the litigation environment of a firm and its impact on ... litigation environment of a firm and its...

TRANSCRIPT

The Litigation Environment of a Firm and its Impacton Financial Policy∗

Alan D. Crane†

April 6, 2009

∗I would like to thank seminar participants at the University of Texas Austin. I would also liketo acknowledge financial support from the Dora Bonham Memorial Fund. All errors are my own.

†Graduate Student, Department of Finance, McCombs School of Business, The Uni-versity of Texas at Austin, 1 University Station B6600, Austin, TX, 78712; email:[email protected]

Abstract

Several studies have documented the impact of litigation on shareholders. Lawsuits can havesignificant explicit costs and have been shown to cause negative stock price reactions whenfiled. However, little is known about how firm managers respond to this costly reality. Anec-dotal evidence suggests firms may adjust financial policy to build a war chest in anticipationof litigation. Alternatively, firms may increase the probability of bankruptcy to reduce thepayoffs to potential litigants and protect shareholder assets. By looking at changes to afirm’s litigation environment, I test whether and how a firm’s risk of litigation impacts itsoverall financial policy. I find that higher litigation exposure leads firms to choose higherleverage. I show that this leverage increase is brought on by an active decision to repurchaseshares. These repurchases appear to be financed with a combination of excess cash andshort term debt as they coincide with a significant decrease in cash holdings and an increasein short term liabilities. Furthermore, these results appear to be stronger in firms that arefinancially distressed and face a higher chance of bankruptcy due to litigation. I show thatthese findings are not the result of changes in an industry equilibrium brought about bythe financial distress of other sued firms, but rather a strategic response to an increase inlitigation risk. These results are consistent with the idea that firms strategically take actionin the face of increased litigation risk to shield their assets from potential fees, judgements,and settlements due to litigation.

1 Introduction

Litigation exposure is an undeniable reality for firms in today’s marketplace. Blockbuster

product liability suits against large corporations frequently make headlines in the news media

and tort reform is a common political talking point. A firm exposed to major civil litigation

can find itself spending millions in legal fees, settlements, and/or judgements. In extreme

cases, large judgments have the potential to force firms into bankruptcy. It is reasonable to

assume that, in equilibrium, a firm’s management takes this risk of litigation into account

in developing operational and financial strategies. In this paper, I examine how firms react

when the legal environment changes. Specifically, I examine whether managers alter financial

policy to shield assets in the face of increased litigation risk.

There are several ways in which firms could use financial policy when considering litigation

exposure. Anecdotal evidence suggests that some firms may increase their cash holdings

(potentially through a reduction in dividends and/or investment) in order to build a “war

chest” to defend against civil litigation.1 Alternatively, firms may choose to increase the use

of debt. As Spier and Sykes (1998) point out, a firm’s capital structure can play an important

role in the bargaining process related to civil litigation if there is a positive probability

that a civil judgment will force the firm into bankruptcy. They show that a firm can use

both secured and unsecured debt to reduce the value of civil claims against the firm. This

finding is due generally to the fact that the civil litigants have a junior claim in bankruptcy.

Strategic financial policy can therefore reduce the cost of litigation borne ultimately by the

shareholders by reducing settlement amounts (which may, ex-ante, reduce the probability of

litigation by reducing the potential payoff to litigants.)

The difficulty in determining whether (or how) firms use financial policy to mitigate exposure

1See for example “Merck & Co Inc - Merck Finally to Answer for VIOXX Injuries”, Market News Pub-lishing, November 9, 2006.

1

to the costs associated with litigation is that the probability that a firm is sued may be related

to the overall financial policy decisions of the firm. There are several reasons why this may be

true. Poor firm performance generally may increase the probability of a lawsuit (for example

if product quality suffers due to cost cutting measures). This same poor performance may

also have a significant impact on the financial policy decisions of the firm. In other cases, the

financial policy decisions of the firm may actually be the cause of the litigation (securities

class-action for example). In either case, this endogeneity with respect to financial policy and

the risk of litigation makes it difficult to study how firms respond specifically to litigation

risk.

In order to mitigate this problem, I take advantage of exogenous variation in the probability

of litigation by proxying for litigation exposure using the number of litigation events within

that firm’s industry over time. Put simply, industry trends in litigation may tell us about the

risk of a lawsuit that a given firm faces even though those industry trends are unrelated to the

specific financial policy decisions of a particular firm. For example, a product liability suit

against firm A may signal a shift in the litigation environment. Due to legal trends, judicial

precedent, or even the success of plaintiffs attorneys, this lawsuit may increase the probability

that firm B is ultimately sued, even though the lawsuit against firm A is independent of firm

B’s financial policy or performance. Using this basic idea and data on actual litigation, I

construct a proxy for exogenous changes in the probability of a lawsuit for each firm through

time and use this measure to test whether (and how) firms respond to changes in their

litigation environment. I validate this proxy by showing that it is significantly related to the

probability that a firm is actually sued.

Using this measure, I test if and how financial policy is impacted by the litigation envi-

ronment. My results indicate that, in periods with a higher risk of litigation, firms choose

higher leverage. I show that this is not a passive result due to firm performance, but rather

an active decision by managers. These firms buy back significantly more shares of common

2

stock when the risk of litigation is high. I show that these share repurchases appear to

be financed with cash holdings and an increase in short-term liabilities. These findings are

consistent with firms increasing the use of debt in order increase bargaining power in the

settlement process and to shield assets from litigants. Finally, I show that these results are

stronger for those firms that are likely to be financially distressed - a result consistent with

the idea that this strategy is effective only when there is a non zero probability that a given

lawsuit will force the firm into bankruptcy. I find no support for the idea that firms may

actually reduce leverage and/or hoard cash in order to build a “war chest” to defend against

litigation.

This paper contributes to the literature in two primary ways. First, it adds to our under-

standing of the litigation process. Prior research has demonstrated the negative impact of

litigation on common shareholders, who ultimately bear the cost of litigation settlements and

judgments.2 This work has established that litigation is costly and that it has a significant

negative impact on shareholders (for example, see the case study of Cutler and Summers

(1987) who examine the costs related to the Texaco-Pennzoil litigation). Several other pa-

pers have established the negative impact of litigation filings on firm stock price as well as

the negative price reaction to firm settlements.3 Because lawsuits are an undeniable and

costly reality to all firms, it is important that we understand if and how management uses

financial policy to best manage the risk and costs associated with litigation. To the best of

my knowledge, this is the first paper that attempts to empirically examine this.4

2Debt holders are largely insulated from litigation concerns provided that a the strict priority rule isfollowed in the case of bankruptcy

3Specifically, Bhagat et al. (1994) examine the wealth effects of inter-firm litigation and show that defen-dant stock price drops and total wealth between firms falls. Bhagat et al. (1998) continue this research byexamining the effect of the type of litigation and by looking at the market reaction upon conclusion of thecase. Karpoff and Lott (1999) show that share price drops after legal settlements.

4The possible exception to this is Haslem (2005), who goes beyond stock price responses by looking atagency conflicts in the settlement process. He looks at litigation and settlements, but focuses on the impactof corporate governance on the settlement process, documenting the fact that the market reacts negatively tosettlements when compared to judgments (even losing judgments) because of the potential agency conflictsassociated with the settlement process. While he provides evidence that certain firm characteristics impactsettlement behavior and market responses, he does not look explicitly at management behavior or financialpolicy

3

Secondly, this paper adds to the literature on the strategic use of financial policy. Several

theoretical works have explored the bargaining aspects of capital structure. These papers

include those on contract bargaining generally (Perotti and Spier (1993)), bargaining with

suppliers and employees (Dasgupta and Sengupta (1993)), bargaining with unions (Bronars

and Deere (1991), and the strategic use of debt in the face of takeovers (Israel (1991)).

