the role and impact of low cost...

TRANSCRIPT

The Role and Impact of Low Cost CarriersThe Role and Impact of Low Cost Carriers

MIT Global Airline Industry Program

William S. SwelbarManaging Director

March 26, 2002

Introduction and Topics to be CoveredIntroduction and Topics to be Covered

! Low Fare/Niche segment is less of a topic without the deterioration of profitability that began in 1998, and the market opportunities presented after 9/11.

! Each of the network carriers placed a capacity reduction bet on 9/12: How much was too much – how little was too little?

– Either way, the low cost segment had/has a solid platform to grow from.

! The cuts in the West would appear to only make a bad situation for the network carriers grow worse.

! Low Fare/Niche carrier growth has continued to penetrate the largest U.S. markets, and no region of the U.S. is immune.

! The RJ is the low cost growth vehicle for the network carriers –Let’s just call a spade a spade.

! Low Fare/Niche segment is less of a topic without the deterioration of profitability that began in 1998, and the market opportunities presented after 9/11.

! Each of the network carriers placed a capacity reduction bet on 9/12: How much was too much – how little was too little?

– Either way, the low cost segment had/has a solid platform to grow from.

! The cuts in the West would appear to only make a bad situation for the network carriers grow worse.

! Low Fare/Niche carrier growth has continued to penetrate the largest U.S. markets, and no region of the U.S. is immune.

! The RJ is the low cost growth vehicle for the network carriers –Let’s just call a spade a spade.

Shar

e of

Tot

al A

SM G

row

thSh

are

of T

otal

ASM

Gro

wth

15-Year Cycles; 15-Year “Bubbles”The Low Fare/Niche-Oriented Carriers and Regional (Small) Jets Have Already Begun Redesigning theNew Competitive Landscape

15-Year Cycles; 15-Year “Bubbles”The Low Fare/Niche-Oriented Carriers and Regional (Small) Jets Have Already Begun Redesigning theNew Competitive Landscape

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000

% Change in Average Stage Length% Change in Average Seats % Change in Scheduled Departures

Technology-Driven Capacity Growth

Technology-Driven Capacity Growth

Competition-DrivenCapacity Growth

Competition-DrivenCapacity Growth

RecessionRecession

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 20000%

10%

20%

30%

40%

50%

60%

70%

80%

Y-O-Y Change in ASMs Y-O-Y Change in RPMs Load Factor

Where Has the Revenue Gone?Where Has the Revenue Gone?

U.S. Scheduled Airlines’ Domestic OperationsU.S. Scheduled Airlines’ Domestic Operations

