the role of actuaries in the healthcare system november 2014 emile stipp

TRANSCRIPT

The role of actuaries in the healthcare system

November 2014Emile Stipp

Providing understanding: The drivers of healthcare inflation

The role of actuaries in different healthcare systems around the world

Developing solutions: Wellness programmes

Agenda

The role of actuaries

Our skills Who we advise

The questions we ask The IAA

Actuaries

Defi ne actuary

ac · tu ·ar ·y, nounA person who compiles and analyzes statistics and uses them to calculate insurance risks and premiums

• Pragmatic

• Numerate, including good understanding of statistics

• But we are data skeptical, and often accept that we work with imperfect data

• We have a very good understanding of how healthcare systems, or administration of healthcare arrangements, impact on costs and risks, and we incorporate this in our analysis and projections

• We have a deep understanding of demographic trends and how they impact on costs and risks

• Strong emphasis on professional standards and ethics• Avoid conflicts of interests• Balanced, objective advice • With full disclosure• Doing our work for the benefit of Society

Defining characteristics

The actuarial toolkit

Projecting mortality & morbidity & financial outcomes

Exposure

Frequency / severity analyses

Good statistical understanding

Reserving for liabilities incurred

Matching of assets and liabilities

Risk immunisation & mitigation

Optimisation

Anti-selection and its antidotes

Managed care organisations

Third party administrators

Advisory services

Public healthcare Private healthcare

Supply side organisations

InsurersHealth

indemnityCritical illness

Long term care

Disability

Policy makers

Governments

Government bodies NGOs

The role of health actuaries

Public healthcare Private healthcare

• Analysis• Capital• Disclosure• Valuation• Product design• Pricing• Risk management & managed

care• Optimisation• Projections

• Budgeting and risk adjustment• Risk equalisation• Demographic and financial

projections• Funding sustainability• Public Private Partnerships• Analysis of cost drivers

The questi ons actuaries ask• What is the current and prospective burden of healthcare in the context of GDP, household income, and other economic

indicators• What drives disability claims experience?• What drives healthcare inflation?• What is the impact of anti-selection on health insurance risks?• How can costs be managed?• Can wellness programmes make a real difference to medical inflation?

• How should products be designed to introduce the right incentives?• What premium should be charged? How to optimise it?• How do we design and select networks of providers to improve efficiencies and quality?• Can alternative reimbursement models be designed to control costs without compromising on quality?• What is the best way to detect and prevent health fraud and abuses in healthcare?• What are risk-adjusted cost differentials between different service providers?

• How can private / public partnerships be structured?• How do we insure low income individuals?• Are out-of-pocket expenses equitably distributed between different levels of income?

• What are the risk consequences of catastrophic events, such as a pandemic?• What capital is required to protect against adverse events?• How will the HIV epidemic affect insurance costs?

• How do we ensure that more people have access to health services and do not suffer financial hardship paying for them?

The 3 dimensions of Universal Coverage

Source: WHO WHR 2010.

Our contribution

– Applying the Mathematical / statistical skills of actuaries to the quantification of cashflow and capital and their associated risks

– Our role is to support policy makers and managers by quantifying expected outcomes and the risks of deviations both in terms of costs and demand on resources

– Expected outcomes are estimated by applying actuarial methodology to factual data and assumptions including the presumed impact of policy decisions

– Enabling decision makers and managers to compare ex-ante the expected impact of policy decisions or strategic interventions facilitate optimisation

– As outcomes are explicitly linked to the various drivers there is value added in the possibility of monitoring the actual outcomes against the expected to identify the causes of the deviations and apply the feed back to improve the decision making

– Our methodology helps understand how incentives of role players affect risks and outcomes

– Our modelling approach tends to be bottom-up & stochastic, rather than top-down & deterministic. We typically don’t assume equilibrium ..

