the locational distribution of foreign banks in china: a

TRANSCRIPT

This article was downloaded by: [NUS National University of Singapore]On: 02 August 2011, At: 00:12Publisher: RoutledgeInforma Ltd Registered in England and Wales Registered Number: 1072954 Registered office: MortimerHouse, 37-41 Mortimer Street, London W1T 3JH, UK

Regional StudiesPublication details, including instructions for authors and subscription information:http://www.tandfonline.com/loi/cres20

The Locational Distribution of Foreign Banks inChina: A Disaggregated AnalysisCanfei He a & Godfrey Yeung ba College of Urban and Environmental Sciences, Peking University, Beijing, 100871, ChinaE-mail: [email protected] Department of Geography, National Singapore University, Singapore, 117570

Available online: 15 Jun 2010

To cite this article: Canfei He & Godfrey Yeung (2011): The Locational Distribution of Foreign Banks in China: ADisaggregated Analysis, Regional Studies, 45:6, 733-754

To link to this article: http://dx.doi.org/10.1080/00343401003614282

PLEASE SCROLL DOWN FOR ARTICLE

Full terms and conditions of use: http://www.tandfonline.com/page/terms-and-conditions

This article may be used for research, teaching and private study purposes. Any substantial or systematicreproduction, re-distribution, re-selling, loan, sub-licensing, systematic supply or distribution in any form toanyone is expressly forbidden.

The publisher does not give any warranty express or implied or make any representation that the contentswill be complete or accurate or up to date. The accuracy of any instructions, formulae and drug doses shouldbe independently verified with primary sources. The publisher shall not be liable for any loss, actions, claims,proceedings, demand or costs or damages whatsoever or howsoever caused arising directly or indirectly inconnection with or arising out of the use of this material.

The Locational Distribution of Foreign Banksin China: A Disaggregated Analysis

CANFEI HE∗ and GODFREY YEUNG†∗College of Urban and Environmental Sciences, Peking University, Beijing 100871, China. Email: [email protected]

†Department of Geography, National Singapore University, Singapore 117570. Email: [email protected]

(Received December 2008: in revised form December 2009)

HE C. and YEUNG G. The locational distribution of foreign banks in China: a disaggregated analysis, Regional Studies. This paper

examines the location choices made by foreign banks of different organizational form and size in China. Results from the con-

ditional logit models suggest smaller foreign banks tend to pursue the ‘follow-the-customer’ strategy, while larger banks are likely

to use the ‘follow-the-competitor’ strategy in China. The agglomeration effect is more important than the first-mover cities as a

determinant of the location choices make by foreign banks in China. This finding could be partially explained by the location-

bounded institutional variables that are unable to be fully reconciled with the recent deregulation policies.

Foreign banks Location choices Conditional logit model China

HE C. et YEUNG G. La distribution geographique des banques etrangeres en Chine: une analyse desagregee, Regional Studies. La

presente etude cherche a analyser le choix d’emplacement des banques etrangeres en Chine en fonction de leur structure orga-

nisationnelle et de leur taille differentes. Les resultats provenant des modeles logit conditionnels laissent supposer qu’en Chine les

plus petites banques etrangeres ont tendance a poursuivre la strategie de ‘suivre le client’, alors que les plus grandes banques sont

plus susceptibles d’adopter la strategie de ‘suivre le concurrent’. L’effet d’agglomeration s’avere plus important que ne l’est le phe-

nomene du premier arrive dans les grandes villes comme determinant des choix d’emplacement des banques etrangeres en Chine.

Ce resultat pourrait, du moins en partie, s’expliquer par des variables institutionnelles qui sont delimitees geographiquement et qui

ne peuvent pas etre conciliees avec les politiques recentes de dereglementation.

Banques etrangeres Choix d’emplacement Modele logit conditionnel Chine

HE C. und YEUNG G. Verteilung der Standorte auslandischer Banken in China: eine disaggregierte Analyse, Regional Studies. In

diesem Beitrag werden die Standortentscheidungen auslandischer Banken verschiedener Organisationsformen und Großen in

China untersucht. Aus den Ergebnissen konditionaler Logit-Modelle geht hervor, dass kleinere auslandische Banken in China

meist eine Strategie des „Dem-Kunden-Folgens“ wahlen, wahrend großere Banken meist auf eine Strategie des „Der-Konkur-

renz-Folgens“ setzen. Der Agglomerationseffekt spielt als Determinant fur die Standortentscheidungen auslandischer Banken in

China eine großere Rolle als die Pionierstadte. Dieses Ergebnis lasst sich teilweise durch die standortgebundenen institutionellen

Variablen erklaren, die sich nicht vollstandig mit den aktuellen Deregulationspolitiken in Einklang bringen lassen.

Auslandische Banken Standortentscheidungen Konditionales Logit-Modell China

HE C. y YEUNG G. La distribucion de ubicacion de los bancos extranjeros en China: un analisis desglosado, Regional Studies. En

este artıculo analizamos las decisiones de ubicacion tomadas por bancos extranjeros de diferentes formas de organizacion y tamanos

en China. Los resultados de los modelos logit condicionales indican que en China los bancos extranjeros mas pequenos tienden a

optar por la estrategia de ‘seguir al cliente’ mientras que los bancos mas grandes tienden a usar la estrategia de ‘seguir a la compe-

tencia’. El efecto de aglomeracion desempena un papel mas importante que el de las ciudades pioneras para determinar las

Regional Studies, Vol. 45.6, pp. 733–754, June 2011

0034-3404 print/1360-0591 online/11/060733-22 # 2011 Regional Studies Association DOI: 10.1080/00343401003614282http://www.regional-studies-assoc.ac.uk

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

decisiones de ubicacion que realizan los bancos extranjeros en China. Estos resultados podrıan explicarse en parte por las variables

institucionales vinculadas a la ubicacion que no pueden reconciliarse totalmente con las recientes polıticas de desregulacion.

Bancos extranjeros Decisiones de ubicacion Modelo logit condicional China

JEL classifications: C10, O53, P21, P33

INTRODUCTION

To prepare for accession to the World Trade Organiz-ation (WTO), China has accelerated the pace of liberal-ization in the banking industry by gradually lifting itsgeographical and customer restrictions on foreignbanks since the late 1990s. The rapidly growingeconomy together with deregulation of the bankingsector has motivated multinational banks to establishbranches in China. By 2007, 193 banks based inforty-seven countries or regions had 242 representativeoffices in China, twenty-four wholly foreign-ownedbanks had 119 branches, two joint-venture banks hadfive branches, and there were three wholly foreign-owned financial companies. Foreign banks’ total assetsamounted to RMB1253 billion (renminbi or yuan) in2007, accounting for 2.38% of China’s total bankingassets (CHINA BANKING REGULATORY COMMISSION

(CBRC), 2008).Another aspect of the major deregulation policies in

China’s banking industry is the introduction of foreignstrategic investors. According to the CBRC (2007),about thirty foreign banking institutions had acquiredstakes in twenty-one Chinese commercial banksthrough strategic investment agreements by 2006.These foreign banking institutions originate from avariety of countries or regions, including the UnitedStates, Japan, Singapore, Germany, Hong Kong,France, Australia, and international institutions such asthe Asian Development Bank (ADB) and InternationalFinance Corporation (IFC). Foreign participation offersdomestic banks the prospect of improved managementpractices, attractive opportunities for businesscooperation, enhancement of their reputation incapital markets, and injections of equity capital (HOPE

and HU, 2006; LENG, 2006).Studies of foreign banking have been flourishing

since the 1980s, with the focus on internationalbanking in developed economies including the UnitedStates, Europe, and Japan, and the determinants of thesize of foreign bank presence in host countries(ALIBER, 1984; CHO, 1985; HULTMAN and MCGEE,1989; GOLDBERG and JOHNSON, 1990; WILLIAMS,1997, 2002). The expansion of international bankingin China has triggered a series of research projects intoforeign banking activities. Existing studies, however,have targeted the expansion of foreign banks in Chinaas a whole or in a particular city (for example, LEUNG,1997; LEUNG and YOUNG, 2005; LU and DEWHURST,2007, etc.). LEUNG and YOUNG (2002) and BONIN

and HUANG (2002) examined the implications ofChina’s accession to the WTO for foreign and domesticbanks, respectively. ZHANG and YANG (2007) examinedthe distribution of foreign banks in sixteen Chinese citiesby 2006, and found, as they predicted, that internationaltrade and per-capita income were significant in deter-mining the location of foreign banks in China.

The current literature, however, is unable to explainthe potential influence of the institutional environment(especially the formal structures of rules and regulationsstipulated by the CBRC) on the location choices madeby foreign banks in China. Foreign banking institutionsin China come from rather diverse backgrounds interms of their parent banks’ sizes and functions. Thelocation of foreign banks may significantly differaccording to the specific type of banking institution.

This paper aims to contribute to the existing litera-ture by examining two major propositions concerningthe location choices made by foreign banks with differ-ent bank assets (small banks versus large banks) and theirentry mode choice of organizational form (branches andsub-branches versus representative offices) in the transi-tional economy of China. The two propositions are thatforeign banks could pursue follow-the-competitor and-customer strategies and/or adopt first-mover citiesand local currency banking strategies. The former prop-osition is derived from Dunning’s eclectic paradigm(GRAY and GRAY, 1981; PETROU, 2007), while thetwo institutional variables – first-mover cities andlocal currency banking – are used to examine thepotential impact of liberalization policies on thelocation choices of foreign banks in China. There isstrong evidence from the conditional logit models tosuggest that different types of foreign banking insti-tutions display specific location patterns. Smallerforeign banks tend to pursue the ‘follow-the-customer’strategy to lower investment risks and maintainbusiness–client networks in their choice of whichChinese cities in which to locate. Foreign banks,especially larger ones, have considerable ownershipadvantages and tend to mimic the location choices oftheir major competitors and select cities with largepotential banking opportunities. To collect vital andup-to-date information, foreign banks tend to locatetheir representative offices in Beijing and Shanghai,with their informational externalities, or other first-mover cities, involved in opening up local currencybanking to reap the locational advantages created bythe deregulation of the Chinese banking industry.

