leasehold/sharing_and_subletting/houses_in_multiple_occupation

Click here for contents 32

Chapter 6 - Day-to-day living

Repairs and renovationsSome wear and tear is inevitable in a property over time, but you will be expected to look after your new home as best as you can. Check your tenancy agreement for the small print on things like whether you can redecorate or put up pictures, and ask your landlord if you’re unsure.

When it comes to repairs, it’s best not to attempt to fix things yourself (unless the tenancy agreement says you can), but to call your landlord instead. The tenancy agreement will also outline the process for reporting faults.

Your landlord has a duty to carry out repairs within a reasonable period of time (which depends on the type of repair). For example, if your toilet is not flushing then your landlord should make arrangements for this to be completed quickly. Don’t stop paying your rent while waiting for repairs to be done, as this would put you in breach of your tenancy agreement and could give your landlord the right to evict you.

Ask your landlord to keep in touch with you about dates for starting repair work, and ask for a rough idea of how long the work might take. If you need to prompt your landlord, you’ll find a link for a useful letter template from Shelter in Chapter 7.

10https://www.gov.uk/private-renting/repairs11http://england.shelter.org.uk/get_advice/renting_and_leasehold/rights_and_responsibilities/tenants_responsibilities

Your landlord has responsibility for maintaining your home, in particular: ▪ The property’s structure and exterior

▪ Basins, sinks, baths and other sanitary fittings, including pipes and drains

▪ Heating and hot water

▪ Gas appliances, pipes, flues and ventilation

▪ Electrical wiring

▪ Making good any damage they cause by attempting repairs

▪ Your landlord or their representative is also usually responsible for repairing common areas, like staircases in blocks of flats10.

As a tenant, you are responsible for: ▪ Looking after internal decorations, furniture and equipment. If the carpet becomes a little thin, it’s fair wear and tear; if you burn a hole in it, you’ll probably have to pay for it

▪ Not using appliances that you think might be unsafe

▪ Reporting any repairs needed or other problems that you are aware of

▪ Minor maintenance (such as checking smoke alarms are working, changing light bulbs, etc.)11

Click here for contents 33

Chapter 6 - Day-to-day living

Repairs and renovations, continued.

If repairs aren’t carried out, you should contact your landlord first, keep a record of the contact you have made and the lack of response. If you’ve exhausted all options with your landlord, contact the local council’s environmental health department. You also have the right to carry them out and deduct the cost of the works from any future rent payments. However, you must give your landlord notice of your intention, obtain three estimates for the job, and go with the lowest of the three.

Major repairsIf repairs are significant, your landlord needs to explain what needs doing, how long it might take and what level of disruption it will cause. It may be that some of your home will be inaccessible while the repairs are taking place, in which case you may be able to get some of your rent back (‘rent abatement’) from your landlord. If you have to move out, the landlord may have to find you alternative accommodation. If you refuse, the landlord could obtain a court order to evict you temporarily while the works are carried out, or permanently. If you move out, make sure you have it in writing that you can move back in again afterwards.

Documenting the need for repairs

It’s a good idea to keep a record of the impact of any damage, and the need for repairs:

▪ Take photographs of the things that need repairing

▪ Keep belongings that have been affected (such as clothes damaged by dampness), or take photographs of them. Work out how much they are worth

▪ Get an expert (such as an environmental health officer from the council) to inspect your home

▪ Keep copies of any doctor’s notes or hospital reports, which show that your health has been affected by poor maintenance

▪ Keep receipts for any money you need to spend because of a problem (for example, if you have to replace clothes or furnishings because of mould, or if you have to pay for pest control or a damp survey)

▪ Keep copies of all correspondence between you and your landlord about the repairs12.

12http://england.shelter.org.uk/get_advice/repairs_and_bad_conditions/disrepair_in_rented_accommodation/repairs_in_private_lets/reporting_repairs_to_a_landlord

Click here for contents 34

Chapter 6 - Day-to-day living

If you have problems with paying the rentLife doesn’t always run smoothly, so make sure you know what to do if you should fall behind with the rent.

If you can’t keep up your rent payments it’s important to take action immediately, as your landlord can evict you. They could also take you to court to claim back any rent and it may affect any future references.

The first thing you should do is talk to your landlord; don’t avoid them. It shows you are committed to clearing your debt and your landlord may be willing to negotiate a way of paying the rent you owe. If the change in your circumstances is temporary, they may also be more willing to help you.

