the legal & general network performance management system

TRANSCRIPT

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 1 of 28

The Legal & General Network Performance Management System

(Adviser)

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 2 of 28

Contents

1) Introduction

2) Recruitment

3) Training and assessment

4) Commencing the role

5) Continuing the role

6) Requirements of L&G network enforced increased individual supervision

7) Enhanced Supervision

8) Supervisors moving to adviser status (or vice versa)

9) Supervision of close relatives

10) Adviser – Long term sickness and maternity leave

11) Key knowledge and skills grid

12) Observations

13) Formal 1:1 meetings

14) Key performance indicators and Management information standards

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 3 of 28

1. Introduction

The Legal & General Network (hereafter called ‘The Network’) Performance Management System (PMS) has been designed to provide a framework to ensure a consistent approach to the supervision of every adviser.

A comprehensive training and coaching programme is essential to ensure that the knowledge and skills of the adviser are appropriate, are developed throughout their careers, identifies development needs and sets the foundation for the continuing professional development of the adviser. By working closely with the adviser and following these guidelines, we believe that it will benefit the relationships between the adviser, the firm, the Network and the customer, as well as satisfying regulatory requirements.

Supervisors must ensure they are comfortable with their ability to carry out all the requirements of this scheme with all advisers within their span of control (SPOC). We would suggest a maximum of 15 advisers per supervisor. Where the SPOC is in excess of 15, the Supervisor or the firms PoCC must document via a fully completed CSmart event (SPOCDEC) the current position and how they will continue to manage the increased SPOC.

An adviser is required to show and maintain competence in 4 key areas:

Knowledge – to have appropriate qualifications, and a continually tested understanding of genericindustry and firm specific products, and of the processes required to fulfil the role

Skills – to have the ability to display a range of technical and interpersonal skills in order to perform therole to the desired standards

Ethics – personal commitment to demonstrate ethical behaviours which improves the customerperception of the industry as a whole and ultimately achieve better customer outcomes

Expertise – the ability to apply their knowledge and skills to achieve positive and fair outcomes for thecustomer, and meet the performance standards required of the role of adviser

The PMS is aimed at providing the steps to allow you to monitor and assess all of the key areas above. To achieve and maintain competent status all the relevant steps in each section of this document must be completed, checked/evidenced and documented in a timely and accurate manner.

The CSmart system is used to document adviser career progress. The CSmart system for advisers normally covers 3 areas known as ‘tracks’ which are now known as:-

Training and assessment

Commencing the role

Continuing the role

The PMS will be regularly reviewed to ensure it remains appropriate and may be updated from time to time. Where no specific ruling or guidance exists within these procedures, we expect that an individual or firm will take an intelligent view in the interest of the customer, or seek guidance from us, rather than seek to exploit any apparent omissions.

Any queries relating to this scheme must be directed to the Business Standards Team.

Any requests for concessions must be submitted to [email protected]. Any concessions granted will be logged on the Adviser’s CSmart track under an event named (BSTCON) and will be granted an end date that must be adhered to.

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 4 of 28

2. Recruitment

Introduction It’s important to have a comprehensive recruitment process to ensure the right calibre of individual is appointed to the role of Adviser. This will contribute to the successful completion of all stages in the Performance Management system and improve customer satisfaction.

Recruitment Process

The recruitment process needs to assess knowledge, skills, behaviour and expertise, and therefore could include but is not limited to : Interviews (including general industry and product knowledge) Role plays Review of Financial standing Review of Disciplinary issues Consideration of the past experiences and successes of the candidate Psychometric testing Interrogation of detail within applicants C.V. Personal effectiveness

It’s also considered good practice to try to attain some detail of Advisers current performance including: Business mix Production track record Proof of earnings Conversion ratios Other relevant KPI data (for example review of complaints history, CFO’s etc)

Other steps to be completed during or prior to this stage:

Step 1: Remuneration Structure Firms should ensure that they have a documented remuneration structure in place that encourages the correct adviser behaviours. Rewards under the structure must not encourage ‘spikes’ in activity or written business. The correct metrics should be used to assess whether any poor behaviour exists, and appropriate sanctions should be included to ensure that this behaviour is not rewarded. Detailed guidance is available in Section 3 of the Operating Procedures.

Step 2: Job description and Principal Accountabilities The recruiting firm must ensure that a job description is available, up to date and reflects the principal accountabilities of the role. This must be held centrally and be available for inspection if required.

Step 3: Appropriate examination level The candidate must be appropriately qualified for the role. The qualifications required are : Mortgage and Protection Adviser – CF1 and CF6 (or CeMap) Mortgage and Protection Adviser wishing to also advise on Lifetime Mortgages – CF1, CF6 and ER1 General Insurance Only Advisers – CF1 only Protection Only Adviser – CF1 only

Supervisors must advise the potential recruit that they will need to provide original certificates of any exams achieved which are appropriate to the role. Copies of original certificates can be provided but need to be validated by an employee of Legal & General, the firms APER, Supervisor or Point of Compliance Contact. Validated copies must be sent to Legal & General Network Training Department along with the Training Registration Form, or with the application pack (see step 5).

Dispensation can be given for previous equivalent exams. If unsure about whether dispensation may apply, please refer to the Business Standards Team.

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 5 of 28

Step 4: Discuss and agree market areas The firm and the potential recruit must discuss and agree the market areas in which the adviser will act in (this may of course be limited by the firms scope of service or the qualifications of the adviser). The normal market areas covered by Legal & General Network are: Standard Mortgages Lifetime Mortgages Mortgage Protection Family Protection General Insurance

Step 5: Application pack requested The firm must ensure the application pack (including Training Registration form) has been acquired and must be fully completed. All relevant documents must be enclosed. Any missing information or documents could cause delays in getting the Adviser authorised.

It’s important to point out that all information must be disclosed or they risk having their application declined.

The fully completed application pack must then be sent to Firms and Individual Approvals Team (FIA) to assess and reference as necessary. The Training Registration Form must be sent to Training Department to gain access to The Learning Network (TLN).

All potential recruits must be advised to chase any outstanding references to aid the speed of the processing of the application.

FIA will also require all potential recruits to complete a Criminal Record Bureau (CRB) check. A link will be sent via email in order that the applicant can complete the CRB check online.