734 Canfei He and Godfrey Yeung

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

As a transitional economy, the authors expected thegradual approach of deregulation implemented by theCBRC to have a significant impact on the locationchoices made by foreign banks in China. The statisticalevidence nonetheless suggests that the potential impactof the institutional environment in the locationdecisions of foreign banks is not as high as expected:the location choice of foreign banks is determinedmore by the agglomeration effects generated by theirmajor competitors and the CBRC deregulation policiesregarding local currency banking, but much less so forthe first-mover cities policy per se. This finding couldbe partially explained by limitations to the location-bounded institutional variables. The CBRC’s deregula-tion policies on first-mover cities could have a biggerimpact on the scale and pace of foreign banks’ invest-ment and the varieties of banking products than thelocation choices of foreign banks alone. This could bethe case as most (coastal) areas that could provide poten-tially lucrative banking opportunities for profit-oriented foreign banks have been opened up for along time. The concentration of foreign banks inthese first-mover cities thus created further agglomera-tion effects for the latecomers.

Before describing the methodology and data sources,a brief review of the literature and the corresponding sixresearch hypotheses are outlined in the next section.The following section then describes the entry patternsand location distribution of foreign banks in China. Thefindings of this paper are then presented and analysedbefore conclusions are given.

UNDERSTANDING FOREIGN BANKING

LOCATIONS

This section discusses the importance of various deter-minants for the location choices of foreign banks inhost countries.

Dunning’s eclectic paradigm of international pro-duction has been widely applied to explain the locationsof the value-added activities of transnational corporationsoutside their home countries: the location choices offoreign direct investment (FDI) by transnationalcorporations are based on a combination of ownership,internalization, and locational advantages (DUNNING,1979, 1981, 2001). The conventional eclectic paradigmapproach (without the institutional elements) is widelyused to explain the international expansion of multina-tional banks (GRAY and GRAY, 1981; YANNOPOULOS,1983; CHO, 1985; PETROU, 2007).

There have been some additions to the electric para-digm in response to the significant changes in the globaleconomy during the last two decades. In addition tonon-equity alliances or contractual relationships(including outsourcing) (DUNNING, 2001), the impor-tance of social capital, where economic institutions are amanifestation of the underlying values and practices of a

given culture (NORTH, 1991), as institutionally relatedlocation advantages for transnational corporations, ishighlighted by LUNDAN (2003).1 MAITLAND andNICOLAS (2003) argued that the new institutionaleconomics could resolve the limitations of location-specific ownership advantages implied by the appli-cation of the electric paradigm. Douglass North’swork on the institutional environment (NORTH,1990, 2005) – the formal rules (such as laws and regu-lations) and informal constraints (such as behaviouralnorms) that could govern the ownership, internaliz-ation, and locational advantages – was adopted byDUNNING (2006) and further incorporated into theeclectic paradigm by DUNNING and LUNDAN (2008).In the banking industry, for instance, the establishedcode of conduct and corporate culture could be insti-tutional-specific assets and, hence, part of the ownershipadvantages of multinational banks in host countries. Tofacilitate their capital flows, multinational banks alsotend to locate in host countries with locationallybounded ‘sticky’ assets, such as more liberal legal andregulation systems.

Ownership and internalization advantages: follow the competitor

or customer

Foreign banks normally possess certain ownershipadvantages that allow their subsidiaries to competewith domestic banks in host countries (MILLER andPARKHE, 1998). These ownership advantages areassumed to be unique to certain banks of a particularnational ownership and could be in the form of spatiallytransferable tangible and intangible assets, ranging fromtheir capabilities and capacities to offer superior bankingproducts and a unique banking experience for theirclients due to their advanced information technologiesand managerial skills (ALIBER, 1984; CHO, 1985;YANNOPOULOS, 1983; WILLIAMS, 1997). By locatingtheir subsidiaries in major global financial centres,such as London and New York, foreign banks reapthe ownership advantages of being able to raise financialcapital at lower costs and gain access to specializedservices provided by other complementary sectors( JONES, 1993). Ownership advantages may triggervarious forms of strategic behaviour between foreignbanks, which commonly include the follow-the-leader, ‘tit-for-tat’ oligopolistic reaction (KNICKER-

BOCKER, 1973) and exchange of threats (GRAHAM,1978). Foreign banks thus mimic each other’s invest-ment behaviour, including the location of theirbranches in host countries (ENGWALL and WALLEN-

STAL, 1998). This ‘follow-the-competitor’ strategy isreported by HELLMAN (1994) as the pattern of theinternational expansion of Swedish and Finnish banks.As China is widely considered a strategic market withhigh profit margins for multinational banks (YEUNG,2009a), the major global banks are likely to follow

Locational Distribution of Foreign Banks in China 735

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

their rivals and set up branches in China to maintaintheir market coverage.

In addition to ownership advantages, multinationalbanks possess greater organizational efficiency thatallows them to provide cross-border services to theirexisting clients in host countries (GRAY and GRAY,1981). Information embodied in clients is difficult toobtain at arm’s length due to the asymmetry of infor-mation in an imperfect market where face-to-faceinteractions are vital for deal making. To preservetheir established customer networks and their affiliatedinformation, multinational banks have to establishrepresentative offices or branches in host countries tointernalize such firm-specific advantages (hence,internalization advantages) ( JONES, 1993; WILLIAMS,1997; MILLER and PARKHE, 1998; YANNOPOULOS,1983).2 The argument for internalization advantagesassumes foreign banks implement the ‘follow-the-customer’ strategy when investing in host countries(KINDLEBERGER, 1983; WILLIAMS, 1997, 2002).

As more than 190 foreign banks of various sizes haveestablished banking institutions in China, the ownershipadvantages derived from the size of the bank could havean impact on the choice of location. Major banks wieldconsiderable market power and could raise fundsthrough the capital market for their overseas expansionsat lower costs. The size of the bank is an importantdeterminant of foreign banking expansion in Japanand Korea (URSACKI and VERTINSKY, 1992), andsmaller firms tend to follow their major competitorsto reap the informational externalities (TORRE,2008). China is not likely to be an exception. The own-ership advantages of large foreign banks may triggerfollow-the-competitor oligopolistic behaviourbetween rival banks in their location choice in China.With fewer ownership advantages and higher levels ofrisk aversion, smaller foreign banks may aim to preservetheir existing business–client networks in their selec-tion of investment sites. Based on the above discussion,the following are inferred:

H1: Larger foreign banks tend to pursue the ‘follow-the-competitor’

strategy to lower their investment risks in their location choices of

Chinese cities.

H2: Smaller foreign banks tend to pursue the ‘follow-the-

customer’ strategy to maintain their business– client networks in

their location choices of Chinese cities.

Locational advantages and formal institutional environment in the

banking industry

Locational advantages, in the form of both non-transferable tangible and intangible assets specific to aparticular area, are vital to the selection of investmentsites by foreign banks across and within host countries.Foreign banks normally aim for market penetrationwhen expanding internationally, by either the ‘follow-the-customer’ or the ‘follow-the-competitor’ strategies

(YANNOPOULOS, 1983; ALIBER, 1984; CHO, 1985;YAMORI, 1998). Market opportunities are typicallydefined by the size of the economy or the bankingmarket in host countries. This hypothesis has beenwidely tested through the location patterns of foreignbanks in their host countries. For instance, it is widelyreported that the foreign investment of US bankspositively correlates with the overseas manufacturingactivities established by US-based firms (GOLDBERG

and SAUNDERS, 1981; NIGH et al., 1986; HULTMAN

and MCGEE, 1989; GOLDBERG and JOHNSON, 1990;GOLDBERG and GROSSE, 1994; MILLER and PARKHE,1998). ESPERANCA and GULAMHUSSEN (2001) furtherreported that foreign banks in the United States followboth their corporate and their non-corporate customers,and a similar trend was also observed by TICKELL (1994)and YAMORI (1998) in the international expansion ofJapanese foreign banks. FOCARELLI and POZZOLO

(2001) found that Organisation for Economic Co-operation and Development (OECD) countries withmore market opportunities and the potential for ahigher level of profitability attract more foreign banks.WELLER and SCHER (2001) confirmed the significanceof market size, real economic growth, profit opportu-nities, and the level of development of domesticbanking markets. MAGRI et al. (2005) reported that theprofit opportunities of the local market in Italy haveproved to be of great importance.

In addition to following their clients in the manufac-turing sectors, foreign banks follow trading companieswith high volumes of transactions in their host countries(GOLDBERG and SAUNDERS, 1980; GOLDBERG andJOHNSON, 1990; GROSSE and GOLDBERG, 1991;HEINKEL and LEVI, 1992; YAMORI, 1998; BUCH,2000; MAGRI et al., 2005). Studying the pattern offoreign bank offices across thirty-seven home andeighty-two host countries, BREALEY and KAPLANIS

(1996) found a significant relationship between thepatterns of bank location, trade, and FDI. Foreignbanks are found to follow their customers within a hostcountry, for example, the total value of imports andexports is closely related to the level of foreign bankingactivity within a particular US state, where the UnitedStates is the host country (GOLDBERG et al., 1989,GOLDBERG and GROSSE, 1994; BAGCHI-SEN, 1995).In China, LEUNG (1997) reported that nearly 92% offoreign banks were engaged in trade finance andprovided loans to Sino-foreign joint ventures. ZHANG

and YANG (2007) examined the distribution of foreignbanks in sixteen Chinese cities by 2006 and found thatthe international trade and per-capita incomes weresignificant determinants of the location of foreignbanks in China.

