the indian media & entertainment industry 2017

TRANSCRIPT

The Indian Media & Entertainment Industry

2017Trends & Analysis - Past, Present & Future

Chaitanya ChinchlikarVice President – Whistling Woods International

Vice President – Mukta Arts [email protected]

Source: FICCI-KPMG Report 2017

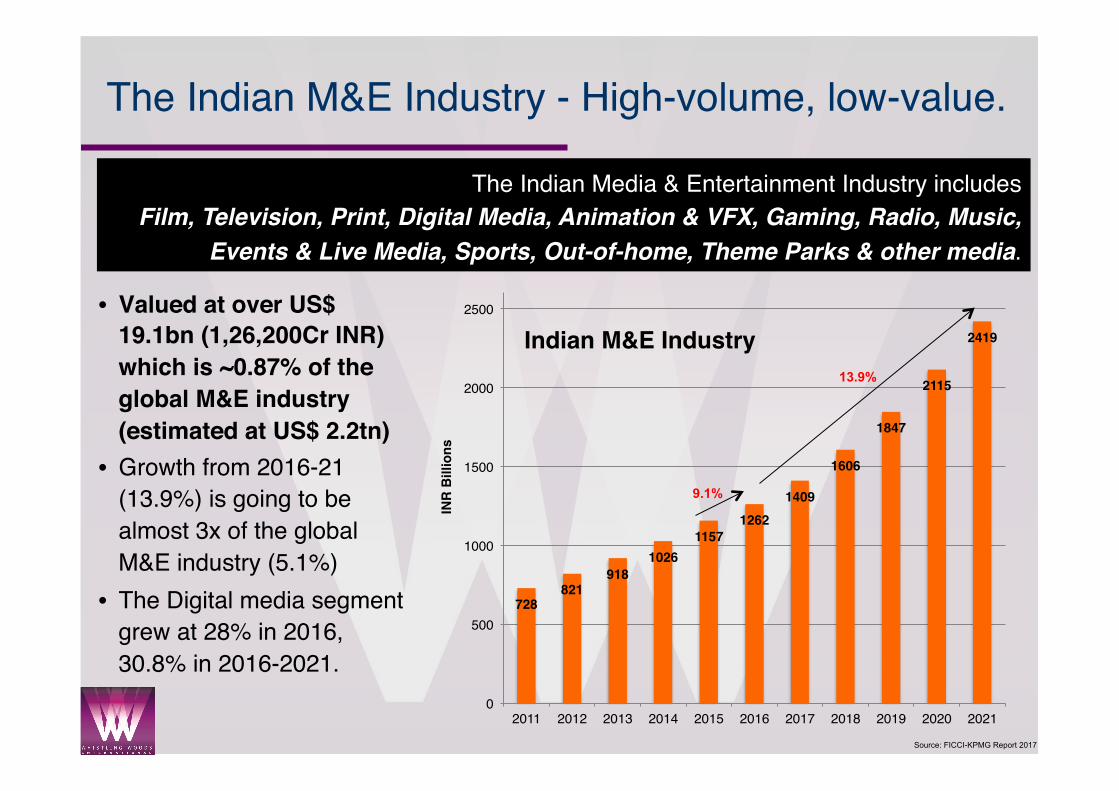

The Indian M&E Industry - High-volume, low-value.

The Indian Media & Entertainment Industry includesFilm, Television, Print, Digital Media, Animation & VFX, Gaming, Radio, Music,

Events & Live Media, Sports, Out-of-home, Theme Parks & other media.

• Valued at over US$ 19.1bn (1,26,200Cr INR) which is ~0.87% of the global M&E industry (estimated at US$ 2.2tn)

• Growth from 2016-21 (13.9%) is going to be almost 3x of the global M&E industry (5.1%)

• The Digital media segment grew at 28% in 2016, 30.8% in 2016-2021.

728821

9181026

11571262

1409

1606

1847

2115

2419

0

500

1000

1500

2000

2500

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

INR

Bill

ions

Indian M&E Industry

9.1%

13.9%

Source: FICCI-KPMG Report 2017

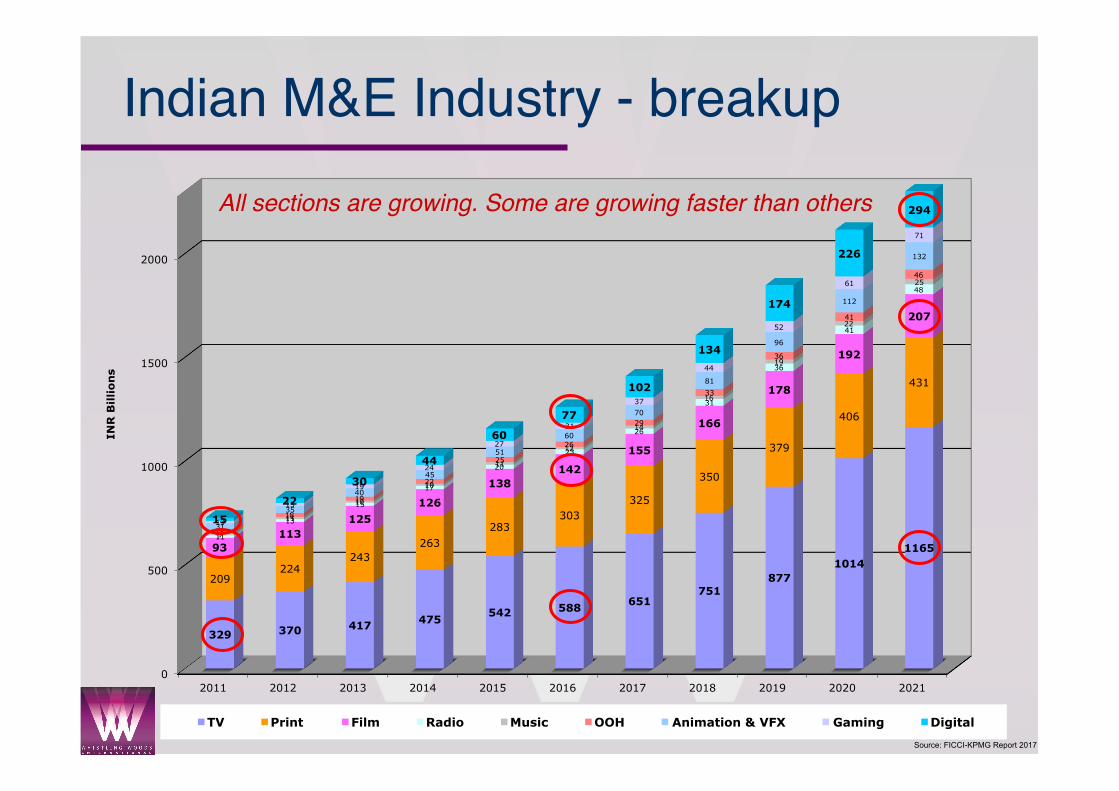

Indian M&E Industry - breakup

0

500

1000

1500

2000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

329 370 417 475 542 588

651 751

877 1014

1165

209 224

243 263

283 303

325

350

379

406

431

93 113

125

126

138 142

155

166

178

192

207

11

13

15

17

20

23

26

31

36

41

48

9

11

10

10

11

12

14

16

19

22

25

18

18

19

22

25

26

29

33

36

41

46

31

35

40

45

51

60

70

81

96

112

132

13

15

19

24

27

31

37

44

52

61

71

15

22

30

44

60

77

102

134

174

226

294

INR

Billio

ns

TV Print Film Radio Music OOH Animation & VFX Gaming Digital

All sections are growing. Some are growing faster than others

Source: FICCI-KPMG Report 2017

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

45% 45% 45% 46% 47% 47% 46% 47% 47% 48% 48%

29% 27% 26% 26% 24% 24% 23% 22% 21% 19% 18%

13% 14% 14% 12% 12% 11% 11% 10% 10% 9%

9%

2% 3% 3% 4% 5% 6% 7% 8% 9% 11% 12%

4% 4% 4% 4% 4% 5% 5% 5% 5% 5% 5%

2% 2% 2% 2% 2% 2% 3% 3% 3% 3% 3%

2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 2% 1% 1% 1% 1% 1% 1% 1% 1% 1% 1% 1%

TV Print Film Digital Animation & VFX Gaming OOH Radio Music

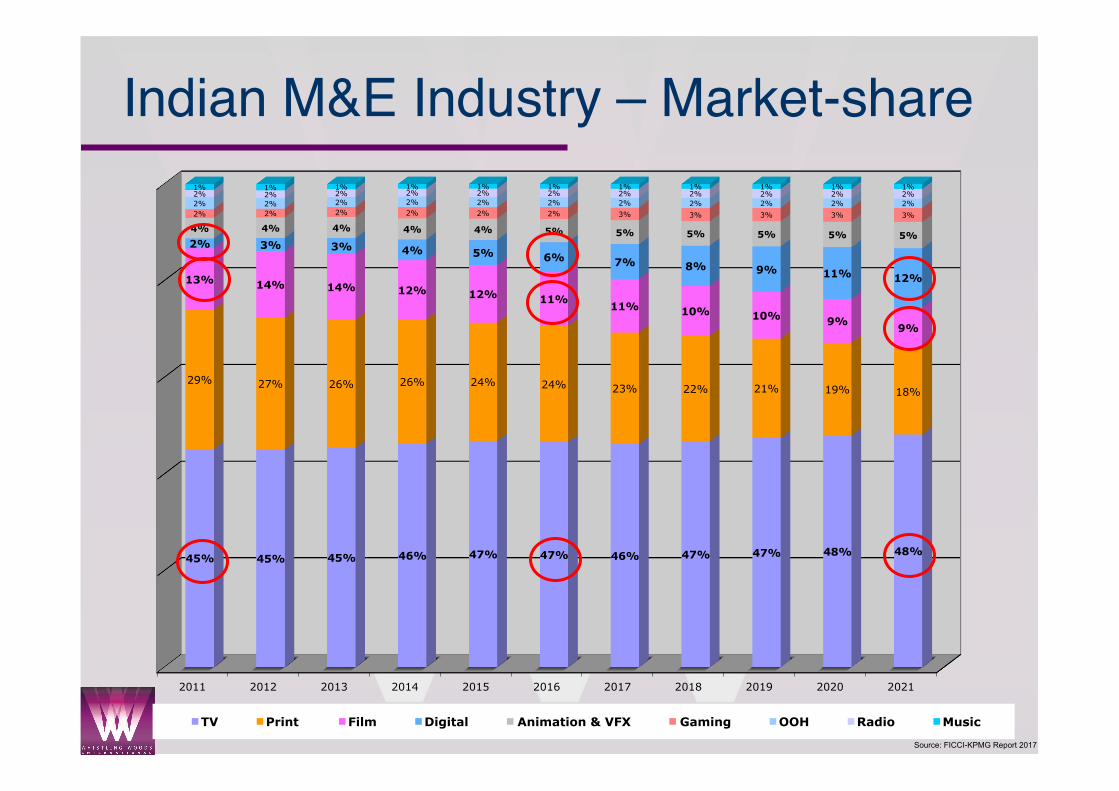

Indian M&E Industry – Market-share

Source: FICCI-KPMG Report 2017

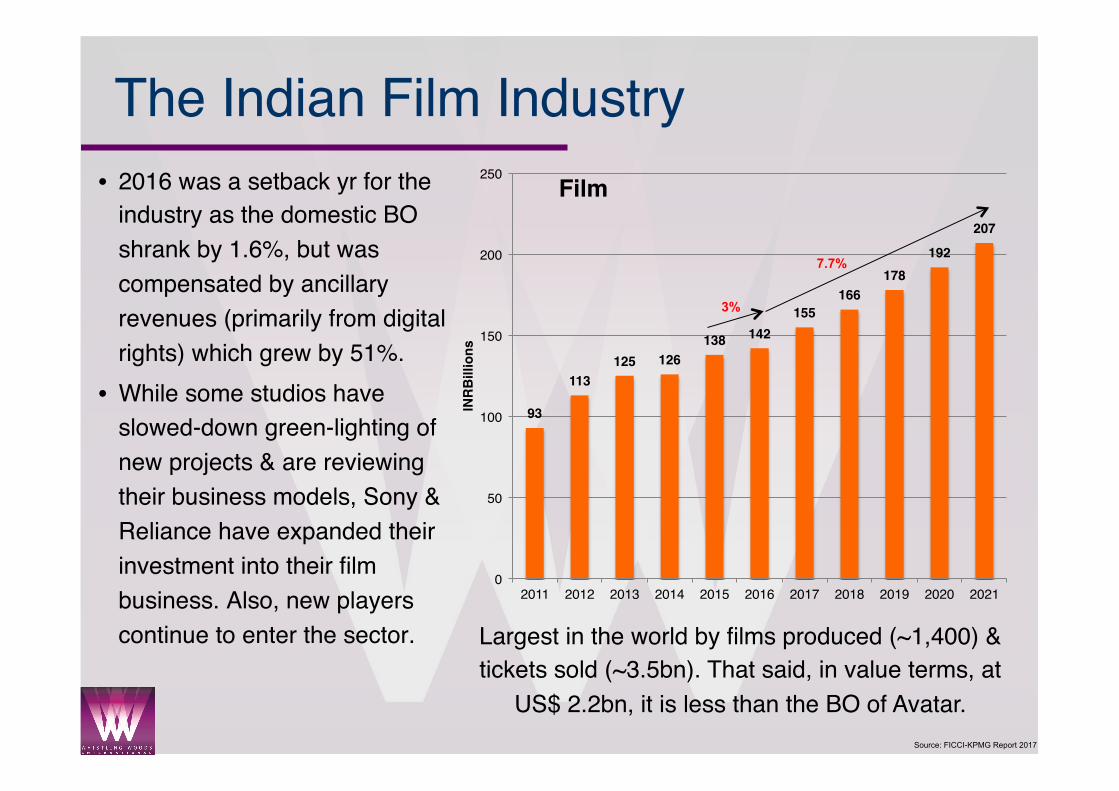

The Indian Film Industry• 2016 was a setback yr for the

industry as the domestic BO shrank by 1.6%, but was compensated by ancillary revenues (primarily from digital rights) which grew by 51%.

• While some studios have slowed-down green-lighting of new projects & are reviewing their business models, Sony & Reliance have expanded their investment into their film business. Also, new players continue to enter the sector. Largest in the world by films produced (~1,400) &

tickets sold (~3.5bn). That said, in value terms, at US$ 2.2bn, it is less than the BO of Avatar.

