the new pension standards gasb statements 67,68 & 71 · implementation •applied...

TRANSCRIPT

The New Pension Standards GASB Statements 67,68 & 71

Florida Court Clerks & Comptrollers

February 6, 2015

Mark White CPA, Audit Partner

Purvis Gray & Company LLP

1

2

Mark…..We Really Love Pension CPE!

Two New Statements Issued June 2012

Amends No. 25

Effective FYE 2014

No. 67 Plan

Reporting Amends No. 27

Effective FYE 2015

No. 68

Employer

Reporting

3

4

Final Statements

Issued 2012

Research Project

Agendas 2006/2008

Invitation To Comment

2009

Preliminary Views

2010

Exposure Draft 2011

5

The GASB’s Deliberative Process

Mostly Notes and

RSI Changes

Change In Pension

Liability

Aggregate Employer

Information

Annual Rate of Return on Plan Assets

6

Summary of No. 67 – Plan Reporting

Very Few FS Recognition Changes

From No. 25

Clarified That Drop Liability Not

Recorded During Buildup

Applies to Pension Plan FS Issued Separately or

as P/T/F of Local Government

The No. 68 Big Picture

7

Unfunded Defined Benefit Pension

Liability

Will Now Be Booked in Members

SONP of Economic Resources FS

Formerly Disclosed In FRS

Notes & RSI

No. 71 Contributions Made After MD

8

ReportingDate (RD)9/30/15

Employer FYE

MeasurementDate (MD)6/30/15

Contributions Made - Deferred Outflow

MD Must Be Within One Year of RD

Who is included?

No. 68 Applies Equally To;

Single Employer

(Local Muni Plans )

Multi-Employer

Agent Plans (FLC)

Multi-Employer

Cost Sharing Plans (FRS)

9

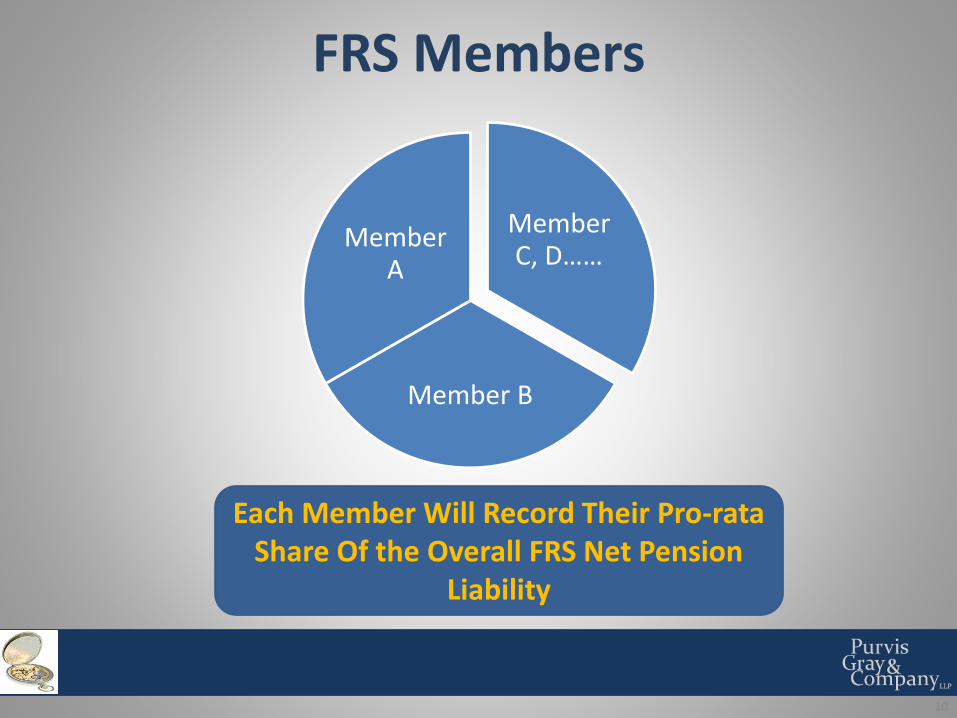

FRS Members

Member C, D……

Member B

Member A

10

Each Member Will Record Their Pro-rata Share Of the Overall FRS Net Pension

Liability

Implementation

• Applied Retroactively, Restate Opening Net Position and New Pension Liability at BOY (PPA Like)

