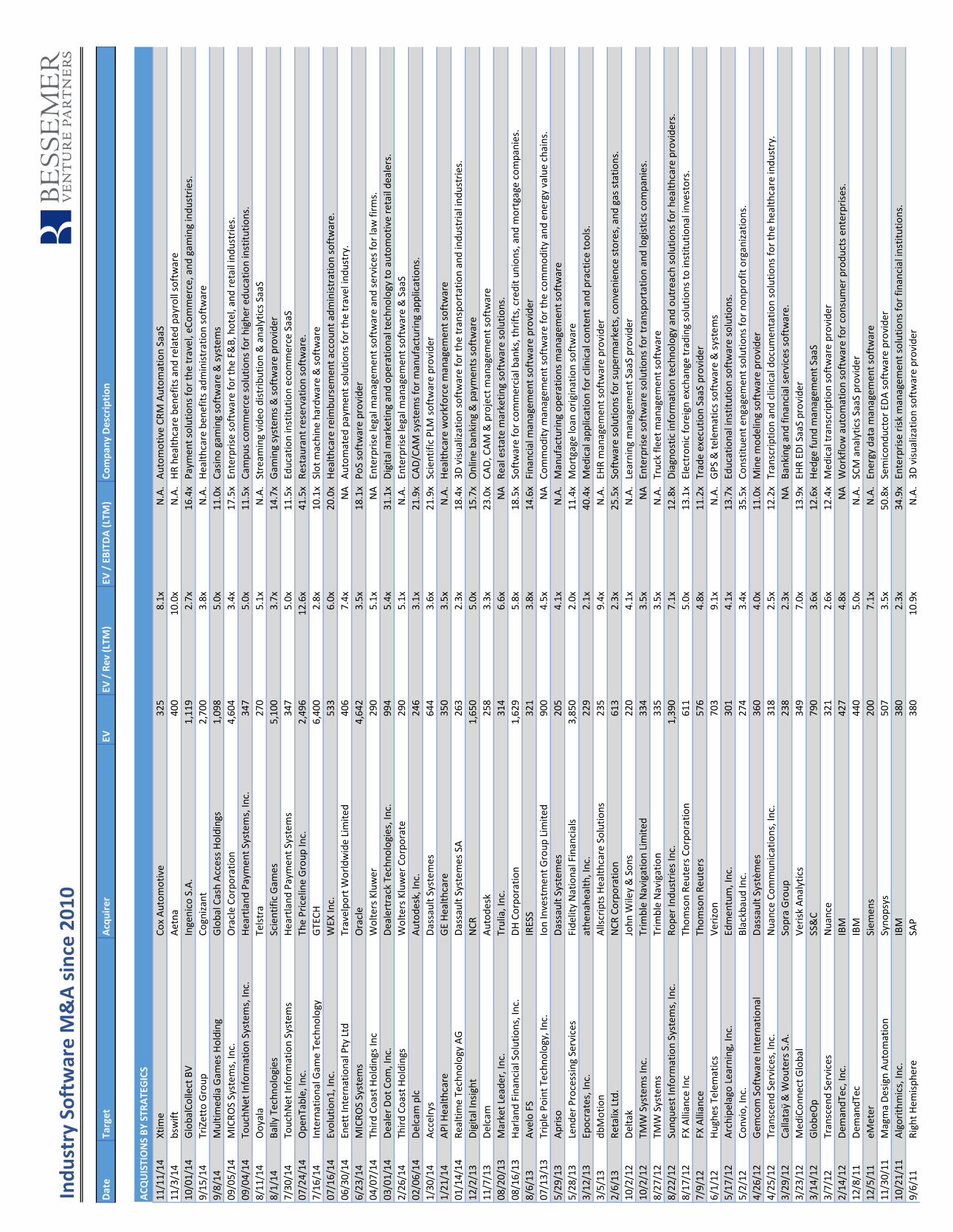

the industry software · pdf fileglobalcollect bv ingenico s.a. 1,119 2.7x 16.4x payment...

TRANSCRIPT

The Industry Software RevolutionBrian Feinstein and Trevor Oelschig

bvp.com2

THE CLOUD’S UNSUNG HERO

Industry-specific cloud software companies don’t get as much attention as their horizontal brethren like Salesforce or Workday. Why? It’s been assumed that the markets they serve are simply too small and sleepy. We think that’s misguided.

While companies like Guidewire, athenahealth, DealerTrack, Veeva, Demandware, and RealPage don’t get much fanfare in the press, they are solving real problems in each of their industries. And they have quietly grown to become multi-billion-dollar publicly-traded companies.

