the role of natural gas in a carbon constrained world€¦ · the role of natural gas in a carbon...

TRANSCRIPT

The Role of Natural Gas in a Carbon Constrained

World

Sergey PaltsevMassachusetts Institute of Technology

IEFE, Bocconi University, Milan, ItalyApril 15, 2011

Questions or comments?

Contact: Sergey Paltsev

Motivation• Carbon content: coal – 24.7 MtC/EJ, crude oil – 19.3

MtC/EJ, gasoline – 18.4 MtC/EJ, natural gas – 13.7 MtC/EJ. Gas is only 55% of coal emissions (add efficiency – numbers cited as low as 30%).

• Shale gas hype• Is gas a big player in a carbon-constrained world?• MIT Future of Natural Gas study • Focus on impacts on the U.S., but world reserves and

trade are important• Model: MIT Emissions Prediction and Policy Analysis

(EPPA)

2

3

4

5

6

77MIT Future of Natural Gas Study

Overarching Conclusion

• Abundant global resources, expanded use, especially electricity

• Increasing share in US, with key role for unconventional resources

• Larger share with CO2 emissions constraints;

• but with very stringent constraints, role of all fossil fuels limited without competitive CCS

• Global gas markets can change dramatically to 2050

7

88

System Studies of Gas Futures• The economic models (EPPA and USREP)

• Strengths• Limitations

• Interactions and uncertainties• Gas Resources (High, Mean, Low)• Greenhouse gas mitigation (3 scenarios)• Technology cost (Sensitivity tests)• International gas markets (Regional vs.

global)

8

9Remaining Recoverable Natural Gas Resources(Excludes unconventional gas outside North America)

Tcf of Gas9

Gas supply curvesGlobal U.S.

10

1111

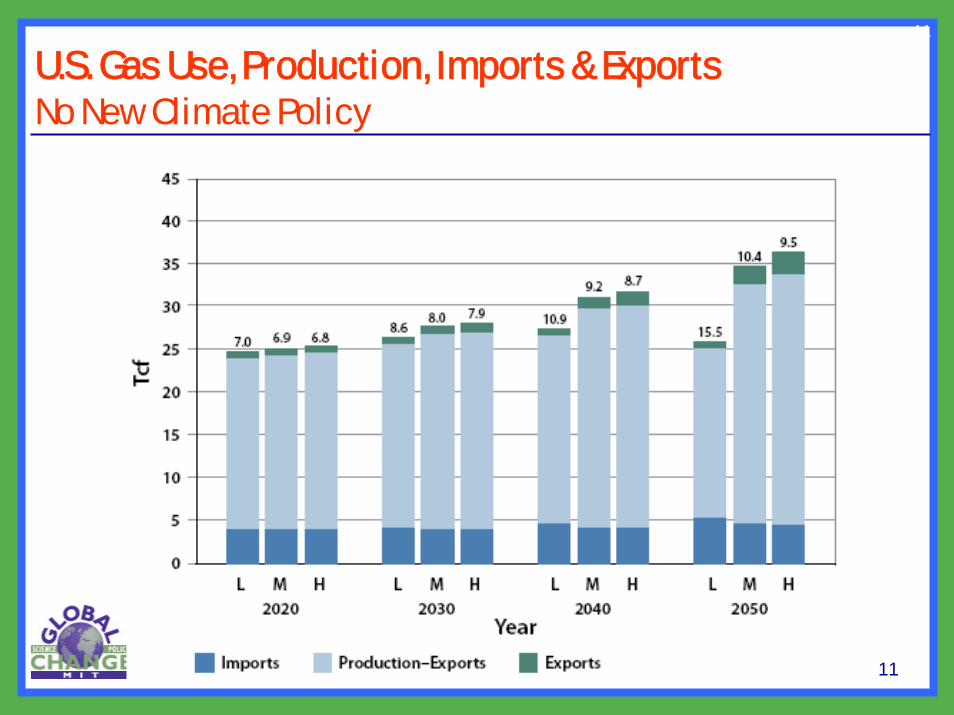

U.S. Gas Use, Production, Imports & ExportsNo New Climate Policy

11

12

U.S. Gas Use, Production, Imports & Exports Price-Based Policy (50% by 2050, No Offsets)

12

7.5 $/Mcf13.3 $/Mcf7.5 $/Mcf

13.3 $/Mcf

12

1313

Price-based mitigation

50% by 2050No offsets

GasCoal Electric sector

Gas

Total energy13

1414

Regulatory mitigation

25% RES 203055% coal retireGas

Electric sector

Renew

Gas

Total energy 14

1515

International Market Evolution

Regional Markets Global Market

7.5 $/Mcf13.3 $/Mcf7.5 $/Mcf

13.3 $/Mcf

5.7 $/Mcf11.4 $/Mcf5.7 $/Mcf

11.4 $/Mcf

15

Case for U.S. gas exports?

• U.S. Producer’s Perspective: floor on U.S. gas prices

• U.S. Consumer’s Perspective: prices would be higher

• U.S. Strategic Perspective: exports today = imports tomorrow? (look at UK example)

• Investment Perspective: price differential between Henry Hub and long-term contracts, competition with lower cost suppliers

16

1717

Regional Gas Markets in 2030 (Tcf)

17

1818

Global Gas Markets in 2030 (Tcf)

18

Global natural gas use (Tcf)

2030

EPPA reg – 130 Tcf

EPPA gl – 160 Tcf

IEA new pol – 152 Tcf

IEA cur pol – 159 Tcf

Exxon – 172 Tcf

BP – 169 Tcf

Shell – 160 Tcf

Nat gas study

19

Cornell Uni - Howarth• Natural gas generation is twice GHG-intensive as

Coal.• Low gas generation efficiency – 28% (other numbers

provided in the table but not in the headlines).• GWP – 20 years vs 100 years.• Legitimate questions about uncertainty.• But:• 28% - efficiency of a peaking gas unit. Gas in NGCC

– 40-54% efficiency, Coal – 30-35%. • GWP – compare near-term impacts with longer-term

impacts (20,100,500-years; need for damage function, but it is highly uncertain).

• Leakage from production can be reduced.• Recalculating using 100-year GWP and efficiency –

gas generation has 50% less GHG than coal.20

“Bridge to where?”

012345678

2010 2020 2030 2040 2050 2060 2070 2080 2090 2100Year

TkW

hReduced Use

Renew

Hydro

Nucl

Gas_CCS

Gas

Oil

Coal_CCS

Coal

A more stringent CO2 reduction, say 80%, would probably require the complete de-carbonization of the power sector. This makes it imperative that the development of competing low carbon technology continues, including CCS for both coal and gas.

21

Main Points• Abundant supplies of natural gas in the world.• Many supplies can be developed and produced at

relatively low cost.• The role of natural gas is likely to continue to expand

as a result of its availability, its utility, and relatively low cost.

• In a carbon-constrained economy, the relative importance of gas is likely to increase even further, as it is one of the most cost-effective means by which to maintain energy supplies while reducing GHGs.

• In the U.S., natural gas sets the cost benchmark against which clean power sources must compete.

• Stringent carbon constraints would require de-carbonization.

22