the search for culprits and recoveries in the credit crisis

TRANSCRIPT

The Search for Culprits and Recoveries

in the Credit Crisis

Wednesday, November 19, 2008 8:00 a.m. to 10:00 a.m.

Jenner & Block LLP 919 Third Avenue, 37th Floor - New York, New York

The Search for Culprits and Recoveries in the Credit Crisis

1

Table of Contents TAB

Presentation Handouts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .A

Presenter Biographies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B

Jenner & Block Client Alert: Managing Risks Arising From the Credit Crisis . . . . . . . .C

Treasury Department’s “Interim Final Rule,” Oct . 20, 2008 (Guidance on Executive Compensation Provisions of TARP) . . . . . . . . . . . . . . . . . . . .D

The Search for Culprits and Recoveries in the Credit Crisis

2

• Stephen L. Ascher Partner Jenner & Block LLP Tel: 212 891-1670 Fax: 212 891-1699 E-mail: sascher@jenner .com

• Joseph J. Floyd Vice President and Managing Director Huron Consulting Group Tel: 646 277-2222 Fax: 212 785-1313 E-mail: jfloyd@huronconsultinggroup .com

• James M. Lukenda CIRA, Managing Director Huron Consulting Group Tel: 646 277-2207 Fax: 508-445-0256 E-mail: jlukenda@huronconsultinggroup .com

• Thomas C. Newkirk Partner Jenner & Block LLP Tel: 202 639-6099 Fax: 202 661-4926 E-mail: tnewkirk@jenner .com

• Andrew Weissmann Partner Jenner & Block LLP Tel: 212 891-1650 Fax: 212 891-1699 E-mail: aweissmann@jenner .com

• Richard F. Ziegler Partner Jenner & Block LLP Tel: 212 891-1680 Fax: 212 909-0854 E-mail: rziegler@jenner .com

Speakers

The Search for Culprits and Recoveries in the Credit Crisis

3

Presentation Handouts

The Search for Culprits and Recoveries in the Credit Crisis

4

1

The Search for Culprits andRecoveries in the Credit Crisis

November 19, 2008Jenner & Block New York Office

The “Enronization” of the Credit Crisis:Potential Criminal and Regulatory Liability for Inaccurate

Valuations and Market Assurance

Richard F. Ziegler, ModeratorPartner

Jenner & Block LLPFormerly General Counsel, 3M Company

Andrew WeissmannPartner

Jenner & Block LLPFormer Director of the Enron Task Force and Chief

of the Criminal Division of the United States Attorney’sOffice for the Eastern District of New York

Thomas C. NewkirkPartner

Jenner & Block LLPFormerly Associate Director of the Division of

Enforcement of the U.S. Securities and Exchange Commission

Joseph FloydVice President and Managing Director

Huron Consulting Group

The Search for Culprits and Recoveries in the Credit Crisis

5

2

3

Introduction: Some Root Causes and Effects of the Meltdown

• Securitization of mortgages helped divorce credit evaluation from credit risk and led to dramatic growth in subprime mortgages (including the “NINJA” loan — no income, job or assets)

• Mortgage-backed securities were rated and sold on the basis of flawed valuation models (the "sunny day" model)

• Derivative exposures (credit default swaps) were used to gain tremendous leverage, and without requiring an insurable interest(naked CDs’ and synthetic CDOs) – a $50-$60 trillion market

• Congress at Wall Street’s behest preempted state gambling laws’potential application to derivatives — Commodity Futures Modernization Act of 2000

4

Introduction, continued:• Swap sellers were allowed to take on huge derivatives risk without

need to post any reserves• Institutions used off-balance sheet vehicles• The market lacked transparency: the size of potential

counterparties’ risk portfolios was unknown – and market participants didn’t care (until it was too late)

• When the real estate market declined, consequences were tremendously magnified

The Search for Culprits and Recoveries in the Credit Crisis

6

3

5

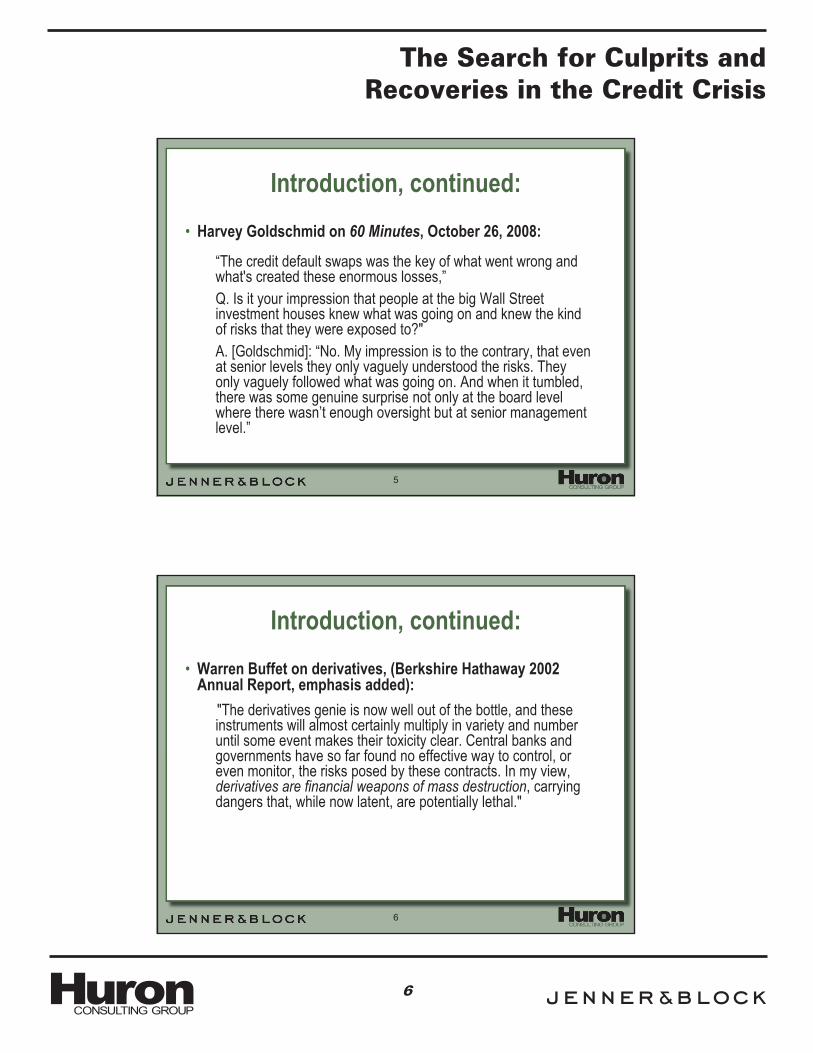

Introduction, continued:• Harvey Goldschmid on 60 Minutes, October 26, 2008:

“The credit default swaps was the key of what went wrong and what's created these enormous losses,”Q. Is it your impression that people at the big Wall Street investment houses knew what was going on and knew the kind of risks that they were exposed to?"A. [Goldschmid]: “No. My impression is to the contrary, that even at senior levels they only vaguely understood the risks. They only vaguely followed what was going on. And when it tumbled, there was some genuine surprise not only at the board level where there wasn’t enough oversight but at senior management level.”

6

Introduction, continued:• Warren Buffet on derivatives, (Berkshire Hathaway 2002

Annual Report, emphasis added):"The derivatives genie is now well out of the bottle, and these instruments will almost certainly multiply in variety and numberuntil some event makes their toxicity clear. Central banks and governments have so far found no effective way to control, or even monitor, the risks posed by these contracts. In my view, derivatives are financial weapons of mass destruction, carrying dangers that, while now latent, are potentially lethal."

The Search for Culprits and Recoveries in the Credit Crisis

7

4

7

Introduction, continued:• In short, a massive failure of risk assessment on both micro and

macro levels (i.e., absence of any “ERM” for financial system as a whole) led to:

– a massive “ponzi scheme” or “game of musical chairs” for which Wall Street got paid handsomely while essentially all investors of all stripes have so far taken a 30% hit to their portfolios

– cries not just of “greed” but of “corruption”– massive pressure to identify and punish culprits and recover

compensation for losses

8

Agenda

• Culpability, or the Confluence of Market Chaos• Major Roles and Responsibilities of Key Players• Common Valuation Problems• Potential Defenses

The Search for Culprits and Recoveries in the Credit Crisis

8

5

9

Culpability, or the Confluence of Market Chaos

Freddie MacCEO allegedly received warnings about the company’s deteriorating

financial health but continued to reassure investors

• In 2004, The New York Times reported that the CEO of Freddie Mac, Richard Syron, received an internal memo from Chief Risk Officer, David Andrukonis, warning him that the firm was financing questionable loans that threatened its financial health.

• According to The New York Times, Mr. Andrukonis, recalled telling Mr. Syron in mid-2004 that the company was buying bad loans that “would likely pose an enormous financial and reputational risk to the company and the country.”

• Mr. Syron stated the following in his annual letters to shareholders:– in June 2005, “Risk Management continues to be a distinguishing strength of Freddie Mac. Across a

range of rigorous measures… the company remains very safe and sound.”– in June 2006, “The company’s interest-rate and credit risks are near historic lows.”– and in March 2007, “Going forward, Freddie Mac remains strongly capitalized.”

• In July 2008, the U.S. Government placed Freddie Mac into conservatorship with full powers to control the assets and operations of the firm.

Source: “At Freddie Mac, Chief Discarded Warning Signs,” The New York Times, August 5, 2008; Freddie Mac Annual Reports, 2004 - 2006

10

Culpability, or the Confluence of Market Chaos

Lehman BrothersExecutives insisted that the company was in a strong liquidity position

just a few months before its collapse

• CNBC reported that on March 18, 2008, Lehman Brothers CFO, Erin Callan, told CNBC that Lehman is unlikely to face the kind of liquidity crisis that brought down Bear Stearns.

• In June 2008, Lehman Brothers raised $4 billion that Ms. Callan insisted was not to be used to decrease leverage. She stated “And over all, we stand extremely well capitalized to take advantage of these new [market] opportunities.”

• On June 16, 2008, Lehman Brothers CEO, Richard Fuld, stated that “Our capital and liquidity positions have never been stronger.”

• On September 15, 2008, Lehman Brothers filed for Chapter 11 Bankruptcy protection.

Source: “Lehman Goes to the Fed’s Discount Window,” CNBC.com, March 18, 2008; “Lehman’s Assurances Ring Hollow,” The New York Times, September 12, 2008

The Search for Culprits and Recoveries in the Credit Crisis

9

6

11

12

Culpability, or the Confluence of Market Chaos

Bear StearnsTwo senior portfolio managers of two hedge funds touted the prospects of the funds,

while privately acknowledging bleak outlook for returnsAccording to the indictment:• Ralph Cioffi and Matthew Tannin managed two hedge funds that invested primarily in high grade debt

securities were marketed as low risk. Bear Stearns Securities Corporation was the prime broker for these funds.

• Throughout March 2007, Mr. Tannin “repeatedly told investors…that he believed that the market presented a buying opportunity and that he was adding to his investment in the Funds.” However, Mr. Tannin allegedly never added to his personal investment in the funds.

