the impact of microfinance on small and medium …

TRANSCRIPT

THE IMPACT OF MICROFINANCE ON SMALL AND MEDIUMENTERPRISES GROWTH IN LIRA DISTRICT.

CASE STUDY OF ADEKOKWOK TRADERS ENTERPRISES FOR LIRAMUNICIPALITY.

BY

AMONG JENIFER.

1153-05014-01099

A RESEACH PROPOSAL SUBMITTED TO THE COLLEGE OF ECONOMICSAND MANAGEMENT IN PARTIAL FULFILLMENT OF THE

REQUIREMENTS FOR THE AWARD OF A BACHELOR’S DEGREE INBUSINESS ADMINISTRATION IN KAMPALA INTERNATIONAL

UNIVERSITY.

2019

1

DECLARATIONI, AMONG JENIFER, do hereby declare that this Dissertation is my own work and has not beensubmitted for a Degree award in any other University or Higher Learning Institution.

Signature....~ ‘

Date....a.&t

DEDICATIONThis research is dedicated to my family, especially my lovely father Mr. Ecal Samuel, mybeloved mother Mrs. Agnes Ecal, my step mother Mrs. Rose Ecal and my brothers and sisters.

I as well dedicate this to my lecturer, Ms. MudondoErinah for her special contribution to myultimate knowledge of this study.

APPROVALI, the undersigned, certif~’ that I have read and hereby recommend for acceptance by KampalaInternational University, a dissertation entitled; The Impact of Microfinance on Small andMedium Enterprises (SME5) growth in Lira District, in partial fulfillment of the requirements foraward~business administration at Kampala International University.

Ms. MudondoErinah.

(Supervisor

Date. ~..... ~.

ACKNOWLEDGMENTSFirst, I am indebted to the all-powerful GOD for all the blessings he showered on me and forbeing with me throughout the study.

I am deeply obliged to my Supervisor, Ms. MudondoErinah for her exemplary guidance andsupport without whose help; this project would not have been a success.

I take this opportunity to express my deep gratitude to the lasting memory of my loving family,and friends who are a constant source of motivation and for their never ending support andencouragement during this project.

Finally, it has been an exciting and instructive study period in Kampala International Universityand I feel privileged to have had the opportunity to carry out this study as a demonstration ofknowledge gained during the period studying for my bachelor’s degree. With theseacknowledgments, it would be impossible not to remember those who in one way or another,directly or indirectly, have played a role in the realization of this research project. Let me,therefore, thank them all equally.

iv

ABSTRACTThis study examines the impact of the Microfinance on growth of the Small and MediumEntrepreneurs (SMEs) in Lira district. The specific objectives of this study are as follows; todetermine at what extent accessibility of microfinance lead to increase the volume of gross salesof participants and to understand other factors enhancing SME’s growth. The study will usecross-sectional research design in which 150 SMEs will be used as a sample size: 75 clients fromBRAC and 75 clients from centenary bank. Data will be collected using questionnaires, directobservations and documentary reviews. Descriptive statistical procedures including descriptiveand frequency distributions from the database template will be used and then, running LinearRegression Model. The result findings revealed that most of the respondents who were engagedin micro enterprises were female. Indeed, they were also in the age of briskest and economicalactive individuals of mean age 31.2 years, and the majority of them had primary level ofeducation. However, the statistical findings also revealed that the following null hypothesis arestatistically significant under t-test at 0.05 level of significance; There is statistical significant onmicrofinance access on SMEs growth. While null hypothesis stated that there is statisticalsignificant relationship between SMEs growth and start-up capital and the other which stated thatthere is no statistical significant that experience on SME activities improves SME’s growthwhich reveals that it is not statistically significant at t-statistic 0.05 level of significance.

V

TABLE OF CONTENTSDECLARATION .1

DEDICATION ii

APPROVAL iii

ACKNOWLEDGMENTS iv

ABSTRACT v

LIST OF ABBREVIATIONS AND ACRONYMS vi

LIST OF TABLES x

LIST OF FIGURES xi

CHAPTER ONE 1

1.0 INTRODUCTION 1

1.1.Overview 1

1.2. Background of the Problem 1

1.2.1. An Overview of SMEs in Uganda 1

1.3. Problem Statement 2

1.4. Research Objectives 3

1.4.1. Overall Objective 3

1.4.2. Specific Objectives 3

1.5. Research Hypothesis 4

1.6. Significance of the Study 4

1.7 Limitations of the study 4

1.8. Organization of the Study 4

CHAPTER TWO 6

2.0 LITERATURE REVIEW 6

2.1.Overview 6

2.2. Theoretical Literature Review 6

2.2.1. Conceptual Definitions 6

2.2.1.1. Micro-finance 6

2.2.1.2. Small and Medium Enterprises 6

2.2.1.3 Contribution of SMEs to the Economy 7

2.2.1.4 Development in the Theory of SME 7

2.2.1.5.1 Passive Learning Model 7

2.2.1.5.2 Stochastic and Deterministic Approaches 7

2.3. Empirical Literature Review 8

2.3.1. Role of Microfinance on SMEs Growth 9

VII

2.3.2. Linkage between Microfinance and SME .11

2.5 Summary of Literature Review 12

CHAPTER THREE 13

RESEARCH METHODOLOGY 13

3.0 Introduction 13

3.1 Research Design 13

3.3. Population 13

3.4 Sample Design 13

3.5 Validity and Reliability 13

3.5.1 Validity 13

3.5.2 Reliability 14

3.6. Sampling Techniques 14

3.6.1. Cluster Sampling Technique 14

3.6.2. Data Collection Tools 14

3.6.2.1. Questionnaire 14

3.6.2.2. Interview 14

3.6.2.3. Documentary Review 15

3.7. Data Processing, Analysis and Presentation 15

3.8 Empirical Framework of SME Growth 15

3.8.1 Dependent Variable 15

3.8.2 Independent Variables 16

3.9. Empirical Model 17

CHAPTER FOUR 18

4.0 DATA ANALYSIS AND DISCUSSION 18

4.1 Overview 18

4.2. Socio-economic and Demographic Characteristics of the Respondents 18

4.2.1 Gender of Respondents 18

4.2.2 Mean Age of Respondents 19

4.2.3 Education Level of Respondents 19

4.2.4 Source of Initial Capital of the SME 20

4.2.5 Client’s Start-up Capital 21

4.2.6 Amount of Loan Accessed 21

4.2.7 Number of Years in Business 22

4.2.8 The Business Type Operated by Respondents 22

4.3 Model Estimation 23

VIII

4.4 Multiple Regression Analysis Results 24

4.4.1 To Determine at What Extent Accessibility of Microfinance Lead to Increase the Volume ofGross Sales of Pa~icipant 25

