the institute of chartered accountants of india (setup … · 2014-05-15 · rise above the storm...

TRANSCRIPT

Rise above the storm andyou will find the sunshine

The Institute of Chartered Accountants of India(Setup by an Act of Parliament)

VOLUME - II 2013l MARCH

THE INSTITUTE OF CHARTERED

ACCOUNTANTS OF INDIA

Tel. :

E-mail :

Web :

WESTERN INDIA REGIONAL COUNCIL

Tel. :

Email :

Web :

BARODA BRANCH OF WIRC OF ICAI

Telefax :

E-mail:

Web :

ICAI Bhawan, Post Box No. 7100,

Indraprastha Marg, New Delhi - 110002.

+91 (11) 39893989

www.icai.org

ICAI Bhawan, 27, Cuffe Parade,

P O Box No. 6081, Colaba, Mumbai - 400 005.

+91 (22) 39893989

www.wirc-icai.org

“ICAI Bhawan”, Kalali-Tandalja Road,

Atladra, Vadodara - 390 012.

+91 (265) 2681115 / 2680593

www.baroda-icai.org

Chairman's Message

Managing Committee

CA. Ashish Parikh CA. Kejal Pandya

CA. Vishal Doshi CA. Ashok Thakkar

CA. Bimal Bhatt CA. Neena Patel

CA. Tejal Parikh

CA. Ashish Parikh

CA. Nayan Kothari

CA. Pradeep Agrawal

CA. Yash Bhatt

CA. Viral Shah

CA. Abhishek Nagori

98252 31545

98244 33445

98985 60967

99243 88339

98243 62211

94260 75397

CA. Arpan Dodia 98983 83530

CA. Dhiren Parikh 93762 11099

CA. Kejal Pandya 98259 77220

Chairman

Vice Chairman

Immediate Past Chairman

Secretary

Treasurer

Ex-officio

Members

Editorial Team

` 20/- COPY

Index

Sudha Murthy, believer of simplicity in life, better known as Narayana Murthy's

wife, from being the first female computer engineer in the precincts of the venerable

Tata Group and a prolific author with as many as 25 titles against her name, to

having an impressive body of philanthropic work, she is a woman of many talents.

At 62, and grandmother twice over, she shows no signs of slowing down.

Baroda Branch of Western India Regional Council of The Institute of Chartered Accountants of India

BARODA BRANCH OF WIRC OF ICAI

Respected Members,

At the onset, I feel extremely privileged to

pen down my first communication as the

Chairman of Baroda Branch of WIRC of ICAI which

has entered its 45th year and stays strong with

1500 plus members on its roll.

The Year 2012 achieved new heights under the leadership of

CA. Pradeep Agrawal when several new initiatives were undertaken. I

congratulate him for the successful completion of his tenure.

I am pleased to announce that Baroda branch of WIRC & WICASA

have been awarded as the “Best Branch of ICAI & WICASA - “BEST

Students’ Association” for the year 2012 at ICAI level and at WIRC

level. I congratulate “TEAM – 2012” of managing committee and

my team at WICASA-2012 for their incredible success .

My journey for the year 2013 is based on philosophy of

“Leaving a Lasting Legacy ”. The way I mean legacy is, ”Legacies are

rare and special gifts, from one person to another, from one

generation to the next” It comes from the idea that everyone,

regardless of rank or position, can make a difference. Legacies

encompass the past, present and future, and force us to consider

where we have been, where we are now and where we're going.

My focus areas for the year would be to lay more emphasis on

conducting intensive courses like International Taxation, Valuation

and Seminars , etc. with subject matter which can include

conservative as well as futuristic issues.

In the month of February, 2013 two mega events were organized,

one of them with Reserve Bank of India. In the month of March 2013,

we have several programs along with most awaited Budget 2013

lined up which are detailed in the newsletter and I hope to see

members taking advantage of the same.

I congratulate our female CA members for their overwhelming

response to our idea of publishing all articles of this newsletter by

only female members, keeping in mind the International Women’s

Day. My heartfelt thanks to all contributors.

My dear members “I’m not a perfect man, I’ll never be a perfect

Chairman, but what I promise you that I will … wake up every single

day, working wholeheartedly for you, Baroda Branch and mother

ICAI as hard as I can,... And I will keep this promise... With three great

essentials to achieve anything worthwhile, first, hard work; second,

stick-to-itiveness; third, common sense.”

With warm regards.

Chairman - 2013

CA. Ashish Parikh

ICAI Office Torch Bearers ... 2

WIRC Office Torch Bearers ... 2

Due Date Planner ... 2

Forthcoming Events ... 3

Income Tax Updates ... 4

Service Tax Updates ... 6

Imperatives for Internal

Audit Success ... 7

Companies Bill 2012 ... 8

Impact of Rev. Sch. VI ... 9

Photo Flash ... 11

Pg.

Baroda Branch of WIRC of ICAI

The most difficult thing is the decision to act, the rest is merely tenacity.- Amelia Earhart

Congratulations... ICAI Torch Bearers 2013-14CA. Subodh Kumar Agrawal

President, ICAI

A combination of erudition, foresight and

professional excellence,

has become the supreme torch-

bearer of Indian accountancy profession as

the President of the Institute of Chartered

Accountants of India (ICAI) for the year

2013-14. A fellow member of the ICAI with 24 years of standing,

he was elected as the President by the 22nd Council of the

Institute on February 12, 2013. He was the Vice President of the

ICAI for the Council Year 2012-13. An altruistic hard-worker

bestowed with exceptional organisational, networking,

administrative and leadership skills, he has been serving as

Central Council member for two terms since 2007.

He has passionately represented Indian accountancy profession

on the international front. He has recently been appointed as

member of SMP (Small and Medium Practices) Committee of

International Federation of Accountants (IFAC) for the year

2013–15, and he has also been appointed as Vice President of

South Asian Federation of Accountants (SAFA) for the year 2013.

CA. Agrawal had also made notable contributions in Eastern India

Regional Council. Under his dynamic Chairmanship, the Eastern

India Regional Council was honoured with ‘Best Regional Council

Award’ in the year 2006. His other areas of interest include sports

and reading management and professional books.

CA. Subodh Kumar

Agrawal

CA. K. Raghu

Vice -President, ICAI

A man of information technology, efficiency,

and professional discipline, having firm

belief in inclusive as well as exclusive growth

of the profession of accountancy,

is the new Vice President of The

Institute of Chartered Accountants of India

for the term 2013-14. He was elected as the Vice President by the

22nd Council of the ICAI on 12th February 2013. He is the second

person from Karnataka to occupy this prestigious position.