• Also in March 2007, Mr. Cioffi moved $2 million of his approximately $6 million investment in one of his managed funds into a different Bear Sterns hedge fund. Mr. Cioffi allegedly led investors to believe that he never made the transfers.

• Privately, Mr. Tannin communicated to Mr. Cioffi: “If we believe [our internal modeling] is ANYWHERE CLOSE to accurate I think we should close the funds now... If AAA bonds are systematically downgraded then there is simply no way for us to make money – ever.”

• In June 2007, the funds collapsed, leading to investor losses of more than $1 billion.• In June 2008, Mr. Tannin and Mr. Cioffi were indicted on charges of conspiracy and fraud.

Source: The United States Attorney’s Office, Eastern District of New York, Press Release, June 19, 2008

The Search for Culprits and Recoveries in the Credit Crisis

10

7

13

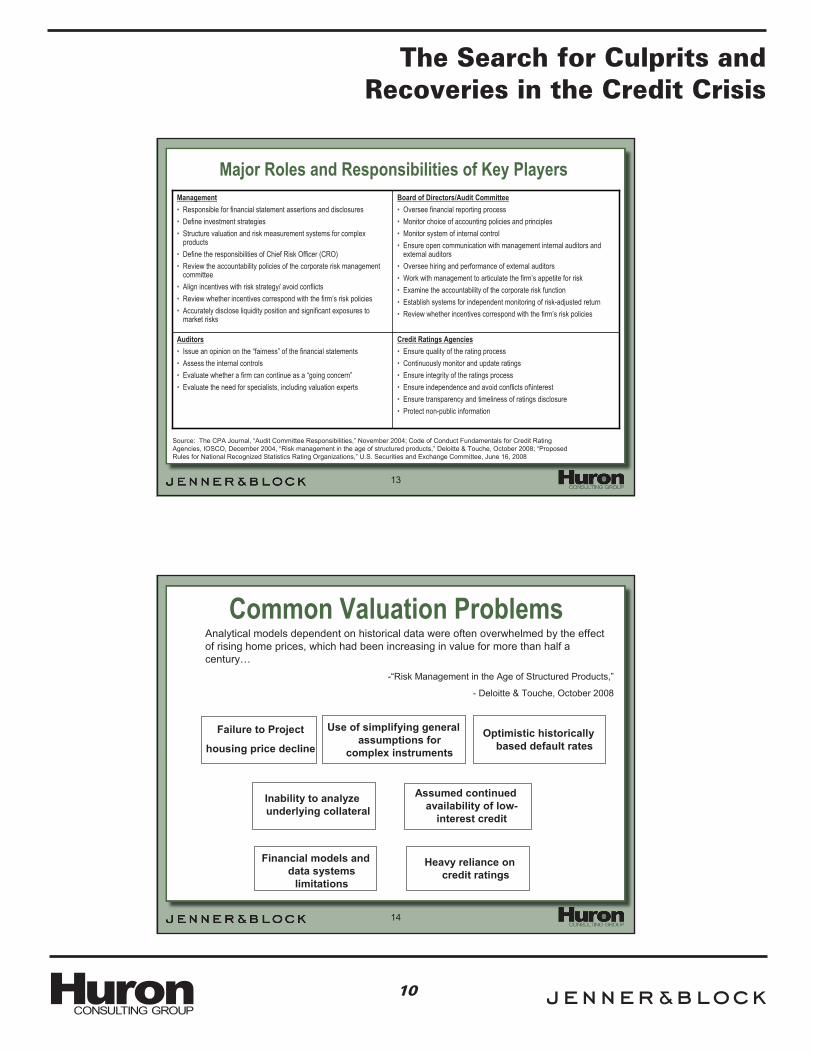

Major Roles and Responsibilities of Key Players

Source: The CPA Journal, “Audit Committee Responsibilities,” November 2004; Code of Conduct Fundamentals for Credit Rating Agencies, IOSCO, December 2004, “Risk management in the age of structured products,” Deloitte & Touche, October 2008; “Proposed Rules for National Recognized Statistics Rating Organizations,” U.S. Securities and Exchange Committee, June 16, 2008

Credit Ratings Agencies• Ensure quality of the rating process• Continuously monitor and update ratings• Ensure integrity of the ratings process• Ensure independence and avoid conflicts of\interest• Ensure transparency and timeliness of ratings disclosure• Protect non-public information

Auditors• Issue an opinion on the “fairness” of the financial statements• Assess the internal controls• Evaluate whether a firm can continue as a “going concern”• Evaluate the need for specialists, including valuation experts

Board of Directors/Audit Committee• Oversee financial reporting process• Monitor choice of accounting policies and principles• Monitor system of internal control• Ensure open communication with management internal auditors and

external auditors• Oversee hiring and performance of external auditors• Work with management to articulate the firm’s appetite for risk• Examine the accountability of the corporate risk function• Establish systems for independent monitoring of risk-adjusted return• Review whether incentives correspond with the firm’s risk policies

Management• Responsible for financial statement assertions and disclosures• Define investment strategies• Structure valuation and risk measurement systems for complex

products • Define the responsibilities of Chief Risk Officer (CRO)• Review the accountability policies of the corporate risk management

committee• Align incentives with risk strategy/ avoid conflicts• Review whether incentives correspond with the firm’s risk policies• Accurately disclose liquidity position and significant exposures to

market risks

14

Common Valuation ProblemsAnalytical models dependent on historical data were often overwhelmed by the effect of rising home prices, which had been increasing in value for more than half a century…

-“Risk Management in the Age of Structured Products,”

- Deloitte & Touche, October 2008

Failure to Project

housing price declineOptimistic historically

based default rates

Use of simplifying general assumptions for

complex instruments

Inability to analyze underlying collateral

Assumed continued availability of low-

interest credit

Heavy reliance on credit ratings

Financial models and data systems

limitations

The Search for Culprits and Recoveries in the Credit Crisis

11

8

15

Potential Defenses

“A sound banker, alas! Is not one who foresees danger and avoids it, but one who, when he is ruined, is ruined in a conventional and orthodox way along with his fellows, so that no one can really blame him.”

- John Maynard Keynes, “The Consequence to the Banks of the Collapse in Money Values,” 1931

Source: Charles Calomiris, “The Subprime Turmoil: What’s Old, What’s New, and What’s Next,” October 2, 2008

16

Potential Defenses

• Management• Board of Directors• Auditors• Credit Ratings Agencies

The Search for Culprits and Recoveries in the Credit Crisis

12

9

17

New Expectations for Governanceand Compliance

• Old Model (Reactive) – Board and management must respond when on notice of misconduct

• New Model (Proactive) –– Management plays a hands-on role in ensuring an

ethics/compliance program to prevent, detect and respond to violations

– Board provides oversight of program

Recovering Credit Crisis Losses:Civil Liability for Structured Finance Investments;

Credit Default Swaps – Parties and Counterparties;Clawing Back Executive Pay

Richard F. ZieglerPartner

Jenner & Block LLPFormerly General Counsel, 3M Company

James M. LukendaCIRA, Managing DirectorHuron Consulting Group

Stephen L. AscherPartner

Jenner & Block LLP

The Search for Culprits and Recoveries in the Credit Crisis

13

10

19

What is a CDO?

20

General CDO Structure (All Cash)

Cash Bonds

$1,000,000,000CDO

Interest and Principal

Coupon

Securities issued by the CDO $1,000,000,000 Total

Assets held by the CDO

Tranche A3 Note: $100,000,000 A/A2Tranche B1 Note: $60,000,000 BBB+/Baa1Tranche B2 Note: $50,000,000 BBB/Baa2Tranche B3 Note: $40,000,000 BBB-/Baa3

Tranche C Note: $30,000,000 BB/Ba2Subordinated Note: $15,000,000 NR

Equity

Tranche A2 Note: $100,000,000 AA/Aa2

Tranche A1 Note: $600,000,000

AAA/Aaa

The Search for Culprits and Recoveries in the Credit Crisis

14

11

21

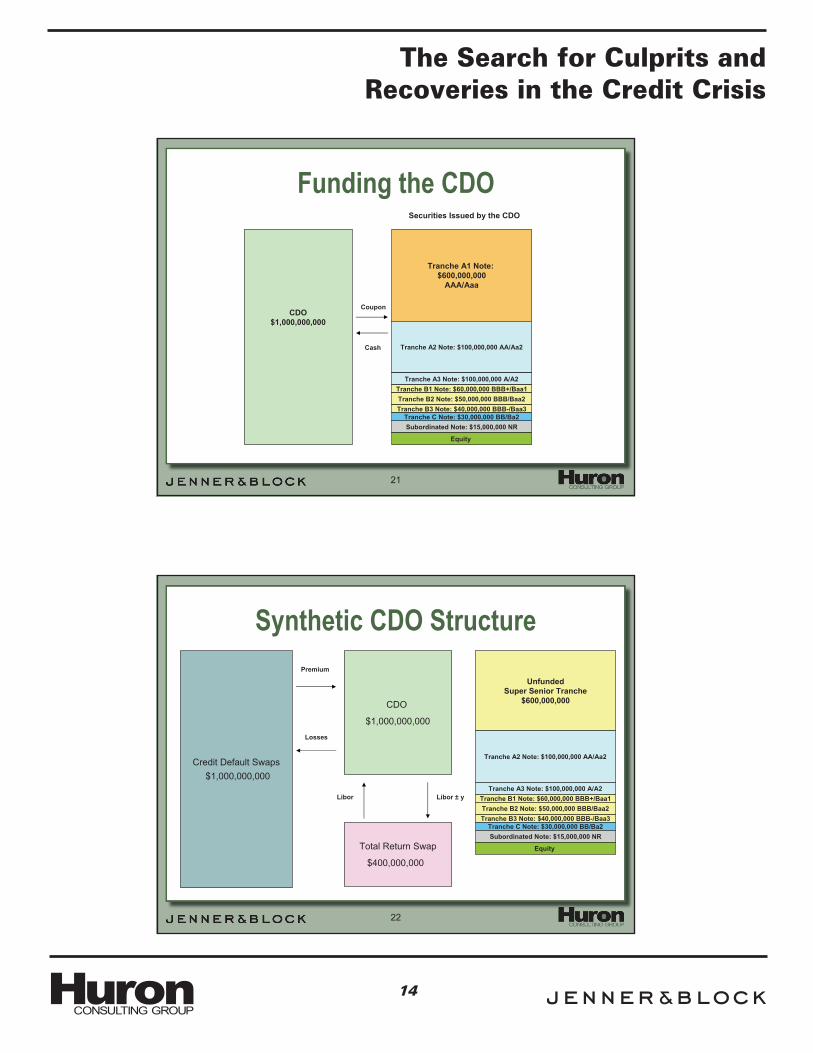

Funding the CDO

Subordinated Note: $15,000,000 NR

Tranche A1 Note: $600,000,000

AAA/Aaa

Tranche A2 Note: $100,000,000 AA/Aa2

Tranche A3 Note: $100,000,000 A/A2Tranche B1 Note: $60,000,000 BBB+/Baa1Tranche B2 Note: $50,000,000 BBB/Baa2Tranche B3 Note: $40,000,000 BBB-/Baa3