4.4.2 To Examine Other Factors Enhancing SME’s Growth 26

4.5 Summary of Chapter Four 28

CHAPTER FIVE 29

5,0 CONCLUSIONS AND RECOMMENDATIONS 29

5.1 Overview 29

5.2 Conclusion 29

5.3. Policy Implications 29

5.4. Area for Fu~her Studies 30

REFERENCES 31

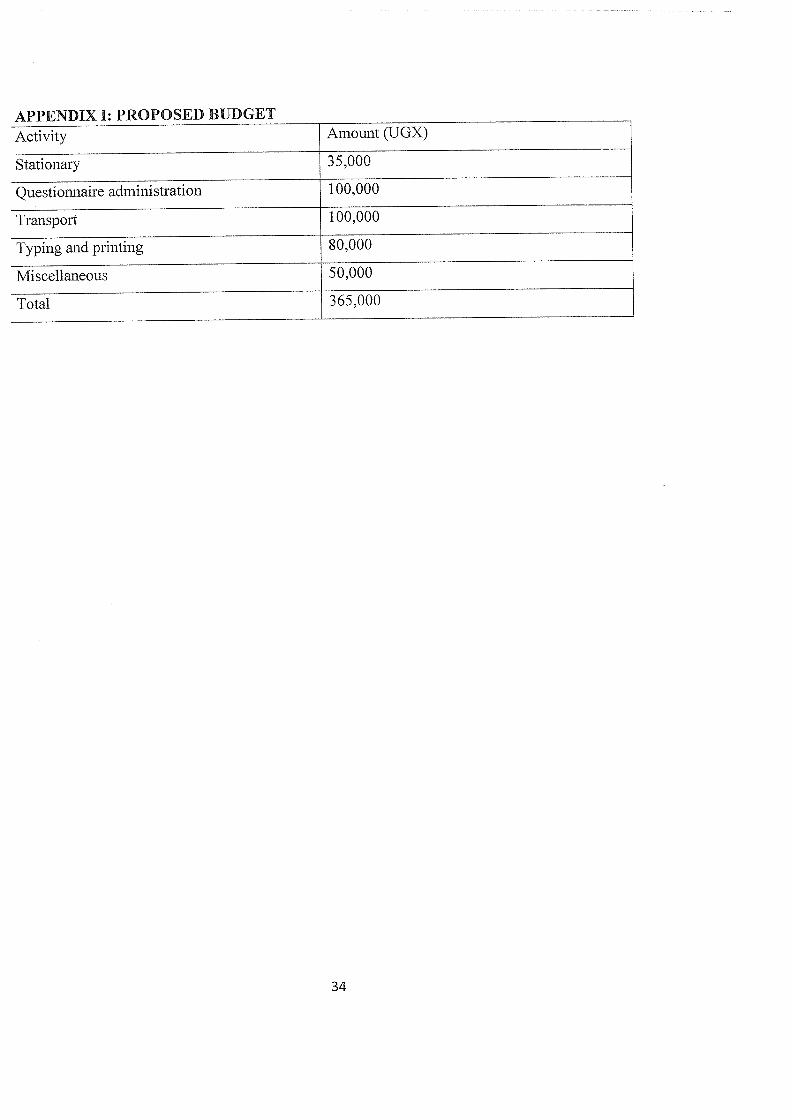

APPENDIX I: PROPOSED BUDGET 34

APPENDIX II 35

QUESTIONNAIRE

SECTION A: BACKGROUND 35

SECTION B: GROWTH

ix

LIST OF TABLESTable 4.1: Number of Respondents Covered 18Table 4.2: Mean Age of Respondents 19Table 4.3. Distribution of source of cap 20Table 4.4: Mean Start — up Capital of Respondents in Uganda 21Table 4.5: Mean Year of Respondent in SME 22Table 4.6: Correlation Matrix for Model Estimation 24Table 4.7: Variables of the Research Model 25

x

LIST OF FIGURESFigure 4.1: Sex of Respondents 19Figure 4.2: Respondent’s Education Level 20Figure 4.3: Distribution for Source Capital 21Figure 4.4: Amount of Loan Accessed by Respondents 22Figure 4.5: Distribution for Business Operated by Respondents 23

xi

CHAPTER ONE1.0 INTRODUCTION1.1. OverviewThis chapter gives attention to the background information to the problem, states the statement ofthe problem, It also stipulates research objectives and research questions. Finally, it provides thesignificance of the study. This chapter concentrates on the introduction which is categorized intothe background information to the problem, statement of the problem, research objectives, andresearch questions. In the same vein, the chapter contains significance of the study.

1.2. Background of the ProblemSmall and Medium Entei~rises (SMEs) all over in the world are known to play a major role insocial and economic development. This is apparently the case in Uganda where SMEs contributesignificantly to employment creation, income generation and stimulation of economic gro~h inboth urban and rural areas. The SMEs nomenclature issued to mean small and medium-sizedenterprises (ILO, 1998).

