the ownership of japanese corporations in the 20 th century julian franks london business school,...

TRANSCRIPT

The Ownership of Japanese Corporations in the 20th Century

Julian FranksLondon Business School, CEPR and ECGI

Colin MayerSaïd Business School, Oxford University, CEPR and ECGI

Hideaki MiyajimaWaseda University and RIETI

Introduction• Law & finance view that stock markets thrive with a strong system

of Anglo Saxon legal protection.• But pre-WW2, low levels of investor protection in UK & yet a

thriving stock market. Franks, Mayer & Rossi (2009) attribute it to trust generating mechanisms such as local stock markets & local investors.

• For example, pre-1948 an equal price rule in mergers prevailed, despite no takeover rules.

• Japan provides a very different ownership setting normally characterized as an insider system with large holdings by banks and corporate cross holdings.

2

Japan: A Remarkable Laboratory

• For half of the 20th century Japan was an outsider system• That half coincided with weak investor protection.• In the middle, there was a structural change (early postwar reforms)

which destroyed institutions and introduced strong investor protection.

• Newly designed outsider system was short-lived, replaced by insider system.

• Japan is unusual in that it switched from one ownership system to another.

• A remarkable laboratory for examining the evolution of the ownership of corporations.

3

The Purpose of the Paper

• Long run evolution of ownership in 20th century in Japan• Collects individual company ownership data• Examines the dispersion of ownership, composition of

shareholders, equity financing• Influence of law & institutions• Contrast first & second half of century

Page 4

Main Results• Investor protection cannot explain results• Japan had dispersed ownership throughout the 20th century but

insider ownership dominated the second half of the century • Pre war, trust mechanisms that encouraged outsider ownership. 1) Business coordinators in the 1900s 2) Zaibatsu HC (family business groups) in the 1930s• Post war: the dissolution of family groups & the lack of institutional

support to sustain outside ownership.• The failure to establish institutions with reputational capital• Institutional trust explains the evolution to insider ownership

5

Our Data Sets

6

Pre-WW2: 2 samples1900-1937 based on largest 100 Cos in 1918 (N=50) & 1930 (N=29), alive in 1940. 1918 sample had to be incorporated pre-1907 (mainly textiles, food, light engineering)1930 sample incorporated pre 1921 (more heavy engineering, shipbuilding, chemicals)No Zaibatsu in 1907, 21 out of 29 zaibatsu affiliated in 1930 sample

Post WW2 sample: Largest 100 firms by assets in 1937 or 1955 (total

126).

Concentration of Ownership: 1900-1937

7

Comparison of Japan with UK: 1900-2000

A comparison of C3 & C5 in UK and Japan

8

Composition of Top 10 Shareholders: Insiders vs. Outsiders

• 1907 Sample: outsider ownership is dominant in the 1900-1937. Insiders are less than 30% and no. of shareholders increased. Business coordinators had significant stake. Major shareholders were individual.

• 1921 Sample: Insider ownership high, small decline during the 1930s, replaced by individuals and insurance firms

9

1900 1907 1914 1921 1928 1933 1937

1907 Sample

% held by top 10 stakes 48.9% 46.5% 44.7% 43.9% 39.5% 40.3% 39.1%

insider ownership 26.9% 27.9% 23.5% 30.3% 28.1% 27.3% 27.6%

No. of shareholders 302 675 1,060 3,893 5,769 5,932 6,682

1921 sample% held by top 10 stakes 65.8% 63.3% 63.6% 59.9%Insider ownership - - - 58.8% 56.4% 54.5% 52.5%Founders/board members - - - 21.7% 16.7% 15.2% 10.7%Holding Company - - - 22.4% 22.9% 26.6% 18.8%Ave. no of shareholders - - - 2,399 2,735 3,973 4,881

Insider vs. Outsider in Postwar Period• Outsider: sole interests are in the

financial returns eg. mutual funds, individuals, business coordinators.

• Insider: derive private benefits eg. managerial ownership, HC, corporations, bank.

• Prewar: outsider dominated (insider ownership less than 30%)

• Postwar reform: completely outsider dominated.