Tranche C Note: $30,000,000 BB/Ba2

Securities Issued by the CDO

Coupon

Equity

Cash

CDO$1,000,000,000

22

Synthetic CDO Structure

CDO

$1,000,000,000

Total Return Swap

$400,000,000

UnfundedSuper Senior Tranche

$600,000,000

Premium

Losses

Libor Libor ± y

Tranche A2 Note: $100,000,000 AA/Aa2

Tranche A3 Note: $100,000,000 A/A2Tranche B1 Note: $60,000,000 BBB+/Baa1

Tranche B3 Note: $40,000,000 BBB-/Baa3Tranche B2 Note: $50,000,000 BBB/Baa2

Tranche C Note: $30,000,000 BB/Ba2Subordinated Note: $15,000,000 NR

Equity

Credit Default Swaps$1,000,000,000

The Search for Culprits and Recoveries in the Credit Crisis

15

12

23

Putting It All Together: Hybrid CDO Structure

Credit Default Swap: $800,000,000

Cash Bonds: $200,000,000

Subordinated Note: $15,000,000 NR

Unfunded Super Senior Tranche: $600,000,000

AAA/Aaa

Assets held by the CDO

Tranche A2 Note: $100,000,000 AA/Aa2

Tranche A3 Note: $100,000,000 A/A2Tranche B1 Note: $60,000,000 BBB+/Baa1Tranche B2 Note: $50,000,000 BBB/Baa2Tranche B3 Note: $40,000,000 BBB-/Baa3

Tranche C Note: $30,000,000 BB/Ba2

Securities Issued by the CDO

Total Return Swap:$200,000,000

Libor + x

Premium

Losses

TRS ReferenceSecurities

Libor ± y

Libor ± yLibor

Coupon

Equity

Cash

CDO$1,000,000,000

24

CDOs: Liquidation Waterfall and Loss Distribution

Losses Erode Subordination from

Bottom Up

Recovery ispaid sequentially from Top Down

Conventional View

In a true senior/subordinated structure:

• Losses from Cash Bonds and CDS erode the tranches from the bottom up.

• Recovery from Cash Bonds and CDS pay principal sequentially from the top down.

Subordinated Note: $15,000,000 NR

Unfunded Super Senior Tranche: $600,000,000

AAA/Aaa

Tranche A2 Note: $100,000,000 AA/Aa2

Tranche A3 Note: $100,000,000 A/A2Tranche B1 Note: $60,000,000 BBB+/Baa1Tranche B2 Note: $50,000,000 BBB/Baa2Tranche B3 Note: $40,000,000 BBB-/Baa3

Tranche C Note: $30,000,000 BB/Ba2

Equity

Credit Default Swap: $800,000,000

Cash Bonds: $200,000,000

Assets held by the CDO

The Search for Culprits and Recoveries in the Credit Crisis

16

13

Recovering Credit Crisis LossesNovember 19, 2008

Credit Default Swaps-Parties and Counterparties

The Search for Culprits and Recoveries in the Credit Crisis

17

14

27

CDS-Credit Default Swaps

CDS – A Credit Default Swap is a contract in which for a series of payments from the buyer (Protection Buyer), the seller (Protection Seller) guarantees a pay-off if a credit instrument such as a bond or loan encounters a specified credit event or goes into default.

“In our view, however, derivatives are financial weapons of mass destruction, carrying dangers that, while now latent, are potentially lethal.”

Warren E. Buffett, February 2003

28

Parties and Definitions(from Derivatives Consulting Group Glossary, ISDA)

• Protection Buyer – The credit default swap counterparty that pays another counterparty to compensate them in the event that the reference entity suffers a credit event.

• Protection Seller – The credit default swap counterparty that takes on credit risk of a reference entity in return for appropriate compensation

• Reference Entity – The underlying company or Sovereign which issues the debt obligation or obligations which constitute the “reference obligation(s)” under the credit derivative.

• Reference Obligation – A bond, loan, or other payment obligation, used by the reference entity. The failure by the reference entity to comply with the material terms of a reference obligation will constitute a “credit event” under a credit derivative.

• Credit Event – An event linked to the deteriorating credit worthiness of an underlying reference entity in a credit derivative. The occurrence of a credit event usually triggers full or partial termination of the transaction and a payment from the protection seller to the protection buyer. Credit events include bankruptcy, failure to pay, restructuring, obligation acceleration, obligation default, and repudiation/moratorium.

The Search for Culprits and Recoveries in the Credit Crisis

18

15

29

CDS Uses - Hedging, Speculation, Arbitrage• Hedging: managing risk which arises from holding debt

Holder of a corporate or municipal bond hedges exposure by entering into a CDS contact as a Protection Buyer. In the event the company or municipality (Reference Entity) defaults, the payment under the CDS contract offsets all or a portion of the losses on the underlying bond. Credit Insurance.

• Speculation: unlike life insurance, there is no requirement to have an insurable interest in the Reference Entity.CDS allow investors to speculate on an entity’s credit quality by being a Protection Buyer or Protection Seller without otherwise having an interest in the Reference Obligation. Protection Buyers and Protection Sellers may also lock in gains and mitigate losses by alternatively being Protections Sellers and Protection Buyers, respectively.

• Arbitrage: CDS transactions can be utilized to execute capital structure arbitrage strategies because a Reference Entity’s stock price and its CDS spread should exhibit negative correlation.

30

The Market

• 2000 - $900 billion• 2007 - $62 trillion, an 81% increase over 2006• Mid-year 2008 - $54 trillion, a 12% decline

• But what is the underlying net value?

“In fact, the reinsurance and derivatives businesses are similar: Like Hell, both are easy to enter and almost impossible to exit.”

Warren E. Buffett, February 2003

Notional Value of CDS (source: ISDA Market Survey Data)

The Search for Culprits and Recoveries in the Credit Crisis

19

16

31

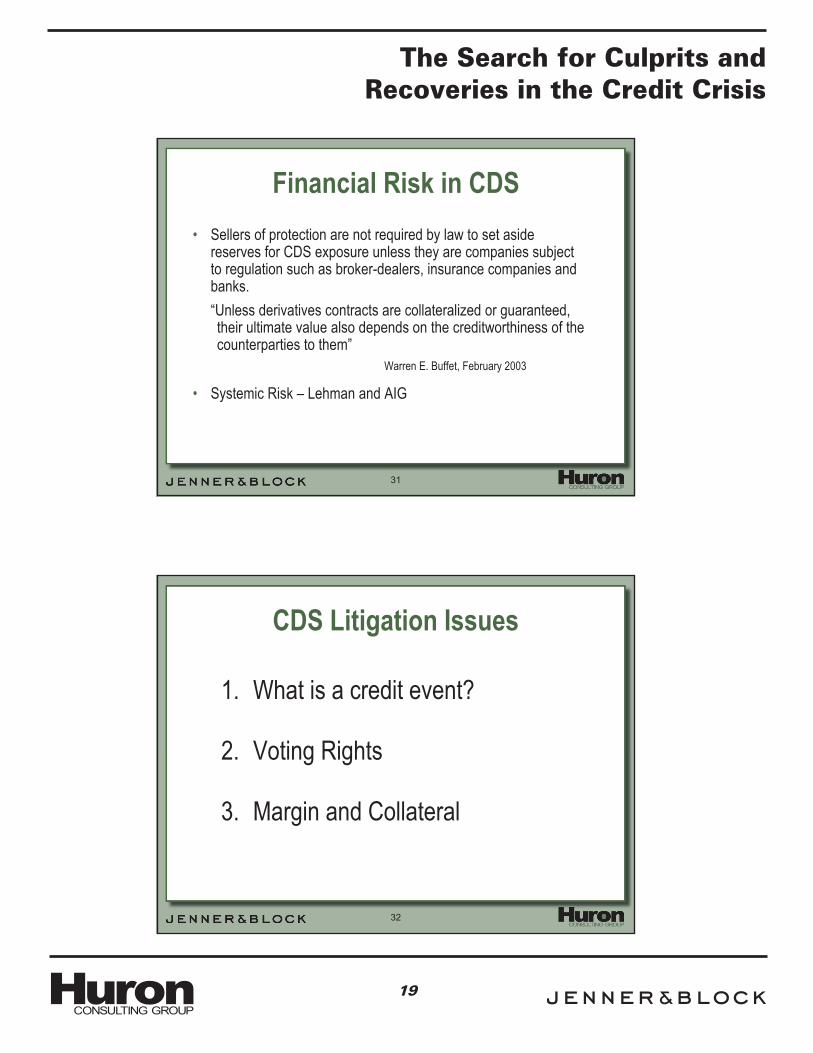

Financial Risk in CDS• Sellers of protection are not required by law to set aside

reserves for CDS exposure unless they are companies subject to regulation such as broker-dealers, insurance companies and banks.“Unless derivatives contracts are collateralized or guaranteed, their ultimate value also depends on the creditworthiness of thecounterparties to them”

Warren E. Buffet, February 2003

• Systemic Risk – Lehman and AIG

32

CDS Litigation Issues

1. What is a credit event?

2. Voting Rights

3. Margin and Collateral

The Search for Culprits and Recoveries in the Credit Crisis

20

17

33

CDO Litigation Issues

1. Controlling Party Issues

2. Waterfall Disputes

3. Liquidations

November 19, 2008

Recovering Credit Crisis Losses:Civil Liability for Structured Finance Investments;

Credit Default Swaps – Parties and Counterparties;Clawing Back Executive Pay

The Search for Culprits and Recoveries in the Credit Crisis

21

18

35

TARP’s Treasure Trove of Civil Claims:

• The “Claw back” Provisions

• The Bar on Incentivizing Excessive Risk-Taking

36

The Intense Focus on Executive Pay• Executive pay has been politicized• Rep. Waxman and AG Cuomo seeking information on all comp

above $250K and 2008 bonuses• NY Times Op-Ed: “Our Risk, Wall Street’s Reward”,

William Cohan, Nov. 16:“…where is it written in stone that bankers and traders have to

be paid millions of dollars for their services? The gibberish aboutneeding to pay that much just to keep superstars from fleeing toprivate-equity firms or hedge funds is just another Wall Street myth.The truth is most of them are lucky to have a job at all and they know it.”

The Search for Culprits and Recoveries in the Credit Crisis

22

19

37

TARP’s “Claw back” Requirement• “the Secretary shall require that the financial institution meet

appropriate standards for executive compensation and corporate governance …. [which] shall include … (B) a provision for the recovery by the financial institution of any bonus or incentive compensation paid to a senior executive officer based on statements of earnings, gains, or other criteria that are later proven to be materially inaccurate”

– TARP, § 111(b)(2)(B)

38

TARP’s “Claw back” RequirementContinued

TARP’s Claw back is Broader than Sarbanes-Oxley’s § 304:“If an issuer is required to prepare an accounting restatement due to the material noncompliance of the issuer, as a result of misconduct, with any financial reporting requirement under the securities laws, the chief executive officer and chief financial officer of the issuer shall reimburse the issuer for — any bonus or other incentive-based or equity-based compensation received by that person from the issuer during the 12-month period following the first public issuance or filing with the Commission (whichever first occurs) of the financial document embodying such financial reporting requirement; and any profits realized from the sale of securities of the issuer during that 12-month period.”

