the merchant’s guide to chargeback management · winning more than 60% of their chargeback...

TRANSCRIPT

The Merchant’s Guide to Chargeback Management

WHITEPAPER

IntroductionDon’t count your chickens before they hatch.

To some extent, chargebacks are like eggs that did not hatch. You already counted a sale as revenue, only for it to be disputed by the customer, then reversed by the bank a few days later.

A chargeback occurs when cardholders ask their banks to reverse a charge. This could be because the transaction is fraudulent, unauthorized, or due to an unsatisfactory shopping experience with a merchant. If the bank approves the request, it’s forwarded to the merchant who is legally required to reimburse the payment.

As intended, the ability to request a credit card charge be reversed gives shoppers protection against fraud. However, it’s also fertile ground for both real fraud and friendly fraud to flourish.

The most obvious impact of chargebacks on merchants is revenue loss. However, it cuts much deeper, especially considering how competitive the current ecommerce landscape is. For instance, incurring chargebacks leads to wasted customer acquisition spending.

Luckily, merchants are not powerless in the face of chargebacks. There are several things online retailers can do to fight this problem. The key is to know how chargebacks work, the best practices to manage costs and how to increase your dispute success rate.

02trustvesta.com

Chargebacks: the basics

Though you likely understand a few basic things about chargebacks, the information here is meant to enrich or fill the gaps in your understanding of the history, how they work and other foundational knowledge.

A brief history of chargebacks

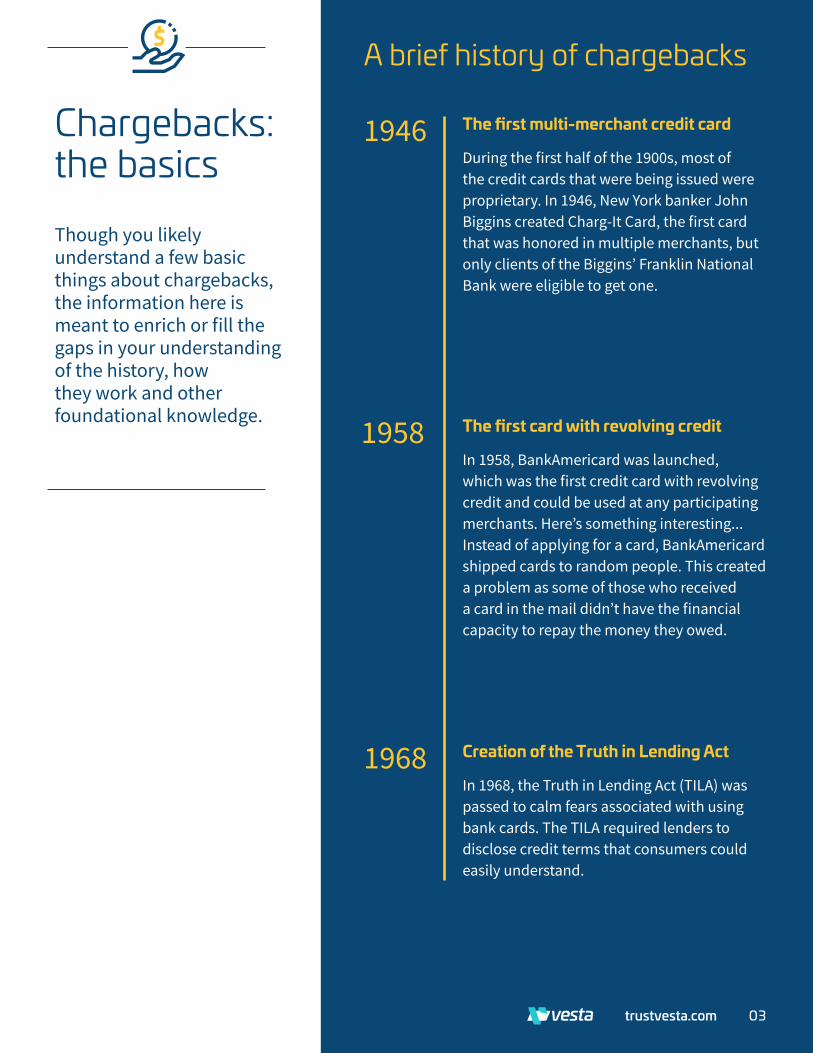

The first multi-merchant credit card

During the first half of the 1900s, most of the credit cards that were being issued were proprietary. In 1946, New York banker John Biggins created Charg-It Card, the first card that was honored in multiple merchants, but only clients of the Biggins’ Franklin National Bank were eligible to get one.