• Applied Retroactively, Restate Opening Deferred Outflows Including Contributions made After MD

• This is Unlike No. 45 OPEB Implementation Which is Being Re-examined and May Soon Change

11

Up Until Now

Accounting Funding

12

Same

Up Until Now

• Employer accounting and actuarial funding/contributions have been ONE

• Old GASB Statement No. 27 (current)

– The employer’s obligation is to fund the plan

– Accounting expense = (ARC) --

an actuarial funding contribution

– Almost Cash Basis, Very Little BS

effect

13

Member

PlanEmployer Funding Obligation

From Now On

• Employer accounting and funding Have Been Separated!

• “We do accounting; actuaries do funding.” – Bob Attmore, GASB Chairman

14

Accounting (Apples)

Funding

(Oranges)

From Now On

• New GASB Statement No. 68 Looks At It This Way;

– The employer’s obligation is “ultimately to the members”

– The Accounting Expense = More Accrual Based (Earned) No Longer Based on Actuarial Funding Contribution

– The BS Liability = Old Unfunded Accrued

Actuarial Liability

15

Plan

Member

Employer

FRS - Two Actuarial Reports Now Needed

Actuarial Report For Accounting Actuarial Report

For Funding

16

Will Allocate NPL In Accounting Report By

Member

Play on Words• I kept wondering why the baseball kept getting

bigger and bigger………then it hit me.

• I know a guy who is addicted to brake fluid…he says he can stop anytime.

• They told me I had “Type A” blood, but it was really …..

a Type-O.

• .

17

The New Pension Liability Equation

TPL•Total Pension Liability, Minus

PNP•Plan Net Position, Equals

NPL•Net Pension Liability

18

Terminology-Definitions– Total Pension Liability (TPL) – the portion of the actuarial present value of

projected benefit payments that is attributable to past periods of employee service in conformity with the requirements of Statement 68.

– Plan Net Position (PNP) - Fair Value of Plan Assets less plan liabilities - FMV as of the measurement date (no longer smoothed).

– Net Pension Liability (NPL) – difference between the TPL and the PNP

– Projected Benefit Payments – All benefits estimated to be payable through pension plan to current active and inactive employees as a result of their past service and their expected future service.

– Measurement Date - (No. 68 only) TPL and NPL measured as of the same date not more than 12 months before the reporting date.

19

TPL Illustrated

20

GASB Liability Definition

21

Liabilities are present obligations to sacrifice resources that the government has little or

no discretion to avoid.

GASB Concepts Statement No. 4

Discount Rate = LTEROR For Plan Assets

Plan Net Position = No Asset Smoothing

TPL Calculated Using Traditional Entry Age Normal Actuarial Cost Method

22

Calculating The Net Pension Liability

Change in Plan

Net Position

Change in Total Pension Liability

Change In Net Pension Liability

Deferred Inflows Outflows

Pension Expense

23

Change in TPL

Recognize Some Parts Immediately

Recognize Some Parts Gradually

Deferred Outflows/In

Change in PNP

Recognize Some Parts Immediately

Recognize Some Parts Gradually

Deferred Outflows/In

24

Immediate vs. Gradual Recognition

Expense Immediately

Annual Service

Cost

Benefits Paid

Plan Benefit

Changes

Interest on PY NPL

25

Changes in TPL Expensed Immediately

26

Changes in TPL Expensed Gradually

Assumption Changes

Actuarial Gains and

Losses

Expense Gradually

Recognized

Immediately

Projected Investment

Earnings

Benefits Paid

Administrative Expenses

Actual Contributions

27

Changes in PNPGradual Recognition

For Difference In Projected Vs. Actual Investment Earnings

Deferred Inflows and Outflows

Deferred Inflows and

Deferred Outflows

Concept Statement No.

4

GASB 53-Derivatives

GASB 60 -SCA

GASB 63-Financial Reporting

GASB 65 –Items

Previously Recognized

GASB 68–

Employer Pension

Reporting

28

Play on Words• I tried to catch some fog the other day but…

I mist.

