the short-run underpricing of initial public offerings-jayantha c. kothalawala

DESCRIPTION

This Research paper covers the reasons and impacts on IPO underpricing in Sri Lankan context. Researched by, Jayantha C. Kothalawala. B.Sc(Mgt)Sp. Hons., ACA,ACMA,MBA-FIN (USJ)TRANSCRIPT

The short-run Underpricing of Initial Public Offerings (IPOs) in Sri Lankan context

Jayantha C. Kothalawala B.Sc (Mgt) Sp. Hons, ACA, ACMA,MBA-FIN USJ)

- 2 -

Abstract

This research is focused to investigate under pricing of IPOs in Sri Lanka and the reasons

and the relationship between Issue Size, Issue type, Investor sentiment and Issuer’s

Industry.

This research proposal comprise mainly with four chapters. Chapter one is the

Introduction. It will give an idea about the problem statement, problem justification,

research questions, and objectives of the study, significance of the study and scope of the

study. Chapter two is the Literature Review. Chapter three is the Research Methodology.

The forth chapter is the conclusion of the Research Proposal.

- 3 -

Table of Contents Chapter: One – Introduction………………………………………………………… 5-7

1.1 Introduction to the study........................................................................................ 5

1.2 Problem Statement………………………………………………………………. 6

1.3 Problem Justification……………………………………………………………. 6

1.4 Significance………………………………………………………………………. 6

1.5 Objectives………………………………………………………………………… 7

1.6 Scope of the study………………………………………………………………… 7

Chapter: Two – Literature Review……………………………………………………. 8-14 2.1 Short-run under pricing in emerging markets…………………………………… 9

2.2 Explanations for the short-run under pricing…………………………………… 10

2.2.1 Under Pricing and issue size……………………………………………… 10

2.2.2 Under pricing and investor sentiment…………………………………….. 10

2.2.3 Under pricing and privatization…………………………………………… 11

2.2.4 Under pricing and Industry……………………………………………….. 12

2.3 Conceptual Framework…………………………………………………………… 13

2.4 List of Hypothesis……………………………………………………………… 14

Chapter: Three - Research Methodology………………………………………… 15-

18

3.1 Research Strategy………………………………………………………………… 16

3.2 Population……………………………………………………………………….. 16

3.3 Sampling………………………………………………………………………… 17

3.4 Statistical Methodology…………………………………………………………. 19

3.5 Operationalization of Variables……………………………………………………19

Chapter: Four – Conclusion………………………………………………………………20 List of References………………………………………………………………………… 21

- 4 -

Chapter: One – Introduction

1.1 Introduction to the Study

Nowadays People are talking on the subject of Share Market and ‘Going Public’ by

private companies. Especially in Sri Lanka, the topic has been given a considerable value

as Sri Lankan Share Market is considered as one of the fastest growing share markets in

today’s world. As a result of this, so many private companies are planning and already

made the ground work for making their IPO for “Going Public”. Even though with this

booming trends almost all the big companies are planning to go public, the main thing

what they have to investigate is that why the Initial Public Offerings are underpriced in

significant percentage.

The under pricing of initial public offering (IPOs) is a well-documented experience in

stock markets around the world. The short-run or initial return, measured as the

difference between the closing price on the first day of trading and the offer price, has

been estimated at an average of 17 % in the United States and at 27% in international

markets (Loughran et al, 1994 (2008 update)).

Here I am going to study and investigate the initial under pricing of IPOs in the Colombo

Stock Exchange (CSE) of Sri Lanka from 1990 to 2009. The sample includes 107 IPOs

consisting for both conventional and privatization issues.

My study on IPO under pricing will be basically focusing the following major steps.

01. This study is focused to examine the distribution of first- day under pricing by

issue year and industry.

02. Performing a univariate analysis of under pricing by small vs. large issues,

investor sentiment, and conventional vs. privatization issues.

- 5 -

03. Examining the ability of the size of the offer, investor sentiment, privatization,

hot market conditions, underwriter size, and industries to singly and jointly

explain the cross – sectional variability of under pricing using regression models.