With a fellowship of the Institute and with more than two decades

of professional standing and of constant and dedicated service to

the cause of accountancy profession, he has always dazzled his

fellow members with his deep and visionary understanding of

Information Technology, and brilliant and uninterrupted service

to the profession that he has been serving since 1990 with an

inextinguishable enthusiasm. He has been continuously

associated with ICAI for the last 21 years in various capacities and

is widely known for his pioneering and far-reaching initiatives of

webcasting, e-learning and ICAI Web TV. He specialises in

Taxation, Business and Technology Consulting.

Before his election to the Central Council, he had recorded his

magnetic presence in the Southern India Regional Council of the

Institute

CA. K

Raghu

DATES COMPLIANCE PERIOD

01.03.2013 VAT / CST E-return - Monthly (For VAT or CST <= 5,000/-)

(with Stock Statement for Oct.'12 to Dec.' 12)

02.03.2013 Submitting (Gujarat) VAT Audit Report (EXTENDED DATE) FY 2011-12

05.03.2013 Payment of Service Tax - Monthly & Quarterly Cases / Excise Duty (for NON SSI) February, 2013

06.03.2013 E-Payment of Service Tax - Monthly & Quarterly Cases / Excise Duty (for NON SSI) 2013

07.03.2013 TDS payment / E-Payment 2013

10.03.2013 Excise Return for units required to submit ER-5 2013

11.03.2013 VAT / CST E-return - Monthly (For VAT or CST > 5,000/-)

(with Stock Statement for Oct.'12 to Dec.' 12)

15.03.2013 Advance Income Tax payment / E-payment - All Assessees - Last Installment A.Y. 2013-14

15.03.2013 Payment of Professional Tax / PF / Excise Duty (for SSI) February, 2013

16.03.2013 Excise Duty E-Payment (for SSI) February, 2013

16.03.2013 VAT / CST E-return - Quarterly (Regular & Lump sum) Q3 (F.Y2012-13)

22.03.2013 VAT / CST payment / E-payment February, 2013

25.03.2013 Filing of Service Tax Return - ST-3 (Revised Form) Jul. 2012 to Oct. 2012

31.03.2013 Service tax Payment - Monthly/Quarterly March, 2013

31.03.2013 Last date for Filing / e-filing of belated Income Tax return (without penalty) A.Y. 2012-13

` December, 2012

February,

February,

February,

December, 2012`

Due Date Planner Compiled by CA. Aparna Ashtaputre

CA. Mangesh Kinare, Chairman

WIRC Office Torch Bearers 2013-04

CA. Parag Raval, Vice Chairman CA. Neel Majithia Secretary CA. Priti Savla, Treasurer

2

Baroda Branch of WIRC of ICAI

If you want the rainbow, you've got to put up with the rain.- Dolly Parton

Forthcoming Events

Lecture Meeting on "Analysis of Budget-2013”

Day & Date :

Time :

Faculty :

Fees :

Venue :

02.03.2013, Saturday

05.00 pm to 08.00 pm

Adv.& CA. Saurabh Soparkar, A'bad

CA. Aniruddh Sonpal, Vadodara

ICAI Bhawan,

` 200/-

Vadodara

CPE 03

Workshop for Accountants - Part - II

Day & Date :

Time :

Topic :

Faculty :

Fees: :

Venue :

09.03.2013, Saturday

06.00 pm to 08.30 pm

Preparation for Income Tax Scrutiny

CA. Nirav Shah

50/-

ICAI Bhawan,

`

Vadodara

Women's Day Celebration

For Female CA members and spouses of CA members (One guest with

participant allowed)

Day & Date :

Time :

Topic Speaker

Fees :

Venue :

08.03.2013, Friday

03.00 pm to 05.30 pm

Etiquettes and Elegance CA. Neena Patel, Mumbai

Health Tips Ms. Kausha Patel,

Talwarkars Gym, Vadodara

Saree Draping Competition -

50 per participant (with high-tea)

ICAI Bhawan,

`

Vadodara

CPE Teleconferencing

Day & Date :

Time :

Topic :

Faculty :

Fees :

Venue :

05.03.2013, Tuesday

11.00 am to 1.00 pm

Finance Bill, 2013

CA. Girish Ahuja, New Delhi

ICAI Bhawan,

` 100/-

Vadodara

CPE 02

Lecture Meeting on

"Practical Issues under G-VAT”

Day & Date :

Time :

Faculty :

Fees :

Venue :

09.03.2013, Saturday

05.30 pm to 07.30 pm

CA. Abhay Desai, Vadodara

ICAI Bhawan,

` 200/-

Vadodara

CPE 02

Full Day Seminar on Companies Bill, 2012

Organised by Committee of Corporate Laws & Corporate Governance,

ICAI & Hosted by Baroda Branch of WIRC of ICAI

Day & Date :

Time :

16.03.2013, Saturday

09.30 am to 05.30 pm

CPE 06

Topic Speaker

Fees :

Venue :

Overview of Companies

Bill, 2012 CCM and Chairman of

Committee of Corporate

Laws and Corporate

Governance, ICAI

Relevant aspects of

accounts and audit Ahmedabad

Various Statutory

compliances under

Companies Bill, 2012

New professional

opportunity - shriking

or expanding

Upto 12.03.2013 900/-,

thereafter . 1100/-

ICAI Bhawan,

CA. S. Santhanakrishnan,

CA. Arpit Patel,

Mr. S. D. Ishrani, Advocate

and Solicitor,(UK) Mumbai

CA. Alok Shah, Vadodara

Vadodara

`.

`

Workshop for Accountants - Part III

Day & Date :

Time :

Topic :

Faculty :

Fees :

Venue :

16.03.2013, Saturday

06.00 pm to 08.30 pm

Overview of Service Tax

CA. Manilal J. Parsiya, Vadodara

ICAI Bhawan,

` 50/-

Vadodara

CPE Teleconferencing

Day & Date :

Time :

Topic :

Faculty :

Fees :

Venue :

22.03.2013, Friday

11.00 am to 1.00 pm

Bank Branch Audit

CA. Amarjit Chopra,

Past President, New Delhi

ICAI Bhawan,

` 100/-

Vadodara

CPE 02

Holi Milan

Day & Date :

Time :

Fees :

Venue :

27.03.2013, Wednesday

09.30 am onwards (followed by lunch)

ICAI Bhawan,

NIL

Vadodara

Full day seminar on Bank Branch Audit

Day & Date :

Time :

Topic Speaker

23.03.2013, Saturday

09.00 am to 05.30 pm

Risk base Audit CA Dhananjay Gokhale,

Mumbai

Audit Planning, Procedure

and RBI Guideline Vadodara

Advances, Assets &

norms- Important Issues Mumbai

LFAR, Tax Audit Report &

Statutory Certificates Vadodara

CA. Manish Baxi,

NPA CA Sandeep Welling,

CA. Rashmi Thakkar,

CPE 06

Branch Events

3

Baroda Branch of WIRC of ICAI

The power to question is the basis of all human progress.- Indira Gandhi

In an era of increasing usage of ‘plastic

money’ & Inernet - with an objective of better

services to members & students, Baroda

Branch is having facilities of Registrations for

seminar & conference by paying through

credit/debit card at ICAI Bhawan or visit

www.baroda-icai.org foronline payment.