Step 6: Approval and Offer Letter issued Once approval has been received from FIA, the PoCC, Supervisor or Firm’s HR department must ensure that : The relevant offer letter is issued to the successful applicant A copy of the offer letter is retained on the Adviser appointment file A written copy of acceptance of offer from the successful applicant/s is submitted to the FIA and the

original retained on the appointment file Start date agreed with Adviser Contracts are signed by new Adviser Copy of signed contracts are sent to FIA A letter is issued to new Adviser confirming contract commencement date and details of Supervisor or

designated point of contact. Adviser is issued with a copy of the contract

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 6 of 28

3. Training and assessment

Steps

Step Action Required By Whom Event Name 1 Check adviser can access training

and can launch material and tests Supervisor/Adviser N/A

2 Set up CSmart access for adviser and coach effective use

Supervisor MNIT

3 Maintain regular contact to track training progress and coach as required

Supervisor MNCONTLOG

4 Supervisor to brief adviser on L&G Network procedures, standards and requirements

Supervisor MNSUPSO

5 Adviser programme – adds development and coaching as necessary

Supervisor/Course Trainers

ADVSPA

6 Ensure adviser is aware of SYSC requirements of L&G and AR firm

Supervisor MNSUPSO

7 Supervisor finalises all tracks and confirms adviser is ready to act as an adviser for the Network

Supervisor MNSUPSO

8 L&G receive sign off notification, assess CSmart and Training tracks. CSmart track closed, new one loaded

Legal and General Network

MNHOSO & MNCOMM

Introduction The purpose of this section is to highlight the Training and Assessment programme that needs to be completed by a new adviser. All activities highlighted in this section must be completed before the new adviser can move in to the next stage of development.

Customer contact Supervisors must ensure new Advisers do not contact customers in connection with any activity (including Mortgages) during this stage of the development programme. If an Adviser is currently licensed under wealth, please call Business Standards Team to discuss a concession.

General The Adviser programme is anticipated to last for around 4 weeks, culminating in a residential course. If an adviser has not successfully completed the programme after 3 months then the key personnel within the firm must fully review the progress made to date and make a business decision whether the individual is likely to achieve the desired key knowledge and skills to be able to perform the role of Adviser.

Steps to be completed by Supervisors during this stage:

Preparation for training

Step 1: Training Registration Form & Training track Once we have received the Training Registration Form, the Adviser will be set up on our Learning and Development system. This will allow the Adviser to access various learning materials and tests designed to build their knowledge and skills in preparation for their role, and for the forthcoming adviser programme.

Dependent upon the detail provided on the Training Registration Form, the appropriate learning will be loaded onto their personal learning plan for them to fully complete. This learning will include:

Core “Standards” via computer based training as listed in the Training track Industry awareness online learning and testing Product workbooks

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 7 of 28

Licence assessments All other requirements under the Advisers Training track

Additionally, Lifetime Mortgage Advisers will be required to complete:

The Lifetime Mortgage Marketplace/Industry awareness The Lifetime Advice Standards, including an assessment of knowledge The submission process How to use Fintal (separate course provided by Ferret) Fintal case study, including assessment

All training must be debriefed, and any areas identified as weaknesses must be included in a development plan and re-tested prior to supervisor signing off as ready to progress to commencing the role.

Supervisors must then ensure Advisers have access to the necessary equipment, backup support and literature to enable them to study efficiently.

Step 2: Adviser is registered on and introduced to CSmart Supervisors must ensure that Advisers can access and use the CSmart system. Supervisors must then introduce and coach Advisers on how to use it effectively. Advisers must then be assigned the Recruitment and Initial Training track. (Assign MNIT - Manual)

Step 3: Adviser contact Supervisors are expected to maintain regular contact (at least weekly) with new advisers to ensure they are on course to finish all the required elements of their training track prior to attendance on the residential selling event. There will also be additional learning requirements following the residential course which will also need to be completed prior to you requesting licences.Contact records must be maintained to detail any training and development undertaken by you to assist new Advisers and this must be updated in CSmart. (MNCONTLOG - AUTO)

Step 4: Briefing on the Legal & General Network, Operating procedures and Performance Management System Supervisors must brief Advisers on the L&G Networks Operating Procedures, its contents and requirements, and must include the following areas: Relevant sections of the operating procedures and expected sales process as documented in the ‘What

good looks like’ guidance (appendix 8.0 of the Operating Procedures) The Key Performance Indicators that have to be met to show and maintain competence (and licences) The use of the Personal Activity Log and how this must be completed to display continuing professional

development The expectations of how the individual will be managed including their 1:1’s, use of development plans

and regular observations The standards of integrity and ethics expected by the Network and the FCA

Supervisors must ensure Advisers are fully briefed on the content and requirements of : Advice Standards (Mortgage Advice Standards and Protection and General Insurance Advice

Standards) The expectations about the quality of records kept and standards of advice given

Supervisors must also ensure Advisers are trained on the content of and quality expected within the documents issued to customers including: PSL letters MRoS letters

(MNSUPSO)

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 8 of 28

Step 5: L&G Network Adviser Programme It’s compulsory that all new advisers fully complete the Adviser Programme which will culminate in the requirement to attend the Legal & General residential selling event.

The adviser programme focuses on the skills and knowledge required to perform the role of Adviser. The induction course will introduce the advisers to the Point of Sale system, allow them to understand and test their knowledge of our Sales Quality requirements, and tests the application of skills and knowledge learnt during the training track and induction course, culminating in a role play assessment of a full interview.

Feedback will be provided to the firm following the adviser’s attendance on the induction course, to define any areas of weakness, concern or specific development required.

Should the Adviser fail their assessment, the Supervisor will be required to complete further development, and a subsequent role play assessment (logged onto CSmart) prior to requesting Legal & General approval for granting the relevant licences. Please contact [email protected] who will provide role play case studies. Course activity will be detailed in an event named ADVSPA.

Full details of the requirements of the programme are detailed here – AP Guide 2014. For an overview of the scheme, click here.

Step 6: Business processes and procedures Supervisors must brief Advisers and ensure they understand all the relevant processes and procedures that occur within their business.

The following is a guide to the areas that could be covered but is not exhaustive : Systems & Controls Internal structures including Reporting lines Roles and Responsibilities Processes and Practices Business orientation Complaints and breach procedures

Step 7: CSmart track completion Supervisors must ensure that all relevant events in CSmart are accurate and fully completed and then signed off. Once complete, the Supervisor will need to certify that they believe the Adviser is ready to commence in their role. This will then trigger a request to grant licences, enabling us to review both TLN and CSmart to ensure that we are satisfied with the development to date. No activity must take place until formal confirmation has been received that we have granted licences. (MNSUPSO - AUTO)

Step 8: Moving to Commencing the Role Once the Supervisor has received formal notification that licences have been granted, they must close the Initial Training Track, and assign the Commencing the Role track. Any outstanding development needs should be transferred on to Advisers Development Plan event in the newly assigned Commencing the Role track.

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 9 of 28

AP OVERVIEW.