93

113125 126

138 142155

166178

192

207

0

50

100

150

200

250

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

INR

Bill

ions

Film

3%

7.7%

Source: FICCI-KPMG Report 2017

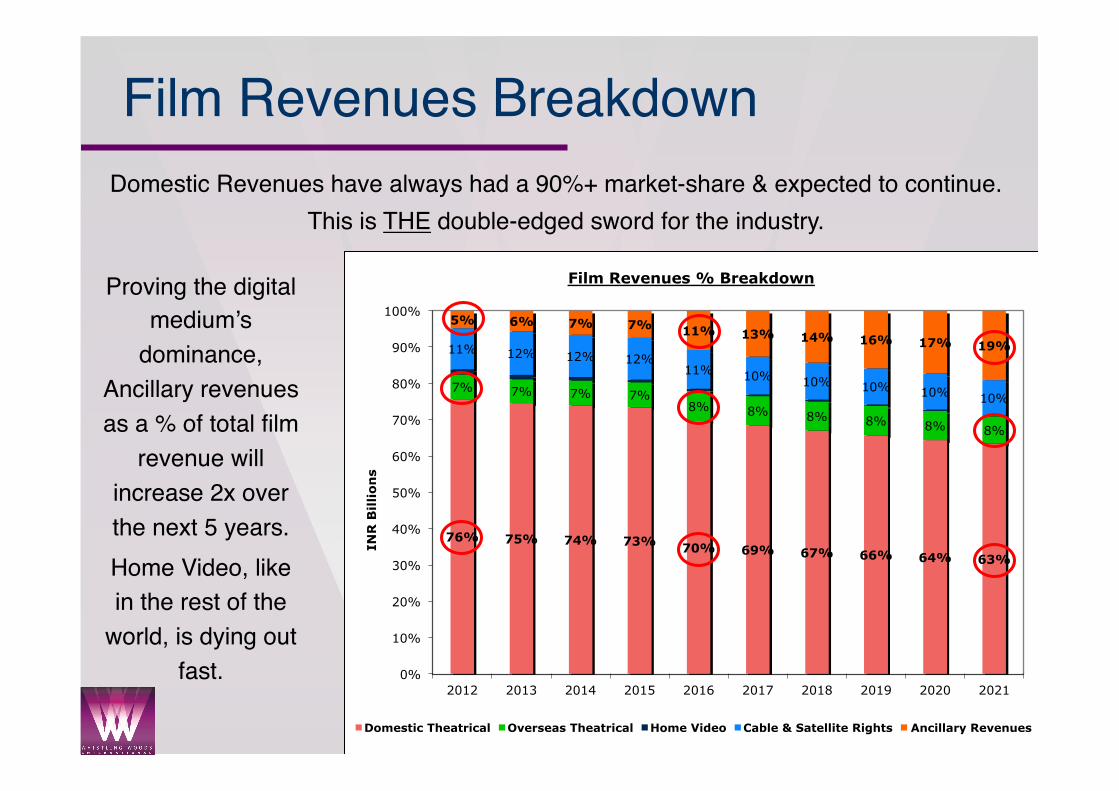

Film Revenues BreakdownDomestic Revenues have always had a 90%+ market-share & expected to continue.

This is THE double-edged sword for the industry.

Proving the digital medium’s

dominance, Ancillary revenues as a % of total film

revenue will increase 2x over the next 5 years.Home Video, like in the rest of the

world, is dying out fast.

76% 75% 74% 73% 70% 69% 67% 66% 64% 63%

7% 7% 7% 7% 8% 8% 8% 8% 8% 8%

11% 12% 12% 12% 11% 10% 10% 10% 10% 10%

5% 6% 7% 7% 11% 13% 14% 16% 17% 19%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

INR

Billio

ns

Film Revenues % Breakdown

Domestic Theatrical Overseas Theatrical Home Video Cable & Satellite Rights Ancillary Revenues

Source: FICCI-KPMG Report 2017

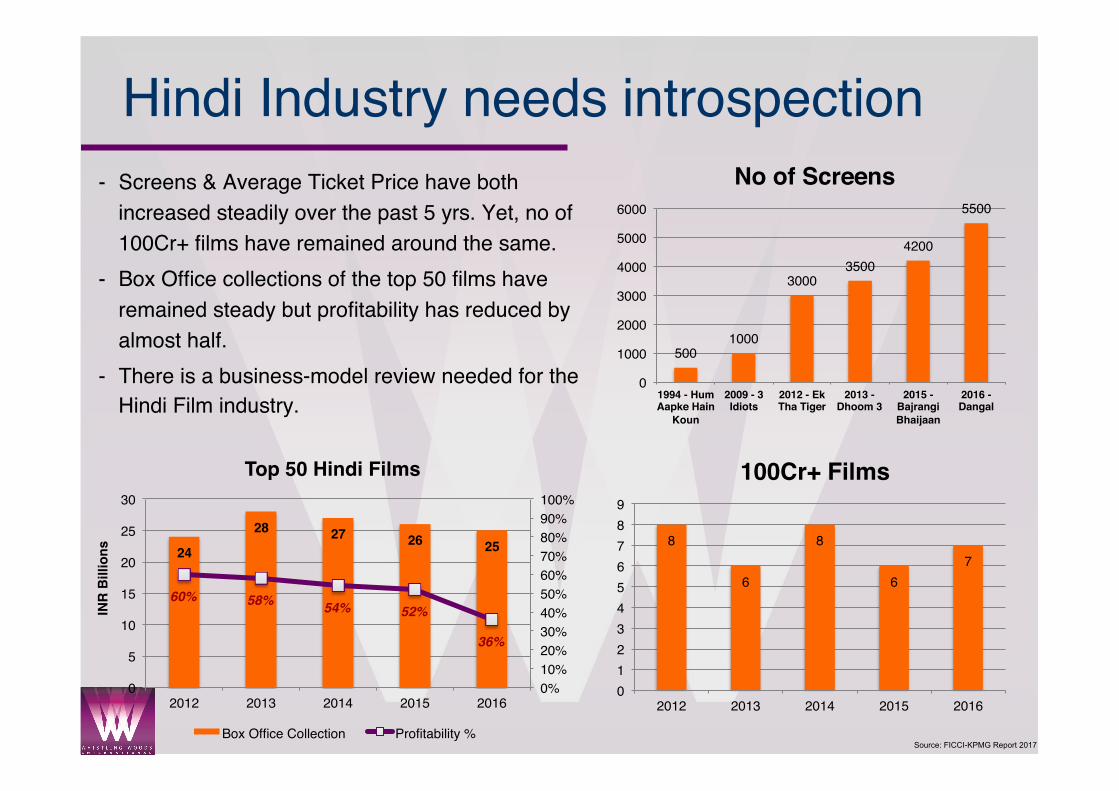

Hindi Industry needs introspection- Screens & Average Ticket Price have both

increased steadily over the past 5 yrs. Yet, no of 100Cr+ films have remained around the same.

- Box Office collections of the top 50 films have remained steady but profitability has reduced by almost half.

- There is a business-model review needed for the Hindi Film industry.

5001000

30003500

4200

5500

0

1000

2000

3000

4000

5000

6000

1994 - Hum Aapke Hain

Koun

2009 - 3 Idiots

2012 - Ek Tha Tiger

2013 - Dhoom 3

2015 - Bajrangi Bhaijaan

2016 - Dangal

No of Screens

8

6

8

67

0123456789

2012 2013 2014 2015 2016

100Cr+ Films

24

28 27 26 25

60% 58% 54% 52%

36%

0%10%20%30%40%50%60%70%80%90%100%

0

5

10

15

20

25

30

2012 2013 2014 2015 2016

INR

Bill

ions

Top 50 Hindi Films

Box Office Collection Profitability %

Source: FICCI-KPMG Report 2017

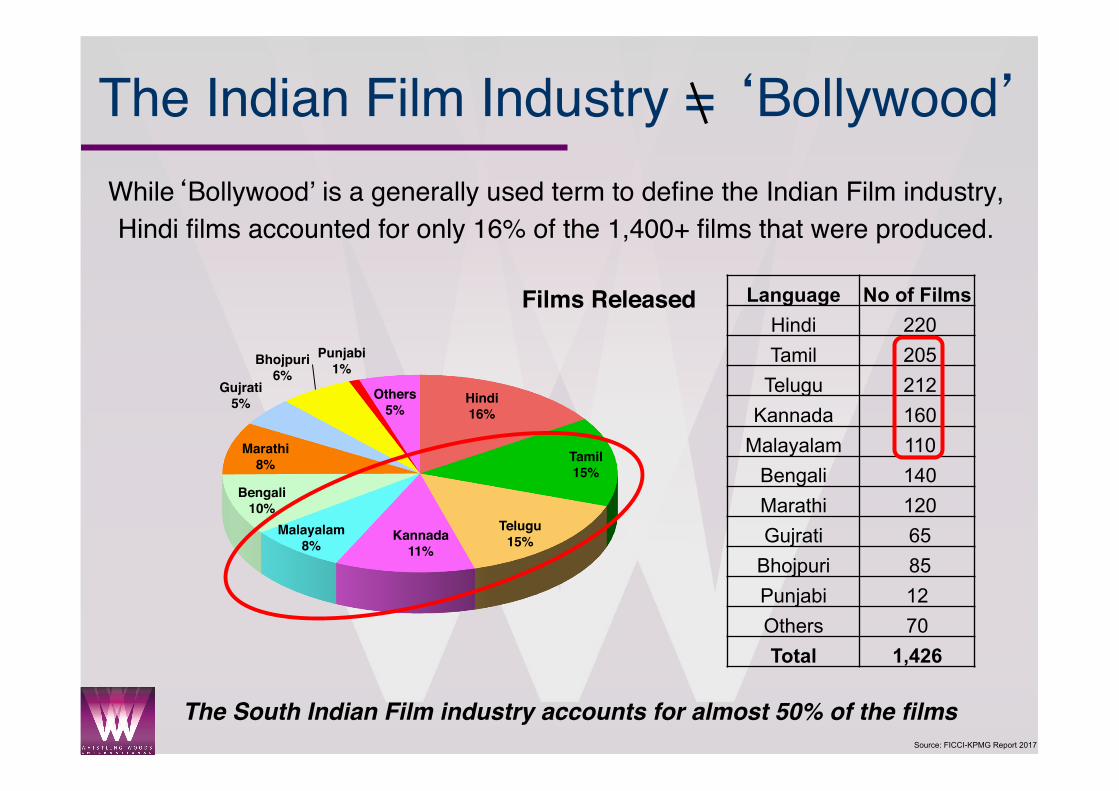

The Indian Film Industry = ‘Bollywood’While‘Bollywood’ is a generally used term to define the Indian Film industry, Hindi films accounted for only 16% of the 1,400+ films that were produced.

The South Indian Film industry accounts for almost 50% of the films

Language No of Films Hindi 220 Tamil 205

Telugu 212 Kannada 160

Malayalam 110 Bengali 140 Marathi 120 Gujrati 65

Bhojpuri 85 Punjabi 12 Others 70 Total 1,426

Hindi16%

Tamil15%

Telugu15%Kannada

11%Malayalam

8%

Bengali10%

Marathi8%

Gujrati5%

Bhojpuri6%

Punjabi1%

Others5%

Films Released

Source: FICCI-KPMG Report 2017

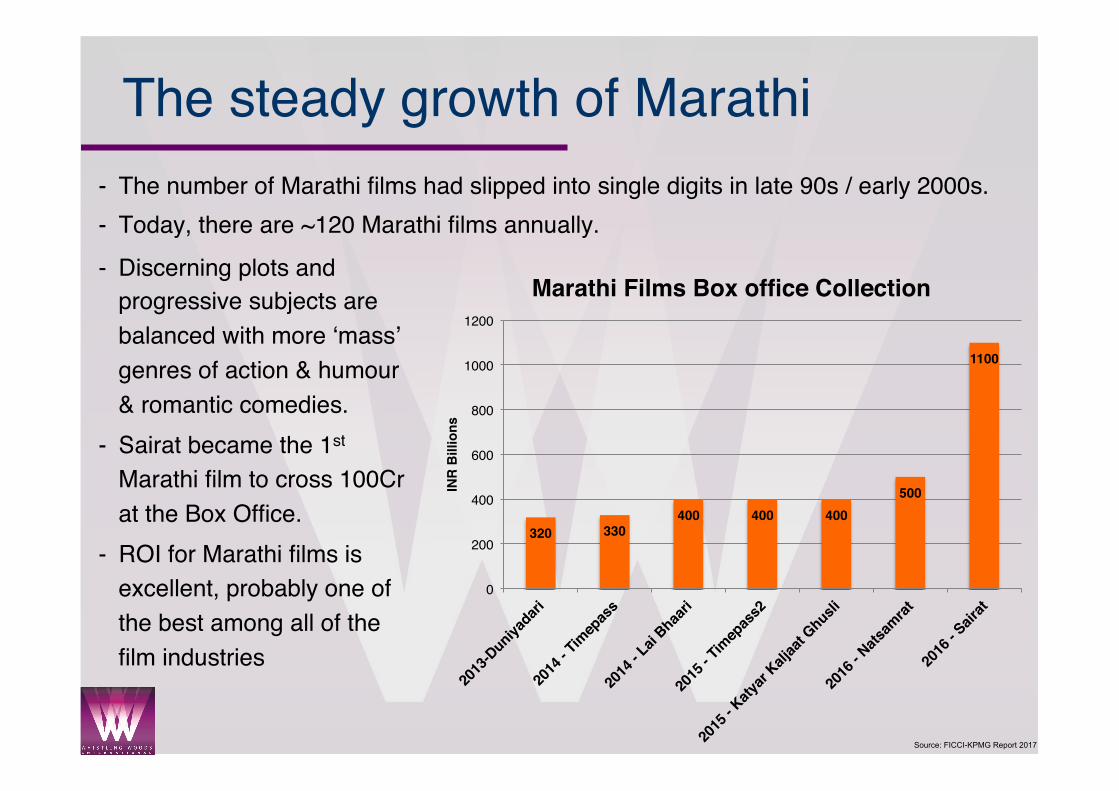

The steady growth of Marathi- The number of Marathi films had slipped into single digits in late 90s / early 2000s.- Today, there are ~120 Marathi films annually.

320 330400 400 400

500

1100

0

200

400

600

800

1000

1200

INR

Bill

ions

Marathi Films Box office Collection- Discerning plots and

progressive subjects are balanced with more ‘mass’ genres of action & humour & romantic comedies.

- Sairat became the 1st Marathi film to cross 100Cr at the Box Office.