This is just the beginning. We’re convinced that many more industries—from banking to mining to agriculture—will be transformed by ditching their legacy vendors and migrating to the cloud.

bvp.com3

AN INDUSTRY SOFTWARE REVOLUTIONWe think there are a few important drivers that make the opportunity to build industry-specific software larger than ever before:

The executives in charge of purchase decisions are a new generation of technology-savvy buyers. They understand that technology is a critical source of competitive advantage. This dynamic can fuel an industry arms race in which all companies in an industry are forced to adopt software as it quickly moves from a “nice to have” to “table stakes.”

A Changing Philosophy Among Buyers

1

This creates a unique opportunity for those that do succeed. Industry insiders talk to each other. They attend the same conferences and run in the same circles. When it comes to software, they typically buy what their peers buy. This creates a virtuous cycle of adoption—resulting in “winner takes most” market share for leaders. And once established as the “gold standard”, the door is open for leaders to cross-sell additional applications.

Winner-Takes-Most Dynamics

2

Cloud and mobile have made software more useful than ever before. Software is now used in the field via mobile devices, in a collaborative web environment, in conjunction with other web services, in a consumer-like user experience, and in a way that doesn’t require a dedicated IT support staff. This has dramatically increased the number and types of customers that can be served by industry software.Cloud/Mobile Capabilities

3

bvp.com4

The most common and most successful playbook to date. While a handful of publicly-traded industry-specific companies that are native to the cloud have emerged, it is still early days. Hundreds of industries are still held captive by terrible software or have been neglected altogether and so are ripe for innovation.

Replace Sleepy Incumbents

1

Cloud software can not only help a business run more effi-ciently, it can also bring a business closer to its customers. Companies like OpenTable drive revenue with features for its end consumers. This was never possible with installed soft-ware.

Help Customers Find New Ways to Grow

2

Enterprise software historically catered only to people at their desks. But today’s mobile apps can make a field worker’s day far more productive, freeing up hours that would otherwise be spent physically filling out forms and pushing paperwork. This slows down everything from real estate (broker updates of listings) to hotels (housekeeping) to transportation (repair logs) to restaurants (food inspections) to local governments (work orders to fix potholes). Data entry and workflow challenges are just the tip of the iceberg—virtually every aspect of enterprise activity in the field will be reimagined thanks to mobile devices.

Focus on the Mobile User

3

PLAYBOOKS THAT EXCITE USWe don’t always get it right, but we’ve been fortunate to learn from many of the best teams in the industry and have picked up quite a bit from them over the years. Here are a few ways we think founders can build big businesses within specific industries:

bvp.com5

PLAYBOOKS THAT EXCITE US (Cont.)

When most people think of software, they imagine a stand-alone product. But cloud connectivity and APIs allow industry cloud software companies to become platforms with an ecosystem of applications around them. We love the plat-form model because it drives long-term customer lock-in. If your customers rely on you to act as the hub for other criti-cal applications, it becomes extremely difficult for any new competitors to replace you.

Build a Platform

5

Not long ago, small businesses were off-limits. It was simply too expensive to hire sales teams to reach them. It was just as problematic to get software up and running. The world is very different today, thanks to the Internet. The key to making this playbook work is to build software with the simplicity of a consumer product.

Attack the SMB Market

4

Customer data used to be siloed in a company's data center. The cloud now makes it possible to aggregate data and draw insights for a company’s customers. Data enables software to do unprecedented things like benchmarking, predictive analytics, and connecting suppliers and buyers between organizations.

Tap into Data at Cloud Scale

6

bvp.com6

PLAYBOOKS THAT EXCITE US (Cont.)

We are in the midst of a hardware revolution. And software is powering it. New hardware platforms will prompt an era of profound opportunity to harness the power of software for industry. Some of the emerging platforms we are excited about include wearables, robots, drones, sensors, and satel-lites. These devices are becoming increasingly inexpensive, powerful, connected, and ubiquitous. We expect to see a new generation of software built to take advantage of these devices with industry-specific applications.

Look to Emerging Hardware Platforms

7

Occasionally, technology is so revolutionary that it can trans-form the way an entire industry works. This is perhaps the most compelling opportunity—an industry-focused startup that uses its software to reshape an industry rather than just selling tools to existing industry incumbents.

Uber is perhaps the best example of this. Uber didn’t build a software application to connect livery companies with pas-sengers. Instead, it used technology to fundamentally change how we book cars. Amazon is using technology to reimagine retail. Airbnb is using software to transform the hospitality sector. And LendingClub is reinventing how the financial markets connect borrowers with capital. These companies don’t feel like technology businesses or application vendors—instead, they are using technology to fundamen-tally reshape the way a good or service is delivered.