• I’m reading a book about anti-gravity,…

I can’t put it down.

• I couldn’t remember how to throw a boomerang…….

but eventually it came back to me.

29

Calculation of Pension Expense

30

Total Pension

Liability

Plan Fiduciary

Net Position

Net Pension

Liability

(a) (b) (a) – (b)

Balances at 12/31/X8 3,045,893$ 2,283,333$ 762,560$ 289,881$ 30,107$

Changes for the year:

Service cost 101,695 101,695 101,695$

Interest 231,141 231,141 231,141

Changes of benefit terms - -

Differences between expected and actual

experience (69,638) (69,638) - 63,582 (6,056)

Changes of assumptions - - - - -

Contributions—employer 109,544 (109,544)

Contributions—employees 51,119 (51,119) (51,119)

Net investment income 199,273 (199,273) (16,804) - (182,469)

Benefit payments, including refunds (126,863) (126,863) -

Administrative expense (3,427) 3,427 3,427

Other 8 (8) (8)

Expense for beginning deferred amounts (60,320) (3,592) 56,728

Net changes 136,335 229,654 (93,319) (77,124) 59,990

Balances at 12/31/X9 3,182,228$ 2,512,987$ 669,241$ 212,757$ 90,097$ 153,339$

Pension

Expense

Deferred

Outflows of

Resources

Deferred

Inflows of

Resources

No. 68 Timing Issues

Reporting Date (RD)=

BS Date

Measurement Date (MD) =

Within 1 Year of RD

31

No. 68 Timing Issues – School Board

32

6/30/15 RD

Employer and FRS FYE Are The Same

One Year

6/30/14MD

6/30/13 Beg Bal. Date

Restate For Beginning Bal

Adjust To Ending Bal

No. 68 Timing Issues – County

33

9/30/15 RD

Employer FYE

Three Months

6/30/15FRS NPL

6/30/14 FRS Beg NPL

FRS FYE

Restate For Beginning Bal

Adjust to Ending Bal

9/30/14Not Available

No. 71 Contributions Made After MD

34

9/30/15 RD

Measurement Date

Employer FYE

Three Months

6/30/15MD

6/30/14 Beg Bal.

Date

Contributions Made - Deferred

Outflow

Timing Issues

35

I don’t know about you but I’m getting a headache!

36

What about FYE 2014?

FRS Members

No Change From PY, Same Note Disclosures, Because No. 67 Applies

to Plan Reporting Only (FRS Must Implement It, Not You!)

• I don’t trust these stairs because……….

they’re always up to something.

• Police were called to a day care where a 3 year old was………..

resisting a rest.

• I used to have a fear of hurdles, but………

I got over it.

