the rcs group consolidated financial … · rcs cards proprietary limited is a registered credit...

TRANSCRIPT

Building on our core strengths

CONTENTS

Directors’ responsibility statement and company secretary statement 2

Directors’ report 3 - 5

Audit committee report 6

Independent auditor’s report 7 - 11

Consolidated statement of financial position 13

Consolidated income statement 14

Consolidated statement of comprehensive income 15

Consolidated statement of changes in equity 16

Consolidated statement of cash flows 17

Accounting policies 19 - 29

Notes to the consolidated financial statements 31 - 58

These financial statements have been prepared under the supervision of the Corporate Finance Manager: HP Fick Chartered Accountant (SA).

These financial statements represent the financial information of The RCS Group and have been audited in compliance with section 30 of the Companies Act of South Africa.

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 01

02 | THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016

DIRECTORS’ RESPONSIBILITY STATEMENT

The directors are responsible for the preparation and fair presentation of the consolidated financial statements of

BNP Paribas Personal Finance South Africa limited, its subsidiaries and its associates (hereafter referred to as

“The RCS Group”), comprising the consolidated statement of financial position as at 31 December 2016, and the

consolidated income statement, the consolidated statements of comprehensive income, changes in equity and cash flows

for the year then ended, and the notes to the consolidated financial statements, which include a summary of significant

accounting policies and other explanatory notes, in accordance with International Financial Reporting Standards (IFRS)

and the requirements of the Companies Act of South Africa. In addition, the directors are responsible for preparing the

directors’ report.

The directors are also responsible for such internal control as the directors deem necessary to enable the

preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or

error and for maintaining adequate accounting records and an effective system of risk management.

The directors have made an assessment of the ability of The RCS Group to continue as a going concern and have no

reason to believe that the businesses will not be a going concern in the year ahead. The auditor is responsible for

reporting on whether the consolidated financial statements are fairly presented in accordance with the applicable

financial reporting framework.

APPROVAL OF THE FINANCIAL STATEMENTSThe consolidated financial statements of The RCS Group, as identified in the first paragraph, were approved by the board of

directors on 24 April 2017 and were signed by:

CP De Wit

Chief Financial officer

COMPANY SECRETARY STATEMENTI hereby confirm, in my capacity as company secretary of BNP Paribas Personal Finance South Africa limited, that for

the year ended 31 December 2016, the company has filed all required returns and notices in terms of the Companies Act,

2008 and that all such returns and notices are to the best of my knowledge and belief true, correct and up to date.

GS Harker

Company Secretary

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 03

DIRECTORS’ REPORT

The directors have pleasure in presenting their report for the year ended 31 December 2016:

1. BuSINESS ACTIVITIESThe RCS Group is an operationally independent consumer finance business that provides a broad range of financial

services under its own brand and in association with a number of retail entities in South Africa, Namibia and

Botswana. The Cards business unit offers various utility card products through participating merchant outlets, while

the loan business unit offers individual unsecured loans and insurance products (for more detail on these segments

refer to note 3 of the financial statements).

2. SuBSIDIARY COMPANIESThe RCS Group constitutes BNP Paribas Personal Finance South Africa limited (registration number:

2000/017884/06) and its subsidiaries, RCS Botswana Proprietary limited, RCS Cards Proprietary limited,

RCS Collections Proprietary limited, RCS Home loans Proprietary limited and RCS Investment Holdings Namibia

Proprietary limited (for more detail on these subsidiaries refer to note 27 of the financial statements).

The financial statements for BNP Paribas Personal Finance South Africa limited are presented in a separate set

of financial statements.

3. GENERAL REVIEw OF OPERATIONSThe results for the year ended 31 December 2016 are described in the accompanying consolidated financial

statements.

4. COMPLIANCERCS Cards Proprietary limited is a registered credit provider (NCR registration number NCRCP 38) and a registered

service provider with the financial services board (FSB registration number 44481).

5. CORPORATE GOVERNANCEThe directors endorse the Code of Corporate Practices and Conduct as suggested by King III. For the financial year

ended 31 December 2016 the directors are satisfied that The RCS Group materially applies King III, apart from the

areas noted in the table on the next page. The main areas of departure are accepted due to the fact that BNP Paribas

Personal Finance South Africa limited is a wholly owned subsidiary of the multi-national banking and financial

services group, BNP Paribas Société Anonyme, listed on the Paris Stock exchange.

04 | THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016

DIRECTORS’ REPORT (continued)

6. CHANGE IN FINANCIAL YEAR ENDDuring the previous financial period, the financial year changed from 31 March to 31 December to align with

the year end reporting requirements of the shareholder. The prior period’s financial results are therefore only

representative of a 9-month period and accordingly are not comparative to the current year under review.

7. EVENTS AFTER THE REPORTING PERIODThe directors are not aware of any matters or circumstances arising since the end of the financial year that may

materially affect the amounts and disclosure of these financial statements.

8. DISTRIBuTION TO SHAREHOLDERA distribution to shareholder amounting to R450 million was declared after the date of the reporting period but

before the financial statements were authorised for issue (31 December 2015: R250 million).

9. DIRECTORSThe directors in office at the date of this report are:

ExEcutivE dirEctors

RF Adams South African (Chief executive officer)

CP De Wit (Appointed 1 August 2016) South African(Chief Financial officer)

NoN-ExEcutivE dirEctors

ACPM van Groenendael Belgian

BPS Cavelier French

I Perret-Noto French

VSK Khandelwal (Appointed 1 August 2016) French

SW van der Merwe South African

E Oblowitz South African

(Independent)

The board should comprise a balance of power, with a majority of non-executive directors. The majority of non-executive directors should be independent.

The majority of non-executive directors should be independent.

As The RCS Group only has one shareholder, BNP Paribas Société Anonyme, there is only one independent non-executive director who also serves as the audit committee chairman, whilst the majority non-executive directors are senior executives of the shareholder.

As The RCS Group only has one shareholder, BNP Paribas Société Anonyme, the shareholder appoints the non-executive directors.

At least one third of the non-executive directors should rotate every year.

King III PrincipleLimited Application

Recommended Practice Application

Comments

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 05

DIRECTORS’ REPORT (continued)

chaNgEs to dirEctors iN thE currENt fiNaNcial yEar

SW van der Merwe resigned as an executive director on 1 August 2016 and remains on the board in a non-executive capacity.

RF Adams was appointed as Ceo on 1 August 2016, having previously served on the board as Chief operating officer.

JJ Snyman resigned as an executive director on 1 August 2016.

oPM Renard resigned as an executive director on 1 August 2016.

VNA Kodjo Diop resigned from the board on 1 August 2016.

10. COMPANY SECRETARYThe company secretary at the date of this report is GS Harker.

11. BuSINESS/REGISTERED ADDRESS

BusiNEss addrEss

RCS Building

Golf Park

Raapenberg Road

Mowbray

7700

12. HOLDING COMPANYThe RCS Group’s immediate holding company is BNP Paribas Personal Finance Société Anonyme. The ultimate shareholder is

BNP Paribas Société Anonyme, incorporated in France and listed on the Paris Stock exchange.

13. NAME CHANGEThe RCS Group holding company, RCS Investment Holdings limited’s name changed to BNP Paribas Personal

Finance South Africa limited on 26 January 2017.

14. AuDITORSThe independent auditing firm Deloitte & Touche audited the financial statements. They were provided with

unrestricted access to all financial records and related data, including minutes of all meetings of the shareholder,

the board of directors and committees of the board. The directors believe that all representations made to

the independent auditors during their audit were valid and appropriate. Deloitte & Touche was appointed as

independent auditors effective 1 June 2016 by the RCS Board Audit Committee. The prior period’s independent

auditors was KPMG. Deloitte & Touche’s audit report is presented on pages 7 to 11.

