the impact of the recession on construction professionals · the impact of the recession on...

TRANSCRIPT

The Impact of the Recession on Construction Professionals A view from the front line

Table of Contents1 INTRODUCTION 1 Surveymethod 1

2 MANAGEMENTSUMMARY 2

Businesschallengesandtherecession 2 Responsestotheeconomicdownturn 2 BusinessAdviceandSupport 3 Membershipofprofessionalbodies 3 Keepinguptodatewithindustrynews 3 Thenext12monthsandtheendoftherecession 3

3 THEPROFILEOFTHOSEINTERVIEWED (QUANTITATIVESURVEY) 4

Size 4 Sub-sector 4 Typeofwork 4 Theclientbase 5 Region 5

4 THEIMPACTOFTHEECONOMICRECESSIONAND EMPLOYERRESPONSES 6

Keycurrentbusinesschallenges 6 Mainimpactsoftherecession(spontaneous) 6 Responsestotherecession/downturn(prompted) 8 a)Staffnumbers,recruitmentandredundancies 9 b)Impactontraining 10 c)Impactonskillneeds 13

5 BUSINESSADVICEANDSUPPORT 14

6 MEMBERSHIPOFPROFESSIONALORINDUSTRYBODIES, ANDKEEPINGUPTODATEWITHINDUSTRYNEWS 15

Keepinguptodatewithindustrynews 167 THENEXT12MONTHSANDTHEENDOFTHERECESSION 17

Futureskillsneeds 18 Theendoftherecession 18

ANNEXA:QUANTITATIVEQUESTIONNAIRE 20

PreparedforConstructionIndustryCouncil(CIC)andConstructionSkillsByIFFResearch

1 Introduction

1.1 ConstructionSkillswasestablishedinSeptember2003,bringingtogethertheConstructionIndustryTrainingBoard(CITB),CITBNorthernIrelandandtheConstructionIndustryCouncil(CIC).

1.2 CICwassetupin1988andistherepresentativeforumfortheprofessionalbodies,researchorganisationsandspecialistbusinessassociationsintheconstructionindustry.Ithasacollectivemembershipof500,000individualprofessionalsand25,000firmsofconstructionconsultants.WithinConstructionSkillsCICrepresentstheviewsofthoseoperatinginprofessional,managerialandtechnicalpositionswithintheindustry.

1.3 Theaimofthecurrentresearchwastoprovideauthoritativeandcomprehensiveanalysison:

•Theimpactoftherecessionon: -thecurrentandexpectedfuturesizeandnature

oftheworkforceintheprofessionalservicessector;

-recruitmentofgraduates; -trainingactivity; -skillrequirements;•Themeasuresthatfirmsinthesectorhavetakenin

responsetotherecession

•Employerviewsontheavailabilityandqualityofbusinesssupportandadvice

•Theextentofanyemergingnewskillrequirements

Survey method

1.4 Theresearchinvolvedtwoelements:

•Aninitialqualitativephase,involving30teledepthswithfirmswithintheprofessionalservicessector.Discussionslastedaround45minutesonaverage,andtookplacefrom19thAugustto18thSeptember2009.

•Aquantitativesurveyof301professionalservicesfirmsemploying5ormorestaffacrosstheUK.Thistookplacefrom7th–19thOctober2009.Thequestionnaireusedisappended(AnnexA)–interviewstookonaveragearound15minutestocomplete.

1.5 AllinterviewswereconductedbyspecialistIFFbusiness-to-businessinterviewers,workingfromIFF’sofficesinLondon.

1.6 SampleforthesurveycamefromConstructionSkills’EmployerPanel,plusadditionalsamplepurchasedfromExperian’sBusinessDatabase.

1.7 Forthequantitativephase,quotasweresettoensureareasonablespreadacrosstheindustrybyregionandsize.

1.8 Surveydataisreportedunweighted.

A note on statistical reliability

1.9 It is worth noting that statistical reliability on asample size of 301 (in the worst case scenario from a reliability point of view of a survey result of 50%) is +/- 6% (i.e. we are 95% confident that the true result, if views had been obtained from all employers rather than a sample, lies within 6% of the survey finding). The statistical reliability is a lot lower where we report results among sub-groups of the sample (for example by region, size of employer or sub-sector, or where we look at results among those that have reduced staff numbers or taken particular action). In these cases results should be treated with some caution, and may best be regarded as indicative only.

2.1 Thisreportpresentsfindingsofresearchinvolving30in-depthinterviewswithemployersandaquantitativesurveyof301telephoneinterviewswithprofessionalservicesfirms,thelatterconductedinthefirsthalfofOctober2009.

Business challenges and the recession

2.2 Theeconomicrecessionwasclearlyverymuchinemployers’minds:whenaskedwhatthekeychallengeswerefacingtheircompany,55%spontaneouslymentionedtheneedtoincreaseworkload,18%mentionedspecificallydealingwiththerecession,and18%weresufferingcashflowdifficulties.Just1%mentionedastheirmainchallengehavingmoreworkthantheycouldhandle,andonly8%hadnokeybusinesschallenges.

2.3 For54%ofcompaniestheirfeeincomeinthelast12monthswaslowerthantheprevious12months.Thiscompareswith11%sayingithadincreased.Thoseinbuildingservicesengineeringappeartohavefaredbetterthanaverage(24%reportedincreasedfeeincome,thoughstillmanymore(41%)hadexperiencedadecrease).Responses to the economic downturn

2.4 Only7%offirmsreportedtakingnoparticularstepstomeetthechallengespresentedbytherecession.Themostcommonactionstakenhavebeen:

•Spendingmoretimebiddingforwork(72%ofallfirms)

•Cuttingbackontheplannedrecruitmentofgraduatesornewlyqualifiedstaff(46%,though8%haveincreasedthispresumablytoreplacemoreexpensive,experiencedstaff)

•Makingredundancies(46%)

•Cuttingbackontheplannedrecruitmentofsupportstaff(37%)

•Reducedworkinghours(27%)

•Cuttingbackontheuseoffreelanceoragencystaff(26%,though10%hadactuallyincreasedthis)

•Recruitingnewstaffwithdifferentspecialismstoenablethefirmtoworkinnewsectors(16%).

2.5 Redundancies:46%ofemployershadmaderedundanciesbecauseoftherecession.Thesehaveaffectedawiderangeofoccupationalgroups,mostoftenadministrativepositions(35%ofemployersmaking

redundancieshadmadesuchstaffredundant),followedbytechnicians(15%),architects(14%),projectmanagers(9%)andmechanical,civilandotherengineers(8%,6%and18%respectively).

2.6 The total number of staff employed:surveyresultssuggestthatthetotalnumberofstaffemployedacrosstheprofessionalservicessectorhasdecreasedby6%comparedwith12monthspriortotheinterview.

2.7 Planned recruitment of graduates and newlyqualified staff:46%offirmshadcutbackonplannedrecruitmentofgraduatesandnewlyqualifiedstaffbecauseoftherecession:theactualnumbertheyhadtakenon(anaverageofapproximately1.5perfirm)wasaroundasixthofthenumbertheyhadplanned.Anothermeasureoftheeffectoftherecessionisinthenumberofgraduatesandnewlyqualifiedstaffemployedbyfirms.Resultsindicatethatacrosstheprofessionalservicesindustrycoveredbythissurvey(whichexcludedmicrofirmswithfewerthan5staff)graduatesandnewlyqualifiedstaffcomprisejustover4%ofthetotalworkforce,halfthenumbertheyemployed12monthsago.

2.8 Over-supply of graduates:giventhefallinthelevelofrecruitmentofgraduatesandnewlyqualifiedstaffitisnotsurprisingthat67%ofprofessionalservicesfirmsfeltthatthesupplyofgraduatescurrentlyexceedsthedemand.Architectswerethedisciplinemostoftenmentionedbyemployersassufferingfromexcesssupply.

2.9 Training:theeconomicdownturnhashadanimpactonthetrainingundertakenbyprofessionalservicesfirms,thoughthisisperhapslessseverethanmighthavebeenanticipated.Whileoverathirdoffirms(35%)hadreducedtheirtrainingspendasaresponsetotherecession,forexamplebyincreasingtheamountofin-housetraining,theproportionthathadreducedtheirtrainingactivity(25%)wasonlyalittlehigherthantheproportionthathadincreasedtrainingasaresponsetotherecession(22%).Similarlyitcouldbeviewedquitepositivelythat‘only’16%ofprofessionalservicesfirmshavereducednextyear’strainingbudgetorplannedtrainingactivity.

2.10 Skills in the recession:20%offirmsfeltthattherecessionhashadanimpactontheskillsthattheyneedfromtheircurrentstafforpotentialrecruits.Themostcommonskillsbecomingmoreimportanttoemployersintherecessionarebusinessdevelopmentskills(16%),specialistjob-specificskills(16%),theabilitytomulti-skill(15%),engineering-relatedskills(13%),andup-gradingexistingskills(13%).

2 Management Summary

2 1

Business Advice and Support

2.11 30%offirmshadsoughtadvice,guidanceandsupportsincethestartoftherecession.Themostcommonorganisationsconsultedwereaccountants(7%ofallfirms),professionalinstitutions(7%),Businesslink(7%),andindependentconsultants(6%).Overall1%ofprofessionalservicefirmshadsoughtadviceorsupportfromeithertheCICorConstructionSkills.

2.12 Reassuringly,thevastmajorityhavebeenabletofindtheadviceandsupportthattheywanted–just7%offirmsindicatedthatthereweretypesofbusinessadviceandsupportthattheyfoundhardtoaccess,thoughthisrisesto13%amongfirmswith5-9staff.Whereemployershadstruggledtofindsupportoradvicethiswasmostoftenforfinancialsupport(3%ofallprofessionalservicesfirms),followedbyIT,training,businessdevelopment,andmarketing(eachmentionedby1%ofemployers).

2.13 Overallthreequartersofprofessionalservicesfirmsratetheavailabilityandqualityofbusinessadviceandguidanceforcompaniesintheprofessionalservicessectoraseithersatisfactory(30%),good(36%)orverygood(8%),comparedagainst7%thatrateitaspoor.Membership of professional bodies

2.14 81%ofprofessionalservicesfirmsweremembersofaprofessionalorindustrybody.13%offirmssaidtherecessionhasledthemtore-considercompanyoremployeemembershipoftheseorganisations.Thisvariedrelativelylittlebysizeoffirm,indicatingtheextenttowhichtherecessioniscausingfirmsofallsizestothinkcloselyabouttheiroperatingcosts.

Keeping up to date with industry news

2.15 Avarietyofmeansareusedtokeepuptodatewithindustrynews,mostcommonly:

•Industrypressandmagazines(mentionedby33%)

•Websites(15%)

•Newsletters/emails(14%)

•Wordofmouthandinformalmeans(13%)

•Meetings,seminars,conferences(8%)

The next 12 months and the end of the recession

2.16 32%ofemployersfeltthattheirfeeincomewouldincreaseoverthenext12months,comparedwith17%expectingthistofall.Thelargestproportionexpectedittoremainataboutthesamelevel(44%),thoughnotsurprisinglysomedidnotfeelconfidenttoanswer(8%).Onbalancethereforethefindingsarereasonablypositive

withapproximatelytwiceasmanyexpectinggrowthasexpectingreducedfeeincome.

