the oil market economics 331b spring 2010

DESCRIPTION

The Oil Market Economics 331b Spring 2010. 1. Basics of oil regulation 2. The integrated world oil market. Major Themes. What are major sources of concern on oil? The Bathtub model of the Oil Market Some simple econometrics of the law of one price Implications for Oil Policy. - PowerPoint PPT PresentationTRANSCRIPT

1

The Oil Market

Economics 331bSpring 2010

1. Basics of oil regulation2. The integrated world oil market

Major Themes

1. What are major sources of concern on oil?2. The Bathtub model of the Oil Market3. Some simple econometrics of the law of

one price4. Implications for Oil Policy

2

Reasons for Regulation of Oil-Using Capital1. Externalities

- Local pollution- Climate change- Congestion- Road accidents

2. Macroeconomic/trade- Impact of oil price on business cycle- Optimal tariff- Political/military

3. Imperfect decisionmaking - Discounting- Split incentives- Poor information

3

First-best policy options

4

Market failure First-best instrument

Externalities

Local pollution Locally determined regulations or feesClimate change Global carbon tax

Congestion Very complicated time and location specific congestion fees

Road accidents Very complicated engineering, training, DUI, etc.

Macroeconomic/trade/political

Impact of oil price on business cycle

Strategic oil reserve and variable oil taxes

Optimal tariff Tax on oil, probably global

Political/ military High tax on oil use plus complicated

Nuclear proliferation ?

Imperfect decisionmakingDiscounting Remove capital market imperfections

Split incentives "Meter" all uses (including Yale students!); peak-load pricing

Poor information Provide information stickers

This is not a bathtub.

5

Basic idea of bathtub model

Oil policy can only be considered in the context of world supply and demand. National policies are effective only to the extent that they contribute to total demands or total supplies.

Oil policy is a pecuniary “global public good.” Pecuniary v. technological externalities.

6

The “Law of One Price”

The Law of One Price (LOP) is an economic hypothesis stating that the common-currency price of a standardized commodity should be the same in different markets.

Conditions to hold are (1) profit maximization and (2) costless transportation, distribution, and resale

Get approximate LOP when have low transport and transactions costs. This is case for oil, but very few other goods.

7

Failure of Law of One Price: All Consumer Prices

8

3.5

3.0

2.5

2.0

1.5

1.0

0.580 81 82 83 84 85 86 87 88 89 90

CPI CanadaCPI FranceCPI ItalyCPI JapanCPI UKCPI GermanyCPI US

300

400

500

600

700

800

900

1,000

1992 1994 1996 1998 2000 2002 2004

Year

Region 1Region 2Region 3Region 4Region 5Region 6

Pri

ce o

f saw

logs

($ p

er 1

000

boar

d-fee

t)

A Not-So-Unified Market: Prices of #2 Douglas Fir Logs in Six Regions of the Pacific Northwest

Source: Log Lines, various dates.

9

200

150

100

5040

30

20

15

10

51998 2000 2002 2004 2006 2008 2010

Pri

ce ($

per

bar

rel)

Prices of Crude Oil in 31 Regional Markets Worldwide

Source: EIA primarily from Platts.10

Comparison of U.S. and European Benchmark Crude Prices

Source: EIA primarily from Platts.

0

20

40

60

80

100

120

140

160

0 40 80 120 160

Cushing West Texas spot ($ per barrel)

Euro

pe

Bre

nt s

pot

($ p

er b

arre

l)

11

The oil price equation (n=18,169)

Independent variableRegression coefficient Standard error t statistic Probability

Price of Brent crude (logarithm) 0.999 0.0008 1212.8 0.0000

Sulfur content (percent) -0.041 0.0006 -62.4 0.0000

API gravity 0.006 0.0001 56.3 0.0000

Constant -0.223 0.0051 -43.3 0.0000

Summary statistics

Adjusted R 2 0.988

Standard error of the regression 0.068

Mean of the dependent variable 3.426

Standard deviation of the dependent variable 0.626

12

Issues Raised by the Integrated World Oil Market

1. Limit oil imports to secure sources?

2. Strategic petroleum reserve should make sure that cover 90 days of US imports?

13

The “Oil Premium”

The “oil premium” is the excess of the marginal cost of oil use over its price. What are the sources of the premium?

1. Vulnerability to import disruption

2. Technological externalities (pollution, global warming)

3. Effect of higher use on oil price

4. Macroeconomic externalities of higher oil prices.

Major point is that these all depend upon global market, not on oil imports!