04. This study assesses the ability of investor sentiment and privatization to explain

the difference in under pricing between small and large issues.

1.2 Problem Statement What are the reasons for under pricing of IPOs? Why smaller issues are more

underpriced than large issues? Are investors sentiments positively related with the IPO

under pricing? Why Privatization IPOs are more underpriced than conventional IPOs?

1.3 Problem Justification

There are several reasons for IPO under pricing and we have to identify those main

reasons for achieving a conclusion

As with previous work in other markets, the univariate results show that small issues

are more under priced, investor sentiment is positively related with under pricing, and

privatization issues are more under priced. Issue size, a measured by gross proceeds

from the issue, is reliably negatively related with under pricing, and small issues are

more under priced than large issues by about 37 %. Investor sentiment, as substitute by

market returns in the three –month period prior to the first day of trading, is positively

related with under pricing. Privatization issues are more under priced than

conventional issues by a large 49 %.

- 6 -

1.4 Significance

This study will be really giving a value addition to the existing investors, potential

investors who are very keen on investing initial public offerings, Private companies

which are planning to “Going Public” in near future, Students who are really interesting

about the share market situations for their researches and projects etc.

1) Private Companies who planning to “Going Public”

By using this analysis, they will have a very clear idea about the reasons for

under pricing and all the related issues to be faced and how to overcome

these issues when they doing their IPO.

2) The Potential investors on IPOs

They will be able to analyze critically what is happening when investing in

IPOs and what is the relationship between the long term performance and

short term IPO under pricing. And also how it will affect to the share value of

what he has already purchased.

3) Students who are interested about share market phenomenon and the

behavior of the share market and the pricing of shares and valuations.

4) This study will help to General Public who are willing to obtain the general

knowledge about the share market of Sri Lanka.

5) In addition to the above mentioned factors, this study will also help

any new researchers that will be carrying out further research on the topic to

be used as a base paper in the future studies.

- 7 -

1.5 Objectives

2. To find out the under pricing percentage of Initial Public Offerings in Sri Lanka.

3. To find out the relationship between small issues and large issues in relation to

IPO under pricing.

4. To investigate the relationship between Privatization issues and conventional

issues relating to IPO under pricing in Sri Lankan context.

5. To identify the relationship between investor sentiment (emotion) and IPO

under pricing in Sri Lankan context.

1.6 Scope of the Study

This study investigates underpricing of IPOs in Sri Lanka. The study basically focus on

the reasons for IPO underpricing and the relationship with various phenomenon which

are directly and indirectly having positive and negative relationships with the

underpricing of IPOs. In addition to that, the study is focusing on the previous studies

have been carried out on the topic and the validity of those studies when comes to Sri

Lankan context.

Chapter: Two – Literature Review

Stock trading in Sri Lanka began in 1896. The Sri Lankan stock market, in its present

form, was established in 1984 with the formation of the Colombo Stock Exchange (CSE).

As of the end of 2008, the CSE had 235 listed companies, and a total market

capitalization of the 489 billion rupees ($4.3 billion). During its 24 year history

from 1985- 2008, the stock market produced a historical average annual return

(excluding dividends) of 18.4 %, and an equity risk premium 3.6 % in local currency

terms. The stock market was liberalized for foreign investors in June 1990. The capital

gains tax was abolished in 1992, and there is no tax on capital gains for either foreign or

- 8 -

local investors. The Securities and Exchange Commission of Sri Lanka, which was

established in 1987, regulates the market. Insider trading is prohibited in Sri Lanka.

There are 15 stock brokering companies in the market. The Sri Lankan stock market is

not a dealership market. Brokers act as intermediaries to transactions, and do not

engage in market making. Trading of securities in the Colombo Stock Exchange is

completely automated, and the CSE is considered one of the finest trading systems in

the world. The automated trading system was introduced in June 1997. Brokers are

electronically connected to a central computer, located at the CSE, which automatically

executes orders on the basis of price-time priority. The settlement period is t+ 5 for buy

and t+ 6 for sell transaction, where t is date of the trade. Transaction cost is 1.125 % for

transactions up to 1 million rupees and 1.025 % for transactions exceeding that amount.