Average Load Factor 63.9%

Average Load Factor 63.9%

Average Load Factor 54%

Average Load Factor 54%

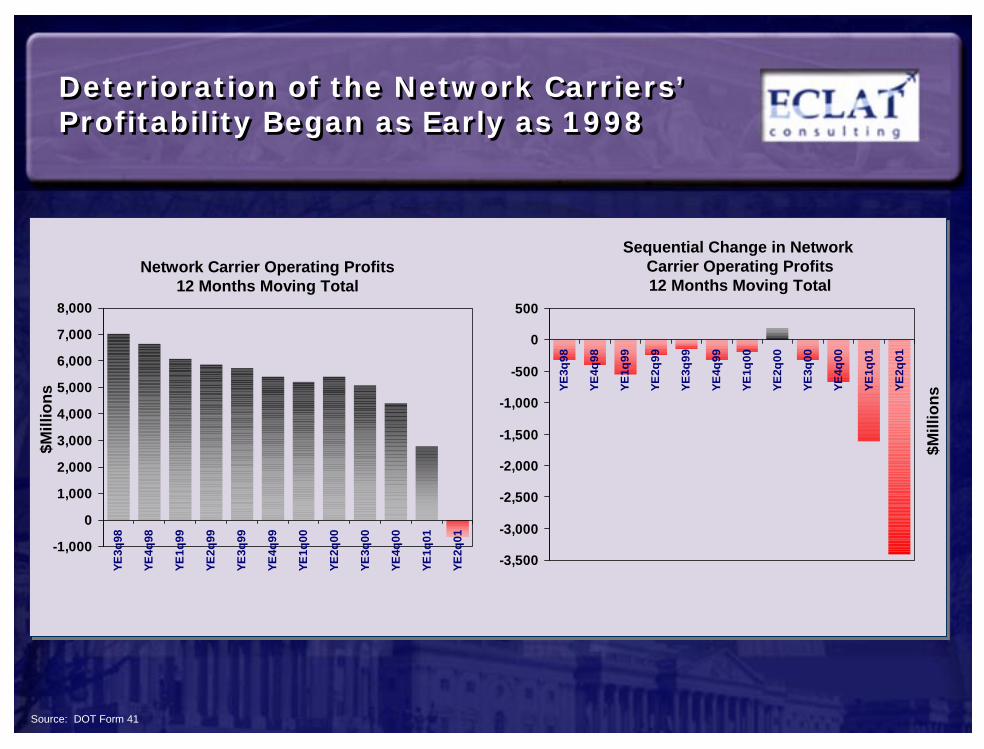

Deterioration of the Network Carriers’ Profitability Began as Early as 1998Deterioration of the Network Carriers’ Profitability Began as Early as 1998

Network Carrier Operating Profits12 Months Moving Total

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

YE3q

98

YE4q

98

YE1q

99

YE2q

99

YE3q

99

YE4q

99

YE1q

00

YE2q

00

YE3q

00

YE4q

00

YE1q

01

YE2q

01

$Mill

ions

$Mill

ions

-3,500

-3,000

-2,500

-2,000

-1,500

-1,000

-500

0

500

YE3q

98

YE4q

98

YE1q

99

YE2q

99

YE3q

99

YE4q

99

YE1q

00

YE2q

00

YE3q

00

YE4q

00

YE1q

01

YE2q

01

Sequential Change in Network Carrier Operating Profits12 Months Moving Total

Source: DOT Form 41

The Underlying Economics Have Not Favored the Network Carrier Segment for Sometime – Overcapacity?

The Underlying Economics Have Not Favored the Network Carrier Segment for Sometime – Overcapacity?

Critical Indices Underlying the Industry’s Operating PerformanceCritical Indices Underlying the Industry’s Operating Performance

1.6%

-3.9%

8.2%

-11.8%-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

ASMs Rev/ASM Cost/ASM OP. Margin(Pts. Change)

Network CarriersPercent Change

1st Half 2001 vs. 1st Half 2000

Network CarriersPercent Change

1st Half 2001 vs. 1st Half 2000

Low Fare/Niche CarriersPercent Change

1st Half 2001 vs. 1st Half 2000

Low Fare/Niche CarriersPercent Change

1st Half 2001 vs. 1st Half 2000

12.8%

0.5%

-1.3% -0.8%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

ASMs Rev/ASM Cost/ASM OP. Margin(Pts. Change)

Network Carrier Operating Profit Change:

-$5.0B

Low Fare/Niche Carrier Operating Profit Change:

$33.7M

Note: Network carriers include American/TWA, America West, Continental, Delta, Northwest, United, and US Airways.

Note: Low Fare/ Niche carriers include Alaska, JetBlue, Frontier, AirTran, Spirit,American Trans Air, Southwest, and Midwest Express.

Assessing the Network Carrier Response: Which Hubs and Network Carriers Cut the Deepest Immediately Following 9/11?

Assessing the Network Carrier Response: Which Hubs and Network Carriers Cut the Deepest Immediately Following 9/11?

-20% 0%-18% -13% -5%-10% -9% -8%

UnitedLAX -22%SFO -22%IAD -19%DEN -17%ORD -12% Northwest

MEM -21%MSP -12%DTW -11%

American/TWA

MIA -12%ORD -12%DFW -8%STL -7%

US AirwaysPHL -11%CLT -9%PIT -7%

ContinentalEWR -17%IAH -4%CLE -1%

DeltaJFK -29%DFW -8%ATL -5%SLC +1%CVG +4%

Source: Eclat Air Service Model, November 2001 vs. September 10, 2001Note: Changes in carrier service reflect total; changes in hub service reflect nonstop only.