Many empirical papers find support for these ideas generally, but this paper provides the

first empirical test demonstrating the strategic use of capital structure when dealing with

litigants - a class of stakeholder that has not been explicitly considered in the prior research.

The rest of the paper is organized as follows: Section 2 describes the data used in the

empirical tests and the construction of the main proxy variable. Section 3 describes the

empirical methodology and results and section 4 concludes.

2 Data and Proxy Construction

2.1 Data

In order to examine the impact of the litigation on a firm’s financial policy, it is necessary

to develop a proxy for the firm’s litigation environment. To do so, I examine those litigation

events that are likely to signal change in the litigation environment of the industry as a

whole. Those industry lawsuits that are most likely to signal this change are likely to be the

large, well publicized cases. To find of a sample of such cases, I use actual litigation events

as reported by the Audit Analytics Litigation database. These data report information on

litigation for the Russell 1000 firms from 1.) legal disclosures filed with the SEC, 2.) litigation

details related to class-action and other civil litigation from disclosures and newswires, and

3.) registrations and legal opinions filed with the SEC. The data cover the period from

4

2000-2007. From this sample of litigation, Audit Analytics collects details related to the

specific litigation, including original date of filing, and if available, the original claim and

settlement amounts.5 While this is in no way an exhaustive list of all litigation faced by the

Russell 1000 firms, it is likely to capture all materially large cases, which for the purposes of

this study are the cases most likely to cause variation in the litigation environment.6

These litigation data are then matched to quarterly financial data over the same period

(January 2000 through December 2007). Cases are matched systematically by CIK code and

firm name to those firms in the CRSP/Compustat merged database. They are then merged

with quarterly financial and return data (calculated from monthly returns) in the quarter in

which the case began. It is important to note that many of the cases may involve multiple

public firms and as such will be matched more than once. Securities class action litigation is

dropped from the sample to avoid endogeneity concerns induced by litigation directly related

to firm financial policy. Table 1 presents the number of cases in the merged sample as well as

summary statistics on the size of the claims and settlements as reported by Audit Analytics.

While there is a relatively large sample of litigation events (7781 cases), the number of cases

with detailed information on the size of the claim or the settlement is relatively small (8.7%

and 10.3% of the overall sample respectively). The second row of table 1 illustrates that for

those cases in which claim data is available, the median claim is quite small at $0.71 million.

However, a number of very large suits skew the results considerably, resulting in a mean

claim value of $31 billion. Because juries are allowed to award no more than the maximum

sought by the plaintiff in the original claim, these numbers are likely to be upwardly biased

relative to the true expected loss the firm faces from the litigation. The settlement numbers,

while also skewed, are more likely to represent the expected value of the litigation. As can

be seen from table 1, the median settlement amount is $7.4 million while the mean of $88.1

million is skewed by a number of very large suits. The standard deviation of the settlement

5Claim and settlement information is available for only a small percentage of the overall cases.6It is unlikely that the omission of certain cases (specifically the small, immaterial ones) will bias the

results discussed below.

5

amounts in the data is $434 million.

The final sample of litigation events covers a wide range of industries. Table 2 shows the

average number of new cases by industry (defined at the 2-digit SIC level) each quarter. The

industry with the largest average number of new lawsuits each quarter is the BUSINESS

SERVICES industry (134 new cases per quarter) which is a broad industry that includes

everything from data processing and security services to advertising and pest control. The

second most sued industry is the CHEMICALS & ALLIED PRODUCTS MFRS which, not

surprisingly, includes the oft-sued pharmaceutical firms and has 118 new lawsuits per quarter.

The industry with the least number of cases in the Audit Analytics data is the Social Services

industry which has approx. .08 new cases per quarter. Table 2 demonstrates that Audit

Analytics provides broad industry coverage with respect to the litigation data. These data

are shown at the 2-digit SIC level for the sake of brevity. As is clear from the BUSINESS

SERVICES category, these industry classifications may be too broad to successfully measure

the litigation environment (it is unlikely that the litigation with respect to pest control will

have a significant impact on the litigation environment of data processing firms). As such,

most of the tests described below will relay on industry classifications defined at the 3 or

4-digit SIC code level.

Table 3 displays summary statistics for the final merged sample used in the analysis. The

variables presented are consistent with the financial policy literature in general (including

work on cash holdings, payout and capital structure) and are used throughout the remainder

of the empirical analysis. Debt/Assets is defined as total debt divided by total assets. Asset

Tangibility is total property, plant, and equipment divided by total assets. Mkt. to Book is

defined as the book value of debt plus the market value of assets divided by the book value

of assets. ROA is earnings before interest, taxes, depreciation, and amortization divided by

total assets. Cash Holdings is cash and short-term investments divided by total assets. Cash

Flow is defined as operating income minus interest, taxes, and dividends divided by assets.

6

2.2 Proxy Construction

To construct a proxy for the litigation environment of a firm, I examine the number of cases

that begin in each industry each quarter. For each firm, i, in each quarter, t, I count the

number of new cases that began for all firms in that industry exclusive of any new cases

involving firm i in that quarter. The calculation for the proxy variable is given by:

LitigationEnvironmenti,t =∑n6=i

k∑1

It

where n is the total number of firms in firm i ’s industry, k is the total number of litigation

cases for firm n across the sample and It is an indicator function equal to 1 if that case began

in quarter t. Industry in this case is defined at the 3-digit SIC code level.7 This variable will

take on larger values when a large number of cases are filed against a firm’s competitors. I

claim that these periods represent times when the probability of litigation is higher across

all firms in the industry, regardless of a firm’s specific characteristics.

To test whether this proxy seems to capture an exogenous increase in the risk of litigation,

I estimate the probability that a firm is sued in quarter t, conditional on that firms charac-

teristics and the LitigationEnvironment at t-1. Table 4 shows the results of conditional logit

estimations under three separate specifications. Each model is estimated with groups defined

at the firm level to control for unobserved firm effects. Year dummies are also included across

specifications and to correct for correlation in the error terms, standard errors are clustered

by 3 digit sic code (because the proxy variable is an industry level variable)8. As shown in

column 1, the impact of the LitigationEnvironmentt−1 is positively and significantly related

to the probability that a firm is sued in the next period, even after controlling for a variety

7All results are qualitatively similar when using a variable defined at the 4-digit level8The groups over which the conditional logit model are defined must be nested within the clusters used

in the standard error correction. Because of this, this model is run only on firms that maintain the same3 digit SIC code over the entire period. Point estimates are similar when the model is run over the entiresample with standard errors clustered by firm. However, in this case the standard errors are also lower

7

of firm specific variables. This result indicates that an increase of 1 lawsuit among other

firms in that industry in the prior quarter increases the odds that a firm will be sued in the

current quarter by 1.017 times, or approximately 1.7%. This result is significant at the 1%

level. The table also shows firms with lower market to book ratios have an economically

and statistically higher probability of being sued. The odds ratios of this variable is approx-

imately 0.60 across all specifications and is significant at the 5% level. In column 3, ROA

and Industry Returnt−1 are added to the model. Neither impact the point estimates or the

standard errors from the previous specifications in any meaningful way. These results across

the three models are consistent with firms that are performing poorly or are in industries

in which there are recent lawsuits being targets for litigation. It is important to note that

even after controlling for a variety of firm characteristics across the three specifications, the

odds ratio on the LitigationEnvironmentt−1 is always economically and statistically signif-

icant, suggesting that this is a reasonable proxy for an exogenous change in the litigation

environment.

Finally, in columns 2 and 3 of table 4, the firm’s debt to assets ratio is included. It is of note

that this does not appear to be an important determinant of the probability of litigation.

Because the debt to assets ratio is relatively time invariant, these estimates may be impacted

by the firm level conditioning in the logit model; nonetheless, it may suggest that if firms are

adjusting their capital structure in response to litigation they may be doing so not to prevent

lawsuits, but instead to increase bargaining power in the settlement of those lawsuits.