SMEs cover non-farm economic mainly manufactu~ing, mining, commerce and activitiesservices. There is no universally accepted definition of SME. Different countries use variousmeasures of size depending on their level of development. The commonly used yardsticks aretotal number of employees, total investment and sales turnover.

1.2.1. An Overview of SMEs in UgandaIt is estimated that SMEs in Uganda constitute 90 percent of the private sector, with 80 percentbeing located in urban areas and, are largely involved in trade, agro-processing and smallmanufacturing (Hatega, 2007), SMEs contribute approximately 75 percent of the gross domesticproduct (GDP) and employ approximately 2.5 million people, signifying their importance in theeconomic development of Uganda. At the same time, SMEs have operational and structuralchallenges. According to Hatega (2007), obstacles that affect SMEs’ ability to compete favorablyinclude limited information on financing products and an inadequate and expensive supply ofpower and telecommunications Ugandan SMEs lack the information, experience, and networksneeded to compete in a world of economic giants (Kigozi, 2006). An important part of thesoltition would be to provide well-researched market information, opportunities, and changes inthe business sector using appropriate information systems and services,

According UBOS (2010) during the Microfinance Census 2010, the total number of functionalSACCQ5 in Uganda is 2,063. Of these, Government has since 2008 enabled establisJ~ent of1085 SACCOs in the same number of sub counties under the policy of one SACCO per Subcounty. Before the recent increment in the number of districts from 80 to 112, the programsargeted 1085 sub counties. Of these, the program is supporting 735 SACCQ5 and Cooperative;rdups with capacity building grants. This represents 64 percent of the sub counties covered. The735 SACCOs under the gover~ent support have mobilized total membership of 841,312

‘eople, with over 28 billion Uganda Shillings in Savings, Loan Portfolio of 44.4 billion Ugandahillings and share capital of 16.3 billion Uganda shillings.

1

Microfinance Institutions in Uganda consist of moneylenders, micro-finance agencies, Non-Government Organizations (NGO5), rural farmers’ schemes and savings societies that providesavings and/or credit facilities to micro and small-scale business people who have experienceddifficulties in obtaining such services from the formal financial institutions. Their range ofactivities include; deposit taking, savings schemes, small-scale enterprises, agriculture, realestate, group lending, retail financial services, giving advice on financial matters and training inbusiness management. For developing countries, small-scale enterprises would generally meanenterprises with less than 50 workers and medium size enterprises would usually mean those thathave 50-99 workers. In Uganda, a small-scale enterprise is an enterprise or a firm employing atleast 5 but with a maximum of 50 employees, with the value of assets, excluding land, buildingand working capital of less than Uganda Shillings 50 million (US$ 30,000), and the annualincome turnover of between Uganda Shillings 10-50 million (US$6,000-30,000). A Mediumsized enterprise is considered a firm, which employs between 50-100 workers.

Unfortunately for Uganda, the financial system is small and with minimal linkage to the realeconomy. Uganda’s saving/GDP ratio is about 12 percent including both private and publicsector savings compared to the continental average of 17.7 percent. The ratio of money supply toGDP is only 12 percent. There is only one bank branch per 180,000 people in Uganda, comparedto an average of 7,000 per bank branch in the Common Market for East and Southern Africa(COMESA) countries. Moreover, bank branches are concentrated in the urban centers. Out of123 branches, 64 are found in the 4 largest urban areas.

The majority of the MFIs in Uganda provide two main categories of financial products; creditand savings. These services are categorized further by terms and size of loans and Type ofdeposits. The survey established an estimated loan portfolio of Uganda Shillings 97 billion (orUS$ 53.3 million) with an average loan size of Uganda Shillings 283, 266 (or US$ 161). Withregard to the volume of savings, the survey established the existence of 909,272 active savers inMFIs countrywide with a total savings volume of Uganda Shillings 107 billion (or US$ 61million). Therefore, the impact study on SME growth as result of microfinance service deliverywas geared towards establishing whether the microfinance service delivery bridges the SMEsgrowth gap in Uganda

1.3. Problem StatementMicrofinance Institutions (MFIs) are set up to provide funding for the enterprising poor. Throughcycles of loans and repayments it is expected that the SMEs are increasingly empowered and togrow. According to Mosley (2001), MEl are said to be a cheaper way of source of finance toSMEs. Despite of MEl service been cheaper way of source of finance to SMEs, very little isknown on the actual cost for microfinance clients to access these services, except interest rates.The interest rate is not the only cost of credit incurred by SMEs, there are also other costs relatedto the process of obtaining information about the services and the whole process of applying forthe loan, cost of getting transportation to make loan payments, time spent obtaining loan andtracking the debt all these are referred as transaction costs.

This study therefore seeks to investigate the impact of microfinance service on the growth ofSMEs in Lira and to investigate the benefit received from microfinance loans if they outweigh

2

the cost incurred by SME’s when servicing the loan liability, and the contribution of MFI in Liraon improvement of household welfare of SME’s.

Also there is no study that have been conducted in Lira which look on the cost and benefit ofMFI loans to SMEs and weather the MFI loan have helped the SMEs to grow despite of the truecost incurred on the process, as a result industry never know if MFI loans have truly helpedSMEs to grow.

Although people have received micro-loan, information documented in Robert (2009) indicatesthat most of SMEs whose secured loans have not yet managed to improve their enterprise’sstatus. More specifically, the impact of micro-financing on SMEs growth through the effortsmade by the several microfinance institutions for residents of Lira Municipality is stillundetermined. Along with this, there is no statistical information attesting the extent to whichmicro-loan has been helpful to beneficiaries (Neeta and Diwan, 2010).

According to Sebstad et al, (1995) there is different range of indicators of growth of SMEs. Thisstudy will use volume of gross sales, income of the SMEs, and size of business production,business profit, and number of employee in the business and revenue as indicator of growth forthe enterprises.

1.4. Research Objectives1.4.1. Overall ObjectiveThe overall objective of this study is to analyze the contribution of microfinance on the SMEgrowth in Lira district.

