the tax refund firm 2019 tax training manual · 8 | p a g e • consent to use form with signature...

TRANSCRIPT

1 | P a g e

The Tax Refund Firm 2019 Tax Training Manual

2 | P a g e

Table of Contents

The Company………………………. 3-4

Current Locations………………… 5-6

Tax Payer Process………………… 7-9

Earned Income Credit……………… 10-12

Tax Appointment Check List…………… 13-14

Tax Preparation Software Training………… 15-24

Tax Glossary………………………………. 25-37

Tax Forms…………………………… 37-42

Tax Schedules………..……………. 42-44

Tax Resolution Forms………………… 45-49

Phone Script………………………… 50-52

Addendum……………………………. 53-54

3 | P a g e

The Company

Welcome

The Tax Refund Firm welcomes you to the best tax preparation company in the industry. We

take pride in making sure our services are extraordinary. This website exists to provide our

clients with information concerning our firm’s unique, low-pressure approach to personal and

professional services.

About us

The Tax Refund Firm is a full-service tax preparation and tax resolution company. We are

headquartered in the Atlanta Metropolitan Area. We have locations in Atlanta, Decatur, GA,

Macon, GA, Augusta, GA, Memphis, TN, Clarksville, TN, Nashville, TN, Huntingdon, TN,

Dallas, TX, Baton Rouge, LA and Las Vegas, NV. Our tax professionals have over 150 years of

tax preparation experience.

The mission of the TRF is to provide clients with superior personalized tax solutions and other

insurance/financial services by implementing practical solutions for our clients’ diverse needs.

Our services consist of tax preparation, amendment preparation, tax resolutions, insurance, and

business/personal credit services.

Services

If you’re looking for a firm that will focus on your individual needs, and always treat you like a

client who matters, look no further. Our firm is large enough to offer a full range of professional

services, but small enough to give you the individual attention that you deserve.

We will thoroughly and conscientiously study your personal situation, and tailor our advice to

your specific needs.

Tax Preparation & Planning

Effective tax preparation and planning can help you to minimize your future tax liability. We can

help you proactively manage both your personal and your business tax issues, including

understanding how upcoming business opportunities impact your tax status and vice versa. Not

all tax planning opportunities are clear. By having us on your team, you are more likely to

4 | P a g e

benefit from those opportunities. We understand how the latest federal, state and local tax

legislation and other developments affect you and your business and we are constantly

identifying new ways to reduce federal, state or local tax liabilities.

Audits, Reviews, and Compilations

Our audit, review and compilation capabilities are a core part of our services. We tailor each

process to the unique needs of your business. We deliver financial statements and reports that are

clear, concise and acceptable to all outside parties and that can provide information and insight to

help you run your business more effectively. We will work closely with you and your key

employees to develop and execute a plan to complete this work by minimizing employee time

spent on the process and without disrupting operations.

Business Consulting

As a true business partner, we are available to help you deal with any business problem or

opportunity. We stand ready to engage in business consulting projects to help you make the right

decisions for the future of your business. Whether you face questions related to expanding,

selling or restructuring your business, we have the necessary business acumen and analytical

capabilities to help you make the right decisions.

IRS Representation

An IRS audit can be an intimidating and complex process. If you or your business face an IRS

audit, we can bring to bear years of experience in dealing with tax matters and IRS audit

procedures to ensure that you are properly represented when dealing with the IRS and other tax

authorities.

Insurance

We provide quality insurance products for Life, Health, and Annuities. We deliver more options,

innovations and value to today’s consumer seeking a strategic response to the evolving world of

financial protection for themselves and their families. In addition, we offer a unique array of

Concierge Medical and Life insurance. These products reduce health insurance premiums for

individuals and employer groups.

5 | P a g e

Current Locations (As of October 1, 2018)

Atlanta Main Location

4153-C Flat Shoals Parkway320F

Decatur, GA 30034

Phone: (404) 382-7922

Atlanta

384 Northyards Blvd Bldg. 10

Atlanta, GA 30313

Phone (800) 686-2360

Augusta

2601 Deans Bridge Rd Suite D

Augusta, GA 30906

Phone: (706) 530-5380

Dallas Main Location

3195 Great Trinity Forest Way Suite C-3

Plaza Now

Dallas, TX 75216

(469) 458-7371

Dallas

1100 E. Pleasant Run Rd

#135

DeSoto, Texas 75115

Phone: (469) 458-7371

Macon

2324 Pio Nona Ave Suite A

Macon, GA 31206

Phone: (478) 239-3849

Memphis

3417 Summer Ave 38122

Memphis, TN 38122

Phone (901) 410-5153

Huntingdon, TN

107 Church Street

6 | P a g e

Huntingdon, TN 38344

Phone (731) 630-4245

Nashville, TN

624-A Jefferson St

Nashville, TN 37208

Phone (800) 686-2360

Clarksville, TN

1860 Wilma Rudolph Blvd Suite 119

Clarksville, TN 37040

Phone (800) 686-2360

7 | P a g e

The Tax Preparer Process

Tax Refund Firm Tax Preparers can make people feel welcomed and comfortable while engaging

in conversation that consist of probing questions to gather the information required to prepare a

complete and accurate tax return. They are encouraged to work with people from diverse cultural

and socio-economic backgrounds.

Tax Preparers are responsible for the following:

Register for your PTIN

Anyone who prepares or assists in preparing federal tax returns for compensation must have a

valid 2018-2019 Preparer Tax Identification Number before preparing returns.

Don't have a PTIN and need to obtain one?

Most first-time PTIN applicants can obtain a PTIN online in about 15 minutes. You can access the

application at https://rpr.irs.gov. Failure to have a current PTIN could result in the imposition of

Internal Revenue Code section 6695 penalties, injunction, and/or disciplinary action by the IRS

Office of Professional Responsibility.

Training and Education

Tax Preparers are encouraged to attend on classroom trainings and attend online webinars and

complete at least 25 tax scenarios for practice. This resource guide will serve as a foundation of

information for a successful tax season!

As a Tax Refund Firm Tax Preparer, compliance documents are vital to complete a thorough,

probing interview of the client to ensure all relevant information is available and

accurate. Documents obtained should be filed and given to the Agency Owner for secure storing

up to 3 years. Below is a list of

Compliance Documents:

• Copy of Taxpayer Driver’s License

• Copy of Taxpayer Social Security Card

• Social Security Card for each Dependent

• Copy of Income Documents I.e. W-2 Form, 1099, Schedule C Declaration, Household

Help Declaration

• Copy of any other documents used to file taxes i.e. Mortgage Interest Statement, Childcare

Expense Statement, Student Loan Interest, Tuition Fees

• Tax Refund Firm Application with Signature

8 | P a g e

• Consent to Use Form with Signature

• E-File Authorization with Signature

• Consent to Disclose Taxpayer Information with Signature

• Check Release Form (if needed)

Client Experience

Whether our clients come to our office, tax stations, or mobile locations the experience should be

positive, professional, and personable. Always remember to greet the client and make them feel

welcomed.

Next, organize their compliance documents, get their consent, and provide them the client

questionnaire to complete. While preparing their federal and state tax return, ensure the clients gets

every credit to which they are entitled, and identify what deposit method will best suit the

client. Please email or print a copy of the clients filed tax return upon submittal. Clients should

always receive a copy for their records.

Tax Preparation Training

1. The three main reasons why your client is getting a refund are: dependents, withholdings,

and the American Opportunity Credit. Please see EIC Cheat Sheet for questions to ask if the

income is below $16,000 or above $16,000.

2. The magic number $16,000 is important if your client has dependents and would like to

receive the maximum amount for the Earned Income Tax Credit.

3. If your client does not have any dependents, the goal is to reduce their taxable income to

zero, so they don’t owe taxes.

4. If your client only has self-employment income the magic number is $10,000.

5. The key reasons why your client’s tax refund may be lower than last year are: income

changed, dependents age changed, withholding amounts is different, school status changed, or

their filing status changed.

6. The difference between a credit and deduction are credits increase your refund amount or

offset if you owe taxes; deductions reduce your annual income and lower the tax bracket you

are in.