Furthermore, different types of foreign bankinginstitutions may respond differently to a variety of loca-tional advantages. Foreign banks normally expand theiroperations in host countries within three organizationalforms: subsidiary, branches, or representative office.

736 Canfei He and Godfrey Yeung

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

Multinational banks normally invest heavily in settingup subsidiaries as they are incorporated into the hostbanking system, while much less investment is requiredto set up representative offices. As the Chinese govern-ment only allowed the incorporation of foreign banks in2007, the establishment of subsidiaries by multinationalbanks will not be examined in this paper. Branches andsub-branches conduct various forms of foreign and localcurrency business, while representative offices aim tocollect information and identify possible businessopportunities, and provide advisory services to foreignfirms in China. Foreign banks may tend to locatetheir branches in cities with more banking opportu-nities to enable them to recoup higher levels of invest-ment, while their choices of representative offices maybe more sensitive to informational advantages in theirselected areas (CHAMLEY, 2003). As illustrated by theinformation and communication technology clustersin Silicon Valley (California) and Silicon Sentier(Paris) (VICENTE and SUIRE, 2007), some foreignbanks may simply imitate the location choices ofother foreign banks to reap the potential benefits ofinformational externalities (and lower the level ofuncertainty), and this could contribute to the agglom-eration of foreign banks in certain Chinese cities.3

The circular causation for agglomerated foreign banksand bankers, which is generated by forward and back-ward linkages, leads to increasing returns to scale andcould be considered by other foreign banks as a loca-tional advantage and thus create an even higher levelof spatial agglomeration (also ROMER, 1986;KRUGMAN, 1991b; and FUJTA and THISSE, 1996).4

Notwithstanding the possibilities of this type of imita-tion decision by some foreign banks, it is suggestedthat risk-averse foreign banks tend to locate their repre-sentative offices in Chinese cities with informationalexternalities to serve their existing clients. Due to thepotential size of local markets, it is likely that majorcities, such as Beijing and Shanghai, are also agglomer-ated with foreign banks in other organizational forms.Therefore, the following are speculated:

H3: Foreign banks tend to locate their branches and sub-branches

in Chinese cities with more potential banking opportunities.

H4: Foreign banks tend to locate their representative offices in

Chinese cities with informational externalities.

In addition to the ‘follow-the-competitor and -custo-mer’ strategies, the institutional environment in thebanking industry could have a significant impact onthe location choices of multinational banks in hostcountries. This is especially the case in a liberalizingbanking industry, where the scale and pace of insti-tutional evolution is path dependent on the politicaland socio-economic stability of China (YEUNG,2009a). As the geographical scale and pace of the liberal-ization of the Chinese banking industry are largely dic-tated by the CBRC’s policies, it is logical to highlight

the formal institutional factors as part of the locationallybounded ‘sticky’ assets discussed with the locationaladvantages in this paper. Informal institutions will notbe incorporated into the model due to the unavailabilityof data. Deregulation in host countries is a critical factoraffecting the location choices of foreign banks. Foreignbanks are found to favour locations with fewer restric-tions to the entry of foreign banking activities (NIGH

et al., 1986; FOCARELLI and POZZOLO, 2001;DOPICO and WILCOX, 2002; LENSINK and DE

HAAN, 2002; CLARKE et al., 2003; HERRERO andPERIA, 2007). NIGH et al. (1986) reported that thedirect investment of US foreign banks was affected bythe openness of developing countries to foreignbanking. GOLDBERG and GROSSE (1994) found thatforeign banks had a greater presence in US states withfewer regulations on foreign activities. DOPICO andWILCOX (2002) also found that foreign banks tend tohave a larger presence in countries that are more opento the foreign ownership of banks.

The Chinese government has gradually lifted its geo-graphical and product restrictions on foreign banks withrespect to the World Trade Organization (WTO) acces-sion agreements (see the next section). Foreign banksmay not always have full autonomy to establish theirbranches in ideal locations based on conventional own-ership, locational, and internalization advantages inChina. Foreign banks were actually under severe geo-graphical and product restrictions in China until asrecently as 2006, when they were granted full accessto the Chinese market as part of the WTO accord.Foreign banks established before WTO accession areexpected to prefer first-mover cities, while those setup since 2002 are less likely to confine themselves tothose financial centres. As the first-mover cities arelargely located in special economic zones with abundantmarket opportunities (where most foreign investors,especially those originating from Chinese-dominatedcommunities, are also located), it is estimated that anumber of foreign banking institutions have establishedtheir branches and sub-branches to provide (full)banking services to their clients. After the CBRCstarted to open up the local currency banking marketin the middle of the 1990s, some (risk-adverse)foreign banks may have established their representativeoffices in these regions to collect vital market infor-mation and to provide basic banking services to theircustomers. Based on all the above discussion, it isreasonable to deduce the following:

H5: Foreign banks tend to locate their branches and sub-branches

in first-mover cities to open up the banking sector and reap the

locational advantages created by the deregulation of the Chinese

banking industry.

H6: Foreign banks tend to locate their representative offices in

first-mover cities to open up local currency banking and reap the

locational advantages created by the deregulation of the Chinese

banking industry.

Locational Distribution of Foreign Banks in China 737

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

From the above discussion, the location choices offoreign banks could be a contest between the follow-the-competitor and -customer strategies and the insti-tutional environment created by the deregulation pol-icies in China. The following section models thelocation choices of foreign banks in China by using aconditional logit technique.

METHODOLOGY AND DATA SOURCES

Modelling the location distribution of foreign banks in China

In this study, the location choices of foreign banks will bemodelled as a conditional logit problem. The conditionallogit model (CLM) assumes that foreign banks evaluate allpossible city attributes and test individual location possi-bilities against a set of alternative locations. Foreignbanks choose cities with the highest expected profit.

Following MCFADDEN (1974), foreign bank i locat-ing in city j in year t will derive a profit pijt, which iscomposed of a deterministic and a stochastic term:

pijt = mijt + 1ijt (1)

where mijt and 1ijt are the deterministic and randomterms, respectively. Alternatively, j will be preferred byforeign bank i if:

pijt . pikt, k = j (2)

The stochastic nature of the profit function implies theprobability that city j is selected by bank i equals:

Pijt = Prob(pijt . pikt), k = j (3)

It is assumed that the expected profit from city j is afunction of the observable urban attributes and arandom disturbance term:

pijt = c + b′Xjt−1 + 1ijt (4)

where c is a constant; Xjt21 is a vector of the observablecity-specific attributes of city j in year t – 1; b is a vectorof the parameters to be estimated; and 1ijt is an error item.

Let Yit be a random variable that indicates the fact thatcity j has been chosen by bank i in year t, then the prob-ability of choosing a specific city j depends on the city’sattributes relative to the attributes of other cities inthe choice set in year t – 1.5 Following MCFADDEN

(1974), if the disturbance terms are independently dis-tributed and they follow a Weibull distribution, thenthe probability of locating in city j is given by:

Prob(Yi = j) = exp(b′Xjt−1)∑N

n=1

exp(b′Xjt−1)(5)

Each city chosen in this study is a location for foreignbanks. For each foreign banking institution, a value of

‘1’ is assigned to the chosen city and a zero for the othercities. This study includes cities that had allowed foreignbanks to conduct local currency business by 2006 andthose hosting foreign banking activities by 2006. Thereare thirty-two cities in the sample: Beijing, Changchun,Chengdu, Chongqing, Dalian, Dongguan, Fuzhou,Guangzhou, Harbin, Haikou, Hangzhou, Jinan,Kunming, Lanzhou, Nanjing, Nanning, Nantong,Ningbo, Qingdao, Shanghai, Shantou, Shenyang, Shenz-hen, Suzhou, Tianjin, Wuhan, Wuxi, Xiamen, Xi’an,Yantai, Yinchuan, and Zhuhai.

The conditional logit model (CLM) assumes theindependence of irrelevant alternative locationchoices. By grouping the alternatives into subgroupsthat allow the variance to differ across the groupswhile maintaining the independence of irrelevantalternative assumptions within the groups, the nestedlogit model (NLM) is one of the ways to relax thehomoscedasticity assumption in the CLM. The NLM,however, is not applicable in this case since eachparent bank may not choose the same set of cities forsubsequent investment, making the location choices offoreign banks not entirely independent. To control theinfluence of the interdependency of the previous andnew location choices of parent banks in China, thevariable OFB is introduced, that is, the number offoreign banking institutions (in the form of branches,sub-branches, or representative offices) established byparent banks with existing investment in Chinesecities in the previous year.

Other explanatory variables are derived from the sixresearch hypotheses outlined in the previous section,ranging from follow-the-competitor and -customer,business seeking, information seeking, first-movercities seeking, and local currency business seeking.To test the ‘follow-the-competitor’ hypothesis (H1),the location choices of foreign banks are quantifiedthrough the number of existing foreign bankinginstitutions established by parent banks withoutpre-existing investment in Chinese cities in the pre-vious year (NFB). The positive significance of NFBindicates that foreign banks follow their competitorsin China.