1.4.2. Specific ObjectivesTo achieve the overall objective, the study will pursue the following specific objectives:

i. To determine at what extent accessibility of microfinance lead to increase the volume of grosssales of a participant.

ii. To examine other factors enhancing SME growth.

1.4.3 Research questions.

The study attempts to answer the following research questions.

i. To what extent does micro financing enhance the survival of SMEs in Lira?

ii. To what extent is the growth of small businesses influenced by the financing capacity ofmicrofinance banks?

iii. How does the injection of microfinance funds into small business operations affect theproductivity of SMEs in Lira?

3

1.5. Research HypothesisIn order to meet the above objectives and get answers to the subject matter under investigation,this study will base on the following research hypothesis:

i . HO: There is no statistical significant relationship between microfinance access and SMEsgrowth.

ii. HO: There is no statistical significant relationship between SMEs growth and start-up capital.

iii. HO: There is no statistical significant that experience on SME activities improves SME’sgrowth.

1.6. Significance of the StudyFirst, this study is intended to shed light on the relationship between microfinance services andgrowth of SME particularly with the focus on their livelihoods for both planners and policymakers in government, agencies and NGOs. This will help them to come out with substantivepossible alternative policy interventions which might help to address problems and challengeswhich small and medium enterprises face. Second, this study will offer empirical evidence on theimpact of microfinance services on the growth of small and medium enterprises for use in shortterm and long term interventions especially in the fight against poverty. A study of this nature isequally very important because it is going to enlighten the government and the public on the roleof .MFI in the SMEs sector. Finally, the study will facilitate the researcher to be awarded of abachelor’s degree in business administration at Kampala International University

1.7 Limitations of the study.The main limitation of the study is the reliance on information supplied by micro and smallbusiness operators who normally do not want to make a full disclosure of their businesses to anunknown person for fear of being subjected to tax payment.

In the same vein, most of the small business operators lack proper recordkeeping practices anddo not adhere to standard book keeping and accounting procedures. Some of them do not havethe necessary skills needed for sound book keeping, auditing and tax assessment; neither do theyemploy qualified personnel to undertake such tasks for them. However, I will rely on scientificmethods to obtain the data and the analysis is based on superior analytical techniques, which Ibelieve allow me generalize my findings.

1.8. Organization of the StudyThis study is organized into five chapters. Chapter one provides information on the background,statement, the general and specific objectives, the research questions, and the significance of thestudy, limitation as well as delimitation and the organization of the study. Chapter twoconcentrates on issues related to micro finance institutions. The chapter continues to present thetheoretical and empirical literature review. Additionally, the chapter three presents thedescription of the study area, research design, sample size and sampling procedures, datacollection methods and tools. The chapter finally discloses data processing and analysis andconclusion. Chapter four presents an analysis and discussion of the research findings of thestudy. In this context, the chapter will analyze data with reference to the research objectives,

4

questions and hypothesis. Lastly is chapter five, this chapter describes conclusions andrecommendations of the study with reference to the designed research objectives and analysismade. The conclusions that have been made hereunder are based on the research findingsobtained from the field data.

5

CHAPTER TWO2.0 LITERATURE REVIEW2.L OverviewThis chapter presents the review of related literature that has been summarized from differentreadings on the topic under study. It forms the literature of the study in two major parts; namely:theoretical literature which focuses on: Definitions of key concepts (microfinance and SME),relationship between microfinance and SMEs growth and the empirical literature review thatfocuses on giving a review of relevant literature on the following sub-sections: Role ofmicrofinance in SME growth, Linkage between Microfinance and SME, Micro-finance Policy inUganda, Review of studies done outside of Uganda

2.2. Theoretical Literature Review2.2.1. Conceptual Definitions2.2.1.1. Micro-financeMicrofinance refers to financial services provided to low-income people, usually to help supportself-employment. Examples include: small loans, savings plans, insurance, payment transfers,and other services that are provided in small increments that low-income individuals can afford.These services help families to start and build “micro” enterprises, the very small businesses thatare important sources of employment, income, and economic vitality in developing countries, Asto REPOA (2006) Micro-finance does not only cover financial services but also non-financialassistance such as training and business advice.

According to MIFOS (2005) micro-finance is sometimes called “banking for the poor.” It is anamazingly simple, proven idea that empowers very poor people around the world to pullthemselves out of poverty. Relying on their traditional skills and entrepreneurial instincts, verypoor people, mostly women, obtain small-unsecured loans, usually less than $200, from localorganizations called micro-finance institutions (MFI5).

Micro finance can be a critical element on effective poverty reduction strategy. Improved accessand efficient provision of savings, credits and insurance facilities in particular can enable thepoor to smooth their consumption, manage risk better; built assets gradually develop microenterprises, enhance their income earning capacity and enjoy improved quality life (Rubambey,2001). The main features of a micro finance institution which differentiate it from othercommercial institutions, are such that, it is a substitute for formal credit; generally, requires nocollateral; have simple procedures and less documentation; easy and flexible repaymentschemes; financial assistance of members of group in case of emergency; most deprivedsegments of population are efficiently targeted; and, last but not least, is groups interaction.

2.2.1.2. Small and Medium EnterprisesThe SME nomenclature is used to mean Small and Medium Enterprises. It is sometimes referredto as micro, small and medium enterprises (MSME5). The SMEs cover non-farm economicactivities mainly manufacturing, mining, commerce and services (URT, 2003). According toKessy and Urio (2006), SMEs can be defined as a productive activity either to produce ordistribute goods and or services, mostly undertaken in the informal sector.

6

2.2.1.3 Contribution of SMEs to the EconomySMEs all over the world are known to play a major role in socio-economic development. URT(2003) estimates that about 1/3 of the GDP originates from SME sector; they tend to be laborintensive thus creating jobs: the International Finance Company (IFC) of the World Bankestimates that there are approximately 2.7 million enterprises in the country. A large majority ofthese (98%) are micro enterprises (employing less than 5 people), effective in the utilization oflocal resources using simple and affordable technology; and complementing large industrialrequirements through business linkages, partnerships and subcontracting relationships (Olomi,2001; URT, 2003).