• Transformed from outsider to insider in the 1950-60s

• After banking crisis: outsider dominated again

10

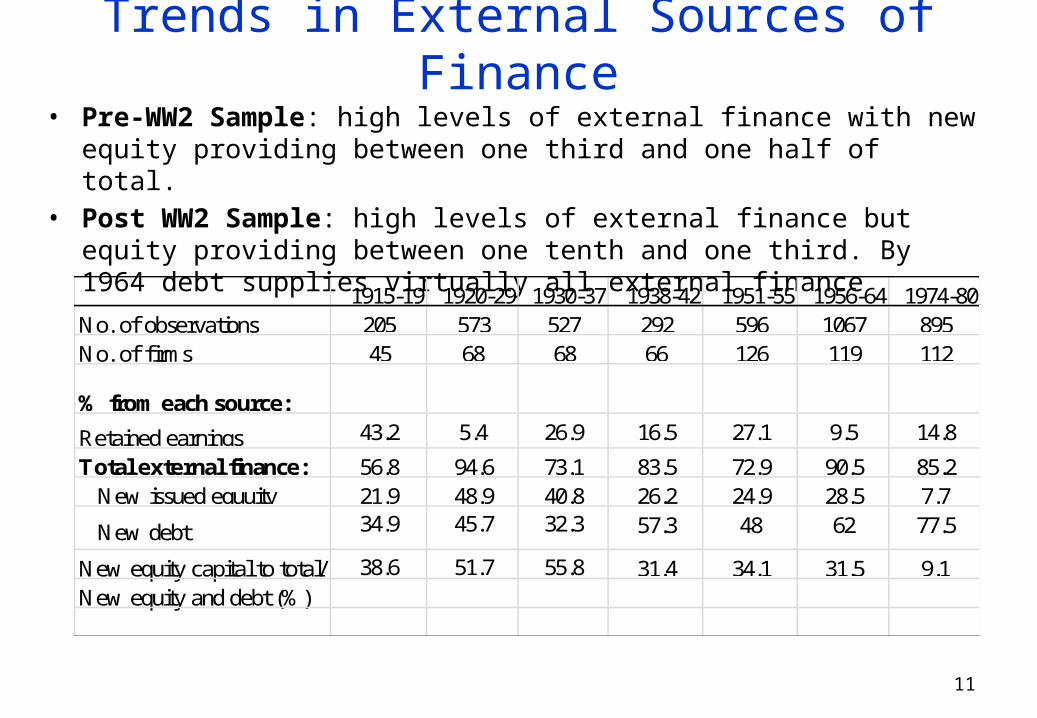

Trends in External Sources of Finance• Pre-WW2 Sample: high levels of external finance with new equity providing

between one third and one half of total.• Post WW2 Sample: high levels of external finance but equity providing between

one tenth and one third. By 1964 debt supplies virtually all external finance

11

1915-19 1920-29 1930-37 1938-42 1951-55 1956-64 1974-80No. of observations 205 573 527 292 596 1067 895No. of firms 45 68 68 66 126 119 112

% from each source:

Retained earnings 43.2 5.4 26.9 16.5 27.1 9.5 14.8

Total external finance: 56.8 94.6 73.1 83.5 72.9 90.5 85.2 New issued equuity 21.9 48.9 40.8 26.2 24.9 28.5 7.7

New debt 34.9 45.7 32.3 57.3 48 62 77.5

New equity capital to total/ 38.6 51.7 55.8 31.4 34.1 31.5 9.1New equity and debt (%)

Can Law Explain This?

Complete reversal

•Investor protection was weak in the first half of the 20th century and was ‘formally’ transformed by the US occupation into a strong regime in the second half of the century.•Post WW2: one share one vote, pre-emption rights, high disclosure (0.9) & Glass Steagall.•How could an insider system emerge in such an investor protection environment?