A Competitive Reality – The Low Fare Carriers Had Built a Strong Base of Traffic Prior to 9/11 …

A Competitive Reality – The Low Fare Carriers Had Built a Strong Base of Traffic Prior to 9/11 …

Low Fare Carriers Out-Carry Every Major Network Carrier at the Cities They Serve in Common

Low Fare Carriers Out-Carry Every Major Network Carrier at the Cities They Serve in Common

Annu

al P

asse

nger

sAn

nual

Pas

seng

ers

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

90,000,000

AA & TWA HP CO DL NW UA USHub Carrier Low Fare Carriers

The Reality – Low Fare Carrier Penetration Has Pierced Many of the Network Industry Strongholds

The Reality – Low Fare Carrier Penetration Has Pierced Many of the Network Industry Strongholds

Core 48 State Cities Served by Low Fare Carriers*Core 48 State Cities Served by Low Fare Carriers*

1997(89 Cities)

PDEWs

1997(89 Cities)

PDEWs

2001(82 Cities)

PDEWs

2001(82 Cities)

PDEWs4-Year Growth

Percent4-Year Growth

Percent

All Network Carriers Average 7,073 7,660 8.2%

Low Fare Carriers Average 1,787 2,610 46.1%

* Cities with at least 20 PDEWs for Low Fare Carriers

Low Fare Penetration inTop 10 CMSA Markets –Note the Migration from West to East

Low Fare Penetration inTop 10 CMSA Markets –Note the Migration from West to East

Total Los Angeles

35%

Total San Francisco

33%

Total Dallas/Ft. Worth

23%

Total Chicago

17%

Total Washington

18%

Total New York

8%

Total Boston

9%

Total Houston

31%

Philadelphia3%

Philadelphia3%

Atlanta 12%

Atlanta 12%

Burbank 70%

Los Angeles 25%

Long Beach 5%

Orange County 25%

Oakland69%

San Jose43%

San Francisco

4%Chicago (ORD)

0.3%

Chicago (MDW) 78%

Houston (IAH) 3%

Houston (HOU) 78%

Dallas/Ft. Worth (DFW) 2% Dallas/Ft. Worth (DAL)

94%

Washington (DCA) 3% Washington (IAD) 3%

Washington (BWI) 41%

Newark2%

New York (JFK) 24% New York (LGA) 4%

Westchester County

Islip55%

Providence 20%

Boston 3%

Manchester 20%

Large Hub

Medium Hub

Small Hub

Ontario 61%

The Low Fare/Niche Carrier Segment: They Keep Growing – Because They Can …

The Low Fare/Niche Carrier Segment: They Keep Growing – Because They Can …

-12%

+35%

+16%

+17%

+20%

+5% -21%

A Constant Reminder:IT Keeps Growing – Because IT Can …A Constant Reminder:IT Keeps Growing – Because IT Can …

Low Fare Carrier Market Penetration Has Been Greatest in the Largest U.S. Markets Since 9/11

Low Fare Carrier Market Penetration Has Been Greatest in the Largest U.S. Markets Since 9/11

Low FareCarrier Service

Low FareCarrier Service

PointsChangePoints

Change

Large Hubs -12.9% +0.7% +2.1%

Medium Hubs -10.0% +0.1% +3.3%

Small Hubs -9.7% +3.9% +2.3%

Non Hubs -12.5% -9.1% +0.7%

We estimate that the Low Fare/Niche carrier segment of the industry has captured 2.4 points of

domestic market share in the past 6 months

Total ServiceIn Markets

Total ServiceIn Markets

The Low Fare/Niche Carrier Segment of the Industry Has Increased Its Share of Service in Every U.S. Region Since 9/11

The Low Fare/Niche Carrier Segment of the Industry Has Increased Its Share of Service in Every U.S. Region Since 9/11

37.8%

32.4%

0% 6% 12% 18% 24% 30% 36% 42%

September 2001

September 2001

March 2002

March 2002

16.1%

14.3%

0% 6% 12% 18% 24% 30% 36% 42%

September 2001

September 2001

March 2002

March 2002

30.3%

28.0%

0% 6% 12% 18% 24% 30% 36% 42%

September 2001

September 2001

March 2002

March 2002

11.7%

10.9%

0% 6% 12% 18% 24% 30% 36% 42%

September 2001

September 2001

March 2002

March 2002

15.5%

13.3%

0% 6% 12% 18% 24% 30% 36% 42%

September 2001

September 2001

March 2002

March 2002

7.4%

9.6%

0% 6% 12% 18% 24% 30% 36% 42%

Sept.2001Sept.2001

March 2002

March 2002

+5.4 pts.

+2.2 pts.

+2.2 pts.