1946

The first card with revolving credit

In 1958, BankAmericard was launched, which was the first credit card with revolving credit and could be used at any participating merchants. Here’s something interesting... Instead of applying for a card, BankAmericard shipped cards to random people. This created a problem as some of those who received a card in the mail didn’t have the financial capacity to repay the money they owed.

1958

Creation of the Truth in Lending Act

In 1968, the Truth in Lending Act (TILA) was passed to calm fears associated with using bank cards. The TILA required lenders to disclose credit terms that consumers could easily understand.

1968

03trustvesta.com

Launch of the Fair Credit Billing Act (FCBA)

In 1974, Congress amended the Truth in Lending Act which gave birth to the Fair Credit Billing Act. This was arguably the first law that enabled credit card holders to dispute charges. The FCBA allowed cardholders to dispute charges that were at least $50 and met the following conditions:

• Unauthorized charges

• The amount charged was incorrect

• Charges for goods that the customers did not receive or accept

• The charge reflects a wrong date

• Calculation errors

• The goods were not as described or damaged

1974

Enactment of the Electronic Fund Transfer Act

The TILA and the FCBA only covered credit card holders. In 1978, the Electronic Fund Transfer Act was passed to give the same protection to debit card holders, although its provisions were not as comprehensive as the FCBA.

1978

04trustvesta.com

The 5 most common reasons for chargebacks

One of the most crucial steps in fighting chargebacks is knowing the reasons why customers file for refunds with their banks in the first place.

Let’s get into the minds of your customers and explore their top motivations and intentions when they file for chargebacks.

1 “I believe I’ve been the target of fraud.”

Fraud is the most legitimate reason for chargebacks and exactly why chargeback-related laws were created in the first place.

30% 30% of all chargeback claims are filed due to unauthorized transactions.

05trustvesta.com

06

2 “I didn’t receive my order.”

Lost parcels, issues with courier services, stock issues, delays in order preparation —there are a host of reasons for goods not reaching your customers.

How do you know whether your customers are telling the truth or just avoiding paying for some reason? (More on this later).

Not receiving an online order is the second most common reason shoppers file for chargebacks, accounting for 26% of all claims.

This type of chargeback represents 15% of all claims made.

26%

3 “This isn’t what I ordered.”

If a customer ordered a fitted sheet for a queen size bed and received one for a king size bed, they can (and will) file a chargeback if unable to sort things out on their own with the merchant.

15%

06trustvesta.com

4

5

“Item is not as described.”

This is arguably the most disputed, sensitive and controversial type of chargeback. When customers feel they were deceived into buying a product, they (understandably) want their money back. This is closely related to another common chargeback reason: customers filing for credit charge reversals when the items they received didn’t match their expectations. These claims may be legitimate or may be due to unreasonable consumer behaviors.

“I was billed incorrectly.”

Incorrect credit card charges can manifest in different ways. This could mean getting billed twice for the same purchase, getting charged for shipping when it’s supposed to be free, and other clerical errors.

These are just the top overarching reasons customers file for chargebacks. If you’ve experienced chargebacks before, you probably already know that there are additional causes represented by reason codes. That said, understanding the above-mentioned reasons cover the most common—and most costly—types of chargebacks that plague merchants.

07trustvesta.com

An overview of the chargeback processOne major complaint of merchants when it comes to the chargeback process is it’s too complicated. In an attempt to simplify things, we created the diagram below.