2.17 Intotal,25%offirmsfeltitwaslikelythattheywouldhavetomakeredundanciesinthenext12months,including3%thathavealreadyplannedtheredundancies.Itismoderatelyencouragingthatmorethinkitquitelikely(17%)thanverylikely(5%)suggestingthatformanythedecisionwilldependontheirperformanceinthecomingmonths.

2.18 40%ofemployersfeelthattheworstoftherecessionisover(interviewstookplaceinearlyOctober2009).Anumberofactionswerequiteoftenfelttobeneededtospeeduptherecoveryinthesector,includingbanksstartingtolendagain(mentionedby19%ofallfirmsspontaneously),morefundingandinvestment(12%),andthenresponsesfocusedonincreasedgovernmentsupportincludingmoregovernmentspendinginthepublicsector(11%)oronnewprojects(8%),bringinggovernmentprojectsforward(7%)andincreasedgovernmentspendingoninfrastructure(6%).

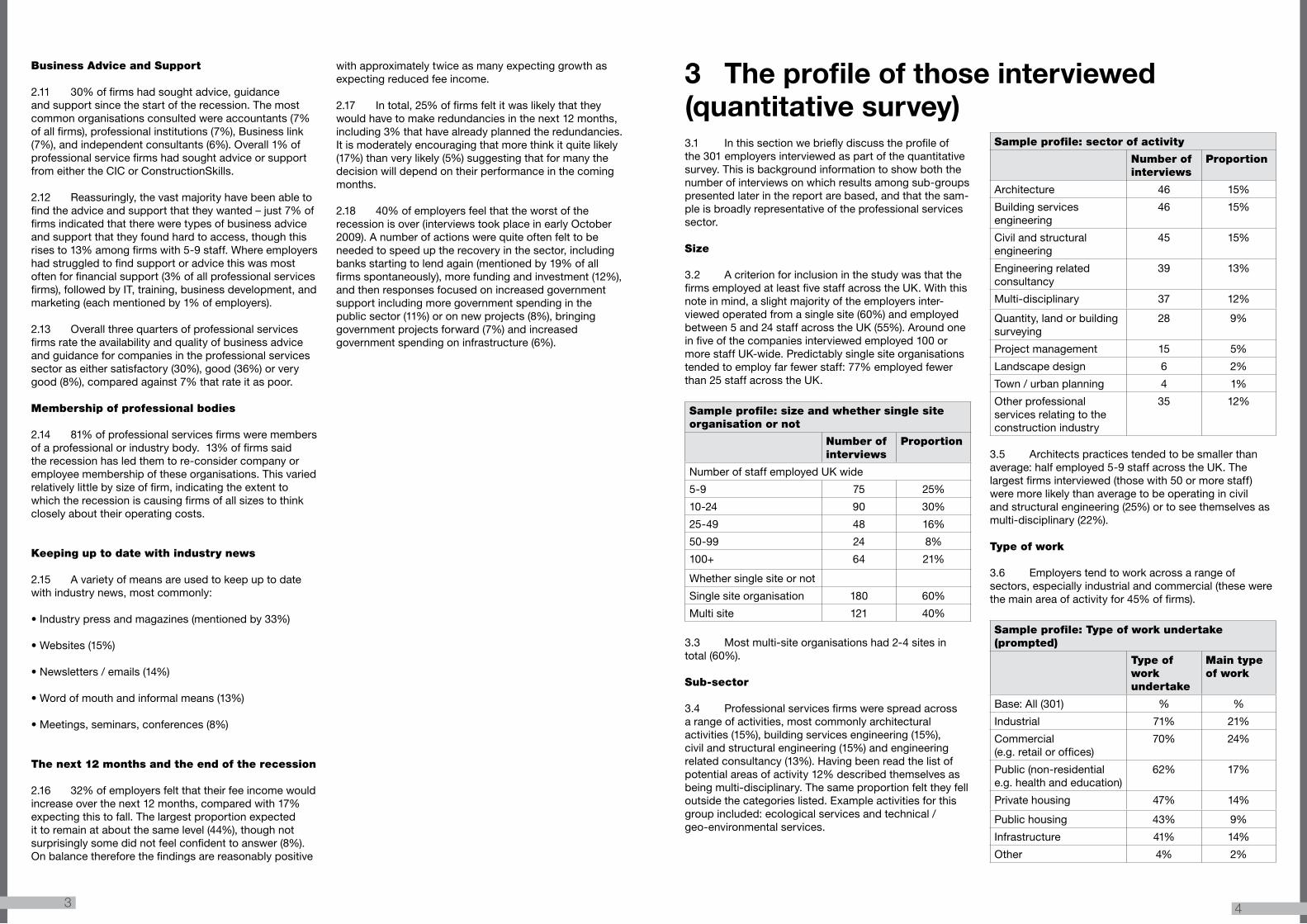

3.1 Inthissectionwebrieflydiscusstheprofileofthe301employersinterviewedaspartofthequantitativesurvey.Thisisbackgroundinformationtoshowboththenumberofinterviewsonwhichresultsamongsub-groupspresentedlaterinthereportarebased,andthatthesam-pleisbroadlyrepresentativeoftheprofessionalservicessector.

Size

3.2 AcriterionforinclusioninthestudywasthatthefirmsemployedatleastfivestaffacrosstheUK.Withthisnoteinmind,aslightmajorityoftheemployersinter-viewedoperatedfromasinglesite(60%)andemployedbetween5and24staffacrosstheUK(55%).Aroundoneinfiveofthecompaniesinterviewedemployed100ormorestaffUK-wide.Predictablysinglesiteorganisationstendedtoemployfarfewerstaff:77%employedfewerthan25staffacrosstheUK.

Sample profile: size and whether single site organisation or not

Number of interviews

Proportion

NumberofstaffemployedUKwide

5-9 75 25%

10-24 90 30%

25-49 48 16%

50-99 24 8%

100+ 64 21%

Whethersinglesiteornot

Singlesiteorganisation 180 60%

Multisite 121 40%

3.3 Mostmulti-siteorganisationshad2-4sitesintotal(60%).

Sub-sector

3.4 Professionalservicesfirmswerespreadacrossarangeofactivities,mostcommonlyarchitecturalactivities(15%),buildingservicesengineering(15%),civilandstructuralengineering(15%)andengineeringrelatedconsultancy(13%).Havingbeenreadthelistofpotentialareasofactivity12%describedthemselvesasbeingmulti-disciplinary.Thesameproportionfelttheyfelloutsidethecategorieslisted.Exampleactivitiesforthisgroupincluded:ecologicalservicesandtechnical/geo-environmentalservices.

Sample profile: sector of activity

Number of interviews

Proportion

Architecture 46 15%

Buildingservicesengineering

46 15%

Civilandstructuralengineering

45 15%

Engineeringrelatedconsultancy

39 13%

Multi-disciplinary 37 12%

Quantity,landorbuildingsurveying

28 9%

Projectmanagement 15 5%

Landscapedesign 6 2%

Town/urbanplanning 4 1%

Otherprofessionalservicesrelatingtotheconstructionindustry

35 12%

3.5 Architectspracticestendedtobesmallerthanaverage:halfemployed5-9staffacrosstheUK.Thelargestfirmsinterviewed(thosewith50ormorestaff)weremorelikelythanaveragetobeoperatingincivilandstructuralengineering(25%)ortoseethemselvesasmulti-disciplinary(22%).

Type of work

3.6 Employerstendtoworkacrossarangeofsectors,especiallyindustrialandcommercial(thesewerethemainareaofactivityfor45%offirms).

Sample profile: Type of work undertake (prompted)

Type of work undertake

Main type of work

Base:All(301) % %

Industrial 71% 21%

Commercial(e.g.retailoroffices)

70% 24%

Public(non-residentiale.g.healthandeducation)

62% 17%

Privatehousing 47% 14%

Publichousing 43% 9%

Infrastructure 41% 14%

Other 4% 2%

3 The profile of those interviewed (quantitative survey)

4 3

The client base

3.7 65%ofprofessionalservicesfirmsworkmainlyforprivateclients.Theremaindersplitevenlybetweenthosewhoworkmainlyforcommercialclients(10%),thegovernmentorpublicsector(11%)orasasub-consultantforconstructionorconsultancyfirms(13%).

3.8 Thesmallestfirms(with5-9staffacrosstheUK)weremorelikelythanaveragetoworkmainlyforprivateclients(72%)andrarelyhadthegovernmentorpublicsectorastheirmainclient.Predictablythelargestfirms(with50ormorestaffacrosstheUK)werefarmorelikelythanaveragetohavethegovernmentorthepublicsectorastheirmainclient(18%),butstillthemajorityworkedmainlyforprivateclients(59%).

Region

3.9 TheinterviewingsoughttoachieveabroadspreadbyregionandcountrytoensurethatallpartsoftheUKwerecovered(ratherthanbestrictlyrepresentativeindistributinginterviewstoregioninexactproportiontotheregion’sshareoftheoverallUKprofessionalservicessector).Asshownonthefollowingtable,basesizesaretoolowtopresentresultswithinthisreportreliablybyindividualregion/country.