2.2.1.4 Development in the Theory of SMEThe last 50 years have witnessed important developments in the conceptualization of the mainissues relating to the SME sector and subsequent theoretical work. The main theory, which goesback to the seminal work by Lewis (1955), is the labor surplus theory. It is argued that thedriving force behind SME development is excess labor supply, which cannot be absorbed in thepublic sector or large private enterprises and is forced into SMEs in spite of poor pay and lowproductivity. Arguably, the SME sector develops in response to the growth in unemployment,functioning as a place of last resort for people who are unable to find employment in the formalsector.

Various theoretical models have been developed which describe the growth of SMEs. One classof theoretical models focuses on the learning process, either active or passive, and the othermodels refer to the stochastic and deterministic approaches.

2.2.1.5.1 Passive Learning ModelIn the Passive Learning Model (PLM) (Jovanic 1982 cited in Agaje 2004), a firm enters a marketwithout knowing its own potential growth. Only afier entry does the firm start to learn about thedistribution of its own profitability based on information from realized profits. By continuallyupdating such learning, the firm decides to expand, contract, or to exit. This learning modelstates that firms and managers of firms learn about their efficiency once they are established inthe industry. Firms expand their activities when managers observe that their estimation ofmanagerial efficiency has understated actual levels of efficiency. As firm ages, the owner’sestimation of efficiency becomes more accurate, decreasing the probability that the output willwidely differ from one year to another. The implication of this theoretical model is that smallerand younger firms should have higher and more viable growth rates (Stranova, 2001,Cunningham and Maloney 2001 and Goedhuys, 2002).

2.2.1.5.2 Stochastic and Deterministic ApproachesThe other set of growth theories of firms include the Stochastic and Deterministic ApproachesThe stochastic model, which is also known as the Gibrat~s Law, argues that all changes in sizeare due to chance. Thus, the size and age of firms has no effect on the growth of SMEs.According to Becchetti and Trovato (2002) empirical of the law has indicated that it onlyconsiders size and age as potential variables which may significantly affect firm growth byneglecting other explanatory variables which may significantly affect firm growth. Thedeterministic approach assumes, on the contrary, that differences in the rates of growth across

7

firms depend on a set of observable industry and firm specific characteristics (Becchetti andTrovato, 2002 and Pier Giovanni et al 2002).

2.3. Empirical Literature ReviewKushoka (2013) adapted a research to examine the contribution of microfinance institutions onenterprise development in Tanzania. The article is aimed at moving poor small-scaleentrepreneurs and/or would-be entrepreneurs from low-growth enterprises to high-growthEnterprises using Microfinance Institutions (MFIs). The study employed both descriptive andexplanatory approaches to seek answers to the research question. The study reveals that there isan increase in the number of employees and amount of working capital of entrepreneurs afterusing the services of Microfinance Institutions (MFIs). The researcher concludes thatMicrofinance Institutions (MFI5) are key players in entrepreneurship development; it isrecommended that Microfinance Institutions (MFIs) should package their services together(financial and non-financial) in order to positively boost growth of Micro Small and MediumEnterprises (MSME5).

Sakthi (2011) and Praveen Kumar S. conducted a research study about the role of microfinanceinstitutions in the development of entrepreneurs in Africa. The study is focus for entrepreneurswho want to run a business and yet can’t afford a piece of equipment and merchandise. Theresearch whereby providing equipment or merchandise to enable the project to run a self-fundingprofitable project. The research found out that only 6 % of Africans borrow money to start abusiness where as 13 % borrow to buy food. 50 % of the population live with less than 1US$ orless per day. Most of the Africans lack the understanding of what it would take to successfulentrepreneurs. They lack necessary technical management skills and confidence. They lackpersonal ambition and willingness for fear of sharing ownership and failed to form partnership.

Ekpe (2010) have studied the effect of Microfinance factors on women Entrepreneurs’performance in Nigeria. Women play a crucial role in the economic development of theirfamilies and communities but certain obstacles such as poverty, unemployment, low householdincome and societal discriminations mostly in developing countries have hindered their effectiveperformance of that role. It is discovered that women entrepreneurship could be an effectivestrategy for poverty reduction in a country; since women are the worst hit in such situation.However, it is discovered that women entrepreneurs, especially in developing countries, do nothave easy access to microfinance factors for their entrepreneurial activity and as such have lowbusiness performance than their men counterparts, whereas the rate of their participation in theinformal sector of the economy is higher than males, and microfinance factors could havepositive effect on enterprise performance.

Mamun (2009) did his studies of microfinance in Bangladesh for graduation Master’s DegreeProgram from the University of Glamorgan, UK. The aim of the study was to assess the factorsthat led to the success of Micro-finance, in particular, Grameen Bank (GB), in Bangladesh. Thestudy was investigated the innovation, design and implementation of GB. Besides, this researchalso examined the adaptation and learning practice of GB and the motivation and contribution ofGB and some environmental factors that supported GB especially in Bangladesh. The studyfindings were in relation to the purpose of this research. This study revealed that some

8

innovation, design and implementation of GB such as group based lending, the collateral freelending system, peer group monitoring system, the designed training staff of GB were the majorfactors that contributed to the success of micro-finance; the adaptation and learning practice suchas flexibility of obtaining a loan, a housing loan with lower interest rate, mandatory andvoluntary savings were the most significant issue; the motivation of GB such as incentiveschemes to staff, encouragement for financial independent by the borrowers of GB, borrowersmotivated to mobilize and allocate resources were also the most leading issue, the contribution ofGB such as microfinance programme contributed to female’s control over resources and decisionmaking at family level enormously as well as the environmental issues such as ongoingpopulation growth that favoured GB very significantly. Finally, the researcher recommended thatGB should necessitate the expansion of the organizational capability to recognize the appropriateinnovation, creating the cultural innovation, sustainable development programme on the basis ofdemands and problems of the borrowers, the initiative for an appropriate macro-economic policyand financial designs in order to alleviate the poverty from the rural economy.