WEEK 1

Overview of programme via Supervisor, including system access

Sales video review

System and local processes training

F2F sales process

Support systems webinar and link essentials

Self study for CBT

Sit CBT (TLN)

Self study for CBT Sit CBT (TLN)

Sales video review

F2F sales process

Induction programme conference call 1

Study/Sit CBT

WEEK 2

I/O webinar 2

I/O case study (client review)

I/O webinar 3

I/O case study

I/O case study

Product presentations

Study/Sit CBT

Trust toolkit

Lifestyle toolkit/podcast

Induction programme conference call 2

Product presentations

WEEK 3

Product presentations

Study/Sit CBT

Quality of advice and record keeping

Study/Sit CBT

Quality of advice and record keeping

F2F sales process

Mortgage advice and record keeping

Protection advice and record keeping

Mortgage advice and record keeping

Protection advice and record keeping

Induction programme conference call 3

Mortgage advice and record keeping

Protection advice and record keeping

WEEK 4

Attend Residential selling event – day 1

Attend Residential selling event – day 2

Attend Residential selling event – day 3

Attend Residential selling event – day 4

Attend Residential selling event – day 5

WEEK 5

Protection application Webinar

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 10 of 28

4. Commencing the Role

Steps

Step Action Required By Whom Event Name 1 Monthly 1:1s following the

expectations as detailed in Section 13 Supervisor MNA121COM1

2 Observation to be carried out within 3 months, prior to 1 year, and upon leaving the Commencing track

Supervisor MNOBSFORMNEW

3 Record of activity undertaken by adviser, discussed with the supervisor to check if any development areas exist

Adviser/Supervisor UCMLOGAH

4 All MRoS letters checked until 3 consecutive deemed as correct

Supervisor MNMROSCHK/MNROSLTF

5 All PSL letters checked until 3 consecutive deemed as correct

Supervisor MNPSLCHK

6 Minimum of 7 file checks per annum Supervisor FILECHKMP 7 Knowledge and skills must be tested

regularly Advisor/Supervisor MNPAL

8 Ensure relevant learning and tests are undertaken when requiring to add a licence. Checks on business written following granting of licence

Supervisor MNACONTACT

9 Supervisor requests competence status review by PoCC/APER

Supervisor/PoCC MNCAS

10 Close Commencing Track and open Continuing Track

Supervisor MNCONT

Introduction The purpose of this section is to highlight the live field activity that must be completed so Advisers can progress towards, and be assessed as Competent in their role. All activities in this section must be completed before Advisers can move into the Continuing the Role track.

Commencing the Role process Advisers must spend a period of at least 3 months in this stage of the training programme under ‘appropriate supervision’. This will enable Supervisors to ensure Advisers consistently demonstrate the knowledge, skills, ethics and expertise necessary to act in the role of Adviser. The period is designed to allow a build up of Key Performance Indicators (KPI’s) and the collation of other evidence to support the confirmation of competence (when granted).

The maximum period that Advisers can remain in this track is 18 months. If Advisers have not demonstrated sufficient knowledge, skills, ethics and expertise necessary by this time, then there must be serious consideration given to terminating their contract. If there are any extenuating circumstances in relation to this that may require consideration for concession, please contact the Business Standards Team.

Appropriate Supervision During this track it’s the Supervisors responsibility to ensure that their Adviser develops their skills and knowledge, uses the appropriate sales processes effectively, follows the L&G Network advice standards, and ensures the advice given is appropriate to the customer’s needs.

Any issues raised in respect of sales activity in this period will be documented against both the Adviser and their Supervisor.

Sales Quality Reviews Sales Quality Review Team (SQRT) randomly check Advisers submitted business even whilst they are in Commencing the Role. Although Supervisors will be responsible for ensuring that business conducted by

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 11 of 28

the Adviser is compliant, SQRT are required to randomly sample all business in order to maintain standards of quality and mitigate the risk of future complaints. Steps to be completed by Supervisors during this stage:

Step 1: Monthly 1:1’s Supervisors must complete formal 1:1’s on a monthly basis during this phase of development. They can be conducted either face to face or using remote meeting software. Within any three month period it’s expected that at least one face to face meeting is completed.

Supervisors must pay particular attention to unaccompanied activity and the progression towards competence, as these are specific to this stage of an Advisers progress.

All 1:1’s must be documented fully and recorded on the appropriate event on CSmart.

Please see section 11 for further information on Formal 1:1 meetings.

Step 2: Observations To ensure that Advisers are progressing towards competency, Supervisors must observe Advisers completing a live competent observation of the full sales process within 3 months of entering this stage. In addition, a further observation must take place prior to deciding whether Advisers are ready to move into the Continuing the Role stage.

An annual observation must also take place, should they remain in the track for more than 12 months.

At least one live observation of the full Lifetime Mortgage sales process (if applicable) must be observed every 12 months.

For clarity, if an adviser is in commencing the role for 16 months, they will require 3 observations.

Please see Section 10 for further information on Observations.

(MNOBSFMNEW – AUTO – for recurring obs, Manual for all others)

Step 3: Unaccompanied activity debrief

Advisers must record all unaccompanied activity on a contact note for discussion with Supervisors at regular 1:1’s.

Supervisors must discuss and log all activity undertaken in order to debrief unaccompanied activity including: Completing unaccompanied activity logs and the debrief document on Advisers CSmart record Ensuring that Records of Suitability are completed according to the standards and that advice given is

suitable (if applicable) Ensuring that PSL’s are completed according to the standards and that advice given is suitable (if

applicable) Checking for trends in cancelling and/or replacing existing policies Investigating where problems have been encountered, and arranging coaching as necessary, and

logging on Advisers development plan Discussing what went well or not so well to assess journey to competence, or establish development

needs What additional activity is required (e.g. mentoring, file checks or further observations)(UCMLOGAH - AUTO)

Step 4: Mortgage Record of Suitability letter checks Supervisors must check all Mortgage Record of Suitability letters in conjunction with the POS record (e.g. file check), prior to issue to the customer, until there have been 3 consecutive satisfactory completions. All checks that take place must be logged on CSmart on the MRoS checklist event. Such checks must be undertaken as well as the file check requirements detailed in step 6.

Where Advisers are also licensed in Lifetime Mortgages all POS sales records for these sales must be checked until 3 consecutive satisfactory completions of Records of Suitability.

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 12 of 28

Supervisors must: Review, along with Advisers, any Records of Suitability you have rejected and highlight any areas

where the requirements (as described in the suitability checklist) are not met or the customer outcome is not appropriate

Agree action that needs to be taken by new Advisers before it’s re-submitted to the Supervisor Agree development activity that needs to be taken to prevent the same issues arising in the future and

log in Advisers development plans.

(MNMROSCHK – Standard Mortgages- Auto) and (MNROSLFT – Lifetime Mortgages – Auto)

Step 5: Protection Suitability letter checks. Supervisors must check all Protection Suitability letters, in conjunction with the POS record (e.g. file check), prior to issue to the customer, until there have been 3 consecutive satisfactory completions. All checks that take place must be logged on Advisers CSmart track on the PSL checklist event. Such checks must be undertaken as well as the file check requirements detailed in step 6.

Supervisors must: Review, along with Advisers, any Protection Suitability Letters you have rejected and highlight any

areas where the requirements as described in the suitability checklist are not met or where the customer outcome is not considered appropriate

Agree action that needs to be taken by Advisers before re-submission to the Supervisor Agree development activity that needs to be taken to prevent the same issues arising in the future and

log in Advisers development plans

(MNPSLCHK - Auto)

Step 6: File checks Supervisors must check a minimum of 7 cases per annum. These must be conducted as follows:

1 case per quarter (4 per annum) Plus, at any point in the year, a further 3 consecutive cases must be checked to determine whether

any poor practices or selling trends are noticeable. However, if the production of the Adviserexceeds 150 cases over a rolling 12 month period, you must check an additional 3 trend analysischecks (e.g. total cases checked = 10)

Where the Quality of Advice rate of the Adviser is published at less than 50%, additional file checks will be expected to be completed by the Supervisor in order to establish the root causes of the issue.