PAYMENT OPTIONS FOR PROGRAM REGISTRATION

e-paymentDrop Box a t 2 -B ,

Ramkrishna Chambers,

BPC Road, Baroda.

Kindly mention your

name, membership

number and program

for which registration is

sought, on back side of

the Cheque

Join us on groupFacebook Baroda Branch of WIRC of ICAIExchange views and news. Be updated about forthcomingevents of Baroda Branch

Members are requested to register themselves in advance

by using above options and avoid spot registration to help

us to serve you better.

Income Tax UpdatesComplied by CA Bhavana Patel

Notifications:

Circulars

Press Releases

Case Laws - Tribunal

1. Specified Territory for the purposes of Section 90

(Notification No. 54/2012 dated 17.12.2012) :

1. Search &Seizure – Assessment of preceding years in

search cases during election period. (Circular No.

10/2012 dated 31.12.2012)

1. Statement of the Finance Minister on GAAR and final

report on GAAR. (Press release dated 14.01.2013)

1. Use of Borrowed Funds for investment u/s 54F:

In exercise of the powers conferred by Explanation 2 to

Section 90 of the Income-tax Act, 1961, the Central

Government has notified ‘Sint Maarten, a part of

Kingdom of Netherlands’, the area outside India as the

‘specified territory’ for the purpose of the said section 90.

The said notification shall come into force with

immediate effect i.e. 17.12.2012.

In order to reduce fructuous and unnecessary

proceedings under the Income-tax Act 1961, in cases

where a search is conducted under Section 132 or

requisition made under Section 132A and cash or other

assets are seized during the election period, and no

evidence is available or investigation is required, the

Central Government has, through Finance Act,2012,

amended the Income Tax Rules, 1962 by inserting a new

Rule 112F, specifying the class or classes of cases in

which the Assessing Officer shall not be required to issue

notice for assessing or reassessing the total income for

six assessment years relevant to the previous year in

which search is conducted or requisition is made.

Further, it mentions that the investigating officer, with

the approval of Director General of Income tax, shall

certify that the search is conducted under Section 132 or

requisition is made under Section 132A in the territorial

area of an assembly or parliamentary constituency; or

the assets seized or requisitioned are connected in any

manner to the ongoing election process in an assembly

or parliamentary constituency; and no evidence is

available or investigation is required for any assessment

year other than the assessment year relevant to the

previous year in which search is conducted or requisition

is made. Such certificate shall be communicated to the

Commissioner of Income tax and the Assessing Officer

having jurisdiction over the case of such person.

Considering all the circumstances and relevant factors,

Government has deferred the implementation of GAAR

to 1st April, 2016 as against the current provision of 1st

April, 2014.

The exemption u/s 54F was denied by A.O. on the ground

Fees :

Venue :

Upto 18.03.2013 After 18.03.2013

Members 900/- 1100/-

Non-members/

students

ICAI Bhawan,

` `

` `700 900/-

Vadodara

1st Charitable Clinic, 2013

In fond memory of Late CA. Ambalal M. Shah, Past Chairman, Baroda

Branch

Day & Date :

Time :

Venue :

30.03.2013, Saturday

03.00 pm to 05.00 pm

ICAI Bhawan, Vadodara

CPE 02

STUDY CIRCLESubsidies available to SMEs

Day & Date :

Time :

Faculty :

Fees :

Venue :

05.03.2013, Tuesday

06.00 pm to 08.00 pm

CA. Hitesh Agrawal

200/-

ICAI Bhawan,

` (for Non-members of Study Circle)

Vadodara

CPE 02

Revisionary Sessions for CA IPCC & Final Students

Day & Date : From 01.03.2013, Friday to

10.04.2013, Wednesday

For further details, refer Baroda branch website /

facebook page of WICASA, Baroda

WICASA EVENT

We regret the sad demise of CA Ambalal M. Shah, Past

Chairman of Baroda Branch on 18.02.2013. We express

our deepest condolences to the bereaved family. May

his soul rest in eternal peace

OBITUARY

4

Baroda Branch of WIRC of ICAI

Never give up, for that is just the place and time that the tide will turn - Harriet Beecher Stowe

that the amount deposited by the assessee in the capital

gains accounts scheme included borrowed funds. It was

held that ultimately the assessee deposited the requisite

amount in the capital gain tax account scheme within the

time stipulated by the statute. The capital gain tax

earned by the assessee can be utilized for other purpose

and as long as the assessee fulfills the condition of

investment either by his own funds or borrowed funds,

the deduction u/s 54F cannot be denied to him. [J V

Krishna RaoVsDy CIT ITA Nos. 1866 & 1867 (Hyd) (2011)]

The A.O. made disallowance/additions to the assessee’s

income as per normal provisions of the Act. Finally,

however, income was determined and tax was computed

u/s 115JB. Thereafter, the A.O. levied penalty u/s

271(1)(C) on all the disallowance/additions. The CIT (A)

deleted the penalty on certain additions while

confirming the same on other additions. The tribunal

deleted the penalty by stating that if finally income tax is

paid on the book profits as determined u/s 115JB, then

for the purpose of levying penalty, normal computation

would not be considered as tax has not been levied

under the normal provisions. [BSEL Infrastructure Realty

Ltd. Vs Asst. CIT ITA No. 6559 (Mum.)(2011).]

The assessee carried on business as a builder and was

entitled to deduction u/s 80-IB (10). In the course of the

search action u/s 132 of the Act, the assessee had made a

declaration of undisclosed income of Rs. 7 Crores. In the

block return, the assessee offered undisclosed income of

Rs. 3.5 Crores. The assessee claimed at the time of

making the statement, the director of the assessee was

unaware of the deduction u/s 80-IB of the Act. The A.O.

did not allow the claim for deduction u/s 80-IB(10) of the

Act and computed the undisclosed income at Rs. 7.68

Crores. CIT(A) and the Tribunal allowed the assessee’s

claim.