Postal addrEss

Po Box 6523

Parow east

Cape Town

7501

06 | THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016

AuDIT COMMITTEE REPORT

The RCS audit committee is an independent statutory

committee appointed by the board of directors in terms of

the Companies Act (Act 71 of 2008) (“the Act”).

The committee comprises of one independent non-executive

director, who is also the chairman of the audit committee,

and two non-executive directors. The audit committee met

three times during the year ended 31 December 2016.

In addition, the chairman of the audit committee held

various meetings with representatives of the internal and

external auditors during the year under review.

The committee’s responsibilities include statutory duties in

terms of the Act. The committee also applies the applicable

principles of the King III Report on Corporate Governance

for South Africa. The committee’s terms of reference are

determined by a board-approved charter. The committee

conducted its affairs in compliance with, and discharged its

responsibilities in terms of, its charter for the period ended

31 December 2016.

The committee performed, inter alia, the following duties

during the year under review:

– Satisfied itself that the external auditor is independent of

the company, as set out in section 94(9) of the Act;

– In consultation with executive management, agreed to the

terms, audit plan and budgeted fees for the

31 December 2016 financial period;

– Approved the nature and extent of non-audit services that

the external auditor may provide;

– Satisfied itself, based on the information and explanations

supplied by management and obtained through

discussions with the independent external auditor and

internal auditors, that the system of internal financial

controls is effective and forms a basis for the preparation

of reliable financial statements;

– Reviewed the accounting policies and The RCS Group

financial statements for the period ended 31 December

2016 and, based on the information provided to the

committee, considers that The RCS Group complies, in

all material respects, with the requirements of the Act

and IFRS;

– Reviewed the audit report of the external auditor that

includes the key audit matters as required by ISA 701

(Communicating Key Audit Matters in the Independent

Auditor’s Report);

– ensured that the company’s internal audit function

is independent and had the necessary resources and

authority to enable it to discharge its duties;

– Approved the internal audit plan as well as any

amendments thereto;

– Met with the external and internal auditors, separately and

together, without management being present;

– Satisfied itself that The RCS Group financial director and

the finance function has appropriate expertise, experience

and competence;

– Considered as part of the approval of the financial

statements any accounting treatments, significant unusual

transactions, or accounting estimates and judgements that

could be contentious; and

– Reviewed management’s assessment of going concern

and sustainability and made a recommendation to the

board that the going concern concept be adopted by

The RCS Group.

E Oblowitz

Audit Committee Chairman

INDEPENDENT AuDITOR’S REPORT

REPORT ON THE AuDIT OF THE FINANCIAL STATEMENTS To the shareholder of BNP Paribas Personal Finance

South Africa limited:

OPINION

We have audited the consolidated financial statements

of BNP Paribas Personal Finance South Africa limited

and its subsidiaries (“The RCS Group”) set out on

pages 13 to 58, which comprise the consolidated

statement of financial position as at 31 December

2016, the consolidated income statement, the

consolidated statement of comprehensive income,

the consolidated statement of changes in equity and

the consolidated statement of cash flows for the year

then ended, and the notes to the consolidated financial

statements, including a summary of significant

accounting policies.

In our opinion, the consolidated financial statements

present fairly, in all material respects, the consolidated

financial position of The RCS Group as at 31 December

2016, and its consolidated financial performance and

consolidated cash flows for the year then ended in

accordance with International Financial Reporting

Standards (IFRSs) and the requirements of the

Companies Act of South Africa.

BASIS FOR OPINIONWe conducted our audit in accordance with

International Standards on Auditing (ISAs). our

responsibilities under these standards are further

described in the Auditor’s Responsibilities for the

Audit of the Consolidated Financial Statements section

of our report. We are independent of The RCS Group in

accordance with the Independent Regulatory Board for

Auditors Code of Professional Conduct for Registered

Auditors (IRBA Code) and other independence

requirements applicable to performing audits of

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 07

financial statements in South Africa. We have fulfilled

our other ethical responsibilities in accordance with

the IRBA Code and in accordance with other ethical

requirements applicable to performing audits in

South Africa. The IRBA Code is consistent with the

International ethics Standards Board for Accountants

Code of ethics for Professional Accountants (Parts A

and B). We believe that the audit evidence we have

obtained is sufficient and appropriate to provide a

basis for our opinion.

KEY AuDIT MATTERSKey audit matters are those matters that, in our

professional judgement, were of most significance in

our audit of the consolidated financial statements of

the current period. These matters were addressed in

the context of our audit of the consolidated financial

statements as a whole, and in forming our opinion

thereon, and we do not provide a separate opinion on

these matters.

08 | THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016

Compliance with laws and regulations

Impairment of card and loan receivables

Liquidity and access to adequate and affordable funding

Key Audit Matter How the matter was addressed in the audit

The global financial services industry has been the subject of significantly increased regulations in the aftermath of the global financial crisis. More recently, due to large failures in, and public outcries about practices in the unsecured lending industry, the industry has also been on the receiving end of increased scrutiny and regulation. These laws and regulations are increasingly complex and difficult to manage due to the impact it has on systems and the increased controls and training required to make sure that staff comply with the myriad of requirements in the process of originating new loans or collecting on existing loans. Recent events in South Africa have also indicated that non-compliance may result in significant fines and that reports of non-compliance, whether proven or not, may also be very damaging to the credibility of the institution impacting on its ability to retain credit ratings and gain access to further funding at affordable rates. Accordingly the compliance with laws and regulations is considered a key audit matter. The RCS Group’s compliance approach is disclosed in note 30.

Card and loan receivables after providing for impairment accounts for more than 85% of the assets of The RCS Group. These receivables are unsecured and generally provided to customers with higher levels of default compared to the more traditional and often secured loans provided by the banking industry. Default on credit granted is a necessary concomitant of unsecured lending. Due to the complexity and subjectivity of the assessment of the required impairment of card and loan receivables, it is considered a key audit matter.

As is required by the accounting standards, and disclosed notes 1.4, 5 and 30, The RCS Group use specialists to assist with inherently subjective impairment assessments of these receivables through complex modelling (using the Markov model) of expected future cash receipts from customers, also considering evidence not yet evident in the mathematical models, to inform their judgement of the final impairment amount recorded.

The nature of the business requires careful and complex liquidity analysis and management taking into account elements such as funding that matures in the 12 months after the financial year-end, the cash available from collections, new card and loan advances, the average tenure of funding agreements, the average credit collection term, expenses incurred in managing the business, and transactions with and support from the shareholder. Access to and the cost of funding is impacted by aspects such as the credit rating of The RCS Group, perceptions about the South African unsecured lending market, and market volatility. The RCS Group’s funders also define events of default and performance covenants that must be complied with. Accordingly, liquidity and access to adequate and affordable funding is considered a key audit matter.

As is disclosed in notes 17 and 30, The RCS Group manages liquidity and funding by preparing cash flow forecasts under both “normal” and “stressed” scenarios.

Our audit procedures included the following procedures:- Understanding and assessing the legal and regulatory framework

that The RCS Group operates in, the compliance culture of the organisation including the tone at the top, the processes, internal controls and governance structures that exist, how these are documented, how compliance matters are dealt with, and the adequacy of compliance disclosures to regulators and in the annual financial statements; and

- Performing tests of these and specific compliance aspects such as with the National Credit Act and its regulations.