File checks must be:

Full case reviews (i.e. full assessment of the record and the sale, and with mortgages and protectionfor the same customer(s) classed as one sale)

Across the full range of products and licences used by the Adviser An assessment of the quality of record keeping and the advice given

Comprehensive case checklists are available from the AR Centre here These checklists must be scanned and attached to the summary of results in the event FILECHKMP in CSmart.

Outcomes must be discussed at 1:1 meetings and any actions arising must be fully documented in both the 1:1 document and development plans as necessary.

(FILECHKMP - Manual)

Step 7: Maintenance of Knowledge and Skills

Supervisors must ensure that Advisers complete the Personal Activity Log with all relevant learning and activities including product and compliance updates prior to each 1:1. Continuing Professional Development should be measurable as well as relevant, and consider learning outcomes.

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 13 of 28

As part of the monthly 1:1 process Supervisors need to: Debrief all entries and test Advisers knowledge of these updates Highlight and log any development areas Ensure there’s a balance of knowledge and skills Validate the activity documented on the Personal Activity Log is accurate Where learning activity documented is minimal, Supervisors must remind Advisers of their duty under

CPD and log in 1:1 as necessary

Team events on PALs may be of a templated nature, provided that individual content is added to this, but the content of all entries must be tested and validated by Supervisors. (MNPAL – Auto)

Step 8: Additional Licences Should any additional licences be required, Advisers must complete all of the relevant stages from Initial Training and Commencing the Role for that licence, eg. Relevant study and product tests, Role play and/or observation of the recommendation and presentation part of the sales process, check written business for content, accuracy and outcome, and check MRoS/PSL’s (depending on the licence added) before issue to the client until 3 consecutive checks are correct.

Step 9: Competence Status sign-off Once all requirements in this stage have been successfully completed, and Supervisors are satisfied Advisers are displaying the desired behaviours associated with competency, and maintaining their level of performance in all areas, they will need to ensure that CSmart records are fully completed and up to date. If the CSmart record successfully demonstrates that the requirements detailed within this section have been successfully completed and that the monitoring and assessment to date doesn’t indicate that any further development is required, the relevant section of the Competence Status request event must be completed and signed off by the Supervisor.

Notification should be then sent to the firms PoCC who needs to review the CSmart record and must countersign the Competence request only if all criteria has been satisfied and they are satisfied that competence has been consistently demonstrated. Where the Supervisor and PoCC are the same person, the Approved Person in the firms should validate the competence request. In the event the Supervisor and PoCC is also the Approved Person you should refer to the Business Standards Team for approval. (MNCAS – Auto)

Step 10: CSmart track completion Supervisors must ensure that all relevant events in CSmart are completed and signed off. Once competence has been confirmed by the PoCC, Supervisors must ensure they fully complete and close the Commencing the Role track prior to assigning the Continuing the Role track in CSmart. (Close MNCOMM and assign MNCONT – Manual)

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 14 of 28

5. Continuing the Role

Steps

Step Action Required By Whom Event Name 1 Quarterly 1:1s following the

expectations as detailed in Section 13

Supervisor MN121CONT

2 Observation to be carried out every 12 months

Supervisor MNOBSFORMNEW

3 Minimum of 7 file checks per annum

Supervisor FILECHKMP

4 & 5 Although Adviser is now deemed competent, knowledge and skills must be tested regularly

Advisor/Supervisor MNPAL

6 Ensure relevant learning and tests are undertaken when requiring to add a licence. Checks on business written following granting of licence

Supervisor MNACONTACT

Introduction The purpose of this section is to highlight the activity that needs to be completed so Advisers can maintain competence in the advisory role. All activities highlighted in this section must be completed on an ongoing basis.

Continuing the role process Advisers have now proved that they can operate to the required standards. It is essential the knowledge, skills, ethics and expertise acquired in the previous stages remain consistent or improve, as this will ensure they perform effectively and successfully in the role of Adviser.

To maintain competence Supervisors must review Advisers performance against the knowledge and skills for the role on a regular basis (See section 9). The procedures detailed on the following pages provide the framework for enabling effective management of competence.

Steps to be completed by Supervisors during this stage:

Step 1: Quarterly 1:1’s Supervisors must complete formal 1:1’s with Advisers on a quarterly basis. These formal 1:1’s can be conducted either face to face, telephone, or using remote meeting software. Within a 12 month period it’s expected that at least 2 face to face/remote ‘webcam’ style meetings are completed. All formal 1:1’s must be fully documented and recorded on the appropriate event on CSmart.

Please see section 11 for further information on Formal 1:1 meetings.

Step 2: Observations Advisers must be observed completing at least one competent live observation every 12 months from the date of entering the Continuing the Role track, of the full sales process. This can be completed in parts or in totality.

The Lifetime mortgage sales process must be observed separately (if applicable).

Please see Section 10 for further information on Observations.

(MNOBSFMNEW - AUTO)

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 15 of 28

Step 3: File checks Supervisors must check a minimum of 7 cases per annum. These must be conducted as follows:

1 case per quarter (4 per annum) Plus, at any point in the year, a further 3 consecutive cases must be checked to determine whether

any poor practices or selling trends are noticeable. However, if the production of the Adviserexceeds 150 cases over a rolling 12 month period, you must check an additional 3 trend analysischecks (e.g. total cases checked = 10)

Where the Quality of Advice rate of the Adviser is published at less than 50%, additional file checks will be expected to be completed by the Supervisor in order to establish the root causes of the issue.

File checks must be:

Full case reviews (i.e. full assessment of the record and the sale, and with mortgages and protectionfor the same customer(s) classed as one sale)

Across the full range of products and licences used by the Adviser An assessment of the quality of record keeping and the advice given

Outcomes must be discussed at 1:1 meetings and any actions arising must be fully documented in both the 1:1 document and development plans as necessary.

(FILECHKMP - Manual)

Step 4: Maintenance of Knowledge and Skills Advisers must complete any centrally issued certifications assessments of key knowledge and skills. This training will be issued via the relevant Training System. Failure to take the assessment(s) on or before the due date may result in removal of licences

It’s important that all designated individuals carry out and evidence this training within the timescales given with each module. Computer Based Training Modules can also be used periodically to carry out refresher training.

By using CSmart and Training Systems, Supervisors can then track and ensure that all key knowledge updates delivered by these systems are completed as required.

Supervisors must ensure that Advisers complete the Personal Activity Log with all relevant learning and activities including product and compliance updates prior to each 1:1. Continuing Professional Development should be measurable as well as relevant, and consider learning outcomes.