7. Once you log into the Tax Refund Firm Software and complete an estimate, it’s important

that you can break down the summary sheet. Note* the top portion is subtraction and the

bottom portion are addition.

8. To help your clients, avoid self-employment taxes, they should establish an EIN for their

business and report their income on a W-2. If they complete household work; they can also

report their income on the household help declaration.

9 | P a g e

Tax Refund Firm Software

Our goal, unlike the competition is to get our client the maximum refund amount possible. Most

over the counter tax preparation software comes in different levels: basic, deluxe, and premier.

Our premier software, and trained tax preparers use customized worksheets that help increase your

tax refund or help decrease your tax debt. For agents the software is user friendly and allows

everything to be virtually completed for your client in less than 20 minutes.

Once you entered the client’s information in the tax return, to navigate through the software

remember to click on the client’s name, which is located at the right hand upper corner of the

screen. This allows you access to the worksheets without returning to the estimator.

The purpose of the estimator is to populate the worksheets needed to file the tax return. You can

always reference the estimator if you receive any errors while submitting the tax return.

Once you calculate the worksheets, anything in red means there are errors and you cannot move

on until they are corrected. Rejection Codes appear once the tax return has been filed to the IRS.

They also appear in red and inform you of what to correct before submitting the tax return again.

Important Tax Topics

Please provide the cell phone number and carrier to the filed tax return. This will keep them

informed about their tax return and any other marketing information from Tax Refund Firm or

TRF Services

To help avoid self-employment taxes, please assist your client in applying for their EIN. Please

visit www.irs.gov and complete the questionnaire. Note* it takes 2 weeks for the EIN to be

recognized by the IRS. Please set up EIN number prior to submitting the client’s tax

return. November of the upcoming filing season is a great time to start.

In some cases, clients W-2 forms may not be accessible. Please visit Tax Refund Firm and click

on the link “W-2 Look Up” so that you can find the information to submit on the W-2 worksheet.

If your client is filing with a pay stub instead of a W-2, please remember to list the gross income

and federal withholdings in the YTD (year to date) column.

We Change Lifestyles!

During Tax Season, our clients are in search of knowledgeable and confident tax preparers who

can either increase their refunds or reduce their tax debt and accurately complete their tax return.

Typically, our clients use refunds to buy things, eliminate debt, and invest in their future.

10 | P a g e

As the experienced TRF Services Agent, you have been provided all the tools, training, and

resources to identify your clients’ needs and inform them of how our services will benefit them.

Our goal is to make financial education trendy while making multi-streams of income from our

products and services. The more we know the more people we can help. Remember, the 3 Vs:

Visual, Verbal, and Vocal.

The key to a successful sale is to recognize who our clients are and how they can benefit from our

software and services.

Earned Income Credit The Earned Income Tax Credit (EITC) is one of the most significant tax credits available in the

entire IRS tax code. It is also simultaneously one of the most complicated and popular tax credits

as well. So, I thought I should provide a long overdue basic overview of what the Earned Income

Credit is, including qualifications, qualified children rules, maximum amount, income limits,

income tables, calculators, and more.

What is the Earned Income Tax Credit?

Let’s start with a basic description of the Earned Income Tax Credit, which is also commonly

referred to as the EITC, Earned Income Credit, and EIC. The EITC is a significant tax credit for

lower and lower-middle income taxpayers that rewards earned income, particularly for those

with children. It was first enacted under the Ford administration in 1975 and was built with the

dual purpose of incentivizing the earning of income and reducing poverty. Its popularity and

impact has led to bi-partisan political support and expansion several times since it was created,

making it one of the largest social welfare programs in the United States today.

The Earned Income Tax Credit is a refundable tax credit, which means that it not only can be

subtracted from taxes owed but can be refunded to the taxpayer if taxes are not owed.

How Much is the Earned Income Credit?

The EITC can be worth as much as $6,318 for the 2017 tax year and $6,444 for the 2018 tax

year. However, the credit amount varies significantly depending on tax filing status, number of

qualifying children, and income earned. It is phased in and then phased out at certain income

thresholds.

Earned Income Tax Credit Qualifications

There are several qualifications that must be met for a taxpayer to be eligible for the Earned

Income Tax Credit.

1. You must first have taxable “earned income”. Taxable earned income includes any of the

following:

▪ Wages, salaries, tips, and other taxable employee pay

▪ Union strike benefits

11 | P a g e

▪ Long-term disability benefits received prior to minimum retirement age

▪ Net earnings from self-employment if:

▪ You own or operate a business or a farm or

▪ You are a minister or member of a religious order (special rules apply)

▪ You are a statutory employee and have income. (statutory employees are contractors and will

have a box on their W2 designating them as ‘statutory’)

▪ Pay received for work while an inmate in a penal institution

▪ Interest and dividends

▪ Retirement income

▪ Social security

▪ Unemployment benefits

▪ Alimony

▪ Child support

2. You, your spouse, and any qualifying child must have an eligible Social Security # that is

valid for employment.

3. You can be any filing status except “married filing separately”.

4. You have qualified children, OR

▪ You (and your spouse if you file a joint return) meet all the EITC basic rules AND

▪ You (and your spouse if you file a joint return) cannot be claimed as a dependent or qualifying

child on anyone else’s return, AND

▪ You (or your spouse if you file a joint return) are between 25 and 65 years old at the end of the

tax year, usually Dec. 31.

5. Your income falls within the eligible income range (highlighted below).

6. Your tax year investment income must be $3,450 or less for the year.

7. Must not file Form 2555, Foreign Earned Income or Form 2555-EZ, Foreign Earned Income

Exclusion. In other words, you must have lived in the U.S. for more than half of the year.

Earned Income Credit Qualifying Children

While it is possible to qualify for the Earned Income Credit without children, the amount of the

credit increases with each qualified child. Qualified children must meet each of the eligibility

tests:

Relationship Test:

▪ Your son, daughter, adopted child, stepchild, foster child or a descendant of any of them such as

your grandchild

▪ Brother, sister, half-brother, half-sister, step brother, step sister or a descendant of any of them

such as a niece or nephew

Age Test:

12 | P a g e

▪ At the end of the filing year, your child was younger than you (or your spouse if you file a joint

return) and younger than 19

▪ At the end of the filing year, your child was younger than you (or your spouse if you file a joint

return) younger than 24 and a full-time student

▪ At the end of the filing year, your child was any age and permanently and totally disabled

Residency Test:

Child must live with you (or your spouse if you file a joint return) in the United States for more

than half of the year

Joint Return:

The child cannot file a joint return for the tax year unless the child and the child’s spouse did not

have a separate filing requirement and filed the joint return only to claim a refund.

Tiebreaker Rules:

Note that only one person can claim a specific qualified child (i.e. in cases of divorce). There are

special “tiebreaker rules“.

Earned Income Credit Table for 2018 Income Limits & Maximum Amounts

And here is the Earned Income Tax Credit table for the 2018 tax year:

Filing Status

No

Qualifying

Children

1

Qualifying

Child

2

Qualifying

Children

3+

Qualifying

Children

Single, Head of Household, Widow(er) Threshold

Phaseout:

$8,510 $18,700 $18,700 $18,700

Single, Head of Household, Widow(er)

Completed Phaseout:

$15,310 $40,402 $45,898 $49,298

Married Filing Jointly Threshold Phaseout: $14,200 $24,400 $24,400 $24,400

Married Filing Jointly Completed Phaseout: $21,000 $46,102 $51,598 $54,998

The EITC maximum credit amounts for 2018 are:

▪ $6,444 with three or more qualifying children

▪ $5,728 with two qualifying children

▪ $3,468 with one qualifying child

▪ $520 with no qualifying children

Can you claim both the EITC and Child Tax Credit in the Same Year?

13 | P a g e

Although I have not personally done this, it is my understanding that you can claim both the

Earned Income Credit and Child Tax Credit within the same year if you meet all of the

qualifications for each. In other words, they are not mutually exclusive credits.

Additional Child tax credit to $2,000 per qualifying child. e maximum amount refundable may

not exceed $1,400 per qualifying child up to 2 children

Tax Appointment Checklist

o Personal information -

• Last year’s income tax if you are a new client

• Name, address, Social Security number and Date of Birth for yourself,

spouse and dependents

• Dependent Provider, Name, Address, Tax ID and S.S.N.

