the sentiment index - q2 2015 - visible and hyde park angels

TRANSCRIPT

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

Q2 2015 Early Stage Investor Sentiment Index

@VisibleVC | @HydeParkAngels Page ! of !1 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

Introduction

The Sentiment Index leverages insights from investors to indicate important trends that meaningfully affect companies, investors, and anyone actively involved in the early-stage market. The survey gauges probable future investment behavior by understanding the market expectations of top early-stage investors to help companies and investors make more informed decisions around fundraising, hiring, and growth strategies.

Contents

I. Methodology & Calculations

II. Sentiment Survey Results & Analysis

III. A Bridge (Round) to Nowhere

IV. Navigating the Series A Crunch

V. Recurring Revenue Rules Again

@VisibleVC | @HydeParkAngels Page ! of !2 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

@VisibleVC | @HydeParkAngels Page ! of !3 32

Visible gives you the power to tell the story around your key performance data. Visualize your most important metrics, organize capitalization and keep all of your

stakeholders engaged all from a single platform.

Try Visible for Free

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

I. Survey Methodology and Index Calculation

The Sentiment Index is an investor confidence report compiled from a survey conducted among investors actively engaged in the Seed and Series A markets. We should note that the determination of what exactly qualifies as Seed and what qualifies as Series A is murky at best and there is certainly no hard boundary. For the purpose of this analysis we’ll borrow from Jason Calacanis’ post from earlier this year to help define the delineation:

• Seed Stage - Companies with a launched product (can be a prototype) raising capital to build out an initial team and get product traction. These companies are almost always raising less than $5mm.

• Series A - Companies who have gained initial traction thanks in part to their Seed Stage fundraise who are now raising funding necessary to scale their product. Companies at the Series A level are generally raising somewhere in the range of $5mm - $15mm.

Investors are often active at both stages since, again, the line is not always clear and because they will often “follow on” (i.e. invest additional capital) in previous investments that show strong traction.

@VisibleVC | @HydeParkAngels Page ! of !4 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

The index is published quarterly by Visible and Hyde Park Angels and assesses investor attitudes on the early stage market landscape on factors like deal and company quality, regional competitiveness and emerging sectors. The survey itself asks respondents a series of nine questions to help determine their view on the current state of the early stage market and their expectations for the near and long term future of the market. Supplemental demographic and current topic questions are asked as well to add depth to the analysis.

The Sentiment Index looks at investor sentiment on the current state of the early-stage market as well as their near (next 12 months) and long-term (next 3 years) expectations for what is to come. Three primary components comprise the Sentiment Index.

• Investment Competitiveness Score tracks how competitive is it for investors to get into the deals they want. If competition is increasing, it indicates an influx of capital into the system and signals that it is or will be a good time for companies to be raising money. If it is decreasing, investors believe that less capital is or will be available within the system for companies looking to raise their next round of funding.

• Investment Attractiveness Score determines whether investors believe that valuations are reasonable and that deal terms are aligned with the quality of companies the are seeing. If investment attractiveness is on the decline, it could signal an impending correction

@VisibleVC | @HydeParkAngels Page ! of !5 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

or a less than welcoming fundraising environment for companies raising capital.

• Company Growth Score seeks to understand changes to the traction of companies investors are seeing. Are their current and prospective portfolio companies hitting the same revenue and user numbers as they were last year? Do they expect to see stronger company growth - due to more receptive markets, stronger products, or better teams - in the future than they are seeing now?

Responses for every question are categorized as positive, negative or neutral. For each question, the number of positive responses is divided by the sum of positive and negative responses. The Overall Early Stage Investor Sentiment Index is the average of the numbers for the survey's nine questions. In short, more positive responses means a higher index; more neutral and/or negative responses means a lower one.