The Search for Culprits and Recoveries in the Credit Crisis

23

20

39

Comparing TARP to SOX:

During the period the Secretary of Treasury holds a meaningful equity or debt position in the company

The 12 month period following issuance of the financial statements including restatements

Claw back - Duration

Bonus or incentive compensation Any bonus or other incentive or equity based compensation

Forms of Compensation Recouped under Provision

No misconduct required – apparently strict liability

Unspecified “misconduct” in preparing financial statements

Conduct that Triggers Claw back Provision

Materially inaccurate “statements of earnings, gains, or other criteria” (performance metrics)

An accounting restatement due to the material non-compliance of the issuer with any financial reporting requirement under the securities laws

Circumstances that Trigger Claw back Provision

Financial Institution -- and derivative shareholders

SEC only -- no private right of action Standing to Enforce Claw back Provision

Senior Executive Officers of both private and public Financial Institutions in which US owns “a meaningful equity or debt position”

CEOs and CFOs of public companies who restate earnings

Individuals Subject to Claw back Provision

TARPSARBANES-OXLEY ACT

40

Comparing TARP to SOXContinued:

The Differences Noted by Treasury’s “Interim Final Rule”:• Five executives rather than Sox’s two• Private as well as public institutions• Broader triggers (not just accounting restatement), potentially

including non-financial reporting metrics• Recovery period not limited to a year

73 Fed. Reg. 62205 at 62209 (Oct. 20, 2008)The Key Differences NOT Noted in Treasury’s Interim Final Rule• No apparent scienter requirement – apparent strict liability standard• No bar on private right of action – derivative claims likelyConsequences:• Potential for Derivative Claims to Enforce Claw back

The Search for Culprits and Recoveries in the Credit Crisis

24

21

41

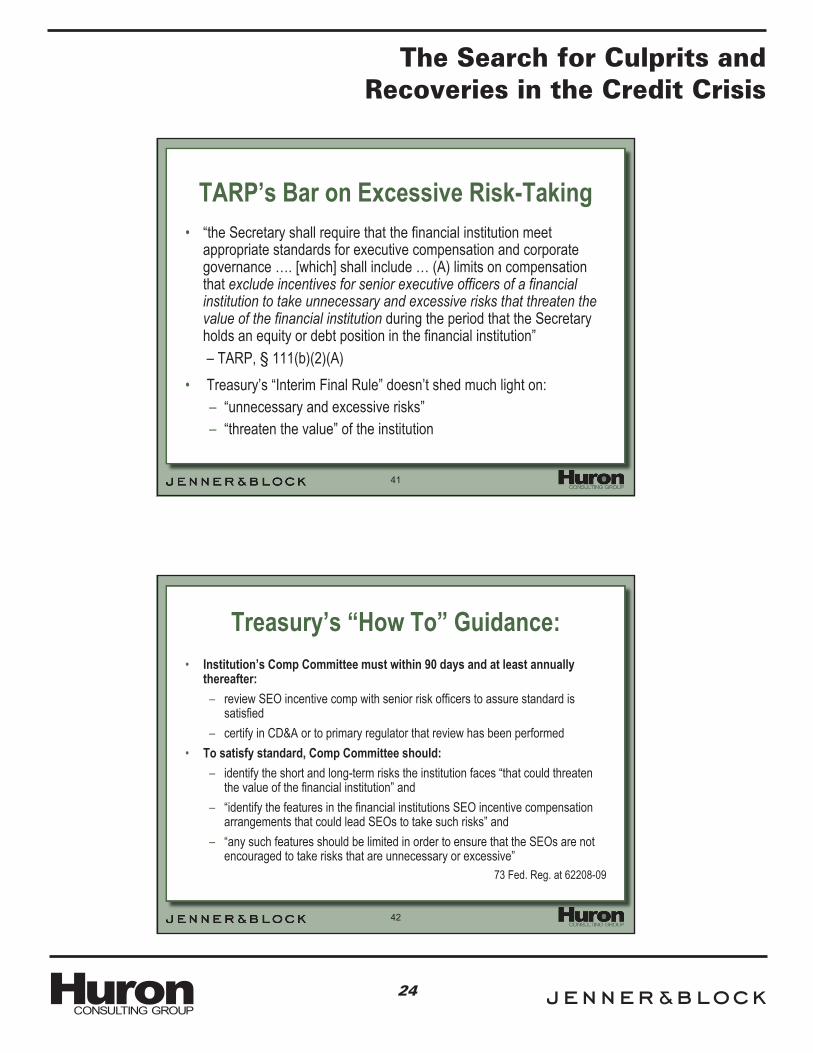

TARP’s Bar on Excessive Risk-Taking• “the Secretary shall require that the financial institution meet

appropriate standards for executive compensation and corporate governance …. [which] shall include … (A) limits on compensation that exclude incentives for senior executive officers of a financial institution to take unnecessary and excessive risks that threaten the value of the financial institution during the period that the Secretary holds an equity or debt position in the financial institution”– TARP, § 111(b)(2)(A)

• Treasury’s “Interim Final Rule” doesn’t shed much light on:– “unnecessary and excessive risks”– “threaten the value” of the institution

42

Treasury’s “How To” Guidance:• Institution’s Comp Committee must within 90 days and at least annually

thereafter:– review SEO incentive comp with senior risk officers to assure standard is

satisfied– certify in CD&A or to primary regulator that review has been performed

• To satisfy standard, Comp Committee should:– identify the short and long-term risks the institution faces “that could threaten

the value of the financial institution” and– “identify the features in the financial institutions SEO incentive compensation

arrangements that could lead SEOs to take such risks” and– “any such features should be limited in order to ensure that the SEOs are not

encouraged to take risks that are unnecessary or excessive”73 Fed. Reg. at 62208-09

The Search for Culprits and Recoveries in the Credit Crisis

25

22

43

Directors’ Exposure to Claims That TARP’s Standards Not Satisfied

• Business Judgment Rule should apply• Usual Comp Committee consultants may not be sufficient• New ideas needed – structural changes in SEO comp

– “One idea is creating escrow accounts at each firm made up of, say, one-third of each year’s allocated compensation, which would be distributed to employees over the next three years —after the account is reduced by losses resulting from poor trades or deals and legal judgments against bankers and traders resulting from their rash behavior.” Cohan Op-Ed, Nov. 16

The Search for Culprits and Recoveries in the Credit Crisis

26

Speaker Biographies

The Search for Culprits and Recoveries in the Credit Crisis

27

Stephen L. AscherPartner Jenner & Block LLPTel: 212 891-1670Fax: 212 891-1699E-mail: sascher@jenner .com

Stephen L. Ascher is a partner in Jenner & Block’s New York office. He is a member of the Firm’s Litigation Department and Securities Litigation, Business Litigation, Class Action Litigation, and White Collar Criminal Defense Practices .

Mr. Ascher’s practice focuses on claims for and against financial institutions, SEC enforcement work, and white-collar criminal matters, in addition to general commercial litigation . He has represented institutions and individuals in cases involving the antitrust laws, RICO claims, fraud and breach of fiduciary duty claims, and the securities laws . Many of those cases have gone to trial or arbitration .

Currently, Mr. Ascher is representing several financial institutions in a wide variety of disputes arising out of the ongoing crisis in the credit markets, including:

• A major financial institution in a dispute concerning billions of dollars of collateralized debt obligations, swaps, and other derivative transactions;

• The trustee for a bankrupt fund in a well-publicized dispute with its prime broker; and

• A large mortgage originator in various matters arising out of the subprime mortgage crisis .

Over the last 15 years, Mr . Ascher has regularly defended institutions and individuals in civil litigation arising out of prior front-page financial scandals, including representing:

• A Big Four accounting firm in two dozen cases alleging malpractice and fraud in connection with tax motivated transactions;

The Search for Culprits and Recoveries in the Credit Crisis

28

• Four of the underwriters in the historic World Com class action;

• Various insurance companies in billion dollar claims involving commodity derivative transactions and credit default swaps relating to Enron and Parmalat .

Mr. Ascher also frequently represents plaintiffs in significant civil litigation . For example:

• From 1999 through 2002, he was responsible for a series of lawsuits that yielded more than $400 million in settlements, including the largest recovery ever obtained by a Japanese company from a U.S. institution .

• From 2002 through 2006, Mr. Ascher represented a large European bank in $500 million claims against two major U.S. banks relating to their foreign exchange trading and prime brokerage units .

In addition, in his SEC and white-collar criminal practice, Mr. Ascher recently defended a securities trader who was indicted as part of the largest insider-trading prosecution in the last twenty years . He also represented a mutual fund executive in the first federal trial involving securities claims relating to “market-timing .” Moreover, Mr . Ascher has represented defendants accused by the SEC and the New York State Attorney General of insider trading, accounting fraud, and “late trading .” Mr . Ascher has appeared in numerous federal and New York State criminal matters, including a seven week jury trial in the Eastern District of New York .

Mr. Ascher has made a significant commitment to pro bono work . For a decade, he represented the Legal Services Corporation in matters relating to various congressional restrictions on recipients of the federal legal aid subsidy . In these matters, Mr . Ascher argued a successful appeal to the Court of Appeals for the Second Circuit and also appeared before the United States Supreme Court. In his pro bono work, Mr . Ascher has also represented more than a dozen

The Search for Culprits and Recoveries in the Credit Crisis

29

families of 9/11 victims before the federal Victims’ Compensation Fund, and a number of indigent criminal defendants pursuant to the Criminal Justice Act .

Mr . Ascher graduated from Harvard College magna cum laude in 1988 and Harvard Law School cum laude in 1991 . From 1991 to 1992, he served as a law clerk for the Honorable Jesse E . Eschbach, Senior Judge, United States Court of Appeals for the Seventh Circuit. Mr. Ascher is a member of the Bar of the United States Supreme Court, the Bar of New York State, and the Bars of several Federal courts .

The Search for Culprits and Recoveries in the Credit Crisis

30

Joseph J. Floyd Vice President, Northeast Region

P 646-277-2222 F 212-785-1313 [email protected]

1120 Avenue of the Americas, 8th Floor New York, NY 10036

Joe has worked on financial reporting engagements, special investigations, forensic accounting assignments, valuation matters and other problem solving assignments for a diverse group of industries. He has qualified as an expert and testified on accounting and financial issues in the trial courts of Massachusetts, Connecticut, and Maine, the United States District Courts in Virginia and Massachusetts and in the United States Bankruptcy Court in New York and Massachusetts. He has also appeared before the SEC to discuss and explain the underlying facts, accounting treatment and reasons for restatement, related to public company financial statement changes.