• Banking information if Direct Deposit Required

o Income Data Required -

• Wages and/or Unemployment

• Interest and/or Dividend Income

• State/Local income tax refunded

• Social Assistance Income

• Pension/Annuity/Stock or Bond Sales

• Contract/Partnership/Trust/Estate Income

• Gambling/Lottery Winnings and Losses/Prizes/Bonus

• Alimony Income

• Rental Income

• Self-Employment/Tips

• Foreign Income

14 | P a g e

o Expense Data Required -

• Dependent Care Costs

• Education/Tuition Costs/Materials Purchased

• Medical/Dental

• Mortgage/Home Equity Loan Interest/Mortgage Insurance

• Employment Related Expenses

• Gambling/Lottery Expenses

• Tax Return Preparation Expenses

• Investment Expenses

• Real Estate Taxes

• Estimated Tax Payments to Federal and State Government and Dates Paid

• Home Property Taxes

• Charitable Contributions Cash/Non-Cash

• Purchase qualifying for Residential Energy Credit

• IRA Contributions/Retirement Contributions

• Home Purchase/Moving Expenses

15 | P a g e

Tax Software Training

Go to www.taxrefundfirm.com, click on Services, Drop down to Tax

Professional 1. Username: taxrefundfirm password: Taxrefund1$$

HOW TO PREPARE A TAX RETURN

Click on Start New Return on the top left side

STEP 1

1. Enter First Name

2. Enter Last Name

3. Enter Social Security Number

4. Select Enter

STEP 2 THE ESTIMATOR PAGE

1. A box will appear that says Family Info, this box will help you to determine the client’s

filing status. Answer all the questions in the box and select next to continue to the next

page. Once all the questions have been answered select finish.

2. The next page that will appear is the Estimator page. Enter the client’s birthday for

number 1. If the questions in this section do not apply to the client skip the questions.

3. Number 2 enter the number of dependents, if the client does not have dependents leave

this section blank.

4. Number 3 enter the number of dependents that qualify for the Child Tax Credit (CTC).

5. Number 4 enter the number of dependents that qualify for Earned Income Credit (EIC).

16 | P a g e

6. Number 5 enter the information for the Child Care Credit. If the client is not claiming the

Child Care Credit leave this section blank.

7. Number 6a enter the wages from the W2 (box 1 on W2) and enter the federal taxes

withheld on the W2 (box 2 on W2). If the client has more than one W2 select +Add

More. If the client has Household Help (Schedule H) income, select +Add More and

enter the total amount of Household Help. If the client has Household Help income check

the box next to the question that says, “Check box if any income above is from household

help performed”.

8. Number 6b is only used if the client and their spouse are filing together. If the spouse has

a W2 and or Household Help, follow the same steps that were used for question 6a. If the

client is not filing with their spouse leave this section blank.

9. Number 7 is only used if the client reported Interest and Dividends on a 1099.

10. Number 8a is the Schedule C section and is for client that have their earned or loss

money from their own businesses. If the client earned money enter the amount (i.e.

5000.00). If the taxpayer loss money from their business enter the amount with a negative

sign (i.e. -5000.00). Leave this section blank if the client does not need to do a Schedule

C. Repeat these steps for 8b if the client’s spouse has a Schedule C if not leave blank.

11. Number 9 is only used if the client has reported IRA or Pension Distribution on a 1099-

R. If the client has a 1099 R enter the amounts in this section if not leave blank.

12. Number 10 is only used for clients that received unemployment compensation. If the

client has received unemployment enter the amounts in this section if not leave blank.

17 | P a g e

13. Number 11 is only used for clients that receive social security income. Enter the social

security amount that is listed on the client’s SSA-1099. If the client did not receive social

security leave this section blank.

14. Number 12 is only used for clients that have won the lottery. If the client received money

from the lottery and has a W2-G enter the amount and the tax withholdings, if not leave

this section blank.

15. Number 13 is only used for other winnings such as Gambling Awards, and Cancellation

of Debt enter those amounts here if not leave blank.

16. Number 14 is only used for Educators Expenses this expense is typically claimed by but

not limited to teachers and paraprofessionals. If the client has paid out of pocket for

educational expenses enter the amount up to 250.00 if not leave blank.

17. Number 15 is only used for Student Loan Interest Expense. If the client has their student

loan interest expense form, then enter the amount here if not leave blank.

18. Number 16 is only used for IRA Contributions enter the total amount here for both the

taxpayer and their spouse if not leave blank.

19. Number 17 is only used if the client Paid Alimony, enter the amount here if not leave

blank.

20. Number 18 is only for Tuition and Fee Deductions up to 4000, enter the amount here if

not leave blank.

21. Number 19 is the Schedule A/Itemized Deduction section. This section will be used to

itemize things such as medical and dental expenses, mileage, charity contributions, etc.

To use this section, check the forced itemize box and the federal worksheets to fill in this

section will appear once you get to the section that contains the federal worksheets.

18 | P a g e

22. Number 20 is the the Student section which is also known as the American Opportunity

Credit. This is also the section for the Lifetime Learning Qualified Expenses. To receive

the full 1000.00 credit the student will have had to pay 4000.00 in out of pocket

expenses. If the student did not spend 4000.00 out of pocket the 1000.00 credit will be

prorated based on what was paid out of pocket. For line A enter the amount of out of

pocket expenses. On line B enter the amount of Lifetime Learning expenses. The federal

worksheets to fill in this section will appear once you get to the section that contains the

federal worksheets.

23. Number 21 is the Retirement Savings Credit and this line is used to put the 401k

contributions from the client’s W2 and the amount will be in box 12 with the code D or

E.

24. Number 22 is only used for the Repayment of First-Time Homebuyer Credit. List the

amount here.

25. Number 23 is used to for other Federal Tax Payments.

26. Number 24 is the State Income Tax section in the drop-down box select the client’s

Resident State. If the client has worked in another state use the next drop-down box to

select the Non-Resident State and click the first arrow. The non-resident state should

appear in the box on the right. To remove a state from this box, click on the state and

click the bottom arrow.

27. The next section is the Non-Estimated Schedules and Forms. This section contains a list

of different forms that may be needed for filing the client’s 1099 Miscellaneous Income,

Health Saving Account, and or Capital Gains and Losses. These are just examples of

19 | P a g e

some of the items/forms that are listed in this section. There is a total of 32 forms listed in

this section.

28. Once the Estimator page is completed click next. Remember to only use the lines that

pertain to your client. Several of the fields on the Estimator page will be left blank.

STEP 3 THE ESTIMATED SUMMARY PAGE

The Estimated Summary Page is the next page, and, on this page, there will be a tax summary.

The tax summary explains the Federal 1040 Tax Return taxable income amounts. There will be a

refund amount listed at the bottom of the page. Do not quote this amount it will change as you

complete the tax return. Click Next to get to the next page.

STEP 4 THE CONSENT AGREEMENT

The Consent Agreement will be the next page. Check the box next to I have received a signed

copy of the Consent to Use form. Click Next to get to the next page.

STEP 5 THE ESTIMATE OPTIONS PAGE

The Estimate Options page will be the next page. Use the drop box to select the refund method.

If the client is filing a state tax return check the box next to Does, the taxpayer want a State RAC

for this return. At the bottom of this page there is a refund amount. Do not quote this amount

until you have completed the tax return. Click Next to go to the next page.

20 | P a g e

STEP 6 THE WORKSHEETS PAGE

The Worksheets page is where all the Federal Worksheets will be listed. A Federal Worksheet is

a form that must be filled out with specific information that will help determine the client’s

refund amount. This page is populated by the information that was given on the Estimator Page.

If you listed amounts on the Estimator Page such as Household Help Income, a Schedule C,

American Opportunity Credit, Unemployment, or anything that requires a Federal Worksheet

you will find the worksheet on this page.

Next to the Federal Worksheet it will either say Edit or Add. Click on Edit or Add to complete

the Federal Worksheet then click save at the bottom once all the information has been entered.