@VisibleVC | @HydeParkAngels Page ! of !6 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

II. Sentiment Survey Results & Analysis

Current Market Conditions & Near Term Market Expectation

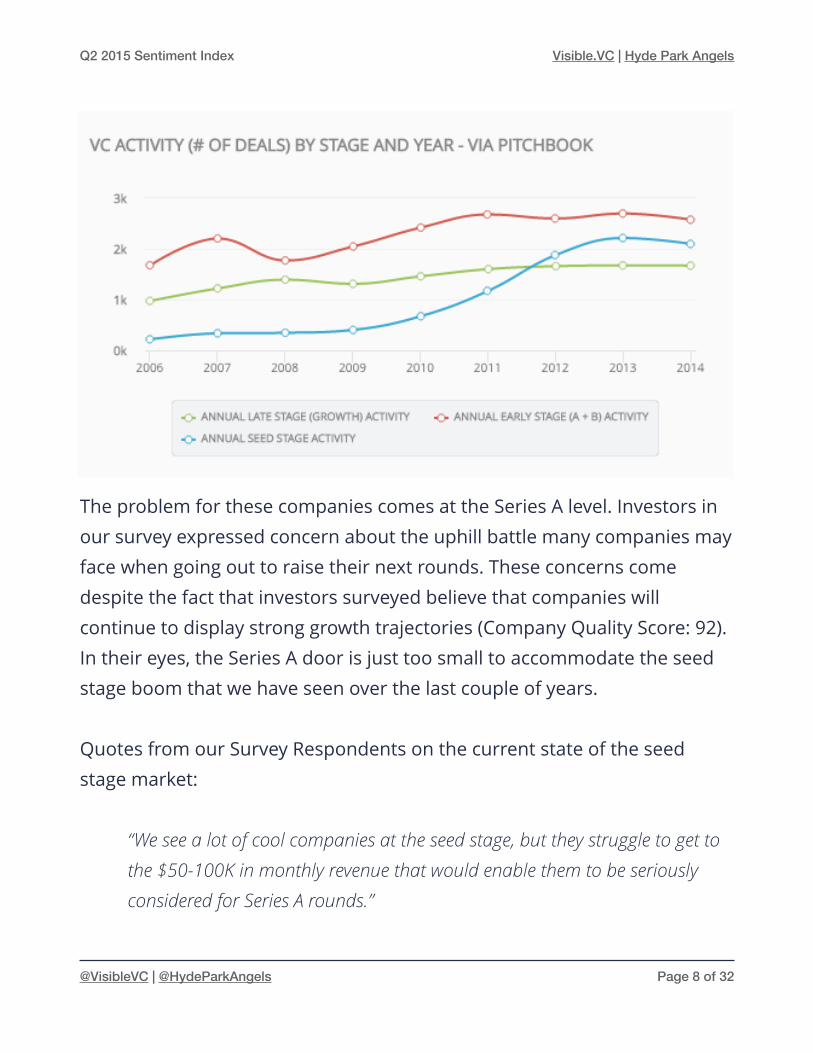

The talk of a bubble in the startup world has been intensifying over the last few years with many people publicly anticipating a major shakeup. The doom and gloom outlook that makes headlines and drives clicks doesn't seem to be shared by our group of survey respondents, at least in the near term. At the seed stage, investors believe that capital will remain widely available (Investment Competitiveness Score: 92), primarily due to the fact that 2014 was a record year for seed fund formation (sub $250MM fund size).

In 2013, according to Pitchbook data, 143 sub-$250mm funds were raised. In 2014, that number grew almost 40% to 198 funds. Firms of this size are most often investing at the Seed and Series A stages. Until these funds are fully invested (which won't occur in the next 12 months) and need to go raise again, companies with competitive traction and strong teams should have no issues raising at the seed stage.

@VisibleVC | @HydeParkAngels Page ! of !7 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

The problem for these companies comes at the Series A level. Investors in our survey expressed concern about the uphill battle many companies may face when going out to raise their next rounds. These concerns come despite the fact that investors surveyed believe that companies will continue to display strong growth trajectories (Company Quality Score: 92). In their eyes, the Series A door is just too small to accommodate the seed stage boom that we have seen over the last couple of years.