A company that reimagines an industry is the most difficult type of company to build. But because it captures much more of the value chain, it also tends to have the biggest upside. Building a company that will see the world differently seems like a lofty goal, but it’s been proven possible. And we think it is inevitable that visionary founders will continue to transform the way we consume industries like financial services, healthcare, education, and real estate.

Transform an Entire Industry

8

bvp.com7

Bankingcontinues to be controlled by core vendors like FIS, Fiserv, and Jack Henry, which use their footprint in core transac-tional systems to cross-sell mediocre point solutions. As a new generation of executives drives purchasing decisions, we expect to see best-of-breed cloud entrants give the core vendors a run for their money.

Governmentis responsible for more IT spending than any other industry but is dominated by dinosaurs like Tyler Technologies, Con-stellation, Infor, and SunGard – all of whom are focused on cash flow and not innovation.

Asset-heavy industrieslike oil and gas, mining, agriculture, manufacturing, and industrials have historically lacked innovative software startups altogether. This will change. Many of the trends we have discussed – including mobility and hardware platforms – are particularly well-suited for these markets.

INDUSTRIES RIPE FOR INNOVATIONWe are far more excited to have founders tell us about industry software opportunities than being prescriptive about where the opportunities lie. With that said, here are a few broad industries that we think are ripe for innovation:

bvp.com8

INDUSTRIES RIPE FOR INNOVATION (Cont.)

Healthcareis a trillion dollar plus industry that continues to be largely operated with paper, fax, and the phone. Large electronic medical record companies like Epic and McKesson built out their systems in the 1970s and 1980s, and we see opportuni-ties for newer cloud competitors to gain share.

Real Estatehas been dominated by a handful of full-suite solutions like RealPage, Yardi, and MRI. Innovative best-of-breed point solutions are taking share from these players and technology-oriented service providers are aiming to trans-form the brokerage industry.

Manufacturingrepresents one of the largest sectors in the economy and drove the growth of software behemoths like SAP, Infor, JDA, and others. This industry has been slow to migrate to the cloud and we expect to see a wave of new cloud innovators take share from the incumbents.

bvp.com9

INDUSTRIES RIPE FOR INNOVATION (Cont.)

Legalis dominated by powerhouses like Thomson Reuters and Lexis Nexis. As large practices see increased pressure to cut costs, we expect a new generation of players to challenge the old guard. And as small practices move away from paper and pencil, new technology will emerge.

Local Servicesare all about SMBs, who have historically lacked access to software. With the cloud making it easy to sell software to SMBs, we're seeing a wave of solutions emerge for local restaurants, yoga studios, home services providers, hotels, and retailers.

Educationis seeing a wave of innovators take share from the likes of Blackboard (software), Apollo (for-profit university), and Pearson (publishing). New delivery models are filling the void left in higher education and the “skills gap” arenas. Cloud-based software solutions are taking share from Blackboard. And new content platforms are transforming the way that education content is delivered.

bvp.com10

CommunicationFinancial ServicesHospitality & Leisure

Real EstateLocal ServicesLegal

EducationConstruction

RetailHealthcare

BVP'S INDUSTRY CLOUD PORTFOLIOCurrent Companies

bvp.com11

acq. by Cox IPO acq. by Towers Watson

IPO acq. by Genstar IPO

IPO acq. by Nielsen acq. by Cisco

BVP'S INDUSTRY CLOUD PORTFOLIOExited Companies

Ind

ust

ry S

oft

war

e M

&A

sin

ce 2

01

0

Dat

eTa

rget

Acq

uir

erEV

EV /

Rev

(LT

M)

EV /

EB

ITD

A (

LTM

)C

om

pan

y D

escr

ipti

on

AC

QU

ISTI

ON

S B

Y S

TRA

TEG

ICS

11/1

1/14

Xti

me

Co

x A

uto

mo

tive

32

5

8.

1x

N

.A.

A

uto

mo

tive

CR

M A

uto

mat

ion

Saa

S

11/3

/14

bsw

ift

Aet

na

40

0

10

.0x

N

.A.

H

R h

ealt

hca

re b

enef

its

and

rel

ated

pay

roll

soft

war

e

10/0

1/14

Glo

bal

Co

llect

BV

Inge

nic

o S

.A.

1,11

9

2.7x

16.4

x

Pay

men

t so

luti

on

s fo

r th

e tr

avel

, eC

om

mer

ce, a

nd

gam

ing

ind

ust

ries

.

9/15

/14

TriZ

etto

Gro

up

Co

gniz

ant

2,70

0

3.8x

N.A

.

Hea

lth

care

ben

efit

s ad

min

istr

atio

n s

oft

war

e

9/8/

14M

ult

imed

ia G

ames

Ho

ldin

gG

lob

al C

ash

Acc

ess

Ho

ldin

gs1,

098

5.