Trading takes place on weekdays, except exchange holidays, from 9:30 A.M. to 12.30

P.M.

A company can be listed in the Colombo Stock Exchange in one of three ways, namely,

offer for subscription, offer for sale, or introduction. An offer of subscription is an offer

by an issuer to sell its own shares to the public. This involves the sale of new shares and

the issuer raises capital through the sale. This is by for the most widely used method for

IPOs in Sri Lanka. An offer for sale is an offer to sell shares held by the existing

shareholders to the public. This method has been used primarily in privatization of

public enterprises by the government to sell its shares of state-owned enterprises to the

public. An introduction is the listing of already existing shares of a company without

making a public issue. This method of listing began in 2000, and since than 15

companies has been listed by way of introduction.

The companies in Sri Lanka are allowed to use fixed-price, auction, as well as book

building methods for IPOs. However, all the IPOs have used the fixed-price method,

except two recent issues which have used the Dutch auction method.

Although underwriting as issue is not mandatory, the practice is to have the issues

underwritten by an investment bank. The issuer is required to obtain the services of a

- 9 -

sponsoring firm registered with the CSE. These sponsors are generally the merchant

and investments banks. The role of the sponsor is to ensure that the share issue

complies with the stock exchange and other regulatory requirements relating to the IPO.

Any investor can subscribe for shares by submitting a completed subscription

application along with a check for the total value of the shares subscribed. An

application can be submitted through any of the 15 registered stock brokering firms.

Except in rare circumstance, such as in privatization IPOs where certain limits to the

number of shares per applicant may be specified, an investor can apply for any number

of shares.

The existing literature shows that small issues are more under priced than large issues

(Ritter, 1984; Beatty and Ritter, 1986), investor sentiment is positively related with

under pricing (Ritter, 1984), and privatization IPOs are more under priced than

conventional IPOs (Jones et al, 1999; Perotti and Guney, 1998).

2.1 Short-run under pricing in emerging markets

Since the present study is based on the emerging stock market of Sri Lanka, previous

evidence on IPO under pricing from emerging markets is particularly relevant. Previous

studies show that initial under pricing is a common phenomenon in markets around the

world. However, there is a great deal of variability in under pricing across markets and

regions. In terms of initial returns in the Asian region, Islam (1999) finds 116 % in

Bangladesh, Chen et al. (2004) report 145 % in China, and Marisetty and Subramanyam

(2005) show 94 % in India. Boulton et al. (2007) show evidence of under pricing for

Indonesia (41%), Malaysia (41 %), South Korea (44 %) , Taiwan (13 %), and

Thailand(26 %). Further, Amihud et a. (2002) reports under pricing of 12 % in Israel,

and Sullivan et al. (1999) finds 23% initial returns in Philippines. Thus, Sri Lanka’s

neighbor india has experienced a very high degree of under pricing. The markets in the

Asia have shown a much larger degree of under pricing than markets in any other

region, largely due to very high under pricing in Bangladesh, China and India.

2.2 Explanations for the short-run under pricing

- 10 -

The present study investigates the cross sectional variation in IPO under pricing by

issue size, investor sentiment, issue type (conventional and privatization issues), and

the issuer’s industry. This section discusses the existing literature and testable

implications related to issue size, sentiment, privatization, and industry.

2.2.1. Under Pricing and issue size

Beatty and Ritter (1986), based on the asymmetric information model of Rock (1986),

present a model in which greater the ex-ante uncertainty about the value of the issue,

the greater the expected under pricing. The theory predicts a direct relation between

ex-ante uncertainty and under pricing. Beatty and Ritter (1986) use gross proceeds as

one of the proxies to capture ex-ante uncertainty because small issues are considered

more risky than large offerings. Consistent with the theory, they find that the inverse of

gross proceeds is significantly positively related with under pricing. High-risk IPOs

should be more underpriced than low-risk issues. Using sales in the 12-month period

prior to the IPO as a proxy for risk, Ritter (1984) finds that higher-risk (lower sales)

issues have higher average initial returns than lower-risk (higher sales) issues. Issue

size has been used as a proxy for ex-ante uncertainty in other studies as well (e.g.,

Amihud at al., 2002; Kiymaz,200; Ljungqvist, 1997). The testable implication of the ex-

ante uncertainty hypothesis is that the smaller the issue size, the larger will be the

initial under pricing. This study tests this implication using gross proceeds as a proxy

for ex-ante uncertainty about the value.