LLSV Score in Japan

12

Japan UK Germany

1900 1990

Year law/rules changed

1900 1990 1900 1990

Anti-director rights

1 4 1950,1974 1 5 1 1

Liabilities standard

0 0.667 1948 0 0.667 0 0

Disclosure 0 0.917 1948 0 0.833 0 0.417

Public enforcement

0 0.658 1948 0 0.750 <0.25 0.25

Creditor rights 3 1 1952 NA 4 NA 3

The Trust Mechanism in The Early 1900s: The Business Coordinator

• In Japan, ‘business co-ordinators’ (equivalent venture capitalists) played a critical role in IPOs: board membership and held significant share stakes. (Miwa and Ramseyer 2000)

• They were individuals with high reputations who sat on large number of boards & frequently took stakes in companies

• Function: 1) monitoring newly established firms in the face of a large number of

cases of fraud 2) providing general business advice and promoting business relations

with other firms • Estimation results: Lower concentration and high no. of shareholders

with business coordinator

13

Test of Business Coordinator and Dispersion of Ownership

2/3 of firms had (at least) 1 business coordinator

Test Sample = 121 firms, 21 firms 1900, 50 firms in 1907 and 1914

C5 & no. of shareholders = F (Cordummy, size, year incorporated, industry, yeardummy)

Cordummy is 1, if coordinator took a seat on board of directors, or/and was one of largest ten shareholders.

Result = significantly negative at 5% level. Lower concentration and high no. of shareholder with business coordinator

14

The Zaibatsu in the 1930’s

1930s is a bull market for equities & IPOs•IPOs & carve outs of subsidiaries of zaibatsu firms,•Given low minority shareholder protection, and ‘tunnelling’ of Business Group (Morck and Namaura 2005) , how is this possible ?

Zaibatsu played the same certification role as business coordinators: •Monitoring by holding company •Risk sharing among groups•Reputational capital

Estimation results: negative relation between zaibatsu and Δownership concentration and positive relation with new equity issues in our panel of firms 15

Test of the Zaibatsu in the 1930’s

• Two cross sectional regressions (N= 69)

• C5 (1933-37)= F(Size, D/A, zaibatsu dummy) Zaibatsu dummy (one = Mitsui, Mitsubishi, Sumitomo,

Furukawa, Nissan) is significantly negative. Larger negative changes in concentration of ownership with zaibatsu (13-15% lower than other firms.

• New equity/total assets 1933-37 =F(Size, D/A, invest, ROE, Zaibatsu). Zaibatsu dummy is significantly positive.

• Small investors regarded zaibatsu as providing a trust mechanism rather than a minority exploitation vehicle. Case study of Mitsubishi

16

Post-WW2 Period: Emergence of Insider Ownership

• Outside ownership was not stable, and gradually replaced by inside ownership of banks and corporate cross-holdings

• Three mechanisms: deleveraging, breakdown of trust mechanisms and external financing requirements

First mechanism: Deleveraging• High Leverage after financial reconstruction of postwar reforms

(Hoshi 1995), debt/asset over 60 %• Creditor unfriendly regulation (Corporate reorganization law in

1953) • Banks and other (creditor) firms of distressed [and bankrupt]