0x

11

.0x

C

asin

o g

amin

g so

ftw

are

& s

yste

ms

09/0

5/14

MIC

RO

S Sy

stem

s, In

c.O

racl

e C

orp

ora

tio

n4,

604

3.

4x

17

.5x

En

terp

rise

so

ftw

are

for

the

F&B

, ho

tel,

and

ret

ail i

nd

ust

ries

.

09/0

4/14

Tou

chN

et In

form

atio

n S

yste

ms,

Inc.

Hea

rtla

nd

Pay

men

t Sy

stem

s, In

c.3

47

5.0x

11.5

x

Cam

pu

s co

mm

erce

so

luti

on

s fo

r h

igh

er e

du

cati

on

inst

itu

tio

ns.

8/11

/14

Oo

yala

Tels

tra

27

0

5.

1x

N

.A.

St

ream

ing

vid

eo d

istr

ibu

tio

n &

an

alyt

ics

SaaS

8/1/

14B

ally

Tec

hn

olo

gies

Scie

nti

fic

Gam

es5,

100

3.

7x

14

.7x

G

amin

g sy

stem

s &

so

ftw

are

pro

vid

er

7/30

/14

Tou

chN

et In

form

atio

n S

yste

ms

Hea

rtla

nd

Pay

men

t Sy

stem

s3

47

5.0x

11.5

x

Edu

cati

on

inst

itu

tio

n e

com

mer

ce S

aaS

07/2

4/14

Op

enTa

ble

, In

c.Th

e P

rice

line

Gro

up

Inc.

2,49

6

12.6

x

41.5

x

Res

tau

ran

t re

serv

atio

n s

oft

war

e.

7/16

/14

Inte

rnat

ion

al G

ame

Tech

no

logy

GTE

CH

6,40

0

2.8x

10.1

x

Slo

t m

ach

ine

har

dw

are

& s

oft

war

e

07/1

6/14

Evo

luti

on

1, In

c.W

EX In

c.5

33

6.0x

20.0

x

Hea

lth

care

rei

mb

urs

emen

t ac

cou

nt

adm

inis

trat

ion

so

ftw

are.

06/3

0/14

Enet

t In

tern

atio

nal

Pty

Ltd

Trav

elp

ort

Wo

rld

wid

e Li

mit

ed4

06

7.4x

NA

Au

tom

ated

pay

men

t so

luti

on

s fo

r th

e tr

avel

ind

ust

ry.

6/23

/14

MIC

RO

S Sy

stem

sO

racl

e4,

642

3.

5x

18

.1x

P

oS

soft

war

e p

rovi

der

04/0

7/14

Thir

d C

oas

t H

old

ings

Inc

Wo

lter

s K

luw

er2

90

5.1x

NA

Ente

rpri

se le

gal m

anag

emen

t so

ftw

are

and

ser

vice

s fo

r la

w f

irm

s.

03/0

1/14

Dea

ler

Do

t C

om

, In

c.D

eale

rtra

ck T

ech

no

logi

es, I

nc.

99

4

5.

4x

31

.1x

D

igit

al m

arke

tin

g an

d o

per

atio

nal

tec

hn

olo

gy t

o a

uto

mo

tive

ret

ail d

eale

rs.

2/26

/14

Thir

d C

oas

t H

old

ings

Wo

lter

s K

luw

er C

orp

ora

te2

90

5.1x

N.A

.

Ente

rpri

se le

gal m

anag

emen

t so

ftw

are

& S

aaS

02/0

6/14

Del

cam

plc

Au

tod

esk,

Inc.

24

6

3.

1x

21

.9x

C

AD

/CA

M s

yste

ms

for

man

ufa

ctu

rin

g ap

plic

atio

ns.

1/30

/14

Acc

elry

sD

assa

ult

Sys

tem

es6

44

3.6x

21.9

x

Scie

nti

fic

PLM

so

ftw

are

pro

vid

er

1/21

/14

AP

I Hea

lth

care

GE

Hea

lth

care

35

0

3.

5x

N

.A.

H

ealt

hca

re w

ork

forc

e m

anag

emen

t so

ftw

are

01/1

4/14

Rea

ltim

e Te

chn

olo

gy A

GD

assa

ult

Sys

tem

es S

A2

63

2.3x

18.4

x

3D v

isu

aliz

atio

n s

oft

war

e fo

r th

e tr

ansp

ort

atio

n a

nd

ind

ust

rial

ind

ust

ries

.

12/2

/13

Dig

ital

Insi

ght

NC

R1,

650

5.

0x

15

.7x

O

nlin

e b

anki

ng

& p

aym

ents

so

ftw

are

11/7

/13

Del

cam

Au

tod

esk

25

8

3.