2.2.2. Under pricing and investor sentiment

Another potential factor influencing under pricing is the investor sentiment before the

first day of trading of an IPO. Ritter (1984) calls this the institutional lag hypothesis

because of the time gap between when the offer price is determined and the new issue

is traded. Investor sentiment is defined as the general attitude of investors in the

aggregate about the short-term direction of the overall market. Positive sentiment,

which investors expect the overall market to trend upward, is likely to increase the

demand for the IPO stocks on the first day of trading resulting in price appreciation.

Similarly, negative sentiment, which shows that investors expect the overall market to

- 11 -

decline in the short-term, is likely to diminish the enthusiasm for the IPO on the first

day of trading. Thus, investor sentiment and under pricing is expected to be positively

related.

Ritter (1984) uses returns on the natural resources index from the registration date to

the offering date as a proxy for institutional lag to investigate high under pricing in

natural resource IPOs. Investor sentiment can also be measured using the market return

for a defined period prior to the first day of trading (e.g., Amihud et al., 2002, Kiymaz,

2000; Ljungqvist, 1997; Kunz and Aggrarwa, 1994). This study tests the implication of

the investor sentiment hypothesis using cumulative market returns for the three-month

period preceding the first day of trading as a proxy for investor sentiment regarding the

direction of the market.

2.2.3. Under pricing and privatization

Privatization IPOs can be considered more risky than conventional IPOs, and therefore

contain more ex-ante uncertainty. This higher uncertainty regarding the value of

privatization IPOs can be attributed to several factors. Perotti (1995) argues that

privatizations are associated with considerable policy uncertainty after the

privatization. Governments may yield to pressure by stake holders to reallocate value

through policy changes such as re-regulation, taxation, changes in regulated rates, and

entry deregulation etc. Hence, government may signal the commitment to a future

policy by under pricing the issue. Privatization IPOs may contain a higher risk premium

due to their greater exposure to political risk (Huibers and Perotti, 1998). These and

other factors may cause more ex-ante uncertainty about the true value of privatization

IPOs relative to conventional IPOs leading to more under pricing of privatization IPOs.

Indeed, previous studies show that for many countries the average initial under pricing

of privatization IPOs is much higher. For example, in a study of share-issue

privatizations, Jones et al. (1999) show that initial under pricing is 34.1 % for initial

offers and 9.4 % for seasoned offers. Others show that under pricing in privatization

issues is higher than that in non-privatization issues (e.g., Perotti and Guney, 1993;

Dewenter and Malatesta, 1997; Jenkinson and mayer, 1988). Huibers and Perotti (1998)

show that privatization stocks in emerging markets exhibit greater exposure to political

- 12 -

risk, and superior post-IPO performance of privatization stocks reflects in part the

progressive resolution of this political risk. Hence, in this study, it is hypothesized that

privatization issues will be more underpriced than conventional issues due to the

increased ex-ante risk in the spirit of the ex-ante uncertainty hypothesis.

2.2.4. Under pricing and Industry

There is also evidence of industry effects in IPO under pricing Ritter (1984), for

example, finds that the hot issue market of 1980 in the U.S. is entirely attributable to

under pricing in the natural resources industry. Evidence on industry clustering has

been found in other work as well. Stocks in Sri Lanka are classified in to 20 industries,

and privatization issues have been particularly shown to be concentrated in some

industries such as footwear and textiles, Plantations, and manufacturing. Hence, it is

reasonable to suspect the presence of industry effects in under pricing. Therefore, this

study investigates the initial returns across the industry categories to detect any

industry effects of under pricing.