If you have recently lost your job or are on low income, you may be able to get housing benefit to help pay your rent. If you are already receiving housing benefit, the council may decide to pay this direct to the landlord. If the problem lies with the council (there’s been a delay in your housing benefit claim) you could receive an interim payment within

14 days called a ‘payment on account’ that may help to stop your landlord from evicting you.

If you can’t afford your rent because there is a shortfall between your housing benefit payments and the rent, you may be entitled to a ‘discretionary housing payment’ that makes up the difference. In Scotland, you might be able to apply for a debt payment programme under the Debt Arrangement Scheme (DAS) – see Useful links in Chapter 8 for how to do this.

Know your rent

You should keep any records of rent payments made and statements in case of a dispute with your landlord.

££

Click here for contents 35

Chapter 6 - Day-to-day living

Continuing your tenancy

Depending on your tenancy type, the tenancy agreement will say when the fixed term is up. If both parties are happy, the tenancy can continue on a periodic basis (rolling on a week-by-week or month-by-month basis) or you can re-negotiate another fixed term. Be aware, some lettings agents will charge you a fee for renewing the tenancy agreement.

Rent increasesFor a fixed-term tenancy, your landlord can only increase the rent if you agree. For any rent increase, your landlord must get your permission if it’s by more than previously agreed, and it must be fair and realistic (compared with local rents, for example). If you think the rent increase is unfair, you can apply to the First-Tier Tribunal (Property Chamber) in England and Wales, or the Private Rented Housing

Panel in Scotland. But be aware, under most tenancy agreements, your landlord can evict you by giving you two months’ notice so may choose to do this instead.

If your landlord goes into mortgage arrearsThe mortgage lender could become your landlord and/or you could face eviction. It depends if your tenancy is binding on the landlord’s lender or not. See Chapter 8 for advice on this from Shelter.

What to do if your landlord won’t accept your rent

If you’re in dispute with your landlord, he or she may refuse to collect the rent, so they can argue you breached the terms of your tenancy agreement, giving them grounds for eviction. If this happens, write to your landlord explaining that you want to pay the rent and keep a copy for your records. Make sure you have the outstanding rent available to pay13.

If you receive housing benefit and your rent changes, you must let the council know straightaway.

13http://england.shelter.org.uk/get_advice/paying_for_a_home/rent_and_rent_increases/private_tenancies

Click here for contents 36

IntroductionWhether it’s your choice to move out or your landlord’s decision, it’s important to know what’s required of both of you. This section will help you avoid owing money, give you advice for getting your deposit back in full and provide you with information about your tenancy type.

Moving out

chapter 7

Click here for contents 37

What to do if you want to leaveIf you want to move, you can’t just pay your last month’s rent, pack your bags and pop your keys through the door.

This is called ‘abandonment’ and your landlord is within his or her rights to continue charging you rent – and use the force of the law to demand that you pay it – until you serve notice correctly. Leaving this way could also jeopardise your chances of renting anywhere else, as most landlords will want a reference from your previous landlord.

If you’re on a fixed-term tenancyIf your tenancy is an AST, you’ll probably have signed up for an initial fixed term of six months or one year. If you have to leave before the end of the fixed term, you’ll need to check if your tenancy agreement includes a break clause, which lets you leave early. If it doesn’t, you should speak to your landlord to see if you can reach an agreement to finish the tenancy – you could offer to help him or her find some new tenants, for example – otherwise you will have to continue paying the rent until the end of the fixed term.

If you want to move out on the date the fixed term ends, you’ll need to give your landlord written notice up to two months beforehand (in Northern Ireland, it’s one month). So if your term ends on 1 December, you’ll want your tenancy to end on 30 November and need to submit your notice by 30 September (or 30 October if you live in Northern Ireland).

If you’re on a periodic tenancyIf the fixed term period of your tenancy has expired and you haven’t been issued with a new one then you will have a periodic tenancy. With a periodic tenancy, your tenancy rolls on each time you make a rental payment. So if you pay rent monthly, you need to give a month’s notice; if it’s weekly, your notice period is weekly, and so on.

Always check the terms of your tenancy agreement (see Chapter 4), to know exactly what notice you need to give your landlord of your departure.

14http://england.shelter.org.uk/get_advice/renting_and_leasehold/ending_a_tenancy_or_licence/ending_a_periodic_agreement

Chapter 7 - Moving out

How to give notice

Give notice in writing and keep a copy for your records. Include in your letter the property’s address, the date you’ll be leaving and how your landlord can contact you. Deliver the letter by hand or post by recorded delivery – and get a receipt. Only give notice by email if your tenancy agreement says you can14.