On appeal by the Revenue, the Bombay High Court

upheld the decision of the Tribunal and held that the

total income/loss for the block period has to be

computed in accordance with the provisions of the Act

and the same would include Chapter VI-A. Section 80-IB

is a part of Chapter VI-A. In view of the above, while

computing the undisclosed income for the block period,

the assessee is entitled to claim deduction from its

income u/s 80IB. [CIT vs. Sheth Developers (P) Ltd. 254

CTR 127 (Bom.)]

The Chief Commissioner rejected the assessee’s

application for waiver of interest u/s 220(2A) of the Act

on the ground that the assessee blocked the recovery

proceedings by obtaining stay against attachment

2. Penalty u/s 271(1)(C) on additions if tax is finally

assessed u/s 115JB:

1. Disclosure of Construction income is eligible for

deduction u/s 80-IB(10):

2. Waiver of Interest u/s Section 220(2A):

Case Laws - High Courts

notices and the assessee had not cooperated in recovery

proceedings and payment of interest would not cause

any genuine hardship to the assessee.

On a writ petition challenging the rejection order, the

Division Bench of the Kerala High Court directed the A.O.

to reduce 25% of interest and held that

“The right to move for stay against recovery during

pendency of an appeal is a statutory right, exercise of

which cannot be said to be an indication of assessee’s

lack of co-operation. Lack of co-operation happens

when the assessee makes recovery difficult for the

Revenue by transferring or siphoning off his assets

leading to protracted enquiry and continuation of

recovery proceedings by the Department.” [Arun Sunny

vs. CCIT 350 ITR 147 (Ker.)]

The assessee, a non-banking financial company, had

been collecting certain sums as ‘contingent deposit’ on

ad hoc basis from the leasing/hire-purchase customers

with a view to protect themselves from sales tax liability.

The assessee did not offer such sums to tax as income on

the ground that such sums were collected as contingent

deposits and was in anticipation of sales tax liability,

which was disputed. Further, it is contended by the

assessee that if it was to succeed in its challenge to the

levy of the said sales tax, the said contingent deposits

from its customers will be refunded back to the

customers.

The Supreme Court stated that the said sum was not kept

in a separate interest bearing bank account but it formed

part of the business turnover. Applying the substance

over form test, the said amount treated as turnover and

taxable as income. [Sundaram Finance Ltd. Vs ACIT

(2012) 349 ITR 356 (SC)]

The assessee had advanced large amounts to Vanchinad

Leather Ltd., a joint sector company promoted by the

assessee. The assessee claimed deduction of Rs.

55,70,949/- as provision for bad debts as a declaration

was made by BIFR that Vanchinad Leather Ltd. had

become sick company. The claim was disallowed on the

ground that no reasonable steps had been taken for

recovery of the debts and further no part of the

outstanding amount had been assessed as the income of

earlier years. Also, the amount was written off in the

assessee’s accounts in claiming bad debts. The CIT (A)

confirmed the disallowance. The tribunal dismissed the

appeal, taking the view that the debt had become

irrevocable during the previous year and that the

condition for claiming deductions u/s 36(2)(i)(b) were

not satisfied.

On an appeal to the Supreme Court (SC) by the assessee,

the SC noted that till the end, the company could not be

1. Amount collected from customers towards disputed

Sales Tax Liability, Capital or Revenue? :

2. Claim of Bad Debts u/s 36(2):

Case Laws - Supreme Court

5

Baroda Branch of WIRC of ICAI

Forgiveness is a virtue of the brave - Indira Gandhi

revived and it had been wound up. In the circumstances,

applying the commercial test and business exigency test,

the SC held that both the conditions u/s 36(1)(vii) read

with section 36(2)(i)(b) of the Act were satisfied. Thus,

according to SC, there was no reason to deny the

assessee the claim for deduction of bad debt. [Kerala

State Industrial Development Corporation Ltd. V CIT 349

ITR 365 (2012) (SC)]

Service Tax UpdatesComplied by CA. Chandrika Parsiya

1. Rendition of passive infrastructure along with mobile

tower site is a ‘service’ and not a ‘deemed sale’.

2. If members of review committee never met together

and they had not recorded any opinion, Department's

appeal before Tribunal was liable to be set aside as

unauthorised.

Assessee was providing passive infrastructure along with

mobile tower site and maintenance services to various

mobile operators on sharing basis and allowing such

operators to install their antenna, microwave radios and

base transreceiver station (BTS). Assessee was paying

service tax on consideration received. VAT Department

sought levy of VAT treating it as transfer of right to use

passive infrastructure.It is held that assessee had not

transferred any right in passive infrastructure to mobile

operators. Assessee had merely granted permission to

mobile operators to have access to passive infrastructure,

a permission to keep their equipments in site belonging

to assessee, a permission to mount antenna, etc. and to

enjoy other facilities so as to operate equipments

belonging to mobile operator. No sale of goods or

transfer of right to use was involved in transaction in

question, hence, it did not fall under article 366(29A)(d) of

Constitution. Accordingly, demand of VAT was set aside

and levy of service tax was upheld. - Indus Towers Ltd. v.

Deputy Commissioner of Commercial Taxes, Bangalore,

[2013] 29 taxmann.com 301 (Karnataka High Court)

Department filed appeal against order of Commissioner

(Appeals) in pursuance of order of Committee of

Commissioners directing filing of such appeal. Assessee

challenged such appeal arguing that members of

Committee had merely put their signature on different

dates on note prepared by junior officers and there was

no valid authorization of filing appeal. It was held that

there was no meeting of members of Committee to

consider such case. Record also did not disclose that

members applied their mind to issue and recorded any

opinion that order of Commissioner (Appeals) was not

legal or proper and was to be challenged in appeal. There

should be a meaningful consideration which should be

reflected on note sheets. Since there was no such

satisfaction or opinion recorded by members of

Committee, appeal was liable to be dismissed -

Commiss ioner of Central Excise , Delhi- I v.