Quotes from our Survey Respondents on the current state of the seed stage market:

“We see a lot of cool companies at the seed stage, but they struggle to get to the $50-100K in monthly revenue that would enable them to be seriously considered for Series A rounds.”

@VisibleVC | @HydeParkAngels Page ! of !8 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

“Tweeners (companies with some growth, but not enough) will have problems raising money. They were able to get seed funding, but will struggle getting institutional funding in a priced round.”

“There is a glut of Seed funded companies doing well, but not well enough to grab one of the limited Series A slots. This playing out will shape a lot of what is to come in the near term."

What others in the market had to say about where we are today:

“If you are a 20-something tech entrepreneur you could be forgiven for thinking that seed-stage investors, Angellist Syndicates and widely available angel money always existed" - Mark Suster of Upfront Ventures

“There is an erosion of valuation discipline across all stages of venture capital right now." - Manu Kumar of K9 Ventures

@VisibleVC | @HydeParkAngels Page ! of !9 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

Long Term Market Expectations

While still edging on the side of optimism (Investment Competitiveness Score: 65), investors see capital moving away from the Seed Stage over the long term, making it more difficult for companies to raise but possibly forcing a return to more reasonable valuations and funding patterns. Since 2006, the average time between raising funds for VC firms has been 3.8 years.

That pacing will mean that 3 years from now (matching up with this survey's definition of “long-term”), many of the sub-$250mm firms that raised funds in 2014 will be back on the road looking to raise their next.

@VisibleVC | @HydeParkAngels Page ! of !10 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

Should the Series A crunch come to pass, as so many seem to think it will, laggard micro VC funds will find it difficult to raise subsequent funds and investors who moved down the venture stack may move back up to capture what could become a more attractive risk/reward equation in the later stages.

Another long-term focused topic that was brought up by survey respondents was the continued consolidation of LP capital with fund backers writing larger checks to fewer firms. In many cases, this means making a decision between hands on, operationally intensive firms and firms with smaller teams representing less involved capital.

In the first half of 2014, for example, nearly 50% of the capital raised was done so by less than 7% of active funds (according to True Bridge Capital Partners). This consolidation has primarily been occurring in the growth stage market, as the leading funds consistently product outsize returns relative to their peers.

@VisibleVC | @HydeParkAngels Page ! of !11 32

Image via True Bridge Capital

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

As the seed stage market matures and newly minted funds begin to establish track records, it is likely the same dynamic will emerge. Whether this will impact the way companies are funded or their ability to remains to be seen.

III. A Bridge (Round) to Nowhere

The term “Series A Crunch", mentioned here many times already, has been looming over the market with varying intensity for the last half decade. As the amount of capital pouring into seed investments continues to rise, investors in our Q2 survey expressed concern that the availability of follow on funding will leave a lot of companies without a path forward in spite of strong traction and a higher level of perceived company quality.

So what will the correction - if there ends up being one - look like and how will it impact the investors, operators and communities that are active in the early stage financing market?

1. "This time it's different" but that doesn't mean investors will end up happy.

In our survey, 53% of investors indicated that investment opportunities in their region were stronger than last year and 95% felt that the traction they

@VisibleVC | @HydeParkAngels Page ! of !12 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

have seen from companies - both within their portfolios and without - is at the same level or higher than it was 12 months ago.

If it is truly a numbers game, and a vast majority of seed funded companies in this cycle don't end up fitting through the Series A door, it is possible that a good portion of the stragglers can weather the storm by working towards profitability at the expense of pouring money into growth. The fact that so many of these emerging businesses operate with a SaaS model also plays into their favor, as those that have hit some level of predictability in their customer retention rates can begin to manage their burn more intelligently and extend their runway.