To test the ‘follow-the-customer’ hypothesis (H2), acity’s volume of international trade (TRADE) and therealized amount of foreign direct investment (FDI) areincluded. Ideally, a city’s trade value or the number offoreign enterprises from the same home country foreach foreign bank should be incorporated in thetesting of the ‘follow-the-customer’ hypothesis. Thedata are, however, not readably available in China. Asthe second best choice, some empirical studies applythe total volume of trade or total FDI to test thefollow-the-customer hypothesis. For instance, GOLD-

BERG and GROSSE (1994) and DOPICO and WILCOX

(2002) found that a country’s volume of internationaltrade with other countries is positively associated withthe entries of foreign banks. In China, there is evidence

738 Canfei He and Godfrey Yeung

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

showing that Hong Kong-based banks are highlyagglomerated in the Pearl River Delta, which is alsothe location of a large number of foreign-financedenterprises originating from Hong Kong (LEUNG,1993; YEUNG, 2009b). Similar agglomerations offoreign banks and foreign-financed enterprises originat-ing from Japan and the United States occur in Beijingand Shanghai (HE, 2003; CHENG and STOUGH,2006). In the context of China, the positive significanceof TRADE and FDI indicates that foreign banks followtheir customers in China.

The total banking deposits and loans (LOAN) areincluded to test the significance of local banking oppor-tunities (H3). To identify the potential impact of owner-ship advantages derived from the parent bank’s size onthe location choice of foreign banks, the data weredivided into two panels: the first group includes banksranked in the top 100 in terms of total assets; and thesecond includes banks ranked outside the top 100 interms of total assets.

Two dummy variables were used to test the signifi-cance of informational externalities for the locationchoices of foreign banks in China (H4). One standsfor the national financial centre in China (NFC),assigning a value of ‘1’ for Beijing and Shanghai,and zero for other cities. The other represents thelocations of regional branches of the central bank,the People’s Bank of China (PBC), assigning a valueof ‘1’ for Tianjin, Shenyang, Nanjing, Jinan, Wuhan,Guangzhou, Chengdu, and Xi’an, and zero for othercities.

To examine the potential influence of deregulationon foreign banking in China, two variables are intro-duced to reflect the significant changes to the insti-tutional environment of the Chinese banking industry.They are ACCESS and RMB: the number of years acity had allowed foreign banks to establish businessoperating entities, and to conduct renminbi business,respectively, when a foreign bank entered the city (H5

and H6). The explanatory variables are summarized inTable 1.

Data sources

Data on foreign banks are from the Almanac of China’sFinance and Banking 2007 (CHINA SOCIETY FOR

FINANCE & BANKING, 2007). Table 2 summarizes theprofiles of foreign banking institutions in China in2006. Foreign banks have established 548 banking insti-tutions in China, including 240 representative offices,207 branches, ninety sub-branches, and eleven headoffices (which are joint-venture banks in China). Thetop 100 banks had established 274 institutions by2006, accounting for 50% of the total. There are 162institutions set up by banks from the Great ChinaDiaspora, 237 from banks based in Europe and NorthAmerica, and 149 from other parts of Asia. Amongthe 548 foreign banking institutions, 303 wereestablished in the pre-WTO period and 245 in thepost-WTO period. Data on the explanatory variablescome from China Urban Statistical Yearbook 2007,China Statistical Yearbook 2007, and China Import andExport Statistical Yearbook 2006 (STATE STATISTICAL

BUREAU (SSB), 2007a, 2007b, 2007c). Informationon ACCESS and RMB is from Report on the Opening-Up of the Chinese Banking Sector (CBRC, 2007).

FOREIGN BANKING OPERATIONS

IN CHINA

Institutional changes for foreign banking operations

The opening up of the Chinese banking industry canbe divided into three stages: 1980–1993, 1994–2001,and 2002 to the present (CBRC, 2007). The firststage (1980–1993) was marked by the establishmentof the representative office of the Japan Import andExport bank in Beijing in 1979 (Fig. 1 and Table 3).The Nanyang Commercial Bank set up a branch inShenzhen in 1981, becoming the first foreign bank toconduct business in China since 1949. To open upfurther the once highly regulated banking market, in1985 the Chinese government promulgated Regulations

Table 1. Definitions and expected signs of explanatory variables

Variable Definition

Expected

sign

OFB Number of foreign banking institutions established by parent banks with existing investment in Chinese cities in the

previous year (‘old foreign banks’)

NFB Number of foreign banking institutions established by parent banks without investment in Chinese cities in the

previous year (‘new foreign banks’)

+

TRADE International trade volume in a Chinese city +FDI Realized amount of foreign direct investment in a Chinese city +LOAN Total banking deposits and loans in a Chinese city +ACCESS ‘First-mover cities’ – number of years for which foreign banks are allowed to establish business operating entities in a

Chinese city

+

RMB ‘Local currency banking’ – number of years for which foreign banks are allowed to conduct renminbi (yuan) business

in a Chinese city

+

NFC Dummy variable for the national financial centres of Beijing and Shanghai +PBC Dummy variable for cities hosting the nine regional branches of the People’s Bank of China +

Locational Distribution of Foreign Banks in China 739

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

on the Administration of Foreign-Funded Banks andChinese–Foreign Joint Venture Banks in Special EconomicZones (CBRC, 1985). These regulations allow foreignbanks to establish branches and conduct foreign cur-rency business in five special economic zones,namely: Shenzhen, Zhuhai, Shantou, Xiamen, andHainan. Facing strict geographical and customerrestrictions, foreign banks have tended to establishrepresentative offices to collect information and ident-ify possible investment opportunities in China. TheChinese government has progressively lifted the geo-graphical restrictions on foreign banks by allowingtheir presence in coastal cities beyond the special econ-omic zones. For instance, the state opened Shanghai toforeign banks in 1990, and another seven cities –Dalian, Tianjin, Qingdao, Nanjing, Ningbo, Fuzhouand Guangzhou – in 1992. Subsequently, moreforeign banks have established representative officesand branches in China.

Further relaxation of the geographical and productconstraints on foreign banks marked the second stage(1994–2001) of the banking reforms in China.Foreign banks, especially those based in the HongKong Special Administrative Region, Japan, theUnited States, the Netherlands, Germany, France, andThailand, entered the Chinese market in the early1990s (Fig. 1 and Table 4). This was consistent withthe growth pattern of foreign investment. In December1996, The Provisional Regulations on Foreign Banking Insti-tutions Renminbi Business on a Trial Basis in ShanghaiPudong Area was implemented by the CBRC (CBRC,1996). For the first time, the CBRC granted foreignbanks access to renminbi (local currency) business forforeign enterprises and overseas residents in China.Shenzhen was selected as the second pilot city to allowforeign banks to conduct renminbi business in 1998. Fur-thermore, foreign banks based in Shanghai and Shenz-hen have been allowed to conduct renminbi businesses

Fig. 1. Foreign banking institutions in China, 1980–2006Source: CHINA SOCIETY FOR FINANCE & BANKING (2007)

Table 2. Summary of foreign banking institutions, 2006

Entry timing Investing banks Country of origin

Institution Total

Pre-WTO

(1979–2001)

Post-WTO

(2002–2006)

Top 100

banks

Smaller

banks

Great China

Diaspora Asia

Europe and North

America

Representative office 240 142 98 82 158 33 85 122

Branch 207 139 68 129 78 72 53 82

Sub-branch 90 11 79 62 28 53 7 30

Head office 11 11 0 1 10 4 4 3

Total 548 303 245 274 274 162 149 237

Notes: The Great China Diaspora includes Hong Kong, Macau, Taiwan, and Singapore; Asia includes South Korea, Japan, and other South East

Asian countries.

WTO, World Trade Organization.

Source: Authors’ computation based on data from CHINA SOCIETY FOR FINANCE & BANKING (2007).

740 Canfei He and Godfrey Yeung

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

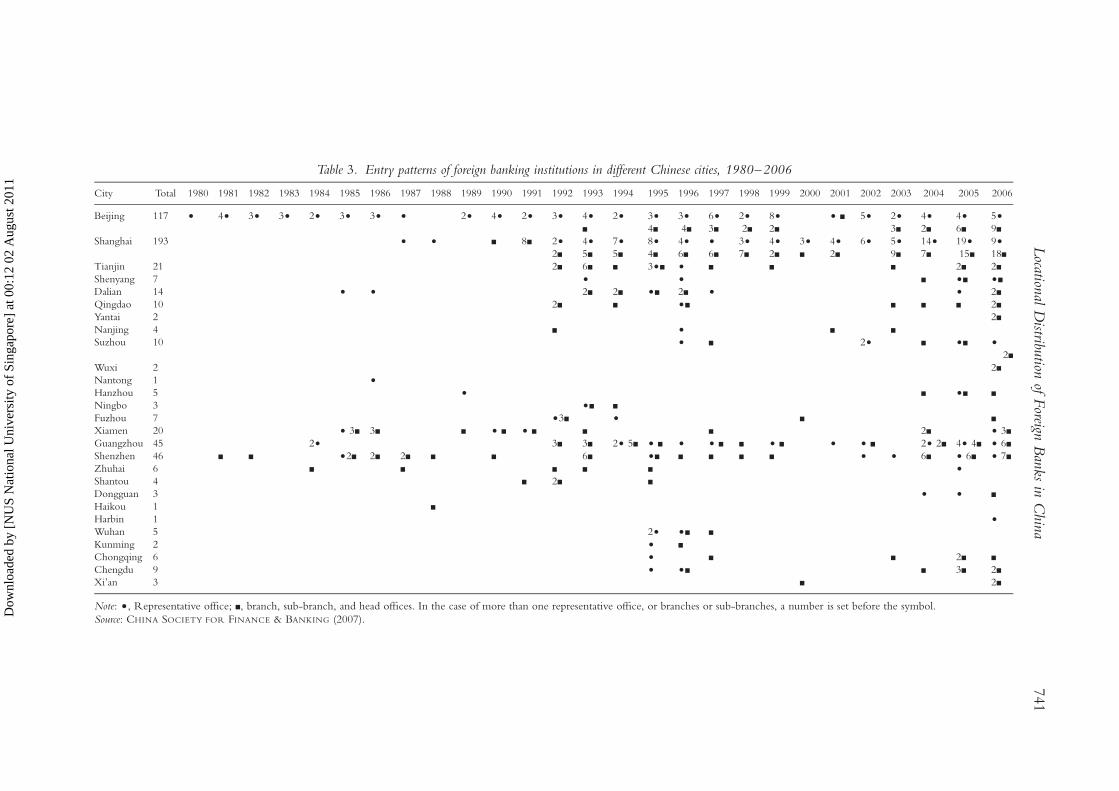

Table 3. Entry patterns of foreign banking institutions in different Chinese cities, 1980–2006