The above diagram can have additional steps if the cardholder decides to dispute again. If the cardholder opts to do so, the entire process starts again. This is called pre-arbitration. If the merchant wins the pre-arbitration, the cardholder can dispute again and the issuing bank starts the arbitration process. This will automatically incur a $250 charge against the merchant. The merchant will recoup this amount if they win the arbitration. However, if the merchant loses, it will incur an additional

$250 charge or more (some card networks impose fines from $500 to $900).

This is why a number of merchants are hesitant to dispute chargebacks, especially because only 21% of chargeback disputes are ruled in favor of ecommerce retailers.

That leads to the billion-dollar question (figurative and literal: How can chargebacks potentially cripple your business?

Is the compelling

evidence sufficent?

Customer calls theirissuing bank to file

a disupute

Does the merchant dispute the chargeback?

The merchant reviews the chargeback and decides whether to

dispute it or not.

The merchant gathers compelling evidence related

to the transaction in question and forwards it to the

acquiring bank.

The acquiring bank reviews the evidence

and forwards it to the card network.

The card network passes the evidence

to the issuing bank for final review.

The acquiring bank forwards the chargeback

to the merchant.

The merchant loses and the customer retains the credit.

The merchant wins and the chargeback is reversed. The

customer loses the credit that was initially given.

The card network facilities the reversal of funds from the merchant’s bank account via an acquirer. This part of the

process involves fees that are later passed on to the merchant

Issuing bank reviews the dispute and

decides whether it’ valid or not.

Is the dispute valid?

End of the chargeback process

The issuing bank immediately issues credit to

the customer and forwards the dispute to the card network.

No

No

Yes

Yes

Yes

No

08trustvesta.com

The frightening facts on how chargebacks impact e-commerce businessesThe facts are frightening: Repercussions of chargebacks in the e-commerce industry are well documented. They’re widespread and they hamper the growth of hardworking merchants like yourself.

It’s time to face some scary statistics:

A multi-billion dollar problem

Merchants are currently losing upwards of $40 billion annually to chargebacks. In many of these cases, the online retailers were not at fault, but they still shoulder the burden of lost revenue, unrecoverable goods and chargeback fees for the disputes they lose. These chargeback-related costs force several merchants to raise their prices to recover some of their losses.

$40Billion

A product of fraud

As mentioned earlier, fraud accounts for most of the chargeback claims filed by shoppers. It’s not surprising that 49% of the revenue merchants lose due to fraud can be attributed to chargebacks.

49%

Growing at an alarming rate

Chargebacks are bulldozing the e-commerce landscape, and increasing at an alarming rate. The number of chargebacks online merchants need to deal with is growing by 20% annually.

20%

Consumers are pulling the trigger on filing chargebacks

In an ideal world, chargebacks should be the last resort of consumers. In the case of unmet expectations, defective goods, and wrong products delivered, the customers should reach out to the merchants first to sort things out. However, 58% of shoppers immediately contact their banks to file for a chargeback.

58%

09trustvesta.com

Merchants on the losing end of chargeback disputes

Merchants are not taking chargebacks lying down. In fact, 80% of merchants dispute chargebacks they believe are illegitimate. However, only 18% of online retailers are winning more than 60% of their chargeback disputes. This means that most of the time, the majority of merchants are losing and are bearing the high costs involved in the chargeback dispute process.

18%

Not-so-friendly fraud

Among all chargeback claims filed, 71% are chargeback fraud and friendly fraud. There’s a slight difference between the two. Friendly fraud involves chargebacks filed because of honest mistakes from customers (i.e. they didn’t recognize a specific legitimate charge on their credit card). Chargeback fraud involves customers trying to use their right to file chargebacks to avoid paying for goods they purchased.

71%

Wasted Customer Acquisition Spend

The average cost per acquisition (CAC) or the cost to acquire a new customer in ecommerce is $45 This means that aside from the revenue and the fees that merchants lose due to chargebacks, the money they spent in acquiring new customers also goes down the drain.