Once the worksheets are complete a green check mark will appear next to it after it has been

saved. The worksheet for the Filing Status will already have a green check mark by it. Move

onto the next worksheets and complete them.

STATE WORKSHEETS

(LOCATED ON THE BOTTOM OF THE WORKSHEETS PAGE)

At the bottom of this page there will be a section to complete the State Worksheets. For Georgia

there will only be two worksheets for this section. Typically, nothing is filled out on these two

worksheets. If the the client has made Contributions (the different types of contributions will be

listed in the GA-500 worksheet) and or if they have Adjustments to Income (for the state) list the

amounts on the GA-500 worksheet page and click save. If the client qualifies for a Driver

Education Credit complete the second worksheet in this section the IND-CR - Individual Credit

worksheet and click save. If a different state has been selected there may be more worksheets to

complete and certain fields will have to be filled in depending on the state.

21 | P a g e

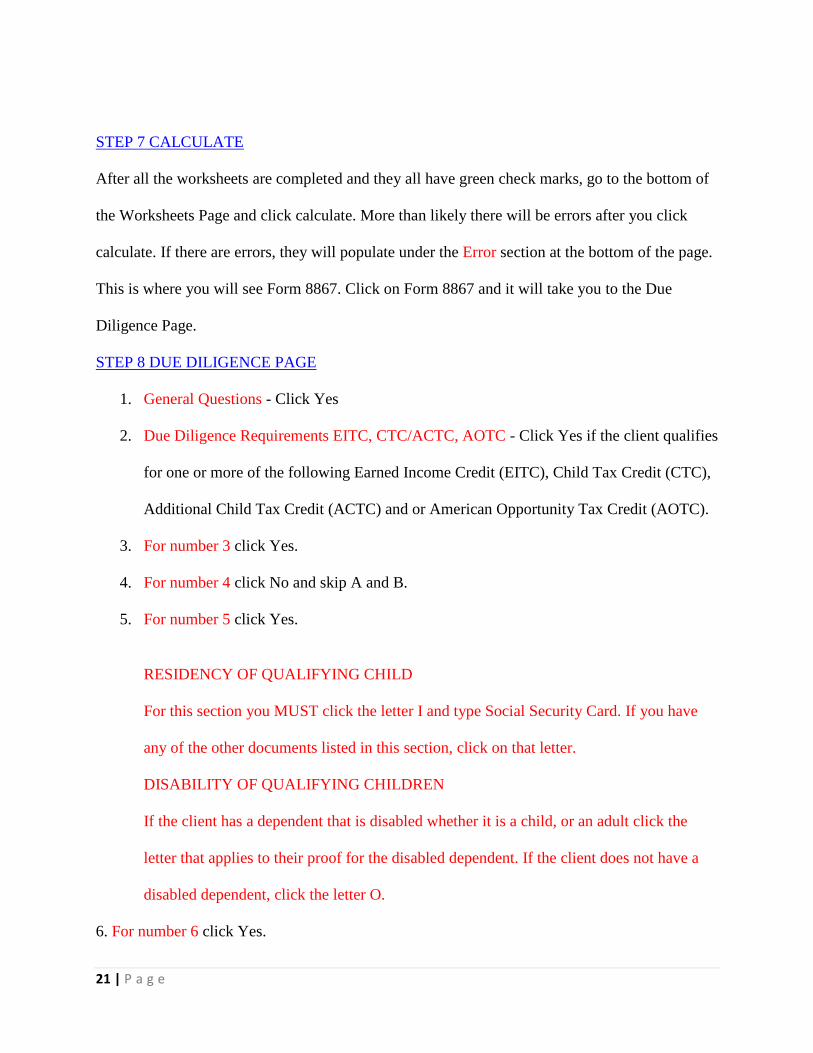

STEP 7 CALCULATE

After all the worksheets are completed and they all have green check marks, go to the bottom of

the Worksheets Page and click calculate. More than likely there will be errors after you click

calculate. If there are errors, they will populate under the Error section at the bottom of the page.

This is where you will see Form 8867. Click on Form 8867 and it will take you to the Due

Diligence Page.

STEP 8 DUE DILIGENCE PAGE

1. General Questions - Click Yes

2. Due Diligence Requirements EITC, CTC/ACTC, AOTC - Click Yes if the client qualifies

for one or more of the following Earned Income Credit (EITC), Child Tax Credit (CTC),

Additional Child Tax Credit (ACTC) and or American Opportunity Tax Credit (AOTC).

3. For number 3 click Yes.

4. For number 4 click No and skip A and B.

5. For number 5 click Yes.

RESIDENCY OF QUALIFYING CHILD

For this section you MUST click the letter I and type Social Security Card. If you have

any of the other documents listed in this section, click on that letter.

DISABILITY OF QUALIFYING CHILDREN

If the client has a dependent that is disabled whether it is a child, or an adult click the

letter that applies to their proof for the disabled dependent. If the client does not have a

disabled dependent, click the letter O.

6. For number 6 click Yes.

22 | P a g e

7. For number 7 click Yes. For 7a skip it or click N/A.

8. For number 8 click Yes if the client has a Schedule C and click No if they do not. If the client

does have a Schedule C click the letter J and type Schedule C Declaration. If the client has any of

the other letters as proof, click on those letters as well if not leave them blank.

DUE DILIGENCE QUESTIONS FOR RETURNS CLAIMING EIC

If the client does not have a dependent that qualifies for EIC skip this section and leave it blank.

9. For 9a click yes if the client has a dependent that qualifies for EIC.

10. For 9b click yes if the client has a dependent that qualifies for EIC

11. For 9c click yes if the client this a dependent that qualifies for EIC.

DUE DILIGENCE QUESTIONS FOR RETURNS CLAIMING CTC

If the client does not have a dependent that qualifies for CTC skip this section and leave it blank.

12. For 10a click yes if the client has a dependent that qualifies for CTC.

13. For 10b click yes if the client has a dependent that qualifies for CTC.

14. For 10c click yes if the client has a dependent that qualifies for CTC

DUE DILIGENCE QUESTIONS FOR RETURNS CLAIMING AOTC

If the client does not have qualify for AOTC or has a dependent that qualifies for AOTC click

NO or skip this section and leave it blank.

15. For number 11 if the client is a qualifying student and or if their dependent is a qualifying

student click yes. Then click the letter that applies to the proof/document that proves the client or

their dependent was or is a student.

16. For number 12 click Yes. Then click Save. Next click Recalculate.

If all the errors have been corrected, then the system will recalculate. If the errors are not all

corrected click on the error and correct it then recalculate until all the errors are gone.

23 | P a g e

STEP 9 SUMMARY PAGE

After all the errors have been corrected and recalculated the Summary Page will appear. The

Summary Page will have the client’s federal refund amount before the fee has been taken out.

Under the Georgia Resident Tax Return section, you will find the state refund amount at the

bottom of the page if a refund is owed. Some people will end up owing the state and there will be

a negative amount listed. Click Next.

Form 8879 will appear click Next.

Next will be the Consent Agreement page click both boxes and then click Next.

The Refund Options page will be next. If you have not picked the client’s refund method use the

drop-down box to select their refund method. If the client is filing a state return, click State RAC

box (the 1st box). If the client is applying for an Advance the only refund method that they can

use is the Check method. If they would like to apply for the Advance check the 3rd box that says

check to apply for Advance with subsequent RT (RT check or New Fast Money Prepaid Card).

This page will break down the total fees that will automatically be taken out of their refund.

Under Totals you will find the refund amount next to Estimated Net Amount You Receive. This

is the amount you can quote to your client. Click Next.

STEP 10 BANK INFORMATION

Fill in the Daytime Phone Number. Next move down to the Bank Account & Identification

Information and use the drop-down box to answer the four questions as they apply. The next

section is the Taxpayer Identification section. Use the drop-down box to select the correct

24 | P a g e

identification type, then type in the client’s I.D./license number, type the Issue Date, type the

Place Issued, and the Expiration Date.

STEP 11 PREPARATION FEE COLLECTION PAGE

Check the box next to I have received a signed copy of the Bank Documents. Then click the back

button and then click next again and you will be taken back to the Preparation Fee Collection

Page click Next.