Our audit procedures included the following:- Understanding:

• The RCS Group’s credit granting and collection strategies; • New loan origination, collections, impairment modelling, and data

management processes, systems and methodologies; and • The related governance processes and controls in place; - Obtaining the required credit and collections data and testing these

for accuracy and completeness;- Using credit and modelling specialists to develop our own

impairment model, to compare the outcome with The RCS Group’s, and to assess differences in terms of accounting standards and standard market practices;

- Assessing The RCS Group’s adjustments to model outcomes for reasonability;

- Considering the adequacy of impairment disclosure in the financial statements; and

- Retrospective testing of prior year impairment provisions.

Our audit procedures included the following:- Obtaining an understanding of:

• the liquidity management process; • the related governance processes and controls in place; • The RCS Group’s funding strategies; • future cash flow requirements; • sources of funding; and • The RCS Group’s market credibility based on: actual funding

experience over the last 12 months and its credit rating.- Testing the reasonability of management’s assessment for the

12 month period after year-end, under normal and in stressed conditions, of: • cash flow forecasts; • funding plans; • covenant compliance; and • the likelihood of events of default occurring.

- Considering the adequacy of liquidity disclosure in the financial statements; and

- Retrospective testing of prior year funding plans.

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 09

INDEPENDENT AuDITOR’S REPORT (continued)

OTHER INFORMATIONThe directors are responsible for the other information.

The other information comprises the Directors’

Responsibility Statement, Directors’ Report and

the Audit Committee’s Report, as required by the

Companies Act of South Africa, which we obtained

prior to the date of this auditor’s report. The other

information does not include the consolidated financial

statements and our auditor’s report thereon.

our opinion on the consolidated financial statements

does not cover the other information and we do not

express an audit opinion or any form of assurance

conclusion thereon.

In connection with our audit of the consolidated

financial statements, our responsibility is to read the

other information and, in doing so, consider whether

the other information is materially inconsistent with

the consolidated financial statements or our knowledge

obtained in the audit, or otherwise appears to be

materially misstated.

If, based on the work we have performed on the other

information that we obtained prior to the date of this

auditor’s report, we conclude that there is a material

misstatement of this other information, we are

required to report that fact. We have nothing to report

in this regard.

RESPONSIBILITIES OF THE DIRECTORS FOR THE CONSOLIDATED FINANCIAL STATEMENTS The directors are responsible for the preparation

and fair presentation of the consolidated financial

statements in accordance with International Financial

Reporting Standards and the requirements of the

Companies Act of South Africa, and for such internal

control as the directors determine is necessary to

enable the preparation of consolidated financial

statements that are free from material misstatement,

whether due to fraud or error.

In preparing the consolidated financial statements, the

directors are responsible for assessing

The RCS Group’s ability to continue as a going

concern, disclosing, as applicable, matters related

to going concern and using the going concern basis

of accounting unless the directors either intend to

liquidate The RCS Group or to cease operations, or

have no realistic alternative but to do so.

10 | THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016

INDEPENDENT AuDITOR’S REPORT (continued)

AuDITOR’S RESPONSIBILITIES FOR THE AuDIT OF THE CONSOLIDATED FINANCIAL STATEMENTSour objectives are to obtain reasonable assurance

about whether the consolidated financial statements as

a whole are free from material misstatement, whether

due to fraud or error, and to issue an auditor’s report

that includes our opinion. Reasonable assurance

is a high level of assurance, but is not a guarantee

that an audit conducted in accordance with ISAs will

always detect a material misstatement when it exists.

Misstatements can arise from fraud or error and are

considered material if, individually or in the aggregate,

they could reasonably be expected to influence the

economic decisions of users taken on the basis of

these consolidated financial statements.

As part of an audit in accordance with ISAs, we

exercise professional judgement and maintain

professional scepticism throughout the audit. We also:

– Identify and assess the risks of material

misstatement of the consolidated financial

statements, whether due to fraud or error, design

and perform audit procedures responsive to those

risks, and obtain audit evidence that is sufficient

and appropriate to provide a basis for our opinion.

The risk of not detecting a material misstatement

resulting from fraud is higher than for one resulting

from error, as fraud may involve collusion, forgery,

intentional omissions, misrepresentations, or the

override of internal control.

– obtain an understanding of internal control relevant

to the audit in order to design audit procedures

that are appropriate in the circumstances, but not

for the purpose of expressing an opinion on the

effectiveness of The RCS Group’s internal control.

– evaluate the appropriateness of accounting policies

used and the reasonableness of accounting estimates

and related disclosures made by the directors.

– Conclude on the appropriateness of the directors’

use of the going concern basis of accounting and

based on the audit evidence obtained, whether

a material uncertainty exists related to events or

conditions that may cast significant doubt on The

RCS Group’s ability to continue as a going concern.

If we conclude that a material uncertainty exists,

we are required to draw attention, in our auditor’s

report, to the related disclosures in the consolidated

financial statements or, if such disclosures are

inadequate, to modify our opinion. our conclusions

are based on the audit evidence obtained up to the

date of our auditor’s report. However, future events

or conditions may cause The RCS Group to cease to

continue as a going concern.

– evaluate the overall presentation, structure and

content of the consolidated financial statements,

including the disclosures, and whether the

consolidated financial statements represent the

underlying transactions and events in a manner that

achieves fair presentation.

– obtain sufficient appropriate audit evidence

regarding the financial information of the entities or

business activities within The RCS Group to express

an opinion on the consolidated financial statements.

We are responsible for the direction, supervision

and performance of The RCS Group audit. We remain

solely responsible for our audit opinion.

We communicate with the directors regarding, among

other matters, the planned scope and timing of the

audit and significant audit findings, including any

significant deficiencies in internal control that we

identify during our audit.

We also provide the directors with a statement that

we have complied with relevant ethical requirements

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 11

INDEPENDENT AuDITOR’S REPORT (continued)

regarding independence, and communicate to them all

relationships and other matters that may reasonably

be thought to bear on our independence, and where

applicable, related safeguards.

From the matters communicated with the directors, we

determine those matters that were of most significance

in the audit of the consolidated financial statements

of the current period and which are therefore the

key audit matters. We describe these matters in our

auditor’s report unless law or regulation precludes

public disclosure about the matter or when, in

extremely rare circumstances, we determine that a

matter should not be communicated in our report

because the adverse consequences of doing so would

reasonably be expected to outweigh the public interest

benefits of such communication.

REPORT ON OTHER LEGAL AND REGuLATORY REquIREMENTSIn terms of the IRBA Rule published in Government

Gazette Number 39475 dated 4 December 2015, we

report that Deloitte & Touche has been the auditor of

BNP Paribas Personal Finance South Africa limited

for 1 year.