Professional experience Financial Statement Errors and Irregularities Investigations Investigated alleged accounting errors and irregularities in the financial statements of public companies. Issues under review included revenue recognition, inventory accounting, expense deferrals and other misapplications of generally accepted accounting principles. Assignments often resulted in the restatement of prior-period financial results for Securities and Exchange (SEC) registrants. Conducted interviews of responsible accounting and finance personnel. Assisted counsel with board of director, audit committee and special committee presentations related to the accounting investigation results and related matters.

Forensic Accounting and Dispute Analysis Assignments Analyzed and prepared economic damage and lost profit calculations due to alleged breach of contract and tort claims. Performed investigative accounting procedures and analysis to identify defalcation schemes. Provided expert testimony at deposition and trial on numerous occasions to describe and support the analysis and opinions.

Valuation and Financial Analysis Matters Prepared valuations for common stock and preferred stock in closely held businesses, restricted stock in publicly traded corporations, stock options, partnerships’ interests and other assets for use in estate and gift tax

planning, business transactions and planning as well as litigation proceedings. Performed numerous purchase price allocation assignments for acquisitions made by public registrants, including intangible asset and in-process research and development valuations. Assisted clients with decision making financial analyses for strategy purposes and corporate planning uses. Assignments included market research and the preparation of complex financial models and spreadsheets.

Education & certification Bachelor of Business Administration, Accounting,

University of Massachusetts at Amherst Juris Doctor, Suffolk University Law School,

Evening Division Certified Public Accountant, New York Certified Fraud Examiner Certified in Financial Forensics Earned AICPA Accreditation in Business Valuation

(ABV) Admitted to Massachusetts Bar

Professional associations American Institute of Certified Public Accountants University of Massachusetts at Amherst,

Accounting Department Advisory Council Association of Certified Fraud Examiners Named as Best Lawyers “Recommended” for

expert services in 2006 and 2007 in Best Lawyers in America

The Search for Culprits and Recoveries in the Credit Crisis

31Jlukenda_bio 10-08

James M. Lukenda Managing Director

P 646-277-2207 F 508-445-0256 [email protected]

1120 Avenue of the Americas, 8th Floor New York, NY 10036

Professional experience Jim provides assistance to clients with troubled debt restructurings, mergers, acquisitions and dispositions, litigation and claims analysis, fraud investigations, and other financial consulting and bankruptcy assignments.

His experience spans numerous industry categories including the heavy manufacturing, retailing, electronics, consumer products and distribution, construction and contracting, communications and publishing, real estate, and hospitality industries.

Jim’s extensive bankruptcy and restructuring experience includes: preparation for and providing expert testimony on issues

of business plans, liquidations, avoidance actions, substantive consolidation, and other reorganization and bankruptcy issues;

development and evaluation of strategic business plans on behalf of debtors and creditors including the evaluation of customer and product profitability, store and plant profitability, overhead structure, and industry viability;

analysis for providing expert testimony on business performance, lost profits, and underlying claims for damages;

preparation and evaluation of valuation reports including enterprise value and liquidation analyses;

negotiation and evaluation of terms of plans of reorganization and underlying post confirmation documents and covenants;

negotiation and evaluation of out-of-court debt restructuring proposals;

negotiation and evaluation of asset and going concern business sales in connection with representation of non-U.S. administrators and receivers;

evaluation of alternative liquidation plans for cessation of business for non-U.S. parent;

providing technical and operational support for liquidation and creditor distribution trustees in handling proofs-of-claim, reserve requirements, taxes, and distributions;

serving as technical advisor to engagement teams on financial and accounting issues regarding "fresh start" reporting and post-petition and post-confirmation accounting.

Representative Restructuring Engagements

Northwest Airlines, Inc.- Debtors The 1031 Tax Group, LLC – Chief Restructuring Officer The Delaco Company – Chief Restructuring Officer and

President of the reorganized company Warnaco - Official Committee of Unsecured Creditors Bradlees Stores, Inc. - Debtors Hillsborough Holdings Corporation - Official Bondholders

Committee Conran's - Advisor to Board of Directors JWP Inc. - Bonding Surety Lomas Mortgage USA, Inc. - Acquirer of Mortgage

Portfolio Olympia & York - Committee of Tower B Bondholders Petrie Retail, Inc. - Equity Investors and DIP Lender Phar-Mor, Inc. - Chapter 11 Acquirer Pocket Communications, Inc. - Debtors Global Crossing - Debtors Robert Maxwell Group - Joint Administrators

Education & certification BSBA, cum laude, Georgetown University School of

Business Administration Certified Public Accountant (New Jersey and New

York) Certified Insolvency and Restructuring Advisor

Professional associations Association of Insolvency & Restructuring Advisors

(AIRA) - Board of Directors (1992 – present), President (2002-2003), Chairman (2004-2005)

INSOL – Board of Directors (1999-2003) Association for Corporate Growth, NJ Chapter Member – American Institute of Certified Public

Accountants

Volunteer Associations Member & Treasurer – Adoptive Parents

Committee NJ Chapter Member - Montclair Cooperative School, Audit

Committee

The Search for Culprits and Recoveries in the Credit Crisis

32

Thomas C. NewkirkPartnerJenner & Block LLPTel: 202 639-6099Fax: 202 661-4926E-mail: tnewkirk@jenner .com

Thomas C. Newkirk is a partner in Jenner & Block’s Washington, DC office. He is a Co-Chair of the Firm’s Securities Litigation Practice and a member of its Corporate, White Collar Criminal Defense and Counseling, and Securities Practices. Mr. Newkirk is AV Peer Review Rated, Martindale-Hubbell’s highest peer recognition for ethical standards and legal ability .

Since joining Jenner & Block in 2004, Mr. Newkirk has represented some of America’s largest companies, chief executive officers, other senior officers, corporate boards, board committees and directors in confidential investigations involving a wide range of issues, including accounting, disclosure, insider trading, and the Foreign Corrupt Practices Act . He has counseled corporate boards and board commmittees with respect to corporate governance, compliance, conducted internal investigations and defended private securities-related litigation .

Before joining Jenner & Block, Mr. Newkirk was a senior official with the U.S. Securities and Exchange Commission for nineteen years. For the last eleven years, he was an Associate Director of the Division of Enforcement, and led the investigations of some of the U.S. Securities and Exchange Commission’s most significant cases.

Some of the landmark SEC cases he directed include:

• SEC v. Time Warner Inc. (formerly known as AOL Time Warner), a financial fraud case alleging that the Company overstated online advertising revenue and the number of its Internet subscribers, and aided and abetted three other companies’ securities frauds .

• In the Matter of The Walt Disney Company, a case charging Disney for failing to disclose certain related party transactions between Disney and its directors, and for failing to disclose certain compensation paid to a Disney director .

The Search for Culprits and Recoveries in the Credit Crisis

33

• SEC v. Wachovia Corporation, a case concerning proxy disclosure and reporting violations arising out of the merger between First Union Corporation and legacy Wachovia Corporation.

• SEC v. Koninklijke Ahold N.V. (Royal Ahold), financial fraud cases against Royal Ahold, several former officers and directors of Ahold, and several former officers of Ahold’s U.S. Foodservice subsidiary for overstating earnings by $829 million and overstating revenues by $30 billion for the years 2000 – 2002 .

• In the Matter of PNC Financial Services Group, Inc., and SEC v. American International Group Inc., financial fraud cases involving the misuse of special purpose entities devised by AIG to boost earnings and remove $762 million of troubled assets from PNC’s balance sheet .

• The Tyco International Ltd. matter, including SEC v. Dennis Kozlowski et al., SEC v. Frank Walsh, a former Tyco director, and In the Matter of Richard P. Scalzo, Jr, CPA, Tyco’s former independent auditor .

• SEC v. Arthur Andersen LLP et al., a case against the firm and several partners for their improper audits of Waste Management Inc .

• In the Matter of Sunbeam Corporation and SEC v. Albert J. Dunlap et al., cases against the firm and former top officers for inflating earnings through the use of cookie jar reserves and other improprieties; In the Matter of Phillip E. Harlow, CPA, a related case against Sunbeam’s outside auditor for improper professional conduct .

• In the Matter of Cendant Corporation and nine related actions, cases involving fraud or other charges against the firm and former officers for overstating earnings and related charges against two outside auditors for aiding and abetting Cendant’s reporting violations .

The Search for Culprits and Recoveries in the Credit Crisis

34

• In the Matter of The Dreyfus Corporation, a case involving mutual fund misallocation of investment opportunities .

• SEC v. Rhino Advisor, Inc., a “death spiral” convertible security manipulation case against Rhino Advisors, Inc . and others .

• SEC v. Prudential Securities, Inc., a case in which the Commission obtained restitution of almost one billion dollars for investors defrauded in the sale of limited partnerships .

• In the Matter of Gruntal & Co. Incorporated, a broker-dealer case concerning misappropriating escheat funds .

• In the Matter of Certain Activities of Options Exchanges, a case involving the failure of certain options exchanges to compete in the listing of options and to police their own markets .

From 1986 to 1992, Mr. Newkirk served as the SEC Enforcement Division’s Chief Litigation Counsel . The cases he directed include the Commission’s litigation against Drexel Burnham Lambert and Michael Milken, SEC v. Drexel Burnham Lambert and Michael Milken, First Jersey, SEC v. First Jersey Securities Inc and Robert E. Brennan, and Eddie “Crazy Eddie” Antar, SEC v. Eddie Antar et al., and many emergency relief cases to halt ongoing frauds and freeze the proceeds of insider trading .

During the late 1970’s and early 1980’s, Mr . Newkirk was the Deputy General Counsel of the U.S. Department of Energy, where he helped secure two of the largest judgments ever collected by the government in U.S. v. Exxon, $2 billion and In re Dept. of Energy Stripper Well Litigation, $1 billion. Previously he was a Senior Attorney in the Office of Legal Counsel in the U.S. Department of Justice, an Assistant Counsel for the U.S. Senate’s Securities Industry Study, and an associate in a major “Wall Street” law firm.

He writes and lectures frequently on SEC enforcement matters.

The Search for Culprits and Recoveries in the Credit Crisis

35

Mr . Newkirk received numerous awards during his government service including two Presidential Meritorious Executive Awards, the SEC Chairman’s Award for Excellence, the SEC’s Law and Policy Award, the SEC’s Capital Markets Award, the SEC’s Distinguished Service Award, the Commission’s highest honor, the Secretary of Energy’s Outstanding Service Award and the Secretary of Energy’s Exceptional Service Award. In 2008, Legal Times named him one of seven “Leading Lawyers” in the area of Corporate Governance (Internal Investigations) on the basis of his accomplishments in private practice .

Mr. Newkirk graduated in 1966 from Cornell Law School, Order of the Coif, Phi Kappa Phi and with distinction . He was a member of the Cornell Law Review’s Board of Editors . He received his B .A . from the College of Arts and Sciences, Cornell University, in 1964.

Mr . Newkirk is admitted to practice in the District of Columbia and New York. He serves on the Federal Bar Association’s Securities Law Committee, Executive Council and he is a member of the American Bar Association .

The Search for Culprits and Recoveries in the Credit Crisis

36

Andrew WeissmannPartnerJenner & Block LLPTel: 212 891-1650Fax: 212 891-1699E-mail: aweissmann@jenner .com

Andrew Weissmann is a partner in Jenner & Block’s New York office and a member of the Firm’s White Collar Criminal Defense and Counseling Practice . He is joined in that practice by eighteen former federal prosecutors and SEC attorneys.