STEP 12 TAX SUBMISSION PAGE

Under submit click the box next to Federal Return and make sure the box next to Georgia

Resident State is checked. Click submit only if the tax return is completely ready to be submitted

to the IRS. If you need to go back and make any changes or have any doubts or questions Do

Not click submit. Once the tax return has been submitted it cannot be changed unless it is

rejected by the IRS. If the tax return is rejected simply click on the reject message and correct the

error and resend submit it. Tax returns will reject for something as minor as a typo in a birthday,

a typo in a name, or it can reject for things such as the dependent or tax payer has already been

claimed by another person. If a dependent has already been claimed that person will have to be

removed off the tax return. This will change the amount of the refund more than likely the refund

amount will be lowered.

25 | P a g e

Tax Glossary

A

Ability to Pay

The concept that taxpayers should have a tax liability consistent with their income level.

Above-the-Line Deduction

Also called an adjustment to income. A type of deduction that you may take without

having to itemize.

Abusive Tax Scheme

An illegal series of transactions designed to hide taxable income from the IRS.

Adjusted Basis

The original value of a piece of property plus the value of improvements and minus

depreciation. The adjusted basis is used to figure your gain or loss on a sale.

Adjusted Gross Income (AGI)

Your gross income reduced by adjustments to income before exemptions and deductions

are applied.

Adjustment to Income

Also called an above-the-line deduction. A type of deduction that you may take without

having to itemize.

Alimony

Regular payments made to an ex-spouse or to a legally separated spouse. Alimony is

considered income for the payee and is tax deductible for the payer.

Allowances

A number on your Form W-4 used by your employer to calculate how much income tax

to withhold from your pay. The greater the number of allowances, the less income tax

will be withheld.

Alternative Minimum Tax (AMT)

26 | P a g e

A special tax system which was originally intended to prevent wealthy taxpayers from

taking advantage of so many tax breaks that they end up paying little or no taxes. The

AMT affects more and more middle-class taxpayers every year.

Amendment / Amended Return

A corrected tax return (using Form 1040X) filed to revise a previous year's tax return.

Amount Due

Your total tax bill. The amount of money you owe in taxes.

Annuity

An annual payment, such as from a retirement plan.

Appeal

To request the review of an IRS decision or adjustment.

Archer Medical Savings Account (MSA)

A tax-deductible savings account containing funds for medical expenses not covered by

insurance. Interest and qualified withdrawals are generally nontaxable.

Audit

An IRS review, or examination, of a tax return. Many audits are random, but returns may

also be deliberately chosen for audit based on several red flags.

B

Basis

The amount a piece of property is worth when you first acquire it.

Blind

For tax purposes, a person is considered blind if they cannot see better than 20/200 with

their best eye using contacts or glasses, or if they have a field of vision which is 20

degrees or less.

C

Canceled Debt

Forgiven debt on a mortgage or other loan. Canceled debt is generally considered taxable

income.

Capital Gain

Profit from the sale or trade of an investment property such as stock or real estate.

Casualty Loss

A deduction taken for property damage suffered during a disaster or other such event.

Child Support

Payments made to an ex-spouse or legally separated spouse for the care of a child. Child

support payments are generally neither taxable nor deductible.

COBRA

The part of the Consolidated Omnibus Budget Reconciliation Act of 1985 that, in many

cases, provides continuation of employer sponsored health insurance for workers who

have lost their jobs.

27 | P a g e

Combat Pay

Income earned while serving in a federally declared combat zone. Combat pay is

generally nontaxable.

Community Property

A law in certain states pertaining to married couples which stipulates that income and

property are owned equally by both spouses.

Constructive Receipt

The legal concept that income is taxed at the time it is received, whether you have cashed

the check or withdrawn the funds from your account.

Coverdell Education Savings Account (ESA)

A tax-deductible savings account containing funds for educational expenses. Interest and

qualified withdrawals are generally nontaxable.

Credit

A dollar-for-dollar reduction of your taxes owed. Some credits are refundable.

D

Decedent

An IRS term for a person who has died.

Deduction

An amount subtracted from your taxable income for certain expenses.

Deficiency

The amount of taxes owed after paying too little, assessed during an audit.

Dependency Exemption

An exemption claimed for a dependent.

Dependent

A child or relative whom you support and who qualifies you to take an exemption.

Depreciation

A deduction taken for the business use of certain items which lose value over time, such

as office furniture.

Direct Deposit

When a tax refund or other payment is sent electronically to your bank account.

Direct Tax

A tax paid directly to the federal government, or to state or local governments, such as

income tax and property tax.

Direct Transfer

Moving funds from one Individual Retirement Account to another.

Disaster Loss

A tax deduction taken by taxpayers who suffered the loss or damage of property during a

federally declared disaster.

Dividend

A stock distribution given to stockholders in the form of cash, property, services, stock

rights, or more stock.

28 | P a g e

E

Earned Income

Money or other compensation given to you for working, whether you receive a paycheck,

or you are self-employed and pay yourself.

Earned Income Credit (EIC)

A refundable tax credit targeted at workers who make low to moderate incomes. Learn

more about the earned income credit.

Efile

To electronically file a tax return. To file your taxes online.

EIN

Employer Identification Number, used by employees to identify their employers to the

IRS.

Elderly

For tax purposes, a person is considered elderly if they are age 65 or older on the last day

of the tax year.

Electronic Filing

Filing your tax return online, also known as efiling or e-filing. This is generally more

secure, more accurate, and faster than filing your taxes by paper through the mail.

Employment Tax

Also called a payroll tax. A tax paid by employers for FICA and FUTA.

Entity

A person or group of people that pays taxes. Types of tax entities include individuals,

businesses, estates, trusts, and charitable organizations.

Estate

A tax entity that receives and reports a person's income and pays taxes after that person's

death.

Estate Tax

A tax, targeted at the wealthy, on the total value of an estate if it exceeds a certain

amount.

Estimated Tax

Quarterly down-payments toward your annual tax bill, required if you expect to make

more than a certain amount of income for the year ($1,000 in 2010) and if your income

taxes are not covered by withholding.

Examination

Another term for audit.

Excise Tax

A special tax on using or selling certain products or services. One example of excise

taxes is luxury taxes .

Exemption

A type of deduction claimed for yourself, your spouse (if filing jointly), and each your

dependents. Personal and dependency exemptions are worth $3,650 each in 2010.

Extension

29 | P a g e

A tax extension, obtained by filing or efiling Form 4868, will delay your filing deadline

by 3 months. Note that this extends your time to file, but not your time to pay, and

interest and penalties may apply to any late tax payments.

F

Fair Market Value

The price for which you could sell a piece of property on the open market under current

economic conditions.

Fellowship

A grant generally received for educational or scholarly purposes. Funds are nontaxable

when used for qualified expenses.

FICA Tax

A tax on employment required by the Federal Insurance Contributions Act. This payroll

tax is used to fund Social Security and Medicare.

Filing Status

A category of taxpayer. Each taxpayer must select a filing status on their tax return:

Single, Head of Household, Married Filing Jointly, Married Filing Separately, or

Qualifying Widow(er). Filing status determines things such as your overall tax rate and

your eligibility and income limits for various credits and deductions.

Flat Tax

A tax based on the same percentage of income for all taxpayers, regardless of income

level.

Flexible Spending Account (FSA)

Also called a reimbursement account. A special employer sponsored account which is

generally used for approved medical expenses. Your contributions are taken directly from

your paycheck before taxes are applied and are sometimes matched by an employer

dollar for dollar. Funds contributed to some FSA's may become unavailable at the end of

the year.

Foreclosure

The legal process by which a lender takes possession of a home when the homeowner has

defaulted on the mortgage.

Fringe Benefit

A fringe benefit is compensation given to you by your employer in addition to your

regular pay. The value of any fringe benefit is generally taxable. Examples of fringe

benefits include: employee discounts, stock options, services, transportation, access to

facilities, group term life insurance, expense reimbursement, etc.

FUTA Tax

A tax on employment required by the Federal Unemployment Tax Act. This payroll tax is

used to fund state unemployment insurance programs and state job agencies.