Capacity Growth by the Low Fare/ Niche Carrier Segment is Forcing the Hand of the Network Carriers

Capacity Growth by the Low Fare/ Niche Carrier Segment is Forcing the Hand of the Network Carriers

The Difference Between Capacity Reductions and Network Effect is Evident

Source: Eclat Air Service Model, March 2002 vs. September 10, 2001Note: Changes in carrier service reflect total; changes in hub service reflect nonstop only.

0%-3%-21% -14% -10% -6% +5%

UnitedLAX -32%SFO -27%IAD -25%DEN -20%ORD -9%

NorthwestMEM -23%MSP -3%DTW -2%

American/TWA

MIA -10%ORD -11%DFW -7%STL -11%

US AirwaysPHL -4%CLT -6%PIT -11%

ContinentalEWR -12%IAH -4%CLE +10%

DeltaJFK -27%DFW+20%ATL +3%SLC +2%CVG +11%

Network Carrier Exposure to Low Fare Carrier Competition Generally, and Southwest Specifically

Network Carrier Exposure to Low Fare Carrier Competition Generally, and Southwest Specifically

Increased Exposure Since 9/11

Delta

American

US Airways

Decreased Exposure Since 9/11

Continental

United

Exposure Unchanged Since 9/11

Northwest

Percent exposure to SouthwestExposure to low fare competition

USAirways

American

Delta

0 20 40 60 80 100

Northwest

United

Continental

Low Fare Index (Delta = 100 )

The Network Carriers’Low Cost Competitive Weapon

The Network Carriers’Low Cost Competitive Weapon

How the Network Carriers Utilize Their Respective Regional Jet FleetsHow the Network Carriers Utilize Their Respective Regional Jet Fleets

1st Quarter 2002 vs. 2nd Quarter 19961st Quarter 2002 vs. 2nd Quarter 1996

0%

10%20%

30%40%

50%60%

70%80%

90%

AA CO DL NW UA US

NewNew Replace JetReplace Jet

0%

5%10%

15%20%

25%30%

35%40%

45%

AA CO DL NW UA US

0%

2%

4%

6%

8%

10%

12%

14%

16%

AA CO DL NW UA US0%

10%

20%

30%

40%

50%

60%

70%

80%

AA CO DL NW UA US

Replace TurboReplace Turbo Supplement JetSupplement Jet

Average 21.3%Average 21.3%

Average 23.6%Average 23.6%

Average 9.0%Average 9.0%

Average 43.0%Average 43.0%

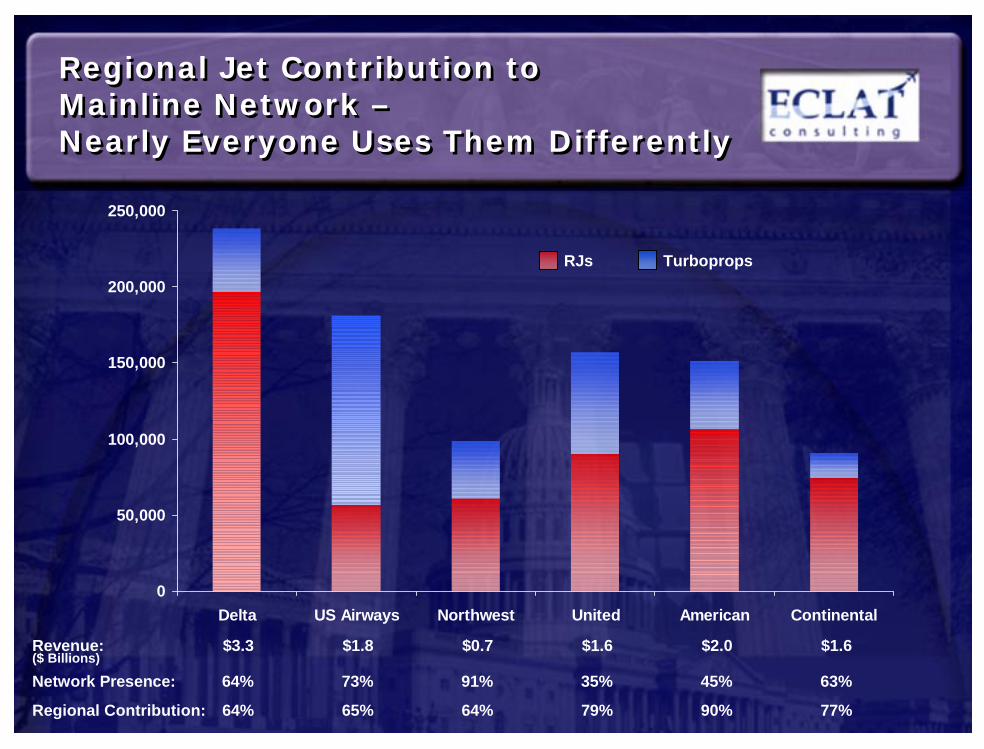

Regional Jet Contribution to Mainline Network –Nearly Everyone Uses Them Differently