Deloitte & Touche

Registered Auditor

Per: Danie Crowther

Partner

24 April 2017

Resilient and positioned

for further growth

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 13

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

31 December 31 December 2016 2015 Notes R’000 R’000

ASSETSCash and cash equivalents 4 553 623 551 918

Card and loan receivables 5 6 277 260 5 961 948

other receivables 6 25 651 11 625

Amount receivable from insurer 7 96 535 94 850

Taxation 69 699 5 935

Property and equipment 8 62 412 68 491

Intangible assets 9 25 206 24 122

Goodwill 10 56 855 56 855

Deferred taxation 11 177 424 172 629

Total assets 7 344 665 6 948 373

EquITYStated capital 14 2 386 636 2 636 636

Accumulated profit / (loss) 149 812 (226 441)

Foreign currency translation reserve 15 4 031 9 298

Total equity 2 540 479 2 419 493

LIABILITIESFunding 17 4 325 167 4 082 400

Trade and other payables 18 479 019 446 480

Total liabilities 4 804 186 4 528 880

Total equity and liabilities 7 344 665 6 948 373

as at 31 December 2016

14 | THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016

CONSOLIDATED INCOME STATEMENT

for the year ended 31 December 2016

12 Months ended 9 Months ended 31 December 2016 31 December 2015 Notes R’000 R’000

Interest earned 20 1 471 362 1 060 127

Interest expense (361 369) (235 420)

Net interest income 1 109 993 824 707

other income 21 789 506 526 376

Transaction fee expense (88 350) (63 075)

Net trading income 1 811 149 1 288 008

operating costs (765 538) (570 859)

Cost of risk 22 (524 902) (439 335)

Profit before taxation 23 520 709 277 814

Taxation 24 (144 456) (79 974)

Profit for the period 376 253 197 840

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 15

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

for the year ended 31 December 2016

12 Months ended 9 Months ended 31 December 2016 31 December 2015 Notes R’000 R’000

Profit for the period 376 253 197 840

Other comprehensive income, net of taxation

Items that are or may be reclassified to profit or loss:

Foreign currency translation differences for foreign operation 15 (5 267) 7 625

effective portion of changes in fair value of cash flow hedges 16 - (712)

Cashflow hedges - reclassified to profit or loss - (10 248)

Other comprehensive income for the period (5 267) (3 335)

Total comprehensive income for the period 370 986 194 505

16 | THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016

CONSOLIDATED STATEMENT OF CHANGES IN EquITY

for the year ended 31 December 2016

Stated Foreign Cash flow Retained Total equity capital currency hedge income / attributable translation reserve (accumulated to

parent

reserve loss) R’000 R’000 R’000 R’000 R’000

Balance at 2 636 636 1 673 10 960 (424 281) 2 224 988 1 April 2015

Total comprehensive - 7 625 (10 960) 197 840 194 505income for the period

Profit for the period - - - 197 840 197 840

other comprehensive income, net of taxation:

Foreign currency translation - 7 625 - - 7 625differences for foreign operations

effective portion of changes in - - (712) - (712)fair value of cash flow hedges

Disposal of cash flow hedge - - (10 248) - (10 248)

Balance at 2 636 636 9 298 - (226 441) 2 419 49331 December 2015

Balance at 2 636 636 9 298 - (226 441) 2 419 4931 January 2016

Total comprehensive (250 000) (5 267) - 376 253 120 986income for the period

Profit for the year - - - 376 253 376 253

Distribution of capital (250 000) - - - (250 000)

other comprehensive income, net of taxation:

Foreign currency translation - (5 267) - - (5 267)differences for foreign operations

Balance at 2 386 636 4 031 - 149 812 2 540 47931 December 2016

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 17

CONSOLIDATED STATEMENT OF CASH FLOwS

for the year ended 31 December 2016

12 Months ended 9 Months ended 31 December 2016 31 December 2015 Notes R’000 R’000

CASH FlOWS FROM OPERATING ACTIVITIES

Cash generated / (utilised) in operations 25 247 464 (38 117)

Taxation paid 26 (213 015) (158 753)

Net cash inflow / (outflow) from operating activities 34 449 (196 870)

CASH FlOWS FROM INVESTING ACTIVITIES

Acquisition of property and equipment (16 645) (19 065)

Acquisition of intangible assets (14 030) (7 352)

Proceeds from disposal of property and equipment 5 164 394

Proceeds from disposal of equity accounted investment - 1 600

Net cash outflow from investing activities (25 511) (24 423)

CASH FlOWS FROM FINANCING ACTIVITIES

Proceeds from funding 5 197 867 3 699 977

Repayment of funding (4 955 100) (3 387 877)

Distribution of capital (250 000) -

Funding repaid by group companies - 10

Decrease in amounts owing from group companies - 81

Proceeds on disposal of interest rate swaps - 14 233

Net cash (outflow) / inflow from financing activities (7 233) 326 424

Net increase in cash and cash equivalents 1 705 105 131

Cash and cash equivalents at beginning of the period 551 918 446 787

Cash and cash equivalents at end of the period 4 553 623 551 918

Optimistic and inspired

by our customers

ACCOuNTING POLICIES

for the year ended 31 December 2016

1. PRESENTATION OF FINANCIAL STATEMENTSThe holding company, BNP Paribas Personal Finance

South Africa limited, is a company domiciled in South

Africa. The consolidated financial statements as at

and for the year ended 31 December 2016 comprise

the company and its subsidiaries (together referred

to as “The RCS Group”). The company has foreign

subsidiaries operating in Namibia and Botswana.

The consolidated financial statements are prepared

in accordance with IFRS and the requirements of the

Companies Act of South Africa. The accounting policies

have been consistently applied with those adopted in

the prior financial period.

During the previous financial period, the financial year

changed from 31 March to 31 December to align with

the reporting requirements of the shareholder. The prior

period financial results are therefore only representative

of a 9-month period. The current and prior period

results are therefore not comparable.

1.1 Basis of PrEParatioN

The consolidated financial statements have been

prepared on the basis that The RCS Group is a going

concern and on the historical cost basis.

The consolidated financial statements were authorised

for issue by the board of directors on 24 April 2017.

1.2 fuNctioNal aNd PrEsENtatioN currENcy

These consolidated financial statements are

presented in South African Rands, which is BNP

Paribas Personal Finance South Africa limited’s

functional and presentation currency. All amounts

have been rounded to the nearest thousand, unless

otherwise indicated.

1.3 Basis of coNsolidatioN

Subsidiaries

The financial statements of subsidiaries are prepared

for a consistent reporting period using consistent

accounting policies.

Business combination

Business combinations are accounted for using the

acquisition method as at the acquisition date, which is

the date on which control is transferred to The RCS Group.

The RCS Group controls an entity when The RCS Group

is exposed to, or has rights to, variable returns from

its involvement with the entity and has the ability to

affect those returns through its power over the entity.

Subsidiaries are fully consolidated from the date on

which control is transferred to The RCS Group. They

are consolidated until the date that control ceases.

The RCS Group measures goodwill at the acquisition

date as:

• the fair value of the consideration transferred; plus

• the recognised amount of any non-controlling interest

in the acquiree; plus

• if the business combination is achieved in stages, the

fair value of the pre-existing equity interest in the

acquiree; less

• the net recognised amount (generally fair value)

of the identifiable assets acquired and liabilities

assumed.

When the excess is negative, a gain on bargain

purchase is recognised immediately in the statement

of comprehensive income.

The consideration transferred does not include

amounts related to the settlement of pre-existing

relationships. Such amounts generally are recognised

in profit or loss.

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 19

20 | THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016

Transaction costs, other than those associated with the

issue of debt or equity securities, that The RCS Group

incurs in connection with a business combination are

expensed as incurred.

Any contingent consideration payable is measured

at fair value at the acquisition date. If the contingent

consideration is classified as equity it is not remeasured.

otherwise, subsequent changes in the fair value of the

contingent consideration are recognised in profit or loss.

loss of Control

on the loss of control, The RCS Group derecognises

the assets and liabilities of the subsidiary, any non-

controlling interest and the other components of equity

related to the subsidiary. Any surplus or deficit arising

on the loss of control is recognised in the statement of

comprehensive income.

Investment in associates

An associate is an entity over which The RCS Group has

significant influence and which is neither a subsidiary

nor a joint arrangement. Significant influence is the

power to participate in the financial and operating

policy decisions of the investee but is not control or joint

control over those policies.