2.3.1. Role of Microfinance on SMEs Growth.Since the World Summit for Social Development the priority given to poverty eradication hasgrown. As stated in the previous report of the Secretary-General on the eradication of poverty, itis now broadly accepted that robust economic growth that is labor-intensive and equitable,combined with larger outlays of social expenditures, especially directed towards the poor (nowestimated at 1.3 billion people), are a winning combination in the fight against poverty(Chaliand, 2003). Several factors have led to increased interest in micro-credit in promotinggrowth with greater equity. There has been a growth in the recognition of the importance ofempowering all people by increasing their access to all the factors of production, includingcredit. In addition, the value of the role of Non-Governmental Organizations in development isreceiving more attention.

It is in that context that micro credit has recently assumed a certain degree of prominence. It isbased on the recognition that the latent capacity of the poor for entrepreneurship would beencouraged with the availability of small-scale loans and would introduce them to the small-enterprise sector. This could allow them to be more self-reliant, create employmentopportunities, and, not least, engage women in economically productive activities. Currently,there are estimated to be about 3000 microfinance institutions in developing countries like inKenya, Malawi, Nigeria, to mention just a few. These institutions also help create deeper andmore widespread. They provide the rural population with access to savings within the local areaand with a certain cushion against economic fluctuations, and they encourage a cooperative andcommunity feeling (Department of Social Development, 2001). The groups formed provide jointcollateral and serve as instruments for spreading valuable information that is useful for economicand social progress.

In many developing countries, many loan takers have been proven to have much benefit as theyget credits. Studies undertaken by Chaliand (2003) and Chijoriga (2000) on the impact of microcredit programs on household income show that participants of such programs usually havehigher and more stable incomes than they did before they joined the programs. Some

9

practitioners still have reservations about the findings of those studies. Moreover, not manymicro credit programs can afford to undertake impact assessments because they are generallyexpensive and time-consuming. There are serious disagreements among experts on the validitymethodologies used in some of the published studies. In some cases, even the more rigorousstudies have produced inconclusive results (Chaliand, 2003).

Chijoriga (2000) revealed that there are limits to the use of credit as an instrument for povertyeradication, including difficulties in identifying the poor and targeting credit to reach the poorestof the poor. Added to this is the fact that many people, especially the poorest of the poor, areusually not in a position to undertake an economic activity, partly because they lack businessskills and even the motivation for business.

Furthermore, it is not clear if the extent to which micro credit has spread, or can potentiallyspread, can make a major dent in global poverty. The actual use of this kind of lending, so far atleast, is rather modest: the overall portfolio of the World Bank, for example, is only $218million. In recent international meetings, it has been stated that a target to reach 100 millionfamilies by the year 2005 would require an additional annual outlay of about $2.5 billion. Thisshould be compared to the total Gross Domestic Product (GDP) of all developing countries,which is now about $6 trillion. A certain sense of proportion regarding micro credit would seemto be in order.

In addition, the administrative structures governing these institutions are commonly either fragileor rudimentary, and often involve large transaction costs. A study by the Organization forEconomic Cooperation and Development (OECD), for example, found that many specializedagricultural institutions were not designed to serve as financial intermediaries. The success offinancial intermediation at any time depends significantly on how efficiently the transaction iscompleted. If the transaction costs, combined with high interest rates, require that the operationin question generate profit margins of the order of 30% to 50%, it is not clear that this would beeconomically beneficial (Chijoriga, 2000). It is not surprising that in many micro lendingoperations, trading activity — with quick turnover and large profit margins — dominates.

In many cases, micro-credit programs have been stand-alone operations. There is nowconsiderable consensus that lending to the poor can succeed provided it is accompanied by otherservices, especially training, information and access to land. According to the World Bank(2000) cited in Asian Development Bank Institute (2010) credit needs to be supplemented withaccess to land and appropriate technology. But such activities require strong support from thepublic sector. In some of the lowest-income countries, lack of access to land is the most criticalsingle cause of rural poverty, which dominates the poverty situation in those countries. Yet, fewcountries have substantial land reform programs.

Moreover, in the proliferation of micro lending institutions, Non-Governmental Organizationsand foreign donors have played an increasing role. Non-Governmental Organizations vary inquality and strength. The best results are produced, research shows, when developing countryGovernments and Non-Governmental Organizations work hand in hand. While donor

10

participation can be positive, it should be noted that total Official Development Assistance(ODA) has declined in recent years.

2.3.2. Linkage between Microfinance and SMESeveral objectives so conceived by the government of Uganda influenced the initiation of TheJMFs schemes, among them, the most commonly mentioned ones include: poverty alleviationand improved living standards, offering financing to the poor Harper et al (1999), women’sempowerment Rahmn (1999), and the development of the business sector as a means ofachieving high standards and reducing market failure (Chijoriga and Cassimon, 1999).

Microfinance and its impact go beyond just business loans. The poor use financial services notonly for business investment in the microenterprises but also to invest in health and education, tomanage household emergencies and to meet the variety of other cash needs that they encounter.

In terms of understanding poverty Chaliand (2003) maintains that a simple distinction can bedrawn within the group ‘the poor’ between the long-term or ‘chronic poor’ and those whotemporarily fall into poverty as a result of adverse shocks, the ‘transitory poor’. Within thechronic poor one can further distinguish between those who are either so physically or sociallydisadvantaged that without welfare support they will always remain in poverty (the ‘destitute’)and the larger group who are poor because of their lack of assets and opportunities. Furthermore,within the non-destitute category one may distinguish by the depth of poverty (how farhouseholds are below the poverty line) with those significantly below it representing the ‘corepoor’, who are sometimes categorized by the irregularity of their income (Chaliand, 2003).