Sample profile: region / country

Number of interviews

Proportion

SouthEast 35 12%

London 35 12%

East 30 10%

SouthWest 30 10%

NorthEast 26 9%

EastMidlands 27 9%

NorthWest 25 8%

Yorkshire&Humberside 25 8%

Scotland 22 7%

NorthernIreland 17 6%

WestMidlands 16 5%

Wales 13 4%

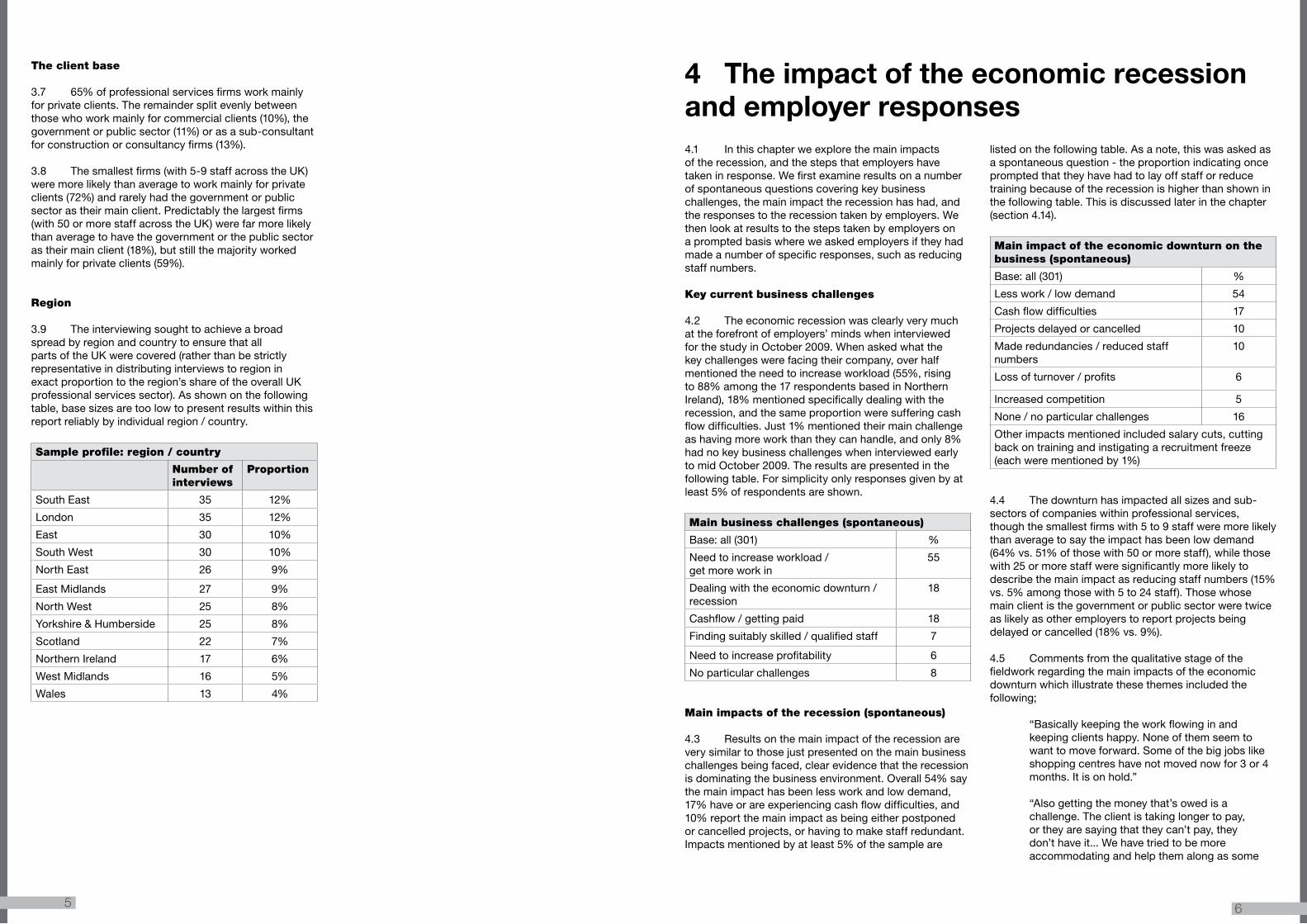

4.1 Inthischapterweexplorethemainimpactsoftherecession,andthestepsthatemployershavetakeninresponse.Wefirstexamineresultsonanumberofspontaneousquestionscoveringkeybusinesschallenges,themainimpacttherecessionhashad,andtheresponsestotherecessiontakenbyemployers.Wethenlookatresultstothestepstakenbyemployersonapromptedbasiswhereweaskedemployersiftheyhadmadeanumberofspecificresponses,suchasreducingstaffnumbers.

Key current business challenges

4.2 Theeconomicrecessionwasclearlyverymuchattheforefrontofemployers’mindswheninterviewedforthestudyinOctober2009.Whenaskedwhatthekeychallengeswerefacingtheircompany,overhalfmentionedtheneedtoincreaseworkload(55%,risingto88%amongthe17respondentsbasedinNorthernIreland),18%mentionedspecificallydealingwiththerecession,andthesameproportionweresufferingcashflowdifficulties.Just1%mentionedtheirmainchallengeashavingmoreworkthantheycanhandle,andonly8%hadnokeybusinesschallengeswheninterviewedearlytomidOctober2009.Theresultsarepresentedinthefollowingtable.Forsimplicityonlyresponsesgivenbyatleast5%ofrespondentsareshown.

Main business challenges (spontaneous)

Base:all(301) %

Needtoincreaseworkload/getmoreworkin

55

Dealingwiththeeconomicdownturn/recession

18

Cashflow/gettingpaid 18

Findingsuitablyskilled/qualifiedstaff 7

Needtoincreaseprofitability 6

Noparticularchallenges 8

Main impacts of the recession (spontaneous)

4.3 Resultsonthemainimpactoftherecessionareverysimilartothosejustpresentedonthemainbusinesschallengesbeingfaced,clearevidencethattherecessionisdominatingthebusinessenvironment.Overall54%saythemainimpacthasbeenlessworkandlowdemand,17%haveorareexperiencingcashflowdifficulties,and10%reportthemainimpactasbeingeitherpostponedorcancelledprojects,orhavingtomakestaffredundant.Impactsmentionedbyatleast5%ofthesampleare

listedonthefollowingtable.Asanote,thiswasaskedasaspontaneousquestion-theproportionindicatingoncepromptedthattheyhavehadtolayoffstafforreducetrainingbecauseoftherecessionishigherthanshowninthefollowingtable.Thisisdiscussedlaterinthechapter(section4.14).

Main impact of the economic downturn on the business (spontaneous)

Base:all(301) %

Lesswork/lowdemand 54

Cashflowdifficulties 17

Projectsdelayedorcancelled 10

Maderedundancies/reducedstaffnumbers

10

Lossofturnover/profits 6

Increasedcompetition 5

None/noparticularchallenges 16

Otherimpactsmentionedincludedsalarycuts,cuttingbackontrainingandinstigatingarecruitmentfreeze(eachwerementionedby1%)

4.4 Thedownturnhasimpactedallsizesandsub-sectorsofcompanieswithinprofessionalservices,thoughthesmallestfirmswith5to9staffweremorelikelythanaveragetosaytheimpacthasbeenlowdemand(64%vs.51%ofthosewith50ormorestaff),whilethosewith25ormorestaffweresignificantlymorelikelytodescribethemainimpactasreducingstaffnumbers(15%vs.5%amongthosewith5to24staff).Thosewhosemainclientisthegovernmentorpublicsectorweretwiceaslikelyasotheremployerstoreportprojectsbeingdelayedorcancelled(18%vs.9%).4.5 Commentsfromthequalitativestageofthefieldworkregardingthemainimpactsoftheeconomicdownturnwhichillustratethesethemesincludedthefollowing;

“Basicallykeepingtheworkflowinginandkeepingclientshappy.Noneofthemseemtowanttomoveforward.Someofthebigjobslikeshoppingcentreshavenotmovednowfor3or4months.Itisonhold.”

“Alsogettingthemoneythat’sowedisachallenge.Theclientistakinglongertopay,ortheyaresayingthattheycan’tpay,theydon’thaveit...Wehavetriedtobemoreaccommodatingandhelpthemalongassome

4 The impact of the economic recession and employer responses

6 5

arestillfindingittricky,buttheywillcomethroughintheendandwewillgetthemoneyintheend.”

“I’vehadtoputthestaffonfourdaysaweekatthemomentbecauseofreducedwork,andreducedfees.Atthemomentwedon’tseeanychinkoflight.”

“Thebiggestproblemwehaveisthebanksandtheirlackoffundingonprojectswhichhasjustkindofkilledhalfofourprofits.We’vegotawholetrackofschemesthatarewaitingtogo,buttheclientscan’tgetfundingfrombanks.”

4.6 Againindicativeoftheextenttowhichprofessionalservicesemployersarebeingaffectedbythedownturn,thevastmajority(82%)hadtakensomestepstomeetthechallengesithaspresentedthemwith.Resultsareshownonthefollowingtable,whichlistsresponsesmentionedbyatleast5%ofemployers.Itshouldbenotedthatthiswasaspontaneousquestion,andtheproportionthathavetakenthesestepswhenaskedasapromptedquestionishigher(seesection4.14).

4.7 Themainresponsestotherecessionhavebeencuttingcostsand/ormakingredundancies(eachmentionedbyaroundaquarter),withsomespecificallymentioningreducingworkinghoursorencouragingunpaidleave(7%).Othershaveputmoreeffortintosalesandmarketing,forexamplebylookingforworkinsectorstheydonottraditionallyworkin(19%)orbyincreasingtheiradvertisingormarketingspend(15%).Commentsfromthequalitativeresearchincluded;

“Inanutshellwe’vehadtodiversifyfromourcorebusiness.Althoughwe’vestillgotexistingclientswhichweareobligedtocompleteworksfor.They’vedriedup.They’relookingattheircoffers.Sowe’vegottokeepourselvesafloatandwe’vebranchedoutintoothermarkets.”

Main steps taken to meet the challenges presented by the economic downturn (spontaneous)

Base:all(301) %

Cutcosts/overheads 27

Maderedundancies 23

Soughtworkinalternative/differentsectors

19

Increasedadvertising/marketing 15

Reducedworkinghours/encouragedstafftoworkparttimeortakeunpaidleave

7

Spentmoretimelookingforwork 6

Increasedefficiency/productivity 5

Increasedtheamountoftraininggiven 5

None/noparticularstepstaken 18

Otherstepstakenincludedreducingtheirfeesorrates(3%),cuttingbackonplannedrecruitment(2%)andreducingtraining(2%).

4.8 Londonemployersandthosewith50ormorestaffemployedacrosstheUKwereparticularlylikelytomentionmakingredundancies(40%and33%respectively).

4.9 Whenaskedspecificallywhethertheirfeeincomehadincreased,decreasedorstayedthesamecomparedwiththeprevious12months,justoverhalfindicatedthishadfallen(54%)comparedwith11%thathadseenfeeincomeincrease.Resultsaresummarisedonthefollowingchart,whichshowstheproportionreportinganincreaseordecrease.Forsimplicity,thosesayingfeeincomehadremainedlargelyunchanged(28%)orwereeitherunsureorrefused(7%)havenotbeenshown.LowbasesizesforWalesandNorthernIrelandshouldbenoted.4.10 Afallinfeeincomehasparticularlyaffectedsmalleremployers,andappearstohaveparticularlyaffectedthoseinNorthernIrelandandWales,thoughlowbasesizesmeanresultsshouldbetreatedwithcaution.Bysub-sector,buildingservicesengineeringappearstohavefaredbetterthanaverage:24%reportincreasedfeeincomeinthelast12monthscomparedwiththeprevious12months,thoughitwasmorecommonforthemtoreportthatincomehaddecreased(41%).

4.11 Thosesayingfeeincomehaddecreasedandwhowereabletogiveafigurefortheextenttowhichithadfalleninthelast12monthscomparedwiththeprevious12months(abaseof138respondents)typicallycitedfallsof10-19%(26%),20-29%(27%)or30-39%(17%).Onaveragethedecreaseinfeeincomewas26%.

4.12 Aswehaveseenfewerreportedanincreaseinfeeincome(11%-abaseof34respondents).Onaveragetheserespondentsreportedanincreaseof25%.

4.13 Thefollowingexamplefromthequalitativeresearchillustratestheimpactoftherecessiononfeeincome;

“Feesarereducedby30%duetocompetitionandlowvolumeandvalueofnewwork.Iftheywantustodoittheywilltellustoreducethefee.Lastweektherewasonewherethequotewas£6k,theysaidifyoucandoitfor£2,500thenyou’vegotit.Weaccepteditbecauseatleastitissomethingcomingin.Wehavetoacceptwhattheclientsays.Theproblemistherearefreelancerswhodonothavetheoverheadswhocanaffordtogoinatalowerprice.”

Responses to the recession / downturn (prompted)

4.14 Followingspontaneousquestions,employerswereaskedpromptedquestionsabouttheirresponsestotheeconomicdownturn.Onceprompted,only7%offirmsreportedtakingnoparticularstepstomeetthechallengespresentedbytherecession.Themostcommonresponsewasspendingmoretimebiddingforworkorwritingproposals(72%).Followingthis,nearlyhalfprofessionalservicesfirmshadcutbackontheplannedrecruitmentofgraduatesornewlyqualifiedstaff(46%)orhadmaderedundancies(46%).Asonementionedatthequalitativephase“Ithinkthatitisinappropriateatthemomenttotakeonnewgraduateswhenpotentiallytheremaybeanotherroundofredundancies.”

4.15 Nearlytwo-fifthsofemployershadcutbackontheplannedrecruitmentofsupportstaff,whilstaroundaquarterhadreducedworkinghoursorcutbackontheuseoffreelanceoragencystaff.