An investment in associate is accounted for using the

equity method, except when the investment is classified

as held for sale in accordance with IFRS 5 Non-current

assets held-for-sale and discontinued operations. under

the equity method, investments in associates are carried

in the consolidated statement of financial position at

cost adjusted for post acquisition changes in The RCS

Group’s share of net assets of the associate, less any

impairment losses.

losses in an associate in excess of The RCS Group’s

interest in that associate, are recognised only to the extent

that The RCS Group has incurred a legal or constructive

obligation to make payments on behalf of the associate.

Any goodwill on acquisition of an associate is included

in the carrying amount of the investment, however, a

gain on acquisition is recognised immediately in the

statement of comprehensive income.

Profits or losses on transactions between The RCS Group

and an associate are eliminated against the investment

to the extent of The RCS Group’s interest therein.

When The RCS Group reduces its level of significant

influence or loses significant influence, The RCS

Group proportionately reclassifies the related items

which were previously accumulated in equity through

other comprehensive income to profit or loss as

a reclassification adjustment. In such cases, if an

investment remains, that investment is measured to fair

value, with the fair value adjustment being recognised in

profit or loss as part of the gain or loss on disposal.

Jointly controlled operations

A jointly controlled operation is a joint arrangement

carried on by each operator using its own assets in

pursuit of the joint operations. The consolidated financial

statements include the assets that The RCS Group

controls and the liabilities that it incurs in the course

of pursuing the joint operation, and the expenses that

The RCS Group incurs and its share of the income that it

earns from the joint operation.

Jointly controlled ventures

A joint venture is a joint arrangement whereby the joint

venturers that have joint control of the arrangement,

have rights to the net assets of the arrangement. A joint

venturer shall recognise its interest in a joint venture as

an investment and shall account for the investment by

applying the equity method.

ACCOuNTING POLICIES (continued)

for the year ended 31 December 2016

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 21

1.4 usE of EstimatEs aNd judgEmENts

The preparation of consolidated financial statements

in conformity with IFRS, requires management to make

judgements, estimates and assumptions that may affect

the application of policies and reported amounts of assets

and liabilities, income and expenses. The estimates

and associated assumptions are based on historical

experience and various other factors that are believed

to be reasonable under the circumstances, the results of

which form the basis of making the judgements about

carrying values of assets and liabilities that are not readily

apparent from other sources. Actual results may differ

from these estimates.

The estimates and underlying assumptions are reviewed

on an ongoing basis. Revisions to accounting estimates

are recognised in the period in which the estimate is

revised if the revision only affects that period, or in the

period of the revision and future periods if the revision

affects both current and future periods.

estimates and judgements made in applying The RCS

Group’s accounting policies, that potentially have a

significant effect on the amounts recognised in the

consolidated financial statements relate to the following:

- Card and loan receivables are disclosed net of any

accumulated impairment losses and future recoveries.

The calculation of the impairment amount is performed

using the internationally-recognised Markov model.

The Markov model uses delinquency roll rates on

customer balances to determine the inherent bad debt

in a receivables book. In addition, in terms of adopting

a conservative approach, management considers

evidence not yet evident in the mathematical models,

such as the macroeconomic environment and portfolio

maturity, to inform their judgement of the required

levels of impairment and whether to add a further

layer over and above the statistical model output. The

directors believe that the card and loan receivables

balances are being measured fairly. Refer to notes 5

and 30 for further explanation.

- The RCS Group reviews goodwill for impairment at

least annually or when events or changes in economic

circumstances indicate that impairment may have

taken place. Impairment reviews are performed by

projecting future cash flows, based upon budgets and

plans and making appropriate assumptions about

rates of growth and discounting these using a rate that

takes into account prevailing market interest rates and

the risks inherent in the business. If the present value

of the projected cash flows is less than the carrying

value of the underlying net assets and goodwill, an

impairment charge is recognised in the statement of

comprehensive income. This calculation requires the

exercise of significant judgement by management. If

the estimates prove to be incorrect or performance

does not meet expectations, which affects the amount

and timing of future cash flows, goodwill may become

impaired in future periods. Goodwill is disclosed in

note 10.

1.5 sEgmENtal rEPortiNg

An operating segment is a component of The RCS Group

that engages in business activities from which it may

earn revenues and incur expenses, including revenues

and expenses that relate to transactions with any of The

RCS Group’s other components. operating segments’

operating results are reviewed regularly by the board,

identified as the chief operating decision-maker, to make

decisions about resources to be allocated to the segment

and assess its performance and for which internal

financial information is available.

Segment results that are reported to the board include

items directly attributable to a segment as well as those

that can be allocated on a reasonable basis.

ACCOuNTING POLICIES (continued)

for the year ended 31 December 2016

22 | THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016

Segment capital expenditure is the total cost

incurred during the period to acquire equipment and

intangible assets.

Amounts reported in The RCS Group’s segmental

analysis are measured in accordance with IFRS.

Inter-segment pricing is determined on an arm’s length

basis.

1.6 fiNaNcial iNstrumENts

A financial instrument is recognised when The RCS

Group becomes a party to the contractual provisions of

the instrument.

Financial assets are derecognised if The RCS Group’s

contractual rights to the cash flows from the financial

assets expire or if The RCS Group transfers the

financial asset to another party without retaining

control or substantially all risks and rewards of the

asset. Regular way purchases and sales of financial

assets are accounted for at trade date, being the date

that The RCS Group commits itself to purchase or

sell the asset. Financial liabilities are derecognised if

The RCS Group’s obligations specified in the contract

expire or are discharged or cancelled.

Non-derivative financial instruments

Non-derivative financial instruments recognised on the

statement of financial position include cash and cash

equivalents, card, loan and other receivables, funding

and trade and other payables.

Initial measurement

Financial instruments are initially recognised at fair

value. For those instruments not measured at fair value

through profit or loss, directly attributable transaction

costs are included on initial measurement.

Subsequent to initial recognition, these instruments

are measured as set out below:

Cash and cash equivalents

Cash and cash equivalents comprises cash on hand

and amounts held on deposit at financial institutions.

Cash is measured at amortised cost less impairment

losses by using the effective interest method.

Card and loan receivables

Card and loan receivables are classified as loans and

other receivables and are measured at amortised cost

using the effective interest method, less accumulated

impairment losses. An impairment allowance is made

for card and loan receivables which are estimated to

be impaired at the reporting date. This impairment

allowance is estimated as discussed in note 1.4.

other receivables

other receivables are carried at amortised cost using

the effective interest rate method less accumulated

impairment losses.

Financial liabilities measured at amortised cost

Non-derivative financial liabilities including interest-

bearing funding and trade and other payables are

recognised at amortised cost comprising original debt

less principal repayments and amortisation.

Derivative financial instruments

The RCS Group uses derivative financial instruments

to hedge its exposure to interest rate risks arising from

operational, financing and investment activities. In

accordance with its treasury policy, The RCS Group

does not hold or issue derivative financial instruments

for trading purposes.

Derivative financial instruments are subsequently

measured at fair value, with the gain or loss on

ACCOuNTING POLICIES (continued)

for the year ended 31 December 2016

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 23

remeasurement being recognised immediately in the

statement of comprehensive income. However, where

derivatives qualify for hedge accounting, recognition

of any gain or loss depends on the nature of the hedge

(refer to hedge accounting policy note 1.6).

The fair value of interest rate swaps is the estimated

amount that The RCS Group would receive or pay

to terminate the swap at the reporting date, taking

into account current interest rates and the current

creditworthiness of the swap counterparties.