The role of the IAA

Mission: To promote the profession

to the benefit of Society Promote professionalism,

develop education, encourage research

Association of worldwide actuarial professional associations, with special interest sections for individual members

Six strategic objectives: Build relationships with key

supranational organisations Expand scientific knowledge and skills

of actuaries Promote common standards of

actuarial education and professional conduct

Develop actuarial profession worldwide

Provide a forum for discussion for actuaries

Improve recognition of actuarial profession

The role of the IAA

IAA Health Section:• Individual membership• Main objectives: library of actuarial papers, research presented at conferences and

webcasts• See example papers on risk equalisation (

http://www.actuaries.org/IAAHS/Webcast/RiskAdjustment/RiskAdjustment_Slides.pdf)• And on stochastic modelling (

http://www.actuaries.org/IAAHS/Webcast/Stochastic/IAAHS_11-15-2010-wocartoons.pdf)

IAA Health Committee:• Representatives of member associations• Purpose to :

o Represent the IAA in international debates on health actuarial matterso Raise profile of health actuarieso Support actuaries working in private and public health systems

Providing understanding: The drivers of healthcare inflation

The role of actuaries in different healthcare systems around the world

Developing solutions: Wellness programmes

Agenda

Using inflation as an example....• Of how actuaries analyse problems• Insights to be gained from actuarial analysis,

and techniques used• Using South African private health for illustration,

with some references to international experience• And also offering a solution with roots in South Africa, but which has

spread across the world in different forms

14

Some preliminaries• Adjusting for exposure is crucial• Consider Simpson’s Paradox:

– In the context of a health insurer with two benefit plans / levels– Average inflation is 0%, and yet each plan’s inflation rate is 10%!

Number of members in

Year 1

Premium per member in

Year 1

Number of members in

Year 2

Premium per member in

Year 2

Increase in per member

contribution from

Year 1 to Year 2

Plan 1 100 1000 200 1100 10%

Plan 2 50 2000 54 2200 10%

Insurer 150 1333.33 254 1333.86 0%

15

Some preliminaries

• Simpson’s paradox is relevant to:– health insurers with more than one plan, – policymakers, considering health inflation across a health

insurance markets– Governments, considering health inflation in a country (e.g. public

and private spending)• It implies:

– All inflation studies should adjust for demographic movements between insurance markets / insurers / benefit packages

– And not look only at overall average– Otherwise it will understate inflation where there are downgrades

and overstate where there are upgrades

Some preliminaries• Consider frequency and severity separately

– As this could provide insight into the reasons for cost increases• Consider price and utilisation separately

– Price measures tariff increases• And how that is set by legislation / competition

– And utilisation should be broken down into• demand side factors and • supply side factors

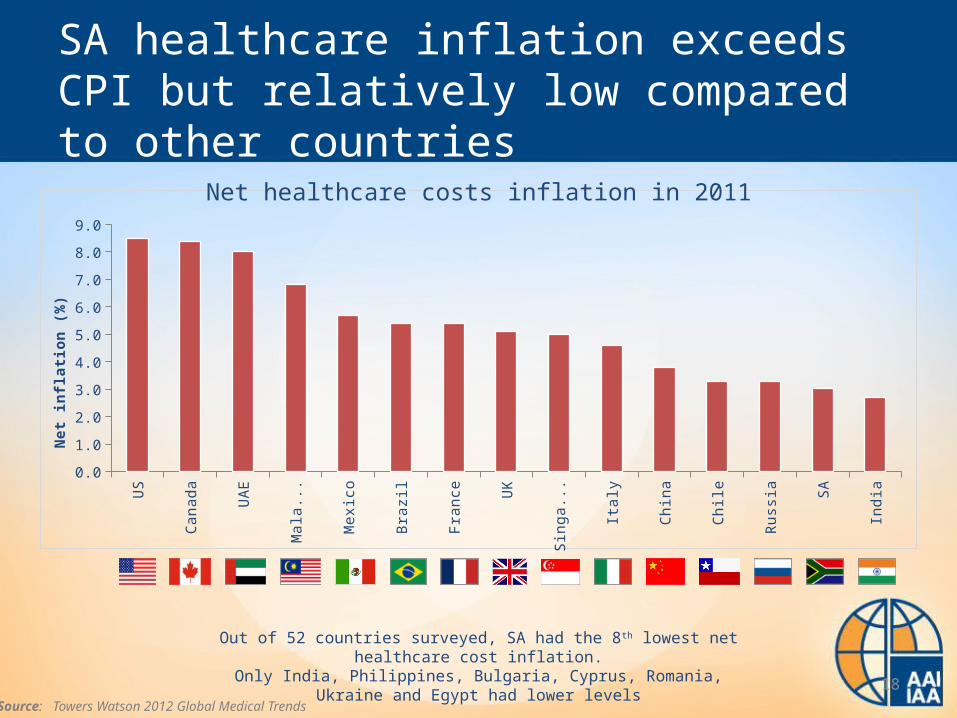

SA healthcare inflation exceeds CPI but relatively low compared to other countries