30 | P a g e

G

Generation Skipping Transfer (GST) Tax

Sometimes called the "Grandparent Tax", the GST tax is a special tax on the transfer of

an estate to your grandchildren, to another relative more than one generation removed

from you, or to a non-relative who is more than 37 and 1/2 years younger than you. The

GST tax is paid in addition to any applicable gift or estate taxes.

Gift Tax

A special tax paid by the giver of a gift (of money or property) worth more than a certain

amount ($13,000 in 2010). Some transfers of money are exempted from the gift tax, such

a gift to a spouse or a gift used to pay medical or educational expenses.

Gross Income

The total amount of income you must report on your tax return. Your income before

applying adjustments, exemptions, credits, and deductions.

H

Head of Household

A filing status claimed by taxpayers who are single but have qualifying dependents.

Hobby

An activity pursued not primarily for financial gain. You may generally deduct hobby

expenses up to the amount of hobby income earned.

Home Office

An area of your home used primarily or exclusively for business purposes, for which you

may be able to take certain deductions.

Household Employee

A person you pay to cook, clean, care for a dependent, etc. in your home. If you pay a

household employee over a certain amount, you will be responsible for paying Social

Security and Medicare taxes, and possibly Federal Unemployment taxes.

I

Income Taxes

Taxes paid by individuals and businesses based on earned and unearned income.

Independent Contractor

A self-employed person who performs services for others in exchange for money or other

compensation.

Indirect Tax

A tax which is not paid directly, but which is paid through a cost increase, such as sales

tax.

Inflation

A decrease in the value of money and credit as consumer prices increase.

Innocent Spouse Relief

A petition filed by a divorced taxpayer (who formerly filed jointly) to be relieved of

responsibility for their ex-spouse's unpaid tax bill.

31 | P a g e

Interest

Money gained from investments, such as bank accounts, bonds, or trusts. Interest

is unearned income.

Internal Revenue Service (IRS)

A bureau of the Department of the Treasury, the IRS is the government agency

responsible for collecting taxes and for enforcing the tax code.

International Tax Returns

Find out how international tax returns are filed in foreign or international tax districts.

Investment Income

Money or other compensation received from profitable investments, generally in the form

of interest or dividends.

Individual Retirement Arrangement (IRA)

Also called an Individual Retirement Account or a Traditional IRA. A special account

designed to encourage saving money for retirement. Contributions up to a certain amount

are generally tax deductible and any interest the account earns is not taxed until you

withdraw funds. Withdrawals of funds before you reach a certain age (59 1/2 in 2010) are

usually penalized. In many cases, it is possible to convert a Traditional IRA to a Roth

IRA.

Itemized Deduction

A deduction for a specific expense that may be claimed if the total amount of all itemized

deductions is greater than the standard deduction.

ITIN

Individual Taxpayer Identification Number. A number used to identify foreign taxpayers

to the IRS. Only taxpayers who do not have a Social Security Number must obtain an

ITIN.

J

"Jock Tax"

A state or local tax targeted at traveling professionals who work in multiple states, such

as athletes.

K

Keogh Plan

A retirement plan for self-employed taxpayers. Contributions are generally tax

deductible.

"Kiddie Tax"

32 | P a g e

The tax paid by parents, at their tax rate, on the unearned income of a child which is in

excess of a certain amount.

L

Levy

To impose a tax. To tax someone, or to put a tax on something.

Like-Kind Exchange

A nontaxable or tax-deferred trade of similar properties.

Local Tax

A tax charged by a local government, such as a city or county.

Luxury Tax

An indirect tax, targeted at the wealthy, attached to certain expensive, nonessential goods

or services such as sports cars or jewelry.

M

Marginal Tax Rate

The tax rate that applies to the last dollar of income earned.

Married Filing Jointly

A filing status claimed by married couples who wish to combine income and file a single

tax return together in order to take advantage of various tax benefits.

Married Filing Separately

A filing status claimed by married couples who do not wish to file a joint return and

agree to report their income separately.

Mortgage

A loan made to purchase property, generally real estate. The borrower pledges the

property to the lender as collateral to guarantee repayment of the loan.

Medical Savings Account (MSA)

See Archer Medical Savings Account.

Multiple Support Agreement

When two or more taxpayers who provide financial support for a particular person agree

to officially designate that person as the dependent of one of the supporting taxpayers, to

allow that taxpayer to claim dependency exemptions and various credits and deductions.

N

"Nanny Tax"

33 | P a g e

Social Security and Medicare taxes paid for a household employee such as a child care

provider.

Nonresident

A person who did not live in a particular state but worked or did business there and so

must file a state income tax return.

Nontaxable

This describes income which is not subject to taxation.

Not Collectible

A label given by the IRS to taxpayers who are unable to pay their tax debt.

O

P

Part-Year Resident

A person who lived in a particular state for only part of the year but must file a state

income tax return there.

Payroll Tax

See Employment Tax.

Penalty

Charges added to your tax bill for late filing and late payment. The IRS may also charge

interest for late tax payments.

Pension

A retirement plan that pays an annuity. Also see Individual Retirement Arrangement.

Personal Exemption

An exemption claimed for yourself and, if married filing jointly, for your spouse.

PIN

Personal Identification Number. A five-digit number used to securely "sign" an

electronically submitted, or efiled, tax return.

Points

Additional charges paid during the financing or refinancing of a mortgage. A point is

equivalent to 1% of the mortgage amount. Payments of points are generally tax

deductible.

Principal Residence

Also called a Primary Residence. The place where a taxpayer lives for the greater part of

the year.

Progressive Tax

A tax based on a percentage of income. The higher your income, the larger a percentage

you pay. Our current federal income tax system.

Property Tax

A tax paid for valuable property such as real estate and vehicles.

Proportional Tax

Another term for Flat Tax.

34 | P a g e

Q

Qualifying Widow(er)

A filing status claimed by a taxpayer whose spouse has died during the

tax year. This status entitles the taxpayer to the tax rates and benefits of

a joint return. If a widow(er) has dependents and does not remarry, that

person may be allowed to claim Qualifying Widow(er) status for 2 more

years.

R

Recapture

The repayment of a tax credit if requirements were not met by the

taxpayer since claiming the credit.

Refund

The amount of money you receive back from the IRS when you have

paid more taxes (usually through paycheck withholding) than you owe.

Refundable

A credit which will paid to you as a refund if you owe no tax.

Report

To give information to the IRS, generally by filling out a form.

Resident Alien

A citizen of a foreign country who lives and works legally in the U.S.A.

but is not a United States citizen. Resident aliens are subject to U.S. tax

laws.

Roth IRA

A special kind of Individual Retirement Account named after Senator

William Roth of Delaware. Contributions are not tax deductible, but

interest and qualified withdrawals (after reaching retirement age) are

completely tax-free.

S

Sales Tax

A tax on retail products, goods, and services. It is based on a certain

percentage (generally set by the state) of the price.

Scholarship

Money awarded for educational purposes. Scholarship funds used to

pay for qualified expenses such as tuition, required fees, books, and

supplies are generally considered nontaxable income.

Schedule C

Use this schedule to report income or loss from a business you operated

or a profession you practiced as a sole proprietor. Also, to file 1099-

MISC.

Self-Employment Tax

35 | P a g e

The tax paid by self-employed taxpayers to support Social Security and

Medicare. The self-employment tax rate in 2010 is 15.3% of self-

employment profit.

SEP (Simplified Employee Pension)

A retirement plan designed for self-employed taxpayers. Contributions

are generally tax deductible.

Severance Pay

Also called Separation Pay. Money and/or benefits given to a laid-off or

retiring employee upon termination of employment. Severance is

generally considered taxable income.

Short Sale (Real Estate)

When a home is sold for an amount that falls short of the amount still

owed on the home's mortgage.

Short Sale (Stocks)

When someone borrows shares of stock and sells them in the hopes that

the stock's price will fall before the original loan must be repaid.

SIMPLE (Savings Incentive Match Plan for Employees)

An employer-sponsored retirement plan designed for employees of

small businesses (but also available to self-employed taxpayers).

Contributions are generally tax deductible and up to 3% of contribution

amounts are generally matched by the employer.