Cashflow hedge accounting

Changes in the fair value of a derivative hedging

instrument designated as a fair value hedge are

recognised in the statement of comprehensive income.

The hedged item is adjusted to reflect changes in its

fair value in respect of the risk being hedged; the gain

or loss attributable to the hedged risk is recognised

in the statement of comprehensive income with an

adjustment to the carrying amount of the hedged item.

To the extent that they are effective, gains and losses

from remeasuring the hedging instruments relating to

a cash flow hedge to fair value are initially recognised

directly in other comprehensive income and presented

in the hedging reserve in equity. If the hedged firm

commitment or forecast transaction results in the

recognition of a non-financial asset or liability, the

cumulative amount recognised in other comprehensive

income, up to the transaction date, is adjusted against

the initial measurement of the asset or liability.

For other cash flow hedges, the cumulative amount

recognised in other comprehensive income is included

in the statement of comprehensive income in the

period when the hedged item affects the statement of

comprehensive income. The ineffective portion of any

gain or loss is recognised immediately in the statement

of comprehensive income.

Where the hedging instrument or hedge relationship

is terminated but the hedged transaction is still

expected to occur, the cumulative unrealised gain or

loss at that point remains in equity and is recognised

in accordance with the above policy when the

transaction occurs. If the hedged transaction is no

longer expected to occur, the cumulative unrealised

gain or loss is recognised in the statement of

comprehensive income immediately.

Offset

Financial assets and financial liabilities are offset and

the net amount reported in the statement of financial

position when The RCS Group has a legally enforceable

right to set off the recognised amounts, and intends

either to settle on a net basis, or to realise the asset

and settle the liability simultaneously.

1.7 ProPErty aNd EquiPmENt

Recognition and measurement

Items of property and equipment are measured at

cost less accumulated depreciation and accumulated

impairment losses.

Cost includes expenditure that is directly attributable

to the acquisition of the asset. Purchased software that

is integral to the functionality of the related equipment

is capitalised as part of that equipment.

When parts of an item of property and equipment have

different useful lives, they are accounted for as separate

items (major components) of property and equipment.

Gains and losses on disposal of an item of property

and equipment are determined by comparing the

proceeds from disposal with the carrying amount

of property and equipment and are recognised

net within “operating costs” in the statement of

comprehensive income.

ACCOuNTING POLICIES (continued)

for the year ended 31 December 2016

24 | THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016

Subsequent costs

The cost of replacing part of an item of property and

equipment is recognised in the carrying amount of the

item if it is probable that the future economic benefits

embodied within the part will flow to The RCS Group

and its cost can be measured reliably. The carrying

amount of the replaced part is derecognised. The costs

of the day-to-day servicing of property and equipment

are recognised in the statement of comprehensive

income as incurred.

Depreciation

Depreciation is recognised in the statement of

comprehensive income on a straight-line basis over

the estimated useful lives of each part of an item of

property and equipment.

The estimated depreciation rates for the current and

comparative periods are as follows:

- Computer hardware 33%

- Furniture and fittings 16% - 20%

- leasehold property 10%

- Motor vehicles 20%

Depreciation methods, useful lives and residual values

are reviewed at each reporting date.

Depreciation of an item of property and equipment

commences when the item is available for use.

1.8 rEiNsuraNcE coNtract issuEd iN cEll

caPtivE arraNgEmENt

In-substance reinsurance contracts issued are those

contracts that transfer significant insurance risk from

the insurer to the respective company in a cell captive

arrangement in a cell captive arrangement.

Insurance premiums

Insurance premiums received or receivable from

the insurer are recognised in the statement of

comprehensive income when due.

Claims

Claims incurred and reported are recognised in the

statement of comprehensive income when the loss

events occur. Claims incurred but not yet reported

are estimated for compensation payable to the

insured and are recognised in the statement of

comprehensive income.

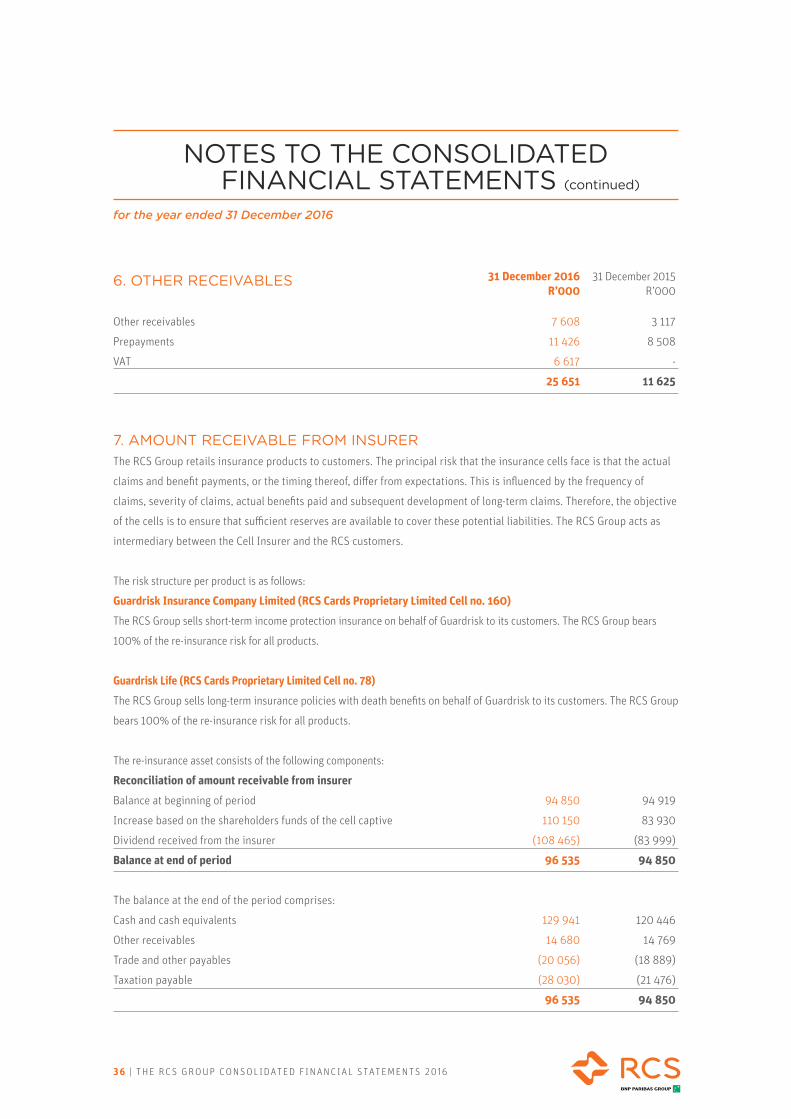

Amount receivable from insurer

The amount receivable from the insurer is initially

recognised at the amount paid for the ordinary shares

issued by the insurer.

The amount receivable from the insurer represents

the right to the residual interest in the cell captive

and is after initial recognition measured based on the

net asset position of the cell captive at the end of the

reporting period. This amount is reduced by dividends

declared by the insurer.

The amount receivable from the insurer is assessed

for impairment at each reporting period. If there is

objective evidence that the amount receivable is

impaired, the carrying amount of the reinsurance asset

is reduced to its recoverable amount. The impairment

loss is recognised in the statement of comprehensive

income.

1.9 goodwill

Goodwill is measured at cost less any accumulated

impairment losses. Goodwill is allocated to cash-

generating units and is not amortised, but tested

annually for impairment and when there is an

indication of impairment.

ACCOuNTING POLICIES (continued)

for the year ended 31 December 2016

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 25

1.10 iNtaNgiBlE assEts

Intangible assets that are acquired by The RCS Group,

which have finite useful lives, are measured at cost

less accumulated amortisation and accumulated

impairment losses.

