the state of the south dakota economy · 2018-11-29 · •sd economy slowing, but not everywhere...

TRANSCRIPT

The State of the South Dakota Economy

Ron Wirtz

Regional Outreach Director

Federal Reserve Bank of Minneapolis

minneapolisfed.org

Disclaimer

The views expressed here are the presenter's and not necessarily

those of the Federal Reserve Bank of Minneapolis or the

Federal Reserve System.

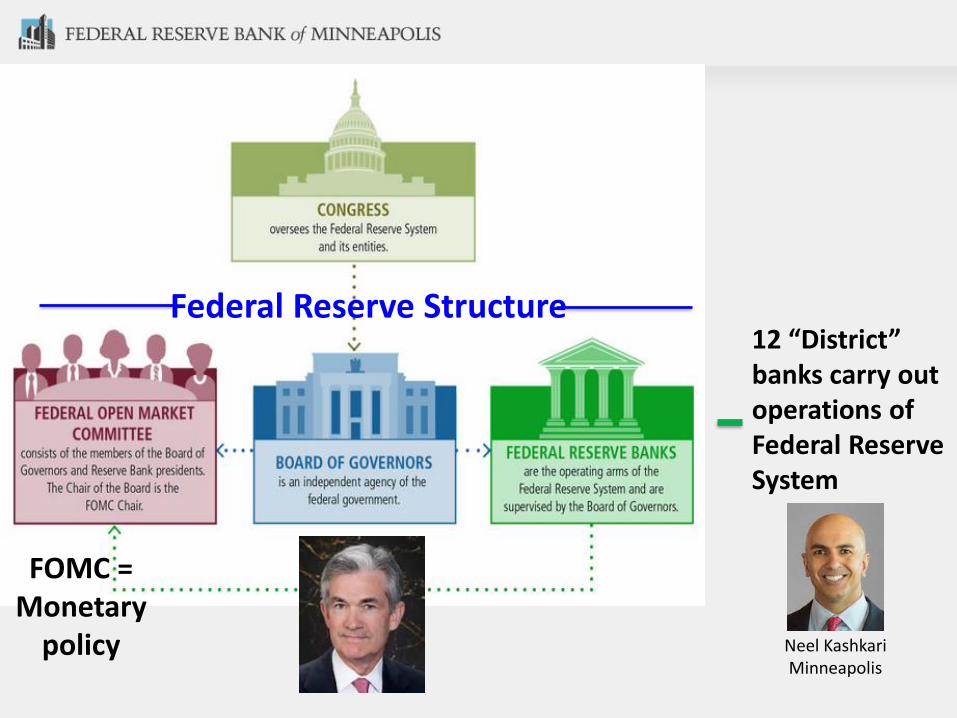

Part 1: The Federal Reserve System

• Central bank of the U.S.

• Established by act of Congress in 1913

What exactly is a central bank?

• Provides financial & banking services for country's government and commercial banking system, with the broad goals of:

– Stability and uniformity of money supply

– Safety and soundness of financial system

Main responsibilities of the Fed

➢Supervise and regulate banks• Mainly bank holding companies (who own lots of banks)

➢ JPMorgan, Wells Fargo, Goldman Sachs, Citigroup

➢Offer financial services• Manage (‘clear’) financial payments between parties• Lender of last resort

➢Set monetary policy • Most familiar tool is interest rates (via FOMC)• Monetary policy guided by “dual mandate”

1) stable prices2) maximum employment

The Federal Reserve System = distributed power

Federal Reserve Structure12 “District” banks carry out operations of Federal Reserve System

FOMC = Monetary

policy Neel KashkariMinneapolis

FOMC voting: Monetary policy in action

FOMC voting = 7 + 1 + 4

• 7 = Board of Governors (BOG)

• 1 = New York Fed president➢ Executes monetary policy in financial markets

• 4 = rotating votes of 11 other presidents• Neel Kashkari (Mpls): 2017 voter, again in 2020

Currently: 4 + 1 + 4 (three BOG vacancies)

Part 2: “The state of the South Dakota economy”

Implied question:

Is the state economy good or bad?

Answer: “Yes”

Lies, damned lies & statistics

“Now, keep in mind that these numbers are only as accurate as the fictitious data, ludicrous assumptions and wishful thinking they're based upon.”