3 Results

Having developed a proxy for a firm’s litigation environment, I examine firm financial policy

decisions to determine if the litigation environment plays a role in those decisions. Specifi-

cally, I look at firm cash holdings, payout policy (specifically stock repurchases), and capital

8

structure. Examining the firms’ capital structure allows us to better understand if firms are

acting strategically to increase their bargaining power in the face of litigation. Cash holdings

will tell us if firms that face a higher probability of litigation maintain higher cash reserves

in support of the ”war chest” theory. Alternatively, firms may reduce their cash holdings,

either through irreversible investment or increased payout, in an effort to reduce the amount

of liquid assets available to potential litigants. Finally, looking at a firm’s payout policy will

help to determine whether managers are taking active steps in the face of this litigation,

or whether capital structure and/or cash holdings are changing passively as a result of firm

performance.

Each of these particular areas of financial policy has extensive literature related to the cross

sectional determinants. I utilize this previous literature and supplement those previously

identified cross-sectional determinants with my proxy for a change in litigation environment.

Harris and Raviv (1991) provide a very extensive summary of capital structure literature as

of 1991. Titman and Wessels (1988) and Hovakimian et al. (2001) provide evidence of the

cross-sectional determinants of debt levels that I rely on in the tests of capital structure.

Rajan and Zingales (1995) look at capital structure internationally but also distill the list of

cross-sectional control variables into a smaller, more manageable set in the face of limited

data. Opler et al. (1999) provide a good summary of literature related to cash holdings.

This work establishes a set of important cross-sectional determinants of the cash holdings of

firms. Finally, Fenn and Liang (2001) provide a review of the literature related to payout

policy as well as a set of control variables for payout policy analysis.

3.1 Capital Structure

If firms are in fact acting strategically to increase their litigation bargaining power, then

those firms facing a higher probability of litigation should utilize more debt in their capital

9

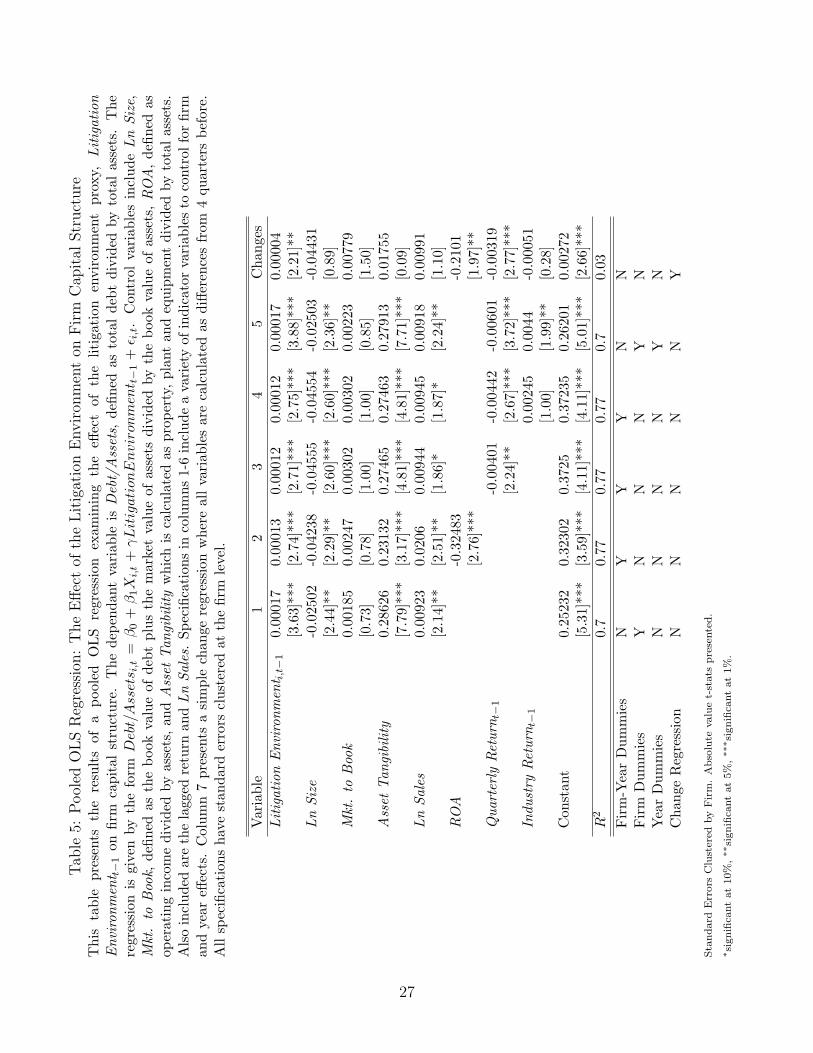

structure. Using the panel of firm specific data described above, I am able to test this

hypothesis. Using the 7 year sample of quarterly data, I run a pooled OLS regression which

includes my proxy variable for the litigation environment. The specification for these tests

generally is:

Debt/Assetsi,t = β0 + β1Xi,t + γLitigationEnvironmentt−1 + εi,t

where Xi,t represents a vector of control variables for firm i at time t. The vector of control

variables includes those shown to be important in the cross-sectional tests of capital structure

(see Titman and Wessels (1988), Hovakimian et al. (2001), Rajan and Zingales (1995), and

Harris and Raviv (1991).) These include Ln Size, Mkt. to Book, Asset Tangibility, Ln Sales,

ROA, and Returnt−1.

Table 5 shows the results of these regressions. Column 1 of the table shows a basic regression

specification using the firm’s litigation environment as an explanatory variable along with

basic firm characteristics and firm fixed effects. This regression shows that as the risk of

litigation increases, leverage actually increases as well. Columns 2-5 of table 5 add various

combinations of control variables and indicator dummies and show that generally, when the

risk of litigation is high, so is firm leverage. These results show that an increase of 1 lawsuit

over a firm’s industry mean is associated with an increase in firm leverage between 0.00012

and 0.00017. These results are robust to using firm-year dummies (Columns 2-4), as well

as to using firm and firm plus year dummies (Column 1 and 5 respectively.) This result is

statistically significant across all of these specifications at the 1% level. In terms of economic

significance, a coefficient of 0.00017 represents an increase of roughly 0.06% of the overall

mean leverage and 0.11% of the median leverage for each additional lawsuit.

As expected, Ln Size, Asset Tangibility, Ln Sales, ROA, and the lagged return are all signifi-

10

cant across the specifications in columns 1-5 and are generally consistent with prior literature.

The coefficient on Ln Size ranges from -0.025 to -0.046 and is statistically significant at the

5% level or better. This result is consistent with prior evidence that smaller firms have lower

leverage. The coefficients on Asset Tangibility range from 0.23 to 0.28 and are statistically

significant at the 1% level across all specifications. Ln Sales is marginally significant in all

specifications, with the largest effect having a coefficient generally around 0.009.

One potential concern regarding the use of the industry lawsuits as a proxy is that this

variable may merely be capturing firm and industry performance. If firms are more likely to

be sued when performance is poor and firms in the same industry suffer poor performance

at similar times, then this variable may only be capturing this effect. In order to control for

this, I include both firm and industry performance variables including ROA, lagged industry

and firm returns, and Mkt. to Book. Even after controlling for this issue, the litigation

environment variable is still positive and significant. ROA and Quarterly Returny−1 are

negative and significant across specifications, consistent with the idea that better performing

firms have less debt. For these specifications, Mkt. to Book is not statistically significant;

this result is inconsistent with much of the prior literature. This is largely attributable to the

specific sample used in this case as well as the firm-year fixed effects. It is worth noting that

the R2 value across the specifications in Columns 1-5 is greater than 70%, indicating that

the variables included explain a great deal of the within firm and within firm-year variation.