Subsequent expenditure is capitalised only when it

increases the future economic benefits embodied

in the specific asset to which it relates. All other

expenditure, including expenditure on internally

generated goodwill and brands, is recognised in the

statement of comprehensive income as incurred.

expenditure on research activities is recognised as

an expense in the period in which it is incurred. An

internally-generated intangible asset arising from

development (or from the development phase of an

internal project) is recognised if, and only if, all of the

following have been demonstrated:

- the intention to complete the intangible asset and use

or sell it;

- the ability to use or sell the intangible asset;

- how the intangible asset will generate probable

future economic benefits;

- the availability of adequate technical, financial and

other resources to complete the development and to

use or sell the intangible asset;

- the ability to measure reliably the expenditure

attributable to the intangible asset during its

development; and

- the technical feasibility of completing the

intangible asset.

The amount initially recognised for internally-

generated intangible assets is the sum of the

expenditure incurred from the date when the

intangible asset first meets the recognition criteria

listed above. Where no internally-generated intangible

asset can be recognised, development expenditure is

recognised in the statement of comprehensive income in

the period in which it is incurred. Subsequent to initial

recognition, internally-generated intangible assets are

reported at cost less accumulated amortisation and

accumulated impairment losses, on the same basis as

intangible assets acquired separately.

Client lists

Client lists acquired by The RCS Group are stated at

historical cost less accumulated amortisation and

impairment losses. Amortisation is recognised in the

statement of comprehensive income on a straight-line

basis over the estimated useful lives of the client lists.

The annual rate for the amortisation is 20%.

Computer software

Computer software acquired by The RCS Group is stated

at historical cost less accumulated amortisation and

impairment losses. Amortisation is recognised in the

statement of comprehensive income on a straight-line

basis over the estimated useful lives of intangible

assets. The annual rate for the amortisation is 33%.

The above amortisation rates are consistent with the

comparative period. Amortisation methods, useful

lives and residual values are reassessed at each

reporting date.

1.11 imPairmENt

Non-derivative financial assets

A financial asset not classified as at fair value through

profit or loss is assessed at each reporting date to

determine whether there is any objective evidence

that it is impaired. A financial asset is considered

to be impaired if objective evidence indicates that

one or more events have had a negative effect on the

estimated future cash flows of that asset, that can be

reliably measured.

ACCOuNTING POLICIES (continued)

for the year ended 31 December 2016

26 | THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016

An impairment loss in respect of a financial asset

measured at amortised cost is calculated as the difference

between its carrying amount and the present value of the

estimated future cash flows discounted at the original

effective interest rate.

Individually significant financial assets are tested for

impairment on an individual basis. Those found not to be

specifically impaired are then collectively assessed for any

impairment that has been incurred but not yet identified.

Assets that are not individually significant are collectively

assessed for impairment by grouping together assets with

similar credit risk characteristics.

All impairment losses are recognised in the statement of

comprehensive income.

An impairment loss is reversed if the reversal can be

related objectively to an event occurring after the

impairment loss was recognised. For financial assets

measured at amortised cost the reversal is recognised in

the statement of comprehensive income.

Non-financial assets

The carrying values of The RCS Group’s non-financial

assets, other than deferred tax assets, are reviewed at

each reporting date to determine whether there is any

indication of impairment. If any such indication exists then

the asset’s recoverable amount is estimated.

For goodwill and intangible assets that have indefinite

useful lives or that are not yet available for use, the

recoverable amount is estimated at each reporting date.

An impairment loss is recognised if the carrying amount of

an asset or its cash-generating unit exceeds its recoverable

amount. A cash-generating unit is the smallest identifiable

asset group that generates cash flows that are largely

independent from other assets and groups. Impairment

losses are recognised in the statement of comprehensive

income. Impairment losses recognised in respect of cash-

generating units are allocated first to goodwill and then to

reduce the carrying amount of the other assets in the unit

(group of units) on a pro rata basis. The recoverable amount

of an asset or cash-generating unit is the greater of its value

in use and its fair value less costs to sell. In assessing value

in use, the estimated future cash flows are discounted to

their present value using a pre-tax discount rate that reflects

current market assessments of the time value of money and

the risks specific to the asset.

An impairment loss in respect of goodwill is not reversed.

In respect of other assets, impairment losses recognised in

prior periods are assessed at each reporting date for any

indications that the loss has decreased or no longer exists.

An impairment loss is reversed if there has been a change

in the estimates used to determine the recoverable amount.

An impairment loss is reversed only to the extent that the

asset’s carrying amount does not exceed the carrying amount

that would have been determined, net of depreciation or

amortisation, if no impairment loss had been recognised.

1.12 statEd caPital aNd rEsErvEs

Stated capital

ordinary shares are classified as equity. Incremental

costs directly attributable to the issue of ordinary shares

are recognised as a deduction from equity, net of any

taxation effects.

Foreign currency translation reserve

Gains and losses arising on translation of the assets,

liabilities, income and expenses of foreign operations

are recognised directly in equity as a foreign currency

translation reserve.

Cash flow hedge reserve

A non-distributable reserve arises as a result of the

application of hedge accounting gains or losses on

interest rate swaps.

ACCOuNTING POLICIES (continued)

for the year ended 31 December 2016

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 27

1.13 dividENds

Dividends and the related withholdings tax are

accounted for in the period when the dividend is

declared. Dividends declared on equity instruments

after the reporting date, and the related withholding

taxation thereon, are accordingly not recognised as

liabilities at the reporting date.

1.14 iNtErEst EarNEd

Revenue comprises interest income. Interest is

recognised on a time-proportion basis taking account

of the principal outstanding and the effective interest

rate over the period to maturity, when it is probable

that such income will accrue to The RCS Group.

1.15 iNtErEst ExPENsE

Interest expense comprises interest which

has been incurred on borrowings. All borrowing

costs are recognised in the statement of

comprehensive income.

1.16 othEr iNcomE

Club income

Club income is recognised in the statement of

comprehensive income when due.

Collection income

Collection income is recognised in the statement of

comprehensive income when due.

Net insurance premiums

Insurance premiums are recognised, net of claims, in

the statement of comprehensive income when due.

Merchant commission income

Merchant commission income is recognised when

the related transaction on which the commission is

earned has been concluded.

Service and initiation fee income

Service fee income is recognised in the statement

of comprehensive income when due. Initiation fee

income is deferred in the statement of comprehensive

income on a straight-line basis.

1.17 oPEratiNg lEasE

leases where the lessor retains the risks and

rewards of ownership of the underlying asset are

classified as operating leases. Payments made under

operating leases are recognised in the statement of

comprehensive income on a straight-line basis over the

term of the lease.

1.18 taxatioN

Income taxation expense comprises current and

deferred taxation.

Income taxation expense is recognised in the

statement of comprehensive income except to the

extent that it relates to a transaction that is recognised

directly in other comprehensive income or in equity,

in which case it is recognised in other comprehensive

income or equity as appropriate.

Current taxation is the expected taxation payable/

receivable, calculated on the basis of taxable income

for the period, using the taxation rates enacted or

substantively enacted at the reporting date, and

any adjustment of taxation payable/receivable for

previous periods.