"Sin Tax"

An excise tax attached to certain goods, collected at the point of sale,

intended to discourage their use (such as cigarettes and alcohol).

Single

A filing status claimed by those who are unmarried, divorced, or legally

separated and who do not qualify for Head of Household status.

Standard Deduction

A specific amount that differs by filing status. You may deduct this

amount from your taxable income if you do not itemize deductions.

Standard Mileage Rate

A specific amount per mile driven for business, charitable, or medical

purposes, which may be deducted from your taxable income.

T

Tariff

A tax on imports.

Tax Avoidance

Using legal tax planning strategies to reduce your tax bill.

Tax Base

All resources available to the government for taxation. All the nation's

taxable income added together.

Tax Bracket

A range of incomes that is taxed at a specified tax rate. Also, the

bracket into which the last dollar of one's income falls.

Tax Break

36 | P a g e

A general term for exemptions, credits, deductions, or any legal way to

reduce your taxes.

Tax Burden

The total amount of taxes owed by the American people, or by a

segment of the population.

Tax Code

The entire body of tax laws, regulations, and procedures.

Tax Cut

A reduction of tax rates.

Tax-Deferred

When taxes levied now are owed at a later time, such as interest

on IRA contributions.

Tax Evasion

Illegally hiding income from the IRS. Deliberately underpaying taxes or

using an abusive tax scheme.

Tax Liability

The total amount of taxes you owe.

Tax Rate

The percentage of income that is owed as tax.

Tax Shelter

An investment, business, or other activity designed primarily

to avoid or evade taxes.

Tax Shift

When a tax is levied on one group of people but is in practice paid by

another group. Tax shift can also refer to the process of lowering some

taxes and making up the revenue by raising or implementing other

taxes.

Tax Year

The 12-month period covered by a tax return. Returns for a specific Tax

Year are usually filed in the subsequent year. For example, Tax Year

2010 Tax Returns are due to the IRS in 2011.

Taxable Income

Your Adjusted Gross Income reduced by all applicable exemptions,

credits, and deductions. The amount of income that is taxed.

Taxpayer Advocate

The Taxpayer Advocate Service is an independent organization within

the IRS in charge of resolving problems that may arise between a

taxpayer and the IRS. Taxpayer advocates provide free and confidential

advice, guidance, and representation. The IRS calls the Advocate

Service "your voice inside the IRS". There is at least one taxpayer

advocate stationed in every state, as well as in Washington, D.C. and

Puerto Rico.

Trust

A type of tax entity that manages a person's assets during their life or

after their death. A trust is a separate entity from an individual and is

managed by an appointed trustee.

37 | P a g e

U

Unearned Income

Income which was not earned by working, such as investment

income or gifts.

Use Tax

A special tax levied by a state on goods used in that state but purchased

in another state.

V

Value-Added Tax (VAT)

A tax, popular in Europe, levied on a product at each stage of

production, depending on the overall value added to the product at each

stage. The consumer pays the accumulated taxes at the point of sale. For

example, taxes may be attached to a car when the body is assembled,

when the engine is added, and when the car is painted--and the buyer

will pay all these taxes to the car dealer, who passes them on to the

government.

Voluntary Compliance

The concept that our tax system relies on taxpayers to pay the correct

amount of taxes on time of their own free will.

W

"Wealth Tax"

Another name for the Alternative Minimum Tax.

Withholding

Money held back from your paycheck and used to pay taxes. This

amount is applied to your annual tax liability.

Withholding Allowance

An amount chosen on your Form W-4 which tells your employer how

much money to withhold from your paycheck for taxes.

X

Y

Z

Tax Forms

Form 1040

You might think of this as the grandfather of tax forms. Many of the other forms and

schedules are tied to it. For example, the amount in Box 1 of Form W-2 is reported on Form

38 | P a g e

1040, line 7. Form 1040 is a summary of your income, adjustments, deductions, taxes and credits

for your tax year, which, for most individuals, is the calendar year. Relevant supporting forms

and schedules must be filed with Form 1040.

There are simplified versions of Form 1040: Form 1040A and Form 1040EZ. These forms can be

used instead of Form 1040 when certain conditions apply. You can use Form 1040EZ if you

meet all eleven conditions in the checklist on page 7 of the 1040EZ Instructions. Similarly, you

can use Form 1040A if you meet all six conditions itemized on page 13 of the 1040A

Instructions.

Most tax-preparation software chooses the appropriate form for you automatically. For help

choosing the best tax service, see our Top Tax Software Review, plus check out our list of free

filing options.

Another 1040 version is Form 1040X, which you file when you need to amend a previously filed

return. This form cannot be e-filed and must be mailed with a copy of your 1040 return “As

Amended” and any schedules that changed, plus any new tax documents that show federal

withholding.

Form W-2

Employers use Form W-2 to report wages and salaries as well as income tax, social security, and

Medicare taxes withheld during the year. This information is reported to the IRS as well as the

employee. State and local income tax withholdings are also reported on Form W-2.

Other information commonly reported on Form W-2 includes voluntary contributions to a

retirement plan, the amount the employer paid for the employee’s health insurance, and

employer contributions to an employee’s HSA (Health Savings Account) – all of these are noted

in Box 12 with specific codes. Box 10 records employer-provided dependent care benefits. The

most common entry in Box 13 is a check in the box labeled “Retirement Plan.”

Note that this year, some 50 million W-2s have a verification code on them. This 16-digit

alphanumeric code needs to be reported when W-2s are entered in tax-preparation software.

They are found in Box 9 or elsewhere on the W-2. Not all W-2s have them.

Form W-2G

This form is used to report winnings over certain amounts from bingo, slot machines, keno,

poker tournaments, and racing, for example. These amounts are generally reported on Form

1040, line 21, Other Income.

39 | P a g e

Form W-4

Form W-4 is the Employee’s Withholding Allowance Certificate. When you first begin working

for an employer, you fill out a W-4 to let your employer know how much income tax to withhold

from your paycheck, based on your filing status and the number of qualified dependents. Later,

you can fill out a new W-4 to change the number of exemptions you claim for withholding

purposes.

Generally speaking, the fewer exemptions claimed, the more income tax is withheld. When you

file your tax return, you are reconciling the tax you owe on your income with the tax you have

pre-paid through withholding. Ordinarily, you want tax owed and tax withheld to be about the

same. If, during the year, you got married, divorced, had a baby, or had a child leave the nest,

you should file a new W-4 to reflect changes so that your employer will not withhold too much

or too little.

For more detail, check out our complete Form W-4 Guide.

Form 1099

There are many forms 1099, each with a following letter or letters indicating its particular

purpose. These forms typically report various kinds of income. The most common ones are

included below. For more detail, check out our complete Form 1099 Guide.

Form 1099-R

Records pension or annuity income or a distribution from an IRA. These amounts are reported on

Form 1040, lines 15a, b and 16a, b. Lines 15a and 16a are total amounts of the distributions, and

lines 15b and 16b are the taxable amounts. The amount on a and b may differ because of

employee contributions to retirement accounts during working years, or because of a basis (non-

deductible contributions) in an IRA.

Form 1099-INT

Reports interest earned from banks, credit unions or brokerage accounts. The interest may be

reported on Schedule B, and the total reported on Form 1040, line 8a (taxable interest) or 8b

(tax-exempt interest).

Form 1099-DIV

Reports dividends earned, most commonly from a brokerage account, but also from stock owned

directly in a company. Dividends are reported on Schedule B and the totals transferred to Form

1040, lines 9a (total dividends) and 9b (qualified dividends). Qualified dividends are stated

40 | P a g e

separately on the return because they are taxed at capital gains rates, which are lower than the tax

rates for ordinary income (such as wages).

Form 1099-B

Reports stock or bond transactions in a brokerage account. The transactions usually result in a

gain or loss, which is reported on Schedule D and the net loss or gain on Form 1040, line 13.

Form 1099-C

Reports canceled debt that may have to be reported as income on your tax return (on Form 1040,

line 21).

Form 1099-G

Reports certain government payments, such as a state tax refund or unemployment

compensation. These amounts are reported on Form 1040, lines 10 or 19.