- ROI for Marathi films is excellent, probably one of the best among all of the film industries

Source: FICCI-KPMG Report 2017

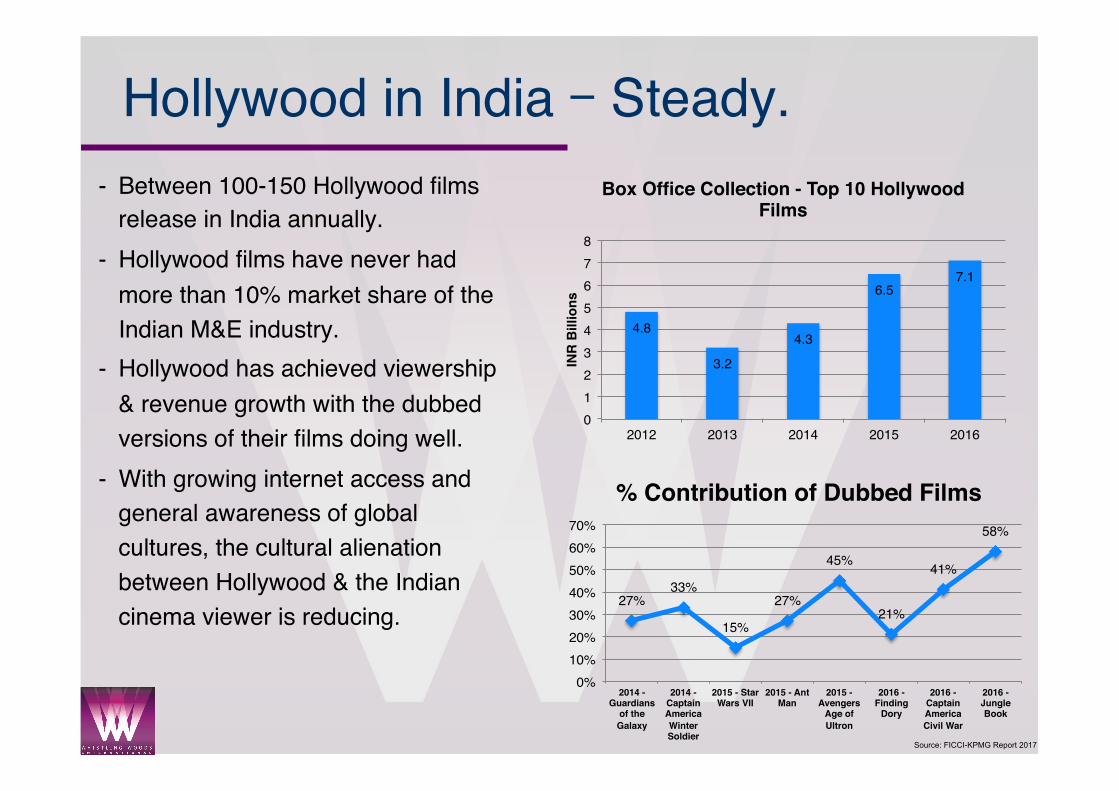

Hollywood in India – Steady.- Between 100-150 Hollywood films

release in India annually.- Hollywood films have never had

more than 10% market share of the Indian M&E industry.

- Hollywood has achieved viewership & revenue growth with the dubbed versions of their films doing well.

- With growing internet access and general awareness of global cultures, the cultural alienation between Hollywood & the Indian cinema viewer is reducing.

4.8

3.2

4.3

6.57.1

012345678

2012 2013 2014 2015 2016

INR

Bill

ions

Box Office Collection - Top 10 Hollywood Films

27%33%

15%

27%

45%

21%

41%

58%

0%10%20%30%40%50%60%70%

2014 - Guardians

of the Galaxy

2014 - Captain America Winter Soldier

2015 - Star Wars VII

2015 - Ant Man

2015 - Avengers

Age of Ultron

2016 - Finding

Dory

2016 - Captain America Civil War

2016 - Jungle Book

% Contribution of Dubbed Films

Source: FICCI-KPMG Report 2017

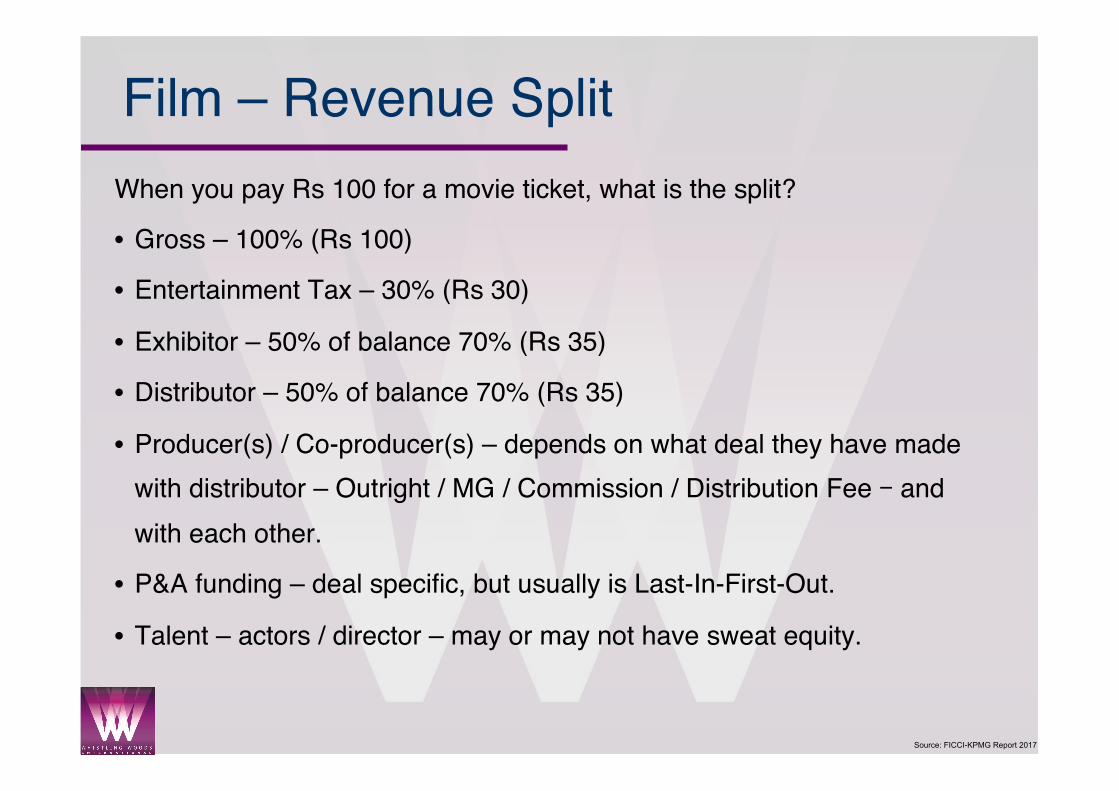

Film – Revenue SplitWhen you pay Rs 100 for a movie ticket, what is the split?

• Gross – 100% (Rs 100)

• Entertainment Tax – 30% (Rs 30)

• Exhibitor – 50% of balance 70% (Rs 35)

• Distributor – 50% of balance 70% (Rs 35)

• Producer(s) / Co-producer(s) – depends on what deal they have made with distributor – Outright / MG / Commission / Distribution Fee – and with each other.

• P&A funding – deal specific, but usually is Last-In-First-Out.

• Talent – actors / director – may or may not have sweat equity.

Source: FICCI-KPMG Report 2017

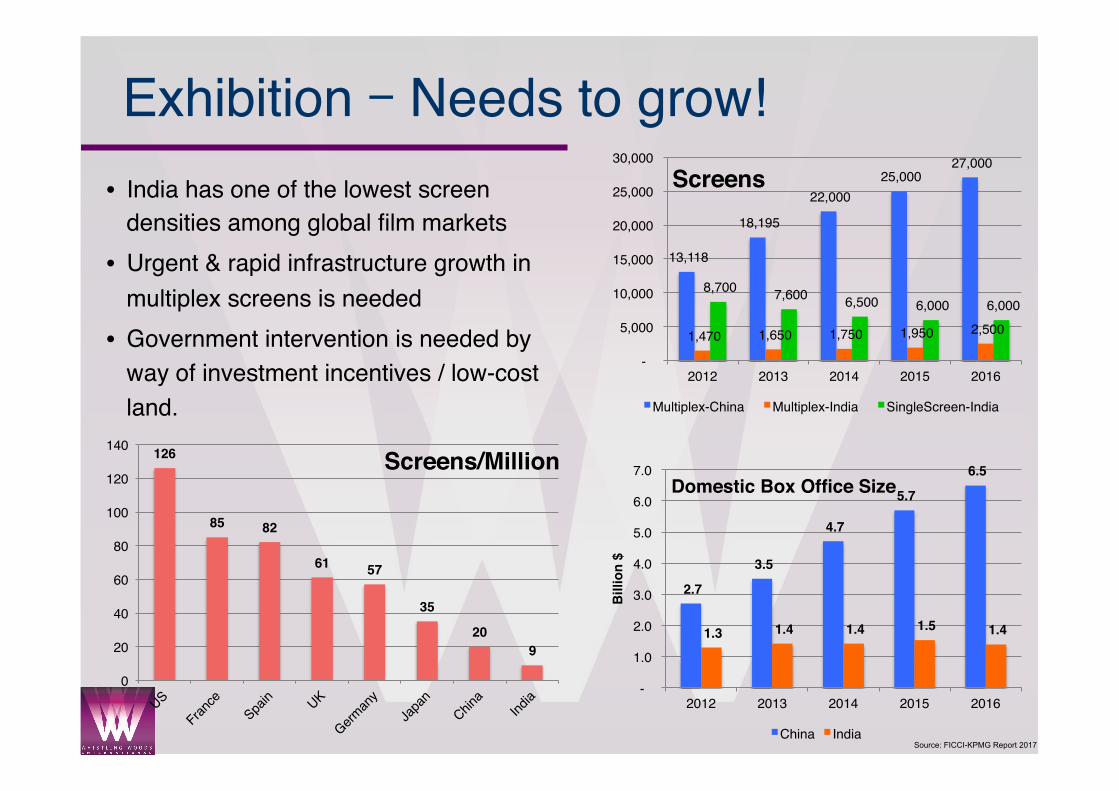

Exhibition – Needs to grow!• India has one of the lowest screen

densities among global film markets• Urgent & rapid infrastructure growth in

multiplex screens is needed• Government intervention is needed by

way of investment incentives / low-cost land.

126

85 82

61 57

35

209

0

20

40

60

80

100

120

140Screens/Million

2.7

3.5

4.7

5.7

6.5

1.3 1.4 1.4 1.5 1.4

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2012 2013 2014 2015 2016

Bill

ion

$

Domestic Box Office Size

China India

13,118

18,195

22,000 25,000

27,000

1,470 1,650 1,750 1,950 2,500

8,700 7,600 6,500 6,000 6,000

-

5,000

10,000

15,000

20,000

25,000

30,000

2012 2013 2014 2015 2016

Screens

Multiplex-China Multiplex-India SingleScreen-India

Source: FICCI-KPMG Report 2017

The Indian Film Industry - Key points• Urgent and significant scale needed in Film education.• Screens need to grow to double in 5 yrs; Government incentive

schemes will be needed.• Globally-merchandisable, home-grown IP brand(s) needed.• Hindi industry needs to review its business model. If costs are going to

continue to rise, the films need to start doing better in overseas high-value markets. Alternatively, be more cost efficient and viewer-relevant.• Regional shows its importance – Marathi, Gujarati, Punjabi• Hollywood films box office growing (on the back of dubbed films),

though not as much as to threaten domestic content. • Funding avenues, beyond the studios, grow with banks (IDBI, Exim,

Kotak, YES), Film Funds, Crowd-funding all becoming serious options.

Source: FICCI-KPMG Report 2017

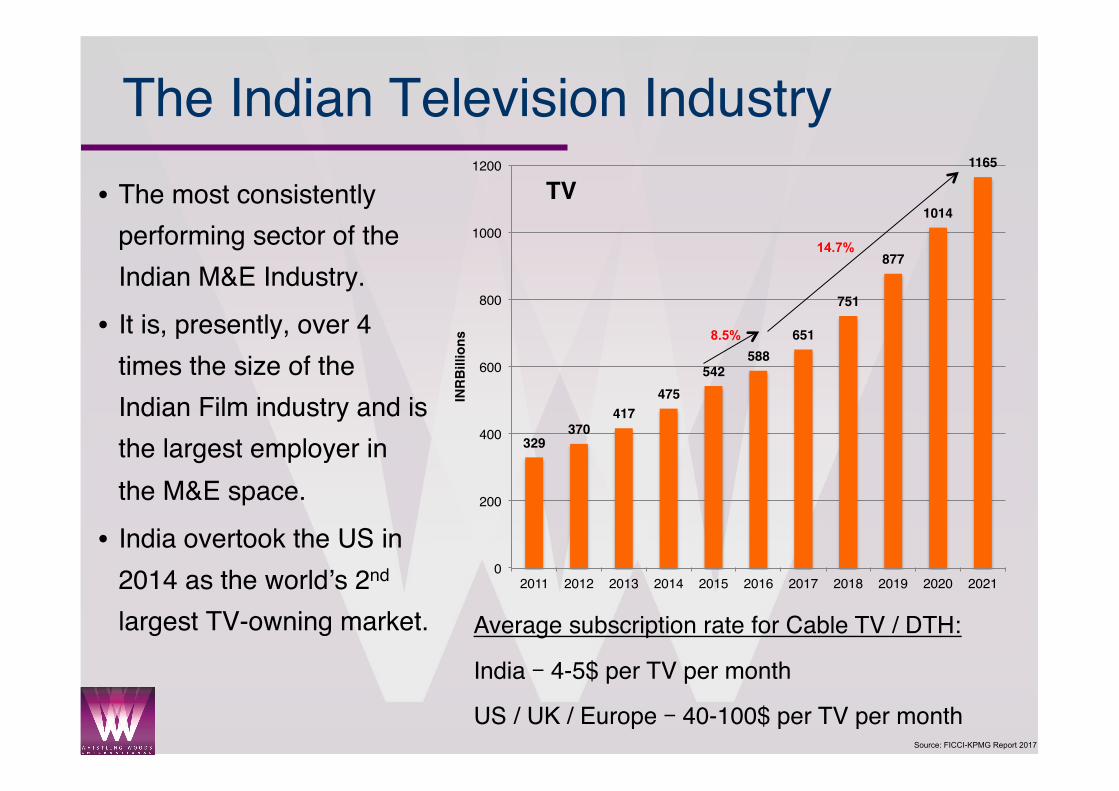

The Indian Television Industry• The most consistently

performing sector of the Indian M&E Industry.