US

Cana

da

UA

E

Mal

aysi

a

Mex

ico

Braz

il

Fran

ce UK

Sing

apor

e

Ital

y

Chin

a

Chile

Russ

ia SA

Indi

a

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Net

infla

tion

(%)

Out of 52 countries surveyed, SA had the 8th lowest net healthcare cost inflation.Only India, Philippines, Bulgaria, Cyprus, Romania, Ukraine and Egypt had lower levels

Source: Towers Watson 2012 Global Medical Trends

Net healthcare costs inflation in 2011

18

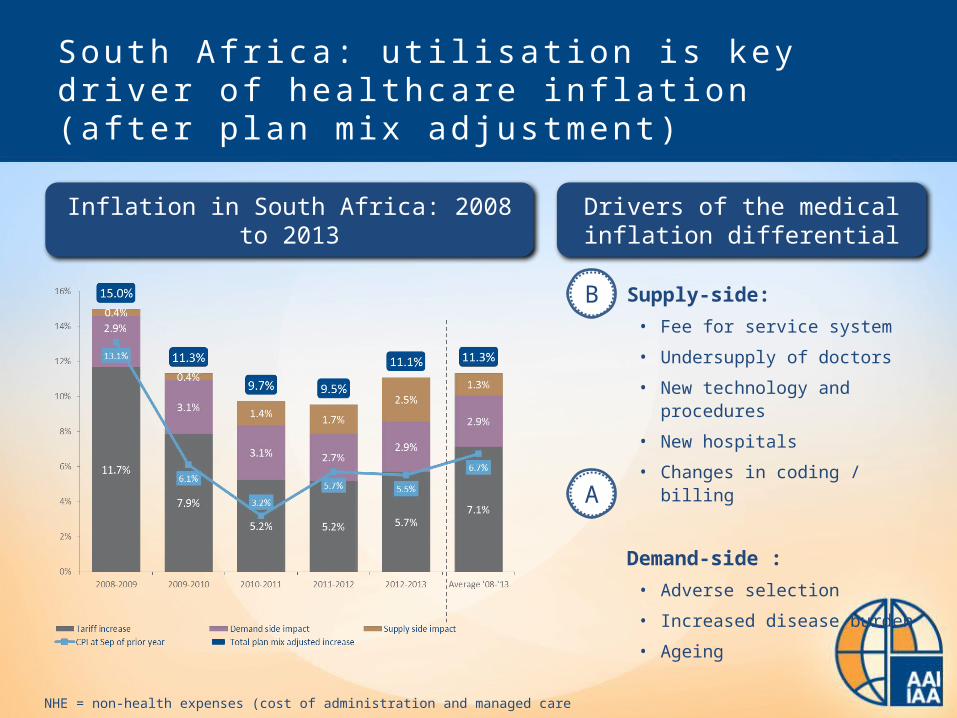

S o u t h A f r i c a : u ti l i s a ti o n i s ke y d r i ve r o f h e a l t h c a re i n fl a ti o n ( a ft e r p l a n m i x a d j u s t m e n t )

Inflation in South Africa: 2008 to 2013 – in Rand amounts

NHE = non-health expenses (cost of administration and managed care

S o u t h A f r i c a : u ti l i s a ti o n i s ke y d r i ve r o f h e a l t h c a re i n fl a ti o n ( a ft e r p l a n m i x a d j u s t m e n t )

Supply-side:• Fee for service system

• Undersupply of doctors

• New technology and procedures

• New hospitals

• Changes in coding / billing

Demand-side :• Adverse selection

• Increased disease burden

• Ageing

Inflation in South Africa: 2008 to 2013 Drivers of the medical inflation differential

B

A

NHE = non-health expenses (cost of administration and managed care

Demand side: 2002 to 2012A

Demand-side: Adverse selecti on conundrum

• Young people opt out of medical schemes

• Medical schemes have higher proportions of older people

“Impact of adverse selection estimated at R13.5bn – 23% of total contributions for open medical schemes”Barry Childs, Lighthouse Actuarial Consulting