KundaliaIndustries[2013] 29 taxmann.com 322 (Delhi

High Court)

Assessee - manufacturer took credit of service tax paid by

consignment agent of raw material supplier on goods

transport agency's services relating to transport of inputs

to assessee's premises. Department denied credit

contending that since consignment agent was not

entitled to avail such credit, he could not have passed on

such credit to buyer viz. assessee. It was held that in view

of precedent decisions, invoices issued by consignment

agents are proper documents for availment of Cenvat

credit of service tax paid on goods transport services by

consignment agent. Hence, credit was held allowable. -

Mittal Pigments (P.) Ltd. v. Commissioner of Central

Excise, Jaipur, [2013] 29 taxmann.com 324 (New Delhi -

CESTAT)

Assessee, a manufacturer and exporter, did not pay

service tax on goods transport agency services and

foreign commission agent's services received by it under

reverse charge. Assessee also didn't show them in its

service tax returns. On being pointed out, assessee paid

service tax along with interest. Department sought levy of

penalty under section 78 for intent to evade. It is held that

since assessee had paid service tax, it was entitled to take

credit of same. In that view, it could not be said that by

suppressing facts, assessee was going to get extra

benefit. Therefore, penalty under section 78 was not

sustainable. - India Trimmings (P.) Ltd. v. Commissioner of

Central Excise, Coimbatore, [2013] 29 taxmann.com 425

(Chennai - CESTAT)

Assessee took credit of service tax paid on Business

Auxiliary Services of commission agent engaged in

selling of assessee's goods. Department denied credit

contending that said activity had no relation with

manufacture. It is held that “sales promotion" is expressly

figured in inclusion part of definition of input service.

Where a particular activity is expressly mentioned in

inclusion part of definition, one need not bother to

examine whether it has satisfied ingredients of main part

of definition. Since commission agent's services fell

under 'sales promotion', they were eligible for input

service credit - Wadpack (P.) Ltd. v. Commissioner of

Central Excise, Bangalore, [2013] 30 taxmann.com 209

(Bangalore - CESTAT)

3. Service tax paid by consignment agent of raw

material supplier for inward transport of raw

materials to assessee's premises is eligible for credit;

and invoice issued by consignment agent is a valid

document for taking such credit

4. If service tax paid belatedly along with interest was

eligible as CENVAT Credit to assessee, evasion penalty

under section 78 could not be levied.

5. Business Auxiliary Services of commission agent

engaged in selling of assessee's are eligible for credit.

6

Baroda Branch of WIRC of ICAI

What is the value of education which does not inculcate passion and fearlessness for setting right what is wrong?- Kiran Bedi

Imperatives for Internal Audit SuccessCompiled by CA Rachna Parikh

For a successful internal audit organization the two key

attributes are the ability to articulate stakeholder

expectations and the ability to exceed stakeholder

expectations on a consistent basis. The strong alignment of

internal audit priorities with key stakeholder expectations is

the ultimate best practice.

While primary stakeholder expectations will differ from one

organization to another, they typically include a combination

of the following:

- Institute a comprehensive risk-based audit plan

- Inform directors about the tone of the organization and

its control processes

- Provide expertise and assurance on risks and controls

- Facilitate greater understanding of the organization’s

risks and its risk management processes

- Provide an objective set of eyes and ears across the

organization

- Serve as a trusted advisor

- Provide expertise and assurance on internal controls

- Offer and provide insight, advice, and assurance on

enterprise risks

- Deliver timely and relevant information to facilitate risk

management and business decisions

- Assist management with identification of emerging risks

or events

- Identify key risks facing the organization and assess the

effectiveness of controls to mitigate those risks

- Provide insight into the adequacy of financial controls

- Execute a risk-based audit plan addressing financial risks

and relevant IT controls

The following ten imperatives provide the foundation for

a high performance internal audit function in the years

ahead.

Ideally, a chief audit executive will report functionally to

the audit committee. However, a reporting relationship

alone will not create prominence or stature. To be

successful, a CAE needs to be perceived as strategic and

as a member of senior management or its operating

equivalent. Audit leaders who reach these milestones

strive continuously to ensure that internal audit’s

priorities align effectively with those of the audit

committee and senior management. They make a point

of communicating regularly with the chairman of the

1. The audit committee and board expect internal audit

to:

2. Management expects that internal audit will:

3. External auditors, regulators, and others expect

internal audit to:

4. Achieve sufficient strategic stature for internal audit

within the organization.

audit committee, on both a formal and informal basis.

Such proactive steps are likely to be even more

important in the years ahead as pressures mount for

internal audit to demonstrate value beyond providing

controls assurance.

To navigate the inevitable changes, it will be more

important than ever for organizations to have a formal

strategic plan in place. To be effective in driving change,

a strategic plan should:

- Describe the organization’s vision for the future of

internal audit—one that is clearly aligned with the needs

of the organization and its stakeholders

- Serve as a primary basis for change and management of

the function

- Outline the major risks and trends affecting the company

and its industry

- Describe how internal audit is organized to deliver

service

- Suggest specific goals or strategic initiatives to bridge

capability gaps and to achieve internal audit’s strategic

vision

A CAE needs to keep senior management and the board

informed about emerging risks to the enterprise as well

as systemic risk and control-related trends that are

gleaned from audits. The CAE and senior internal audit

managers should cult ivate act ive two-way

communication channels with the chairman of the audit

committee and with the company’s external auditors.

IT audit strategies need to lay the groundwork for

integrating IT audit expertise within audit teams. An IT

audit plan should center on an annual IT risk assessment,

reflecting a clear linkage between IT risk assessments

and IT audit planning. In addition, it should address risks

within individual business processes and provide for

continuous enhancement of IT audit capabilities. It’s also

important for the plan to be clearly articulated, formally

documented, and well aligned with organizational IT

strategies and objectives.

5. Develop and regularly update a formal strategic plan

aligned with key enterprise-wide objectives and

stakeholder expectations.

6. Communicate frequently with key stakeholders on

their needs, expectations, and satisfaction with

internal audit.

7. Take an integrated approach to IT audit, one

designed to strengthen IT capabilities.

Revised passing requirements for Common

Proficiency Test (CPT) effective from June, 2013

www.icai.org

Refer ICAI website for Notification No. 1-CA(7)/145/2012

dated 1st August, 2012 mentioning passing criteria.

ANNOUNCEMENT

7

Baroda Branch of WIRC of ICAI

Don't compromise yourself. You are all you've got - Janis Joplin

Companies Bill 2012and Registered ValuerCA Tejal Parikh

The Companies Bill, 2012 was introduced and passed in the

LokSabha on 18 December 2012. The Bill when enacted would

replace the Companies Act, 1956 (1956 Act).The Bill come up

with 29 Chapters, 470 Clauses, 7 schedules and 95 definitions.

The Companies Bill, 2012 has introduced the concept of

‘Registered Valuer’ through Chapter XVII to cover valuation of

any property, stock, shares, debentures, securities, goodwill

or any other assets of the company as well as its net worth and

liabilities. The qualification and experience of the person

registered as a valuer and the basis of valuation shall be

prescribed through Rules by the Central Government.