- 13 -

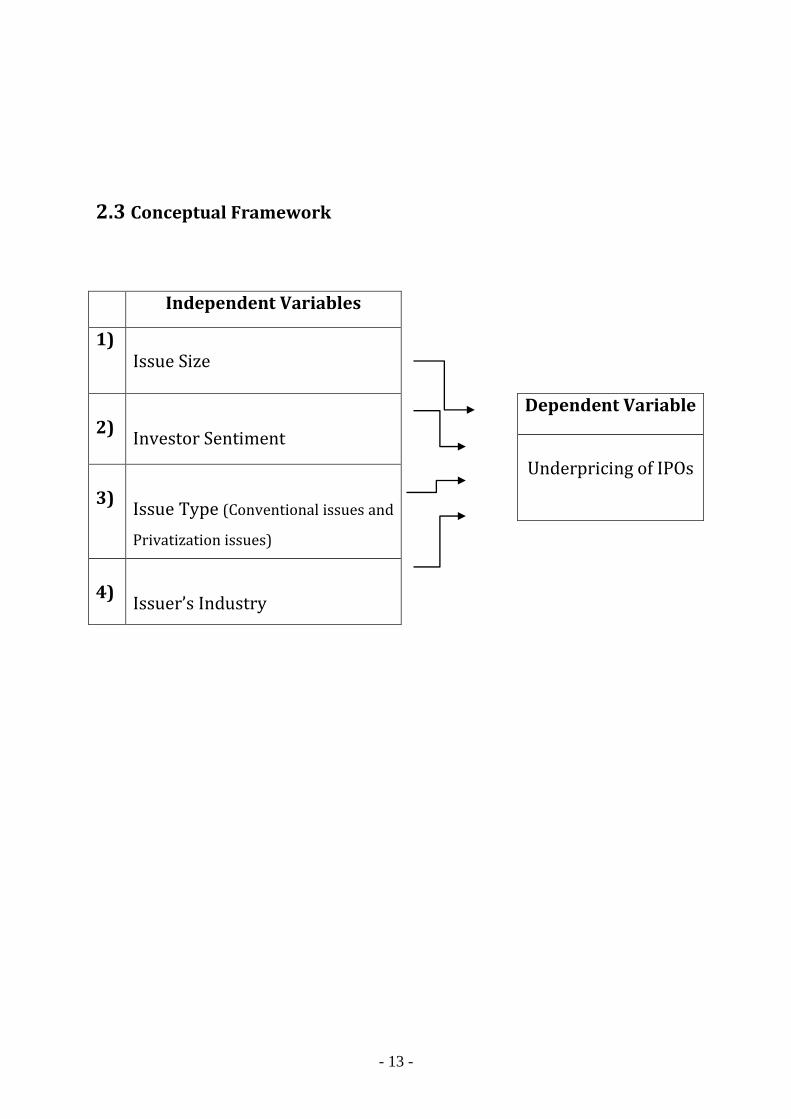

2.3 Conceptual Framework

Independent Variables

1) Issue Size

2)

Investor Sentiment

3)

Issue Type (Conventional issues and

Privatization issues)

4)