3x

23

.0x

C

AD

, CA

M &

pro

ject

man

agem

ent

soft

war

e

08/2

0/13

Mar

ket

Lead

er, I

nc.

Tru

lia, I

nc.

31

4

6.

6x

N

A

R

eal e

stat

e m

arke

tin

g so

ftw

are

solu

tio

ns.

08/1

6/13

Har

lan

d F

inan

cial

So

luti

on

s, In

c.D

H C

orp

ora

tio

n1,

629

5.

8x

18

.5x

So

ftw

are

for

com

mer

cial

ban

ks, t

hri

fts,

cre

dit

un

ion

s, a

nd

mo

rtga

ge c

om

pan

ies.

8/6/

13A

velo

FS

IRES

S3

21

3.8x

14.6

x

Fin

anci

al m

anag

emen

t so

ftw

are

pro

vid

er

07/1

3/13

Trip

le P

oin

t Te

chn

olo

gy, I

nc.

Ion

Inve

stm

ent

Gro

up

Lim

ited

90

0

4.

5x

N

A

C

om

mo

dit

y m

anag

emen

t so

ftw

are

for

the

com

mo

dit

y an

d e

ner

gy v

alu

e ch

ain

s.

5/29

/13

Ap

riso

Das

sau

lt S

yste

mes

20

5

4.

1x

N

.A.

M

anu

fact

uri

ng

op

erat

ion

s m

anag

emen

t so

ftw

are

5/28

/13

Len

der

Pro

cess

ing

Serv

ices

Fid

elit

y N

atio

nal

Fin

anci

als

3,85

0

2.0x

11.4

x

Mo

rtga

ge lo

an o

rigi

nat

ion

so

ftw

are

3/12

/13

Epo

crat

es, I

nc.

ath

enah

ealt

h, I

nc.

22

9

2.

1x

40

.4x

M

edic

al a

pp

licat

ion

fo

r cl

inic

al c

on

ten

t an

d p

ract

ice

too

ls.

3/5/

13d

bM

oti

on

Alls

crip

ts H

ealt

hca

re S

olu

tio

ns

23

5

9.

4x

N

.A.

EH

R m

anag

emen

t so

ftw

are

pro

vid

er

2/6/

13R

etal

ix L

td.

NC

R C

orp

ora

tio

n6

13

2.3x

25.5

x

Soft

war

e so

luti

on

s fo

r su

per

mar

kets

, co

nve

nie

nce

sto

res,

an

d g

as s

tati

on

s.

10/2

/12

Del

tak

Joh

n W

iley

& S

on

s2

20

4.1x

N.A

.

Lear

nin

g m

anag

emen

t Sa

aS p

rovi

der

10/2

/12

TMW

Sys

tem

s In

c.Tr

imb

le N

avig

atio

n L

imit

ed3

34

3.5x

NA

Ente

rpri

se s

oft

war

e so

luti

on

s fo

r tr

ansp

ort

atio

n a

nd

logi

stic

s co

mp

anie

s.

8/27

/12

TMW

Sys

tem

sTr

imb

le N

avig

atio

n3

35

3.5x

N.A

.

Tru

ck f

lee

t m

anag

emen

t so

ftw

are

8/22

/12

Sun

qu

est

Info

rmat

ion

Sys

tem

s, In

c.R

op

er In

du

stri

es In

c.1,

390

7.

1x

12

.8x

D

iagn

ost

ic in

form

atio

n t

ech

no

logy

an

d o

utr

each

so

luti

on

s fo

r h

ealt

hca

re p

rovi

der

s.

8/17

/12

FX A

llian

ce In

cTh

om

son

Reu

ters

Co

rpo

rati

on

61

1

5.

0x

13

.1x

El

ectr

on

ic f

ore

ign

exc

han

ge t

rad

ing

solu

tio

ns

to in

stit

uti

on

al in

vest

ors

.

7/9/

12FX

Alli

ance

Tho

mso

n R

eute

rs5

76

4.8x

11.2

x

Trad

e ex

ecu

tio

n S

aaS

pro

vid

er

6/1/

12H

ugh

es T

elem

atic

sV

eri

zon

70

3

9.

1x

N

.A.

G

PS

& t

elem

atic

s so

ftw

are

& s

yste

ms

5/17

/12

Arc

hip

elag

o L

earn

ing,

Inc.

Edm

entu

m, I

nc.

30

1

4.

1x

13

.7x

Ed

uca

tio

nal

inst

itu

tio

n s

oft

war

e so

luti

on

s.

5/2/

12C

on

vio

, In

c.B

lack

bau

d In

c.2

74

3.4x

35.5

x

Co

nst

itu

ent

enga

gem

ent

solu

tio

ns

for

no

np

rofi

t o

rgan

izat

ion

s.

