the status of underground natural gas storage in europe

TRANSCRIPT

The Status of Underground Natural Gas Storage in Europe------------

and its Impact on Energy Security

Jean-Marc LeroyPresident, GSE CEO, Storengy

UNECE “Energy Week”, Committee on Sustainable Energ yGenève, 24 th November 2010

2

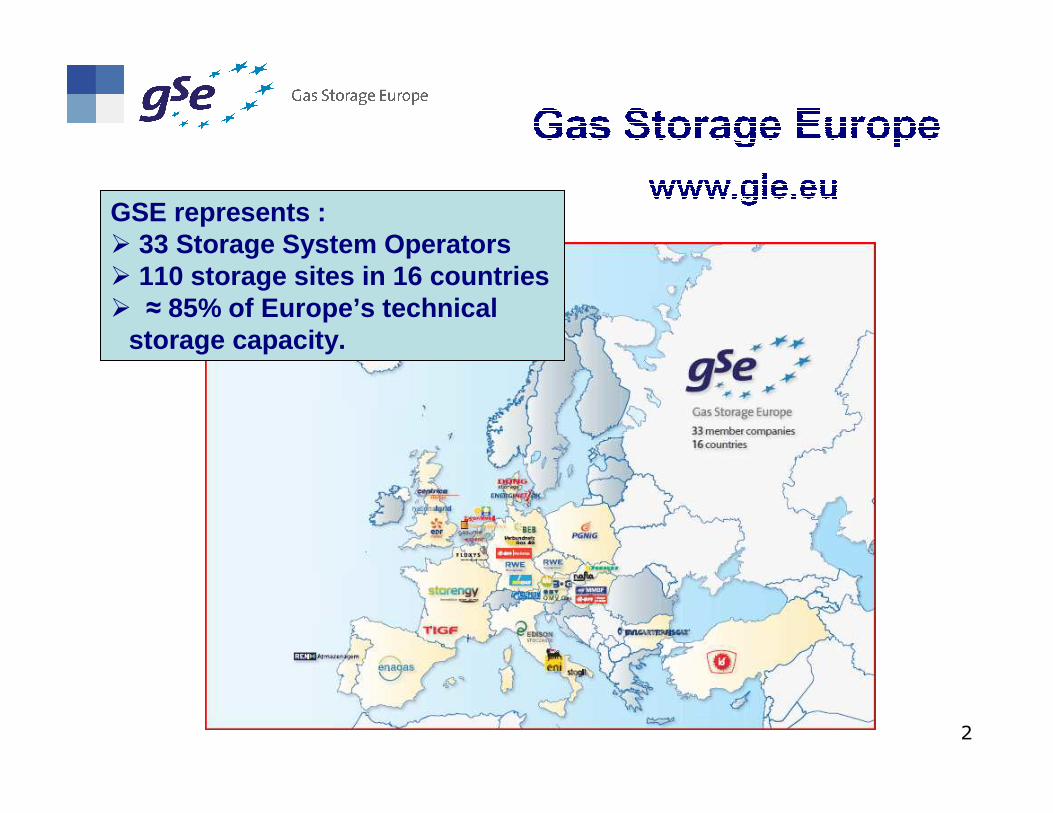

GSE represents : � 33 Storage System Operators� 110 storage sites in 16 countries � ≈ 85% of Europe’s technical

storage capacity.

3

Agenda

1. The key role of natural gas storage in security o f supply

2. Gas storage development perspectives

3. Risks and incentives

4. Conclusions

4

1. The key role of natural gas storage

in security of supply

5

Security of supply : Security of supply : a a «« highhigh --visibilityvisibility »» topictopic

January 2009

January 2010

October 2010

Reduction in gas supply in %, January 2009

Regulation onSecurity of Gas

Supply

6

Natural gas storage : Natural gas storage : A key role in the A key role in the European policyEuropean policy

sustainability

security of supply

The European energy policy

� Large proven reserves (conventional + unconventional )