Issuer’s Industry

Dependent Variable

Underpricing of IPOs

- 14 -

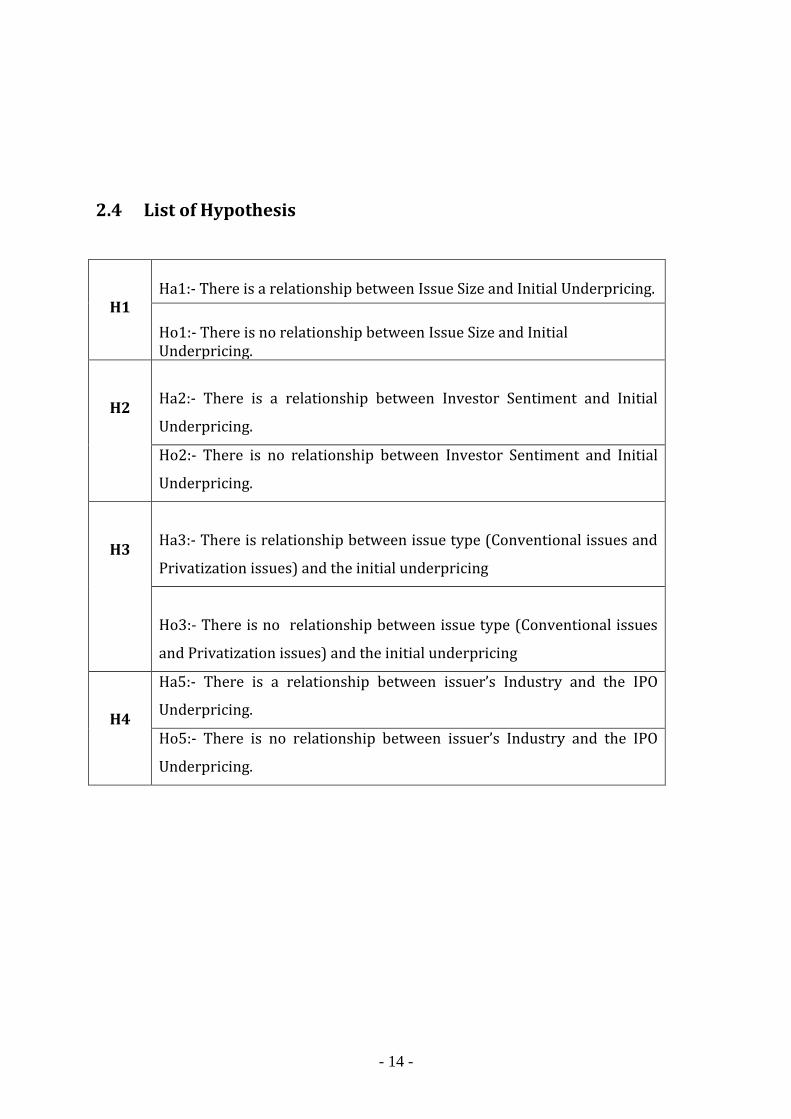

2.4 List of Hypothesis

H1

Ha1:- There is a relationship between Issue Size and Initial Underpricing.

Ho1:- There is no relationship between Issue Size and Initial Underpricing.

H2

Ha2:- There is a relationship between Investor Sentiment and Initial

Underpricing.

Ho2:- There is no relationship between Investor Sentiment and Initial

Underpricing.

H3

Ha3:- There is relationship between issue type (Conventional issues and

Privatization issues) and the initial underpricing

Ho3:- There is no relationship between issue type (Conventional issues

and Privatization issues) and the initial underpricing

H4

Ha5:- There is a relationship between issuer’s Industry and the IPO

Underpricing.

Ho5:- There is no relationship between issuer’s Industry and the IPO

Underpricing.

- 15 -

Chapter: Three – Research Methodology

This research will be carried out after analyzing all the related theoretical background

on the topic. For the research to be well performed, I already have created certain

hypothesis in relation to the IPO under pricing. The study has to be carried through

Deductive Reasoning method as the research has been involved with so many

hypothesis testing.

The short-run performance of IPOs is measured by the initial return calculated as the

difference between the first-day closing price and the offer price as a percent of the offer

price.

This can be explained as follows.

First-Day Closing Price – Offer Price 100

Initial Return =

Offer Price

To study the time-series and cross sectional patterns of initial performance of IPOs, this will

be examined equally-weighted initial returns by

(1) Issuer year

(2) Issuer’s industry

(3) Issue size

(4) Investor sentiment

(5) Privatization vs. conventional issues.

The differences in average initial returns between categories have to be tested using the

two-sample t-test allowing for unequal variances. Then, the relation between the initial

- 16 -

returns and size, sentiment, privatization, and industry has to be investigated through a

multivariate cross-sectional regression models. The motivation for the regression analysis

is to provide a test of the ability of these factors to jointly explain the cross sectional

variation in initial IPO returns in Sri Lanka.