Reprinted with permission from CartoonStock

My goal: Help inform your opinion of the South Dakota economy, via:

• a variety of performance metrics • tabulated over long(ish) timeframes• using different/peer comparisons

State comparisons• South Dakota• Minnesota• Montana• US average• What about North Dakota?

Metro comparisons• Rapid City• Sioux Falls• Peer metros

Today’s economic themes• SD economy slowing, but not everywhere

• Ag is dragging, not pulling, state economy

• Bi/tri-furcation of state economy

• Trajectory matters as much/more than current measures

• Tight labor means future growth depends on workforce, workforce, workforce

On to the charts!

Timeframe matters: Pre-recession GDPSouth Dakota on top of the pile

Annualized quarterly output, inflation adjusted

Source: Bureau of Economic Analysis

90

95

100

105

110

115

120

125

130

135

SouthDakota

UnitedStates

GDP index: 2005 Q2 = 100

Post-recession GDPSouth Dakota losing pace in recovery

Annualized quarterly output, inflation adjusted

Source: Bureau of Economic Analysis

90

95

100

105

110

115

120

125

United States

Minnesota

Montana

South Dakota

GDP index: 2009 Q2 = 100

12-month real GDP growthQ2 2017 to 2Q 2018

2.9%

2.1%

1.1%

0.8%

United States Montana Minnesota South Dakota

Source: Bureau of Economic Analysis

12-month GDP growth, by sector2017:Q2 to 2018:Q2

-10 -5 0 5 10 15

Finance and insurance

Agriculture and forestry

Accommodation and food services

Transportation and warehousing

Wholesale trade

Construction

Retail trade

Real estate and rental and leasing

Health care and social assistance

Other services (except government…

Professional, scientific, and technical…

Manufacturing

Information

Source: Bureau of Economic Analysis

South Dakota metros: Good/bad newsSF & RC similar to US, but below neighbors

Source: Bureau of Economic Analysis

90

100

110

120

130

140

150

160

Bismarck, ND

Billings, MT

Mankato, MN

US metro ave.

Rapid City, SD

Sioux Falls, SD

GDP index: 2009 output = 100

GDP: Metros vs. rest of state Opposite directions since 2015

90

95

100

105

110

115

120

2009 2011 2013 2015 2017

Rapid City

Sioux Falls

Rest of SD

GDP index: 2009 output = 100

Source: Dodge Analytics

South Dakota annual construction spending strong, but cooling in 2018*

$0

$1

$1

$2

$2

$3

$3

$4

2014 2015 2016 2017 2018*

Bill

ion

s

Residential

Nonresidential

Nonbuilding

*Projected annual figure based on the first eight months of 2018

Residential shifting toward more multi-familyAnnual permitted units

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Multi-family

Single-family

Source: U.S. Census

*Projected annual figure based on the first eight months of 2018

Housing & population growth: What’s the relationship?

0

50

100

150

200

250

300

350

Single-family

Multi-family

Population

H & P index: 1990 = 100

Source: U.S. Census*Projected annual figure based on the first eight months of 2018

Overview of the South Dakota banking

• 64 commercial banks chartered in South Dakota

– Down 25% from 10 years ago

– Less consolidation than nationwide (32% over same period)

• Profile of typical South Dakota bank hasn’t changed much over the last decade

– Ag production loans & loans secured by farmland make up 50% of the average SD bank

• SD banks among strongest performers in the 9th District

Median SD bank has the highest capital ratio among 9th District States

7%

8%

9%

10%

11%

12%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Tie

r 1

Cap

ital

/ R

isk

We

igh

ted

Ass

ets

SD MN MT ND

Capital ratios have increased nearly 100 bps since 2014

Earnings steadily improving at median SD bank

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Pre

tax

Ret

urn

on

Ave

rage

Ass

ets

SD MN MT ND

Pretax ROAA is back to pre-crisis levels at SD banks

Loan growth has stabilized over the past year at the median SD bank

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

Year

-ove

r-ye

ar c

han

ge in

net

loan

s

SD MN MT ND Loan growth remains at the lower end of the historical range

Continued weakness in ag is a primary concern to bank health

• Tariffs and ongoing trade disputes are likely to persist in the near future

• USDA forecast for net farm income in 2018 is the lowest in 15 years

• Debt repayment capacity is nearing its maximum level for the average farm

• Cropland values fell in SD from 2017q1 to 2018q1 (most recent data)