Where at any time, a company having a share capital

proposes to increase its subscribed capital by the issue of

further shares, such shares shall be offered to any

persons, if it is authorised by a special resolution,

whether or not those persons include the persons

referred to in clause (a) (offer of shares to the existing

holders) or clause (b)(offer to employees under a scheme

of employees’ stock option scheme), either for cash or

for a consideration other than cash, if the price of such

shares is determined by the valuation report of a

registered valuer subject to such conditions as may be

prescribed

No company shall enter into an arrangement by which —

(a) a director of the company or its holding, subsidiary or

associate company or a person connected with him

acquires or is to acquire assets for consideration other

than cash, from the company; or

(b) vice-versa unless prior approval for such arrangement is

accorded by a resolution of the company in general

meeting and if the director or connected person is a

director of its holding company, approval under this sub-

section shall also be required to be obtained by passing a

resolution in general meeting of the holding company.

The notice for approval of the resolution by the company

or holding company in general meeting shall include

the particulars of the arrangement along with the value

of the assets involved in such arrangement duly

calculated by a registered valuer.

Where a compromise or arrangement is proposed—

CLAUSES WHERE VALUATION REQUIRED:

Clause 62(1)(c)– For Valuing further Issue of Shares:

Clause 192(2)– For Valuing Assets involved in

Arrangement of Non Cash transactions involving

Directors:

Clause 230(2)(c)(v)– For Valuing Shares, Property

and Assets of the company under a Scheme of

Corporate Debt Restructuring :

�

�

�

(a) between a company and its creditors or any class of

them; or

(b) between a company and its members or any class of

them, the Tribunal may, on the application of the

company or of any creditor or member of the company,

or in the case of a company which is being wound up, of

the liquidator, order a meeting of the creditors or class of

creditors, or of the members or class of members, as the

case may be, to be called, held and conducted in such

manner as the Tribunal directs.

The company or any other person, by whom an

application is made under subsection (1), shall disclose

to the Tribunal by affidavit any scheme of corporate

debt restructuring consented to by not less than

seventy-five per cent. of the secured creditors in value,

including a valuation report in respect of the shares and

the property and all assets ,tangible and intangible,

movable and immovable, of the company by a registered

valuer.

Where a meeting is proposed to be called in pursuance

of an order of the Tribunal under sub-section (1), a notice

of such meeting shall be sent to all the creditors or class

of creditors and to all the members or class of members

and the debenture-holders of the company, individually

at the address registered with the company which shall

be accompanied by a statement disclosing the details of

the compromise or arrangement, a copy of the valuation

report, if any, and explaining their effect on creditors, key

managerial personnel, promoters and non-promoter

members, and the debenture-holders and the effect of

the compromise or arrangement on any material

interests of the directors of the company or the

debenture trustees, and such other matters as may be

prescribed:

Where an order has been made by the Tribunal under

sub-section (1), merging companies or the companies in

respect of which a division is proposed, shall also be

required to circulate the report of the expert with regard

to valuation, if any, along with other required

documents.

The Tribunal, after satisfying itself that the procedure

�

�

�

Clause 230(3)- Under a Scheme of Compromise /

Arrangement, along with the notice of creditors /

shareholders meeting, a copy of Valuation Report, if

any shall be accompanied

Clause 232(2)(d)- The report of the expert with

regard to valuation, if any would be circulated for

meeting of creditors/members

Clause 232(3)(h)- Where under a Scheme of

Compromise/Arrangement the transferor company

is a listed company and the transferee company is an

unlisted company, for exit opportunity to the

shareholders of transferor company, valuation may

be required to be made by the Tribunal .8

Baroda Branch of WIRC of ICAI

I'm not afraid of storms, for I'm learning to sail my ship - Louisa May Alcott

Impact ofon presentation of Profit And Loss Account:A Case of Tata Steel Ltd.

Revised Schedule VI

Complied by Prof. Dr. CA. Amita S. Kantawala

As is known the Revised Schedule VI is announced and is

made applicable for all companies for the financial

statements to be prepared for the financial year commencing

on or after 1st April 2011.

In the present note an attempt is made to understand how the

presentation differs and how it facilitates the analysis with the

Case study of TATA Steel Ltd.

specified in sub-sections (1) and (2) has been complied

with, may, by order, sanction the compromise or

arrangement or by a subsequent order, make provision

for payment of the value of shares held by them and

other benefits in accordance with a pre-determined

price formula or after a valuation is made, if shareholders

of the transferor company decide to opt out of the

transferee company.

As per the sub-section (1) of the clause, in the event of an

acquirer, or a person acting in concert with such acquirer,

becoming registered holder of ninety per cent. or more

of the issued equity share capital of a company, or in the

event of any person or group of persons becoming

ninety per cent majority or holding ninety per cent. of the

issued equity share capital of a company, by virtue of an

amalgamation, share exchange, conversion of securities

or for any other reason, such acquirer, person or group of

persons, as the case may be, shall notify the company of

their intention to buy the remaining equity shares.

The acquirer, person or group of persons under sub-

section (1) shall offer to the minority shareholders of the

company for buying the equity shares held by such

shareholders at a price determined on the basis of

valuation by a registered valuer in accordance with such

rules as may be prescribed under sub-section (2).

Without prejudice to the provisions of sub-sections (1)

and (2), the minority shareholders of the company may

offer to the majority shareholders to purchase the

minority equity shareholding of the company at the price

determined in accordance with such rules as may be

prescribed under sub-section (2).

As per sub-section(1) of the clause, the company

administrator shall perform such functions as the

Tribunal may direct .As per sub-section (2) of the clause,

without prejudice to the provisions of sub-section (1),

the company administrator may cause to be prepared

with respect to the company a valuation report in respect

of the shares and assets in order to arrive at the reserve

price for the sale of any industrial undertaking of the

company or for the fixation of the lease rent or share

exchange ratio;

Where the Tribunal has made a winding up order or

appointed a Company Liquidator, such liquidator shall,

within sixty days from the order, submit to the Tribunal, a

report containing the nature and details of the assets of

the company including their location and value, stating

separately the cash balance in hand and in the bank, if

�

�

�

Clause 236(2) – For Valuing Equity Shares held by

Minority Shareholders.