The effect of the issue size on initial return will be captured through size, which is the

natural logarithm of proceeds of the issue.

It is important to capture any industry effects on initial returns. To incorporate industry

effects, the regression models will have to be modified with certain industry categories. T-

statistics will be used to assess the statistical significance of the coefficients.

In order to investigate the impact of the investor sentiment on small vs. large issues the

initial returns will have to be further classified by sentiment and size. In this analysis,

sentiment is classified as either positive or negative. Market conditions in which the

cumulative market returns over the three – month period preceding the first-trading day

are greater than zero will be used to proxy for positive market sentiment. Accordingly,

sentiment will be defined as a dummy variable which takes the value of 1 if the sentiment is

positive is positive and 0 if the sentiment is negative.

Further, to examine the impact of privatization on small vs. large issues, initial returns will

have to be categorized by privatization and size. This classification is used to assess if any

size-effect is attributable to a privatization –effect, and there by provide clarity to the

uncertainty hypothesis.

3.1 Research Strategy

This research is basically a quantitative research and so some of the quantitative

research strategies will have to be used for reaching a justifiable conclusion. As a result

of this, empirical study will be carried out with some of the quantitative techniques such

as Regression Analysis, Student-t distribution etc.

- 17 -

3.2 Population

There are 238 companies have been listed in Colombo Stock Exchange from 1987 to

2009. The data on Sri Lankan IPOs were obtained from the Colombo Stock Exchange,

and the Securities and Exchange Commission of Sri Lanka. The data include the name,

industry, offer price, the number of shares offered, name of the underwriter, first date of

trading and the first-day closing price in respect of all new issues of shares that took

place in the 22-years period from 1987 to 2009.

3.3 Sampling

When selecting the sampling technique for selecting the justifiable sample, following

factors have been considered.

IPOs of non-voting common stocks and preferred stocks are excluded. The study also

excludes the listings made through introductions, since they do not have an offer price.

The total number of IPOs of voting common stocks is 118.

For the purpose of the study, IPOs with the issue size greater than 900 million rupees

and initial returns greater than 300 % are considered outliers, and hence excluded from

the sample.

After considering all the above exclusions, the final sample selected is 107 IPO issues

from 1987 to 2009.

The performance of the overall market is measured by the All Share Price Index (ASPI)

of the CSE, which is a value-weighted price index (excluding dividends) of all listed

stocks. The sample includes 30 privatization IPOs and conventional or non-privatization

issues.

- 18 -

Year of Industry

Number of IPOs

Aggregate Proceeds

Conventional

issues

Privatization

Issues

Total

Rs Mn.

%

Selected sample : By Year

1987 3 0 3 147 0.88

1988 7 1 8 132 0.79

1989 1 1 2 140 0.84

1990 1 0 1 7 0.04

1991 3 1 4 139 0.83

1992 7 2 9 1,765 10.60

1993 7 3 10 1,631 9.80

1994 12 3 15 3,248 19.51

1995 11 3 14 2,428 14.58

1996 2 7 9 1,573 9.45

1997 4 2 6 833 5.00

1998 1 4 5 330 1.98

1999 3 1 4 496 2.98

2000 1 2 3 100 0.60

2001 0 0 0 - -

2002 3 0 3 133 0.80

2003 5 0 5 1,170 7.03

2004 1 0 1 300 1.80

2005 1 0 1 600 3.60

2006 1 0 1 400 2.40

2007 0 0 0 - -

2008 1 0 1 396 2.39

2009 2 0 2 682 4.10

Total 77 30 107 16,650 100.00

- 19 -

3.4 Statistical Methodology

Explaining the Short- and Long-Term IPO Anomalies by R&D

Re-Jin Guo, Baruch Lev, and Charles Shi

Simple statistics method and Regression Analysis. Correlation Coefficient

U.S.-Bound IPOs: Issue Costs and Selective Entry

Robert Bruner, Susan Chaplinsky, Latha Ramchand

Hypothesis analysis and Regression analysis. Robustness Tests

Analyst Following of Initial Public Offerings

Raghuram Rajan, Henri Servaes

Simple statistics method and Correlation Coefficient

A Review of the New Issue Puzzles

S. Ghon Rhee,

Simple statistics method and Regression Analysis.