Deferred taxation is recognised in respect of temporary

differences between the taxation base of an asset or

liability and its carrying amount. Deferred taxation is

not recognised for the following temporary differences:

the initial recognition of goodwill; the initial

recognition of assets and liabilities in a transaction

that is not a business combination and that affects

ACCOuNTING POLICIES (continued)

for the year ended 31 December 2016

28 | THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016

neither accounting nor taxable profit; and temporary

differences relating to investments in subsidiaries to

the extent that they probably will not reverse in the

foreseeable future. Deferred taxation is measured at

the taxation rates that are expected to be applied to

temporary differences when they reverse, based on the

laws that have been enacted or substantively enacted by

the reporting date.

Deferred taxation assets are recognised for all

deductible temporary differences and assessed losses

to the extent that it is probable that taxable profit will

be available against which such deductible temporary

differences and assessed losses can be utilised. Deferred

taxation assets are reviewed at each reporting date and

are reduced to the extent that it is no longer probable

that the related taxation benefit will be realised.

Deferred taxation assets and liabilities are off-set if

there is a legally enforceable right to off-set current

taxation liabilities and assets, and they relate to income

taxes levied by the same taxation authority on the same

taxable entity, or on different tax entities, but they

intend to settle current taxation liabilities and assets on

a net basis, or their taxation assets and liabilities will be

realised simultaneously.

1.19 EmPloyEE BENEfits

Short-term employee benefits

The cost of all short-term employee benefits are

recognised in the statement of comprehensive income

during the period in which the employee renders the

related service.

The accruals for employee entitlements to wages,

salaries, annual and sick leave represent the amount

which The RCS Group has a present obligation to pay as

a result of employees’ services provided to the reporting

date. The short-term benefits have been calculated

at undiscounted amounts based on current wage and

salary rates.

Defined contribution plans

The holding company and its subsidiaries contribute to

the following defined contribution plans:

Post-employment benefits

A defined contribution plan is a post-employment

benefit plan under which an entity pays fixed

contributions into a separate entity and will have no

legal or constructive obligation to pay further amounts.

obligations for contributions to defined contribution

pension, provident and retirement funds are recognised

as an employee benefit expense in the statement

of comprehensive income as the related service is

provided. Prepaid contributions are recognised as an

asset to the extent that a cash refund or a reduction in

future payments is available.

Medical aid schemes

The RCS Group contributes to medical aid schemes

for the benefit of permanent employees and their

dependants. The contributions to the schemes

are recognised in the consolidated statement of

comprehensive income as the related service is

provided.

1.20 forEigN currENciEs

Foreign currency transactions

Transactions in currencies other than the entity’s

functional currency are translated at the rates of

exchange ruling on the transaction date.

Monetary assets and liabilities denominated in such

currencies are translated at the rates ruling at the

reporting date.

ACCOuNTING POLICIES (continued)

for the year ended 31 December 2016

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 29

Non-monetary assets and liabilities denominated in

such currencies are translated using the exchange rate

at the date of the transaction.

Foreign currency gains and losses arising on

translation are recognised in the statement of

comprehensive income.

Foreign operations

As at the reporting date, the assets and liabilities of

foreign operations, including goodwill and fair value

adjustments arising on acquisition, are translated into

the presentation currency of The RCS Group at the

rate of exchange ruling at the reporting date and the

income and expenses are translated at the exchange

rates at the dates of the transactions or the average

rates if it approximates the actual rates.

Gains and losses arising on translation of the assets,

liabilities, income and expenses of foreign operations

are recognised in other comprehensive income, and

presented in the foreign currency translation reserve

in equity.

ACCOuNTING POLICIES (continued)

for the year ended 31 December 2016

RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 00

Delivering uncomplicated digital solutions

for our customers

THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016 | 31

2. NEw STANDARDS AND INTERPRETATIONS

2.1 adoPtioN of NEw aNd rEvisEd ifrs

In the current year The RCS Group has adopted all of the revised standards and Interpretations issued by the

International Accounting Standards Board (IASB) and the IFRS interpretations committee (IFRIC) of the IASB that

are relevant to its operations and effective for accounting periods before or on 1 January 2016. The adoption of these

standards and interpretations has not resulted in any adjustments to the amounts previously reported in the Annual

Financial Statements (AFS) for the year ended 31 December 2015.

2.2 staNdards aNd iNtErPrEtatioNs Not yEt EffEctivE

There are standards and interpretations in issue that are not yet effective. These include the following standards and

interpretations that are applicable to the company and may have an impact on future financial statements:

IFRS 9 Financial Instruments

IFRS 9 (2009) introduces new requirements for the classification and measurement of financial assets. under IFRS

9 (2009), financial assets are classified and measured based on the business model in which they are held and the

characteristics of their contractual cash flows. IFRS 9 (2010) introduces additions relating to financial liabilities. In

addition, the IFRS 9 impairment model has been changed from an “incurred loss” model in IAS 39 to an “expected

loss” model. The final version of IFRS 9 was issued in July 2014 and applies to an annual reporting period beginning

on or after 1 January 2018 with retrospective application.

The RCS Group, with the assistance of the ultimate shareholder and in consultation with external professional expert

input, is in the final stages of an impact analysis for The RCS Group and is on track for implementation of IFRS 9

requirements for the 2018 financial year.

IFRS 15 Revenue from Contracts with Customers

IFRS 15 specifies how and when an entity will recognise revenue as well as requiring such entities to provide users of

financial statements with more informative, relevant disclosures. The standard contains a single model that applies

to contracts with customers and two approaches to recognising revenue: at a point in time or over time. The model

features a contract-based five-step analysis of transactions to determine whether, how much and when revenue is

recognised. The standard is effective for annual periods beginning on or after 1 January 2018.

The impact on the financial statements for The RCS Group is not considered to be material.

IFRS 16 leases

IFRS 16 sets out the principles for the recognition, measurement, presentation and disclosure of leases for both

parties to a contract, ie the customer (‘lessee’) and the supplier (‘lessor’). IFRS 16 replaces the previous leases

Standard, IAS 17 leases, and related interpretations. IFRS 16 has one model for lessees which will result in almost all

leases being included on the Statement of Financial position.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

for the year ended 31 December 2016

32 | THe RCS GRouP CoNSolIDATeD FINANCIAl STATeMeNTS 2016

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS (continued)

for the year ended 31 December 2016

The standard is effective for annual periods beginning on or after 1 January 2019, with early adoption permitted only if

the entity also adopts IFRS 15. The RCS Group is assessing the potential impact on the financial statements resulting

from the application of IFRS 16.

3. OPERATING SEGMENTS The RCS Group has two reportable segments, as described below, which are The RCS Group’s strategic business units.

The strategic business units offer different products and services, and are managed separately because they require

different technology and marketing strategies. For each strategic business unit, The RCS Group’s board reviews

internal management reports on a monthly basis. The following summary describes the operations in each of The RCS

Group’s reportable segments:

- Cards segment - a general utility and private label card product offered to consumers, delivered via participating

merchant outlets in South Africa, Namibia and Botswana and their related insurance products.

- loans segment - short and medium-term loans offered to consumers and related insurance products provided to

individuals.

- All other segments includes BNP Paribas Personal Finance South Africa limited, RCS Home loans Proprietary

limited, RCS Collections Proprietary limited and once-off corporate costs.

• BNP Paribas Personal Finance South Africa Limited acts as the external funding vehicle for The RCS Group.

Commercial paper and bonds are issued via this entity (see note 17).

• RCS Home Loans Proprietary Limited operations include the servicing of current home loans.

• RCS Collections Proprietary Limited is a registered debt collector.

• None of these segments meet any of the quantitative thresholds for determining reportable segments in the current

or previous financial periods.

The RCS Group’s external customers and assets are predominantly situated in South Africa, and no single customer

comprises 10% or more of revenue for The RCS Group.