1

Adverse selection in open medical schemes

A

2

1

2

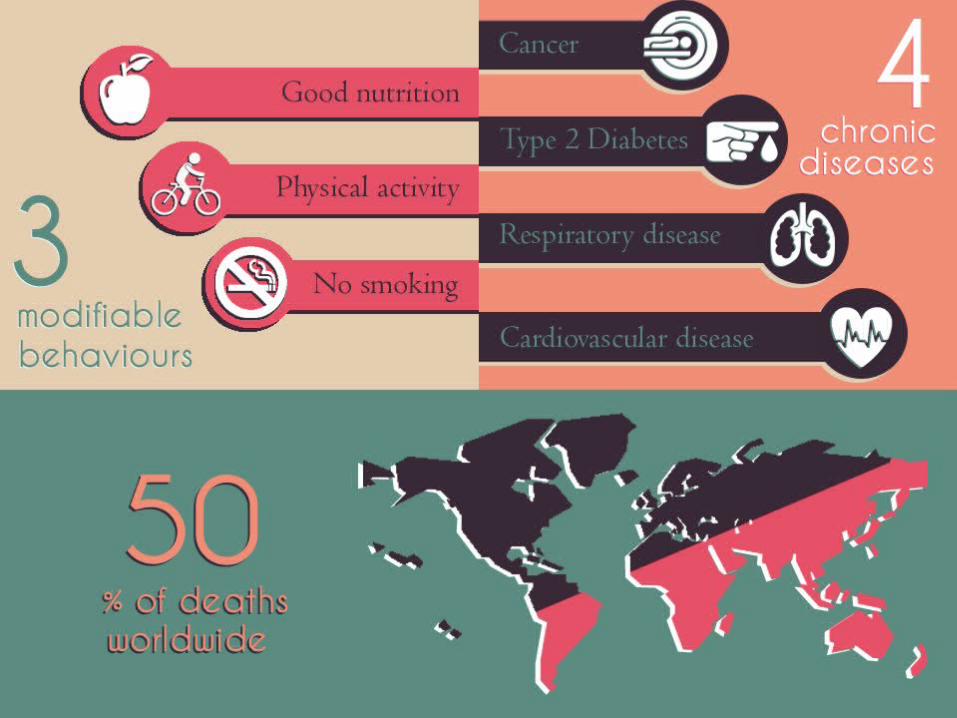

Demand side: Increasing burden of disease

3

4

50

Three controllable behaviours

Four chronic diseases of lifestyle

Fifty percent of deaths worldwide

Source: DHMS data, indexed to 2008

Epidemic of lifestyle diseases Increasing disease burden in medical schemes

A

Demand side infl ati on in South Afr ica

• Mostly attributable to:– Lack of a mandate– Open enrolment, guaranteed acceptance and

community rating– Very limited underwriting allowed– Resulting adverse selection – age and chronic

• Roughly 3% to 4% per year attributable to demand side inflation

A

Supply s ide: Shortage of doctors

25

SA Russia Brazil China India France Germany US UK AustraliaBRIC Developed economies

5.5

43

17

14

6

3735

27

21

10

• SA needs to train 2,400 doctors p.a. just to remain on par with current low figures

• Average age of specialists in SA = 55 years

• SA’s graduates have remained at 1,200 p.a. for the last 2 decades

Source: World Health Stats 2012

BRICS Developed

B

Doctors per 10,000 lives

Supply side: High cost of new medicines

26

Growth in claimants for high-cost drugs

B

Supply side: relationship between market concentration and bed supply per 1000 lives

27

In some regions: high bed supply even where low concentration

B

Supply s ide infl ati on in South Afr ica

• Attributable to:– Radiology / pathology– Increases in hospital beds– Price of new technologies

• About 1% to 2% per year• Overall utilisation therefore 4% to 6% per year

above inflation

B

Another v iew of healthcare infl ati on

• CPI is an average of different inflation indices• Some components of inflation are always higher

than others, e.g. healthcare vs electronic consumer goods– Especially those aspects linked to skilled services