In principle, micro finance can relate to the chronic (non-destitute) poor and to the transitorypoor in different ways. According to WB (2000) cited in Asian Development Bank Institute(2010) the condition of poverty has been interpreted conventionally as a lack of access by poorhouseholds to the assets necessary for a higher standard of income or welfare, whether assets arethought of as human (access to education), natural (access to land), physical (access toinfrastructure), social (access to networks of obligations) or financial (access to credit).

Lack of access to credit is readily understandable in terms of the absence of collateral that thepoor can offer conventional financial institutions, in addition to the various complexities andhigh costs involved in dealing with large numbers of small, often illiterate borrowers (Chestnut,2010). The poor thus have to rely on loans from either moneylenders, at high interest rates, orfriends and family, whose supply of funds will be limited. Microfinance institutions attempt toovercome these barriers through innovative measures such as group lending and regular savingsschemes, as well as the establishment of close links between poor clients and staff of theinstitutions concerned.

Microfinance has consistently proven to be one of the most effective strategies in the Growth ofSME in developing countries. Today, microfinance institutions around the world reach a littlemore than 100 million people (Asian Development Bank Institute, 2010). Thus most citizensearn their livings through self-employment, creating and operating their own tiny enterprises.Without financial services to fuel their productivity, the poor can never grow their microenterprises into businesses that help them escape poverty.

11

Therefore, by providing very poor families with small loans to invest in their micro enterprises,they become able to rescue themselves from poverty. They use these loans to start, establish,sustain, or expand very small, self-sustaining businesses (Begu, et al 2000). For example, awoman may borrow 150 000 Ugshsto buy chickens, so she can sell eggs. As the chickensmultiply, she will have more eggs to sell. Soon she can sell the chicks.

2.5 Summary of Literature ReviewThe current theories on microfinance postulate that microfinance structures are essential fordevelopment which is based on three basic assumptions: one is that poor populations possess thecapacity to implement income generating activities. Two is the idea that poor people givenaccess to capital and guided properly are in a position to implement and manage incomegenerating business enterprises. Three is that once the financial systems are established, the poorpeople t1are able to use it (the financial tools) for productive purposes and progressivelyincorporate themselves into the financial milieu, repaying the loans, and accumulating savings”.This is because microfinance provides the means to generate income that eventually leads to asustainable development. The informal sector became more important in the 1 970s and 1 980s asthe reliance of household members on formal wage earnings was replaced by informal incomegenerating activities (Tripp, 1996).

The rapid growth was initiated by the informal enterprises themselves as a measure of survivalfollowing the failure of the state (Maliyamkono&Bagachwa, 1990; Rutashobya&Olomi 1999).The decline of real wages, persistent inflation, and the decline of the formal sector employmentattributed to the rapid expansion of the informal sector (Bagachwa 1995). In addition,commercial banks were encouraged to provide services to this sector through loan quotas,subsidies, tax breaks, training and guarantees against defaults. Despite massive subsidies,development banks created by Governments in developing countries have had little success inreaching the intended beneficiaries (UNCTAD 1995).

Finally, the effect of microfinance on small and medium business has not received adequateresearch attention in Uganda. This means that there is a major gap in the relevant literature ondeveloping countries including Somalia, which has to be covered by the research. This researchattempts to fill this gap by studying the situation in Uganda and providing more empiricalevidence on the effects of microfinance on the growth of enterprise.

12

CHAPTER THREERESEARCH METHODOLOGY3.0 IntroductionThis chapter outlines the methods that were used in the study. The Chapter is divided into sixmain sections that describes the research design, target population, sample design, validity andreliability, data collection procedures, data analysis and presentation.

3.1 Research DesignResearch design involves turning research questions into research project (Robson, 2002). Thismeans that to answer the research questions, the appropriate strategies, methods and techniquesshould be adopted. Nachmias and Nachmias (1993) define research design as the program thatguides the investigator in the process of collecting, analyzing and interpreting data. Yin (1994)proposes that the types of research questions determine the most suitable strategy. The researchquestions in this study focus mainly on what questions asked. And to answer this type ofquestion, a survey strategy is preferred (Yin, 1994). Kothari (2008) describe several types ofresearch, e.g. experimental, descriptive, exploratory and interpretive. Descriptive research aimsat identifying and recording a phenomenon, processor system and may be conducted usingsurveys (Fellows and Liu, 2003). The research question that were presented in this study were ofdescriptive survey design that was appropriate for preliminary and exploratory studies so as toallow the researcher gather information, summarize, present and interpret data for the purpose ofclassification (Orodho, 2003).

3.3. PopulationThe population consisting of all the Small and Medium enterprises in Lira District which wasapproximately in excess of 5000 enterprises.

3.4 Sample DesignThe sampling plan describes the sampling unit, sampling frame, sampling procedures and thesample size for the study. The sampling frame describes the list of all population units fromwhich the sample will be selected (Cooper & Schindler, 2003). A convenient sample of 150SMEs werestudied. The sample were selected from registered businesses operating in LiraDistrict. In order to carry out a scientific study, the sample of 150 enterprises was desirably takeninto account of the fact that the researcher will be limited in resources in terms of time andmoney.

3.5 Validity and Reliability3.5.1 ValidityValidity shows whether the instrument measures what they are designed to measure (Borg andGall, 1989). Ensuring the validity of the data collection instrument involved going throughquestionnaire in relation to the set objectives and making sure that they contained all theinformation that could enable answering these objectives. The tools are developed by theresearcher and content and face validity are to be established. The content validity were

13

established to ensure the accuracy of instruments (Leeds, 1993). The face validity was to ensurethat the instrument appear to measure what it is purported to measure.