Farm revenue down, but still well above earlier levels in 2000s

Cash receipts from marketings

$0

$5

$10

$15

$20

$25

Bill

ion

s

Minnesota

South Dakota

Montana

Source: Bureau of Economic Analysis

Farm income has plungedTotal farm proprietors’ income

-$1

$0

$1

$2

$3

$4

$5

$6

Bill

ion

s

South Dakota

Montana

Minnesota

Source: Bureau of Economic Analysis

Production expenses swamping lower prices

Total farm production expenses

$0

$4

$8

$12

$16

$20

Bill

ion

s

Minnesota

South Dakota

Montana

Source: Bureau of Economic Analysis

Chapter 12 bankruptcies rising, still modest in South Dakota

(previous 12 months, from June of each year)

0

10

20

30

40

50

60

70

80

90

MTSDNDMNWI

Source: United States Courts

Source: Bureau of Labor Statistics

Unemployment: South Dakota well below traditional definition of “full” employment

0

2

4

6

8

10

12

2006 2008 2010 2012 2014 2016 2018

US

Montana

South Dakota

Minnesota

September of each year

Perc

ent

Metro unemployment: Ultra low

Source: Bureau of Labor Statistics

0

1

2

3

4

5

6

7

8

2006 2008 2010 2012 2014 2016 2018

Billings, MT

Rapid City, SD

Bismarck, ND

Sioux Falls, SD

Mankato, MN

September of each year

Perc

ent

Job growth South Dakota trailing nation; uptick?

Source: Bureau of Labor Statistics

90

95

100

105

110

115

2006 2008 2010 2012 2014 2016 2018

US

Minnesota

Montana

South Dakota

September of each year, seasonally unadjusted

Jobs index: 2006 = 100

SD metro jobs Sioux Falls out front, Rapid City accelerating

Source: Bureau of Labor Statistics

90

95

100

105

110

115

120

125

2006 2008 2010 2012 2014 2016 2018

Sioux Falls, SD

Mankato, MN

Bismarck, ND

Rapid City, SD

Billings, MT

Jobs index: 2006 = 100

September of each year, seasonally unadjusted

Job growth: Concentrated in Sioux Falls and Rapid City

90

95

100

105

110

115

120

125

Sioux Falls

Rapid City

Rest of SD

Jobs index: 2009 = 100

Source: Bureau of Labor Statistics

Source: Bureau of Labor Statistics

2009 2011 2013 2015 2017

Sioux Falls Rest of SD Rapid City

Goods jobs (16% of total)

90

95

100

105

110

115

120

125

2009 2011 2013 2015 2017

Services jobs(84% of total)

Jobs index: Goods vs. services

Rural service jobs are lagging

Hiring demandSouth Dakota job postings down, pivoting?

Online job postings tracked by state, September of each year

Source: South Dakota Dept. of Labor & Regulation

0

10,000

20,000

30,000

40,000

50,000

Total jobopenings

New jobpostings

Real median household incomeLower, but rising steadily in South Dakota

Source: U.S. Census

$30,000

$35,000

$40,000

$45,000

$50,000

$55,000

$60,000

$65,000

$70,000

2000 2002 2004 2006 2008 2010 2012 2014 2016

MN

US

SD

MT

Real median HH incomes flat in metros, and growing faster in rural counties

$35,000

$40,000

$45,000

$50,000

$55,000

$60,000

$65,000

$70,000

2000 2002 2004 2006 2008 2010 2012 2014 2016

Hughes

Minnehaha

Brookings

Pennington

Beadle

Source: U.S. Census

A quick recap

• GDP sluggish; tri/bi-furcation in the state• Slow ag economy• SD metros doing better, esp. Sioux Falls

• Very low unemployment • Solid hiring demand• Modest (but decelerating) job growth• Slow service job growth in rural SD

• Accelerating wage growth

So where is this all headed? And why?