• Wages generally keep up with inflation• Hence all that happens is that people devote a larger

proportion of their salaries to healthcare over time• “The Baumol Effect”, after William Baumol’s “The

cost disease”, 2011

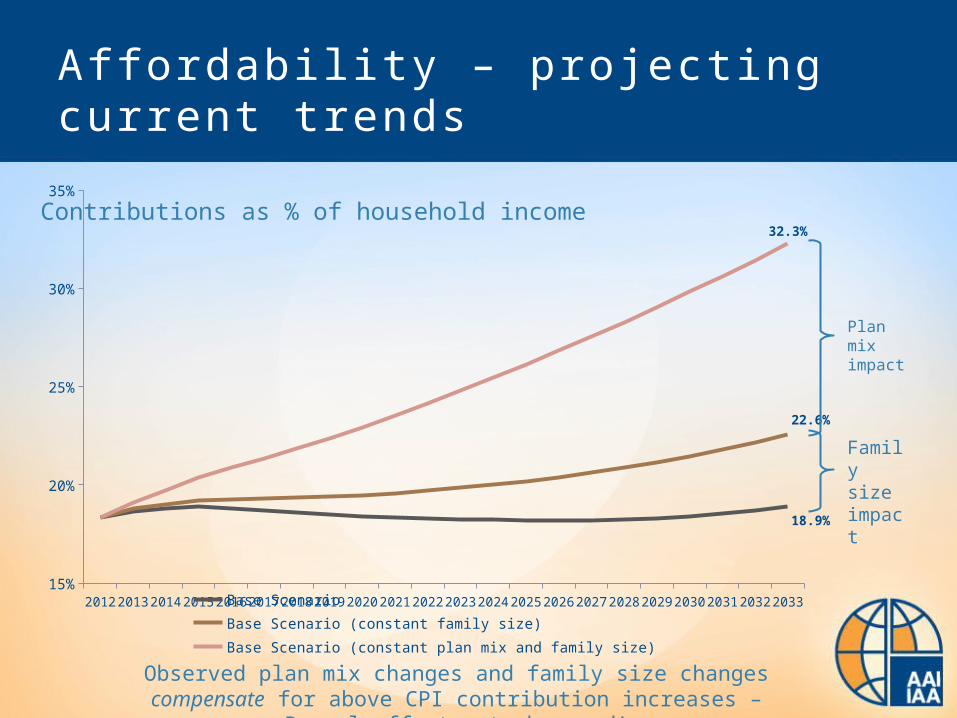

But. . . .

• It may be true that healthcare inflation is and always will be higher than average inflation

• But it is not true that people will continue to spend a larger proportion of their salaries on healthcare

• In South Africa, we see that people effectively buy down their cover to maintain a roughly similar percentage of their salaries devoted to healthcare

Aff ordabi l i ty – projecti ng current trends

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 203315%

20%

25%

30%

35%

18.9%

22.6%

32.3%

Base Scenario Base Scenario (constant family size)Base Scenario (constant plan mix and family size)

Plan mix impact

Family size impact

Observed plan mix changes and family size changes compensate for above CPI contribution increases – Baumol effect not observed!

Contributions as % of household income

Providing understanding: The drivers of healthcare inflation

The role of actuaries in different healthcare systems around the world

Developing solutions: Wellness programmes

Agenda

Soluti ons?

One solution to mitigate all of these effects:

Keep people healthy!

Do we have evidence that incentive based wellness programmes work?

A case for wellness:Low-levels of wellness engagement; impact of behavioural factors

Und

er c

onsu

mpt

ion

of p

reve

ntiv

e ca

re Lack of information

Over-optimism

Hyperbolic discounting

True efficacy of different health and wellness approaches is not well understood

People tend to overestimate their abilities and health status

Future rewards of a healthy lifestyle are significantly undervalued relative to cost today

Sickness Wellness

Benefits are immediate, price is hidden

Benefits are hidden, price is immediate

A behavioural solution to the under-consumption of wellness:Member experience

Complete an HRA

Determine Vitality Age and set health goals

Earn points and achieve a Vitality status

Earn Vitality rewards

Obtain a Personal Pathway

Know your health Improve your health Enjoy the rewards1 2 3

Age

Results of the model:Vitality benefit utilisation

2006 2007 2008 2009 2010 20110

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

2006 2007 2008 2009 2010 2011 -

5

10

15

20

25

Gym visits (million, calendar year)

kulula.com flights (calendar year)

Feb-09

Jun-09

Oct-09

Feb-10

Jun-10

Oct-10

Feb-11

Jun-11

Oct-11

Feb-12

Jun-12 -

40

80

120

160

200

240

280

320

360

Cumulative HealthyFood cashback(R Million since inception)