@VisibleVC | @HydeParkAngels Page ! of !13 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

Since private market performance data on individual companies is nearly impossible to parse in any meaningful way we cannot know for sure to what extent market participants as a whole are prepared for a squeeze. But if the the financial metrics of venture-backed IPOs can be used as a loose proxy for their seed stage siblings, today's companies start on a path to revenue earlier in their life cycles and, at the very least, understand the importance of profitable unit economics.

Long term, this sequence of events may be good for companies, forcing discipline and improving customer success efforts in order to minimize churn. On the other hand, VCs are tasked by their LPs with exceeding returns available in other asset classes and the failure to do so means that

@VisibleVC | @HydeParkAngels Page ! of !14 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

the opportunity to raise subsequent funds is not available. If you are one of the firms left Unicorn-less at the end of the day, no matter how many of your companies are still a going concern, then the bubble may as well have burst, regardless of what happens to the rest of the market.

It is possible that this dynamic, fueled by high valuations with unattainable growth benchmarks (thanks for explaining that one, Silicon Valley) along with a less than robust acquisition market at the later stages is what is causing some of the “sky is falling" talk from investors.

2. The money that has moved into the seed stage from non-traditional participants (later stage investors and new models) has caused a lack of discipline among all market participants that will leave many "swimming naked when the tide goes out”.

@VisibleVC | @HydeParkAngels Page ! of !15 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

The amount of capital being allocated to seed stage investments has risen dramatically in recent periods. This has many causes - low yields in other asset classes pushing investors into earlier stage deals and a willingness to pay up in order to avoid missing the next Slack or Snapchat chief among them.

In our Q2 survey, investors noted high (and increasing) level of competitiveness to get access to the best deals and hottest companies. Almost 40% of investors felt that competitiveness to invest in top deals in their region had increased in the past year while just 7% felt it had decreased.

@VisibleVC | @HydeParkAngels Page ! of !16 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

With more than $4 billion raised across over 200 seed stage firms, as well as platforms like AngelList (through their Syndicates model) pumping money into the system, seed capital is becoming easier to raise than ever before, no matter where you may be located. This has led some investors to lament the lack of discipline shown by many executive teams, throwing money at inefficient growth channels in the pursuit of vanity metrics and assuming that their A round will come together as easily as their seed.

If burn rates across the industry are too high, as YCombinator's Sam Altman suggests, companies may not have enough time to steer the ship in the right direction in the event of interest rate or risk-appetite changes.

In Altman's words: "It's OK if you want to spend money to be aggressive for growth or speed. The thing that is not OK is if the plans change or environment changes, you should be able to reach profitability on the money you have. What is OK is to spend money for productivity. What is not OK is just to light money on fire."

3. The traditional venture funding cycle no longer matches up with the prevailing company building rhythm and a fundamental shift needs to occur.

While the lack of first party information across the market makes it difficult to know which, if either, of the first two scenarios will play out, the data around the third scenario paints a more compelling picture of what might

@VisibleVC | @HydeParkAngels Page ! of !17 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

happen to the early stage landscape over the long term, regardless of how this specific business and funding cycle play out.

As USV's Fred Wilson recently noted, labor productivity has been outpacing gains in employment and wages since the 1980's and one of the outcomes of this divergence (called The Great Decoupling in this Harvard Business Review study) has been and will continue to be an increase in entrepreneurship.

@VisibleVC | @HydeParkAngels Page ! of !18 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

According to the Babson Global Entrepreneurship Monitor, early stage entrepreneurial activity across the globe has increased steadily over the past 5 years, with the percentage of working-age individuals involved in such endeavors jumping from 14.8% to 19.0% in 2014. As independent, control-driven Millennials move to become the largest generation of working age, this trend will only continue. According to a recent Bentley University study, about two thirds of millennial strive to start their own business.

Obviously, a large majority of these companies won't ever desire or require venture funding. But with the increased focus of sharing knowledge in the early stage world in the service of building startup communities, more regions, teams and individuals hold the knowledge and networks to build what would have traditionally been considered a company worthy of venture capital consideration.