As part of the monthly 1:1 process Supervisors need to: Debrief all entries and test Advisers knowledge of these updates Highlight and log any development areas Ensure there’s a balance of knowledge and skills Validate the activity documented on the Personal Activity Log is accurate Where learning activity documented is minimal, Supervisors must remind Advisers of their duty under

CPD and log in 1:1 as necessary

Team events on PALs may be of a templated nature, provided that individual content is added to this, but the content of all entries must be tested and validated by Supervisors. (MNPAL – Auto)

Comprehensive case checklists are available from the AR Centre here These checklists must be scanned and attached to the summary of results in the event FILECHKMP in CSmart.

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 16 of 28

Step 5: Maintenance of Knowledge and Skills (Lifetime Mortgages)

Supervisors must review Advisers knowledge and skills around the Lifetime Mortgage Marketplace every six months to ensure there’s no deterioration in the knowledge or skills.

At least 3 Lifetime sales are expected within a 12 month period in order to retain the Lifetime licence. If sales of Lifetime Mortgages are less than this, the licence may be removed (please refer to Review of Performance (production and licence activity) in Section 11: Formal 1:1’s. Step 6: Additional Licences Should any additional licences be required, Advisers must complete all of the relevant stages from Initial Training and Commencing the Role for that licence, e.g. Relevant study and product tests, Role play and/or observation of the sales process, check files for content and accuracy, and check MRoS/PSL’s (depending on the licence added) before issue to the client until 3 consecutive checks are correct.

The event MNTR (training event) must be used in CSmart to indicate any additional training that has been received, specifically in relation to product training and process training (e.g. CAU referral process).

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 17 of 28

6. Requirements of L&G Network enforced Increased Individual Supervision

The L&G Network takes it regulatory responsibility very seriously and the effective supervision of Advisers is of paramount importance. If we deem it necessary, Adviser’s will be placed under enhanced supervision and oversight. The reasons for this may include one or more of the following:

An Adviser who is experiencing or has experienced financial difficulties Where concerns are identified about an Advisers sales practices or record keeping Where lenders have notified us of concerns with the quality of an Adviser’s submitted business

This will result in the SYSC team assigning additional tasks which the Supervisor will be required to carry out in order to satisfy the L&G Network that the selling practices of the Adviser are consistent with expectations. These additional events will be logged on a separate track and may include, but are not limited to:

More frequent 1:1 meetings Additional file checks Customer contact programs Additional analysis of sales based on certain KPI’s and KRI’s Completion of unaccompanied activity logs Additional or more in depth Fiscal Probity questionnaires

All of the above are in addition to the requirements detailed elsewhere in this scheme.

(EHSTRACK1 or EHSTRACK2 – Legal & General risk and controls will load relevant track)

7. Enhanced Supervision

Enhanced supervision must be considered by the firm where:

3 or more Key Performance Indicators are at Amber and/or any Key Performance Indicator is at Red.If you deem that enhanced supervision is necessary then this may include: Root Cause Analysis (e.g. client contact, pipeline audit, review of submissions, review of previous

observations etc) Development Needs Analysis to create a Development Plan addressing KPI problems and

agreeing development areas based on highest risk. Action plans from the Development Plan may include:

a) Increased contact activityb) Monthly reviews of action plansc) Additional case reviewsd) Observations

Legal & General’s Systems and Controls Team may impose a higher level of supervision based on their own risk assessments, see Section 6 - Requirements of Increased Individual Supervision.

8. Supervisors moving to Adviser Status (or vice versa)

Any requests to move existing L&G Network Supervisors into Adviser roles (or Advisers moving to Supervisor status) must be referred to the L&G Network Business Standards Team who will give details of the training path to follow.

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 18 of 28

9. Supervision of close relatives

Advisers should not be supervised by family members. However in some Firms this may be unavoidable. Therefore in such cases to mitigate any possible conflicts of interest between the Adviser and the Supervisor the following additional controls are required:

Step 1: Notification of the relationship The L&G Network Firm or Key Account Manager (KAM) must advise the L&G Network Business Standards Team of the nature of any relationship

Step 2: Additional checks to be carried out by the Business Quality Consultants. BQC to complete an assessment check of the ongoing monitoring of advisory skills i.e. Observations,

Sales Quality, record keeping, knowledge retention BQC to validate development activity in relation to maintaining knowledge and skills

Family members are defined as being :- spouse, brother, sister (including step-brothers/sisters) parent, grandparent, cousin, uncle, aunt, niece and nephew. (Note: this list is not exhaustive, if in doubt, please contact the L&G Network Business Standards Team)

10. Adviser - Long Term Sickness and Maternity Leave

In the event that Advisers are absent long term (3 months or more) due to sickness or on maternity leave, the following steps must be taken (depending upon the period of absence) :

Period of absence:

3-6 months The Advisers track on CSmart must remain open, however Supervisors must manually void any

mandatory events such as 1:1’s, observations etc if necessary (the notes must reflect the period of absence and the reason). Observation events must be added back in to reflect when the yearly observation should be due.

Supervisors must conduct an analysis of any development needs, and a Development Plan must bebuilt (and CSmart event completed accordingly) and must include:

Knowledge retention checks Product licence MOT checks Evidence of Adviser reading and understanding all Regulatory and Technical updates issued

during the period of leave, and their PAL’s must be validated to evidence understanding

6-12 months Supervisors must immediately send an email to [email protected] advising them of the absence

and requesting that Advisers tracks on C-Smart are closed.

Once returned to work, Supervisors must request via [email protected] that Advisers arereinstated on CSmart.

Advisers must initially enter into the Commencing the Role track until the knowledge and skills arerefreshed.

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 19 of 28

Supervisors must conduct an analysis of any development needs, and a Development Plan must bebuilt (and attached to CSmart) and must include:

Knowledge retention checks Product licence MOT checks Ensure Adviser reads and understands all Regulatory and Technical updates issued during the

period of leave, and PAL’s validated to evidence understanding

Once Supervisors are satisfied that Advisers have demonstrated the required knowledge, skills, behaviours and abilities detailed above then the Adviser can return to their role as a competent Adviser for the L&G Network.

12 months or more Supervisors must send an email to [email protected] advising them of the absence once 6

months has elapsed, requesting that Advisers tracks on C-Smart are closed.

In the event of Advisers being absent for 12 months or more they will be assigned with an “InitialTraining” track until all areas of knowledge and skills are satisfactorily refreshed, and then into‘Commencing the Role’.

The Return to Work Check Sheet must be completed to identify any areas where Advisers may need torefresh their knowledge following the period of absence.

Any areas identified requiring improvement must be recorded on a Development plan.

Review of Knowledge and Skills includes but is not limited to : Product licence MOT checks Appropriate exams passed Significant changes affecting the Industry communicated, i.e. Regulation, Taxation, New

Products All the “Standards” computer based training is up to date i.e. DPA, Complaints, Anti Money

Laundering Ensure that all Technological and Regulatory communications issued during the period of leave

have been read and PAL’s validated to evidence understanding Refresher training provided on all internal AR systems i.e. Launchpad, C-Smart, General IT

skills Observations of the full sales cycle 3 consecutive successful MRoS checked and logged 3 consecutive successful PSL checked and logged

(MNRTWCHK - Manual)

Supervisors can only complete a Competent Status request once they are satisfied that all of the aboveareas are complete, or at the required level, and:

Training and development programme is complete Monitoring and assessment doesn’t indicate any further development in respect of competence

The relevant section of the Competence Status Request must then be completed and signed by the Supervisor, notification sent to the firms PoCC, who needs to review the record and countersign the Competence Status Request providing that all the above criteria has been satisfied. Where the Supervisor and Point of Compliance contact are the same person the Approved Person must validate the competence request. In the event that the Supervisor is also the Approved Person, you must refer this to the L&G Network Business Standards Team.