City Total 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Beijing 117 † 4† 3† 3† 2† 3† 3† † 2† 4† 2† 3† 4†

B

2† 3†

4B

3†

4B

6†

3B

2†

2B

8†

2B

† B 5† 2†

3B

4†

2B

4†

6B

5†

9B

Shanghai 193 † † B 8B 2†

2B

4†

5B

7†

5B

8†

4B

4†

6B

†

6B

3†

7B

4†

2B

3†

B

4†

2B

6† 5†

9B

14†

7B

19†

15B

9†

18B

Tianjin 21 2B 6B B 3†B † B B B 2B 2B

Shenyang 7 † † B †B †B

Dalian 14 † † 2B 2B †B 2B † † 2B

Qingdao 10 2B B †B B B B 2B

Yantai 2 2B

Nanjing 4 B † B B

Suzhou 10 † B 2† B †B †

2B

Wuxi 2 2B

Nantong 1 †

Hanzhou 5 † B †B B

Ningbo 3 †B B

Fuzhou 7 †3B † B B

Xiamen 20 † 3B 3B B † B † B B B 2B † 3B

Guangzhou 45 2† 3B 3B 2† 5B † B † † B B † B † † B 2† 2B 4† 4B † 6B

Shenzhen 46 B B †2B 2B 2B B B 6B †B B B B B † † 6B † 6B † 7B

Zhuhai 6 B B B B B †

Shantou 4 B 2B B

Dongguan 3 † † B

Haikou 1 B

Harbin 1 †

Wuhan 5 2† †B B

Kunming 2 † B

Chongqing 6 † B B 2B B

Chengdu 9 † †B B 3B 2B

Xi’an 3 B 2B

Note: †, Representative office; B, branch, sub-branch, and head offices. In the case of more than one representative office, or branches or sub-branches, a number is set before the symbol.

Source: CHINA SOCIETY FOR FINANCE & BANKING (2007).

Location

alD

istribution

ofForeign

Ban

ksin

Chin

a741

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

in their neighbouring provinces of Jiangsu, Zhejiang,Guangdong, Guangxi, and Hunan since 1999. Partlydue to the Asian financial crisis of 1997–1998, theselandmark regulations nonetheless only attracted theestablishment of fifteen new foreign banking institutionsin China between 1998 and 2001 (CBRC, 2007).

Accession to the WTO and the phased-in liberaliza-tion of access for foreign banking marked the thirdstage (2002 to the present) of foreign bank operationsin China. Following accession to the WTO in 2001,China amended or issued a series of laws and regulationsregarding foreign banking institutions during the five-year grace period allowed under the WTO accessionagreement (CBRC, 2007). Foreign banks in Shanghai,Shenzhen, Tianjin, and Dalian were allowed toconduct renminbi business, which was expanded toforeign banks located in Guangzhou, Zhuhai,Qingdao, Nanjing, and Wuhan in 2002 and to those inJinan, Fuzhou, Chengdu, and Chongqing in 2003.Meanwhile, foreign banks were permitted to undertakecorporate business in renminbi in these open cities. InDecember 2003, the CBRC issued Administrative RulesGoverning the Equity Investment in Chinese Financial Insti-tutions by Overseas Financial Institutions (CBRC, 2003),setting forth the qualification requirements for overseasinvestors with respect to their asset size, capital require-ment, and profit-earning capacity as well as the upperlimits of such equity investment. In 2004, another fivecities – Kunming, Beijing, Xiamen, Shenyang, andXi’an – allowed foreign banks to conduct renminbibusiness, which was further expanded to Shantou,Ningbo, Harbin, Changchun, Lanzhou, Yinchuan, andNanning in 2005. By December 2006, foreign bankshad been permitted to engage in a similar range of finan-cial services to those offered by Chinese banks and wereto be treated and regulated in the same way as domesticbanks. All non-prudential market access constraints onforeign banks that restricted the ownership, operations,and juridical forms of foreign banking institutions,including those on internal branches and licenses, werelifted by the CBRC. From 2007 onwards, foreignbanking operations in China entered a new stagewhereby all geographical and customer restrictions onforeign banks were eliminated (YEUNG, 2009a,2009b). The accession to the WTO further opened upthe Chinese banking industry to foreign investors, stimu-lating another expansion drive for foreign banking oper-ations in China (Fig. 1 and Tables 3 and 4).

Entry pattern and the location distribution of foreign banks in

China

Foreign banks in China have their headquarters in morethan forty-seven countries or regions, with HongKong, Japan, and the United States at the top of thelist (Table 4). There were 127 institutions from HongKong, eighty from Japan, and forty-nine from theUnited States, accounting for 47% of total foreign

banking institutions in China in 2006. South Koreaand Singapore are other important investors in theChinese banking industry. Cultural and geographicalproximity may have facilitated the entry of overseasChinese banks and other Asian banks. Foreign banksfrom Hong Kong, Singapore, Japan, and South Koreamay have followed their customers to invest in China.Although most developed countries have establishedtrade or investment linkages with China, these econom-ies are culturally and geographically distant from Chinaand companies based in these countries are likely tokeep their original bank–client relationships to savetransaction costs.

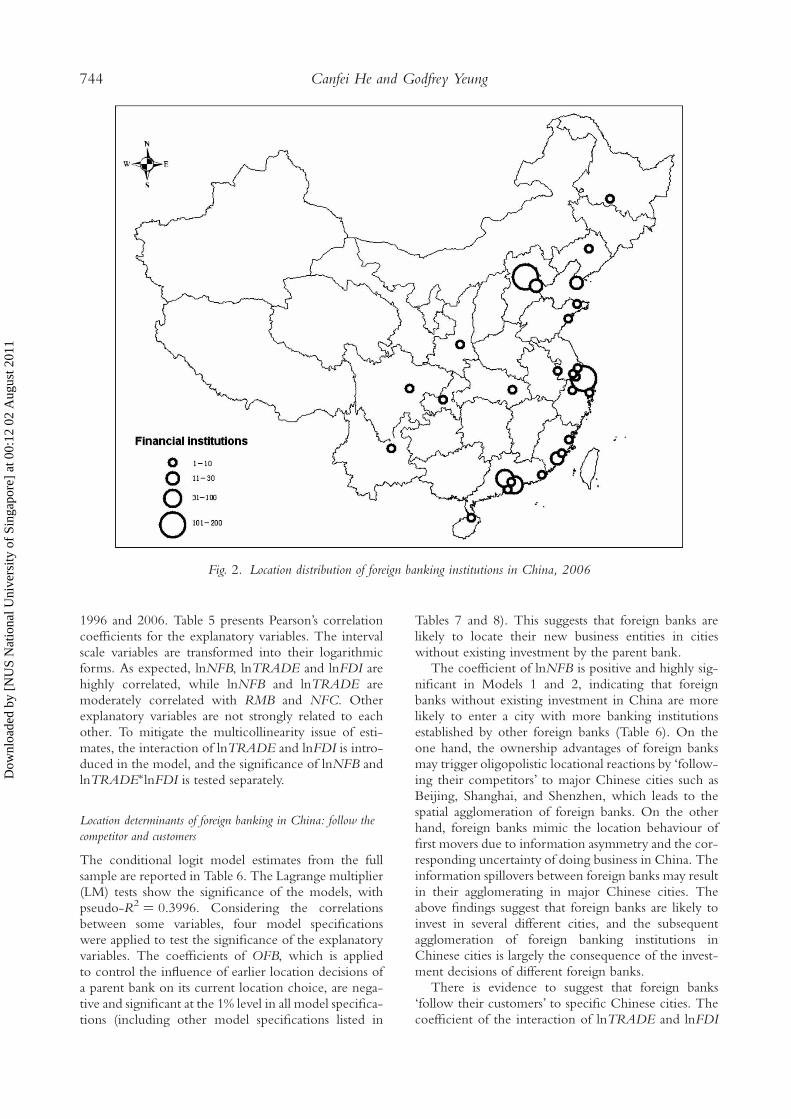

Foreign banking institutions are highly agglomeratedin selected Chinese cities. Shanghai and Beijing are thetwo most favoured locations due to a variety of loca-tional advantages, which may include the strategicnature of the banking market, information externalitiesand proximity to the central bank, and early openness toforeign banks (Fig. 2). Shenzhen and Guangzhou rankin the second tier of cities for attracting foreign banks,followed by Xiamen, Tianjin, Dalian, Qingdao, andSuzhou. Foreign banks have also targeted some inlandcities including Harbin, Xi’an, Chengdu, Chongqing,Kunming, and Wuhan. Foreign institutions set up bysmaller banks are largely concentrated in the economiccore areas in the coastal region, while those of the top100 banks are relatively dispersed, with more emphasison Beijing and Shanghai (Fig. 3). Many institutionsestablished by smaller banks are highly concentrated inShanghai, Beijing, Shenzhen, and Guangzhou.