Form 1099-MISC

Reports several kinds of miscellaneous income, the most frequent being Non-Employee

Compensation (box 7) for amounts greater than $600 paid to independent contractors. But it is

also used for reporting Rents and Royalties. Amounts from Box 7 are typically reported on

Schedule C, with the net profit reported on Form 1040, line 12. Rents and Royalties are reported

on Schedule E, and the net amount reported on Form 1040, line 17.

Form 1099-S

Reports proceeds from the sale or exchange of real estate. This is another scenario where capital

gains may be involved. Whether the gain is taxable depends on the circumstances pertinent to the

sale.

Form 1099-SSA

Reports income from social security. The total amount and taxable amount are reported on Form

1040, lines 20a and 20b, respectively. All social security may not be taxable. The taxable portion

depends upon other income items on the return.

Form 1098

Other forms may be related to adjustments or deductions on Form 1040 or Schedule A (Itemized

Deductions). The most common ones are included below. For more detail, check out our

complete Form 1098 Guide.

41 | P a g e

Form 1098

Form 1098, Mortgage Interest Statement, reports the amount of interest paid to the mortgage

holder on real estate (typically, the taxpayer’s home), as well as any points paid on the purchase

and mortgage insurance premiums. If your mortgage payments include property taxes, that

amount may be reported on Form 1098 as well. If it is not reported on the form itself, it may be

included in the transaction detail that frequently is received with Form 1098.

The amounts on Form 1098 are deductions that are reported on Schedule A, Itemized

Deductions, which you would want to do if your Itemized Deductions are greater than your

Standard Deduction (based on your filing status). Itemized Deductions higher than your Standard

Deduction means that your Taxable Income and Tax will be lower. Real estate taxes go on line 6

of Schedule A; home mortgage interest and points go on line 10; mortgage insurance premiums

go on line 13. Unless Congress decides otherwise, 2016 is the last year mortgage insurance

premiums may be deducted.

Form 1098-E

Form 1098-E, Student Loan Interest Statement, reports the amount of student loan interest the

recipient paid during the year. If the student has loans from more than one source, he or she may

receive a 1098-E from each one. Student loan interest paid is a downward adjustment to income

on Form 1040, line 33, which lowers adjusted gross income and taxable income up to a

maximum of $2,500 per return.

It is worth keeping in mind that the person legally responsible for the student debt may take the

student loan interest adjustment, not necessarily the person who pays it. So, if a student’s

benevolent uncle is paying the student loan and interest, but the student is legally responsible for

the debt, the student gets the adjustment to income, not the uncle.

Form 1098-T

Form 1098-T is a Tuition Statement. It records the amount of tuition and fees received or billed

by a qualifying educational institution, scholarships or grants the student received, whether the

student is at least a half-time student, and whether he or she is doing graduate work.

This form is essential in order to claim the various education benefits:

• Tuition and Fees adjustment which is recorded on Form 8917, with the allowed amount reported

on Form 1040, line 34 (2016 is the last year for this adjustment, unless Congress extends it).

• The American Opportunity Credit or Lifetime Learning Credit (figured on Form 8863, with the

allowed amount recorded on Form 1040, line 50 to offset tax liability). A portion of the American

Opportunity Credit may be refundable, which is entered on Form 1040, line 68. The American

Opportunity Credit is available for the first four years of undergraduate, post-secondary education

only. After that, the Lifetime Learning Credit must be used.

42 | P a g e

Forms 1095-A, B, and C

These three forms deal with health coverage.

Form 1095-B comes from the Health Coverage provider and indicates who in the household is

covered and for how long. Form 1095-C is issued by the employer, and indicates who is covered

by the employer’s health coverage and for how long. It also indicates if there was an offer of

coverage to the employee and may indicate the monthly cost. This information can be used to

determine if the employee (and, possibly, the family) may be exempted from coverage based on

the affordability of the offer as a percentage of the employee’s household income.

Form 1095-A is provided by the Insurance Marketplace if health insurance was purchased there.

It indicates who in the household was covered and for how long. It also indicates whether the

taxpayer qualified for the Premium Tax Credit and if a portion of that was paid in advance to

reduce the monthly health coverage premium due. If you receive a Form 1095-A, and the

advanced premium tax credit was paid, you must file a return to reconcile the Advanced

Premium Tax Credit, even if you would not otherwise have to file. The reconciliation is done

on Form 8962 and may result in having to repay a portion of the credit (which goes on Form

1040, line 46), or in an additional credit being paid to you (Form 1040, line 69).

Tax Schedules

Schedule A (Form 1040)

Information about Schedule A (Form 1040), Itemized Deductions, including recent updates,

related forms and instructions on how to file. Schedule A (Form 1040) is used by filers to report

itemized deductions.

Schedule B (Form 1040-A or 1040)

Information about Schedule B (Form 1040), Interest and Ordinary Dividends, including recent

updates, related forms and instructions on how to file. Form 1040 Schedule B is used by filers to

report interest and ordinary dividend income.

Schedule C (Form 1040)

Schedule C (Form 1040) is used to report income or loss from a business operated or a

profession practiced as a sole proprietor. Also, use Schedule C to report wages and expenses that

occurred as a statutory employee. Publication 525 discusses many kinds of income (money,

property, or services) and explains whether they are taxable or nontaxable. Use this schedule to

report income or loss from a business you operated or a profession you practiced as a sole

proprietor.

Schedule C-EZ (Form 1040)

43 | P a g e

Schedule C-EZ (Form 1040) is used instead of Schedule C by qualifying small businesses and

statutory employees with expenses of $5,000 or less. You can use this schedule if you operated a

business or practiced a profession as a sole proprietorship or qualified joint venture, or you were

a statutory employee and you have met all the requirements listed in Schedule C-EZ, Part I.

Schedule D (Form 1040)

Information about Schedule D (Form 1040), Capital Gains and Losses, including recent updates,

related forms and instructions on how to file. Schedule D (Form 1040) is used to report sales,

exchanges or certain involuntary conversions of capital assets, certain capital gain distributions,

and nonbusiness bad debts. The form includes the tax computation using maximum capital gain

rates.

Schedule E (Form 1040)

Information about Schedule E (Form 1040), Supplemental Income and Loss, including recent

updates, related forms and instructions on how to file. Schedule E (Form 1040) is used by filers

to report income from rental real estate, royalties, partnerships, S corporations, estates, trusts,

and residual interests in real estate mortgage investment conduits (REMICs).

Schedule EIC (Form 1040-A or 1040)

Information about Schedule EIC (Form 1040), Earned Income Credit, including recent updates,

related forms and instructions on how to file. Schedule EIC (form 1040) is used by filers who

claim the earned income credit to give the IRS information about the qualifying child.

Schedule F (Form 1040)

Information about Schedule F (Form 1040), Profit or Loss from Farming, including recent

updates, related forms and instructions on how to file. Use this schedule to report farm income

and expenses.

Schedule H (Form 1040)

Schedule H (Form 1040) is used by household employers to report household employment taxes.

Use this schedule to report household employment taxes if you paid cash wages to a household

employee and the wages were subject to social security, Medicare, or FUTA taxes, or if you

withheld federal income tax.

Schedule J (Form 1040)

Information about Schedule J (Form 1040), Income Averaging for Farmers and Fishermen,

including recent updates, related forms and instructions on how to file. Use this schedule to elect

to figure your income tax by averaging, over the previous 3 years (base years), all or part of your

taxable income from your trade or business of farming or fishing.

Schedule R (Form 1040-A or 1040)

44 | P a g e

Information about Schedule R (Form 1040), Credit for the Elderly or the Disabled, including

recent updates, related forms and instructions on how to file. Use this schedule to figure the

credit for the elderly or the disabled.

Schedule SE (Form 1040)

Information about Schedule SE (Form 1040), Self-Employment Tax, including recent updates,

related forms and instructions on how to file. Schedule SE (Form 1040) is used by self-employed

persons to figure the self-employment tax due on net earnings.

Schedule 8812 (Form 1040)

Information about Schedule 8812 (Form 1040), Child Tax Credit, including recent updates,

related forms and instructions on how to file. Schedule 8812 (Form 1040) is used by taxpayers to