• It is, presently, over 4 times the size of the Indian Film industry and is the largest employer in the M&E space.

• India overtook the US in 2014 as the world’s 2nd largest TV-owning market. Average subscription rate for Cable TV / DTH:

India – 4-5$ per TV per month

US / UK / Europe – 40-100$ per TV per month

329370

417475

542588

651

751

877

1014

1165

0

200

400

600

800

1000

1200

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

INR

Bill

ions

TV

8.5%

14.7%

Source: FICCI-KPMG Report 2017

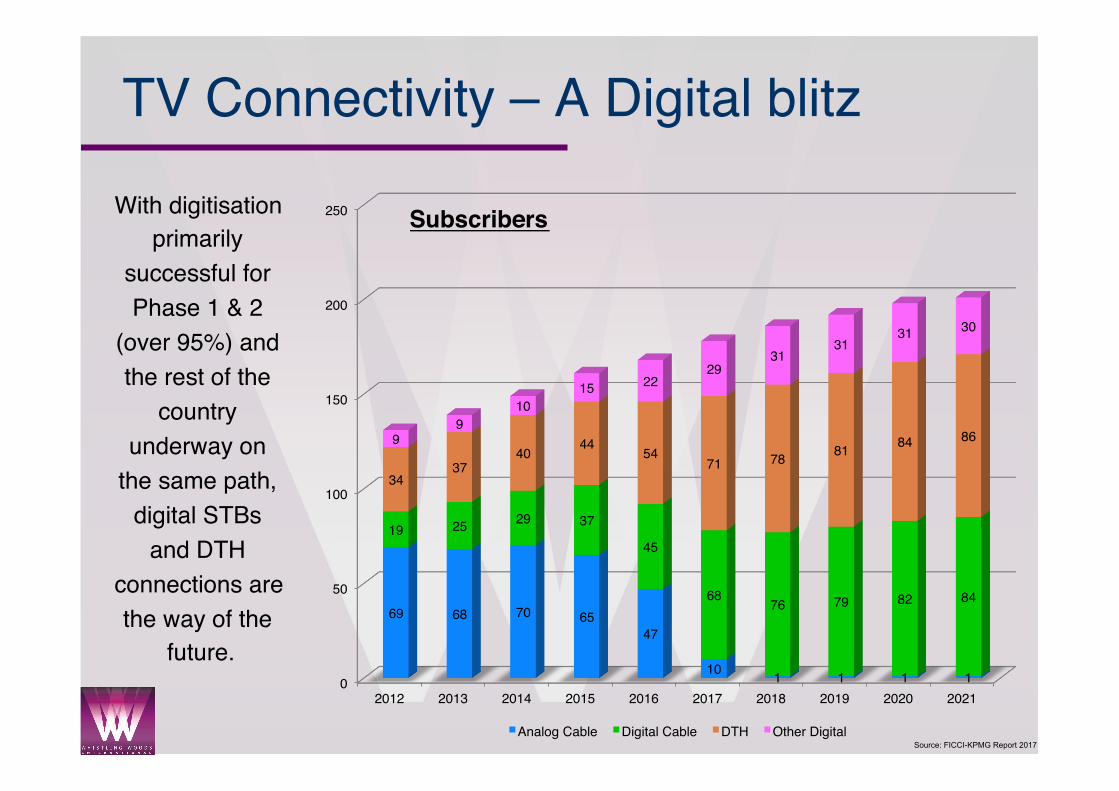

TV Connectivity – A Digital blitz

With digitisation primarily

successful for Phase 1 & 2

(over 95%) and the rest of the

country underway on

the same path, digital STBs

and DTH connections are the way of the

future.0

50

100

150

200

250

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

69 68 70 6547

10 1 1 1 1

19 25 29 37

45

68 76 79 82 84

3437

40 44 5471 78 81 84 869

910

15 2229

3131

31 30

Subscribers

Analog Cable Digital Cable DTH Other Digital

Source: FICCI-KPMG Report 2017

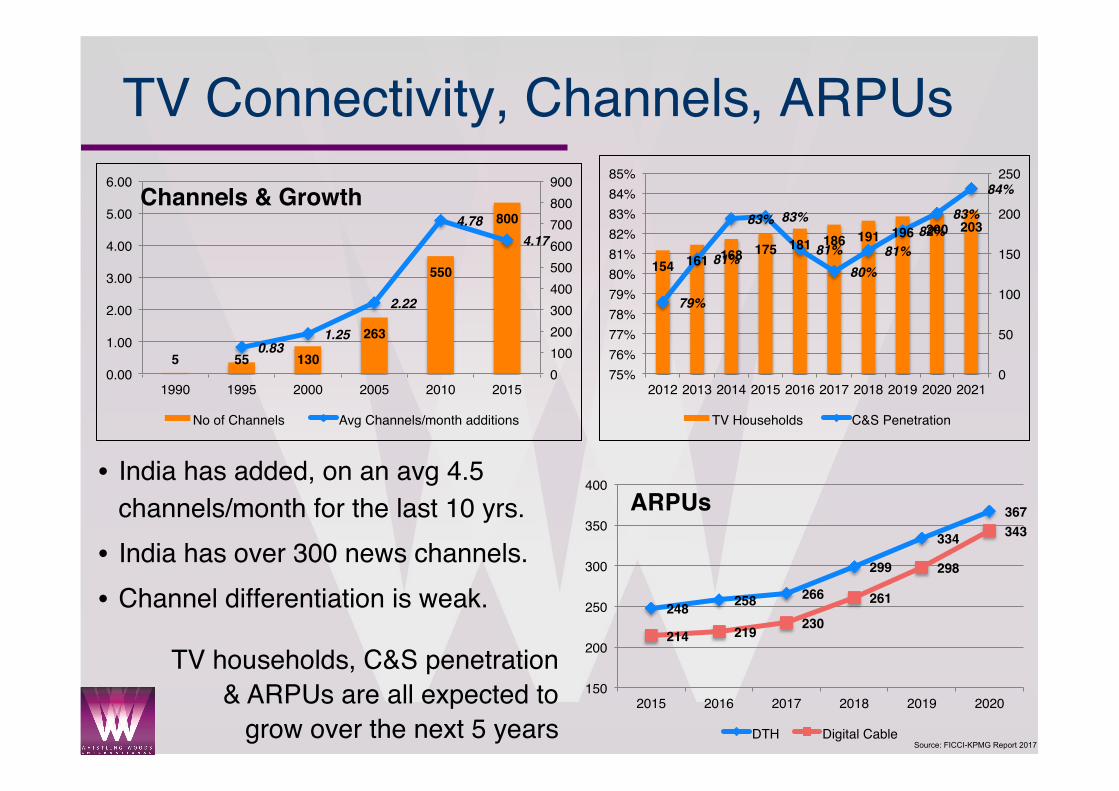

TV Connectivity, Channels, ARPUs

• India has added, on an avg 4.5 channels/month for the last 10 yrs.

• India has over 300 news channels.• Channel differentiation is weak.

TV households, C&S penetration & ARPUs are all expected to

grow over the next 5 years

5 55 130

263

550

800

0.831.25

2.22

4.784.17

0100200300400500600700800900

0.00

1.00

2.00

3.00

4.00

5.00

6.00

1990 1995 2000 2005 2010 2015

Channels & Growth

No of Channels Avg Channels/month additions

154 161 168 175 181 186 191 196 200 203

79%

81%

83% 83%

81%80%

81%82%

83%

84%

0

50

100

150

200

250

75%76%77%78%79%80%81%82%83%84%85%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

TV Households C&S Penetration

248 258 266

299

334

367

214 219 230

261

298

343

150

200

250

300

350

400

2015 2016 2017 2018 2019 2020

ARPUs

DTH Digital Cable

Source: FICCI-KPMG Report 2017

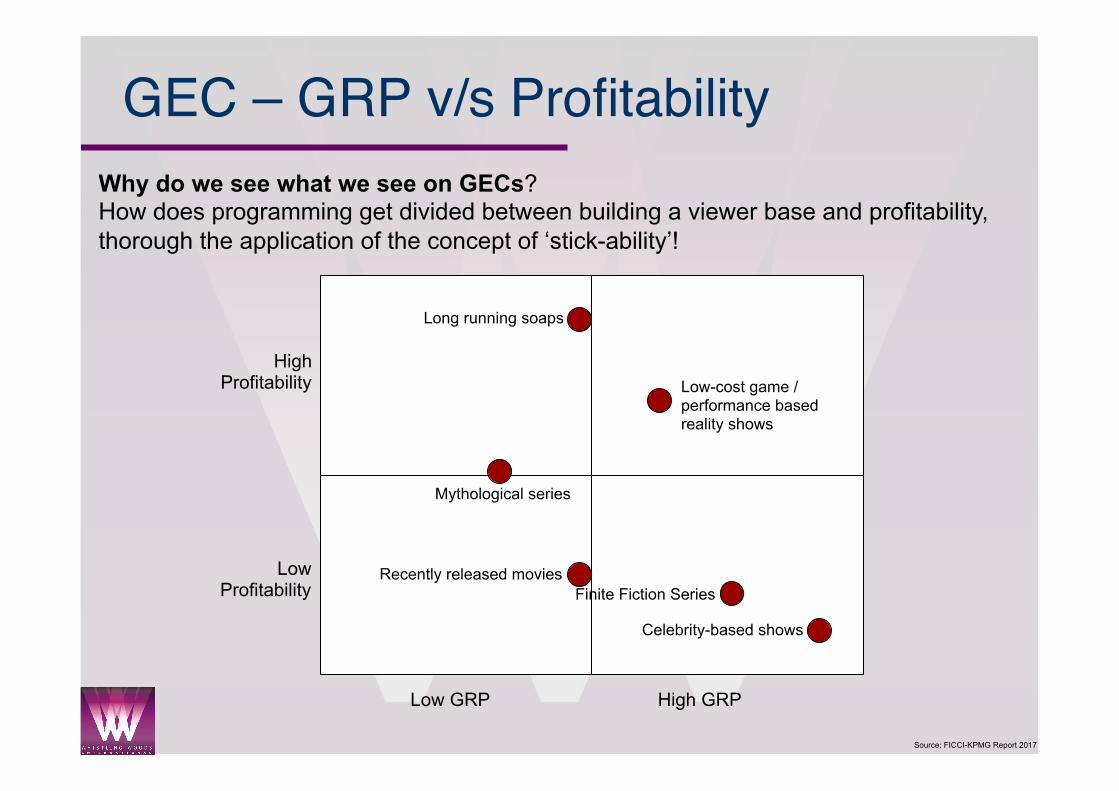

GEC – GRP v/s Profitability

Low GRP High GRP

Low Profitability

High Profitability

Long running soaps

Low-cost game / performance based reality shows

Mythological series

Recently released movies

Celebrity-based shows

Why do we see what we see on GECs? How does programming get divided between building a viewer base and profitability, thorough the application of the concept of ‘stick-ability’!

Finite Fiction Series

Source: FICCI-KPMG Report 2017

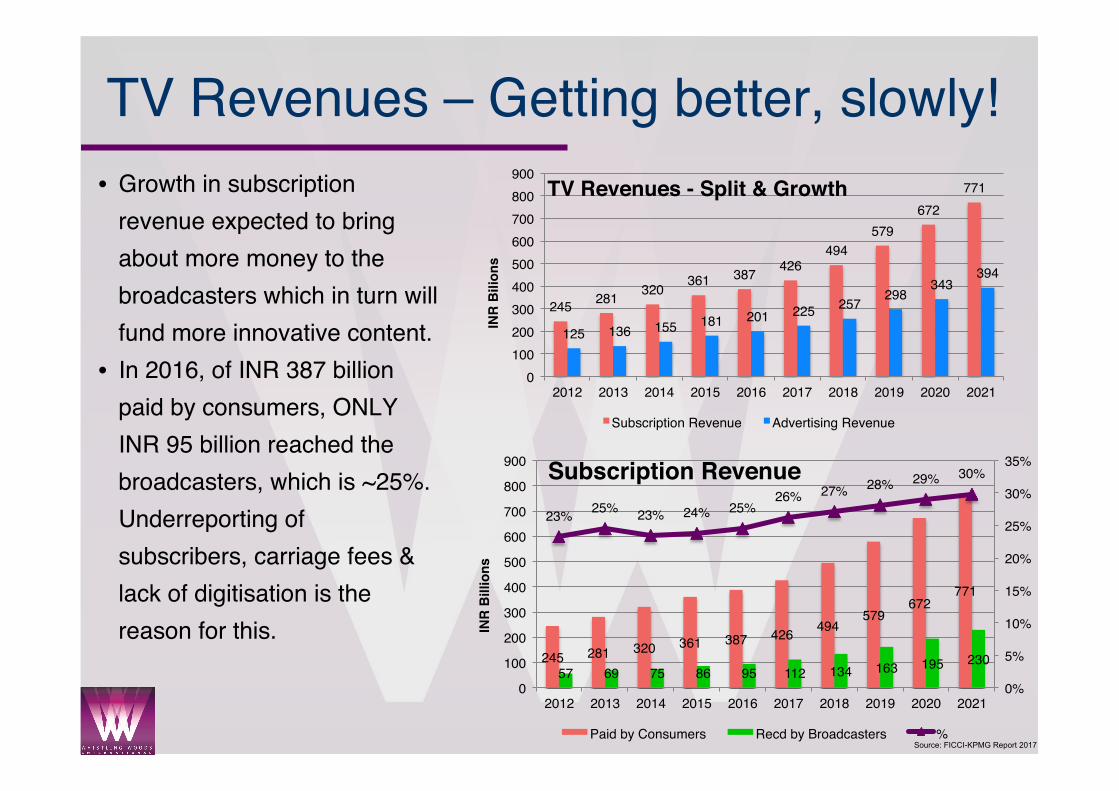

TV Revenues – Getting better, slowly!• Growth in subscription

revenue expected to bring about more money to the broadcasters which in turn will fund more innovative content.

• In 2016, of INR 387 billion paid by consumers, ONLY INR 95 billion reached the broadcasters, which is ~25%. Underreporting of subscribers, carriage fees & lack of digitisation is the reason for this.