Click here for contents 38

What to do if your landlord serves noticeDepending on your tenancy type, there are set procedures your landlord must follow to serve notice.

Section 21 noticeIf your landlord intends to end the AST then he must serve you with written notice, which should be for a certain period of time: two months or two weeks depending on the circumstances. In most cases, the notice issued will be for two months and is often referred to as a ‘Section 21 notice’ (this refers to the legal section as set out in housing law).

Your landlord does not need to specify a reason for eviction when using a Section 21 notice. But unless there’s a break clause in your tenancy it’s likely to be at the end of your fixed notice period (e.g. 12 months) – in which case, the landlord will need to serve the notice two months prior to this date. If your tenancy is running as a periodic (see page 19), your landlord should still give you two months notice – so two months to find somewhere else to live and move out – and will end on the day before the rent is paid.

If you don’t move outIf you don’t move out by the time the notice period is up, your landlord will need to go through the court to evict you. Be aware that staying in the property isn’t something you should consider lightly, as your landlord may charge you any fees incurred in going to court to evict you.

Your landlord will present all the written documents relating to your tenancy at court and it will be their decision to issue a ‘possession order’, which gives the landlord permission to evict you from the property.

Where a Section 21 notice has been served, the court will usually allow eviction, providing the papers are accurate and have been served correctly. Generally, a court order will give you four to six weeks to leave the property; you may be allowed to ask the court for extra time, but this will be at the court’s discretion.

Chapter 7 - Moving out

Illegal eviction

Only bailiffs can evict you physically from the property, not your landlord. If he or she does this, it is a serious offence.

If you have not left after the possession order has ended, then you will be issued with a bailiff’s warrant. This means the bailiffs can physically remove you from the property if you have not moved out by the expiry date on the warrant.

Click here for contents 39

Other noticesThere are occasions when a different notice can be served. In certain circumstances, you may be issued with a two-week notice to leave the property, even if you have a fixed term tenancy. This might be because:

▪ You are late paying rent

▪ You are in rent arrears

▪ The property is mortgaged and your landlord’s lender is repossessing the property

▪ Your landlord thinks the condition of the property is worsening while you are in occupation

▪ There are complaints about anti-social behaviour (see page 29).

When the notice period has ended, your landlord can follow a similar court eviction process if you have not left. This means evidence will be presented to the court relating to the reason for eviction. If the court is satisfied with this information, then a possession order will be issued.

If you are still in the property after this time, your landlord will request a bailiff’s warrant. This will give you seven to ten days to leave the property. It is important to have left before the bailiff warrant ends because then you no longer have any legal right to remain in the property, and they are authorised by the court to physically remove you from the property.

You may be able to ask a court to stop or delay an eviction – but you will need to do this straightaway. Visit Shelter’s advice line (see the useful links in Chapter 8) to find out if you have a valid case.

15http://scotland.shelter.org.uk/get_advice/advice_topics/eviction/eviction_of_private_tenants

Chapter 7 - Moving out

Giving notice in Scotland

In Scotland, the eviction process is similar, but your landlord will need to serve different notices15.

What to do if your landlord serves notice, continued.

Click here for contents 40

Chapter 7 - Moving out

Getting your deposit backYou should avoid using your deposit to pay your last month’s rent – especially if you’re unlikely to receive it back in full (perhaps due to some accidental damage) – as your landlord could take you to court for unpaid rent.

If you have an AST and your deposit has been protected, the deposit has to be given back to you within 10 days of the tenancy ending. If you’re not going to receive the full deposit back, your landlord needs to explain why, in writing, and show you copies of any receipts they have received for works carried out. If you dispute what your landlord says, the tenancy deposit protection scheme will hold onto the deposit until it has been resolved. They are likely to recommend you contact their free Alternative Dispute Resolution service to try and find a solution, or you can go to the courts.

££ £

£ ££££ £

Click here for contents 41

Glossary and useful links

chapter 8

Click here for contents 42

GlossaryAssured Shorthold Tenancy (AST)The most common form of tenancy since the 1996 Housing Act, it is a type of assured tenancy. In Scotland, it is known as the Short Assured Tenancy.

Break clauseA break clause in your tenancy agreement enables you to move out and stop paying rent before the end of the fixed term.