Mr. Weissmann is a nationally-recognized white collar litigator, and in 2007 he was named one of the 100 Most Influential People in Business Ethics by Ethisphere magazine. He represents U.S. and foreign corporations and executives in connection with criminal and civil investigations, including representation before the Department of Justice, the Securities and Exchange Commission, and state and local authorities. Mr. Weissmann was also appointed by two federal courts to serve as a Special Master overseeing gun dealers that had been sued by the City of New York as part of its effort to curtail the flow of illegal firearms into the City. He also is a member of the board of Manhattan Legal Services.

Mr. Weissmann joined Jenner & Block after serving as the Director of the Enron Task Force, the Chief of the Criminal Division of the United States Attorney’s Office for the Eastern District of New York, and the Special Counsel to the Director of the Federal Bureau of Investigation. As Enron Task Force Director, Mr. Weissmann oversaw the prosecution of more than 30 individuals in connection with the company’s collapse, including the indictments of Kenneth Lay, Jeffrey Skilling and Andrew Fastow.

Previously, Mr. Weissmann served as Chief of the Criminal Division in the U.S. Attorney’s Office for the Eastern District of New York where he supervised over 110 prosecutors. Mr. Weissmann oversaw a wide array of white collar crime investigations involving, among others, securities, FCPA, health care, environmental, computer crime and tax fraud. In addition, Mr. Weissmann personally prosecuted dozens of corrupt brokers and short sellers for stock market manipulation .

The Search for Culprits and Recoveries in the Credit Crisis

37

An experienced jury trial lawyer, Mr. Weissmann successfully tried more than 25 cases, including major racketeering prosecutions . Those included the successful prosecution of the boss of the Genovese Crime Family, Vincent Gigante, who had feigned mental illness for years, as well as scores of leaders and members of the Gambino and Colombo families. Mr. Weissmann was also selected by the Director of the Federal Bureau of Investigation to be his Special Counsel, where he worked on a variety of confidential national security matters .

Mr. Weissmann has written and lectured widely on compliance and other white collar matters, speaking in the U.S. and overseas to private and public companies, boards of directors, professional associations, conferences and law schools. Mr. Weissmann recently took a leadership role in originating, writing, and editing The Ethics and Compliance Handbook: A Practical Guide for Leading Organizations, a first-of-its-kind resource published by the Ethics and Compliance Officer Association which aims to create an industry-wide standard for ethics and compliance programs . He has also been an adjunct professor of law and clinical professor at Fordham Law School and Brooklyn Law School.

Mr. Weissmann graduated from Columbia Law School as a Harlan Fiske Stone Scholar. At Columbia, he received the Negroni Award and was on the Managing Board of the Columbia Law Review . Mr. Weissmann earned his bachelor of arts degree, magna cum laude, from Princeton University where he received the Walter Phelps Hall Senior Thesis Prize and a European Cultural Studies Certificate. He also attended graduate school on a Fulbright Fellowship at the University of Geneva. Mr. Weissmann is admitted to the Bars of the U.S. Supreme Court, the U.S. Court of Appeals for the Second Circuit and the U.S. District Courts of the Eastern District and the Southern District of New York .

The Search for Culprits and Recoveries in the Credit Crisis

38

Congressional Testimony

• Prosecutorial Authority to “Preserve Assets” for Restitution, Written and Oral Testimony, United States House Judiciary Committee’s Subcommittee on Crime, Terrorism, and Homeland Security (April 3, 2008)

• Examining Approaches to Corporate Fraud Prosecutions and the Attorney-Client Privilege Under the McNulty Memorandum, Written and Oral Testimony, United States Senate Committee on the Judiciary (September 18, 2007)

• The McNulty Memo’s Effect on the Right to Counsel in Corporate Investigations, Written and Oral Testimony, United States House of Representatives Subcommittee on Crime, Terrorism, & Homeland Security of the Committee of the Judiciary (March 8, 2007)

• The Thompson Memorandum’s Effect on the Right to Counsel in Corporate Investigations, Written and Oral Testimony, United States Senate Committee on the Judiciary (September 12, 2006)

Representative Speaking Engagements

• 9th Annual Legal Reform Summit, U.S. Chamber Institute for Legal Reform, Washington, DC (October 29, 2008)

• Keynote Speech at the Conseil Constitutionnel, Global Council for Business Ethics and Aspen Institute–France, Paris, France (October 23, 2008)

• Conference on Cross Border Investigations, Cercle Montesquieu, Paris, France (October 22, 2008)

• The Second Annual Capital Markets Summit: Strengthening U.S. Capital Markets for All Americans, U.S. Chamber of Commerce Center for Capital Markets Competitiveness, Washington, DC (March 26, 2008)

The Search for Culprits and Recoveries in the Credit Crisis

39

• The Lengthening Arm of Criminal Law: Criminalization of Corporate Conduct, The Chatham House City Series, London, England (November 30, 2007)

• Legal Reform Solutions Summit, Civil Justice Reform Group, Chicago (July 17, 2007)

• Securities Law Symposium, Bloomberg, CLE Institute, New York County Lawyers’ Association, New York (June 29, 2007)

• SuperConference 2007, The Changing Privilege Landscape, InsideCounsel, Chicago (May 15, 2007)

• Sponsoring Partner Forum, Ethics and Compliance Officers Association, Weston, Florida (April 18, 2007)

• 11th Annual Corporate Counsel Institute, GeorgetownCLE, Washington, DC (March 8-9, 2007)

• Enron: The Lay/Skilling Trial — A Case Study, Edward Bennett Williams Inn of the American Inns of Court Pupilage Group, Washington, DC (November 16, 2006)

• Corporate Fitness for Crisis, PricewaterhouseCoopers and the University of Delaware Directors’ College, Newark (November 15-17, 2006)

• Conducting Forensic Investigations Conference, American Conference Institute, New York (December 5-6, 2006)

• Seventh Annual Fall Bench & Bar Retreat, The Federal Bar Council, Lenox (October 27-29, 2006)

• The Future of the Thompson Memorandum, New York City Bar Association, New York (October 16, 2006)

The Search for Culprits and Recoveries in the Credit Crisis

40

• Lecture and Seminar With Law and Government Students Regarding Criminal Prosecutions, Harvard Law School & Kennedy School of Government, Cambridge (October 12, 2006)

• Federal Prosecution of Corporations: The Effect of U.S. v. Stein on DOJ and SEC Policies, Ethics & Compliance Officer Association, New York (August 9, 2006)

• What the Government Expects From Ethics and Compliance Programs, Ethics and Compliance Officer Association, Washington, DC, (December 13, 2005)

• 19th Annual National Institute on White Collar Crime 2005, American Bar Association Conference, Las Vegas (March 2-4, 2005)

• Obstruction of Justice and White Collar Prosecutions, American Society of Corporate Secretaries, Salt Lake City (June 3, 2003)

• Lessons from the Arthur Andersen Case, National Association of Securities Dealers National Meeting, Washington DC (October 2, 2002)

Available Publications:

• “Nonprosecution Agreements: They are useful devices,” The National Law Journal, May 5, 2008

• Client Advisory: H.R. 4110 — Proposed Increases in Prosecutorial Authority to Restrain Assets Pre- and Post-Indictment, April 4, 2008

• Prosecutorial Authority to “Preserve Assets” for Restitution, Written and Oral Testimony, United States House Judiciary Committee’s Subcommittee on Crime, Terrorism, and Homeland Security, April 3, 2008

• “A Smear By Any Other Name,” Legal Times, Vol . XXX, No . 47, Novmeber 19, 2007

The Search for Culprits and Recoveries in the Credit Crisis

41

• Client Alert: Managing Risks Arising From the Credit Crisis, November 15, 2007

• “‘Brady’: Second Circuit Upends Prosecutorial Practice,” New York Law Journal, November 6, 2007

• “Fighting governmental efforts to limit defense access to evidence,” Midwest In-House, October 2007

• “Examining the Current Corporate Charging Policies of the Justice Department,” Privacy & Data Security Law Journal, September 2007

• Examining Approaches to Corporate Fraud Prosecutions and the Attorney-Client Privilege Under the McNulty Memorandum, Written and Oral Testimony, United States Senate Committee on the Judiciary, September 18, 2007

• Client Advisory: District Court Dismisses Charges Against 13 Former KPMG Employees, July 23,2007

• “Rethinking Criminal Corporate Liability,” Indiana Law Journal, Vol . 82, No. 2, Spring 2007

• “White-Collar Defendants and White-Collar Crimes,” 116 The Yale Law Journal Pocket Part 286, (2007)

• Client Advisory: Second Circuit Rejects Ancillary Jurisdiction in Fee Indemnification Claim Against KPMG, June 5, 2007

• The McNulty Memo’s Effect on the Right to Counsel in Corporate Investigations, Written and Oral Testimony, United States House of Representatives Subcommittee on Crime, Terrorism, & Homeland Security of the Committee of the Judiciary, March 8, 2007

• “The McNulty Memorandum,” The National Law Journal, February 5, 2007

The Search for Culprits and Recoveries in the Credit Crisis

42

• “Thompson Gunners: DOJ vs. The Senate Judiciary Committee — The New Rules On How To Indict Corporations,” The Deal, January 29, 2007

• Client Advisory: DOJ Replaces Thompson Memorandum with McNulty Memorandum, December 15, 2006

• Client Advisory: Congressional Scrutiny of the Thompson Memo, October 2006

• “Perspectives on Compliance Programs: The Enron Verdict” Law Journal Newsletters – The Corporate Compliance & Regulatory Newsletter, Vol . 4, No . 1, October 2006

• The Thompson Memorandum’s Effect on the Right to Counsel in Corporate Investigations, Written and Oral Testimony, United States Senate Committee on the Judiciary, September 12, 2006

• “No Choice: It’s Time to Reverse The DOJ’s ‘Principles of Federal Prosecution of Business Organizations’,” The Deal, August 7, 2006

• Client Advisory: United States v. Stein, July 28, 2006

• Client Advisory: District Court Rules the Government’s Use of the Threat of Corporate Indictment Was Unconstitutional, July 2006

• “Obstruction for Data Destruction After ‘Andersen,’” New York Law Journal, Vol . 235, No . 110, June 8, 2006

• “Think of the Corporate Office As a Potential Crime Scene?” New York Law Journal, May 30, 2006

• “Sexual Equality Under the Pregnancy Discrimination Act,” Columbia Law Review, 83 Col . L . Rev . 690, (1983)