Workforce, workforce, workforceJob growth and GDP/output are very connected to labor force growth, esp. when productivity is unchanged

Nonfarm labor

productivity(Annual percent change,

seasonally adjusted)

0

1

2

3

4

5

6

7

1990 1993 1996 1999 2002 2005 2008 2011 2014 2017

Labor force growth: Flat in SD

Source: Bureau of Labor Statistics, LAUS

Labor force: Those 16 and over that are working or looking for work

90

95

100

105

110

115

120

125

130

135

140

1990 1994 1998 2002 2006 2010 2014 2018

US

Montana

South Dakota

Minnesota

Labor force index 1990 = 100

Sioux Falls labor force sprinting ahead of peers

90

100

110

120

130

140

150

160

170

180

1901

99

01

99

21

99

41

99

61

99

82

00

02

00

22

00

42

00

62

00

82

01

02

01

22

01

42

01

62

01

8

Sioux Falls, SD

Rapid City, SD

Bismarck, ND

Mankato, MN

Billings, MT

Labor force index 1990 = 100

Labor force trends are tied to:

• Population growth • Demographics• Labor force participation

Population growthSouth Dakota lagging, but gap is holding

Source: U.S. Census, via FRED

95

100

105

110

115

120

125

130

135

140

1990 1994 1998 2002 2006 2010 2014 2018

Montana

US

Minnesota

South Dakota

Population index 1990 = 100

SD population projection remains pretty steady

Tho

usa

nd

s

0

200

400

600

800

1000

1200

1990 2000 2010 2020 2030 2040

Forecast

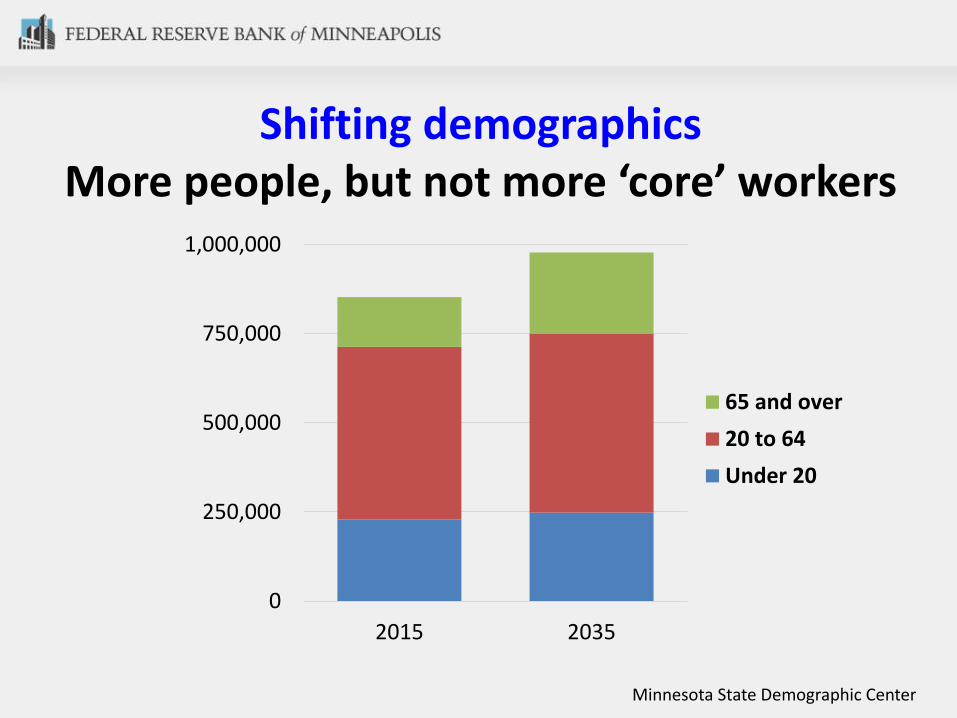

Shifting demographicsMore people, but not more ‘core’ workers

Minnesota State Demographic Center

0

250,000

500,000

750,000

1,000,000

2015 2035

65 and over

20 to 64

Under 20

Labor force participation ratesLong, slow decline; hitting plateau?

Source: Bureau of Labor Statistics

Labor force participation rate = 16 yrs old and over, employed or looking for work

55

60

65

70

75

80

Minnesota

South Dakota

U.S.