4.16 10%offirmshadincreasedtheiruseoffreelanceoragencystaffand8%hadincreasedtheirplannedrecruitmentofgraduatesornewlyqualifiedstaff.

69%

76%

50%

57%

61%

24%

6%

7%

19%

16%

7%

11%

Decreased Increased

All (301)

Base: all

Fee income in the last 12 months compared with the previous 12 months

41%

47%

54%

5-9 staff (75)

10-24 staff (90)

25-49 staff (48)

50+ staff (88)

Wales (13)

Building services engineering (46)

Northern Ireland (17)

8%

8%

10%

16%

26%

27%

37%

46%

46%

72%

None / no particular steps taken

Increased planned recruitment of graduates or newly qualified staff

Increased use of freelance or agency staff

Recruited different specialisms

Cut back on use of freelance or agency staff or consultants

Reduced working hours

Cut back on planned recruitment of support staff

Made staff redundant

Cut back on planned recruitment of graduates or newly qualified staff

Spend more time bidding for work / writing proposals

Base: All respondents (301)

Responses to the economic downturn (prompted)

8 7

4.17 Thereappeartobesomedifferencesbysizeofcompany,subsectorandregioninhowcompanieshaverespondedtotheeconomicdownturn:

•Largerfirmswithover50staffweresignificantlymorelikelythanthosewith5-9stafftohavemadestaffredundant(67%vs.32%),tohavecutbackonplannedrecruitmentofsupportstaff(44%vs.25%),tohavecutbackonuseoffreelanceoragencystaff(36%vs.20%5-9staff)ortohaverecruitednewspecialismstoenablethefirmtoworkinnewsectors(17%vs.7%).

•Bycountry/region,employersinNorthernIrelandwerethemostlikelytohavespentmoretimebiddingforwork(94%inNorthernIrelandcomparedwith72%UK-wide).FirmsintheSouthEastweretheleasttohavetakenanystepsinresponsetothedownturn(17%comparedto7%acrossallfirms).

•Buildingservicesengineeringfirmswerethemostlikelytohavemadenospecificresponsetotheeconomicdownturn(17%comparedtoaverageof7%acrossallfirms),confirmingthatthisappearstobethesub-sectorleastaffectedbythedownturn.Civilandstructuralengineeringfirmswereconsistentlymorelikelythan

averagetohavetakeneachofthesteps:64%hadcutbackonrecruitingnewgraduates,58%hadreducedtheuseofsupportstaff,56%hadmaderedundancies,42%hadcutbackontheuseoffreelancestaffand40%hadreducedworkinghours.

a) Staff numbers, recruitment and redundancies

4.18 Resultssuggestthatthetotalnumberofstaffemployedacrosstheprofessionalservicessectorhasdecreased6%overthepast12months.Thefallismostmarkedforthesmallestfirmscurrentlyemploying5to9staffacrosstheUK(21%).

4.19 46%ofthecompaniesinterviewedhadrespondedtotheeconomicdownturnbyreducingstaffnumbers.Theseredundancieshaveaffectedawiderangeofoccupationalgroups,asshowninthefollowingchart,whichlistsoccupationsmentionedbyatleast4%oftheseemployers.Employersthathadreducedstaffnumbersweremostlikelytohavemaderedundanciesinadministrativepositions,followedbytechnicians,architects,projectmanagersandmechanical,civilandotherengineers.

4.20 16%ofprofessionalservicesfirmshadrespondedbyrecruitingstaffwithdifferentspecialismstoenablethefirmtoworkinnewsectors.Amongthese47respondents,awiderangeofoccupationshadbeentakenon,mostcommonlyengineers(29%),environmentalandrenewableenergyspecialists(11%),architects,technicians,andHR,legalandbusinessprofessionals(each6%).Otheroccupationsmentionedbyjustoneortwoemployersincludedtownplanners,healthandsafetyspecialists,projectmanagers,CADdraftsmenandConstructionDesignManagement(CDM)co-ordinators.4.21 Lookingspecificallyatgraduatesandnewlyqualifiedstaff,thenumberofsuchemployeestakenonbyfirmshasdroppedconsiderablyasaresultoftherecession,and46%ofcompanieshadcutbackontheplannedrecruitmentofgraduatesornewlyqualifiedstaff.Amongthe138firmsinterviewedthathadtakenthisstep,theactualnumbertheyhadtakenon(anaverageofapproximately1.5perfirm)representedjust17%ofthenumbertheyhadplannedtotakeon(anaverageofjustover9perfirm).

4.22 Thesefiguresrefertotherecruitmentofgraduatesandnewlyqualifiedstaff.Anothermeasureoftheeffectoftherecessioninthisareaisinthenumberofgraduatesandnewlyqualifiedstaffcurrentlyemployedbyfirms.Resultsindicatethatacrosstheprofessionalservicesindustrycoveredbythissurvey(whichexcludedmicrofirmswithfewerthan5staff)graduatesandnewlyqualifiedstaffmakeupjustover4%ofthetotalworkforce,halfthenumber(49%)theyemployed12monthsago.

4.23 Giventhefallinthelevelofrecruitmentofgraduatesandnewlyqualifiedstaffitisnotsurprisingthatasmanyas67%ofprofessionalservicesfirmsfeltthatthesupplyofgraduatescurrentlyexceedsthedemand.Architecturalfirmswerethemostlikelytoagreethatthiswasthecase(85%),andarchitectsweretheoccupationmostoftenmentionedwherethesupplyofgraduateswasfelttoexceeddemand.Resultsaresummarisedinthefollowingtable,basedfirstonthosethinkingsupplyexceedsdemand,andthenonallemployers.

Main disciplines where supply of graduates exceeds demand

Base: Thosethinkingsupplyexceeddemand(202)

All(301)

% %

Architects 21 14

Civilengineers 14 10

Acrosstheboard 11 7

QuantitySurveyors 10 7

StructuralEngineers 8 6

MechanicalEngineers

7 5

ElectricalEngineers 7 5

Engineers(unspecified)

7 5

Environmentaloccupations

6 4

BuildingSurveyors 4 3

Don’tknow 7 15

4.24 Thesefindingswerebackedupfromthequalitativeanalysis.

“The supply of graduates is currently exceeding demand. I would say probably architecture first, then engineering, project management, and quantity surveying.”

4.25 Thequalitativephasealsoindicatedthatanumberofemployersfelttheover-supplyofgraduateswasmostlyduetoHigherEducationbeingdrivenbythenumberofapplicationstoparticulardisciplines,ratherthanbytheneedforgraduatesofsuchsubjects.

“It’s a business, it’s bums on seats gets them money. If they can take on 60 graduates they will, I don’t think the end concern is whether there are jobs available. They would still take 60 even if they knew there were only 20 jobs available, because they get the money... They could drop the numbers and make it a lot harder. They could take on fewer but specialise more on them, so you would be getting quality rather than quantity at the end.”

b) Impact on training

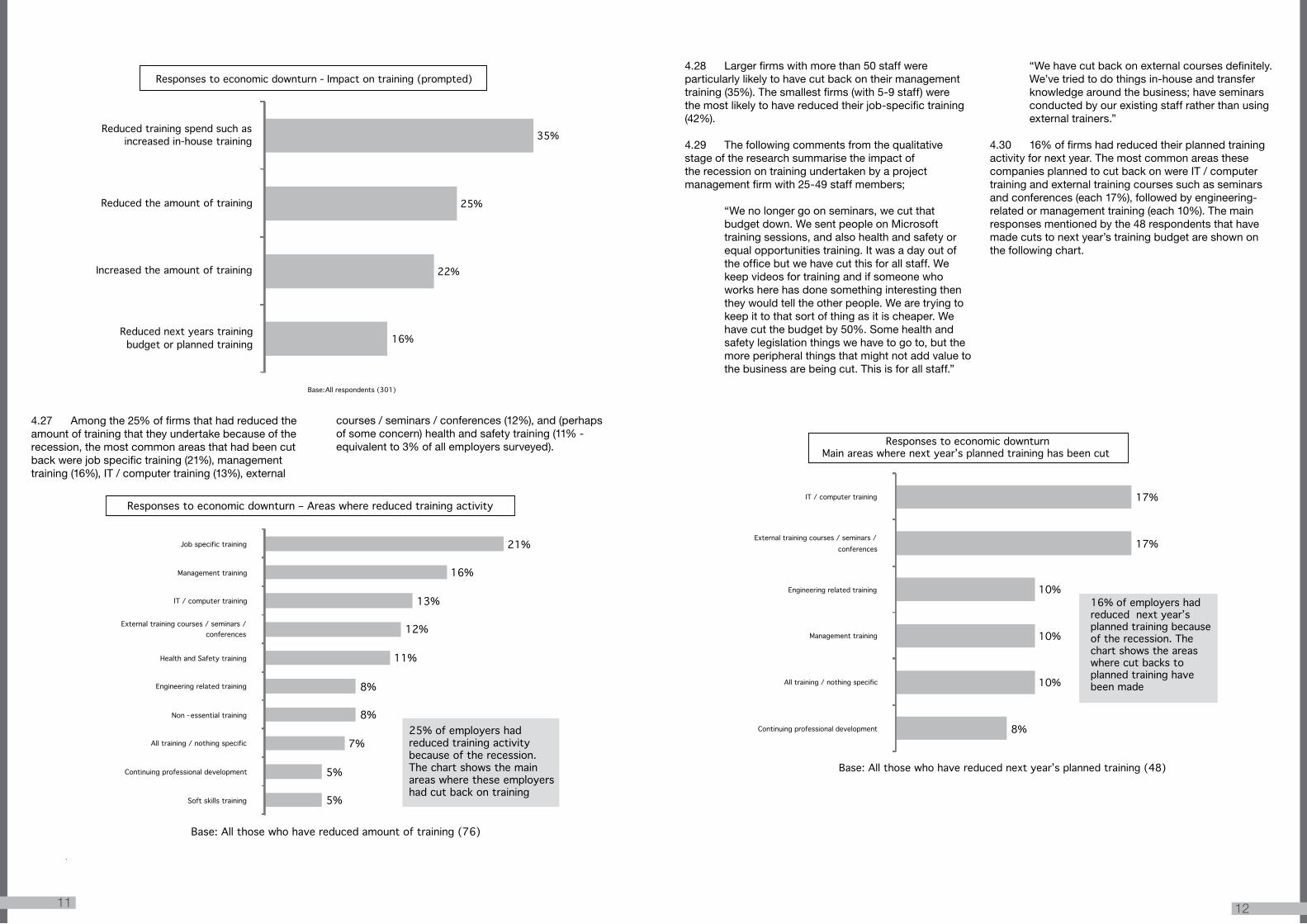

4.26 Theeconomicdownturnhashadanimpactonthetrainingundertakenbyprofessionalservicesfirms,thoughthisisperhapslessseverethanmighthavebeenanticipated.While35%offirmshadreducedtheirtrainingspendforexamplebyincreasingtheamountofin-housetraining,theproportionthathadreducedtheamountoftrainingthattheyundertake(25%)wasonlyalittlehigherthantheproportionthathadincreasedtheamountoftrainingasaresponsetotherecession(22%).Similarlyitcouldbeviewedquitepositivelythat‘only’16%ofprofessionalservicesfirmshavereducednextyear’strainingbudgetorplannedtrainingactivity.