The locational patterns of representative offices,branches, and sub-branches are different. Representa-tive offices, whose task is to collect information andseek business opportunities, are more concentrated inBeijing, Shanghai, and Guangzhou (Fig. 4). The twomajor headquarters of the People’s Bank of China(PBC) are located in Beijing and Shanghai; Guangzhouis the location of one of its nine regional headquarters.Foreign banks can benefit from informational external-ities by locating themselves close to the PBC. Branchesconducting foreign or local currency business are dis-persed along the developed coastal cities. Sub-branches,which are strongly attached to branches, are largelyagglomerated in the major cities such as Shanghai,Beijing, Tianjin, and Shenzhen. During the post-WTO period, the Yangtze River Delta has become afavoured region for foreign banks. Foreign banks inShanghai can serve the larger hinterland of theYangtze River Delta and its neighbouring regions.

EXPLANATION OF THE LOCATIONAL

DISTRIBUTION OF FOREIGN BANKING

IN CHINA

Due to the data available, the authors could only modelthe location choice of foreign banks in China between

742 Canfei He and Godfrey Yeung

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

Table 4. Entry pattern of foreign banking institutions into China, 1980–2006

City Total 1980 1981 1982 1983 1984 1985 1986 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Hong Kong 127 B B †2B 2B B †B 3B 2B †7B †10B 2†B 2†3B 2†2B 4B 3†2B †2B B 5B 3†11B 3†14B 32B

Japan 80 † † 3† †B †B †B † †2B †3B 2† 5†2B 9†4B 4†2B †B † B 2† 3† 6†3B 7†2B 2†4B

United States 49 B †B B † 2B 2† 2†2B † 2B †3B †2B 2B † 2† †B †B 3†6B 3†5B

UK 31 † B †B B † B 2B † † †B B 2† B 2†7B 5B

South Korea 27 2† B 2B 2B 2B B B † 4B †2B 6B 2B

Germany 25 † † † B †2B 2† †B 2† †3B † † † 2B 3B

France 25 † †B B 3B 2B 2B B 2†2B †B †B B 2† †B

Singapore 20 B 2B 3B B 2†B 2B B †B 2B 3B

Netherlands 19 † B †B 2†B † 2B B B 3B 4B

Italy 18 † † † 3† † B †B † B 2† 3† †

India 11 † 2† 2†B 4†B

Canada 10 † † 2B B B † † 2B

Switzerland 10 † B † † † B 3† †

Thailand 9 B B 3† 2B B B

Spain 8 † † † † 3† †

Australia 7 † † 2B † † †

Taiwan 15 B B † 8† †B B B

Belgium 6 † B 2B B B

Russia 6 † † † † 2†

Sweden 6 † † † † 2B

Philippines 5 †B † B B

Notes: †, Representative office; B, branch, sub-branch and head office. In the case of more than one representative office, or branches or sub-branches, a number is set before the symbol.

Only foreign banks with five or more institutions established in China by 2006 are included.

Source: CHINA SOCIETY FOR FINANCE & BANKING (2007).

Location

alD

istribution

ofForeign

Ban

ksin

Chin

a743

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

1996 and 2006. Table 5 presents Pearson’s correlationcoefficients for the explanatory variables. The intervalscale variables are transformed into their logarithmicforms. As expected, lnNFB, lnTRADE and lnFDI arehighly correlated, while lnNFB and lnTRADE aremoderately correlated with RMB and NFC. Otherexplanatory variables are not strongly related to eachother. To mitigate the multicollinearity issue of esti-mates, the interaction of lnTRADE and lnFDI is intro-duced in the model, and the significance of lnNFB andlnTRADE∗lnFDI is tested separately.

Location determinants of foreign banking in China: follow the

competitor and customers

The conditional logit model estimates from the fullsample are reported in Table 6. The Lagrange multiplier(LM) tests show the significance of the models, withpseudo-R2 ¼ 0.3996. Considering the correlationsbetween some variables, four model specificationswere applied to test the significance of the explanatoryvariables. The coefficients of OFB, which is appliedto control the influence of earlier location decisions ofa parent bank on its current location choice, are nega-tive and significant at the 1% level in all model specifica-tions (including other model specifications listed in

Tables 7 and 8). This suggests that foreign banks arelikely to locate their new business entities in citieswithout existing investment by the parent bank.

The coefficient of lnNFB is positive and highly sig-nificant in Models 1 and 2, indicating that foreignbanks without existing investment in China are morelikely to enter a city with more banking institutionsestablished by other foreign banks (Table 6). On theone hand, the ownership advantages of foreign banksmay trigger oligopolistic locational reactions by ‘follow-ing their competitors’ to major Chinese cities such asBeijing, Shanghai, and Shenzhen, which leads to thespatial agglomeration of foreign banks. On the otherhand, foreign banks mimic the location behaviour offirst movers due to information asymmetry and the cor-responding uncertainty of doing business in China. Theinformation spillovers between foreign banks may resultin their agglomerating in major Chinese cities. Theabove findings suggest that foreign banks are likely toinvest in several different cities, and the subsequentagglomeration of foreign banking institutions inChinese cities is largely the consequence of the invest-ment decisions of different foreign banks.

There is evidence to suggest that foreign banks‘follow their customers’ to specific Chinese cities. Thecoefficient of the interaction of lnTRADE and lnFDI

Fig. 2. Location distribution of foreign banking institutions in China, 2006

744 Canfei He and Godfrey Yeung

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

Fig. 3. Location distribution of foreign banking institutions established by the top 100 banks (a) and smaller banks (b)

Locational Distribution of Foreign Banks in China 745

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

Fig. 4. Location distribution of representative offices (a), branches (b), and sub-branches (c) in China, 2006

746 Canfei He and Godfrey Yeung

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

is positive and highly significant in Models 1 and 3,implying that foreign banks are inclined to set upbases in cities with a large volume of internationaltrade or had inflows of utilized FDI in previous years(Table 6). Foreign companies involved in internationaltrade or investment in China are potential customersfor foreign banks. China has been the major destinationfor FDI and the top international traders since the early1990s, second only to the United States and Japan inrecent years. Foreign banks have the incentive to main-tain the established business–client linkages with theirhome countries’ companies with extensive trade andinvestment in China.

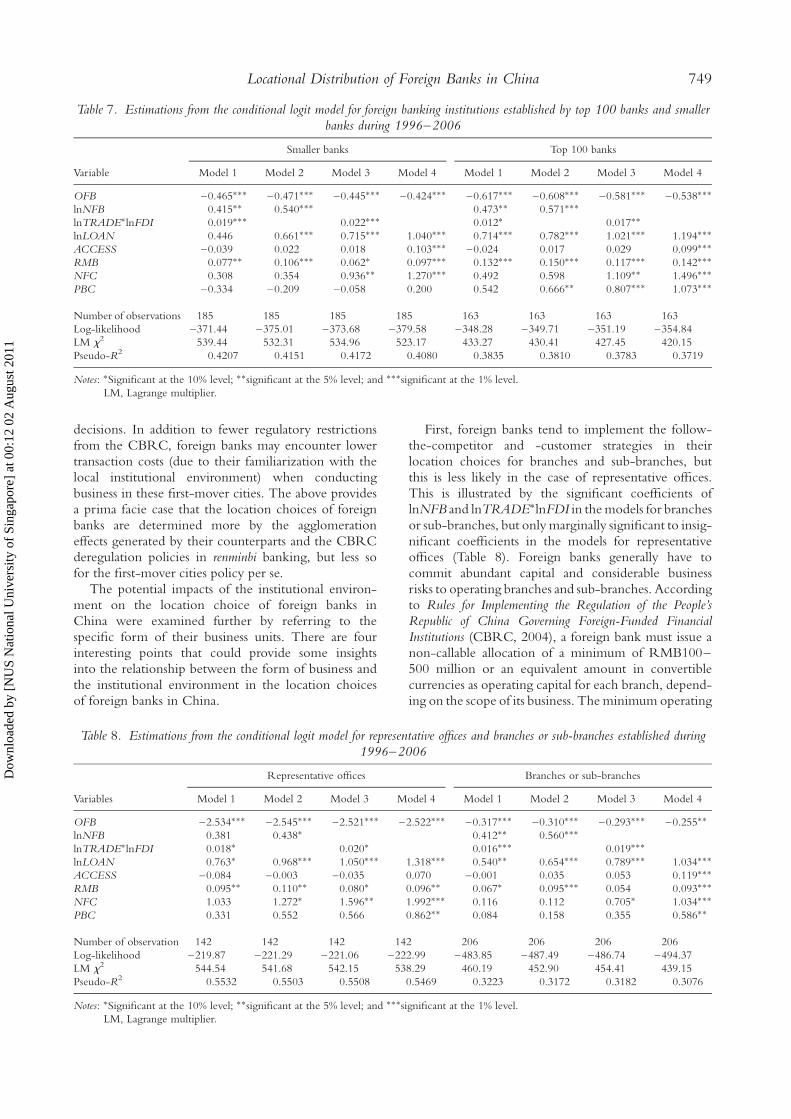

The impact of ownership advantages derived fromthe size of banks on location choices are reported inTable 7. All OFB and lnNFB coefficients are significantat the 1% level and at higher values in the models ofthe top 100 banks than those of the smaller banks.With significant ownership advantages, larger foreignbanks are more likely to choose different cities to setup establishments for their sequential investment inChina. They are also more likely to follow theirmajor competitors in their location choices, probablydue to the oligopolistic locational reactions. Smallerforeign banks are more likely to ‘follow their custo-mers’ to Chinese cities, which is illustrated by the

more significant and larger coefficient value of lnTRA-DE∗lnFDI in the models for smaller banks. By main-taining the existing business–client ties developed intheir home countries, smaller banks may benefit fromownership and internalization advantages in hostcountries. Thus, the hypotheses that larger banks usethe ‘follow-the-competitor’ strategy (H1) and smallerbanks use the ‘follow-the-customer’ strategy (H2) aresupported.