$45.27

010trustvesta.com

If chargebacks are left unchecked, you can easily hemorrhage hard-earned revenue. There are other risks associated with chargebacks. For instance, a high chargeback ratio can lead to the cancellation of your merchant account. The account preventing you from accepting payments from that specific payment channel. This will lead to further customer and revenue loss.

The statistics are indeed scary.

Fortunately, it’s not all doom and gloom for merchants. In fact, merchants are far from being helpless when it comes to preventing or minimizing chargebacks.

011trustvesta.com

The 10 commandments of chargeback management

“The worst time to develop a plan is when you get a chargeback. Chargebacks can catch owners by surprise very often, but then they have a minimal amount of time to respond, so there’s no time to learn what it is or how to respond.”

– Chip RogersPresident and CEO, Asian American Hotel Owners Association

The question is not whether chargebacks will happen, but rather: How strong are the defenses you put in place to minimize their effects and how prepared are you to mitigate loss if you get hit with a chargeback claim?

012trustvesta.com

1

• The chargeback amount cannot exceed the transaction amount

• Chargebacks cannot be claimed as a chargeback remedy for cashback transactions

• For orders that were delivered late, customers should first attempt to return the products to get a refund from the merchant before filing for a chargeback

• For chargebacks with reason codes requiring customers to sort things out with the merchants first, the issuing bank has the responsibility to verify that a customer has contacted the merchant before entertaining a chargeback claim

• In cases of returned items, the issuing bank should wait 15 days before processing a chargeback to give the merchant an opportunity to respond

• A chargeback should be filed within the allowable time period

• All chargeback process steps should be completed before moving the dispute to pre-arbitration and arbitration

• All merchants have the right to chargeback representment or to dispute chargebacks using all legal means

You shouldn’t be shy in exercising these rights to protect your business from chargebacks, especially if you have compelling evidence to prove that a chargeback was lodged against you incorrectly.

Know thy rights as a merchantJust as consumers have rights to file for chargebacks, the law also affords merchants certain rights to protect themselves from malicious chargeback claims. These rights include the following:

Vesta’s 10 commandments of chargeback management

013trustvesta.com

• Choose a secure payment gateway that uses a dynamic risks database to increase fraud prevention while allowing legitimate orders to go through

• If available and possible, choose a merchant solution that combines merchant processing and settlement, fraud prevention, and chargeback management

• Use a multi-layered authorization and verification system

• Use automated fraud detection and prevention tools. Budget permitting, invest in artificial intelligence or machine learning fraud prevention technology

• Use manual reviews periodically to allow your fraud managers to understand what transactions were automatically accepted, declined, and submitted for further evaluation

If you win the battle against fraud, you’re preventing the biggest potential source of chargebacks that might hurt your business.

2

Strengthen your fraud protectionThe equation is quite simple:

Low fraud = low chargebacks.

Of course, this is easier said than done. It takes a strategic mix of good fraud detection and prevention practices and technologies to achieve this:

014trustvesta.com

3

• Proof of delivery Signed delivery receipts to prove that your customers received the goods you shipped

• Communications log Documented communications between you and your customers pertaining to the disputed transaction

• Address matches Proof of a matching addresses bolster your chance that the transaction was legitimately made (customer name matches billing address, customer name matches shipping address, shipping address matches billing address).

• Purchase history If a customer has purchased an item from you before, especially if the customer has purchased a similar item involved in the transaction in dispute

• Email Should match with the email provided by the customer during the time of the transaction

• Successful payment results The billing/shipping address of the transaction matches the billing address of the cardholder in the issuing bank’s records. This also refers to previous transactions made by the same cardholder using the same identity and card information that didn’t result in a chargeback.

• Browsing data The transaction was made using devices used by the cardholder in other transactions

Thou shall collect data for possible disputesData is the biggest ally of merchants in disputing wrongfully filed chargebacks against them. The only way to win chargeback disputes is to gather compelling evidence that you held up your end of the bargain.