4%

4%

4%

5%

6%

6%

8%

8%

9%

14%

15%

18%

35%

Production staff

HR, legal and business professionals

Architectural technologists

Building Surveyors

I.T. staff

Civil Engineers

Quantity Surveyors

Mechanical Engineers

Project managers

Architects

Technicians

Other Engineers

Administrative staff

46% of employers hadreduced staff numbersbecause of the recession.The chart shows the mainoccupations where theseemployers had reducedstaff numbers

Base: All those who have reduced staff numbers in response to the recession (139)

Responses to the economic downturn: Occupations where employers have reduced staff numbers

10 9

4.27 Amongthe25%offirmsthathadreducedtheamountoftrainingthattheyundertakebecauseoftherecession,themostcommonareasthathadbeencutbackwerejobspecifictraining(21%),managementtraining(16%),IT/computertraining(13%),external

courses/seminars/conferences(12%),and(perhapsofsomeconcern)healthandsafetytraining(11%-equivalentto3%ofallemployerssurveyed).

4.28 Largerfirmswithmorethan50staffwereparticularlylikelytohavecutbackontheirmanagementtraining(35%).Thesmallestfirms(with5-9staff)werethemostlikelytohavereducedtheirjob-specifictraining(42%).

4.29 Thefollowingcommentsfromthequalitativestageoftheresearchsummarisetheimpactoftherecessionontrainingundertakenbyaprojectmanagementfirmwith25-49staffmembers;

“Wenolongergoonseminars,wecutthatbudgetdown.WesentpeopleonMicrosofttrainingsessions,andalsohealthandsafetyorequalopportunitiestraining.Itwasadayoutoftheofficebutwehavecutthisforallstaff.Wekeepvideosfortrainingandifsomeonewhoworksherehasdonesomethinginterestingthentheywouldtelltheotherpeople.Wearetryingtokeepittothatsortofthingasitischeaper.Wehavecutthebudgetby50%.Somehealthandsafetylegislationthingswehavetogoto,butthemoreperipheralthingsthatmightnotaddvaluetothebusinessarebeingcut.Thisisforallstaff.”

“Wehavecutbackonexternalcoursesdefinitely.We’vetriedtodothingsin-houseandtransferknowledgearoundthebusiness;haveseminarsconductedbyourexistingstaffratherthanusingexternaltrainers.”

4.30 16%offirmshadreducedtheirplannedtrainingactivityfornextyear.ThemostcommonareasthesecompaniesplannedtocutbackonwereIT/computertrainingandexternaltrainingcoursessuchasseminarsandconferences(each17%),followedbyengineering-relatedormanagementtraining(each10%).Themainresponsesmentionedbythe48respondentsthathavemadecutstonextyear’strainingbudgetareshownonthefollowingchart.

16%

22%

25%

35%

Reduced next years training budget or planned training

Increased the amount of training

Reduced the amount of training

Reduced training spend such as increased in-house training

Base: All respondents (301)

Responses to economic downturn - Impact on training (prompted)

5%

5%

7%

8%

8%

11%

12%

13%

16%

21%

Soft skills training

Continuing professional development

All training / nothing specific

Non - essential training

Engineering related training

Health and Safety training

External training courses / seminars / conferences

IT / computer training

Management training

Job specific training

Base: All those who have reduced amount of training (76)

Responses to economic downturn – Areas where reduced training activity

25% of employers hadreduced training activitybecause of the recession. The chart shows the main areas where these employers had cut back on training

8%

10%

10%

10%

17%

17%

Continuing professional development

All training / nothing specific

Management training

Engineering related training

External training courses / seminars / conferences

IT / computer training

Base: All those who have reduced next yearʼs planned training (48)

Responses to economic downturnMain areas where next yearʼs planned training has been cut

16% of employers hadreduced next yearʼsplanned training becauseof the recession. Thechart shows the areaswhere cut backs toplanned training havebeen made

12 11

c) impact on skill needs

4.31 20%offirmsfeltthattherecessionhashadanimpactontheskillsthattheyneedfromtheircurrentstafforpotentialrecruits.Thisdifferedlittlebysizeoffirm,butchangingskillneedsweremoreoftenreportedbymulti-disciplinarycompanies(35%)andprojectmanagementfirms(40%,thoughonarelativelylowbaseof15respondents).

4.32 Theskillsbecomingmoreimportanttoemployersintherecessionaremostoftenbusinessdevelopmentskills(16%),specialistjob-specificskills(16%),theabilitytomulti-skill(15%),engineering-relatedskills(13%),andup-gradingexistingskills(13%).

4.33 Theskillsofincreasingimportancedifferedsomewhatbysizeoffirm,andamongthoseidentifyingchangingskillneedsasaresultoftherecession:

•Firmswith5-9staffwereparticularlylikelytomentiontheneedforimprovedspecialistjob-specificskills(29%),

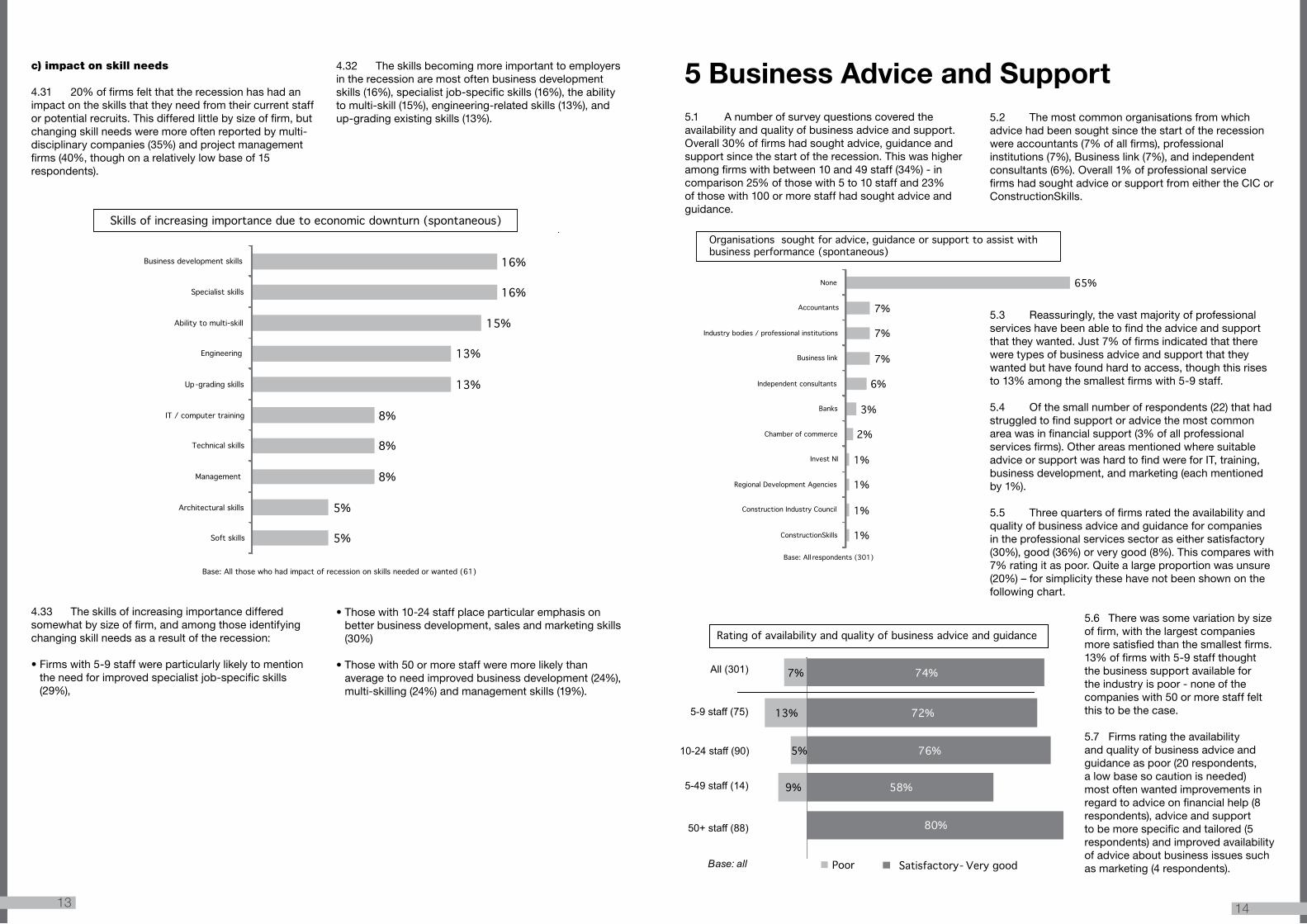

5.1 Anumberofsurveyquestionscoveredtheavailabilityandqualityofbusinessadviceandsupport.Overall30%offirmshadsoughtadvice,guidanceandsupportsincethestartoftherecession.Thiswashigheramongfirmswithbetween10and49staff(34%)-incomparison25%ofthosewith5to10staffand23%ofthosewith100ormorestaffhadsoughtadviceandguidance.

5%

5%

8%

8%

8%

13%

13%

15%

16%

16%

Soft skills

Architectural skills

Management

Technical skills

IT / computer training

Up-grading skills

Engineering

Ability to multi-skill

Specialist skills

Business development skills

Base: All those who had impact of recession on skills needed or wanted (61)

Skills of increasing importance due to economic downturn (spontaneous)

1%

1%

1%

1%

2%

3%

6%

7%

7%

7%

65%

ConstructionSkills

Construction Industry Council

Regional Development Agencies

Invest NI

Chamber of commerce

Banks

Independent consultants

Business link

Industry bodies / professional institutions

Accountants

None

Base: All respondents (301)

Organisations sought for advice, guidance or support to assist with business performance (spontaneous)

9%

5%

13%

7%

80%

58%

76%

72%

74%

Poor Satisfactory - Very good

All (301)

Base: all

Rating of availability and quality of business advice and guidance

5-9 staff (75)

10-24 staff (90)

5-49 staff (14)

50+ staff (88)

•Thosewith10-24staffplaceparticularemphasisonbetterbusinessdevelopment,salesandmarketingskills(30%)

•Thosewith50ormorestaffweremorelikelythanaveragetoneedimprovedbusinessdevelopment(24%),multi-skilling(24%)andmanagementskills(19%).

5 Business Advice and Support5.2 Themostcommonorganisationsfromwhichadvicehadbeensoughtsincethestartoftherecessionwereaccountants(7%ofallfirms),professionalinstitutions(7%),Businesslink(7%),andindependentconsultants(6%).Overall1%ofprofessionalservicefirmshadsoughtadviceorsupportfromeithertheCICorConstructionSkills.

5.3 Reassuringly,thevastmajorityofprofessionalserviceshavebeenabletofindtheadviceandsupportthattheywanted.Just7%offirmsindicatedthatthereweretypesofbusinessadviceandsupportthattheywantedbuthavefoundhardtoaccess,thoughthisrisesto13%amongthesmallestfirmswith5-9staff.

5.4 Ofthesmallnumberofrespondents(22)thathadstruggledtofindsupportoradvicethemostcommonareawasinfinancialsupport(3%ofallprofessionalservicesfirms).OtherareasmentionedwheresuitableadviceorsupportwashardtofindwereforIT,training,businessdevelopment,andmarketing(eachmentionedby1%).5.5 Threequartersoffirmsratedtheavailabilityandqualityofbusinessadviceandguidanceforcompaniesintheprofessionalservicessectoraseithersatisfactory(30%),good(36%)orverygood(8%).Thiscompareswith7%ratingitaspoor.Quitealargeproportionwasunsure(20%)–forsimplicitythesehavenotbeenshownonthefollowingchart.