@VisibleVC | @HydeParkAngels Page ! of !19 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

In the absence of even more money trickling down into the earliest stages of the fundraising landscape, the market may begin to bifurcate to a greater extent than it already has.

Of the three possibilities this seems to be the healthiest for the market although it certainly won't come to pass without some degree of handwringing and headache. Companies stuck in the middle may find their cap tables too crowded to take the “Indie" path yet not scalable enough to continue raising sizable venture rounds.

@VisibleVC | @HydeParkAngels Page ! of !20 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

IV. Navigating the Series A Crunch

Raise Your Round Even in Difficult Circumstances

Over the course of our research, as discussed so far, we have seen that investors believe there is plenty of funding available for seed rounds, but a much more limited amount for Series A rounds.

As a company, you might fall into a number of categories: not raising any capital yet, still gathering your Seed, or raising your Series A. Regardless of where you are in the early-stage investment cycle, the crunch directly affects you.

Ultimately, based on our research, the Series A crunch is here to stay for at least the next few years, so you’ll have to grapple with it sooner or later. But that doesn’t mean your Series A round is doomed to fail. Here’s what you can do to prepare.

Take a Fine-Toothed Comb to Your Financials

When you’re dealing with an especially difficult round to raise, it’s crucial for you to know what your true capital needs are. Look at your budget and evaluate whether all of your items are correct. It’s critical that you know how much funding you need to make it through the next 18–24 months.

@VisibleVC | @HydeParkAngels Page ! of !21 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

Going through your financials will also help you understand your burn rate, revenues, and general expense patterns on a clear enough level that you’ll be able to have an informed conversation with investors. This automatically adds to your credibility. Entrepreneurs who present shaky financials they don’t fully understand raise massive red flags.

@VisibleVC | @HydeParkAngels Page ! of !22 32

Get started with your own customizable dashboard for free on Visible

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

Understand the Logic Behind Your Numbers

It’s one thing to have data about your company, and another to know how your business operates. Understanding the elements of your business — your customers, your revenue streams, your employees, your growth trajectory, and so much more — allows you to develop a logic for predicting its patterns, both present and future. This will help you make decisions about future goals and strategies for growth, catch inefficiencies and opportunities for improvement, and finally, determine how to best measure your performance.

Your measuring mechanisms must be rooted in an underlying logic. Otherwise, the numbers you end up using to track your progress will lack real meaning. More importantly, if somehow the numbers you review or present turn out wrong, you can quickly correct them.

Knowing your numbers puts you in a better position to pitch your vision to investors because they can serve as quick reference points for success. Knowing the logic behind your numbers establishes you as an expert on your business, which doesn’t just make it easier to pitch, but demonstrates you’re investable as a founder.

Here’s a full list of numbers you’ll need to be prepared to understand and explain.

@VisibleVC | @HydeParkAngels Page ! of !23 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

Be Honest with Yourself About Your Company’s Progress

Once you truly, deeply understand your metrics, you have to ask yourself an important question. If you were an objective third-party, would you invest in your company based on its growth, traction in the market, and potential for success? Have you hit the milestones you said you would hit when you raised your seed? If the answer is no, you need to take a close look at your business and figure out what’s keeping you from achieving your goals.

You might not be at the right stage for a Series A round, in which case you need to consider alternatives. Can you charge for your services and ramp up revenue? Should you consider a bridge round? Too often, getting caught up in the idea that you need to raise another round prevents entrepreneurs from honestly evaluating their companies and comparing options. Don’t fall into that trap.

Cultivate Strong Relationships with Investors

The more effort you put into building meaningful relationships with investors before you need capital, the more chance you have of successfully funding your next round. This applies to any round you’re raising, but will help you when you’re looking for Series A funding.

The investors that know you, the ones who have already dedicated a lot of time and thought to your business, are more likely to support you

@VisibleVC | @HydeParkAngels Page ! of !24 32

Q2 2015 SENTIMENT INDEX VISIBLE.VC

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

financially. You have less to prove to them, and they already have skin in the game. Plus, they can help you find other investors who will invest with them, reducing the amount of time and energy you spend trying to get funded.