The Search for Culprits and Recoveries in the Credit Crisis

43

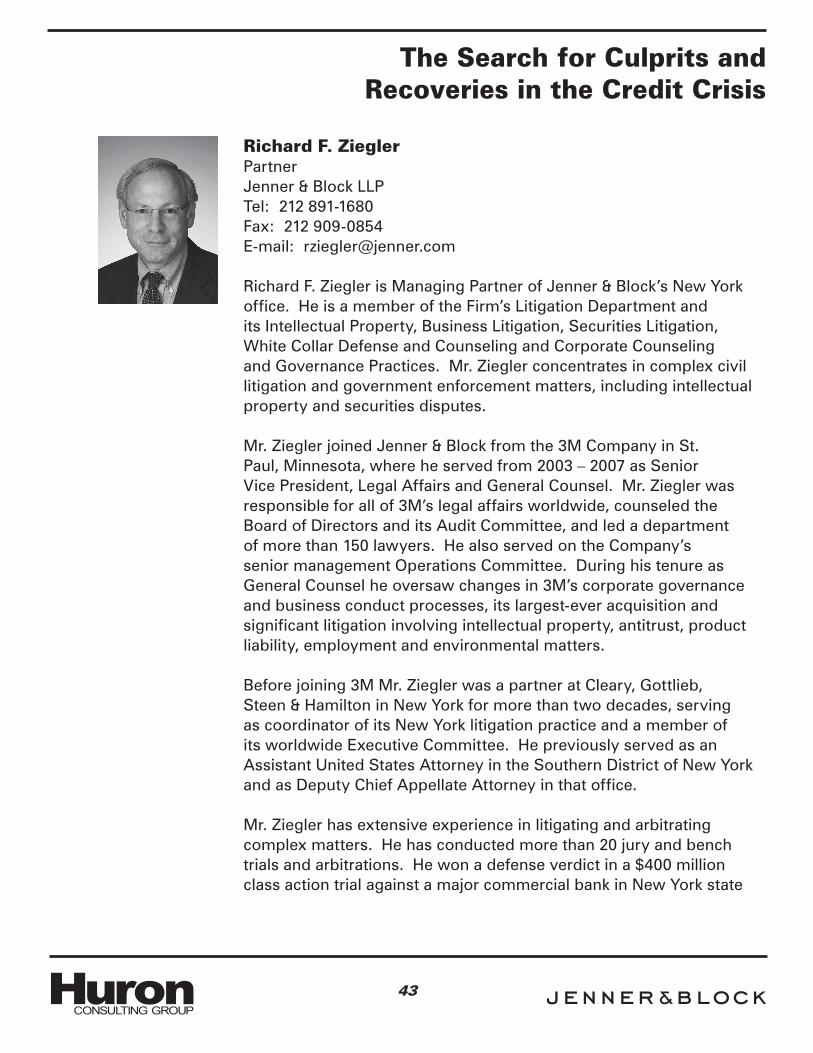

Richard F. ZieglerPartnerJenner & Block LLPTel: 212 891-1680Fax: 212 909-0854E-mail: rziegler@jenner .com

Richard F. Ziegler is Managing Partner of Jenner & Block’s New York office. He is a member of the Firm’s Litigation Department and its Intellectual Property, Business Litigation, Securities Litigation, White Collar Defense and Counseling and Corporate Counseling and Governance Practices. Mr. Ziegler concentrates in complex civil litigation and government enforcement matters, including intellectual property and securities disputes .

Mr. Ziegler joined Jenner & Block from the 3M Company in St. Paul, Minnesota, where he served from 2003 – 2007 as Senior Vice President, Legal Affairs and General Counsel. Mr. Ziegler was responsible for all of 3M’s legal affairs worldwide, counseled the Board of Directors and its Audit Committee, and led a department of more than 150 lawyers . He also served on the Company’s senior management Operations Committee . During his tenure as General Counsel he oversaw changes in 3M’s corporate governance and business conduct processes, its largest-ever acquisition and significant litigation involving intellectual property, antitrust, product liability, employment and environmental matters .

Before joining 3M Mr. Ziegler was a partner at Cleary, Gottlieb, Steen & Hamilton in New York for more than two decades, serving as coordinator of its New York litigation practice and a member of its worldwide Executive Committee . He previously served as an Assistant United States Attorney in the Southern District of New York and as Deputy Chief Appellate Attorney in that office.

Mr. Ziegler has extensive experience in litigating and arbitrating complex matters . He has conducted more than 20 jury and bench trials and arbitrations . He won a defense verdict in a $400 million class action trial against a major commercial bank in New York state

The Search for Culprits and Recoveries in the Credit Crisis

44

court and represented another major financial institution in its $600 million resolution of federal criminal charges and related civil claims in the Southern District of New York. He has handled numerous SEC investigations .

Mr. Ziegler also has substantial experience in patent litigation, having won the Federal Circuit’s en banc ruling in Honeywell v. Hamilton Sundstrand . His other notable victories include landmark rulings in which the Delaware Supreme Court, en banc, clarified the scope of directors’ immunity from monetary damages for disclosure violations (Arnold v. Society for Savings), the Second Circuit changed the limitations period in securities actions (Ceres Partners v. GEL Associates), the Eighth Circuit determined criteria for vicarious liability under the RICO statute (Tonka v. Luthi ), and the New York Court of Appeals clarified the law of tortious interference with contract in the merger context (NBT Bancorp v. Fleet/Norstar) .

Mr. Ziegler was Chairman of the Committee on Professional Responsibility of the New York State Bar Association. He has taught a seminar on ethics and complex litigation at Columbia Law School and has been a member of the faculty of the trial advocacy program at Cardozo Law School. He also serves on the Board of Trustees of the William Mitchell College of Law in St. Paul and chaired the school’s Audit & Finance Committee .

Mr. Ziegler has frequently appeared as a speaker at professional conferences and has co-chaired the Annual General Counsel Conference and PLI’s Corporate Counsel Institute, both in New York . He has written for The National Law Journal and other professional publications .

Mr. Ziegler graduated from Yale College summa cum laude in 1971, where he became a member of Phi Beta Kappa . He received his J.D. from Harvard Law School magna cum laude in 1975 and was an editor of the Harvard Law Review. Mr. Ziegler also clerked for Federal District Court Judge Milton Pollack in Manhattan . He is a member of the bar of New York and Minnesota, the United States Supreme Court and numerous federal circuit and district courts .

The Search for Culprits and Recoveries in the Credit Crisis

45

Recent Speaking Engagements:

• Co-Chair, Corporate Counsel Institute 2008, Practising Law Institute, New York, September, 2008

• Comparing the Proposed New York Rules of Professional Conduct to the ABA Model Rules of Professional Conduct: A Business Law Perspective, American Bar Association 2008 Annual Meeting, New York, August, 2008

• An In-House Perspective on Professional Responsibility, Eighth Annual SuperConference, InsideCounsel and Jenner & Block, Chicago, May, 2008

• Chair, Setting the Tone: New Techniques for Driving Effective Compliance Programs, Corporate Secretary East Coast Think Tank, New York, May, 2008

• Evaluating and Managing FCPA and Internal Controls Risk in M&A Transactions, Twentieth Annual Corporate Law Institute, Tulane University Law School, New Orleans, April, 2008

• The Next Generation in Corporate Compliance, Securities Litigation & Compliance Seminar, Jenner & Block, Navigant Consulting, Inc., and PricewaterhouseCoopers, Chicago, October, 2007

• General Counsel Panel, 2007 Hedge Fund General Counsel Summit, American Lawyer Media, Greenwich, September, 2007

• Co-Chair, Corporate Counsel Institute 2007, Practising Law Institute, New York, September, 2007

• Conducting an Internal Investigation, General Counsel Panel, Minnesota State Bar Association, Minneapolis, December, 2006

• Beyond Law and Compliance: Creating Ethical Cultures in the 21st Century, Center for Ethical Business Cultures/University of St. Thomas Law School, Minneapolis, November, 2006

The Search for Culprits and Recoveries in the Credit Crisis

46

• Co-Chair, The 18th Annual General Counsel Conference, Corporate Counsel Magazine, New York, June, 2006

• Crossing Borders, Second General Counsel Roundtable, Economist Conferences, New York, December, 2004

• Commercial Litigation, Hennepin County Bar Association CLE program, Minneapolis, October, 2004

• Perspectives on the Sarbanes-Oxley Act, Cleary Gottlieb Symposium, New York, February, 2004

• Policing the Profession: The Changing Landscape of Lawyer Regulation, Dorsey & Whitney Corporate Counsel Symposium XIV, Minneapolis, November, 2003

• Chair, Ethics Fundamentals for Experienced and Newly-Admitted Lawyers, New York State Bar Association, New York City and three other cities, Fall, 2000

The Search for Culprits and Recoveries in the Credit Crisis

47

Jenner & Block Client Alert: Managing Risks Arising From the Credit Crisis

The Search for Culprits and Recoveries in the Credit Crisis

48

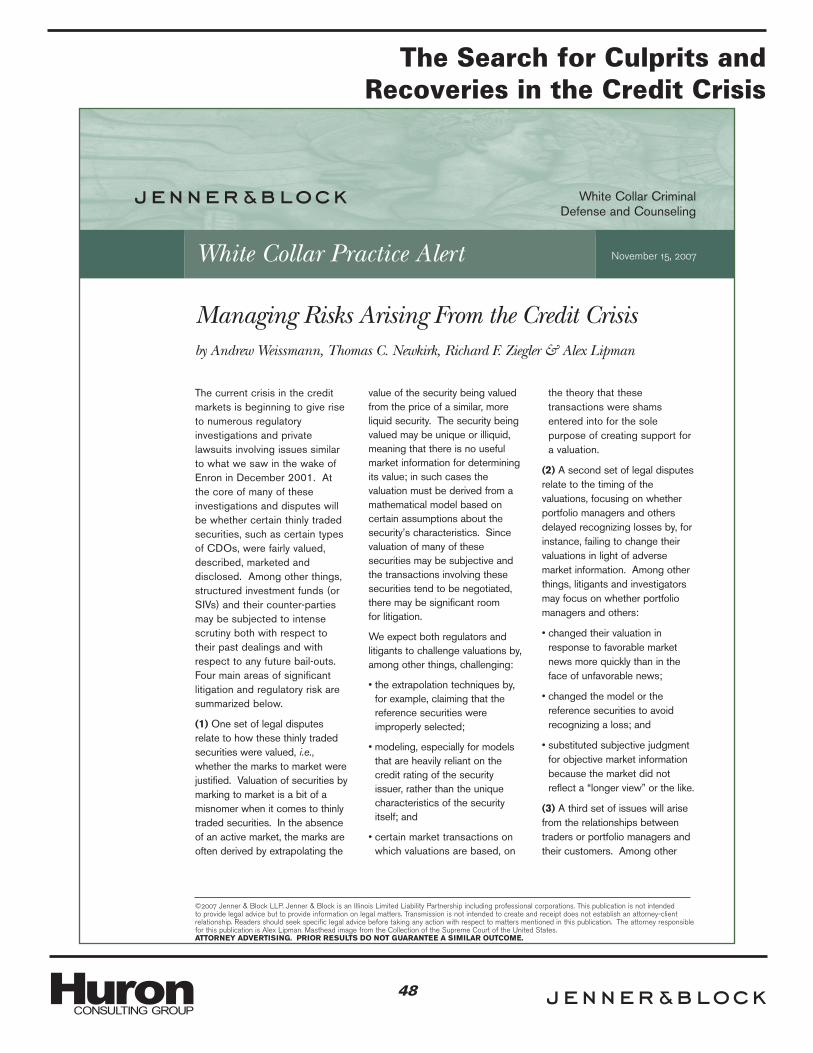

White Collar Practice Alert

Managing Risks Arising From the Credit Crisisby Andrew Weissmann, Thomas C. Newkirk, Richard F. Ziegler & Alex Lipman

White Collar Criminal Defense and Counseling

November 15, 2007

The current crisis in the creditmarkets is beginning to give riseto numerous regulatoryinvestigations and privatelawsuits involving issues similarto what we saw in the wake ofEnron in December 2001. Atthe core of many of theseinvestigations and disputes willbe whether certain thinly tradedsecurities, such as certain typesof CDOs, were fairly valued,described, marketed anddisclosed. Among other things,structured investment funds (orSIVs) and their counter-partiesmay be subjected to intensescrutiny both with respect totheir past dealings and withrespect to any future bail-outs.Four main areas of significantlitigation and regulatory risk aresummarized below.