Once competence status has been confirmed, the Adviser can then move back into “Continuing the Role”.

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 20 of 28

11. Key knowledge and skills grid

The table below details the key knowledge and skills that we would expect Advisers to have in order to be assessed as competent in their role. It is also aimed at providing Supervisors with the methods of measuring that Advisers have the relevant knowledge and skills to be judged as or remain competent.

Knowledge / Skill Areas required Possible ResourcesProduct Knowledge Mortgages

Protection GI Qualification – appropriate

exam

Workbooks Mock exams CII Website/Manuals/CBTs CeMAP/CF6 Manuals The Learning Network

Industry Knowledge FCA/Regulatory knowledge Govt. / Taxation/Trusts Competitors

Internet FCA Website CII Website CeMAP/CF1 Manual Training systems AR Centre

AR Operating Procedures and Standards

Approved Persons andSystems and controls

L&G Market Place /Relationship

Performance Management Anti Money Laundering Data Protection Act Breach Procedures Complaints Appropriate customer

outcome

Induction Reports and accounts Office orientation and briefing by

manager Performance Management

System Training systems/TLN Operating Procedures CBT’s AR Centre

IT / Systems Point Of Sale system CSmart Internal AR systems Training Systems

Manager briefing Watching an expert TLN/Training systems Induction Course

L&G Network Sales Process

Questioning skills Communication skills Presentation skills Listening skills Factfinding skills Prospecting Letter Writing skills Appropriate customer

outcome

Workshops Record Of Suitability checking Demands and Needs checking Full, themed or risk-based file

checking Observation of the Sales Cycle Computer Based Training What good looks like Sales

process document

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 21 of 28

12. Observations

Observations are an essential tool for Supervisors to assess how Advisers are performing and to ensure that customers are receiving an excellent service, and a journey that complies with all regulatory requirements. The Supervisor can then create effective development and action plans to ensure consistent and sustained improvement. It’s important Supervisors give appropriate feedback to Advisers following any observation.

Standard Mortgages, Life and Health Protection, and Property and Contents can be observed as one sale, Lifetime Mortgages (if applicable) must be conducted as a separate observation. The standard observation forms provided by L&G Network must be used to assess Advisers (see Appendix 1.2 of the Operating Procedures).

All required observations carried out must be logged in CSmart under the event (MNOBSFMNEW), and follow up process must include a full review of the sales documentation within 1 month of the observation taking place (except where it is conducted as a role play).

Competent Sales Definition is: 1) Adviser must achieve 100% of all documented mandatory areas assessed as competent (or

competent with development needs) and 2) Adviser must achieve 70% of all other documented requirements assessed as competent (or

competent with development needs).

If Advisers are deemed as not competent in any mandatory area (definition 1 above), no further unaccompanied activity can be undertaken in that area of the sales process until remedial action has been completed and Advisers have been confirmed as competent through observation of that part of the sales process.

If the result is as per definition 2 above, further training must be undertaken to bring them up to the required level and further observation of that stage of the sales process must be conducted.

Supervisors can observe 2 out of the 4 stages via role play (except for the first required observation in the commencing the role stage) with the remainder being deemed competent via live observation. If the previous observation had a role play element in it, that same part cannot be role played in the next observation, it must be seen in a live situation (for example if parts 1 and 2 were role played last time, they must be observed live when next due).

The file check documentation must then be attached to CSmart (FILECHKMP). Evidence gained during the observation must be scanned and attached to the observation event in CSmart, (where this is not possible then the paper record must be retained).

Role plays must be assessed using the approved role plays available from Training department. Please contact [email protected] who will provide full details. Best practice is for 3 people to be involved in role plays, leaving Supervisors to purely observe and document.

Only the Supervisor who has observed the Adviser should sign off and complete theObservation event in the Advisers track.

Any concessions relating to the due date of observations must be referred to the L&G NetworkBusiness Standards Team in good time prior to the date that the concession is needed.

WARNING –Observation events annually recur from the date of entering the track. It is the supervisors responsibility to ensure that observations take place within the timeline described within this scheme.

(MNOBSFMNEW) Mortgage and Protection (any additional Observations can be carriedd out by adding further MNOBSFMNEW events to the Advisers track). (MNOBSLF1IAN…MNOBSLF2FF…MNOBSLFPR…MNOBSLF4CL - Manual) Lifetime

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 22 of 28

13. Formal 1:1 meetings

The 1:1 meeting must cover: Review of previous 1:1 and review of outcome of action points raised from this Review of Performance (production activity) Review and Update of Study plan (if applicable) Review Progress towards competence (if applicable) Unaccompanied activity debrief (including non-sales) Review of any Introducers of business to the adviser (business levels and quality – assessing any

potential risk) Management Information and Key Performance indicators Personal Activity Log (check of knowledge gained and validation) Review of file checks completed Review of observations carried out (if applicable) Review/test regulatory and technology updates Review and update development plan on CSmart to include any outcome from this 1:1 Fiscal Probity (Quarterly)

Supervisors must include full details of their discussion with Advisers within or attached to the appropriate 1:1 event in CSmart.

MN121IT – Initial Training MNA121COM1 – Commencing the Role MN121CONT – Continuing the Role – All auto

Review of previous 1:1 and review of outcome of action points raised from this

Supervisors must review the previous 1:1 to address any outstanding action points or issues. Where these remain outstanding, these should be addressed and/or added to Advisers development plans.

Review of Performance (production and licence activity)

Review of performance must include penetration ratios to assess how the adviser uses all products within the licences held.

Where use of product knowledge or use of licences isn’t evidenced within a 6 month period, you must:

identify areas where the product/licence knowledge has not been evidenced within the previous 6months

agree appropriate action with the adviser including what learning should be undertaken Re-test knowledge in areas where licence not used for 6 months review these actions at 1:1s and document in CSmart Check first 2 sales records after licence used (PSLs and/or MRoS)

As it is a requirement of the Protection Advice Standards that you must attempt to discuss the customers protection needs, removal of a licence should be considered a last resort, once the above measures have been exhausted. If removal is the only option:

Consider whether termination or licence removal will provide the better business solution If removing, advise Training department to ensure licences and linked learning are removed Additionally, inform the Business Standards Team how protection business will be generated or dealt

with following licence removal

Supervisors must also assess whether each individual licence is being used on a regular basis, for example, where no protection is sold for a 12 month period, the removal of protection licences must be

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 23 of 28

considered as the Adviser holds a higher risk due to lack of activity in this field (e.g. observations are not being carried out on protection, no KPI data available and less likely to be keeping up with regulatory changes in this field). In addition, if more than one product is linked to a licence, you should ensure that the Adviser is competent (by testing knowledge and skills) in all of the product areas within that licence. The alternative to this is moving back to Commencing the Role due to inability to prove competence.