Beyond the follow-the-competitor and -customerstrategies, foreign banks also pursue local bankingopportunities. Foreign banks are more likely to entercities with larger total banking deposits and loans, asindicated by the positive and highly significant co-efficients of lnLOAN in all model specifications(Table 6). Higher volumes of deposits and loans in acity indicate a larger potential banking market andmore profit-making opportunities for foreign banks.Other foreign banks may mimic the location distri-bution of their counterparts, resulting in furtherspatial agglomeration of foreign banks. The highly sig-nificant positive coefficients of lnLOAN in all fourmodels for the top 100 banks further illustrate thatlarger banks are more likely to set up in cities with abun-dant local banking opportunities (Table 7). Larger bankspossess significant ownership advantages and have the

Fig. 4. Continued

Locational Distribution of Foreign Banks in China 747

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

capital to explore and compete with the long-estab-lished domestic state-owned banks in China. They arewilling to invest in areas as long as their investment isjustified by potential banking opportunities. Thus, thethird hypothesis of the business-seeking strategy bylarger foreign banks (H3) is accepted. The above find-ings are comparable with the hypotheses outlined byENGWALL and WALLENSTAL (1998) and WILLIAMS

(1997, 2002) on the banking industry.Moreover, the statistical results may provide partial

support for the argument concerning the informationaladvantages for foreign banks. The national and regionalfinancial centres in China are attractive locations forforeign banks when the agglomeration effects ofbanking institutions (follow the competitor and custo-mer) are disregarded. Both coefficients of NFC andPBC are positive and highly significant in Model 4,but insignificant in Model 1 when lnNFB andlnTRADE∗lnFDI are included (Tables 6 and 7). Thegeographical proximity to China’s central bank allowsforeign banks to have easy access to the decision-makers about financial policy and establish local businessnetworks. The informational externalities can signifi-cantly moderate the business risks encountered byforeign banks. Meanwhile, foreign banks may benefit

from the information spillovers derived from theagglomerations of foreign banks in the financialcentres and this could be the reason for the insignificantcoefficients in Model 1.

Formal institutional environment and locations of foreign banks

The gradual deregulation policies implemented by theCBRC may influence the location choices of foreignbanks in China. The institutional variable of ACCESSis significant at the 1% level and positive in Model 4when the influence of following their competitors andcustomers (lnNFB and lnTRADE∗lnFDI) are not con-sidered (Tables 6 and 7). This rather unexpected resultimplies that the location choice of foreign banks ismore determined by the agglomeration effects gener-ated by their counterparts than the CBRC’s policieson first-mover cities for foreign banks. Before a con-clusion on this crucial point is drawn, one should havea closer look at the coefficients in the other modelspecifications. The coefficients of RMB are expectedlysignificant at the 1% level in all model specifications(with the sole exception of Model 3 in smaller banks),implying that foreign banks are likely to pursue a localcurrency business-seeking strategy in their location

Table 5. Correlation coefficients among explanatory variables

OFB lnNFB lnTRADE lnFDI lnLOAN ACCESS RMB NFC PBC

OFB 1.00

lnNFB 0.44 1.00

lnTRADE 0.39 0.73 1.00

lnFDI 0.31 0.60 0.79 1.00

lnLOAN 0.33 0.48 0.59 0.53 1.00

ACCESS 0.22 0.38 0.60 0.43 0.29 1.00

RMB 0.47 0.53 0.59 0.46 0.53 0.46 1.00

NFC 0.38 0.61 0.37 0.35 0.46 0.07 0.33 1.00

PBC 0.02 0.07 0.00 0.15 0.13 –0.23 0.12 –0.15 1.00

Table 6. Estimations from the conditional logit model for foreign banking institutions established during 1996–2006

Foreign banking institution

Variable Model 1 Model 2 Model 3 Model 4

OFB –0.524∗∗∗ –0.517∗∗∗ –0.494∗∗∗ –0.456∗∗∗

lnNFB 0.439∗∗∗ 0.553∗∗∗

lnTRADE∗lnFDI 0.015∗∗∗ 0.019∗∗∗

lnLOAN 0.574∗∗∗ 0.705∗∗∗ 0.857∗∗∗ 1.097∗∗∗

ACCESS –0.029 0.020 0.025 0.102∗∗∗

RMB 0.098∗∗∗ 0.121∗∗∗ 0.083∗∗∗ 0.112∗∗∗

NFC 0.384 0.446 1.001∗∗∗ 1.372∗∗∗

PBC 0.125 0.251 0.397∗ 0.658∗∗∗

Number of observation 348 348 348 348

Log-likelihood –724.16 –728.85 –729.20 –738.46

LM x2 963.83 954.44 953.76 935.23

Pseudo-R2 0.3996 0.3957 0.3954 0.3877

Notes:∗Significant at the 10% level; ∗∗significant at the 5% level; and ∗∗∗significant at the 1% level.

LM, Lagrange multiplier.

748 Canfei He and Godfrey Yeung

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

decisions. In addition to fewer regulatory restrictionsfrom the CBRC, foreign banks may encounter lowertransaction costs (due to their familiarization with thelocal institutional environment) when conductingbusiness in these first-mover cities. The above providesa prima facie case that the location choices of foreignbanks are determined more by the agglomerationeffects generated by their counterparts and the CBRCderegulation policies in renminbi banking, but less sofor the first-mover cities policy per se.

The potential impacts of the institutional environ-ment on the location choice of foreign banks inChina were examined further by referring to thespecific form of their business units. There are fourinteresting points that could provide some insightsinto the relationship between the form of business andthe institutional environment in the location choicesof foreign banks in China.

First, foreign banks tend to implement the follow-the-competitor and -customer strategies in theirlocation choices for branches and sub-branches, butthis is less likely in the case of representative offices.This is illustrated by the significant coefficients oflnNFB and lnTRADE∗lnFDI in the models for branchesor sub-branches, but only marginally significant to insig-nificant coefficients in the models for representativeoffices (Table 8). Foreign banks generally have tocommit abundant capital and considerable businessrisks to operating branches and sub-branches. Accordingto Rules for Implementing the Regulation of the People’sRepublic of China Governing Foreign-Funded FinancialInstitutions (CBRC, 2004), a foreign bank must issue anon-callable allocation of a minimum of RMB100–500 million or an equivalent amount in convertiblecurrencies as operating capital for each branch, depend-ing on the scope of its business. The minimum operating

Table 8. Estimations from the conditional logit model for representative offices and branches or sub-branches established during1996–2006

Representative offices Branches or sub-branches

Variables Model 1 Model 2 Model 3 Model 4 Model 1 Model 2 Model 3 Model 4

OFB –2.534∗∗∗ –2.545∗∗∗ –2.521∗∗∗ –2.522∗∗∗ –0.317∗∗∗ –0.310∗∗∗ –0.293∗∗∗ –0.255∗∗

lnNFB 0.381 0.438∗ 0.412∗∗ 0.560∗∗∗

lnTRADE∗lnFDI 0.018∗ 0.020∗ 0.016∗∗∗ 0.019∗∗∗

lnLOAN 0.763∗ 0.968∗∗∗ 1.050∗∗∗ 1.318∗∗∗ 0.540∗∗ 0.654∗∗∗ 0.789∗∗∗ 1.034∗∗∗

ACCESS –0.084 –0.003 –0.035 0.070 –0.001 0.035 0.053 0.119∗∗∗

RMB 0.095∗∗ 0.110∗∗ 0.080∗ 0.096∗∗ 0.067∗ 0.095∗∗∗ 0.054 0.093∗∗∗

NFC 1.033 1.272∗ 1.596∗∗ 1.992∗∗∗ 0.116 0.112 0.705∗ 1.034∗∗∗

PBC 0.331 0.552 0.566 0.862∗∗ 0.084 0.158 0.355 0.586∗∗

Number of observation 142 142 142 142 206 206 206 206

Log-likelihood –219.87 –221.29 –221.06 –222.99 –483.85 –487.49 –486.74 –494.37

LM x2 544.54 541.68 542.15 538.29 460.19 452.90 454.41 439.15

Pseudo-R2 0.5532 0.5503 0.5508 0.5469 0.3223 0.3172 0.3182 0.3076

Notes: ∗Significant at the 10% level; ∗∗significant at the 5% level; and ∗∗∗significant at the 1% level.

LM, Lagrange multiplier.