Finally, in Column 6 of table 5, I present a simple changes model. This model calculates

the changes of all variables from their value 4 quarters before. This has the same effect as

the fixed effects regression in terms of removing unobserved heterogeneity, but it may be

easier to interpret. Under this specification, the coefficient on LitigationEnvironmentt−1 is

still positive and significant, albeit slightly smaller. Nonetheless, under this simple change-

on-change framework, the overall results still hold.

11

In unreported results, I also conducted this analysis in a Tobit framework to account for

the truncation of leverage at 0 (Hovakimian et al. (2001)). These results are qualitatively

similar, although the interpretation of firm dummies is difficult in the non-linear setting. The

results are also robust to using longer lags to proxy for the litigation environment, including

LitigationEnvironmentt−2 and LitigationEnvironmentt−4.

3.2 The Mechanism for Increased Leverage

The above results support the idea that firms may be using their capital structure strategi-

cally as the risk of litigation arises. In the following section I investigate how this increase

in leverage occurs. On one hand, it is possible that as the litigation environment changes,

firms suffer in terms of performance. If this poor performance leads to write-downs of assets

then the increase in leverage may be largely mechanical, and not in fact attributable to some

strategic decision made by firm management. On the other hand, firms may be taking active

measures that increase leverage, either through a reduction in assets via dividends or share

repurchases, or by raising additional debt capital.

I examine this issue by looking first at the payout policy of firms using a pooled OLS

regression similar to the analysis for capital structure above. The specification is:

Payouti,t = β0 + β1Xi,t + γLitigationEnvironmentt−1 + εi,t

where Xi,t represents a vector of control variables for firm i at time t. Payout is defined as

either Payout/Assets,calculated as total dividends plus total repurchases divided by assets

or Common Share Repurchase/Assets depending on the specification. I again use control

variables based on prior literature on the determinants of payout policy. As in Fenn and

12

Liang (2001), I include Ln Size, Mkt. to Book, Debt/Assets, and ROA as control variables.

These regressions also includes firm-year dummies, so estimates are based on variation within

firm-years.

Table 6 shows the results from these regressions. Column 1 presents the results of the

regression specification using total payout as the dependent variable. Due to the lack of

variation in dividends generally, this model has relatively little explanatory power overall.

As expected, these results show that Payout/Assets is increasing in firm performance (as

measured by Mkt. to Book and ROA). The coefficients (t-stats) are 0.00031 (1.86) and

0.0037 (2.33) respectively. In this specification, the coefficient on Litigation Environmentt−1

is statistically significant but with a coefficient of zero at four decimal places. As the risk of

litigation increases, total payout appears to be relatively unaffected.

Given the steady nature of dividends, this is not surprising. In Columns 2-4 I estimate

models excluding dividends and preferred share repurchases. In these models, Litigation

Environmentt−1 is statistically significant at the 5% level (10% in specification 2). The

coefficients range from 0.00055 to 0.00067. Economically, these coefficients represent between

14% and 18% increase over the mean Common Share Repurchase/Assets over the entire

sample. In these specifications Mkt. to Book is positive and significant at the 5% level with

a coefficient of between 0.84 and 0.85. The coefficients on ROA range from -0.76 to -0.81

and are significant at the 1% level.

3.3 Funding Share Repurchase

Overall, the results suggest that managers are in fact taking active measures to increase

leverage when the risk of litigation is high. While dividends do not appear to be effected,

share repurchases are significantly higher when a firm’s peers face a greater number lawsuits.

13

In unreported tests, I find no evidence that firms are raising more debt capital. It appears

that the effect on leverage is exclusively through share repurchase. However, the question

still remains as to where the funds for the repurchase of these shares comes from.

To answer this question, I look first at cash holdings using a pooled OLS regression repre-

sented by the following equation:

CashHoldingsi,t = β0 + β1Xi,t + δi + γ∆LegalEnvironmentt−1 + εi,t

where Xi,t represents a vector of control variables for firm i at time t and δi represents

firm-year fixed effects. This regression is run on quarterly data where the control vari-

ables included are based on those variables determined by Opler et al. (1999) to have a

significant impact on firm cash holdings. These include Ln Size, Cash Flow, Net Working

Capital/Assets, Mkt. to Book, Debt/Assets, R&D/Sales, and lagged returns. The regression

also includes firm-year fixed effects.

Table 7, column 1, shows the results of this regression. We see that cash holdings are lower

for firms facing a higher risk of litigation. The coefficient is -0.00006 and is significant

at the 5% level. Mkt. to Book, Cash Flow, and both lagged firm and industry returns

are positively and significantly related to cash holdings. The coefficients on Net Working

Capital/Assets and Debt/Assets are both negative and significant. While the coefficient

on Litigation Environmentt−1 is small, it still represents approximately 0.03% of the overall

mean cash holdings, suggesting that, on the margin, an increase in litigation exposure does

reduce the cash holdings of firms on average. Column 2 of table 7 shows no significant effect

of the litigation environment on total current assets.

The last two columns of table 7 examine another potential source of funds for the share repur-

chases shown above. Firms, in addition to reducing cash, may increase short term liabilities.

14

By using this short term leverage, firms may be provided with an additional source of capital

that they can use to fund share repurchases. We see from columns 3 and 4 that the litigation

environment has a positive and significant effect on both accounts payable and total current

liabilities. In column 3, the coefficient on Litigation Environmentt−1 is 0.00004 (or roughly

0.02% of the overall average accounts payable. The coefficient of Litigation Environmentt−1

on total current liabilities is 0.00018, an increase of 0.08% for each additional lawsuit. Taken

in conjunction with the results on cash holdings, these results suggests that firms are increas-

ing their short term liabilities, and at the same time reducing their cash holdings when faced

with an increased risk of litigation. These two results suggest a potential source of funds

for these firms to increase leverage through share repurchase. Additionally, these results

suggests that, on average, firms are not hoarding cash in preparation for litigation but are

using cash to increase their overall leverage

3.4 Litigation and Industry Equilibrium

A potential alternative explanation for why firms’ capital structure may change in response

to a litigation event within the industry is that the litigation event may have triggered a

shift in the industry leverage equilibrium. Shleifer and Visny (1992) suggest that the leverage

within an industry is determined in part by the competitive nature of that industry. Certain

firms position themselves to take advantage of growth opportunities in market up-swings

(high leverage firms) while other firms in that industry may choose low leverage, leaving

debt capacity so that they can acquire assets of highly levered firms during downturns in

the business cycle. Significant firm litigation may lead to financial distress on the part of

one firm within the industry, resulting in a shift in the equilibrium leverage across firms

within that industry. Empirically, if what we are observing in capturing industry litigation

is competition, we would expect those firms with lower leverage in an industry to be in

a position to take advantage of distressed assets. These low leverage, low financial distress

15

firms should be the ones increasing their leverage and at the same time increasing investment.

Alternatively, as Spier and Sykes (1998) point out, the use of leverage to strategically impact

the litigation process is only a valid strategy when the risk of bankruptcy is real. If the

behavior we observe with respect to capital structure and litigation is strategic, we would

expect those firms with a higher probability of bankruptcy to increase their leverage more

than those firms who are unlikely to default. This empirical prediction is counter to what

we would expect if our leverage effect was do to industry competition and a change in the

industry equilibrium leverage.

To test between these alternatives, I utilize the regression framework presented in table 5 and

proxy for the probability of financial distress. I use three proxies for financial distress:firm

size, above median leverage within the industry, and below investment grade or unrated

debt. Each of these proxies is interacted with Litigation Environmentt−1. Results for these

regressions are given in table 8. Column 1 presents results of the standard specification

from table 5. Also included in this specification is an interaction term of firm size with

my proxy of the litigation environment. If smaller firms are more likely to be bankrupt

by litigation, then we would expect that those firms are more likely to adjust their capital

structure strategically. As shown in Column 1, the results are consistent with this hypothesis.