These decisions may also be taken by L&G Network where necessary.

Review and update of study plan (if applicable)

Supervisors must review Advisers ongoing study plan to ensure timescales are being achieved and Advisers are studying efficiently to reach target (if applicable). Any gaps identified should be added to Advisers development plans.

Review Progress towards competence (Advisers in commencing the role)

Supervisors must review Advisers progress towards competence, set action plans or development plans to assist Advisers and make them aware of the outcomes required for them to achieve competence.

Unaccompanied activity debrief (Advisers in commencing the role)

Advisers must record all unaccompanied activity on a contact note for discussion with Supervisors at 1:1’s. Supervisors must debrief all unaccompanied activity (including non-sales) and: Complete unaccompanied activity logs and the debrief document on Advisers CSmart records Ensure that Records of Suitability are completed according to the standards and that advice given is

suitable (if applicable) Ensure that PSL’s are completed according to the standards and that advice given is suitable (if

applicable) Check for trends in cancelling and/or replacing existing policies Investigate where problems have been encountered, and arrange coaching as necessary, and log in

Advisers development plans Discuss what went well or not so well to assess journey to competence, or establish development

needsWhat assistance needs to be called upon if required, for example mentoring, further observations etc (UCMLOGAH - AUTO)

Activity debrief

Supervisors must investigate areas of Advisers activities to identify problems or highlight opportunities in order to increase Advisers Productivity. Any development areas must be logged in Advisers development plan.

Management Information (MI) and Key Performance Indicators (KPI)

Supervisors must review Advisers performance against the standards required by the L&G Network at each 1:1. The Key Performance Indicators and Management Information to be reviewed are: Production / Add-Ons (including individual product sales) Product Mix Lender Spread Mortgage Product types Market Areas (all remortgage/FTB/Equity Release) Rejected or referred cases (SQ) Non-Disclosure Persistency CFO’s NPW’s Complaints Breaches Mortgage Key Risk Indicators

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 24 of 28

Supervisors must first review the KPIs above. This will require confirmation that the rates are at the required level and whether there’s a positive or stable trend. If they’re not or there’s a negative trend, then Supervisors must document the action that is to be taken and the effect the action should have on Advisers future performance.

In addition Supervisors need to look at trends across different KPI’s and to determine if any development activity is required, even if each single KPI or MKRI is at the required standard.

KPI’s are only indicators to what might be occurring with Advisers business. It must be investigated accordingly, and the result must be documented, regardless of whether there’s an issue found. All Red KPI’s must be investigated and then appropriate action taken, for example development plan, action plan or increased observations.

Details of these discussions and confirmation of KPI data must be documented in Advisers 1:1 on CSmart.

See section 13 for full details of KPI benchmarks.

Personal Activity Log (PAL) check of knowledge gained and validation Supervisors must ensure that Advisers complete the Personal Activity Log with all relevant learning and activities including product and compliance updates prior to each 1:1. Continuing Professional Development should be measurable as well as relevant, and consider learning outcomes.

As part of the monthly 1:1 process Supervisors need to: Debrief all entries and test Advisers knowledge of these updates Highlight and log any development areas Ensure there’s a balance of knowledge and skills Validate the activity documented on the Personal Activity Log is accurate Where learning activity documented is minimal, Supervisors must remind Advisers of their duty under

CPD and log in 1:1 as necessary

Team events on PALs may be of a templated nature, provided that individual content is added to this, but the content of all entries must be tested and validated by Supervisors. (MNPAL – Auto)

Review of file checks completed

Supervisors must debrief Advisers on any files checked to ensure Advisers are aware of trends or material issues that need addressing (including SQRT checks). Supervisors must consider coaching Advisers in areas of shortfall to eradicate common errors. These discussions should be documented in the 1:1, and any actions arising should be documented in Advisers development plans.

Review of observations carried out (if applicable) Supervisors must debrief any observations (including call monitoring where applicable) carried out in the previous period. These discussions should be documented in the 1:1, and any actions arising should be documented in Advisers development plans.

Regulatory and technology updates

Supervisors must ensure Advisers have updated systems where applicable, and make sure that any regulatory updates have been implemented and embedded in the Advisers normal practice and test their knowledge in relation to these updates. These discussions should be documented in the 1:1, and any actions arising should be included in Advisers development plans.

Review and update Development Plans

Supervisors must review Advisers ongoing development plans at each 1:1 (even if there are no additional development needs), ensure that any outstanding items have been addressed, and amend and update as necessary with any further development needs. This review must cover: Activity completed Further areas of development established Activity required to meet new/amended development areas

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 25 of 28

Each year a new development plan event will automatically drop onto the Advisers track. Only 1 live development plan must be open at any time. The existing event must therefore be closed and any ongoing developments must be transferred across onto the new development plan. (MNDNADP – Auto)

Fiscal Probity (Quarterly)

As part of the fiscal probity check the Adviser must be asked the following: Whether they have any County Court Judgments (CCJs) or any other bad debts, and include numbers,

amounts and expected settlement dates Whether there are any other financial concerns

In instances where Supervisors have concerns, a copy of the review/report must be forwarded to the Credit Management Team ([email protected]), Network Operations ([email protected]) and your Firms Business Quality Consultant BQC). If the Firm wishes to retain the Adviser then they must put forward a robust action plan for monitoring future sales to the BQC and the L&G Network Business Standards Team.

Once all the information is received a decision will be made on the retention of the Adviser and this will be communicated to the Firm. Where remedial actions have been agreed, full details of agreed actions must be recorded on CSmart and signoff must be obtained from the Business Quality Consultant that all activities have been appropriately covered.

The Credit Management Team will contact the advisor periodically (timescales to be agreed depending upon the severity of the individual case) to confirm the issues are being dealt with. There may also be additional requirements as documented in Section 6 - Requirements of Increased Individual Supervision (Event – MNFV)

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 26 of 28

14. Key Performance Indicators and Management Information Standards

Each KPI is benchmarked. The benchmarks given are subject to change as and when deemed necessary by the Legal & General Network. Key Performance Indicators will flag a Green, Amber, or Red status. Monitoring of these will be based upon agreed standards.

NOTE – THESE ARE ONLY INDICATORS WHICH MAY OR MAY NOT INDICATE THAT A PROBLEM EXISTS. SUPERVISORS MUST THEREFORE INVESTIGATE ANY ROOT CAUSE TO ESTABLISH IF THERE ARE ANY SUCH PROBLEMS THAT REQUIRE FURTHER ACTION.

Production / Add-Ons One of the key performance indicators is productivity (including add-on’s). It’s important to establish the root cause of any underperformance in order to agree an appropriate action plan to provide a sustained improvement.