companies exchanged their debt for equity i.e. through swaps17

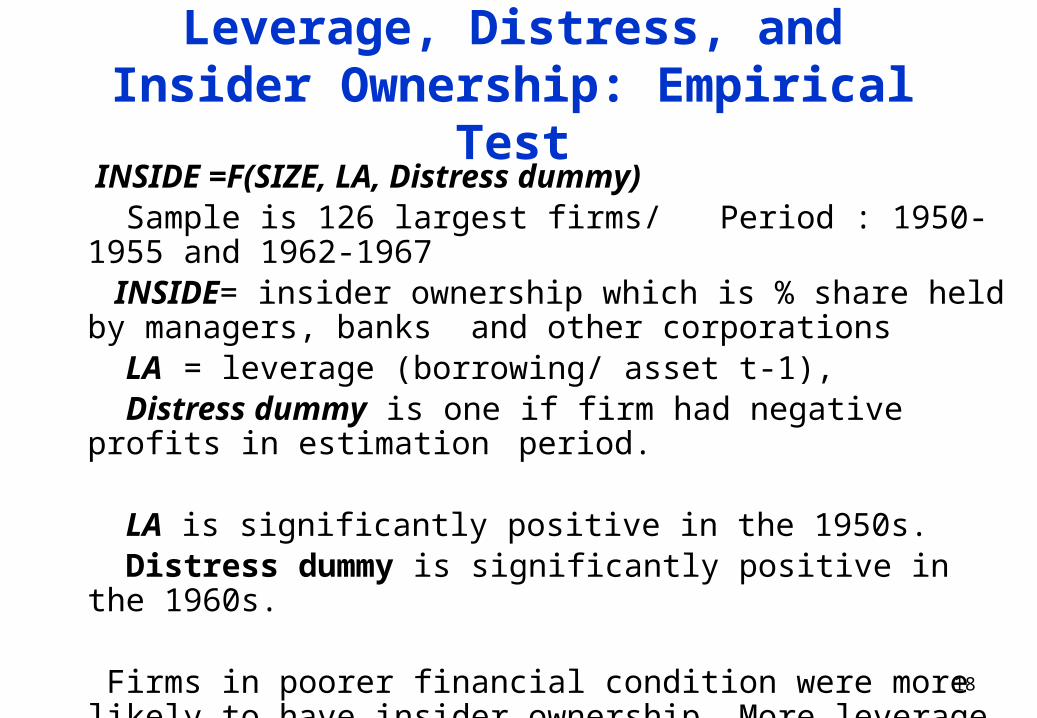

Leverage, Distress, and Insider Ownership: Empirical Test

INSIDE =F(SIZE, LA, Distress dummy) Sample is 126 largest firms/ Period : 1950-1955 and 1962-1967 INSIDE= insider ownership which is % share held by managers, banks

and other corporations LA = leverage (borrowing/ asset t-1), Distress dummy is one if firm had negative profits in estimation period.

LA is significantly positive in the 1950s. Distress dummy is significantly positive in the 1960s.

Firms in poorer financial condition were more likely to have insider ownership. More leverage is associated with higher insider ownership.

18

Deleveraging Through Debt for Equity Swaps

Evidence: Distressed companies reorganized through the Corporate Reorganization code: 19 cases of 30 bankrupt firms engaged in debt for equity swap from 1953-1965 (equity swapped was 75% of post-swap equity).

Case study 1: Workout. Oumi Silk had debt ratio of 71% in 1951. Faced financial distress after Korean War ended. Through debt for equity swap insider ownership rose from 28% in 1953 to 60% in 1955.

Case study 2: Bankruptcy. Sun Wave Corporation. 1964 plan of reorganization offered debt for equity swaps with 18 secured creditors of which 10 were banks. 9 refused and shares allocated to other 3 largest creditors including Iwai Industrial Co. Mitsui & Nissan Steel.

Page 19

A Second Mechanism: Lack of Trustworthy Institutions

• Conventional understanding: takeover defence• Equity boom in the late 1950s and early 1960s. (Toyota)• A lot of market manipulation and fraud by securities firms in the

1960s. Investment trusts grew to 12% of market in 1960, collapsed by 1970:

• Stock price collapse in 1962• 2 institutions set up to buy Japanese equities in 1964/65. Purchased

5% of all equities.• Purchased more of fast growing companies that made frequent

equity issues. Eg. Toyota stake 9.4%.• 1968: Sold stakes predominantly to insiders.

20

Third Mechanism: Private Placement

• In early 1970s, move from rights issues to new seasoned equity offerings

• Securities houses refocused their business away from investment management to underwriting.

• In collaboration with firms allocated new equity to friendly third parties at a substantial discount.