The IPO effect and measurement of risk

John D. Knopf John L. Teall

Regression Analysis and Correlation

The Effect of Market Conditions on Initial Public Offerings

Raghuram Rajan, Henri Servaes

Simple statistics Method and Regression analysis.

- 20 -

3.5 Operationalization of Variables

Regression Analysis and Correlation Coefficient technique have been widely used in

previous studies by the several Researchers who already investigated the issues

relating to Initial Public Offerings. So the same methods will be used in this research as

well.

Primary data will be obtained by having face to face interviews with share market

professionals and the experts in the field. In addition to that, secondary data will be

obtained from the books, CDs and annual reports published by the Colombo Stock

Exchange and Securities Exchange Commission of Sri Lanka.

Chapter: Four – Conclusion

As clearly mentioned in the Problem Statement, there are some IPO related anomalies

which are still not properly investigated especially in Sri Lankan context. Several studies

have been carried out in other countries and in the analysis of Literature review, it is clear

that the issues are exist in almost all the countries which are having Stock Exchanges.

Article Name

Author Technique

- 21 -

As a result of this, there is a genuine need to carry out a comprehensive research on the

concerned area to achieve the main objectives mentioned in the Research Objectives.

This Study will really facilitate to understand the relationship between Short run

underpricing of Initial Public Offerings in Sri Lanka and the four independent variables

mentioned in the Conceptual Framework.

- 22 -

List of References Aggarwal, R., Leal, R., Hernandez, L., 1993. The aftermarket performance of initial public offerings in Latin America. Financial Management 22, 42-53. Amihud, Y., Hauser, S., Kirsh, A., 2002. Allocations, adverse selection and cascades in IPOs: Evidence from Tel Aviv stock exchange. Working paper, New York University, New York. Alli, K. L., Subrahmanyam, V., Gleason, K. C., 2006. Short and long-run performance of IPOs in post-apartheid South Africa. Working paper, Mercer University, Atlanta. Beatty, R. P., Ritter, J. R., 1986. Investment banking, reputation, and the underpricing of initial public offerings. Journal of Financial Economics 15, 213-232. Boulton, T. J., Smart, S. B., Zutter, C. J., 2007. IPO underpricing and international corporate governance. Working paper, Miami University, Oxford. Chahine, S., 2008. Underpricing versus gross spread: New evidence on the effect of sold shares at the time of IPOs. Journal of Multinational Financial Management 18, 180-196. Chen, G., Firth M., Jeong-Bon K., 2004. IPO underpricing in China’s new stock markets. Journal of Multinational Financial Management 14, 283-302. Dewenter, K., Malatesta, P., 1997. Public offerings of state-owned and privately–owned enterprises: An international comparison. Journal of Finance 52, 1659-1679. Wang.L, Picheng L, Chen-Lung Chin and Gary Kleinman 2005. The impact of financial forecasts regulation on IPO anomalies: Evidence from Taiwan,15-25 Rottke. N, Schiereck.D, Winkel.O, 2008. Underpricing of European property companies and The IPO cycle: a note, 12-20 Thomas J. W, Michael Y. L., 2007. Dynamic relationships and technological innovation in hot and cold issue markets, 5-15 Ghon Rhee.S, Luke K.J, 2002. Review of the New Issue Puzzles, 5-10 James R. B, Lena C. B.2003. Agreeing to Disagree: Why IPOs are underpriced, 12-15 Re-Jin G, Baruch .L, Charles. S. 2005. Explaining the Short- and Long-Term IPO Anomalies by R&D ,4-20 John D. K, John L. T.1999. The IPO effect and measurement of risk. Journal of Financial and Strategic Decisions Volume 12 Number 2, 13-2

- 23 -

Your comments and reviews are greately appreciated by the Author. Researched by,

Jayantha C. Kothalawala. B.Sc (Mgt)Sp. Hons., ACA,ACMA,MBA-FIN(USJ)