When reviewing Supervisors must: analyse Advisers production against target establish the cause of below target production review levels of leads from lead source review other KPI’s to determine if there are common areas where issues arise set and agree revised targets

Standard (Rolling 12 month NIC) Measure Best Practice GREEN AMBER RED Production £25000 >£20000 £15000-£20000 <£15000

Product Mix When reviewing product mix Supervisors must: analyse the monthly product mix statistics analyse local records demonstrating range of advice identify products that have not been sold for 6 months or more analyse trends in relation to changes in product mix ratios analyse reasons for changes in product mix review other KPI’s to determine if there are common areas where issues arise

Standard (Monthly / Quarterly / Rolling 12 month) Measure Best Practice GREEN AMBER RED Mortgages – L2M >70% >50% 35% - 50% <35% Protection – - Term + CIC - IPB - ASU

>70% >25% >25%

>40% >10% >10%

20% - 40% 5% - 10% 5% - 10%

<20% <5% <5%

General Insurance – GI2M >60% >50% 35% - 50% <35%

Lender Spread / Mortgage Product Types / Market Areas When reviewing these areas Supervisors must: analyse whether there are particular lenders being used too regularly analyse the spread of lenders used analyse Advisers knowledge of lenders who offer similar products analyse where there has been use of a small group of lenders only analyse whether only particular products are being recommended analyse whether all clients are in one market area such as re-mortgage, FTB, debt consolidation or

equity release

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 27 of 28

Cases reviewed by Sales Quality Review Team (SQRT) When reviewing, Supervisors must: discuss all cases reviewed by SQRT in the previous period, analyse the ratings given for those cases,

especially those which required clarification or had material issues and analyse if there is a trend (low income, wrong lender being used)

review complete sales records carry out root cause analysis to identify reasons if standard is Amber all cases to be checked until 3 consecutive satisfactory completions if standard is Red Supervisors should perform 100% checking to be completed until status of KPI

altered

Standard (Rolling 3 Months) Measure Best Practice GREEN AMBER RED Technically Clean rate 100% <70% 50% - 69% >50%

Non Disclosure When reviewing Supervisors must: review how many instances have occurred in last 3/6/12 month periods investigate why the non-disclosure has occurred revisit product knowledge observe the sign up stage of a live sale

Standard (Monthly) Measure Best Practice GREEN AMBER RED Non Disclosure 0 0 1 >1

Persistency / CFO’s / NPW’s When reviewing Supervisors must: discuss all individual CFO’s, NPW’s, Lapses, and cancellations with Advisers check a cross section of files for trends in cancelling existing policies and replacing previous policies consider whether there was sufficient contact post sale in order to ensure the client was retained consider whether anything more could have been done during or post sale to prevent the lapse review other KPI’s to determine if there are common areas where issues arise

Supervisors must review CSmart KPI data and assess the most recent quarters figures against the table below. For example if the Q1 figures are not yet available, then review the previous Q4 figures.

Standard (Persistency / CFO – 12 & 24 months, NPW – 12 month)

Measure Best Practice GREEN AMBER RED Cumulative Figures Persistency - 12 mth Persistency – 24 mth

>92% >85%

>90% >75%

90% - 85% 65% - 75%

<85% <65%

CFOs – 12 mths CFOs – 24 mths

<5% <5%

<10% <10%

10% - 20% 10% - 20%

>20% >20%

NPWs – 12 mths <15% <25% 25% - 40% >40%

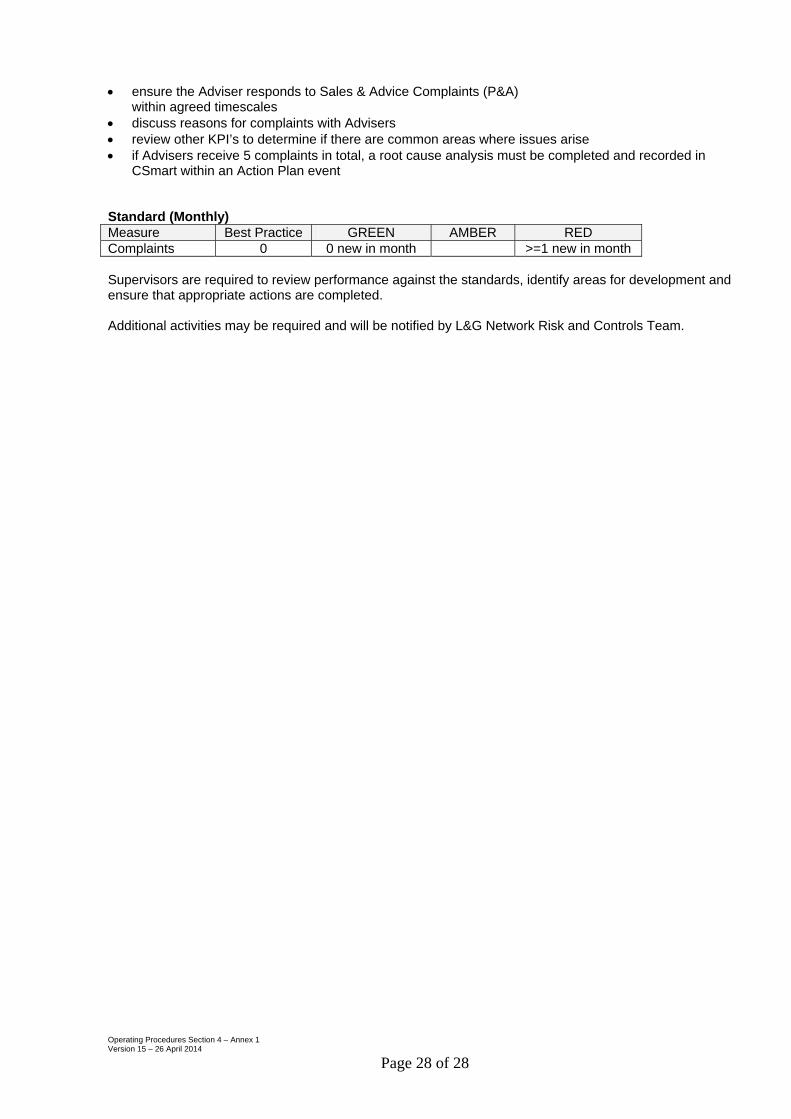

Complaints When reviewing Supervisors must: investigate whether any complaints have been received previously analyse the complaints made to determine if there is a trend discuss why the complaint arose ensure any areas where a trend has been identified are discussed with Advisers

Operating Procedures Section 4 – Annex 1 Version 15 – 26 April 2014

Page 28 of 28

ensure the Adviser responds to Sales & Advice Complaints (P&A)within agreed timescales

discuss reasons for complaints with Advisers review other KPI’s to determine if there are common areas where issues arise if Advisers receive 5 complaints in total, a root cause analysis must be completed and recorded in

CSmart within an Action Plan event

Standard (Monthly) Measure Best Practice GREEN AMBER RED Complaints 0 0 new in month >=1 new in month

Supervisors are required to review performance against the standards, identify areas for development and ensure that appropriate actions are completed.

Additional activities may be required and will be notified by L&G Network Risk and Controls Team.