Montana

Pe

rce

nt

of

pe

op

le w

ork

ing,

16

ye

ars

or

old

er

Disability finally seeing change in trendSSI & SSDI enrollment trends

3%

4%

5%

6%

7%

8%

9%

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Disability enrollment as a share of labor force

SSI & SSDI enrollment

Source: Social Security Administration

Tight labor math: Short-term

• Hiring demand can change quickly (+/-)• Labor supply changes very slowly (+/-)

The only realistic short-term relief to tight labor is for hiring demand to decrease(aka economic slowdown/recession)

• Do nothing, and except slower growth• Increase productivity above trend (hard)• Subsidize fertility ($$) • Allow/encourage immigration/migration• Embrace approaches that convince more

people to work, esp. under-utilized groups• Labor force participation is critical

Tight labor math: Long-term

U6 unemployment A better picture of “full” labor slack

U-6 unemployment rate = Total unemployed, plus all marginally attached workers, plus total employed part time for economic reasons, as a percent of the civilian labor force plus all marginally attached workers, percent, 4-quarter moving average, not seasonally adjusted.

Source: Bureau of Labor Statistics

0

2

4

6

8

10

12

14

16

18

U.S.

Montana

South Dakota

Minnesota

Last measure: January 2018

Per

cen

t

Native American unemployment incredibly high

Source: Bureau of Labor Statistics

Pe

rce

nt,

20

16

0

5

10

15

20

25

30

Minnesota Montana NorthDakota

SouthDakota

Wisconsin

Statewide rate

AIAN

Why does high minority unemployment matter? They are the future workforce

SD worker GROWTH

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

White

Other minoritygroups

American Indian

South Dakota workers

50

100

150

200

250

300

Otherminoritygroups

AmericanIndian

White

Change since 20003 of 8 new workers is nonwhite, and the rate is accelerating

Source: U.S. Census

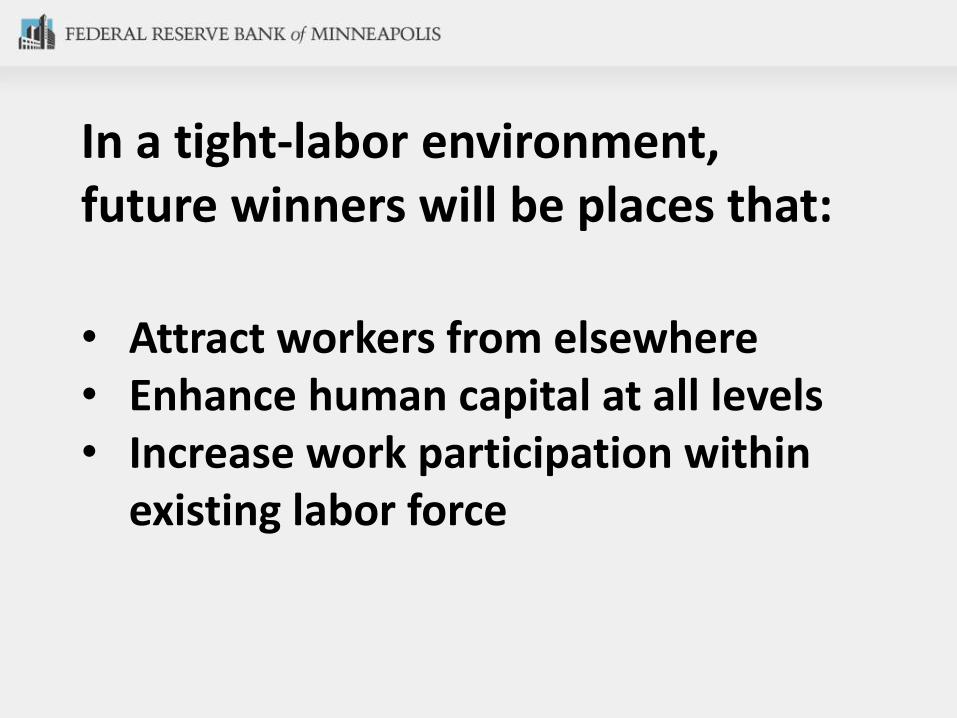

In a tight-labor environment, future winners will be places that:

• Attract workers from elsewhere• Enhance human capital at all levels• Increase work participation within

existing labor force

Increasing labor force/participation

• Wages, wages, wages• Jobs with career opportunities• Find ways to bring more workers into

the labor force➢ Available jobs – alone – not enough

for some people to work more➢ Housing, transportation, day care,

healthcare

Part 3: Tell the Fed …

What’s happening at your firm?

The Minneapolis Fed wants to know!

Step 1: Send text to 22333Step 2: Text the word: minneapolisfed

minneapolisfed.org

Thank you!

Questions for me?Comments for the Bank?

Twitter: @RonWirtz