5.6 Therewassomevariationbysizeoffirm,withthelargestcompaniesmoresatisfiedthanthesmallestfirms.13%offirmswith5-9staffthoughtthebusinesssupportavailablefortheindustryispoor-noneofthecompanieswith50ormorestafffeltthistobethecase.

5.7 Firmsratingtheavailabilityandqualityofbusinessadviceandguidanceaspoor(20respondents,alowbasesocautionisneeded)mostoftenwantedimprovementsinregardtoadviceonfinancialhelp(8respondents),adviceandsupporttobemorespecificandtailored(5respondents)andimprovedavailabilityofadviceaboutbusinessissuessuchasmarketing(4respondents).

14 13

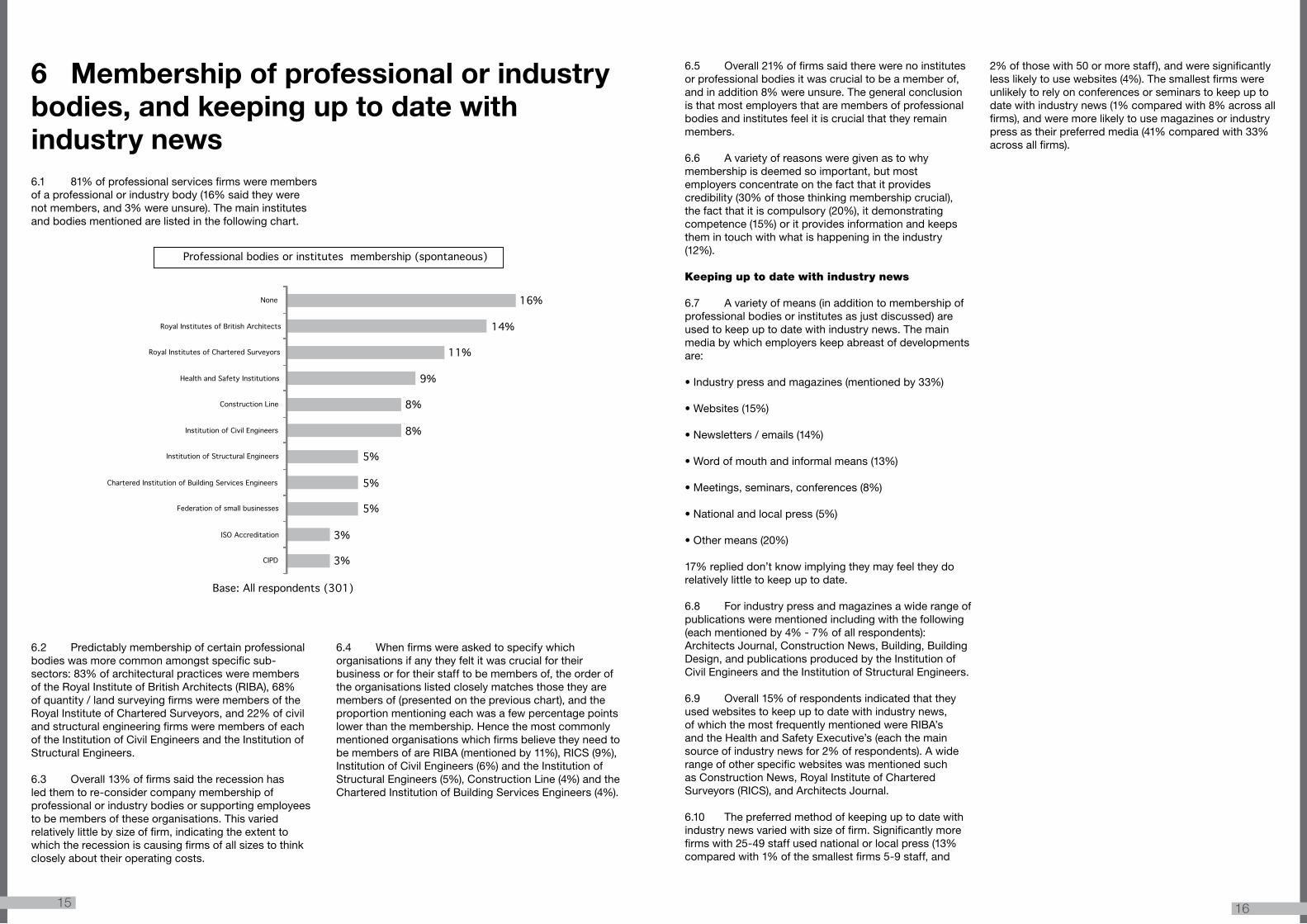

6.1 81%ofprofessionalservicesfirmsweremembersofaprofessionalorindustrybody(16%saidtheywerenotmembers,and3%wereunsure).Themaininstitutesandbodiesmentionedarelistedinthefollowingchart.

6.2 Predictablymembershipofcertainprofessionalbodieswasmorecommonamongstspecificsub-sectors:83%ofarchitecturalpracticesweremembersoftheRoyalInstituteofBritishArchitects(RIBA),68%ofquantity/landsurveyingfirmsweremembersoftheRoyalInstituteofCharteredSurveyors,and22%ofcivilandstructuralengineeringfirmsweremembersofeachoftheInstitutionofCivilEngineersandtheInstitutionofStructuralEngineers.

6.3 Overall13%offirmssaidtherecessionhasledthemtore-considercompanymembershipofprofessionalorindustrybodiesorsupportingemployeestobemembersoftheseorganisations.Thisvariedrelativelylittlebysizeoffirm,indicatingtheextenttowhichtherecessioniscausingfirmsofallsizestothinkcloselyabouttheiroperatingcosts.

6.4 Whenfirmswereaskedtospecifywhichorganisationsifanytheyfeltitwascrucialfortheirbusinessorfortheirstafftobemembersof,theorderoftheorganisationslistedcloselymatchesthosetheyaremembersof(presentedonthepreviouschart),andtheproportionmentioningeachwasafewpercentagepointslowerthanthemembership.HencethemostcommonlymentionedorganisationswhichfirmsbelievetheyneedtobemembersofareRIBA(mentionedby11%),RICS(9%),InstitutionofCivilEngineers(6%)andtheInstitutionofStructuralEngineers(5%),ConstructionLine(4%)andtheCharteredInstitutionofBuildingServicesEngineers(4%).

6.5 Overall21%offirmssaidtherewerenoinstitutesorprofessionalbodiesitwascrucialtobeamemberof,andinaddition8%wereunsure.Thegeneralconclusionisthatmostemployersthataremembersofprofessionalbodiesandinstitutesfeelitiscrucialthattheyremainmembers.

6.6 Avarietyofreasonsweregivenastowhymembershipisdeemedsoimportant,butmostemployersconcentrateonthefactthatitprovidescredibility(30%ofthosethinkingmembershipcrucial),thefactthatitiscompulsory(20%),itdemonstratingcompetence(15%)oritprovidesinformationandkeepsthemintouchwithwhatishappeningintheindustry(12%).

Keeping up to date with industry news

6.7 Avarietyofmeans(inadditiontomembershipofprofessionalbodiesorinstitutesasjustdiscussed)areusedtokeepuptodatewithindustrynews.Themainmediabywhichemployerskeepabreastofdevelopmentsare:

•Industrypressandmagazines(mentionedby33%)

•Websites(15%)

•Newsletters/emails(14%)

•Wordofmouthandinformalmeans(13%)

•Meetings,seminars,conferences(8%)

•Nationalandlocalpress(5%)

•Othermeans(20%)

17%replieddon’tknowimplyingtheymayfeeltheydorelativelylittletokeepuptodate.

6.8 Forindustrypressandmagazinesawiderangeofpublicationswerementionedincludingwiththefollowing(eachmentionedby4%-7%ofallrespondents):ArchitectsJournal,ConstructionNews,Building,BuildingDesign,andpublicationsproducedbytheInstitutionofCivilEngineersandtheInstitutionofStructuralEngineers.6.9 Overall15%ofrespondentsindicatedthattheyusedwebsitestokeepuptodatewithindustrynews,ofwhichthemostfrequentlymentionedwereRIBA’sandtheHealthandSafetyExecutive’s(eachthemainsourceofindustrynewsfor2%ofrespondents).AwiderangeofotherspecificwebsiteswasmentionedsuchasConstructionNews,RoyalInstituteofCharteredSurveyors(RICS),andArchitectsJournal.

6.10 Thepreferredmethodofkeepinguptodatewithindustrynewsvariedwithsizeoffirm.Significantlymorefirmswith25-49staffusednationalorlocalpress(13%comparedwith1%ofthesmallestfirms5-9staff,and

2%ofthosewith50ormorestaff),andweresignificantlylesslikelytousewebsites(4%).Thesmallestfirmswereunlikelytorelyonconferencesorseminarstokeepuptodatewithindustrynews(1%comparedwith8%acrossallfirms),andweremorelikelytousemagazinesorindustrypressastheirpreferredmedia(41%comparedwith33%acrossallfirms).

3%

3%

5%

5%

5%

8%

8%

9%

11%

14%

16%

CIPD

ISO Accreditation

Federation of small businesses

Chartered Institution of Building Services Engineers

Institution of Structural Engineers

Institution of Civil Engineers

Construction Line

Health and Safety Institutions

Royal Institutes of Chartered Surveyors

Royal Institutes of British Architects

None

Base: All respondents (301)

Professional bodies or institutes membership (spontaneous)

6 Membership of professional or industry bodies, and keeping up to date with industry news

16 15

7.1 Thisfinalchapterofthereportlooksathowfirmsintheprofessionalservicessectorexpecttheindustrytorecoverinthenext12months,andhowsoontheeventualupturnintheeconomymaytakeplace.

7.2 Asdiscussedearlierinthereport,54%offirmshaveseenafallintheirfeeincomeoverthelast12months.Employerswereaskedhowtheyexpectedtheirfeeincometochangeinthenext12months:32%felttheirfeeincomewouldincreasecomparedwith17%expectingthistofall.Thelargestproportionexpectedittoremainataboutthesamelevel(44%)–notsurprisinglysomedidnotfeelconfidenttoanswer(8%).Onbalancethereforethefindingsarereasonablypositivewithap-proximatelytwiceasmanyexpectinggrowthasexpectingreducedfeeincome.

7.3 Firmswith10-24staffwerethemostlikelytoex-pectanincrease(40%),whilstfirmswith25-49staffweretheleastlikelytoexpectanincreaseinfeeincome(19%)andthemostlikelytoexpectadecrease(19%).

7.4 EmployersinNorthernIrelandandWalesseemmorepessimisticthanaverage(thoughlowbasesizesshouldbenoted,17and13interviewsrespectively):inbothcountriesjustoverathirdexpectadecreaseinfeeincomeoverthenext12months.Fewprofessionalserv-icesfirmsbasedinNorthernIrelandexpectanyincreasesinfeeincome(6%).

7.5 Firmsfromdifferentsub-sectorsalsohadvaryingforecastsforthenext12monthswitharchitecturalfirmsmorelikelythanaveragetoexpectanincreaseinfeeincome(46%),andquantity/landsurveyingfirmsmorepessimisticthanaverage.