Clause 260(2)c – For preparing Valuation report in

respect of Shares and Assets to arrive at the Reserve

Price for Company Administrator

Clause 281(1) – For Valuing Assets for submission of

report by Liquidator

any, and the negotiable securities, if any, held by the

company, provided that the valuation of the assets shall

be obtained from registered valuers for this purpose;

As per the sub-section (1) of the Clause, where it is

proposed to wind up a company voluntarily, its director

or directors, or in case the company has more than two

directors, the majority of its directors, shall, at a meeting

of the Board, make a declaration verified by an affidavit

to the effect that they have made a full inquiry into the

affairs of the company and they have formed an opinion

that the company has no debt or whether it will be able

to pay its debts in full from the proceeds of assets sold in

voluntary winding up.

As per the sub-section (2), a declaration made under

sub-section (1) shall have no effect for the purposes of

this Act, unless where there are any assets of the

company, it is accompanied by a report of the valuation

of the assets of the company prepared by a registered

valuer.

Any member of the transferor company who did not vote

in favour of the special resolution and expresses his

dissent there from in writing addressed to the Company

Liquidator and left at the registered office of the

company within seven days after the passing of the

resolution, may require the liquidator either—

(a) to abstain from carrying the resolution into effect; or

(b) to purchase his interest at a price to be determined by

agreement or the registered valuer

The concept of a registered valuer as introduced in

Companies Bill 2012, is likely to have a big impact on Industry,

professionals, shareholders and government. The increase in

requirements for valuation will lead to a substantial increase

in professional opportunities for CAs…….

�

�

Clause 305(2)(d) – For report on the Assets of the

company for preparation of declaration of solvency

under voluntary winding up

Clause 319(3)(b) – For Valuing the interest of any

dissenting member of the transferor company who

did not vote in favour of the special resolution, as

may be required by the Company Liquidator

Impact of Change

9

Baroda Branch of WIRC of ICAI

Anger is never without an argument, but seldom with a good one.- Indira Gandhi

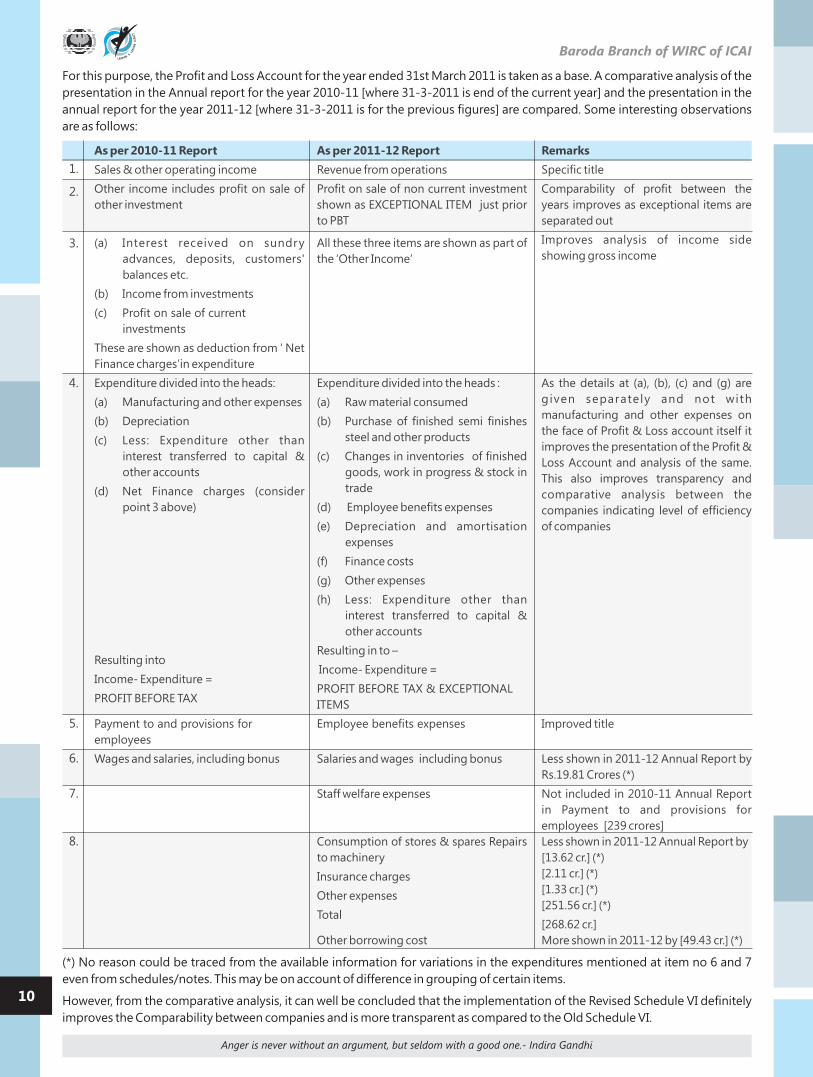

As per 2010-11 Report

Sales & other operating income

Other income includes profit on sale of

other investment

(a) Interest received on sundry

advances, deposits, customers'

balances etc.

(b) Income from investments

(c) Profit on sale of current

investments

These are shown as deduction from ‘ Net

Finance charges’in expenditure

Expenditure divided into the heads:

(a) Manufacturing and other expenses

(b) Depreciation

(c) Less: Expenditure other than

interest transferred to capital &

other accounts

(d) Net Finance charges (consider

point 3 above)

Resulting into

Income- Expenditure =

PROFIT BEFORE TAX

Payment to and provisions for

employees

Wages and salaries, including bonus

As per 2011-12 Report

Revenue from operations

Profit on sale of non current investment

shown as EXCEPTIONAL ITEM just prior

to PBT

All these three items are shown as part of

the ‘Other Income’

Expenditure divided into the heads :

(a) Raw material consumed

(b) Purchase of finished semi finishes

steel and other products

(c) Changes in inventories of finished

goods, work in progress & stock in

trade

(d) Employee benefits expenses

(e) Depreciation and amortisation

expenses

(f) Finance costs

(g) Other expenses

(h) Less: Expenditure other than

interest transferred to capital &

other accounts

Resulting in to –

Income- Expenditure =

PROFIT BEFORE TAX & EXCEPTIONAL

ITEMS

Employee benefits expenses

Salaries and wages including bonus

Staff welfare expenses

Consumption of stores & spares Repairs

to machinery

Insurance charges

Other expenses

Total

Other borrowing cost

Remarks

Specific title

Comparability of profit between the

years improves as exceptional items are

separated out

Improves analysis of income side

showing gross income

As the details at (a), (b), (c) and (g) are

given separately and not with

manufacturing and other expenses on

the face of Profit & Loss account itself it

improves the presentation of the Profit &

Loss Account and analysis of the same.