DepositA payment, usually equivalent to four to six weeks’ rent given to the landlord or letting agent prior to moving in. It protects them if you leave without paying or any damage is caused to the property or its contents.

Fixed termThe length of time specified in the tenancy agreement. Usually you can’t move out and stop paying rent before this is up, unless you have a break clause.

GuarantorSomebody who will ‘guarantee’ your rent i.e. be responsible for paying rent if you fall into arrears, or pay for any damage you cause that the deposit doesn’t cover.

Holding depositA deposit (usually non-refundable) to ‘reserve’ a rental property, which is then deducted from the full deposit.

House of Multiple Occupation (HMO)A house or flat in which two or more households live as their main or only residence, and where some of these households share basic facilities, such as a kitchen, toilet or bathroom. If you live in an HMO, your landlord is required to undertake additional safety standards.

Housing benefitA means-tested benefit you may receive towards rent and some service charges.

Illegal evictionThis is a serious offence and one that can be committed if anybody except a bailiff (or sheriff in Scotland) attempts to remove you forcibly from the rental property.

InventoryA document outlining what fittings, furnishings and appliances are provided as part of the rental agreement. It also includes information about the

Chapter 8 - Glossary and useful links

property condition at the start of the tenancy. You and your landlord or letting agent need to sign and date it for the document to be valid. In Northern Ireland, it’s mandatory for new tenancies.

Letting agentSomebody who lets the property on behalf of your landlord. They will probably charge you higher fees than if you rent a property directly from a landlord.

Letting feesLetting agents may charge you a range of fees under different names. In Scotland, it’s illegal for landlords or letting agencies to ask for any fees.

Local Housing AllowanceHow housing benefit is determined in the private rental sector. Local Housing Allowance rates are based on the size of household and area in which you live, so vary across the country.

Longer-term letUsually defined as a rental period of more than 12 months.

Periodic tenancyA tenancy that rolls on each month or week

Glossary, continued.

Chapter 8 - Glossary and useful links

Click here for contents 43

(depending on how regularly rent is paid). Most ASTs default to a periodic tenancy, unless they are renewed at the end of the fixed term.

Rent arrearsThe name for late rent payments.

Service chargesCharges to cover the cost of maintaining communal facilities – like insurance for the building, lighting communal ways or management agent fees.

Short-term letUsually defined as a rental period of less than six months.

Tenancy agreementA contract between you and your landlord that outlines the rights and responsibilities of both parties. You can have individual or joint tenancy agreements.

Tenancy deposit protection schemeThe name given to the scheme that protects your deposit.

Universal creditThis is the incoming system for paying benefits, which is being phased in gradually. With universal credit, people looking for work or on a low income will receive a single universal credit payment, rather than several different benefits (including housing benefit).

Click here for contents 44

Chapter 8 - Glossary and useful links

Chapter 2 Budget planner https://www.moneyadviceservice.org.uk/en/tools/budget-planner

Find out your council tax band https://www.gov.uk/council-tax-bands

Shelter Scotland’s online toolkit for reclaiming letting agent fees http://www.reclaimyourfees.com/toolkit/

Shelter’s advice finder http://england.shelter.org.uk/get_advice/advice_services_directory http://scotland.shelter.org.uk/get_advice

BBC’s ‘Where can I afford to live?’ calculator http://www.bbc.co.uk/news/business-23234033

Housing advice for private rental tenants in Northern Ireland http://renting.housingadviceni.org

Understand credit scoring http://www.moneysavingexpert.com/loans/credit-rating-credit-score

If you have a criminal record, check if your conviction is spent with this calculator http://www.disclosurecalculator.org.uk

Find out more about the electoral registration system www.aboutmyvote.co.uk

Register to vote www.gov.uk/register-to-vote

Chapter 3Shelter has a useful checklist for assessing rental properties http://england.shelter.org.uk/__data/assets/pdf_file/0015/23361/Checklist_-_assessing_rental_properties.pdf

Check an area’s crime statistics Police.uk

Citizens Advice Bureau – for advice on legal, money and other issues http://www.citizensadvice.org.uk

Association of Residential Letting Agents www.arla.co.uk

National Approved Letting Scheme www.nalscheme.co.uk

National Landlords Association www.landlords.org.uk

Residential Landlords Association www.rla.org.uk

SAFEagent www.safeagents.co.uk

UK Association of Letting Agents www.ukala.org.uk

Find a home to renthttp://www.zoopla.co.uk/to-rent/property/uk/

Chapter 4Find a legal adviser http://find-legal-advice.justice.gov.uk

Department of Work and Pensions for finding out your benefits entitlement https://www.gov.uk/browse/benefits/entitlement