“The CEO is the investor's user interface into the business” - Dharmesh Shah, Hubspot Founder

Know How to Sell Your Strengths

What are the key factors that make you investable? Do you have a group of core power users? What about unique strategic partners that give you the competitive advantage? Ultimately, you need to be honest and upfront about your business when you pitch to investors, but you also need to sell what positively differentiates you.

Don’t get bogged down in explaining the details of your company; start simple. Articulate the pain the market, and your company’s true value — how it solves that problem so effectively it actually changes behavior. Then layer on your other assets.

@VisibleVC | @HydeParkAngels Page ! of !25 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

V. Recurring Revenue Rules Once Again

Last quarter investors expressed heavy bullishness on the future of Enterprise SaaS, something that continued this quarter. The chart on the next page breaks down which industries investors in our survey are most bullish on over the next 12 months.

As competition to get into notable enterprise SaaS deals continues to heat up, the companies themselves look strong (high growth, huge markets, etc.) while the valuation environment has many concerned.

“We see the bubble way more on the enterprise side than on the consumer side, which is the opposite of the bubble in '99. We see the crazier prices in terms of revenue multiples on enterprise side than on the consumer side. Uber and Lyft revenues growing so rapidly that you can at least make an argument for those prices. We're involved in some enterprise software companies trading 40, 50 60x, 80x sales." - Paul Martino, Bullpen Capital

“It’s very difficult to switch SaaS vendors once they’re embedded into business workflow. SaaS customers, by definition, made the decision to have an outside vendor manage the application. In the perpetual license model, in-house IT staff managed all software instances and thus could incur the internal costs to switch vendors if they so chose.” - Andreessen Horowitz

@VisibleVC | @HydeParkAngels Page ! of !26 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

@VisibleVC | @HydeParkAngels Page ! of !27 32

0% 5% 10% 15% 20% 25%

6%

8%

9%

15%

23%

0% 5% 10% 15% 20% 25%

4%

11%

11%

6%

25%

B2B SaaS

Big Data

On-Demand

Health

FinTech

B2B SaaS

Big Data

On-Demand

Health

FinTech

Q1 2015

Q2 2015

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

On Demand...for everything

Speaking of the Ubers and Lyfts of the world, interest in the On-Demand market continues to rise and now comes in at #2 in our investor bullishness ranking, with 11% of investors considering it to be the market with the most potential.

According to CB Insights, funding in the On-Demand market exploded in 2014, growing 514% to $4.12 billion.

@VisibleVC | @HydeParkAngels Page ! of !28 32

2015 is Projected Investment $ - CBInsights.com

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

In May, Haystack's Semil Shah hosted the first edition of the On Demand Conference in Palo Alto where investors and operators discussed the evolution and future of the market in depth. All of this seems to be speeding up the creation of On-Demand companies.

In a panel on investing in the On-Demand market, Greylock's Simon Rothman noted that his firm had met with (not just heard of or seen present) around 1,000 companies in the market during the last 18 months. Fellow panelists agreed, stating that they're seeing new companies in the space - whether focuses on B2B, B2C or market infrastructure - emerge on a daily basis.