This also improves transparency and

comparative analysis between the

companies indicating level of efficiency

of companies

Improved title

Less shown in 2011-12 Annual Report by

Rs.19.81 Crores (*)

Not included in 2010-11 Annual Report

in Payment to and provisions for

employees [239 crores]

Less shown in 2011-12 Annual Report by

[13.62 cr.] (*)

[2.11 cr.] (*)

[1.33 cr.] (*)

[251.56 cr.] (*)

[268.62 cr.]

More shown in 2011-12 by [49.43 cr.] (*)

1.

2.

3.

4.

5.

6.

7.

8.

(*) No reason could be traced from the available information for variations in the expenditures mentioned at item no 6 and 7

even from schedules/notes. This may be on account of difference in grouping of certain items.

However, from the comparative analysis, it can well be concluded that the implementation of the Revised Schedule VI definitely

improves the Comparability between companies and is more transparent as compared to the Old Schedule VI.

For this purpose, the Profit and Loss Account for the year ended 31st March 2011 is taken as a base. A comparative analysis of the

presentation in the Annual report for the year 2010-11 [where 31-3-2011 is end of the current year] and the presentation in the

annual report for the year 2011-12 [where 31-3-2011 is for the previous figures] are compared. Some interesting observations

are as follows:

10

Baroda Branch of WIRC of ICAI

The minute you settle for less than you deserve, you get even less than you settled for.- Maureen Dowd

Orientation for Campus Interview on 08.02.2013

CA. Manish Baxi CA. Maulik Mehta CA. Piyush K. Jain

CA. Jay ChhairaCCM

Dr. Hasmukh B.Patel

CA. Yogesh Dubey

Teleconference on 08.02.2013 Mr. Biharilal Deora, Surat on Study Circle 12.02.2013Managing Committee with Past PresidentCA. Uttam Prakash Agrawal on 18.02.2013

CA Atur Mehta Workshop for Accountants on 23.02.2013 Joint Programme with Bharuch Branch on 23.02.2013 Participants Union Budget 2013 on 28.02.2013

OTHER EVENTS

Radha Krishna Pillai with Study Circle Team 2013 Study Circle Birthday Celebration Study Circle Team 2012

Study Circle Annual Programme on 24.02.2013

FEMA on 16.02.2013

CA. Maulik Mehta, CA. Ashish Parikh & CA. Yash Bhatt

Participants

WICASA Events

Participants

Mr. Ashish RajmaniCA. Chirag Baxi CA. Rajesh Gandhi Ms. Jayanti RoychoudhariK. Neethi Raghavan

Dias on FEMA

Celebration of Valentines Day at Old Age Home 14.02.13 “Present Your Dream Budget” competition on 23.02.13

11

DISCLAIMER :

[email protected]/[email protected]

The ICAI and the Baroda Branch of WIRC of ICAI is not in any way responsible for the result of any action taken on the basis of the advertisement published in the Newsletter.

The members, however, may bear in mind the provisions of the Code of Ethics while responding to the advertisements. The views and opinion expressed or implied in the Newsletter are

those of the authors / contributors and do not necessarily reflect those of Baroda Branch. Unsolicited matters are sent at the owner's risk and the publisher accepts no liability for loss or

damage. Material in this publication may not be reproduced, whether in part or in whole, without the consent of Baroda Branch. Members are requested to kindly send material of

professional interest to . The same may be published in the newsletter subject to availability of space & editorial editing.

If undelivered, please return to :

Baroda Branch of WIRC of

The Institute of Chartered Accountants of India

www.baroda-icai.org WIRC : www.wirc-icai.org ICAI: www.icai.orgl l

Back Cover (4 color) 15,000 Inside Front/ Cover (4 color)Back 10,000 Full Page (1 Color) 7,500 Half Page (1 Color) 5,000

ADVERTISEMENT TARIFF : * Discount - 3 to 6 issue of 10%, 7 to 12 issue 15% * Circulated to more than 1800 Chartered Accountants

ADVERTISEMENTS :

SUBSCRIPTION RATES :

PRINTED AND PUBLISHED BY : Published at

The tariff for advertising given below are duly approved by the Managing Committee of the Baroda Branch. Advertisements are received directly by the Branch and no

advertising agency has been appointed for this purpose.

This Newsletter is circulated without any charges to its members and other important categories of recipients as per ICAI Advisory on Newsletters. Subscription

rate is Rs. 20/- per issue for others.

CA. Pradeep Agrawal on behalf of Baroda Branch of WIRC of ICAI. “ICAI Bhawan”, Kalali-Tandalja Road, Atladra, Vadodara - 390 012

Multiprints, 30/B, Gandhi Oil Mill Compound, Near BIDC, Gorwa, Vadodara - 390016. Ph.: 0265-2285592Printed at

“ICAI Bhawan”, Kalali-Tandalja Road,

Atladra, Vadodara - 390 012.

Telefax : +91 265 2681115 / 2680593

Baroda Branch of WIRC of ICAI

I do not know the word 'quit.' Either I never did, or I have abolished it.- Susan Butcher

HONGKONG – -from

24th May ’13 to 31st May ’13 (Friday to Friday)

MACAU SHENZHEN

INTERNATIONALRESIDENTIAL REFRESHER COURSE

(RRC)

@Hotels No. of days /

& nights

Names of Hotel

HONGKONG 3 Nights / 3 Days Royal View Hotel or similar 4 Star Hotel

MACAU 2 Nights / 3 Days Venetian Hotel – World’s Best 5 Star Hotel

SHENZHEN 1 Night / 1 Day Century Plaza or similar 4 Star Hotel

Tour cost: Amount (Rs.) Inclusions

Adult Per Person Twin Sharing Rs. 87,000/- Economy Class return airfare Ex. Ahmedabad.

Airport Taxes (Any fluctuation in the taxes may

reflect on the Tour Cost)

Hong Kong, Macau & Shenzhen visa are on arrival

without cost

To & Fro : Baroda - A’bad by Bus.

*Payments to be made by Cheque / DDs payable at Baroda are to be drawn on “Baroda Branch of WIRC of ICAI”

�

�

�

�

Child with bed Rs. 75,000/-

Child no bed Rs. 65,500/-

Baroda Branch requests its Members to register their name

in advance as seats are limited to 40 people. Registration

will be based on “First Come – First Serve” basis.

BARODA BRANCH ON 2680593, 2681115.

FOR ANY ENQUIRY CONTACT

CHAIRMAN, BARODA BRANCH.

M. No. 9825231545

REGISTER YOUR NAME WITH

CA ASHISH PARIKH,

12