4/26

/12

Gem

com

So

ftw

are

Inte

rnat

ion

alD

assa

ult

Sys

tèm

es3

60

4.0x

11.0

x

Min

e m

od

elin

g so

ftw

are

pro

vid

er

4/25

/12

Tran

scen

d S

ervi

ces,

Inc.

Nu

ance

Co

mm

un

icat

ion

s, In

c.3

18

2.5x

12.2

x

Tran

scri

pti

on

an

d c

linic

al d

ocu

men

tati

on

so

luti

on

s fo

r th

e h

ealt

hca

re in

du

stry

.

3/29

/12

Cal

lata

ÿ &

Wo

ute

rs S

.A.

Sop

ra G

rou

p2

38

2.3x

NA

Ban

kin

g an

d f

inan

cial

ser

vice

s so

ftw

are.

3/23

/12

Med

iCo

nn

ect

Glo

bal

Ve

risk

An

alyt

ics

34

9

7.

0x

13

.9x

EH

R E

DI S

aaS

pro

vid

er

3/14

/12

Glo

beO

pSS

&C

79

0

3.

6x

12

.6x

H

edge

fu

nd

man

agem

ent

SaaS

3/7/

12Tr

ansc

end

Ser

vice

sN

uan

ce3

21

2.6x

12.4

x

Med

ical

tra

nsc

rip

tio

n s

oft

war

e p

rovi

der

2/14

/12

Dem

and

Tec,

Inc.

IBM

42

7

4.

8x

N

A

W

ork

flo

w a

uto

mat

ion

so

ftw

are

for

con

sum

er p

rod

uct

s en

terp

rise

s.

12/8

/11

Dem

and

Tec

IBM

44

0

5.

0x

N

.A.

SC

M a

nal

ytic

s Sa

aS p

rovi

der

12/5

/11

eMet

erSi

emen

s2

00

7.1x

N.A

.

Ener

gy d

ata

man

agem

ent

soft

war

e

11/3

0/11

Mag

ma

Des

ign

Au

tom

atio

nSy

no

psy

s5

07

3.5x

50.8

x

Sem

ico

nd

uct

or

EDA

so

ftw

are

pro

vid

er

10/2

1/11

Alg

ori

thm

ics,

Inc.

IBM

38

0

2.

3x

34

.9x

En

terp

rise

ris

k m

anag

emen

t so

luti

on

s fo

r fi

nan

cial

inst

itu

tio

ns.

9/6/

11R

igh

t H

emis

ph

ere

SAP

38

0

10

.9x

N

.A.

3D

vis

ual

izat

ion

so

ftw

are

pro

vid

er

Ind

ust

ry S

oft

war

e M

&A

sin

ce 2

01

0

Dat

eTa

rget

Acq

uir

erEV

EV /

Rev

(LT

M)

EV /

EB

ITD

A (

LTM

)C

om

pan

y D

escr

ipti

on

8/16

/11

Ren

aiss

ance

Lea

rnin

gP

erm

ira

Fun

ds

44

6

3.

3x

11

.7x

Ed

uca

tio

nal

so

ftw

are

pro

vid

er

8/10

/11

Seis

mic

Mic

ro-T

ech

no

logy

, In

c.IH

S In

c.5

02

8.4x

20.2

x

Geo

scie

nce

inte

rpre

tati

on

so

ftw

are

for

the

exp

lora

tio

n a

nd

pro

du

ctio

n in

du

stry

.

6/30

/11

Ap

ach

e D

esig

n S

olu

tio

ns

AN

SYS

30

6

6.

7x

N

.A.

Se

mic

on

du

cto

r ED

A s

oft

war

e p

rovi

der

6/14

/11

Exp

lore

Info

rmat

ion

Ser

vice

s, L

LCC

laim

s Se

rvic

es G

rou

p, I

nc.

51

9

6.

6x

16

.7x

D

ata

and

an

alyt

ic t

oo

ls f

or

the

auto

mo

tive

pro

per

ty a

nd

cas

ual

ty in

sure

rs.

5/13

/11

RP

Dat

a P

ty L

td.

Co

reLo

gic,

Inc.

29

4

4.

7x

13

.4x

P

rop

erty

info

rmat

ion

an

d r

isk

man

agem

ent

solu

tio

ns

for

the

real

est

ate

ind

ust

ry.

5/9/

11Te

kla

Co

rpo

rati

on

Trim

ble

Nav

igat

ion

47

5

5.

5x

25

.3x

C

on

stru

ctio

n in

du

stry

so

ftw

are

pro

vid

er

4/30

/11

Loo

pN

et, I

nc.