Vitality clinical foundation: Published research

Name of study Journal Date published

Hypotheses/ research objective

Fitness-Related Activities and Medical Claims Related to Hospital Admissions — South Africa, 2006

Preventing Chronic Disease

October 2009 Fitness engagement and health and cost outcomes

The Association Between Medical Costs and Participation in the Vitality Health Promotion Program Among 948,974 Members of a South African Health Insurance Company

American Journal of

Health Promotion

January/ February 2010

Vitality engagement and cost outcomes

Participation in Fitness-Related Activities of an Incentive-Based Health Promotion Program and Hospital Costs: A Retrospective Longitudinal Study

American Journal of

Health Promotion

May/June 2011 Longitudinal assessment of fitness engagement and health and cost outcomes

Eating Better for Less: A National Discount Program for Healthy Food Purchases in South Africa

American Journal of

Health Behaviour

In Press To assess impact of the discount on healthy food on fruit and vegetable intake

Name of study Journal Date published

Hypotheses/ research objective

Engaged members experienced lower costs per patient compared to other groups

Note: Categorisation based on diagnosis-related groupers using ICD-10, CPT-4 and local procedural codesSource: “Participation in an Incentive-based Wellness Program and health care costs: Results of the Discovery Vitality Insured Persons Study”. Please do not quote without written permission from Discovery or PruHealth.

Canc

er

Men

tal

Kidn

ey a

nd U

TI

Endo

crin

e, n

utriti

onal

...

Resp

irato

ry

Ner

vous

and

mus

culo

s...

Dig

estiv

e

Card

iova

scul

ar

Ove

rall

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

P < 0.001 for all categories (including overall result) except cancer where P < 0.01

Not engaged benchmark

30-40% 15-20% 10-15%

Risk-adjusted hospital admission costs: engaged vs. not engaged Vitality members

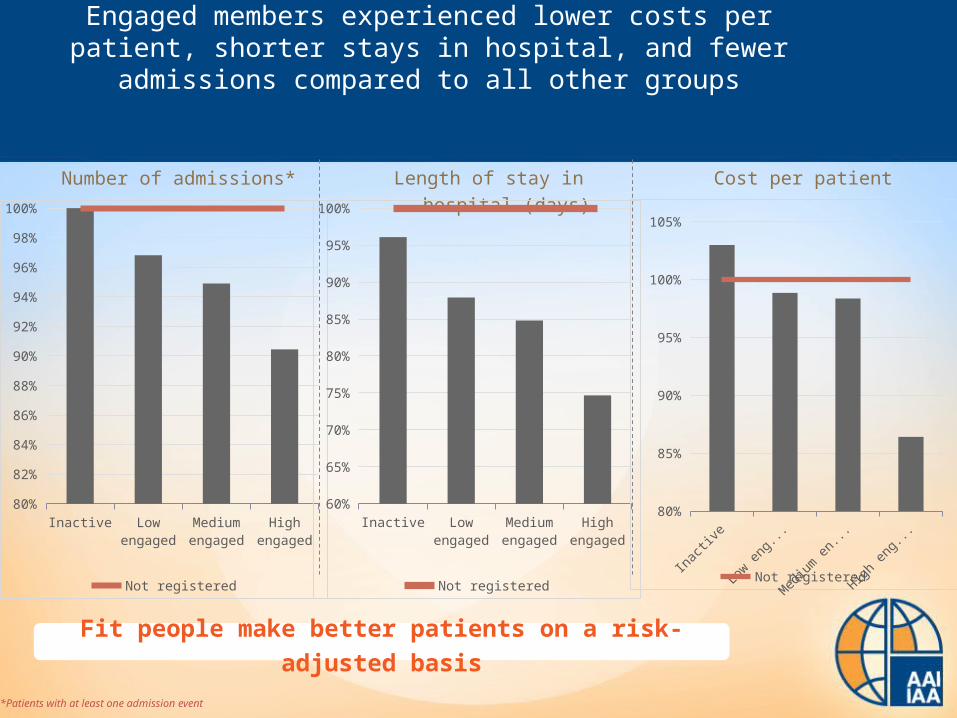

Engaged members experienced lower costs per patient, shorter stays in hospital, and fewer admissions compared to all other groups

*Patients with at least one admission event

Inac

tive

Low e

ngag

ed

Med

ium e

ngag

ed

High e

ngag

ed80%

82%

84%

86%

88%

90%

92%

94%

96%

98%

100%

Not registered

Number of admissions* Length of stay in hospital (days) Cost per patient

Inac

tive

Low e

ngag

ed

Med

ium e

ngag

ed

High e

ngag

ed60%

65%

70%

75%

80%

85%

90%

95%

100%

Not registered

Inac

tive

Low e

ngag

ed

Med

ium e

ng...