� Large panel of routes and suppliers

� A storable energy

� A market-oriented storage industry which proved its efficiency through crisis

7

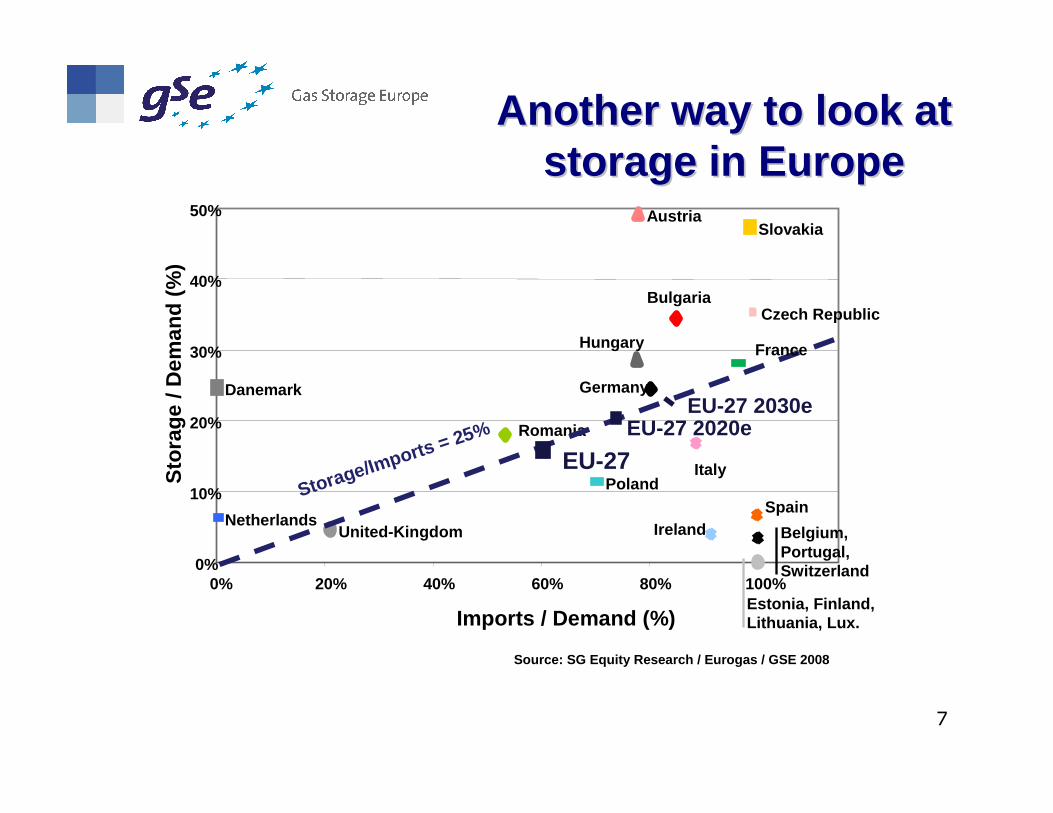

Austria

Belgium, Portugal,Switzerland

Bulgaria

Hungary

Ireland

Italy

Netherlands

Poland

Romania

Slovakia

Spain

United-Kingdom

Danemark

Czech Republic

Estonia, Finland,Lithuania, Lux.

0%

10%

20%

30%

40%

50%

0% 20% 40% 60% 80% 100%

Imports / Demand (%)

Sto

rage

/ D

eman

d (%

)

EU-27Storage/Imports = 25% EU-27 2020e

EU-27 2030eGermany

France

Source: SG Equity Research / Eurogas / GSE 2008

Another way to look at Another way to look at storage in Europestorage in Europe

8

2. Gas storage developmentperspectives

9

1. Need for security of supply � Decline of local production

� Increase of import contracts & remoteness of sourcing

=> two major driverstwo major drivers

Sou

rce

: Ced

igaz

200

5

10

2. Need for flexibility� Decline of local production

� estimated additional seasonal swing demand ≈ 14 Bcm in 2030

� Development of trading

� Exple : traded volumes on NCG

� Increase of CCGT

� Increase of wind power generation

� estimated additional peak swing demand ≈ 10 Bcm in 2020

=> two major driverstwo major drivers

Sou

rce

: E.O

N E

nerg

y T

radi

ng

11

19,6

12,3

14

1,6

2,3

2,8

3,7

5,04,3

4,1

1,0

0,7

2,7

0,4

Spain

France

Belgium

UK

Netherlands

Germany

Poland

Latvia

Italy

Denmark

Czech R.

Slovakia

Austria

Croatia

Romania

Bulgaria

0,2

Portugal

Source: GSE 2009, CEDIGAZ 2009, IGU 2009

4,2

3,1

14,3

P

P

P

P

p

Storage volumesStorage volumesin Europein Europe

–– current situation current situation ––Hungary

0,6

Europe storage facilities : working gas volume in bcm

Total around 80 bcm

1,6

Turkey

12

19,6

12,3

14

1,6

2,8

3,7

5,0

4,3

4,1

1,0

0,7

2,7

0,4

Spain

France

Belgium

UK

Netherlands

Germany

Poland

Latvia

Italy

Denmark

Czech R.

Slovakia

Austria

Croatia

Romania

Bulgaria

0,2

Portugal

Source: GSE 2009, CEDIGAZ 2009, IGU 2009

4,2

3,1

14,3

P

P

P

P

p

2,3

Storage Storage projectsprojectsin Europein Europe

Hungary

0,6around 70 bcm

0,2

Albania

3,2

0,1

2,4

0,1

Bosnia-H.

0,5

0,8

1,8

8,7

2,3

11

1

0,5

Lithuania4,5

1,7

2,2

5,8

Serbia

5,9

20

Pro

ject

in b

cm

Cu

rren

t in

bcm

12

1,6 1,5

Turkey

13

• A worldwide oversupply situation � Economic crisis => fall of the demand (2009 : -3% / -4%)

� New GNL capacities (+50% from 2009 to 2013)

� Rise of non conventional gas

• Impact on the flexibility market � Spot prices < Long term oil indexed prices

� Squeeze of the seasonal spread

=> ……but short term uncertaintiesbut short term uncertainties

13

14

3. Development :Risks & incentives

15

� Stability of the regulation Stability of the regulation : a necessity for attracting funding

Regulatory instabilityRegulatory instability

(three directives in ten years !)

several dozen billion EUR to be invested in the next 20 years

RISK

Incentives

16

GSE believes that :

- strategic storage is definitely damaging

- choice of access regime should be market-oriented

- negotiated TPA should be the preferred choice wherever market conditions allow : ⇒ best regime to facilitate investments⇒ best regime to foster commercial creativity and provide best response to the demand

Inappropriate regulatory frameworkInappropriate regulatory frameworkRISK

Incentives

17

4. Conclusion

18

� Transparency

� Market Orientation

� Dialogue

keywords

EuropeEurope ’’s etymology : s etymology : ““ the farthe far --seeing oneseeing one ””

www.gie.eu.www.gie.eu.