@VisibleVC | @HydeParkAngels Page ! of !29 32

2015 is Projected Investment $ - CBInsights.com

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

FinTech investment takes off while optimism flatlines

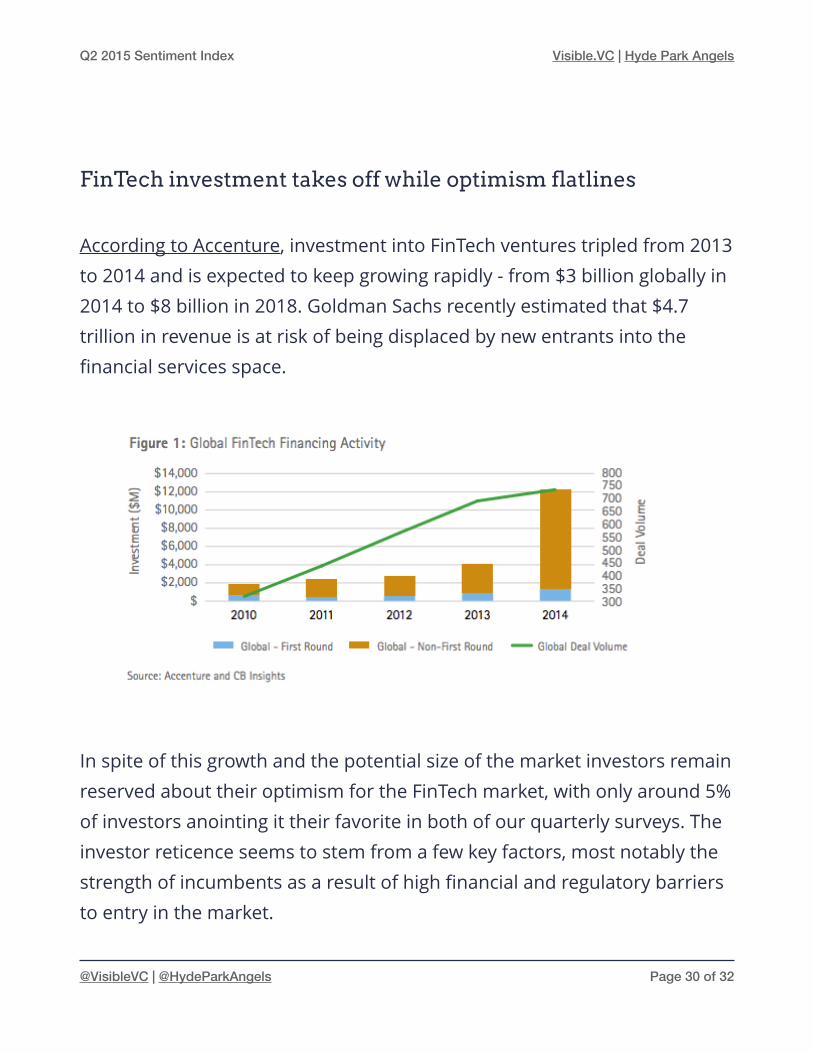

According to Accenture, investment into FinTech ventures tripled from 2013 to 2014 and is expected to keep growing rapidly - from $3 billion globally in 2014 to $8 billion in 2018. Goldman Sachs recently estimated that $4.7 trillion in revenue is at risk of being displaced by new entrants into the financial services space.

In spite of this growth and the potential size of the market investors remain reserved about their optimism for the FinTech market, with only around 5% of investors anointing it their favorite in both of our quarterly surveys. The investor reticence seems to stem from a few key factors, most notably the strength of incumbents as a result of high financial and regulatory barriers to entry in the market.

@VisibleVC | @HydeParkAngels Page ! of !30 32

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

The Sentiment Index Beta, powered by Visible is free and comes with enhanced charts, supplemental video and audio

analysis on the early stage market.

@VisibleVC | @HydeParkAngels Page ! of !31 32

Access The Sentiment Index Beta

Q2 2015 Sentiment Index Visible.VC | Hyde Park Angels

Visible

Visible gives you the power to tell the story around your key performance data. Visualize your most important metrics, organize capitalization and keep all of your stakeholders engaged all from a single platform. Brett Bivens Visible.VC [email protected]

Hyde Park Angels

Hyde Park Angels is the largest and most active angel group in the Midwest. With a membership of over 100 successful entrepreneurs, executives, and venture capitalists, the organization prides itself on providing critical strategic expertise to entrepreneurs and the entrepreneurial community.

Alida Miranda-Wolff Hyde Park Angels [email protected]

@VisibleVC | @HydeParkAngels Page ! of !32 32