245 281 320 361 387 426494

579672

771

125 136 155 181 201 225 257 298343

394

0100200300400500600700800900

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

INR

Bili

ons

TV Revenues - Split & Growth

Subscription Revenue Advertising Revenue

245 281 320 361 387 426 494579

672771

57 69 75 86 95 112 134 163 195 230

23% 25% 23% 24% 25%26% 27% 28% 29% 30%

0%

5%

10%

15%

20%

25%

30%

35%

0

100

200

300

400

500

600

700

800

900

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

INR

Bill

ions

Subscription Revenue

Paid by Consumers Recd by Broadcasters %

Source: FICCI-KPMG Report 2017

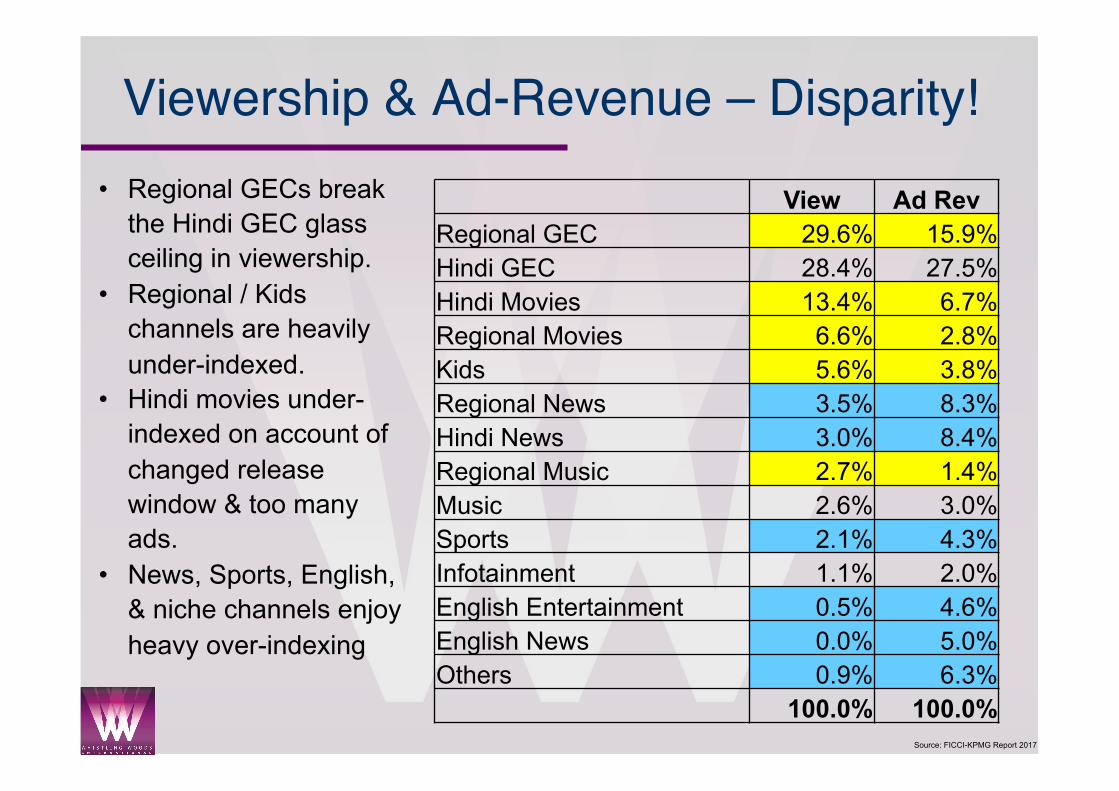

Viewership & Ad-Revenue – Disparity!

View Ad Rev Regional GEC 29.6% 15.9% Hindi GEC 28.4% 27.5% Hindi Movies 13.4% 6.7% Regional Movies 6.6% 2.8% Kids 5.6% 3.8% Regional News 3.5% 8.3% Hindi News 3.0% 8.4% Regional Music 2.7% 1.4% Music 2.6% 3.0% Sports 2.1% 4.3% Infotainment 1.1% 2.0% English Entertainment 0.5% 4.6% English News 0.0% 5.0% Others 0.9% 6.3%

100.0% 100.0%

• Regional GECs break the Hindi GEC glass ceiling in viewership.

• Regional / Kids channels are heavily under-indexed.

• Hindi movies under-indexed on account of changed release window & too many ads.

• News, Sports, English, & niche channels enjoy heavy over-indexing

Source: FICCI-KPMG Report 2017

Indian Animation picks up• Broadcasters are willing to pay over

double for good quality Indian Animated content as compared to daily soaps / Hindi general entertainment content, even though this segment gets only 5.6% of the viewership, as compared to 28.4% for Hindi GECs.

• Also the fact that this segment continues to be under-indexed, with only 3.8% ad-revenue share doesn’t bother broadcasters as this content has long-tail revenue

• It offers repeat viewing value, multi-language dubbing value and merchandising value.

Source: FICCI-KPMG Report 2017

Hindi GEC Fiction content changing. Slowly.

• GECs have finally embraced the tele-series format with season-based programming

• The value:volume ratio is reversed in such programming as compared to the daily / weekly soaps.

• For the past 20-odd years, the content has largely mirrored American programming of the 70s-80s, with our soaps comparable to content like the Bold & The Beautiful, Santa Barbara, Dallas, etc.

Source: FICCI-KPMG Report 2017

TV – Key Points• Digitisation – increased revenue for the broadcaster, should lead to

more investment in content (& hence better quality content)• Global proliferation of Indian-origin content is increasing, albeit for

the Indian diaspora only. This is THE BIG opportunity.• Indian animation on TV is starting to matter.

• Hindi GECs are exploring new content programming & a changed value:volume mix in revenue models.

• Lack of quality viewership measurement systems (CPRP v/s CPT) is an issue. Hopefully, BARC should resolve this.

• Targeted advertising is the next step

Source: FICCI-KPMG Report 2017

Digital – Growth galore!

1522

30

44

60

77

102

134

174

226

294

0

50

100

150

200

250

300

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

INR

Bill

ions

Digital is expected to quadruple its size in the next 5 yrs

Source: FICCI-KPMG Report 2017

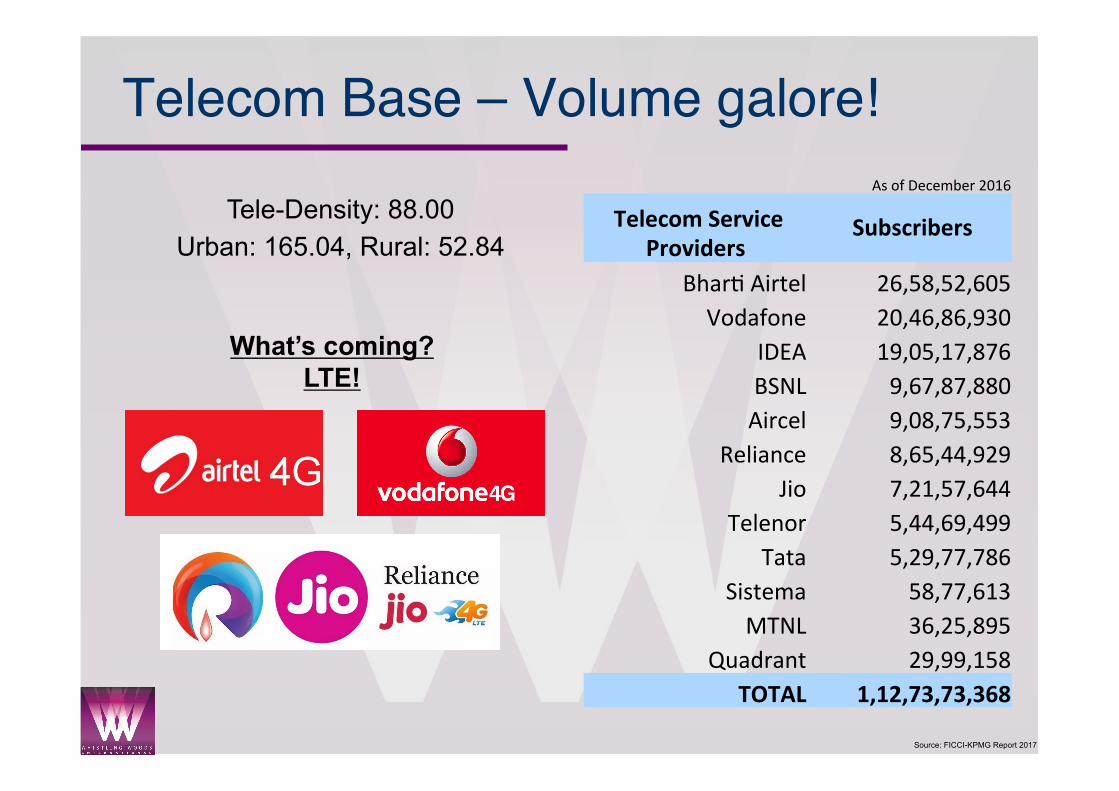

Telecom Base – Volume galore!

Tele-Density: 88.00 Urban: 165.04, Rural: 52.84

What’s coming? LTE!

AsofDecember2016

TelecomServiceProviders

Subscribers

Bhar3Airtel 26,58,52,605Vodafone 20,46,86,930

IDEA 19,05,17,876BSNL 9,67,87,880Aircel 9,08,75,553

Reliance 8,65,44,929Jio 7,21,57,644

Telenor 5,44,69,499Tata 5,29,77,786

Sistema 58,77,613MTNL 36,25,895

Quadrant 29,99,158TOTAL 1,12,73,73,368

Source: FICCI-KPMG Report 2017

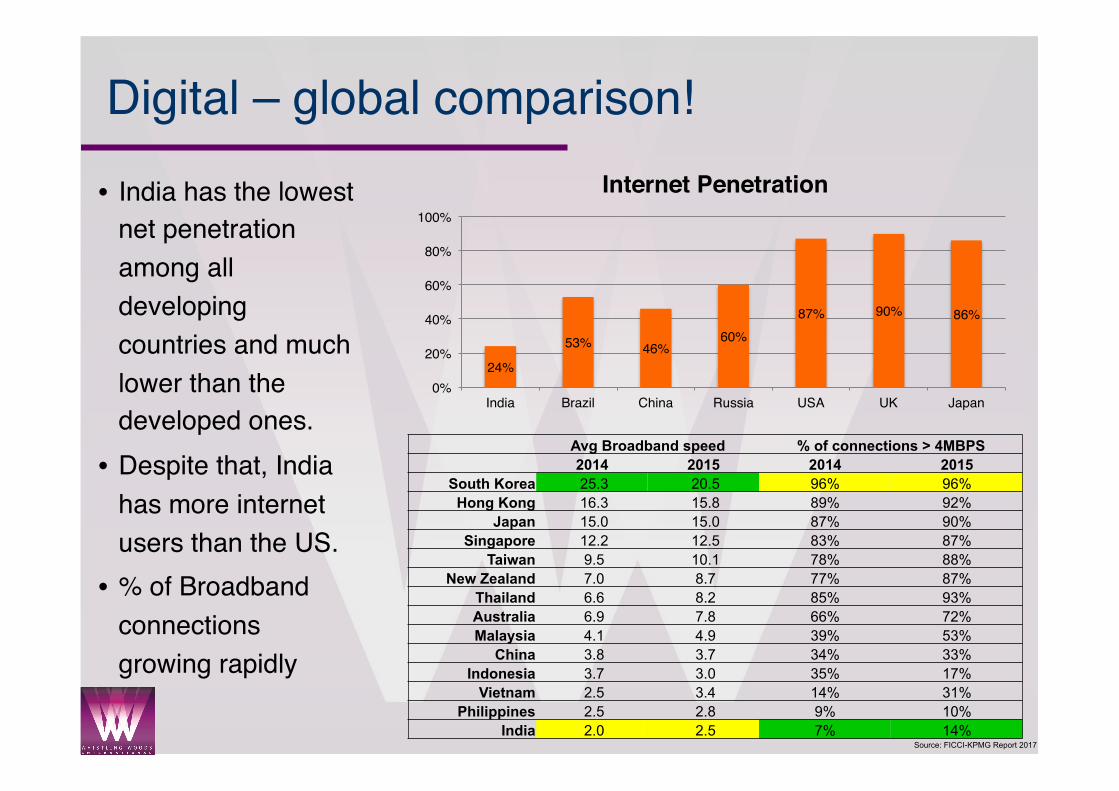

Digital – global comparison!

• India has the lowest net penetration among all developing countries and much lower than the developed ones.

• Despite that, India has more internet users than the US.

• % of Broadband connections growing rapidly

Avg Broadband speed % of connections > 4MBPS 2014 2015 2014 2015

South Korea 25.3 20.5 96% 96% Hong Kong 16.3 15.8 89% 92%

Japan 15.0 15.0 87% 90% Singapore 12.2 12.5 83% 87%

Taiwan 9.5 10.1 78% 88% New Zealand 7.0 8.7 77% 87%

Thailand 6.6 8.2 85% 93% Australia 6.9 7.8 66% 72% Malaysia 4.1 4.9 39% 53%

China 3.8 3.7 34% 33% Indonesia 3.7 3.0 35% 17%

Vietnam 2.5 3.4 14% 31% Philippines 2.5 2.8 9% 10%

India 2.0 2.5 7% 14%

24%

53% 46%60%

87% 90% 86%

0%

20%

40%

60%

80%

100%

India Brazil China Russia USA UK Japan

Internet Penetration

Source: FICCI-KPMG Report 2017

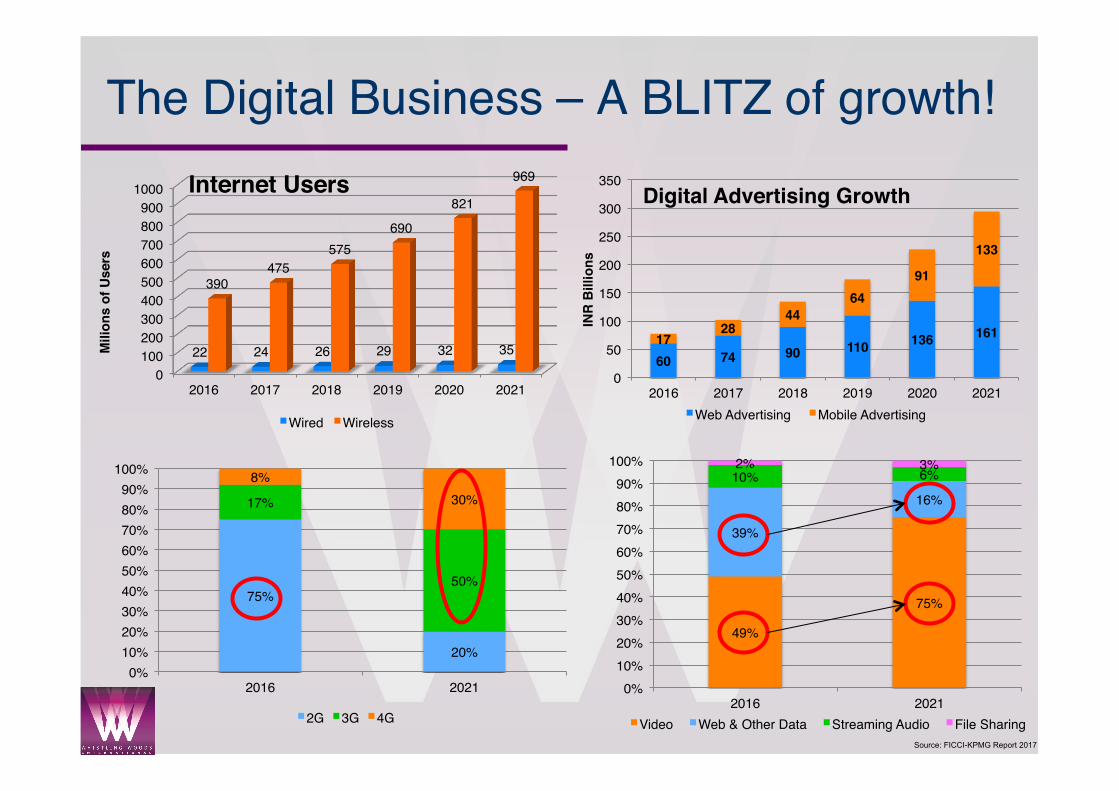

The Digital Business – A BLITZ of growth!