LHA Direct calculator to find out the maximum amounts of local housing allowance in different areas https://lha-direct.voa.gov.uk/search.aspx

Universal credit https://www.gov.uk/universal-credit

Tenancy rights checker from Shelter (England only) http://england.shelter.org.uk/get_advice/downloads_and_tools/tenancy_checker

Advice on joint tenancies if you live in England http://england.shelter.org.uk/get_advice/private_renting/private_renting_agreements/joint_tenancies

Advice on joint tenancies if you live in Scotland http://scotland.shelter.org.uk/get_advice/advice_topics/families_and_households/sharing_rented_accommodation/joint_tenancies

Advice on housing when a relationship breaks down http://m.england.shelter.org.uk/__data/assets/pdf_file/0020/23393/ShelterGuide_RelationshipBreakdown.pdf

If a relationship breaks down violently, one of these organisations might be able to help you www.womensaid.org.uk

www.mensadviceline.org.uk

Tenancy deposit schemes in England and Wales:Mydeposits http://www.mydeposits.co.uk

The Deposit Protection Service http://www.depositprotection.com

The Tenancy Deposit Scheme http://www.tds.gb.com

In Scotland:Mydeposits Scotland http://www.mydepositsscotland.co.uk

Safe Deposits Scotland http://www.safedepositsscotland.com

Useful links

Click here for contents 45

Chapter 3 - Finding a property

Letting Protection Service Scotland http://www.lettingprotectionscotland.com

In Northern Ireland:Mydeposits http://www.mydepositsni.co.uk

Letting Protection Service Northern Ireland www.lettingprotectionni.com

TDS Northern Ireland www.tdsnorthernireland.com

Chapter 5Residential Property Tribunal: who to appeal to if you live in England and think your rent is too high https://www.gov.uk/housing-tribunals

Shelter has a useful gas and fire safety checklist http://england.shelter.org.uk/__data/assets/pdf_file/0018/23364/Checklist_-_gas_and_fire_safety.pdf

Fire safety advice https://www.gov.uk/firekills

Useful moving home checklist http://www.bbc.co.uk/homes/property/moving_checklist.shtml

Shelter has a sample inventory form http://england.shelter.org.uk/get_advice/paying_for_a_home/tenancy_deposits/making_an_inventory

How to Rent: the checklist for renting in England https://www.gov.uk/government/publications/how-to-rent

Chapter 6Check your rights as a tenant https://www.gov.uk/private-renting

Government guide for people living in HMOs https://www.gov.uk/government/publications/licensing-of-houses-in-multiple-occupation-in-england-a-guide-for-tenants

Having trouble with anti-social behaviour? Find contact details for your local council

https://www.gov.uk/find-your-local-council and ask to speak to the anti-social behaviour co-ordinator

Shelter’s advice on repairs http://england.shelter.org.uk/get_advice/repairs_and_bad_conditions/disrepair_in_rented_accommodation/repairs_in_private_lets/reporting_repairs_to_a_landlord

If you want to apply for the Debt Arrangement Scheme in Scotland, you need to ask a money adviser to make an application on your behalf http://www.moneyadvicescotland.org.uk/find-adviser

Shelter’s advice on repossession by a landlord’s lender http://england.shelter.org.uk/get_advice/repossession/repossession_by_a_landlords_lender

If you need advice on rent arrears http://england.shelter.org.uk/get_advice/how_we_can_help/housing_advice_helpline

Chapter 7Find out how much notice your landlord must give you with Shelter’s Eviction Checker http://england.shelter.org.uk/get_advice/eviction/eviction_of_private_tenants/interactive_tools?a=179840

Shelter’s free advice helpline http://england.shelter.org.uk/get_advice/how_we_can_help/housing_advice_helpline

Click here for contents 46

Chapter 8 - Glossary and useful links

Change of address checklist

WHO TO INFORM OF CHANGE OF ADDRESS CONTACTED?Doctor

Electoral register

Bank or building society

Local council (council tax, housing benefit)

Utility providers (electricity, gas, water)

School and/or nursery

DVLA (driving licence)

TV licence (and cable or satellite TV services)

Phone and broadband

Dentist

Subscriptions (including magazines, Netflix)

Other financial services providers