7.6 Predictablytherewasacorrelationbetweenperformanceoverthelast12monthsandexpectedperformanceforthecomingyear.Thosewhosefeeincomehadincreasedoverthelast12monthsweremorelikelythanaveragetoanticipateincreasesoverthenext12months(50%)),whilethosethathadseenfallsinfeeincomewerelessoptimisticaboutthecomingyear,thoughstillmoreexpectedincreasesintheirfeeincome(31%)thanexpectedittofall(23%).

7.7 Combiningresultsforpastandexpectedfeeincome:

•5%ofallfirmshadexperiencedincreasedfeeincomeinthelast12monthsandexpectedittoincreaseinthenext12months

•12%offirmshadexperiencedfallsinfeeincomeandexpectedthesetocontinue

•17%offirmsdescribedtheirfeeincomeasstaticinthelast12monthsandexpectedittostayataboutthesameleveloverthenext12months.

7.8 Overall25%ofprofessionalservicesfirmsfeltitwaslikelythattheywouldhavetomakeredundanciesinthenext12months,whichincludes3%thathavealreadyplannedtheredundancies.Itismoderatelyencouraging

Main skills expected to become more important in the next 2-3 years

Base: Those anticipating increased importance of some skills (104)

All (301)

% %

Specialist job-specific skills 35 12

Environment / sustainability 21 7

Management skills 13 4

IT skills 12 4

Sales / marketing / business acumen 12 4

Engineering-related 9 3

Legislation awareness 5 2

Health and safety 3 1

Other 11 4

Don’t know 2 1

7.11 Amongemployersanticipatingchangingskillneeds,environmentalandsustainabilityskillswerementionedbyafifth,andthesewereseenasparticularlyimportantforarchitectsandtechnicalstaff.Atthequalitativephaseoneemployerexplainedtheneedasfollows:

“More and more of our clients are sharing more awareness of environmental change, and we would comply with their demands. We have to be part of their supply chain so we have to comply with their specifications. We would train our men on site in environmental awareness.”

The end of the recession

7.12 40%ofemployersfeltthattheworstoftherecessionwasover(interviewstookplaceinearlyOctober2009).Firmswith25-49staff(29%),thosebasedinNorthernIreland(24%)andthoseoperatinginbuildingservicesengineering(33%)werelesslikelythanaveragetofeelthattheworstoftherecessionwasover.

7.13 Themajorityoffirmsinterviewedforthequalitativephasewereconfidentthattheywouldsurvivetherecession;

“We are fairly confident that we’ll survive the recession, because we have such a diverse client base. We were able to shelter ourselves from the worst that was happening.” Howeversomefirmsdidexpressconcern;

“I am not confident we will survive. We are funded by a board of directors at the group, and if we have not been making money since we started then they may well consider restructuring. The group has seen redundancies and as we have not made money - I am concerned they may shut us down.”

7.14 Thefollowingchartshowsresponsestothequestionofwhatemployerswouldliketoseedonetohelpthesectorcomeoutoftherecession.

36%

9%

38%

35%

12%

19%

18%

12%

17%

21%

46%

31%

6%

33%

19%

40%

29%

32%

Decreased Increased

All (301)

Base: all respondents (301)

Fee income changes expected in next 12 months

5-9 staff (75)

10-24 staff (90)

5-49 staff (48)

50-99 staff (88)

Wales (13)

Architecture (46)

Northern Ireland (17)

Quantity surveying (28)

7 The next 12 months and the end of the recession

1817

thatmorethinkitquitelikely(17%)thanverylikely(5%)suggestingthatformanyfirmsthedecisionwilldependontheirperformanceinthecomingmonths.Largercompanieswerethemostlikelytoanticipatetheneedtoreducestaffnumbers(30%ofthosewithover50staffwereexpectingtomakeredundanciesinthenext12months).

7.9 Resultssuggestthatredundanciesaremostlikelytoaffectadministrativestafffollowedbyarchitects,civilengineers,andotherengineers.

Future skills needs

7.10 35%ofprofessionalservicesfirmsfelt,independentoftherecession,thattherewerecertainskillstheyexpectedtobecomemoreimportantoverthenext2-3years.Thesearelistedonthefollowingtable.

7.15 Themostcommonresponsewasthatthebanksshouldstartlendingagain(mentionedby19%ofallfirms),whilstmorefundingandinvestmentwasmentionedby12%.Anumberofotherwaystohelpthesectorcomeoutoftherecessionfocusedaroundincreasedgovernmentsupportincluding;increasedgovernmentspendinginthepublicsector(11%),increasedgovernmentspendingonnewprojects(8%),governmentprojectsbroughtforward(7%)andincreasedgovernmentspendingoninfrastructure(6%).Clearlymanyprofessionalservicesfirmsfeelthereismorethegovernmentcoulddotohelpthesectoremergemorequicklyfromtherecession.

Annex A: QUANTITATIVE QUESTIONNAIRE

PRIVATE&CONFIDENTIAL CICSurveyTelephone

j4769

QUOTASA)TAKEREGIONFROMSAMPLE:

NorthernIreland 1 WestMidlands 7

Scotland 2 EastMidlands 8

Wales 3 SouthWest 9

NorthWest 4 East 10

NorthEast 5 SouthEast 11

Yorkshire&Humberside 6 London 12

CHECKQUOTAS(min15ineach)

B)TAKESECTORTYPEFROMSAMPLE:

Professionalservices(74.2) 1

C)TAKESIZEFROMSAMPLE:

5-9 1 CHECKQUOTAS

10-24 2

25-49 3

50+ 4

D)TAKESECTORTYPEFROMSAMPLE:

Panellist 1

Newsample 2

REASSURANCESTOBEUSEDASREQUIRED:

•Pleasebereassuredthateverythingwillbestrictlyconfidential.NothingwillbereportedbacktotheConstructionIndustryCouncil(CIC)abouthowindividualcompaniesrespondtothesurvey(weareonlyreportingbackaggregatedstatistics).

•ContactatCIC:MarkWayon07785730466

•ContactatIFFResearch:BenDavies/MarkWinterbothamon02072503035.

•ResultswillhelpCICtoensurethattrainingprovisionmeetstheneedsoftheindustry.

3%

2%

2%

2%

3%

5%

5%

6%

7%

8%

11%

12%

19%

Nothing

Change in government

Better regulation of financial market

More governement help in private sector

Less red tape

Lower taxes

Increase customer confidence

Increased governement spending on infrastructure

Bring forward government backed projects

Increased government spending on new projects

Increased government spending in public sector

More funding and investment

Banks to start lending again

Base: All respondents (301)

Ways to help the sector come out of the recession (spontaneous)

2019

S1. ASKALL Can I speak to[IFPANELLIST:INSERTCONTACTNAME]

[IFNOTPANELLIST:the most senior person here who has responsibility for human resource and personnel issues or the person responsible for training and development? INTERVIEWERPROMPT:

Yes – transferred 1 CHECK S2

Yes – correct respondent speaking 2

Definite appointment 3 MAKE DEFINITE APPOINTMENT / SOFT CALL BACK

Soft appointment 4

Nobody in office able to answer the questions 5 ASK FOR NAME & CONTACT DETAILS FOR ALTERNATIVE RESPONDENT

Refusal 6 ASK S1A

Refusal – company policy 7

Not available in deadline 8

[IF NAMED CONTACT] No-one of that name works here / Person no longer works here

9 RE-ASK S1 ABOUT SENIOR PERSON

S2) IFAPANELLIST(OTHERSGOTOS3) Good morning / afternoon. My name is XXX calling from IFF Research in London. You may remem-

ber that in the past you helped us with an on-going study that we are conducting for [ALLEXCEPTNORTHERNIRELAND:ConstructionSkills/IFSAMPLE=NORTHERNIRELAND:CITB Northern Ireland / ConstructionSkills] looking at attitudes and views of employers like yourself on training, learning and qualifications. You mentioned then that you would be willing to take part in further research. We are now conducting research for ConstructionSkills and the Construction Industry Council (CIC) among Professional Services firms. It will just take 20-25 minutes. Is now a good time?

Yes 1 GOTOQ1

No-Definiteappointment 2 MAKEDEFINITEAPPOINTMENT/SOFTCALLBACKNo-Softappointment 3

Refusal–notinterested 4 THANKANDCLOSE

S3) IFNON-PANELLIST(PANELLISTSGOTOQ1) We are conducting a study for the Construction Industry Council (CIC) looking at the impact of the

recession, and skills and training. Results will help CIC to ensure that education and training provision meets the needs of the industry. It will just take 20-25 minutes.

Can I just check are you the best person or one of the most appropriate people in the company to talk to about issues such as training and qualifications?

Yes 1 ASKQ1

No 2 ASKFORNAMEANDCONTACTDETAILSOFTHISPERSON,THENRE-INTRODUCE

Don’tknow/dependsonthequestions 3 ASKQ1

SECTION A: ABOUT THE COMPANYASKALL1) First, how many people does your company employ across the UK? PROBEFORBESTESTIMATE

WRITEINEXACTNUMBERANDCODERANGE

1(respondentonly) 1 THANKANDCLOSE

2-4 2

5-9 3 CONTINUE

10-24 4

25-49 5

50-99 6

100+ 7

1a) How many did you employ across the UK 12 months ago?PROBEFORBESTESTIMATE

WRITEINEXACTNUMBERANDCODERANGE

1(respondentonly) 1

2-4 2

5-9 3

10-24 4

25-49 5

50-99 6

100+ 7

1b) Which one of the following best describes the primary activity undertaken by your business? READOUT.SINGLECODEONLY

Architecture 1 CONTINUE

Town/urbanplanning 2

Landscapedesign 3

Quantitysurveying 4

CivilandStructuralengineering 5

BuildingServicesEngineering 6

Engineering-relatedconsulting 7

ProjectManagement 8

Multi-disciplinary 9

Otherprofessionalservicesrelatingtotheconstructionindustry(SPECIFY)

0

Noneoftheabove x THANKANDCLOSE

IFMULTIDISCIPLINARY(CODE9ATQ1b)1c) What would you describe as your lead discipline?

22 21

IFMULTIDISCIPLINARY(CODE9ATQ1b)1d) And what are your secondary disciplines?

ASKALL2) Which of the following sectors do you work in?....READOUT.

IFMORETHANONEATq2)2a) Which of these is the main sector that you work in?(SHOWANSWERSFROMQ1e)

Q2 Q2A

Privatehousing 1 1

Publichousing 2 2

Infrastructure(i.e.roads,railways,bridges,harbours)

3 3

Commercial(i.e.retail,entertainment,offices) 4 4

Industrial(i.e.factories,warehouses) 5 5

Publicnon-residential(i.e.health,education) 6 6

Other(SPECIFY) 7 7

3) Do you work mainly for …READOUT(MULTICODEALLOWED)

Privateclients 1

Asasub-contractorforconstructionorconsultancyfirms 2

Commercialclients 3

Governmentorpublicsectorclients 4

Orforothertypesofclient(PLEASESPECIFY) 5

4) Is this…READOUT(CODEFIRSTMENTIONED)

theonlylocationofyourorganisation 1 ASK4b

theheadquartersofyourcompanyintheUK 2 ASK4a

abranch 3

[DONOTREADOUT]Other(PLEASESPECIFY) 4

IFMORETHANONEOFFICE/BRANCH4a) How many offices in total do you have across the UK?