Co

Star

Gro

up

, In

c.7

52

8.2x

30.3

x

On

line

mar

ketp

lace

fo

r b

uyi

ng

and

sel

ling

com

mer

cial

rea

l est

ate.

4/26

/11

Sch

oo

lNet

Pea

rso

n2

30

3.1x

N.A

.

Edu

cati

on

man

agem

ent

soft

war

e p

rovi

der

3/24

/11

Mo

rtga

geb

ot

Dav

is +

Hen

der

son

23

2

6.

2x

11

.5x

M

ort

gage

ori

gin

atio

n s

oft

war

e p

rovi

der

3/1/

11So

ph

is T

ech

no

logy

Lim

ited

Mis

ys p

lc (

nka

:Mis

ys L

imit

ed)

60

4

5.

9x

N

A

P

ort

folio

an

d r

isk

man

agem

ent

soft

war

e fo

r th

e fi

nan

cial

ind

ust

ry.

1/14

/11

No

rko

m T

ech

no

logi

esB

AE

Syst

ems

23

2

3.

6x

27

.0x

Fi

nan

cial

an

ti-f

rau

d s

oft

war

e p

rovi

der

12/7

/10

Med

icit

yA

etn

a5

00

16.7

x

N.A

.

Hea

lth

care

info

rmat

ion

exc

han

ge s

oft

war

e

9/7/

10C

ham

ber

linEd

mo

nd

sEm

deo

n2

60

3.0x

11.9

x

Pat

ien

t sc

ree

nin

g an

d e

nro

llmen

t so

ftw

are

pro

vid

er

8/24

/10

Eclip

sys

Co

rpo

rati

on

Alls

crip

ts S

olu

tio

ns,

Inc.

1,17

0

2.3x

21.6

x

Clin

ical

, rev

enu

e cy

cle,

an

d p

erfo

rman

ce m

anag

emen

t so

ftw

are.

8/11

/10

Ph

ase

Forw

ard

Inc.

Ora

cle

Co

rpo

rati

on

59

1

2.

7x

19

.5x

In

tegr

ated

clin

ical

res

earc

h s

uit

e fo

r lif

e sc

ien

ces

com

pan

ies.

6/9/

10Ec

lipsy

sA

llscr

ipts

Hea

lth

care

So

luti

on

s1,

181

2.

3x

16

.9x

EH

R m

anag

emen

t so

ftw

are

pro

vid

er

6/1/

10R

iskM

etri

cs G

rou

p, L

LCM

SCI I

nc.

1,61

9

5.3x

16.2

x

Ris

k m

anag

emen

t an

d g

ove

rnan

ce s

olu

tio

ns

for

the

fin

anci

al s

ervi

ces

mar

ket.

5/27

/10

Ve

nty

x, In

c.A

BB

Ltd

.1,

000

4.

0x

N

A

En

terp

rise

so

ftw

are

for

ener

gy, d

efen

se, a

nd

tra

nsp

ort

atio

n in

du

stri

es.

4/16

/10

Ph

ase

Forw

ard

Ora

cle

74

3

3.

5x

25

.7x

D

ata

man

agem

ent

SaaS

pro

vid

er

3/1/

10R

iskM

etri

cs G

rou

pM

SCI

1,61

2

5.3x

16.3

x

Fin

anci

al r

isk

man

agem

ent

soft

war

e

Mea

n:

$9

03

5.

0x19

.4x

Med

ian

:$

43

3

4.3x

16.5

x

AC

QU

ISIT

ION

S B

Y P

RIV

ATE

EQ

UIT

Y

05/1

2/14

Trav

elC

lick,

Inc.

Tho

ma

Bra

vo9

30

3.1x

13.1

x

Rev

enu

e-ge

ner

atin

g so

luti

on

s fo

r h

ote

liers

.

2/18

/14

AFS

Tec

hn

olo

gies

Co

urt

Sq

uar

e3

03

3.7x

11.3

x

Trad

e p

rom

oti

on

man

agem

ent

12/3

1/13

Tota

l Sp

ecif

ic S

olu

tio

ns

(TSS

) B

.V.

Co

nst

ella

tio

n S

oft

war

e3

29

1.4x

NA

Pu

blic

sec

tor

soft

war

e so

luti

on

s.

11/1

5/13

Act

ive

Net

wo

rk, L

LCV

ista

Eq

uit

y P

artn

ers

96

1

2.

1x

63

.6x

Ev

ent

man

agem

ent

soft

war

e so

luti

on

s.

11/0

4/13

Gre

en

way

Med

ical

Tec

hn

olo

gies

, In

c.V

ista

Eq

uit

y P

artn

ers

63

2

4.