Larger firms are significantly less likely to increase leverage compared to smaller firms during

periods when the litigation risk is high.

In column 2 of table 8 I look at the effect of a firm’s relative leverage. I let High Debt

Dummyt−1 equal 1 if the firm has higher than its industry median leverage in the prior

quarter and zero otherwise. This term is then interacted with Litigation Environmentt−1.

The results suggest that firms that are most likely to be financially distressed (those with

the highest leverage) will increase their leverage significantly more than those firms with low

leverage. This result is significant at the 10% level and is consistent with the results on firm

16

size.

Finally, column 3 of table 8 examines the interaction of Litigation Environmentt−1 with

Investment Grade Dummyt−1, which is set to 1 if the firm has an investment grade debt

rating and is zero if the firm is either not investment grade or is unrated. The results are

consistent with those from columns 1 and 2 and show that more credit worthy firms adjust

their debt/assets ratios less than those low credit quality firms when the litigation exposure

is high. Taken together, these results suggest that the actions firms take when faced with an

increased risk of litigation are a strategic response to the litigation risk and not a response

to a shift the industry leverage equilibrium. Additionally, I find no evidence of an increase

in investment when litigation risk is higher, suggesting that I am not capturing those firms

that have positioned themselves to take advantage of distressed assets.

A second related alternative explanation is that litigation against another firm in the industry

may result in the undervaluation of peer firms. If the market believes that peer firms have

similar liabilities as the sued firm, these firms may find their market values falling. If the

management of these firms knows the firm does not in fact have such a liability, they may

repurchase shares in an effort to time the market (Baker and Wurgler (2002)) or signal

firm value (Vermaelen (1981)). In such a case, controlling for firm and industry returns in

the regression may not adequately control for the effect. However, if this is the case, we

would expect those firms who find themselves in industries that are being sued but are not

sued themselves to subsequently outperform. In untabulated results, I find no evidence that

these firms’ returns are higher in the following quarters or year, suggesting that this observed

behavior is not a response to undervaluation but a strategic response to the risk of litigation.

17

3.5 Litigation Reform

Thus far, I have proxied for changes in the litigation environment by examining the number

of lawsuits in a given industry. However, the litigation environment for a firm can also be

altered by legislation and court decisions that make it harder or easier to sue a given firm

or an industry. To provide further support for the results above without the noise induced

by the litigation proxy variable, I turn to federal tort reform acts that reduced the expected

litigation claims against firms within particular industries at some point in time.

While there have been 29 federal tort reforms according the American Tort Reform Asso-

ciation, many of these reforms apply to individuals or government agencies. However, two

specific tort reforms relate to reducing the liability of particular industries.9 These include

the Black Lung Benefits Act of 1972 and the The General Aviation Revitalization Act of

1994.10 The former set up a federal fund to pay coal miners suffering from pneumoconiosis,

reducing the incentive to litigate against mining companies. The later placed limitations on

the ability of litigants to sue aircraft manufacturers in the event of an airline crash.

I examine the firms of both the coal mining and aircraft manufacturing industries, before

and after the tort reforms described above to see if behavior changes are consistent with the

results described in the previous sections. To do this, I split each industry into constrained

firms (closer to financial distress) and unconstrained firms. I then look at these firms both

before and after the tort reforms were enacted. This difference-in-differences approach will

show whether the litigation reform appears to have changed the financial policy decisions of

those firms. Based on the results above, prior to the tort reform (when the risk of litigation

was higher) we would expect those constrained firms to hold less cash, have more short term

debt (in terms of accounts payable) and repurchase more shares. We would then expect this

9There are many more state level tort reforms, however, because most public companies do business inmultiple states, it is difficult to determine which reforms affected which firms

10The Private Securities Litigation Reform Act of 1995 was specifically excluded from this analysis becauseof the endogeneity associated with financial policy and securities litigation

18

difference to be smaller after the litigation reform as the risk to those firms decreases.

Table 9 shows the results of this analysis. Each column represents one of the three financial

policy variables (cash holdings, accounts payable, and share repurchases). Constrained firms

(those more likely to be placed in financial distress by litigation) are defined as those firms

smaller than the median firm within their industry in a given year.11 Column 1 shows that

the constrained firms hold less cash in general. We see that after litigation reform, this

difference is smaller, consistent with the idea that these firms no longer have to shield as

many of their assets. We see that with respect to accounts payable, the point estimates are

consistent with the constrained firms using more short term debt and that this difference is

smaller after the reduction in litigation exposure. However, these results are not statistically

significant due to the low power of this test (with only two industries). Finally, column

3 shows the results for the share repurchase behavior of the firms. Again the results are

insignificant but the point estimates are consistent with the results in the previous section.

Overall, while not overwhelmingly conclusive, these results suggest provide support for the

large sample evidence without the need of a noisy proxy variable.

4 Conclusion

Litigation is an undeniable and costly realty for all firms in today’s market place. While a

great deal is known about the costs associated with litigation12, very little is known about

the role that financial policy plays in dealing with this costly reality. Taking advantage of

exogenous variation in the probability of litigation I use actual litigation events to construct

a proxy for each firms litigation environment and test whether that environment impacts

firm financial policy. My results indicate that, in periods with a higher risk of litigation,

11The results using debt levels to proxy constraint are qualitatively similar12See Haslem (2005) for a summary of these findings

19

firms choose higher leverage. I show that this is not a passive result due to firm performance,

but rather an active decision by managers. These firms buy back significantly more shares

of common stock when the risk of litigation is high and finance these repurchases using

cash holdings and an increase in short-term liabilities. These findings are consistent with

firms increasing the use of debt in order increase bargaining power in the settlement process.

Finally, I show that these results are stronger for those firms that face a greater risk of

default due to litigation. After legislative reform, differences in financial policy between the

firms most at risk of litigation and other firms in the industry decrease. These results are

consistent with the idea that firms use financial policy strategically to increase bargaining

power and ultimately limit the payoffs to potential litigants. Furthermore, I find no evidence

that firms on average are hording cash in preparation for legal battles.

Overall, these results suggest that there may be a role for financial policy in dealing with

civil litigation. They suggest that additional work in the area would be valuable in helping

to determine to what extent managers are successful in mitigating litigation exposure and

minimizing costs.

20

References

Baker, Malcolm and Wurgler, Jeffrey. Market timing and capital structure. The Journal of

Finance, 57(1):1–32, 2002.

Bhagat, Sanjai, Bizjak, John, and Coles, Jeffrey. The shareholder wealth implications of

corporate lawsuits. Financial Management, 27:5–27, 1998.

Bhagat, Sanjai, Brickley, James, and Coles, Jeffrey. The wealth effects of interfirm lawsuits.

Journal of Financial Economics, 35:221–247, 1994.

Bronars, Stephen and Deere, Donald. The threat of unionization, the use of debt, and the

preservation of shareholder wealth. Quarterly Journal of Economics, 106(1):231–254, 1991.

Cutler, David M. and Summers, Lawrence H. The costs of conflict resolution and finan-

cial distress: Evidence from the Texaco-Pennzoil litigation. Rand Journal of Economics,

19:157–172, 1987.

Dasgupta, Supdipto and Sengupta, Kunal. Sunk investment, bargaining and choice of capital

structure. International Economic Review, 34(1):203–220, 1993.

Fenn, George and Liang, Nellie. Corporate payout policy and managerial stock incentives.

Journal of Financial Economics, 60:45–72, 2001.

Harris, Milton and Raviv, Artur. The theory of capital strucutre. The Journal of Finance,

46(1):297–355, 1991.