High e

ngag

ed80%

85%

90%

95%

100%

105%

Not registered

Fit people make better patients on a risk-adjusted basis

P = 0.001 for multiple metabolic conditions, all single conditions are not statistically significant

Multiple metabolic conditions

Mental illness Cancer Hypertension Dyslipidaemia0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Beneficiaries with single conditions

Not engaged benchmark

20-30% 8-10%

Engaged chronic members experienced lower costs per patient compared to other groups

First model to test impact of increasing engagement

This analysis looks at all Health & Vitality members who subscribed uninterruptedly for a full three year period to both products. The VEM1 is tracked over this period and the life is categorised into a longitudinal engagement category. An outcome or target is then explored during the course of the fourth year.

The analysis explores the association between changes in engagement and morbidity measures

1 Vitality engagement metric is the before limit point summation tracking true engagement in the form of activity related events excluding carry over points, bonus points and outcome points

A longitudinal view of engagement

• Compile a three year monthly VEM per beneficiary• Regress a straight line through the data points• Use the results parameters – i.e. the intercept parameter β0 and the slope parameter β1 • The parameters are then grouped to create a progression matrix of engagement where the top right hand

corner represent the most engaged group of people– This was done for various iterations but a 6 month cumulative VEM view was chosen to be the

champion of a three year engagement view

vs

Consider

Unengaged

Engaged

Most & increasingly

engaged

Constantly unengaged

y = 71.429x + 166.67y = 30x + 570

0

10 000

20 000

6 12 18 24 30 36

Year 1 Year 2 Year 3

VEM

Agent C's points Agent D's points

3 year trend for Agent C 3 year trend for Agent D

y = 1652.9x + 2580

y = 1059.1x + 8408

0

10 000

20 000

6 12 18 24 30 36

Year 1 Year 2 Year 3

VEM

Agent A's points Agent B's points

3 year trend for Agent B 3 year trend for Agent A

Rate of changecategory

Sta

rtin

g p

oin

t ca

teg

ory

0.87 0.79

0.91

0.97

1

0.87

0.790.87

0.79

0.79

0.91

0.87 0.87

0.97 0.91

Heat map of morbidity rates with risk adjustment

Notes:1 - estimated parameter for each cellStarting level refers to the intercept of the straight lineRate of change refers to the slope of the line, where the line refers to the regression fitted on each individual’s VEM

Increased engagement

Decreased engagement

Started low

Started high

11

1.17 1.17

0.741.17

0.460.670.82

0.46

0.46

0.46

0.69

0.461.48 1.48

Heat map of relative effect on mortality

Notes:1 - estimated parameter for each cellStarting level refers to the intercept of the straight lineRate of change refers to the slope of the line, where the line refers to the regression fitted on each individual’s VEM

Increased engagement

Decreased engagement

Started low

Started high

Concluding remarks – inflation & wellness programmes

1. Both demand and supply side causes of medical inflation in South Africa

2. Incentivised wellness programme is one of the potential solutions

3. We observe the impact of both selection and behaviour change

4. Increased engagement in wellness activities is associated with significantly lower mortality and morbidity risks

5. The combined financial impact of positive risk selection / retention and health engagement generate significant financial benefits for members of medical schemes

6. But also leads to significant mortality improvements over time....

BOTTOM LINE: EVERYONE SHOULD EXERCISE!

Conclusion

• We believe actuaries have deep insight into healthcare systems that could be of value to policy makers

• Whether in the Public or Private sector

• Our insights are based on detailed but pragmatic analyses, and we are “data sceptical”

• We emphasise context: role players’ incentives, impact of administration arrangements

Conclusion

• We place strong emphasis on professionalism and ethics, and we are objective and balanced in our advice

• We focus on understanding long and short term risks and how to mitigate them

• We aim to do our work to the benefit of Society