Table 7. Estimations from the conditional logit model for foreign banking institutions established by top 100 banks and smallerbanks during 1996–2006

Smaller banks Top 100 banks

Variable Model 1 Model 2 Model 3 Model 4 Model 1 Model 2 Model 3 Model 4

OFB –0.465∗∗∗ –0.471∗∗∗ –0.445∗∗∗ –0.424∗∗∗ –0.617∗∗∗ –0.608∗∗∗ –0.581∗∗∗ –0.538∗∗∗

lnNFB 0.415∗∗ 0.540∗∗∗ 0.473∗∗ 0.571∗∗∗

lnTRADE∗lnFDI 0.019∗∗∗ 0.022∗∗∗ 0.012∗ 0.017∗∗

lnLOAN 0.446 0.661∗∗∗ 0.715∗∗∗ 1.040∗∗∗ 0.714∗∗∗ 0.782∗∗∗ 1.021∗∗∗ 1.194∗∗∗

ACCESS –0.039 0.022 0.018 0.103∗∗∗ –0.024 0.017 0.029 0.099∗∗∗

RMB 0.077∗∗ 0.106∗∗∗ 0.062∗ 0.097∗∗∗ 0.132∗∗∗ 0.150∗∗∗ 0.117∗∗∗ 0.142∗∗∗

NFC 0.308 0.354 0.936∗∗ 1.270∗∗∗ 0.492 0.598 1.109∗∗ 1.496∗∗∗

PBC –0.334 –0.209 –0.058 0.200 0.542 0.666∗∗ 0.807∗∗∗ 1.073∗∗∗

Number of observations 185 185 185 185 163 163 163 163

Log-likelihood –371.44 –375.01 –373.68 –379.58 –348.28 –349.71 –351.19 –354.84

LM x2 539.44 532.31 534.96 523.17 433.27 430.41 427.45 420.15

Pseudo-R2 0.4207 0.4151 0.4172 0.4080 0.3835 0.3810 0.3783 0.3719

Notes: ∗Significant at the 10% level; ∗∗significant at the 5% level; and ∗∗∗significant at the 1% level.

LM, Lagrange multiplier.

Locational Distribution of Foreign Banks in China 749

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

capital for a branch was reduced to RMB100 million bythe CBRC in 2006 (but a foreign bank must have main-tained a representative office in China for at least twoyears before being allowed to apply to set up a branch),according to Regulations of the People’s Republic of Chinaon Administration of Foreign-Funded Banks (CBRC,2006). In addition to following their customers andlocating in cities with plenty of banking opportunities,it is logical for foreign banks to mimic the locationchoices of their major competitors to offset unnecessarybusiness risks in an environment of asymmetrical infor-mation. The third hypothesis of the business-seekingstrategy of branches and sub-branches (H3) is thusaccepted.

Second, foreign banks are likely to pursue informa-tional externalities in their location choice for represen-tative offices. This is illustrated by the positive,significant, and larger coefficients of both NFC andPBC in Model 4 for representative offices when theeffects of following the competitor and customer arenot considered (Table 8). As mentioned previously,representative offices aim to collect information andprovide advisory services to foreign enterprises inChina. It is logical for foreign banks to locate theirrepresentative offices in major financial centres to reapthe informational advantages of being spatially close tothe headquarters of China’s central and domestic com-mercial banks. The fourth hypothesis of the infor-mation-seeking strategy of representative offices (H4)is thus accepted. This finding enhances the existing lit-erature, such as MAGRI et al. (2005), by specifying thedeterminants of the different business forms foreignbanks take.

Third, foreign banks are more likely to open repre-sentative offices in cities which allow them to conductrenminbi business, while they tend to locate theirbranches or sub-branches in first-mover cities openedup to foreign banking services. The coefficients forRMB are significant in all of the representative officemodels (especially Model 1), while the coefficient forACCESS is positive and highly significant only inModel 4 for branches and sub-branches when theeffects of follow the competitor and customer are disre-garded (Table 8). This finding could be partiallyexplained by the fact that the location of foreignbanks and their provision of banking services to localcurrency businesses are largely determined by therestrictions stipulated by the CBRC in a relativelysmall number of open cities. This is especially the casebefore China’s WTO accession when foreign banks inthe Shenzhen special economic zone were onlyallowed to conduct renminbi business in 1998. Thesixth hypothesis of local currency business-seeking byrepresentative offices (H6) could be accepted.

Fourth, it appears that the agglomerating effect ofbanking institutions again has a larger impact on thelocation choice of foreign banks than the institutionalvariable of first-mover cities (Table 8). The coefficient

of ACCESS is only significant in Model 4 for branchesand sub-branches when follow-the-competitor and-customer (lnNFB and lnTRADE∗lnFDI) variablesare not considered. This provides further evidencethat the agglomeration effect is more important as adeterminant of the choice of location than first-moveradvantages for foreign banks in China. One possibleexplanation is that foreign banks in China use theagglomeration economies and the affiliated informa-tional externalities to mitigate their business risks inChina. The availability of skilled labour and externaleconomies through product and market informationin major cities are vital for the Marshallian typeof spatial concentration of specialized industries(KRUGMAN, 1991a). Proximity to banks allowsbankers to conduct brief but frequent face-to-face com-munication, and this could facilitate the exchange ofvital information concerning the newly implementedbanking regulations by the CBRC (also TORRE,2008). This explanation is consistent with the prop-osition that agglomeration could develop as a result offirms pursuing informational externalities (WOOD andPARR, 2005; VICENTE and SUIRE, 2007).

Nonetheless, one has to be aware of the potential pit-falls of this strong argument, partly due to the limit-ations of the selected institutional variables. The twomajor variables for the institutional environment aregeographically based: cities opened to foreign bankingbusinesses in the case of ACCESS and cities openedto local currency banking in the case of RMB. TheCBRC’s deregulation policies could have a biggerimpact on the scale and pace of foreign bank investmentand the variety of banking products than the locationchoices of foreign banks alone. This is especially thecase since the late 1990s, when most coastal citieswere already opened up to foreign banks.

Foreign banks are profit oriented and thus tend toselect coastal cities already open to foreign banks (first-mover advantages), which are also those areas withmore banking opportunities. Foreign banks aim topenetrate and conquer the lucrative segments of the(urban) banking market rather than ‘race to thebottom of the pile’ with the state-owned banks andrural credit cooperatives in the vast but razor-thinprofit-margin banking market in rural areas. Instead ofaiming for the blanket coverage of banking servicesover the whole country geographically, foreign banksstrategically target the highly lucrative market ofprivate banking business in China, which has anaverage profit rate ten times higher than that of the Euro-pean and American retail banking businesses. It is esti-mated that the number of households with more thanUS$1 million in liquid assets in China had increasedfrom 124 000 in 2001 to 310 000 by the end of 2006.It is expected that this number will double by the year2011. Foreign banks realize that they are able toprovide more sophisticated personal banking productsthan Chinese banks to the new middle classes and

750 Canfei He and Godfrey Yeung

Dow

nloa

ded

by [

NU

S N

atio

nal U

nive

rsity

of

Sing

apor

e] a

t 00:

12 0

2 A

ugus

t 201

1

entrepreneurs (who are service rather than price elastic)in the first-mover cities, even though publicly listedstate-owned commercial banks are aggressively improv-ing their services (YEUNG, 2009a). The concentration offoreign banks in these first-mover cities creates anagglomeration effect over time and this could offsetthe sensitivity of the geographically based institutionalvariables used in this paper. Based on the above discus-sion, the fifth hypothesis of first-mover city-seeking bybranches of foreign banks (H5) can only be partiallyaccepted.

If the above arguments hold any water, the two loca-tionally based variables, especially the first-mover citiesvariables (ACCESS), for institutional environments aresurely unable to reveal the full impact of the deregula-tion of banking product provisions – such as QualifiedForeign Institution Investors (QFII), which allowsforeign financial institutes to invest in local currencyand local securities markets – on the location choiceof foreign banks. It is unfortunate that the authors areunable to identify a reliable data set to examine thisproposition further. This could be an important areafor further research.

DISCUSSION AND SUMMARY

This paper aims to contribute to the existing literatureby examining two major propositions concerning thelocation choices of foreign banks based on their differ-ent business forms and bank assets in a major transitionaleconomy, that of China. In addition to the following-the-competitor and -customer proposition derivedfrom Dunning’s eclectic paradigm (GRAY and GRAY,1981; PETROU, 2007), two institutional variables wereintroduced in the form of first-mover cities and localcurrency banking to examine the potential impacts ofthe liberalization policies implemented by the regulat-ory authority – the China Banking Regulatory Com-mission (CBRC) – on the location choices foreignbanks make in China. The data set was also dividedinto two panels to identify the potential differencesbetween business forms (branches and sub-branchesversus representative offices) and bank assets (smallbanks versus large banks) to test the six research hypoth-eses, that choices are determined by: following compe-titors and customers, business seeking, informationseeking, first-mover cities seeking, and local currencybusiness seeking.

There is strong evidence from the conditional logitregression models to suggest that different types offoreign banking institutions display distinct locationpatterns. Smaller foreign banks (partly due to lowerownership advantages) tend to pursue a ‘follow-the-customer’ strategy to lower investment risks and main-tain business–client networks in their choice ofChinese cities. Large foreign banks have ownershipadvantages and tend to mimic the location choices of

their major competitors and select cities with largepotential banking opportunities. To collect vital andup-to-date information, foreign banks tend to locatetheir representative offices in Beijing and Shanghaiwith their informational externalities, or other first-mover cities (initially special economic zones) to openup local currency banking and reap the locationaladvantages created by the deregulation of the Chinesebanking industry. These findings are not only compar-able with the general hypotheses outlined in the existingliterature (such as ENGWALL and WALLENSTAL, 1998;WILLIAMS, 1997, 2002; and MAGRI et al., 2005), butalso improve on them by specifying the determinantsof different business forms and the size of foreign banks.

As a transitional economy, China has graduallyrelaxed its geographical and customer restrictions onforeign banking operations. Right after the open-doorpolicy, China allowed foreign banks to set up represen-tative offices in Beijing, and later allowed foreign banksto establish business operations in special economiczones and other coastal cities. Progressively, the geo-graphical restrictions on foreign banks were fullylifted. Since 1996, the Chinese government hasallowed foreign banks in Shanghai to conduct renminbibusiness, and this was expanded to twenty-five citiesby November 2006. Foreign banks were guaranteedphased access to the Chinese market with the elimin-ation of all restrictions on their business activities bythe end of 2006. A significant institutional impact onthe location choices of foreign banks in China isexpected.