Haslem, Bruce. Managerial opportunism during corporate litigation. The Journal of Finance,

60(4):2013–2041, 2005.

Hovakimian, Armen, Opler, Tim, and Titman, Sheridan. The debt-equity choice. The

Journal of Financial and Quantitative Analysis, 36(1):1–24, 2001.

21

Israel, Ronen. Capital structure and the market for corporate control: The defensive role of

debt financing. The Journal of Finance, 46(4):1391–1409, 1991.

Karpoff, Jonathan and Lott, John. On the determinants and importance of punitive damage

awards. Journal of Law and Economics, 42:527–573, 1999.

Opler, Tim, Pinkowitz, Lee, Stulz, Rene, and Williams, Rohan. The determinants and

implications of corporate cash holdings. Journal of Fiancial Economics, 52:3–46, 1999.

Perotti, Enrico and Spier, Kathryn. Capital structure as a bargaining tool: The role of

leverage in contract renegotiation. The American Economic Review, 83(5):1131–1141,

1993.

Rajan, Raghuram and Zingales, Luigi. What do we know about capital structure? some

evidence from international data. The Journal of Finance, 50(5):1421–1460, 1995.

Shleifer, Andrei and Visny, Robert. Liquidation value and debt capacity: A market equilib-

rium approach. The Journal of Finance, 47(4):1343–1366, 1992.

Spier, Kathryn and Sykes, Alan. Capital strucutre, priority rules, and the settlement of civil

claims. International Review of Law and Economics, 18(2):187–200, 1998.

Titman, Sheridan and Wessels, Roberto. The determinants of capital structure. The Journal

of Finance, 43(1):1–19, 1988.

Vermaelen, Theo. Common stock repurchases and market signalling *1: An empirical study.

Journal of Financial Economics, 9(2):139–183, 1981.

22

Table 1: Summary Statistics: Litigation FilingsThis table presents summary statistics related to the cases in the Audit Analytics databasethat were successfully matched with the CRSP/Compustat merged database. Claim andsettlement means and medians are calculated conditional on being reported

Variable Observations Mean($MM) Median($MM) Std.Dev($MM)

Cases 7781

Claim 681 31,000 0.71 783,000

Settlement 806 88.1 7.4 434

23

Table 2: Average Number of New Litigation Cases Each Quarter by IndustryThis table presents the average number of new litigation cases per quarter by industry overthe 2000-2007 period in the final merged sample. The industry is classified at the two-digitSIC code level. Only those industries with at least 1 case over the sample period are includedin the table.

Industry SIC Mean Cases

AGRICULTURAL PRODUCTION-CROPS 1 0.21

AGRICULTURAL PRODUCTION-LIVESTOCK 2 0.18

COAL MINING 12 1.74

OIL & GAS EXTRACTION 13 12.31

MINING & QUARRYING-NONMETALLIC MINERALS 14 0.67

BUILDING CONSTRUCTION-GEN CONTRACTORS 15 2.81

HEAVY CONSTRUCTION EXCEPT BUILDING 16 1.89

CONSTRUCTION-SPECIAL TRADE CONTRACTORS 17 0.72

FOOD & KINDRED PRODUCTS MFRS 20 16.04

TOBACCO PRODUCTS MFRS 21 3.15

TEXTILE MILL PRODUCTS MFRS 22 1.91

APPAREL & OTHER FINISHED PRODUCTS MFRS 23 3.28

LUMBER & WOOD PRODS EXCEPT FURNTR MFRS 24 2.12

FURNITURE & FIXTURES MFRS 25 2.06

PAPER & ALLIED PRODUCTS MFRS 26 6.88

PRINTING PUBLISHING & ALLIED INDUSTRIES 27 7.48

CHEMICALS & ALLIED PRODUCTS MFRS 28 118.07

PETROLEUM REFINING & PLASTICS MFRS 29 10.05

RUBBER & MISCELLANEOUS PLASTICS MFRS 30 6.77

LEATHER & LEATHER PRODUCTS MFRS 31 2.73

STONE CLAY GLASS & CONCRETE PRODS MFRS 32 4.36

PRIMARY METAL INDUSTRIES MFRS 33 8.24

FABRICATED METAL PRODUCTS MFRS 34 8.08

INDUSTRIAL & COMMERCIAL MACHINERY MFRS 35 53.82

ELECTRONIC & OTHER ELECTRICAL EQUIP MFRS 36 97.81

TRANSPORTATION EQUIPMENT MFRS 37 18.6

MEASURING & ANALYZING INSTRUMENTS MFRS 38 40.53

MISCELLANEOUS MANUFACTURING INDS MFRS 39 4.94

RAILROAD TRANSPORTATION 40 1.56

MOTOR FREIGHT TRANSPORTATION/WAREHOUSE 42 2.66

WATER TRANSPORTATION 44 1.06

TRANSPORTATION BY AIR 45 7.58

PIPELINES EXCEPT NATURAL GAS 46 0.11

TRANSPORTATION SERVICES 47 1.08

COMMUNICATIONS 48 29.38

ELECTRIC GAS & SANITARY SERVICES 49 35.8

WHOLESALE TRADE-DURABLE GOODS 50 13.2

WHOLESALE TRADE-NONDURABLE GOODS 51 13.05

BUILDING MATERIALS & HARDWARE 52 2.09

GENERAL MERCHANDISE STORES 53 11.59

FOOD STORES 54 4.22

AUTOMOTIVE DEALERS & SERVICES STATIONS 55 2.6

APPAREL & ACCESSORY STORES 56 10.92

HOME FURNITURE & FURNISHING STORES 57 5.89

EATING & DRINKING PLACES 58 7.08

MISCELLANEOUS RETAIL 59 16.84

DEPOSITORY INSTITUTIONS 60 24.91

NONDEPOSITORY CREDIT INSTITUTIONS 61 8.72

SECURITY & COMMODITY BROKERS 62 31.74

INSURANCE CARRIERS 63 27.01

INSURANCE AGENTS BROKERS & SERVICES 64 8.64

REAL ESTATE 65 0.53

HOLDING & OTHER INVESTMENT OFFICES 67 11.05

HOTELS ROOMING HOUSES & CAMPS 70 3.44

PERSONAL SERVICES 72 3.4

BUSINESS SERVICES 73 132.75

AUTO REPAIR SERVICES & PARKING 75 0.85

MOTION PICTURES 78 7.83

AMUSEMENT & RECREATION SERVICES 79 5.35

HEALTH SERVICES 80 12.36

EDUCATIONAL SERVICES 82 4.07

SOCIAL SERVICES 83 0.08

ENGINEERING & ACCOUNTING & MGMT SVCS 87 14.84

MISCELLANEOUS SERVICES NEC 89 0.16

ADMIN-ENVIROMENTAL QUALITY PROGRAMS 95 0.11

NATIONAL SECURITY & INTERNATIONAL AFFAIR 97 1.2

24

Table 3: Summary StatisticsThis table presents firm level summary statistics for the main variables used in the empiricalanalysis. Debt/Assets is defined as total debt divided by total assets. Asset Tangibility istotal property, plant, and equipment divided by total assets. Mkt. to Book is defined as thebook value of debt plus the market value of assets divided by the book value of assets. ROAis earnings before interest, taxes, depreciation, and amortization divided by total assets.Cash Holdings is cash and short-term investments divided by total assets. Cash Flow isdefined as operating income minus interest, taxes, and dividends divided by assets.