37

Play on Words

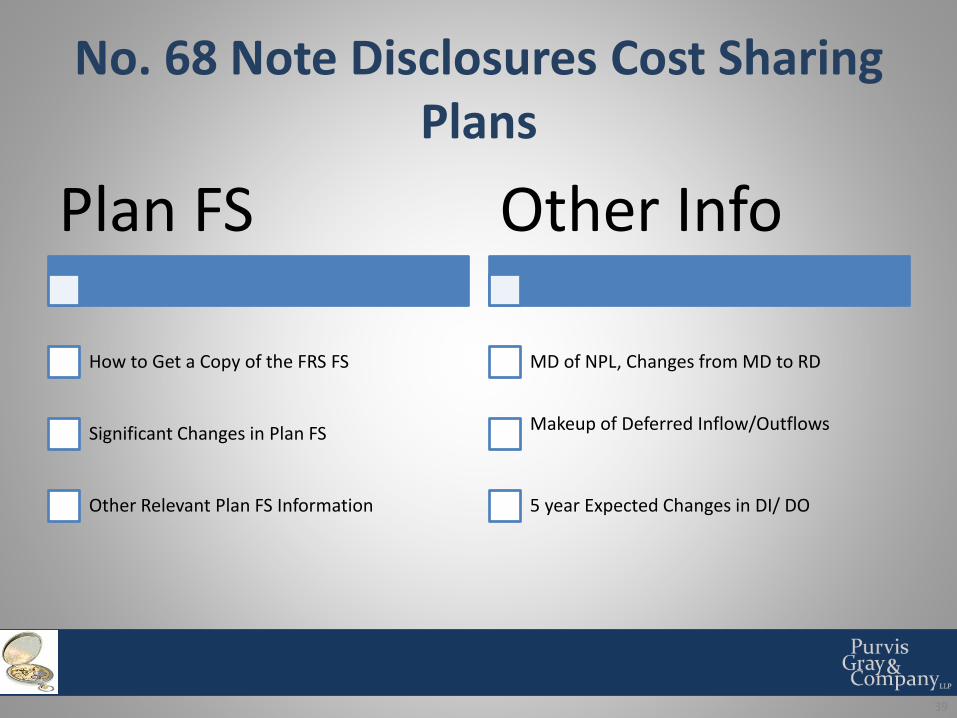

No. 68 Note Disclosures Cost Sharing Plans

Plan Description

Name, Type, Terms, Admin

Classes Covered, Benefits, Authority

# participants, contributions

Assumptions

All NPL Assumptions,

LTEROR Overall and by Investment Class

Discount Rate, NPL +1%, -1% Disc. % Change

38

No. 68 Note Disclosures Cost Sharing Plans

Plan FS

How to Get a Copy of the FRS FS

Significant Changes in Plan FS

Other Relevant Plan FS Information

Other Info

MD of NPL, Changes from MD to RD

Makeup of Deferred Inflow/Outflows

5 year Expected Changes in DI/ DO

39

No. 68 RSI Cost Sharing Plans

10 Yr. NPL & Change in NPL

Employer’s proportion % and amount of NPL, DI & DO

Employers Covered Payroll

NPL as % of Covered Payroll, Plan Net Position as % of TPL

10 Yr. Schedules of

Actuarial Contributions, Required & Actual

Difference in Above

Actual Contributions as % of Covered PR

40

Issues With Cost Sharing Plans - FRS

Need Total FRS NPL Allocated To;

Member A

Member C Member D

Member B

Member E

41

Issues With Cost Sharing Plans FRS

42

AICPARECENTLY ISSUED;

TWO WHITE PAPERS

DESCRIBING ISSUES

THREE AUDIT INTERPRETATIONS

PRESCRIBING SOLUTIONS

TESTING CENSUS DATA & INFO FOR

ER REPORTING

PLAN AUDITOR TO ISSUE

REPORT ON INFO BY PLAN PARTICIPANT

AND TEST CENSUS DATA

Audited CS Plan FS

Unaudited Participant

Data

Not Sufficient ER Audit Evidence

43

AICPA Audit Interpretations

WHY?

Audited CS Plan FS

Audited Participant

Data

Sufficient ER Audit Evidence

44

AICPA Audit Interpretations

However ER auditor has responsibility to recalculate the numerator of the percentage used in the allocation process by the plan.

Materiality Level?

Play on Words

• The dead batteries were given away……

free of charge.

• I was going to look for my lost watch but..

I could never find the time.

• A popular new broom just came out, it’s…….

really sweeping the nation.

45

High-Level Implications

46

More Fuel to Pension Rollback Movement

Net Position May Go Negative

Higher Profile in

CAFR

Liability From Notes

to BS

High-Level Implications

More Volatile FS as Pension Liability Bounces With Market Fluctuations

47

High-Level Implications

Executive Staff and Elected Officials

Press

Employees

48

Communication Challenges

High-Level Implications

Local Governments

Rush To Implement New Std.

49

Start Talking With Your Auditors & FRS

Now

Play on Words• I was struggling to figure out how lightning

works……….

then it struck me.

• I used to be addicted to soap, but……..

I’m clean now.

• A hole was found in the nudist colony’s wall, the police are……..

looking into it.

50

51

The New Pension Standards GASB Statements 67,68 & 71

Florida Court Clerks & ComptrollersFebruary 6. 2015

Mark White CPA, Audit PartnerPurvis Gray & Company LLP

52