(1) One set of legal disputesrelate to how these thinly tradedsecurities were valued, i.e.,whether the marks to market werejustified. Valuation of securities bymarking to market is a bit of amisnomer when it comes to thinlytraded securities. In the absenceof an active market, the marks areoften derived by extrapolating the

value of the security being valuedfrom the price of a similar, moreliquid security. The security beingvalued may be unique or illiquid,meaning that there is no usefulmarket information for determiningits value; in such cases thevaluation must be derived from amathematical model based oncertain assumptions about thesecurity’s characteristics. Sincevaluation of many of thesesecurities may be subjective andthe transactions involving thesesecurities tend to be negotiated,there may be significant room for litigation.

We expect both regulators andlitigants to challenge valuations by,among other things, challenging:

• the extrapolation techniques by,for example, claiming that thereference securities wereimproperly selected;

• modeling, especially for modelsthat are heavily reliant on thecredit rating of the securityissuer, rather than the uniquecharacteristics of the securityitself; and

• certain market transactions onwhich valuations are based, on

the theory that thesetransactions were shamsentered into for the solepurpose of creating support fora valuation.

(2) A second set of legal disputesrelate to the timing of thevaluations, focusing on whetherportfolio managers and othersdelayed recognizing losses by, forinstance, failing to change theirvaluations in light of adversemarket information. Among otherthings, litigants and investigatorsmay focus on whether portfoliomanagers and others:

• changed their valuation inresponse to favorable marketnews more quickly than in theface of unfavorable news;

• changed the model or thereference securities to avoidrecognizing a loss; and

• substituted subjective judgmentfor objective market informationbecause the market did notreflect a “longer view” or the like.

(3) A third set of issues will arisefrom the relationships betweentraders or portfolio managers andtheir customers. Among other

©2007 Jenner & Block LLP. Jenner & Block is an Illinois Limited Liability Partnership including professional corporations. This publication is not intended to provide legal advice but to provide information on legal matters. Transmission is not intended to create and receipt does not establish an attorney-client relationship. Readers should seek specific legal advice before taking any action with respect to matters mentioned in this publication. The attorney responsiblefor this publication is Alex Lipman. Masthead image from the Collection of the Supreme Court of the United States. ATTORNEY ADVERTISING. PRIOR RESULTS DO NOT GUARANTEE A SIMILAR OUTCOME.

The Search for Culprits and Recoveries in the Credit Crisis

49

2

things, the focus here will be onwhether:

• customers were fully informedabout the nature and the risks ofindividual securities or securitiesportfolios;

• customers had in fact agreed topurchase the securities in theiraccounts;

• traders parked troubled securitieswith customers by agreeing to re-purchase them at a guaranteedprice to avoid taking a loss;

• traders re-purchased securitiesfrom favored clients at inflatedprices in order to help clientsavoid losses; and

• market participants engaged intransactions for the sole purpose

of creating the appearance of anactive market to support theirmarks.

(4) Finally, all of these issuesimpact earnings disclosures bypublic companies, such as banksand other large financialinstitutions, as well as earningsand valuation disclosures toinvestors of hedge funds or mutualfunds. In this regard, it is safe toexpect a panoply of securitiesfraud, books and records, andother related claims andinvestigations focusing on thetiming and nature of disclosures oflosses or expected losses.Significant attention will be on:

• whether earnings reported inpast periods were inflatedbecause the mark to market (or

The authors have significant experience with the issues identified in this Alert. Mr. Weissmann is the former Director ofDOJ’s Enron Task Force. Mr. Newkirk is the former Associate Director of the SEC’s Division of Enforcement. Mr. Zieglerrecently joined Jenner & Block from the 3M Company in St. Paul, Minnesota, where he served from 2003 – 2007 asSenior Vice President, Legal Affairs and General Counsel. Mr. Lipman worked on the Enron matter as a Branch Chief atthe SEC’s Division of Enforcement.

With 18 former federal prosecutors and senior SEC enforcement attorneys among the more than 50 partners in ourSecurities Litigation and White Collar Criminal Defense and Counseling groups, we bring a wealth of experience to alllegal matters involving allegations of financial fraud: internal investigations, Department of Justice and SEC proceedings,class action and derivative shareholder litigation, and insurance coverage disputes.

November 15, 2007

For more information, please contact:

Thomas C. NewkirkPartnerTel: 202 639-6099Email: [email protected]

Richard F. ZieglerPartnerTel: 212 891-1680Email: [email protected]

Alex LipmanPartnerTel: 212 891-1605Email: [email protected]

Andrew WeissmannPartnerTel: 212 891-1650Email: [email protected]

mark to model) valuations weretoo high historically; and

• how public companies and fundsreacted to current marketconditions, i.e., whether publicdisclosure of losses was timelyand comprehensive, given whatmanagement knew or shouldhave known at the time.

To be prepared, financialinstitutions — and those who havedealt with them — must take asober, comprehensive look at theirportfolios, business practices andreporting procedures.Understanding the scope andnature of any potential problem, ofcourse, puts one in the bestposition to address any litigation,governmental investigations, or topursue claims.

The Search for Culprits and Recoveries in the Credit Crisis

50

Treasury Department’s “Interim Final Rule,” Oct. 20, 2008 (Guidance on Executive Compensation Provisions of TARP)

NOTICE 2008-PSSFI I. PURPOSE This Notice, issued pursuant to sections 101(a)(1), 101(c)(5), and 111 of the Emergency Economic Stabilization Act of 2008, Div. A of Pub. Law No. 110-343 (EESA), provides guidance on certain executive compensation provisions applicable to a financial institution from which the Department of the Treasury (Treasury) acquires troubled assets through programs for systemically significant failing institutions (program). II. BACKGROUND RELATING TO EESA EXECUTIVE COMPENSATION

PROVISIONS Section 101(a) of EESA authorizes the Secretary of the Treasury to establish a Troubled Assets Relief Program (TARP) to “purchase, and to make and fund commitments to purchase, troubled assets from any financial institution, on such terms and conditions as are determined by the Secretary, and in accordance with this Act and policies and procedures developed and published by the Secretary.” Section 120 of EESA provides that the TARP authorities generally terminate on December 31, 2009, unless extended upon certification by the Secretary of the Treasury to Congress, but in no event later than two years from the date of enactment of EESA (October 3, 2008) (the TARP authorities period). Thus, the TARP authorities period is the period from October 3, 2008 to December 31, 2009 or, if extended, the period from October 3, 2008 to the date so extended, but not later than October 3, 2010. Section 111 of EESA provides that financial institutions that sell assets to the Treasury may be subject to specified executive compensation standards. In the case of auction purchases from a financial institution that has sold assets to the Treasury in an amount that exceeds $300 million in the aggregate (including direct purchases), the financial institution is prohibited under section 111(c) of EESA from entering into any new employment contract with a senior executive officer (SEO) that provides a golden parachute to the SEO in the event of the SEO’s involuntary termination, or in connection with the financial institution’s bankruptcy filing, insolvency, or receivership. This prohibition applies during the TARP authorities period. The Treasury has issued separate guidance on these provisions (Notice 2008-TAAP).

In addition, for auction purchases, section 302 of EESA enacted tax provisions as

amendments to sections 162(m) and 280G of the Internal Revenue Code that address compensation paid to certain executive officers employed by financial institutions that sell assets under TARP. The Treasury and the Internal Revenue Service have issued separate guidance on these provisions (I.R.S. Notice 2008-94).

In the case of direct purchases, section 111(b)(1) of EESA requires financial

institutions to meet appropriate standards for executive compensation and corporate governance, as set forth by the Secretary of the Treasury. The Treasury has issued

2

guidance on section 111(b) in the form of interim final regulations with respect to the TARP Capital Purchase Program (CPP) (31 CFR Part 30), which applies the following standards with respect to the CPP: (a) limits on compensation that exclude incentives for SEOs of financial institutions to take unnecessary and excessive risks that threaten the value of the financial institution; (b) required recovery of any bonus or incentive compensation paid to a SEO based on statements of earnings, gains, or other criteria that are later proven to be materially inaccurate; (c) prohibition on the financial institution from making any golden parachute payment to any SEO; and (d) agreement to limit a claim to a federal income tax deduction for certain executive remuneration. The provisions apply while the Treasury holds an equity or debt position in the financial institution.

This Notice 2008-PSSFI addresses the direct purchase provisions under section

111(b) of EESA as they pertain to financial institutions participating in the program, applying similar standards to those set out in the interim final regulations, except for a more stringent rule with respect to golden parachute payments. Further guidance will be issued for any additional programs.

Q-1: To what financial institutions does this Notice apply? A-1: (a) General rule. This Notice applies to any financial institution that

participates in the program. (b) Controlled group rules. For purposes of section 111(b) of EESA, two or more

persons who are treated as a single employer under section 414(b) of the Internal Revenue Code (employees of a controlled group of corporations) and section 414(c) of the Internal Revenue Code (employees of partnerships, proprietorships, etc., that are under common control) are treated as a single employer. However, for purposes of section 111(b) of EESA, the rules for brother-sister controlled groups and combined groups are disregarded (including disregarding the rules in section 1563(a)(2) and (a)(3) of the Internal Revenue Code with respect to corporations and the parallel rules that are in section 1.414(c)-2(c) of the Treasury Regulations with respect to other organizations conducting trades or businesses). See Q&A-11 of this Notice for special rules where a financial institution is acquired.

Q-2: Who is a SEO under section 111 of EESA? A-2: (a) General definition. A SEO means a “named executive officer” as

defined in Item 402 of Regulation S-K under the federal securities laws who: (1) is employed by a financial institution that is participating in the program while the Treasury holds an equity or debt position acquired under the program; and (2)(i) is the principal executive officer (PEO) (or person acting in a similar capacity) of such financial institution (or, in the case of a controlled group, of the parent entity); (ii) the principal financial officer (PFO) (or person acting in a similar capacity) of such financial institution (or, in the case of a controlled group, of the parent entity); or (iii) one of the

3

three most highly compensated executive officers of such financial institution (or the financial institution’s controlled group) other than the PEO or the PFO.

(b) Determination of three most highly compensated executive officers. For