7x

N

A

B

usi

nes

s p

roce

ss m

anag

emen

t so

ftw

are

for

the

hea

lth

care

ind

ust

ry.

10/1

0/12

Del

tek,

Inc

Tho

ma

Bra

vo

1,02

9

3.0x

18.2

x

Ente

rpri

se s

oft

war

e fo

r p

rofe

ssio

nal

ser

vice

s an

d g

ove

rnm

ent

con

trac

tin

g se

cto

rs.

08/1

7/12

MM

od

al In

c.O

ne

Equ

ity

Par

tner

s1,

074

2.

3x

9.

6x

Clin

ical

do

cum

enta

tio

n s

olu

tio

ns

for

the

hea

lth

care

ind

ust

ry.

08/1

5/12

Ale

geu

s Te

chn

olo

gies

, LLC

Ligh

tyea

r C

apit

al3

35

2.8x

9.9x

H

ealt

hca

re a

nd

ben

efit

pay

men

t so

luti

on

s.

07/3

0/12

Par

adig

m L

td.

Ap

ax P

artn

ers;

JM

I Eq

uit

y1,

000

5.

0x

N

A

So

ftw

are-

enab

led

so

luti

on

s fo

r th

e o

il an

d g

as in

du

stry

.

7/2/

12M

Mo

dal

On

e Eq

uit

y1,

083

2.

4x

9.

2x

Spee

ch r

eco

gnit

ion

so

ftw

are

pro

vid

er

06/0

1/12

Mis

ys p

lcV

ista

Eq

uit

y P

artn

ers

2,04

2

3.2x

16.4

x

Ban

kin

g an

d f

inan

cial

ser

vice

s so

ftw

are.

4/10

/12

eRes

earc

hTe

chn

olo

gyG

enst

ar C

apit

al3

82

2.1x

8.4x

M

edic

al d

ata

soft

war

e p

rovi

der

3/19

/12

Mis

ysV

ista

Eq

uit

y2,

217

3.

5x

15

.1x

Fi

nan

cial

so

ftw

are

pro

vid

er

11/0

2/11

Emd

eon

Inc.

Hel

lman

& F

ried

man

; B

lack

sto

ne

3,30

6

3.1x

13.1

x

Rev

enu

e an

d p

aym

ent

cycl

e m

anag

emen

t fo

r th

e h

ealt

hca

re in

du

stry

.

10/0

4/11

Bla

ckb

oar

d In

c.P

rovi

den

ce E

qu

ity

Par

tner

s1,

767

3.

7x

22

.3x

En

terp

rise

tec

hn

olo

gy a

nd

so

luti

on

s fo

r th

e ed

uca

tio

nal

ind

ust

ry.

9/15

/11

Fun

dte

chG

TCR

29

6

2.

0x

14

.9x

Tr

ansa

ctio

n p

roce

ssin

g so

ftw

are

pro

vid

er

08/2

2/11

Rad

ian

t Sy

stem

s, In

c.N

CR

Co

rpo

rati

on

1,13

9

3.1x

20.7

x

Solu

tio

ns

for

man

agin

g si

te o

per

atio

ns

of

ho

spit

alit

y an

d r

etai

l bu

sin

esse

s.

5/23

/11

Ipre

o H

old

ings

KK

R4

25

3.3x

N.A

.

Secu

riti

es is

suan

ce m

anag

emen

t so

ftw

are

01/3

1/11

Op

enB

et T

ech

no

logi

es L

imit

edV

itru

vian

Par

tner

s LL

P2

92

5.3x

NA

Inte

ract

ive

gam

ing

and

bet

tin

g so

luti

on

s.

10/0

7/10

Hea

lth

Gra

des

, In

c.V

est

ar C

apit

al P

artn

ers

25

6

4.

4x

19

.5x

O

nlin

e in

form

atio

n p

latf

orm

ab

ou

t p

hys

icia

ns

and

ho

spit

als.

07/1

6/10

Logi

bec

Inc.

OM

ERS

Pri

vate

Eq

uit

y2

48

3.5x

10.5

x

Clin

ical

an

d a

dm

inis

trat

ive

info

rmat

ion

sys

tem

s.

Me

an:

$9

55

3.

2x17

.2x

Med

ian

:$

93

0

3.1x

14.0

x

* P

ub

licly

dis

clo

sed

tra

nsa

ctio

ns

ab

ove

$2

00

M o

f EV

. Sp

ecia

l th

an

ks t

o M

ark

Ba

illie

an

d h

is t

eam

at

Stif

el a

nd

Mik

e W

ilkin

s a

nd

his

tea

m a

t H

arr

is W

illia

ms

for

thei

r h

elp

ass

emb

ling

th

is d

ata

.