21

Example: Toyota

• PKO bought Japanese equities in 1964/65

• Collected data from annual accounts for our 126 firms for equity issuance

• Toyota made 10 equity issues 1961-1974 when insider ownership rose from about 35% to 80%

• Some of these issues made without pre-emption rights and at a discount (19.8% for Yokohama Rubber in 1973)

• • Frequency of equity issuance related to growth of insider holdings

Page 22

Toyota: Equity Issues and Insider Ownership

1953 1954 1955 1956 1957 1958 1959 1960 1961 1962 1963 1964 1965 1966 1967 1968 1969 1970 1971 1972 1973 19740

200000

400000

600000

800000

1000000

1200000

0%

10%

20%

30%

40%

50%

60%

70%

80%

Figure 4 Insider Shareholdings and Paid-in Capital:Toyota Motor

# Issued Shares Insider1

Insider ownership

PKO

New equity

23

Determinants of Growth of Insider Holdings for Post WW2: Regression

Results • Significant variables: no. of share issues (+), price support

institutions (+), keiretsu membership (-), firm size (-)

• Sub period 1 1964-1969 (whole sample): individual ownership at the beginning (++), price support institutions (++) but not no. of share issues

• Sub period 2 1969-1974 (whole sample): individual ownership at the beginning (++), # of seasoned issues (++), no. of years of negative ROA

• Implication: Growth in insider holdings correlated with equity issuance and sales by price support institutions

Page 24

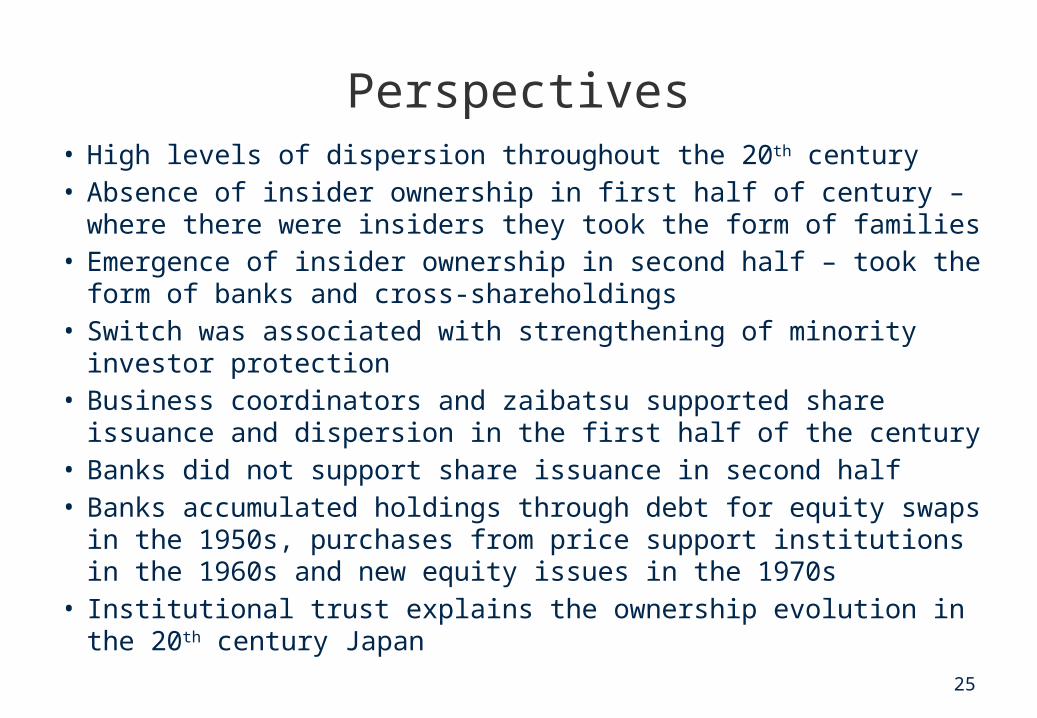

Perspectives• High levels of dispersion throughout the 20th century• Absence of insider ownership in first half of century – where there were

insiders they took the form of families• Emergence of insider ownership in second half – took the form of banks

and cross-shareholdings• Switch was associated with strengthening of minority investor protection• Business coordinators and zaibatsu supported share issuance and

dispersion in the first half of the century• Banks did not support share issuance in second half• Banks accumulated holdings through debt for equity swaps in the 1950s,

purchases from price support institutions in the 1960s and new equity issues in the 1970s

• Institutional trust explains the ownership evolution in the 20th century Japan

25