0100200300400500600700800900

1000

2016 2017 2018 2019 2020 2021

22 24 26 29 32 35

390475

575690

821

969

Mili

ons

of U

sers

Internet Users

Wired Wireless

60 74 90 110 136 1611728

4464

91

133

0

50

100

150

200

250

300

350

2016 2017 2018 2019 2020 2021

INR

Bill

ions

Digital Advertising Growth

Web Advertising Mobile Advertising

75%

20%

17%

50%

8%30%

0%10%20%30%40%50%60%70%80%90%

100%

2016 2021

2G 3G 4G

49%

75%

39%

16%10% 6%2% 3%

0%10%20%30%40%50%60%70%80%90%

100%

2016 2021Video Web & Other Data Streaming Audio File Sharing

Source: FICCI-KPMG Report 2017

Content - Global Digital Platforms

Source: FICCI-KPMG Report 2017

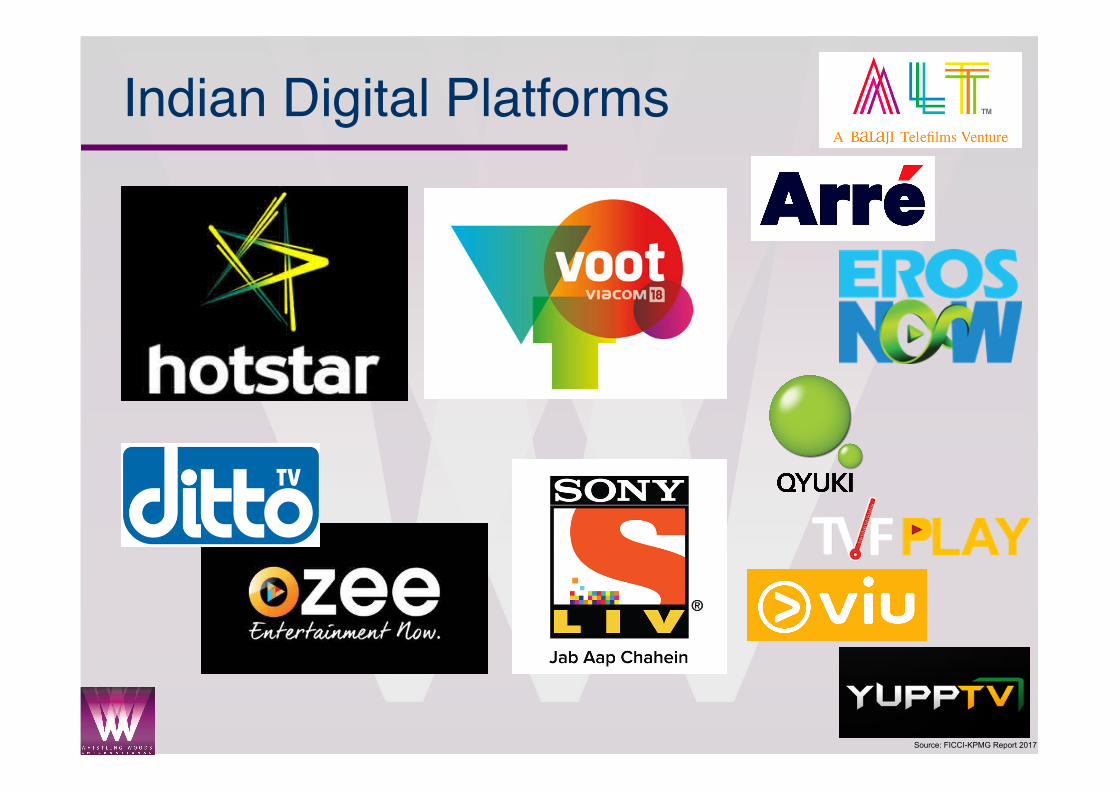

Indian Digital Platforms

Source: FICCI-KPMG Report 2017

Source: FICCI-KPMG Report 2017

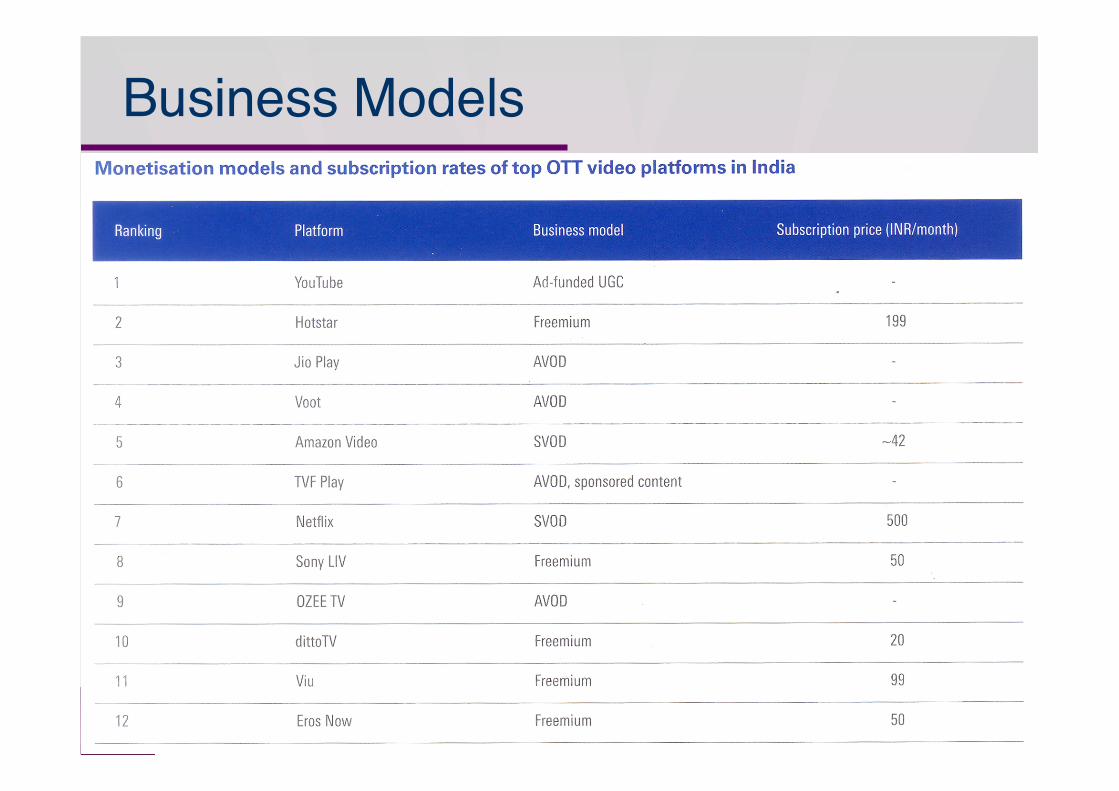

Business Models

Source: FICCI-KPMG Report 2017

YouTube• Clear Market leader:

o YouTube has over 1 billion users — 1/3rd of all net users see at least 1 YouTube video everyday.

o People watching a YouTube video online has grown 40% & watch-time has grown ~50%, annually for the past 2 years

o Creator revenue has increased 50% annually for the past three years.o All of the top 100 global brands run ads on YouTubeo YouTube has paid out over $1 billion for legitimate content claims

• YouTube has launched local versions in more than 88 countries & in 76 different languages (covering 95% of the Internet population).

• Over 50% of YouTube views come from mobile devices. On mobile, the average viewing session is now more 40 minutes.

Source: FICCI-KPMG Report 2017

Digital – No more a ‘also’ platform• The Digital platforms of web, mobile & web-connected smart TVs are the

present & the future.

• Content expected to follow a parallel trajectory to Cable & Satellite TV.

• Content consumption modes & patterns are changing with a large number of sub-18-yr-olds finding their ‘stars’ online.

• YouTube is taking the Indian market very seriously and has set up their 7th global ‘YouTube Space’ & also a ‘YouTube Educator Lab’ in India, in partnership with Whistling Woods.

• ANALYTICS & TARGETING – Audience analytics, Content-based analytics, Predictive analytics, Campaign analytics

Source: FICCI-KPMG Report 2017

The Opportunities in Digital• IP Creation• Digital is a writers’ medium – HOW?

• Look beyond digital as JUST a 3rd screen with limited censorship

• Multi-formatting ALL content to include Digital platforms (10% extra effort)

• Specialised writing / content structure for ‘Indian’ digital platforms

• Utilising the entire spectrum of the platform – clickable / interactive video, AR/VR (360 deg video, etc), gamification of content & more

In any industry, building volume is hard. India already has the volume and is likely to be the largest digital free market by 2020-22. We now need to build

value to each unit of volume. Only way to do it is quality.

Source: FICCI-KPMG Report 2017

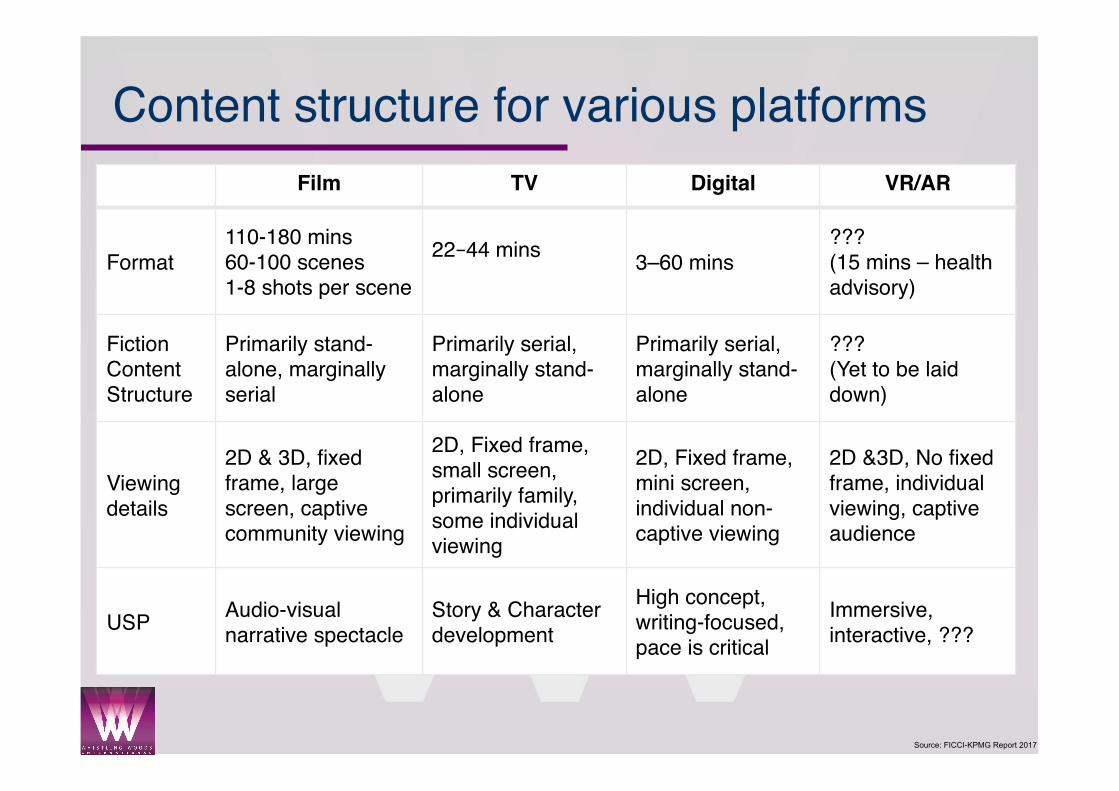

Content structure for various platformsFilm TV Digital VR/AR

Format110-180 mins60-100 scenes1-8 shots per scene

22–44 mins 3–60 mins???(15 mins – health advisory)

Fiction Content Structure

Primarily stand-alone, marginally serial

Primarily serial, marginally stand-alone

Primarily serial, marginally stand-alone

???(Yet to be laid down)

Viewing details

2D & 3D, fixed frame, large screen, captive community viewing

2D, Fixed frame, small screen, primarily family, some individual viewing

2D, Fixed frame, mini screen, individual non-captive viewing

2D &3D, No fixed frame, individual viewing, captive audience

USP Audio-visual narrative spectacle

Story & Character development

High concept, writing-focused, pace is critical

Immersive, interactive, ???