14

0

5

10

15

20

25

30

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

Pe

tro

leu

m a

s p

erc

en

t o

f to

tal i

mp

ort

s

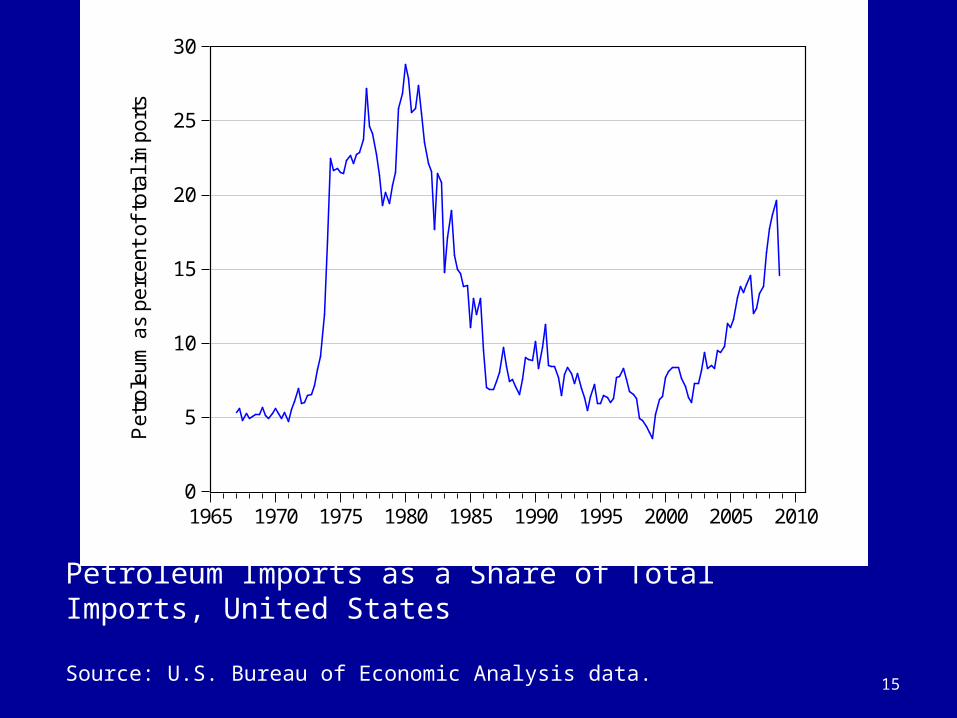

Petroleum Imports as a Share of Total Imports, United States

Source: U.S. Bureau of Economic Analysis data.15

National Security Concerns

1. Grabbing oil is primarily a wealth transfer and not a pricing issue.

2. The cost of protecting trade routes or going to war over oil is misguided and wasteful.

3. The value of sanctions and embargoes is nil.

4. The competition for access to resources is a misguided worry.

16

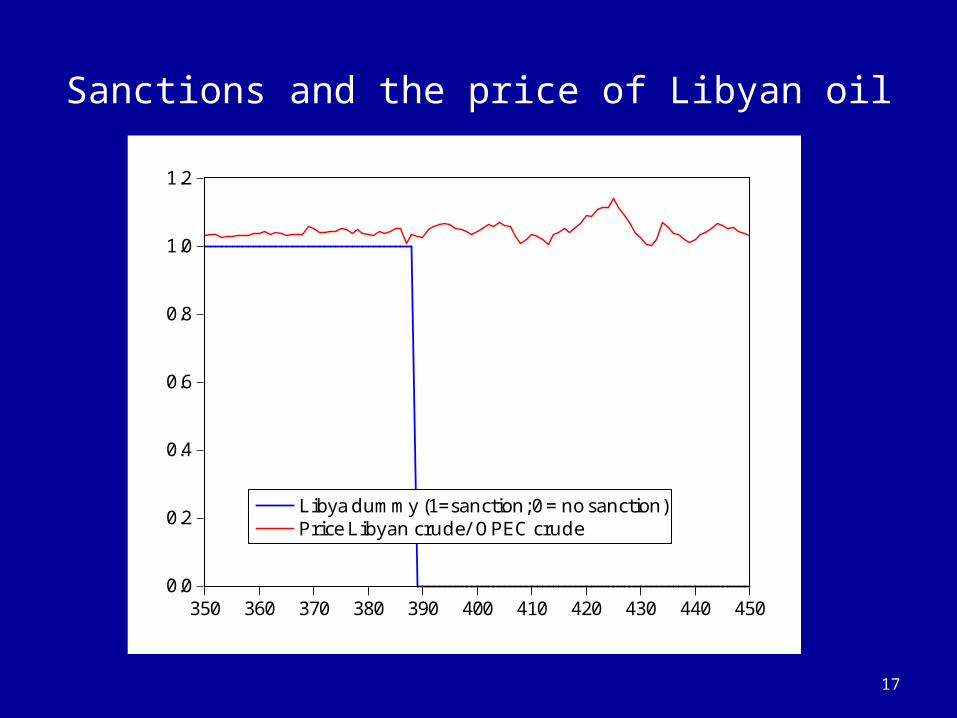

Sanctions and the price of Libyan oil

17

0.0

0.2

0.4

0.6

0.8

1.0

1.2

350 360 370 380 390 400 410 420 430 440 450

Libya dummy (1=sanction; 0 = no sanction)Price Libyan crude/ OPEC crude

EEconometrics of sanctions

18

Dependent Variable: LOG(price Libyan crude) Method: Least Squares Sample (adjusted): 1 645 Included observations: 645 after adjustments

Variable Coefficient Std. Error t-Statistic Prob. C -9.872807 1.645015 -6.001652 0.0000

Dummy for Libya sanctions 0.001856 0.006153 0.301621 0.7630

LOG(p Saudi crude) 0.968326 0.005930 163.2838 0.0000 YEAR 0.005010 0.000827 6.060142 0.0000

R-squared 0.995664 Mean dependent var 3.485963

Adjusted R-squared 0.995644 S.D. dependent var 0.608497 S.E. of regression 0.040162 Akaike info criterion -3.585632 Sum squared resid 1.033901 Schwarz criterion -3.557915

Appropriate Policies for Oil in the Integrated World Market

Objectives:1. Oil prices should be low, stable, and sustainable.2. Oil policy can only be rational if the price of carbon is

appropriately set.

Policies (assuming 2 is met):1. Encourage production everywhere (no domestic

subsidies)2. Discourage consumption everywhere (not just at

home), particularly with respect to subsidies.

19