Here are the important data that you need to collect:

015trustvesta.com

Make sure your customers can easily recognize that a charge on their credit card statement came from you. Using your company’s trade name instead of your online store’s name can create confusion among shoppers and may flag a legitimate transaction as fraudulent.

4Use a clear payment descriptor

016trustvesta.com

5“Padding” your product descriptions to make them more attractive and lure buyers is a surefire way to incur chargebacks.It creates unrealistic expectations among shoppers. This will not only cost you money in chargebacks but will also ruin your reputation.

When shoppers read your product descriptions, they should clearly know what they will be getting in the mail. Provide a detailed description, photos, and other visual aids. If there are discrepancies from product to product because of production, make sure to mention them.

Provide accurate product descriptions

017trustvesta.com

6To avoid chargebacks due to late deliveries, make sure that you have a solid procurement/production, assembly, and shipping timelines. Employ good stock management practices. Your fulfillment center should be aware of your delivery schedule. The courier you use should be reliable. In the event that you cannot meet the agreed delivery date, communicate with the customers and take the appropriate steps, before the delivery date arrives.

Ensure thy delivery timelines are met

018trustvesta.com

7Instead of filing a chargeback with their banks, you want your customers to reach out to you and facilitate a refund and return for products that did not meet their expectations. Make sure that your return and refund policies are prominently displayed on all relevant channels such as your website, social media channels, order confirmation emails and receipts.

Communicate a clear return and refund policy

019trustvesta.com

8If your customers feel that it would be easier to talk to their banks than to sort things out with you, they will immediately file for a chargeback to get their money back instead of using it as a last resort. Excellent customer service is not only a non-negotiable when it comes to customer acquisition and retention. It is also a necessary ingredient for chargeback minimization.

Provide five-star customer service

020trustvesta.com

Investing in fraud-related chargeback guarantees is similar to investing in insurance policies. For instance, Vesta’s Payment Guarantee solution covers funds for all accepted CNP transactions with no liability to merchants for fraud-related chargebacks. Merchants incur zero chargebacks, fines or fees related to third-party fraud and unauthorized charges.

The reality is at some point, you will be hit with fraud-related chargebacks. The volume of chargebacks can be higher or lower depending on the season (i.e. peak shopping seasons are often associated with higher chargebacks). Having a chargeback guarantee minimizes the financial loss on your end.9

Invest in fraud-related chargeback guarantees

021trustvesta.com

While we all want to dispute every chargeback that comes our way, we do not recommend fighting all chargebacks tooth and nail. Remember, the chargeback process favors customers more than merchants. Evaluate the situation. Does the chargeback include a minimal amount? Is the reason behind the chargeback (i.e. lost goods) difficult to challenge? Do you have enough compelling evidence to argue your case? There will be times when disputing a chargeback will only result in more lost money and time. Choose your battles strategically.

Implementing these 10 strategies does not guarantee that your chargebacks will disappear overnight, nor can it guarantee that you will have zero chargebacks moving forward. Realistically speaking, no merchant is chargeback-proof.

That said, implementing these 10 chargeback management commandments gives you a comprehensive defense against chargebacks. They also ensure that chargebacks will not make a significant dent on your profitability.

10

Choose thy chargeback battles wisely

022trustvesta.com

Final words: You’re in charge

While chargebacks are not inherently evil, using it inappropriately and maliciously can hurt merchants. It’s an ugly truth everyone in the ecommerce business has to face, manage and mitigate. And just like any crisis, your preparedness to deal with chargebacks can spell the difference between failure and success.

Are you looking for a chargeback mitigation and management partner you can trust? Vesta is here for you. Vesta Corporation is a pioneer in processing fully guaranteed Card Not Present (CNP) payment transactions for ecommerce merchants. We offer scalable protection payment solutions and patented fraud protection services. We focus on protecting your revenue from chargebacks and fraud so you can focus on your company’s strategic growth. Our team is ready to help you.

023trustvesta.com

Get in TouchFind out How

Take charge of chargebacks with Vesta