Source: FICCI-KPMG Report 2017

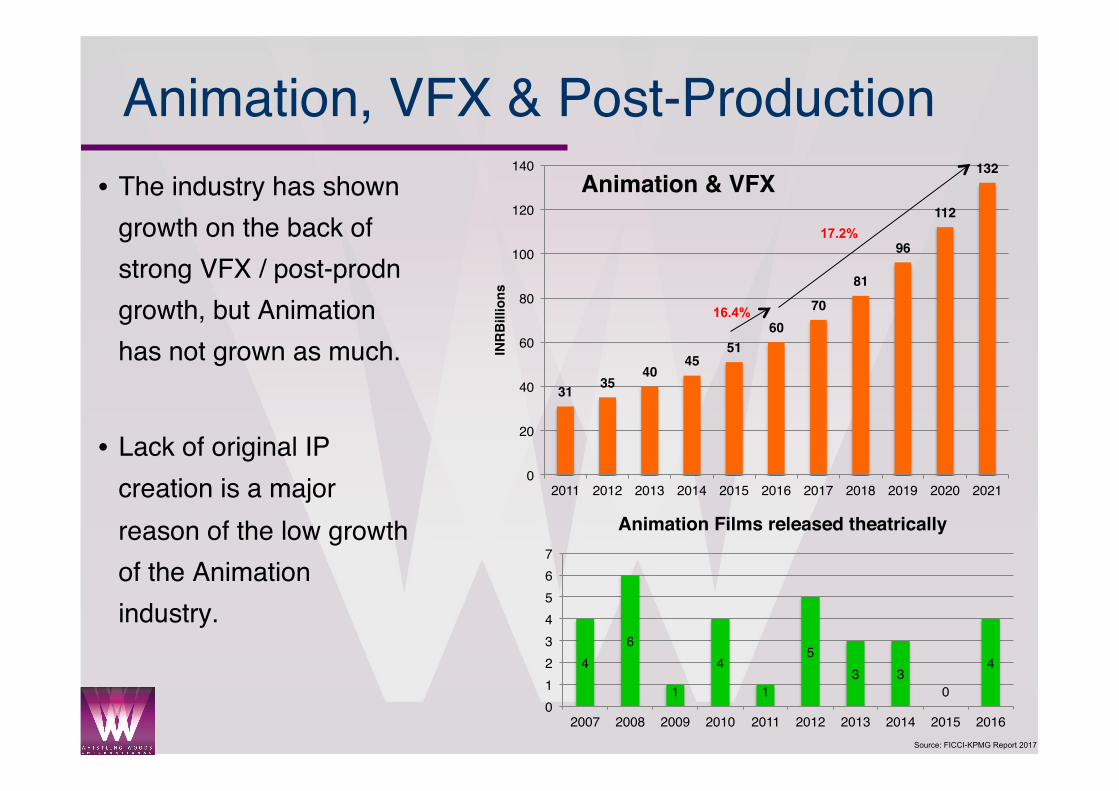

31 3540

4551

6070

81

96

112

132

0

20

40

60

80

100

120

140

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021IN

RB

illio

ns

Animation & VFX

Animation, VFX & Post-Production• The industry has shown

growth on the back of strong VFX / post-prodn growth, but Animation has not grown as much.

• Lack of original IP creation is a major reason of the low growth of the Animation industry.

17.2%

16.4%

46

1

4

1

53 3

0

4

01234567

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Animation Films released theatrically

Source: FICCI-KPMG Report 2017

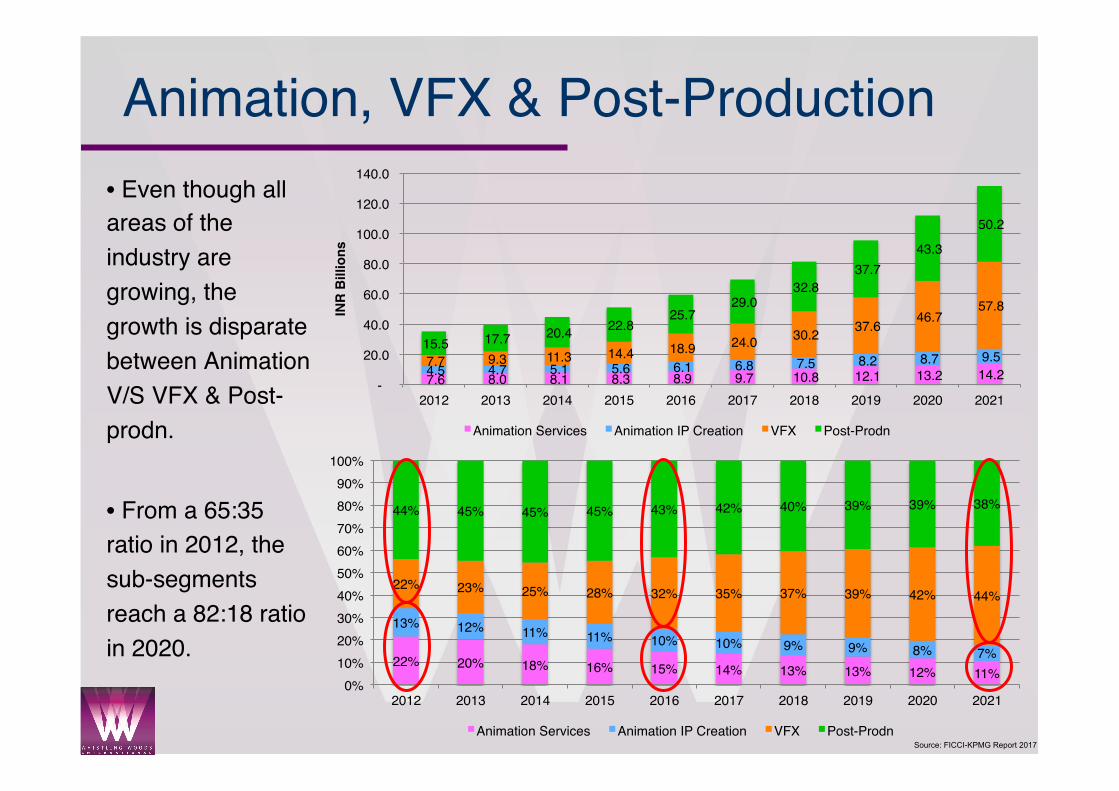

22% 20% 18% 16% 15% 14% 13% 13% 12% 11%

13% 12% 11% 11% 10% 10% 9% 9% 8% 7%

22% 23% 25% 28% 32% 35% 37% 39% 42% 44%

44% 45% 45% 45% 43% 42% 40% 39% 39% 38%

0%10%20%30%40%50%60%70%80%90%

100%

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Animation Services Animation IP Creation VFX Post-Prodn

7.6 8.0 8.1 8.3 8.9 9.7 10.8 12.1 13.2 14.2 4.5 4.7 5.1 5.6 6.1 6.8 7.5 8.2 8.7 9.5 7.7 9.3 11.3 14.4 18.9 24.0 30.2 37.6 46.7 57.8

15.5 17.7 20.4 22.8 25.7

29.0 32.8

37.7 43.3

50.2

-

20.0

40.0

60.0

80.0

100.0

120.0

140.0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

INR

Bill

ions

Animation Services Animation IP Creation VFX Post-Prodn

Animation, VFX & Post-Production• Even though all areas of the industry are growing, the growth is disparate between Animation V/S VFX & Post-prodn.

• From a 65:35 ratio in 2012, the sub-segments reach a 82:18 ratio in 2020.

Source: FICCI-KPMG Report 2017

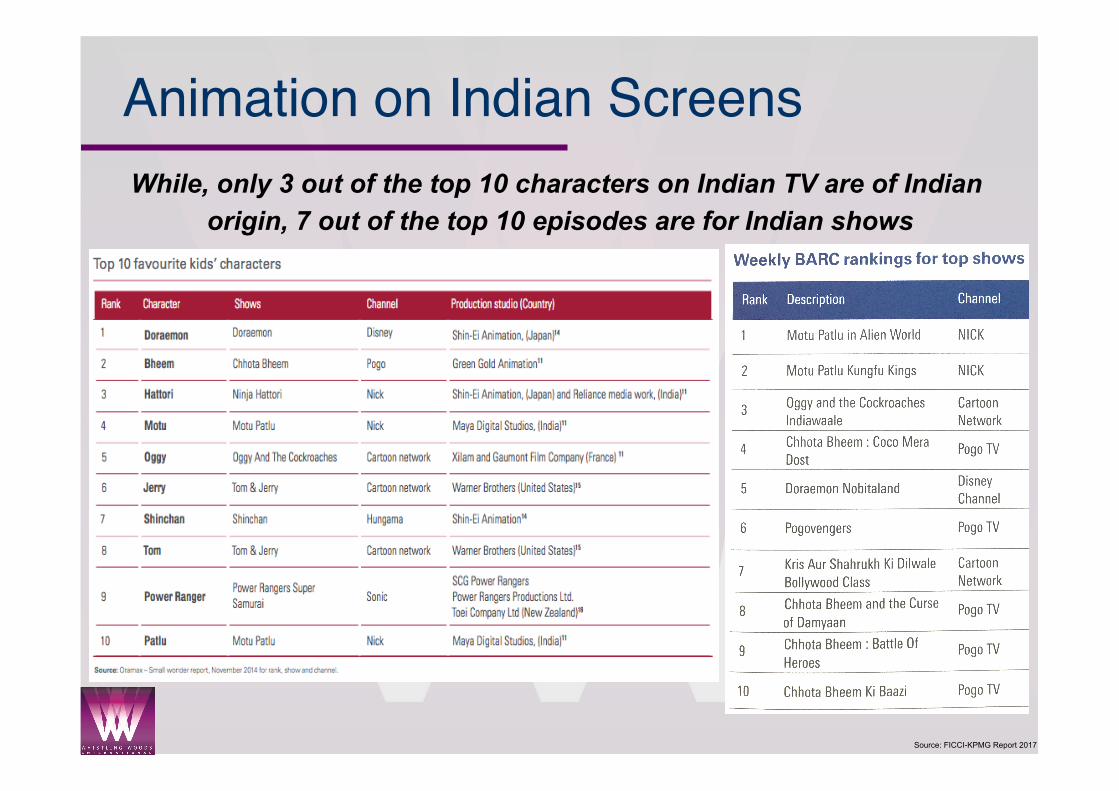

Animation on Indian ScreensWhile, only 3 out of the top 10 characters on Indian TV are of Indian

origin, 7 out of the top 10 episodes are for Indian shows

Source: FICCI-KPMG Report 2017

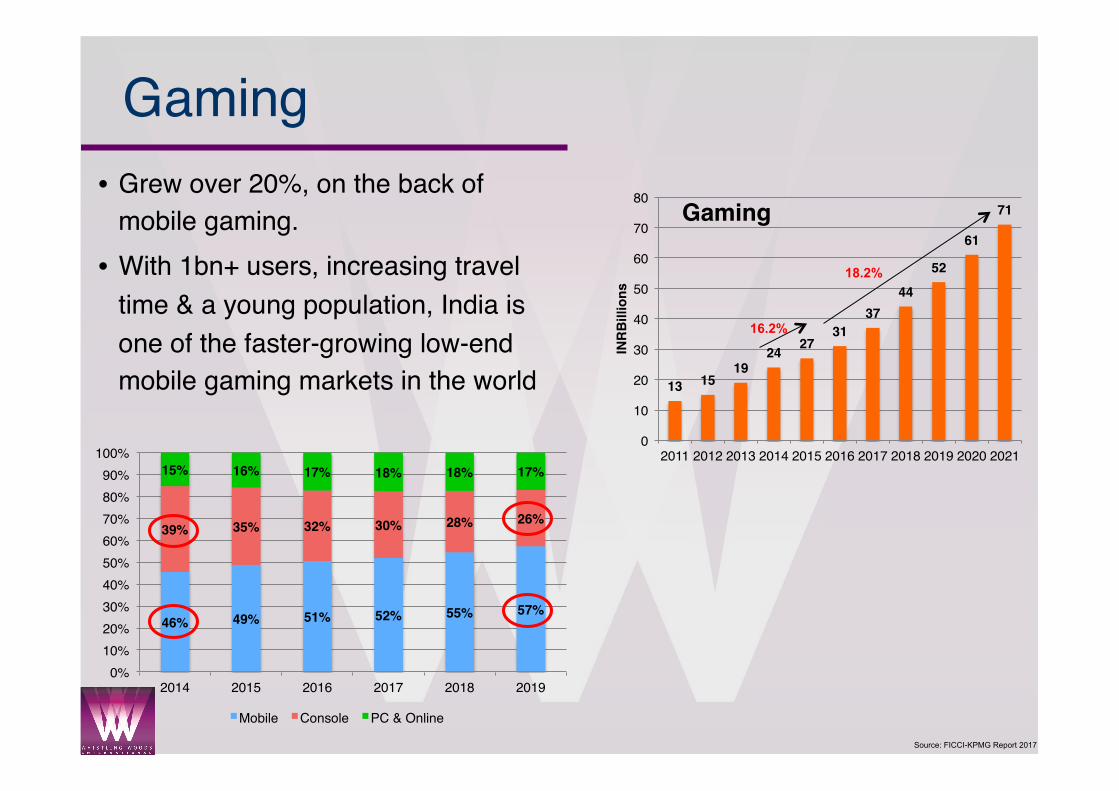

13 1519

24 2731

3744

52

61

71

0

10

20

30

40

50

60

70

80

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

INR

Bill

ions

Gaming

Gaming• Grew over 20%, on the back of

mobile gaming.• With 1bn+ users, increasing travel

time & a young population, India is one of the faster-growing low-end mobile gaming markets in the world

18.2%

46% 49% 51% 52% 55% 57%

39% 35% 32% 30% 28% 26%

15% 16% 17% 18% 18% 17%

0%10%20%30%40%50%60%70%80%90%

100%

2014 2015 2016 2017 2018 2019

Mobile Console PC & Online

16.2%

Source: FICCI-KPMG Report 2017

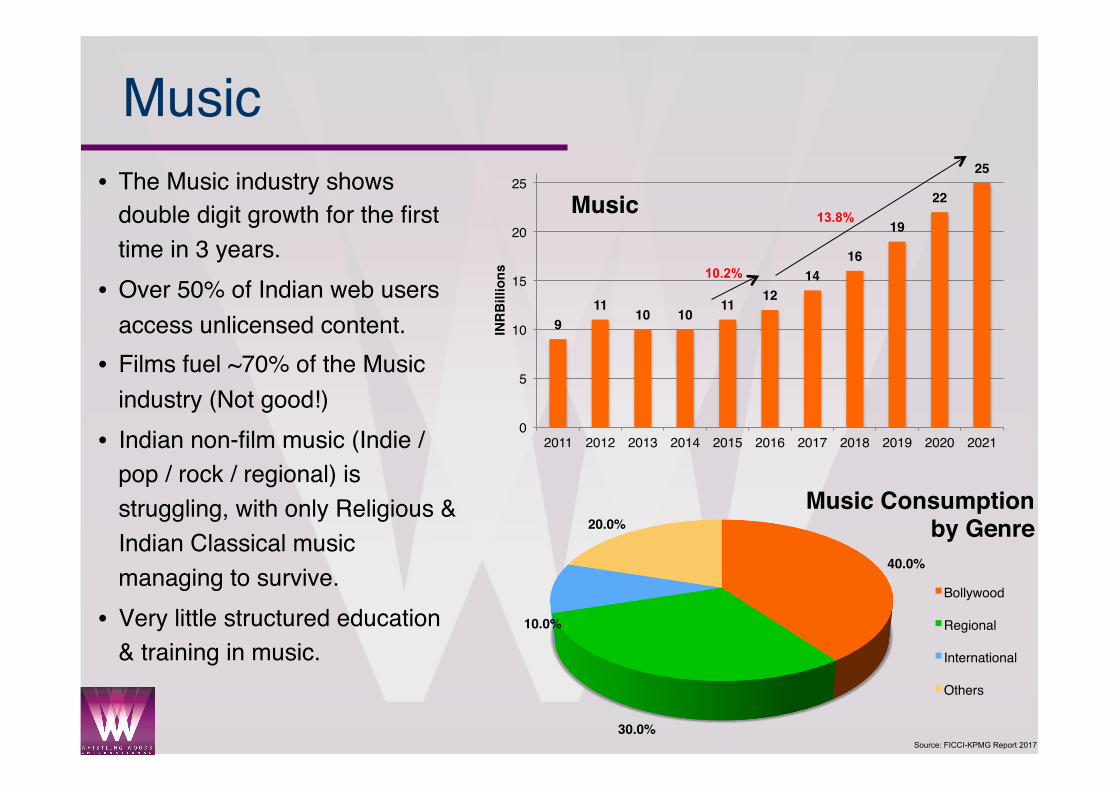

911

10 1011

1214

16

19

22

25

0

5

10

15

20

25

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

INR

Bill

ions

Music

Music• The Music industry shows

double digit growth for the first time in 3 years.