Variable Mean Median Std. Deviation Min Max

Debt/Assets 0.20 0.16 0.20 0 1.01

Asset Tangibility 0.26 0.18 0.23 0.00 0.99

Mkt. to Book 1.87 1.23 2.24 0.01 101.42

Ln Sales 3.96 4.02 2.33 -6.91 11.50

ROA 0.002 0.024 0.060 -0.318 0.125

Ln Size 5.96 5.46 2.06 -6.91 12.58

Cash Holdings 0.22 0.11 0.25 0.00 1.00

Cash Flow 0.002 0.015 0.065 -6.001 5.813

Net Work. Cap/Assets 0.05 0.03 0.18 -0.76 0.53

R&D/Sales 0.03 0.02 0.04 0.00 1.92

25

Table 4: Conditional Logit Model: Estimating the Probability of a LawsuitThis table presents a conditional logit model estimating the probability of a lawsuit in agiven quarter for a given firm. The dependent variable is equal to 1 if the firm is sued inthat quarter and zero otherwise. The groups for the conditional model are defined at thefirm level to control for firm specific omitted variables. Control variables include Ln Size,Mkt. to Book, defined as the book value of debt plus the market value of assets divided bythe book value of assets, and Asset Tangibility which is calculated as property, plant andequipment divided by total assets. All specifications include firm-year fixed effects. OddsRatios are presented in lieu of coefficients. Standard errors are clustered at the 3 digit siccode.

Variable 1 2 3

Litigation Environmenti,t−1 1.017 1.017 1.017

[4.13]∗∗∗ [4.21]∗∗∗ [4.40]∗∗∗

Payout 1.10 1.09 0.99

[0.15] [0.14] [0.02]

Cash Holdings 0.54 0.38 0.24

[0.37] [0.50] [0.62]

Ln Size 1.30 1.33 1.57

[0.65] [0.73] [0.92]

Mkt. to Book 0.60 0.60 0.61

[2.44]∗∗ [2.52]∗∗ [2.53]∗∗

Asset Tangibility 0.29 0.59 0.20

[0.34] [0.16] [0.44]

Debt/Assets 0.19 0.22

[0.78] [0.77]

ROA 0.001

[1.04]

Industry Returnt−1 1.12

[0.38]

Year Dummies Y Y Y

Groups defined at the firm levelRobust z statistics clustered by 3-digit SIC code in brackets.∗ significant at 10%; ∗∗ significant at 5%; ∗∗∗ significant at 1%

26

Tab

le5:

Pool

edO

LS

Reg

ress

ion:

The

Effec

tof

the

Litig

atio

nE

nvir

onm

ent

onFirm

Cap

ital

Str

uct

ure

Thi

sta

ble

pres

ents

the

resu

lts

ofa

pool

edO

LS

regr

essi

onex

amin

ing

the

effec

tof

the

litig

atio

nen

viro

nmen

tpr

oxy,

Litig

atio

nEnv

iron

men

t t−

1on

firm

capi

tal

stru

ctur

e.T

hede

pend

ant

vari

able

isD

ebt/

Ass

ets,

defin

edas

tota

lde

btdi

vide

dby

tota

las

sets

.T

here

gres

sion

isgi

ven

byth

efo

rmD

ebt/

Ass

ets i

,t=

β0

+β

1X

i,t+

γL

itig

ati

onE

nvir

onm

ent t−

1+

ε i,t.

Con

trol

vari

able

sin

clud

eLn

Size

,M

kt.

toBoo

k,de

fined

asth

ebo

okva

lue

ofde

btpl

usth

em

arke

tva

lue

ofas

sets

divi

ded

byth

ebo

okva

lue

ofas

sets

,RO

A,de

fined

asop

erat

ing

inco

me

divi

ded

byas

sets

,an

dA

sset

Tan

gibi

lity

whi

chis

calc

ulat

edas

prop

erty

,pl

ant

and

equi

pmen

tdi

vide

dby

tota

las

sets

.A

lso

incl

uded

are

the

lagg

edre

turn

and

Ln

Sale

s.Sp

ecifi

cati

ons

inco

lum

ns1-

6in

clud

ea

vari

ety

ofin

dica

tor

vari

able

sto

cont

rolf

orfir

man

dye

areff

ects

.C

olum

n7

pres

ents

asi

mpl

ech

ange

regr

essi

onw

here

allva

riab

les

are

calc

ulat

edas

diffe

renc

esfr

om4

quar

ters

befo

re.

All

spec

ifica

tion

sha

vest

anda

rder

rors

clus

tere

dat

the

firm

leve

l.

Var

iabl

e1

23

45

Cha

nges

Litig

atio

nEnv

iron

men

t i,t−

10.

0001

70.

0001

30.

0001

20.

0001

20.

0001

70.

0000

4[3

.63]

***

[2.7

4]**

*[2

.71]

***

[2.7

5]**

*[3

.88]

***

[2.2

1]**

Ln

Size

-0.0

2502

-0.0

4238

-0.0

4555

-0.0

4554

-0.0

2503

-0.0

4431

[2.4

4]**

[2.2

9]**

[2.6

0]**

*[2

.60]

***

[2.3

6]**

[0.8

9]M

kt.

toBoo

k0.

0018

50.

0024

70.

0030

20.

0030

20.

0022

30.

0077

9[0

.73]

[0.7

8][1

.00]

[1.0

0][0

.85]

[1.5

0]A

sset

Tan

gibi

lity

0.28

626

0.23

132

0.27

465

0.27

463

0.27

913

0.01

755

[7.7

9]**

*[3

.17]

***

[4.8

1]**

*[4

.81]

***

[7.7

1]**

*[0

.09]

Ln

Sale

s0.

0092

30.

0206

0.00

944

0.00

945

0.00

918

0.00

991

[2.1

4]**

[2.5

1]**

[1.8

6]*

[1.8

7]*

[2.2

4]**

[1.1

0]RO

A-0

.324

83-0

.210

1[2

.76]

***

[1.9

7]**

Qua

rter

lyRet

urn t−

1-0

.004

01-0

.004

42-0

.006

01-0

.003

19[2

.24]

**[2

.67]

***

[3.7

2]**

*[2

.77]

***

Indu

stry

Ret

urn t−

10.

0024

50.

0044

-0.0

0051

[1.0

0][1

.99]

**[0

.28]

Con

stan

t0.

2523

20.

3230

20.

3725

0.37

235

0.26

201

0.00

272

[5.3

1]**

*[3

.59]

***

[4.1

1]**

*[4

.11]

***

[5.0

1]**

*[2

.66]

***

R2

0.7

0.77

0.77

0.77

0.7

0.03

Fir

m-Y

ear

Dum

mie

sN

YY

YN

NFir

mD

umm

ies

YN

NN

YN

Yea

rD

umm

ies

NN

NN

YN

Cha

nge

Reg

ress

ion

NN

NN

NY

Sta

ndard

Err

ors

Clu

ster

edby

Fir

m.

Abso

lute

valu

et-

stats

pre

sente

d.

∗si

gnifi

cant

at

10%

,∗∗

signifi

cant

at

5%

,∗∗∗si

gnifi

cant

at

1%

.

27

Table 6: Pooled OLS Regression: The Effect of the Litigation Environment on Total Payoutand Share RepurchasesThis table presents the results of a pooled OLS regression examining the effect of the litiga-tion environment proxy, Litigation Environmentt−1 on firm payout. The dependent variablesare Payout/Assets, calculated as total dividends plus total repurchases divided by assets andShare Repurchase/Assets. The regression is given by the form Payouti,t = β0 + β1Xi,t +γLitigationEnvironmentt−1 + εi,t. Control variables include Ln Size, Mkt. to Book, defined asthe book value of debt plus the market value of assets divided by the book value of assets, ROA,defined as operating income divided by assets, and Debt/Assets, defined as total debt divided bytotal assets. Also included are the lagged returns at the firm and industry level. All specificationsinclude firm-year fixed effects.