Regional Jet Contribution to Mainline Network –Nearly Everyone Uses Them Differently

0

50,000

100,000

150,000

200,000

250,000

Delta US Airways Northwest United American Continental

TurbopropsRJs

Revenue: $3.3 $1.8 $0.7 $1.6 $2.0 $1.6($ Billions)

Network Presence: 64% 73% 91% 35% 45% 63%

Regional Contribution: 64% 65% 64% 79% 90% 77%

American’s Non-Hub Flying With RJs –Non-Mainline Markets With Strategic Value to the Overall Network

American’s Non-Hub Flying With RJs –Non-Mainline Markets With Strategic Value to the Overall Network

Raleigh/Durham

New York-LGA

Nashville

BaltimoreColumbus

Washington-DCA

New York-JFKNewark

Norfolk

Philadelphia

Richmond

Cleveland

Detroit

Ft. Lauderdale

Washington-IAD

Pittsburgh

Phoenix

Los Angeles

Oakland

Albuquerque

-15% or More-10% to -14%-5% to -9%0% to -4%

Fayetteville

Hartford

Boston

Bangor

Westchester Co.

Providence

Portland

Post-9/11 CapacityReductions by Region

Deployment of RJ CapacitySince 9/11 – Is This US Airways’ Network or Delta’s?

Deployment of RJ CapacitySince 9/11 – Is This US Airways’ Network or Delta’s?

Bangor

New York-LGA

Baltimore

Newark

PensacolaMobile

Oklahoma City

Orlando

TallahasseeAlbany

Dothan

Indianapolis

Grand Rapids

Augusta

HarrisburgChicago

Kansas City

Jacksonville

Monroe

Atlanta

Toronto

Halifax

Boston

Portland

PhiladelphiaAllentown

South Bend

Montreal

Charlottesville

Texarkana

Wilkes Barre

Pittsburgh

Cincinnati

Detroit

Toledo

Albany

Houston-HobbyHouston-IAH

Corpus Christi

San Antonio

Baton Rouge

Evansville CharlestonNewport News

Huntington

AshevilleTri-CitiesNashville Raleigh/DurhamMemphis

FlorenceHuntsville

Dallas/Ft. WorthBrunswick

-15% or More-10% to -14%-5% to -9%0% to -4%

Post-9/11 CapacityReductions by Region

Conclusions/QuestionsConclusions/Questions

! Over the most recent past, the Low Cost/Niche carriers have measurably increased their share of the domestic market. In justthe past six months, they have potentially increased their share2.5 points.

! The network carriers’ fear of significant encroachment is underscored by the capacity expansions announced by the largest carriers.

! The influence of the low cost carriers in the West was significant,and further inroads have been made since 9/11.

! Likewise, the low fare segment has increased its presence significantly along the East Coast over the past six months –a trend that will continue.

! Also, the growth of the mid-continent hubs by the low fare segment should be a concern, as pricing discipline will only increase. This growth will undermine pricing in the transcon market, which will bean important footnote in a bankruptcy filing or a loan guaranteeapplication.

! Over the most recent past, the Low Cost/Niche carriers have measurably increased their share of the domestic market. In justthe past six months, they have potentially increased their share2.5 points.

! The network carriers’ fear of significant encroachment is underscored by the capacity expansions announced by the largest carriers.

! The influence of the low cost carriers in the West was significant,and further inroads have been made since 9/11.

! Likewise, the low fare segment has increased its presence significantly along the East Coast over the past six months –a trend that will continue.

! Also, the growth of the mid-continent hubs by the low fare segment should be a concern, as pricing discipline will only increase. This growth will undermine pricing in the transcon market, which will bean important footnote in a bankruptcy filing or a loan guaranteeapplication.

Eclat Consulting, Inc.1555 Wilson Boulevard, Suite 602

Arlington, VA 22209 USAwww.eclatconsulting.com

Telephone 703.294.5880 Facsimile 703.294.5899