• Over 50% of Indian web users access unlicensed content.

• Films fuel ~70% of the Music industry (Not good!)

• Indian non-film music (Indie / pop / rock / regional) is struggling, with only Religious & Indian Classical music managing to survive.

• Very little structured education & training in music.

13.8%

10.2%

40.0%

30.0%

10.0%

20.0%Music Consumption

by Genre

Bollywood

Regional

International

Others

Source: FICCI-KPMG Report 2017

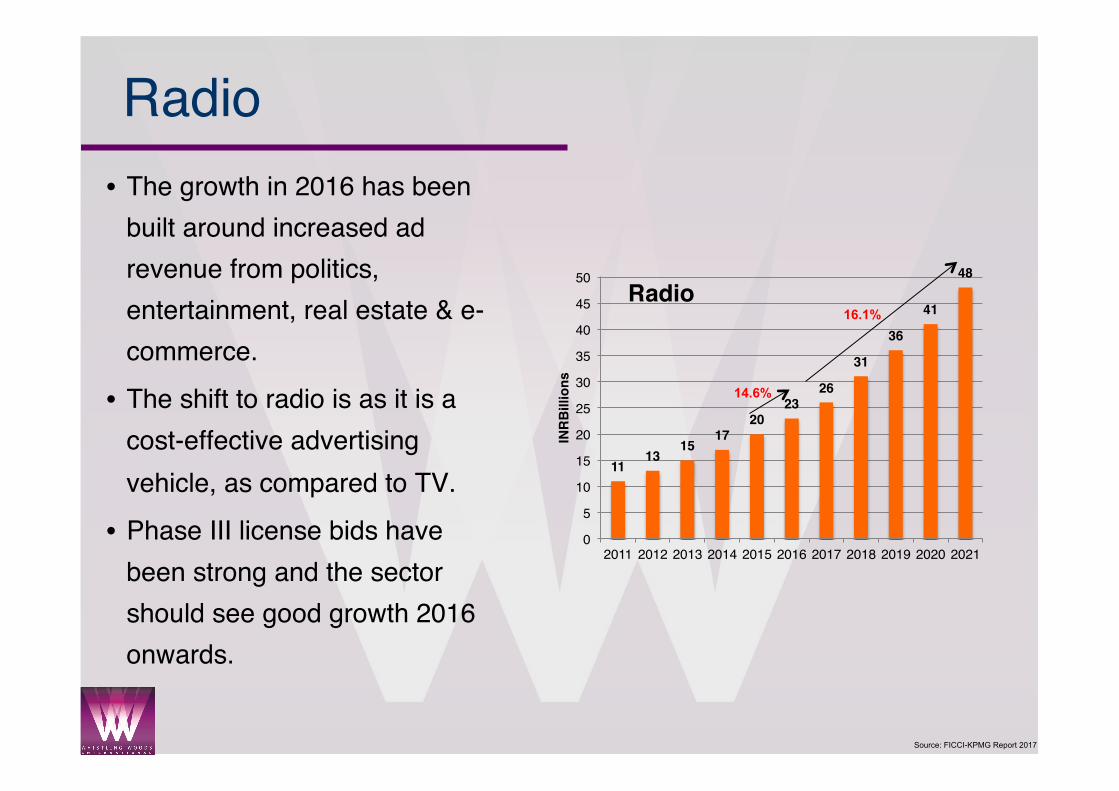

1113

1517

2023

26

31

36

41

48

0

5

10

15

20

25

30

35

40

45

50

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021IN

RB

illio

ns

Radio

Radio• The growth in 2016 has been

built around increased ad revenue from politics, entertainment, real estate & e-commerce.

• The shift to radio is as it is a cost-effective advertising vehicle, as compared to TV.

• Phase III license bids have been strong and the sector should see good growth 2016 onwards.

16.1%

14.6%

Source: FICCI-KPMG Report 2017

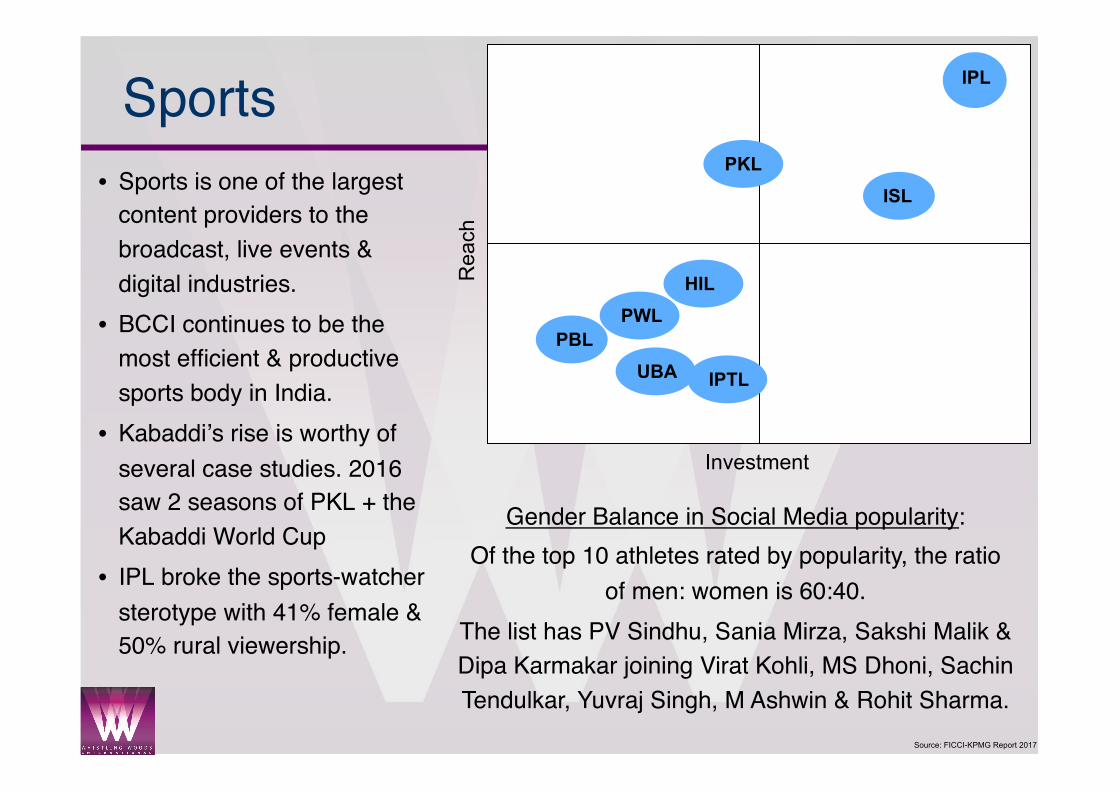

Sports• Sports is one of the largest

content providers to the broadcast, live events & digital industries.

• BCCI continues to be the most efficient & productive sports body in India.

• Kabaddi’s rise is worthy of several case studies. 2016 saw 2 seasons of PKL + the Kabaddi World Cup

• IPL broke the sports-watcher sterotype with 41% female & 50% rural viewership.

IPL

Rea

ch

Investment

ISL PKL

IPTL

PWL PBL

UBA

HIL

Gender Balance in Social Media popularity:Of the top 10 athletes rated by popularity, the ratio

of men: women is 60:40.The list has PV Sindhu, Sania Mirza, Sakshi Malik & Dipa Karmakar joining Virat Kohli, MS Dhoni, Sachin Tendulkar, Yuvraj Singh, M Ashwin & Rohit Sharma.

Source: FICCI-KPMG Report 2017

Live Events

• Yet to be ‘organised’

• Growth of ~33%

• Margin growth flat

• Government / Political spending (elections / events) still the largest contributor

• Licensing issues

• Taxation issues

• Live IP-based entertainment on the rise:

o Stand up Comedy

o Theatre

Source: FICCI-KPMG Report 2017

Theme Parks

• Current size Rs 29.3 billion. Expected to grow to Rs 70 billion by 2021 with a 19.1% CAGR.• Destination tourism based around entertainment yet to

consolidate• Evolution:

o 1980s – Appu Gharo 1990s & 2000s – Esselworldo 2010s – Imagica & Wonderlao 2016 – INR 300 bn+ investment committed for 10 parks across India

Source: FICCI-KPMG Report 2017

Theme Parks

Source: FICCI-KPMG Report 2017

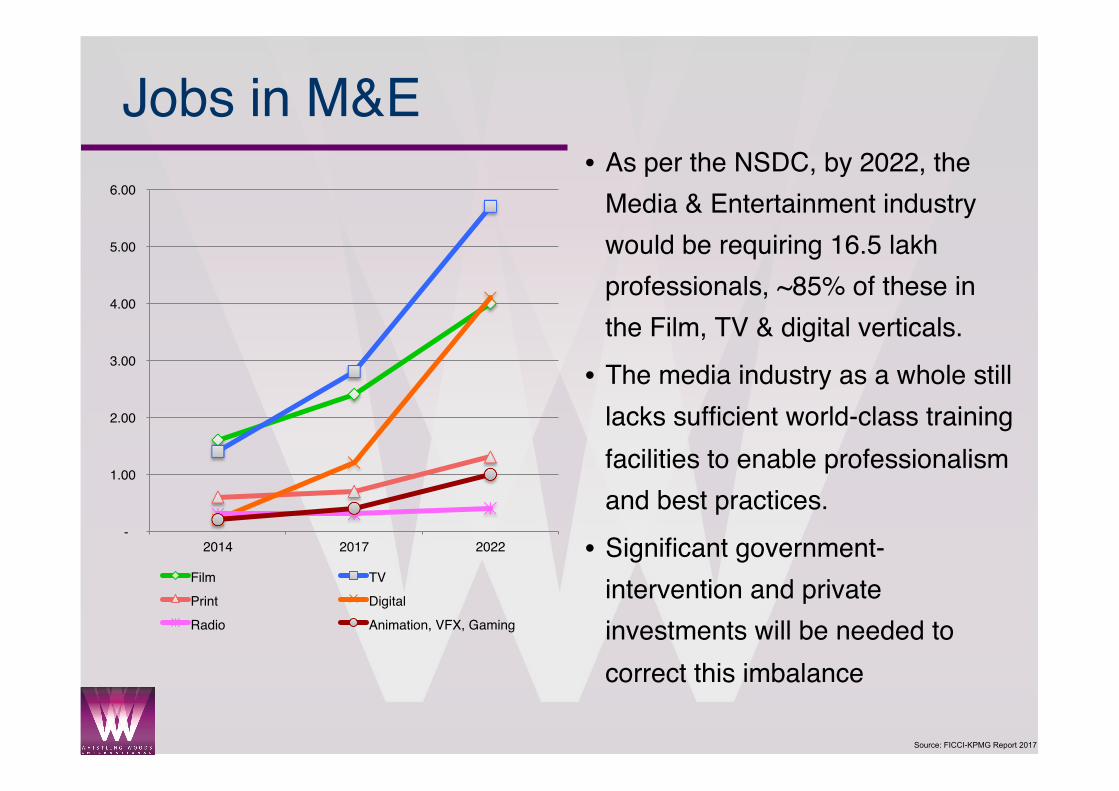

Jobs in M&E• As per the NSDC, by 2022, the

Media & Entertainment industry would be requiring 16.5 lakh professionals, ~85% of these in the Film, TV & digital verticals.

• The media industry as a whole still lacks sufficient world-class training facilities to enable professionalism and best practices.

• Significant government-intervention and private investments will be needed to correct this imbalance

-

1.00

2.00

3.00

4.00

5.00

6.00

2014 2017 2022

Film TVPrint DigitalRadio Animation, VFX, Gaming

Source: FICCI-KPMG Report 2017

What are the pain-points of the Indian M&E Industry?

• Lack of original Intellectual Property creation leading to lack of a globally merchandisable brand.

• M&E Education & Training o Of the 4 lakh people employed, nearly 75% involved in content creation have

no formal training.

o Very few world-class Film & Media institutes with a combined output of approx 500 graduates a year, with 200 of them being from a single institute.

• Innovation – Lack of original formats or technical / narrative innovation.

• Piracy - Affects every sector of the industry & causes nearly 35% revenue reduction

Source: FICCI-KPMG Report 2017

The Great Opportunities in M&E

In the M&E industry, building volume is hard. India already has the volume. We now need to build value to each unit of the already

existing volume. This is done by enhancing quality.

The big opportunities in Indian M&E are:

• IP creation – interoperable IPs across Film, TV, Digital

• Education in M&E

• Content for Digital platforms

• Screens for Film

Thank You!Chaitanya Chinchlikar

[email protected] President - Business Development, Whistling Woods International

Chief Technology Officer, Whistling Woods InternationalVice President - Strategy, Mukta Arts Ltd

Business Head - Digital Media, Mukta Arts Ltd