EXACTNUMBER _____

IFDON’TKNOWPROMPTWITHRANGE

2-4 1

5-7 2

8-10 3

Morethan10 4

Don’tknow X

IFMORETHANONEOFFICE/BRANCH4b) In which regions of the UK do you operate in? PROMPTIFNECESSARY

SouthEast 1

London 2

East 3

SouthWest 4

EastMidlands 5

WestMidlands 6

YorkshireandHumberside 7

NorthEast 8

NorthWest 9

Scotland 10

Wales 11

NorthernIreland 12

AllofGreatBritain 13

AlloftheUK 14

Other(SPECIFY) 0

Don’tknow X

ASKALL5) What do you feel are the key business challenges facing your company at the moment?

PROBE: What are the other main challenges you face? (MULTICODEFINE)DONOTREADOUT

Needtoincreasesales/getmoreworkorbusinessin 1

Needtoincreaseprofitability 2

Dealingwiththedownturn/recessiongenerally 3

Havemoreworkthancanhandle 4

Findingsuitablyskilled/qualifiedstaff 5

Gettingfinancetoexpand 6

Cashflowdifficulties 7

Other(WRITEIN) 0

None/noparticularchallenges X

24 23

SECTION B: ECONOMIC DOWNTURN6) What has been the main impact, if any, of the economic downturn on your business?

(MULTICODEFINE)DONOTREADOUT

Lesswork/lowdemand 1

Increasedcompetition 3

Projectsbeingdelayed/cancelled 4

Cashflowdifficulties 5

Reducedtrainingactivity(includingtakinglessworkplacements) 6

Other(WRITEIN) 0

None/noparticularimpact X

7) What steps, if any, have you taken to specifically meet the challenges presented by the economic downturn? (MULTICODEFINE)DONOTREADOUT

Redundancies 1

Hadtocutcosts/overheads(i.e.closeoffices) 2

Cutbackonplannedrecruitmentofotherstaff 3

Reducedworkinghours,orencouragedstafftotakeunpaidleaveortoworkpart-time

4

Reducedtraining 5

Soughtworkinalternative/differentsectors 6

Other(WRITEIN) 0

None/noparticularstepstaken X

8) In the last 12 months has your fee income increased, decreased or stayed at about the same level as compared with the 12 months before that?

Increased 1

Decreased 2

Stayedataboutthesamelevel 3

Refused/don’tknow X

IFINCREASED/DECREASEDATQ88a) By approximately how much has fee income (IF Q8=1: increased / If Q8=2 fallen) in the last 12 months

compared with the 12 months before that?

_____________%

Don’tknow X

ASKALL9) And compared with the last 12 months, do you expect your fee income over the next 12 months to

increase significantly, increase, stay at about the same level, decrease or decrease significantly?

Increasesignificantly 1

Increase 2

Stayataboutthesamelevel 3

Decrease 4

Decreasesignificantly 5

Refused/don’tknow X

ASKALL10) As a response to the downturn have you...?READOUT.CODEALLMENTIONED

Yes No Don’tknow

a)Madestaffredundant 1 2 X

b)Reducedworkinghours,orencouragedstafftotakeunpaidleaveortoworkparttime

1 2 X

c)Increasedyouruseoffreelanceoragencystafforconsultants 1 2 X

IF“NO”ATC:d)Cutbackonyouruseoffreelanceoragencystafforconsultants

1 2 X

ASKALLe)Recruiteddifferentspecialismstoenablethefirmtoworkinsectorsnewto

thefirm

1 2 X

ASKALLf)Cutbackonplannedrecruitmentofgraduatesornewlyqualifiedstaff

1 2 X

IF“NO”ATFg):Increasedplannedrecruitmentofgraduatesornewlyqualifiedstaff

1 2 X

ASKALLh)Cutbackonplannedrecruitmentofsupportstaff

1 2 X

i)Spendmoretimebiddingforwork/writingproposals 1 2 X

IFMADESTAFFREDUNDANT(Q10A/1),OTHERSGOTOQ1211) You mentioned that you’ve made staff redundant as a result of the downturn.

In which occupations have you laid staff off? DONOTREADOUT.CODEALLMENTIONED

Architects 1

ArchitecturalTechnologists 2

BuildingServiceEngineers 3

CivilEngineers 4

Mechanicalengineers 5

OtherEngineers 6

TownPlanners 7

Technicians 8

BuildingSurveyors 9

QuantitySurveyors 10

LandscapeDesigners 11

ProjectManagers 12

Marketing 13

HR,legalandbusinessprofessionals 14

Administrativestaff 15

Others(SPECIFY) 16

2625

ASKALL12) How likely do you think it is that you will need to reduce the number of staff you employ in the next

12 months. Is it...READOUT

Definite–alreadyhavethisplanned 1 ASKNEXTQUESTION

Verylikely 2

Quitelikely 3 ASKNEXTASKALL

Notverylikely 4

Notatalllikely 5

(DONOTREADOUT)Don’tknow/depends 6

IFDEFINITE/VERYLIKELY13) In which occupations do you anticipate having to make staff redundant?

DONOTREADOUT.CODEALLMENTIONED

Architects 1

ArchitecturalTechnologists 2

BuildingServiceEngineers 3

CivilEngineers 4

Mechanicalengineers 5

OtherEngineers 6

TownPlanners 7

Technicians 8

BuildingSurveyors 9

QuantitySurveyors 10

LandscapeDesigners 11

ProjectManagers 12

Marketing 13

HR,legalandbusinessprofessionals 14

Administrativestaff 15

Others(SPECIFY) 16

IFRECRUITEDSTAFF(Q10E/1)13a) You mentioned that you’ve recruited different specialisms to enable the firm to work in sectors new to

the firm. In which occupations have you recruited staff? DONOTREADOUT.CODEALLMENTIONED

Architects 1

ArchitecturalTechnologists 2

BuildingServiceEngineers 3

CivilEngineers 4

Mechanicalengineers 5

OtherEngineers 6

TownPlanners 7

Technicians 8

BuildingSurveyors 9

QuantitySurveyors 10

LandscapeDesigners 11

ProjectManagers 12

Marketing 13

HR,legalandbusinessprofessionals 14

Administrativestaff 15

Others(SPECIFY) 16

IFREDUCEDPLANNEDRECRUITMENTOFGRADUATES(Q10f=1)14) You say you cut back on planned recruitment of graduates or newly qualified staff as a result of the

recession. How many would you have normally taken on?

Number ____

Don’tknow X

14a) And how many did you take on this year?

Number ____

Don’tknow X

ASKALL15) How many recent graduates or newly qualified staff does your company currently employ

across the UK?

Number ____

Don’tknow X

16) And how many recent graduates or newly qualified staff did you employ 12 months ago?

Number ____

Don’tknow X

17) Do you think that across the industry as a whole the supply of graduates currently exceeds demand?

Yes 1 ASKQ17a

No 2 ASKQ18

Don’tknow X

IFYES17a) In which disciplines or occupations do you feel this is the case? PROBE: Any others?

ASKALL18) Thinking about the impact of the recession on training, as a response to the downturn have you...?

READOUT.CODEALLMENTIONED

Yes No DK

a)Reducedtheamountoftrainingthatyouundertake 1 2 3

b)Madeotherchangestotrainingtotrytoreducespendsuchasbringingmoretrainingin-house

1 2 3

IFQ18a)=2c)Increasedtheamountoftrainingyouundertake

1 2 3

d)Reducednextyear’strainingbudgetornextyear’splannedtrainingactivity

1 2 3

28 27

IFQ18a=119) You say you have reduced the amount of training because of the recession. What training have you cut

back on? PROBE: What else?

IFQ18d=120) You say you have reduced next year’s planned training activity. What particular training will you be

cutting back on?

ASKALL21) Has the recession had an impact on the skills you need or want from existing staff or from

potential recruits?

Yes 1 ASKNEXTQUESTION

No 2 ASKNEXTASKALL

Don’tknow X

IFYES22) What skills are of increasing importance to you?

ASKALL23) And independent of the recession, are there any skills you expect to become more important over the

next 2-3 years?

Yes 1 ASKNEXTQUESTION

No 2 ASKNEXTASKALL

Don’tknow X

IFYES24) What skills do you expect to become of more importance in the next 2-3 years?

ENTEREACHSEPARATELY

FOREACHANSWERATPREVIOUSQUESTION25) Which are the main occupations you expect the increase need for<ANSWER>to affect?

Skill Occupation

i)

ii)

iii)

ASKALL26) Since the start of the recession has your company sought advice, guidance or support from external

organisations to assist with business performance?

Yes 1 ASKNEXTQUESTION

No 2 ASKNEXTASKALL

Don’tknow X

IFYES27) Which types of organisation have you sought this advice or guidance from? PROMPTIFNECESSARY

Accountants 1

Banks 2

Benevolentsociety 3

ChambersofCommerce 4

CIC(ConstructionIndustryCouncil) 5

ConstructionSkills 6

Industrybodies/professionalinstituitions 7

Other(SPECIFY) 0

Don’tknow X

28) Are there types of business advice or support that you have wanted but found hard to find or access?

Yes 1 ASKNEXTQUESTION

No 2 ASKNEXTASKALL

Don’tknow X

IFYES29) Which types of advice or support have you found hard to access? PROMPTIFNECESSARY

ASKALL30) Generally speaking, how would you rate the availability and quality of business advice and guidance for

companies in the professional services sector...READOUT?

Verygood 1 ASKNEXTASKALL

Good 2

Ok 3

Poor 4 ASKNEXTQUESTION

Verypoor 5

Don’tknow 6 ASKNEXTASKALL

IFPOOR31) On what sort of issues would you like to see support and guidance improved?

ASKALL32) Which professional bodies or institutes is your company a member of?

SPECIFY

None………V

30 29

33) Has the recession led you to re-consider company membership of professional or industry bodies, or supporting employees to be members of these organisations?

Yes 1

No 2

Don’tknow X

34) Which organisations, if any, do you feel it is crucial for your business or your staff to be members of?

SPECIFY: 1 ASKNEXTQUESTION

None 0 ASKNEXTASKALL

Don’tknow X

IFANYMENTIONED35) Why is this or are these organisations so important to your business?

ASKALL36) What are the main ways that you keep up to date with industry news? DONOTREADOUT

Industrypress/magazines(SPECIFYWHICH) 1

Wordofmouth/informalnetworks 2

Websites(SPECIFYWHICH) 3

National/localpress 4

Other(SPECIFY) 5

Don’tknow 6

37) Do you feel the worst of the recession is over?

Yes 1

No 2

Don’tknow X

38) What, if anything, would you like to see done to help the sector come out of the recession? What else?

Don’tknow..................X

39) Finally, would you be willing to be contacted for research studies in the future by ConstructionSkills or CIC, or research agencies working on their behalf.

Yes 1

No 2

That’s it, thank you for your time today. I just need to record your name, job title and telephone number.

ENTERNAME

ENTERJOBTITLE

THANK RESPONDENT AND CLOSE INTERVIEW

IdeclarethatthissurveyhasbeencarriedoutunderIFFinstructionsandwithintherulesoftheMRSCodeofConduct.

Interviewersignature: Date:

Finishtime: InterviewLength Mins

32 31

CIC26StoreStreetLondonWC1E7BT

T02073997400F02073997425www.cic.org.ukwww.cpdevents.org.uk

ConstructionSkillsistheSectorSkillsCouncilforConstruction.ItisapartnershipbetweentheConstructionIndustryCouncil(CIC),CITB-ConstructionSkillsandCITBNorthernIreland.