Total Payout Common Share RepurchasesVariable 1 2 3 4Litigation Environmentt−1 0.00000 0.00055 0.00067 0.00067

[2.74]*** [1.83]* [1.97]** [1.98]**Ln Size -0.00413 -0.0395 -0.03664 -0.03659

[2.07]** [0.68] [0.63] [0.62]Mkt. to Book 0.00031 0.83664 0.84695 0.84697

[1.86]* [2.05]** [2.08]** [2.08]**ROA 0.00373 -0.81413 -0.76221 -0.76197

[2.33]** [3.00]*** [3.08]*** [3.08]***Debt/Assets 0.00606 0.06533 0.08425 0.08437

[1.55] [0.35] [0.45] [0.45]Quarterly Returnt−1 -0.00012 -0.09573 -0.09633

[0.35] [2.12]** [2.09]**Industry Returnt−1 -0.00115 0.00186

[1.53] [0.10]Constant 0.02827 -0.42422 -0.46267 -0.46362

[2.44]** [0.60] [0.65] [0.65]R2 0.15 0.57 0.58 0.58Firm-Year Dummies Y Y Y Y

Standard Errors Clustered by Firm. Absolute value t-stats presented.

∗significant at 10%, ∗∗significant at 5%, ∗∗∗significant at 1%.

28

Table 7: Pooled OLS Regression: The Effect of the Litigation Environment on Cash Holdings,Current Assets, and Current LiabilitiesThis table presents the results of a pooled OLS regression examining the effect of the litigation envi-ronment proxy, Litigation Environmentt−1 on firm cash holdings, current assets, accounts payable,and current liabilities. The dependant variables are Cash Holdings, defined as cash and short-terminvestments divided by total assets, Current Assets, defined as total current assets scaled by totalassets, Accounts Payable defined as accounts payable scaled by total assets, and Current Liabilitiesdefined as total current liabilities divided by total assets. The regression is given by the formyi,t = β0 + β1Xi,t + γLitigationEnvironmentt−1 + εi,t. Control variables include Ln Size, Mkt. toBook, defined as the book value of debt plus the market value of assets divided by the book valueof assets, Cash Flow, defined as operating income minus interest, taxes, and dividends divided byassets, and Debt/Assets, defined as total debt divided by total assets. All specifications includefirm-year fixed effects.

Variable Cash Current Accounts CurrentVariable Holdings Assets Payable LiabilitiesLitigation Environmenti,t−1 -0.00006 -0.00002 0.00004 0.00018

[1.99]** [1.01] [2.99]*** [4.58]***Ln Size 0.00266 -0.07249 -0.05321 -0.14638

[0.70] [19.83]*** [7.17]*** [8.81]***Mkt. to Book 0.00268 0.00395 0.00214 0.00212

[2.76]*** [6.61]*** [2.84]*** [1.27]Cashflow 0.11598

[7.70]***Net Working Capital/Assets -0.0359

[6.08]***Debt/Assets -0.04439

[2.32]**Asset Tangibility -0.70272 0.03677 0.04587

[42.34]*** [1.92]* [1.51]Ln Sales 0.00327 0.01145 0.02817

[1.86]* [6.38]*** [10.70]***Quarterly Returnt−1 0.00516 -0.00002 0.00004 0.00018

[5.68]*** [1.01] [2.99]*** [4.58]***Industry Returnt−1 0.00307 -0.00262 -0.00245 -0.00402

[1.97]** [2.06]** [1.08] [1.40]Constant 0.18499 1.07293 0.42969 0.88844

[8.19]*** [56.13]*** [9.90]*** [9.68]***R2 0.92 0.94 0.95 0.62Firm-Year Dummies Y Y Y Y

Standard Errors Clustered by Firm. Absolute value t-stats presented.

∗significant at 10%, ∗∗significant at 5%, ∗∗∗significant at 1%.

29

Table 8: Pooled OLS Regression: The Effect of the Litigation Environment and FinancialDistress on Firm Capital StructureThis table presents the results of a pooled OLS regression examining the effect of the litigationenvironment proxy, Litigation Environmenti,t on firm capital structure. The dependant vari-able is Debt/Assets, defined as total debt divided by total assets. The regression is given bythe form Debt/Assetsi,t = β0 + β1Xi,t + γ1LitigationEnvironmentt−1 + γ2FinancialDistress ∗LitigationEnvironment + εi,t. Control variables include Ln Size, Mkt. to Book, defined as thebook value of debt plus the market value of assets divided by the book value of assets, ROA, de-fined as operating income divided by assets, and Asset Tangibility which is calculated as property,plant and equipment divided by total assets. Also included are the lagged return and Ln Sales.Financial distress is defined for columns 1-3 respectively as Ln Size, High Debt Dummyt−1 which isan indicator equal to 1 if the firm has higher leverage than its industry median and zero otherwise,and Investment Grade Dummyt−1 which is an indicator equal to 1 if the firm has investment gradedebt ratings and equal to zero if the debt is unrated or below investment grade.

Variable 1 2 3Litigation Environmentt−1 0.00038 0.00471 0.00491

[2.53]** [3.21]*** [2.50]**Ln Size -0.0432 -0.05001 -0.0456

[2.39]** [2.81]*** [2.56]**Mkt. to Book 0.00303 0.00425 0.00379

[1.01] [1.20] [1.07]Asset Tangibility 0.27414 0.22313 0.27348

[4.80]*** [3.83]*** [4.67]***Ln Sales 0.00929 0.00763 0.00902

[1.82]* [1.53] [1.77]*Quarterly Returnt−1 -0.00437 -0.00483 -0.00396

[2.63]*** [2.93]*** [2.34]**Industry Returnt−1 0.00243 0.00188 0.00258

[1.00] [0.85] [1.13]Size*Litigation Environmentt−1 -0.00005

[1.87]*High Debt Dummyt−1 0.10369

[34.67]***High Debtt−1*Lit.Env.t−1 0.00353

[1.65]*Investment Grade Dummyt−1 -0.00952

[2.24]**Investment Gradet−1*Lit.Env.t−1 -0.00714

[3.14]***Constant 0.35991 0.36191 0.37733

[3.84]*** [3.95]*** [4.07]***R2 0.77 0.78 0.77Firm-Year Dummies Y Y Y

Standard Errors Clustered by Firm. Absolute value t-stats presented.

∗significant at 10%, ∗∗significant at 5%, ∗∗∗significant at 1%.

30

Table 9: Difference in Difference Estimation: Constrained vs. Unconstrained Firms Beforeand After Litigation Reform LegislationThis table presents the results of an OLS regression examining the effect of litigation reformon the financial policy decisions of unconstrained and constrained firms. Unconstrained takesa value of one if the firm is above median size for its industry in a particular year and zerootherwise. Post Reform takes a value of 1 if the observation occurred after the tort reformlegislation for that industry and zero otherwise. This table includes firms from the airlinemanufacturing industry and the coal mining industry. Tort reform occurred in the coalindustry in 1972 (Black Lung Benefits Act of 1972) and the airline manufacturing industryin 1994 (General Aviation Revitalization Act of 1994). Cash Holdings is defined as cashdivided by total assets, Accounts Payable is defined as accounts payable divided by totalassets, and Share Repurchases are defined as share repurchases divided by total assets.

Variable Cash Holdings Accounts Payable Share RepurchasesUnconstrained 0.04318 −0.08471 −242

[3.30]∗∗∗ [3.47]∗∗∗ [1.13]Post Reform 0.0727 −0.00876 −274

[3.01]∗∗∗ [0.22] [1.26]Unconstrained*Post Reform −0.11133 −0.0548 −245

[4.06]∗∗∗ [1.00] [1.13]Constant 0.0342 0.20754 238

[3.27]∗∗∗ [2.69]∗∗∗ [1.11]R2 0.06 0.03 0.02

Standard Errors Clustered by Firm. Absolute value t-stats presented.

∗significant at 10%, ∗∗significant at 5%, ∗∗∗significant at 1%.

31