3.5.2 ReliabilityThe instruments will be piloted in other areas that do not form part of the actual study that is,Lira Municipal Council. This shall enhance the reliability and validity of the instruments(Mugenda and Mugenda, 1999). The result of the piloted instruments is to calculate thereliability coefficient. Reliability is established to ensure accuracy or the consistency of theinstrument, that is, the extent to which the results remain similar over different forms of the sameinstruments (McMillan & Schumacher, 1993).

3.6. Sampling Techniques3.6.1. Cluster Sampling TechniqueCluster sampling technique involves the selection of an entire group from a list of groups (Adamand Kamuzora, 2008). The total population is divided into a number of relatively smallsubdivisions which themselves are clusters of small units. Some of these clusters are thenrandomly selected for inclusion in the overall sample. In this case, the researcher will selectclusters/groups of respondents as sampling frame.

The researcher will select respondents from their clusters/groups receiving financial servicesfrom these micro credit programs. Under this sampling technique, one hundred and fifty (150)respondents were selected from their groups to constitute the sample. This technique will be veryhelpful in the sense that it will help to save time for data collection because the researcher tend tocontact them in groups.

3.6.2. Data Collection ToolsIn order to collect the data needed, the researcher will use questionnaire, and interview forcollecting primary data and documentary method for collecting secondary data. This study willbe involving the application of quantitative approach.

3.6.2.1. QuestionnaireThe researcher used this method to collect primary data from respondents. They were first pretested by a small number of respondents and then after distributed to clients of these micro-creditprograms for collecting the data needed.

Structured Questionnaires: This was used to collect information from households. Questionnaireswere developed to obtain survey data that allowed an understanding of the impact of microfinancing services on the growth of micro and small entrepreneurs. The questions wereformulated in English and translated into luo to make them understandable to respondents. Theywere distributed to collect quantitative data from 150 respondents receiving financial services.

3.6.2.2. InterviewThe researcher used this tool to supplement the questionnaire method of data collection to obtainthe qualitative data. The interview allowed respondents to freely provide their views related tothe problem being investigated. The interview was semi-structured; i.e. some of the questionsand topics were predetermined. Other questions were expected to arise during the interview and

14

thus the method appeared to be informal and conversational, but carefully controlled andstructured.

3.6.2.3. Documentary ReviewUnder this method, the researcher examined whether the data collected were reliable, suitableand adequate. This method helped the researcher to get supportive information thatcomplemented data obtained through use of questionnaire and interview techniques. The methodwas therefore helpful to understand the contribution made by these micro-credit programs indifferent areas and epochs, seeking to explore the magnitude of the problem as documented byother researchers. Different books, journals, newsletters, electronic information and other formsof documented materials were perused.

3.7. Data Processing, Analysis and PresentationOnce the questionnaire or other measuring instruments have been administered, the mass of rawdata collected must be systematically organized in a manner that facilitates analysis (Mugendaand Mugenda, 1999). In order to facilitate the analysis of data from questionnaires, interviewsand documentary sources, findings were extracted and presented to answer the researchquestions.

Statistical Package for Social Sciences (SPSS) computer software for storage, processing andanalysis of data so as to obtain answers to the research questions. SPSS computer software wasused for data processing before data analysis. The data analysis is important since it distil crudedata into clear and interpretable ones (Kerlinger, 1986). Descriptive statistical analysisprocedures including cross-tabulations and frequency distributions from the database templatewere used to determine the relations between pairs of variables. The inferential statisticalanalysis, namely t-test was used. The t-test was employed to test the research hypothesis.Qualitative data (unstructured questions) wasanalyzed through content analysis method. Contentanalysis is the systematic, quantitative analysis of communication content, including verbal,visual, print, and electronic communication. Under this method, a researcher applies objectiveand systematic counting and recording procedures to create a quantitative description of thesymbolic content in a text (Neuman, 2003).

3.8 Empirical Framework of SME Growth3.8.1 Dependent VariableThere is little agreement in the existing literature on how to measure growth, and scholars haveused a variety of different measures. These measures include, for example, growth of sales,employees, assets, profit, equity, and others (Davidsson, &Wiklund, 2000). The study usedSmall and Medium Enterprises Growth (SME_G) as a dependant variable; in this study aresearcher uses volume of gross sales (in ugsh) per annual as a measure of SME growth. In thisphenomenon, a researcher takes unit price of the commodity multiplied by the total quantity soldof each individual respondent.

GS=~Px~QS(1)

Where; GS denotes Volume of gross sales (in ugsh) per annual, P denotes unit price of acommodity and QS denotes Quantity of goods and services sold per annual.

15

3.8.2 Independent VariablesAmount of Loan (AMOL)

Amount of loan in ugsh, the researcher used this variable as an independent variable to measurethe access of fund on SME. Here, the study was used to measure the total amount of loan thatSME practitioners acquired from MFI in a given period of time.

AMOL=~Lo ± R (2)

Where; AMOL denotes total amount of loan in ugshacquired by SME participant, Lo denotesmicro-loan in ugshand R denotes Rate of interest in ugshfor such micro-loan.

Experience of SME Members (EXPp)

The stud also used Experience of SME participants in particular business; here a researchermeasured the experience of SME member by taking the total number of years in business sinceits operation to the time when this research is conducted.

EXPp=Tt-1 - Tt (3)

Where; EXPp denotes experience of SME members, Tt-1 denotes initial year of businessoperation while Tt denotes present year when research conducted.

SME Member’s Start-up Capital

Start-up capital in ugsh.is another independent variable that will be used by a researcher in itsmodel to analyze the growth of SME. Start-up capital was measured through summing up allsources of capital that SME member accumulated for the purpose of initiating the firm.

STCA = OS ± FC + GR + Lo (4)

Where; STCA denotes Star-up capital in ugsh, OS denotes own saving, FC denotes funds fromfamily, friends, relatives and spouse, GR denotes funds from donors and Lo denotes loan fromcommercial and non-commercial banks.

Education Level

Education level was another independent variable that measured the SMEs growth, a researchertakes the general level of education that a member completed in term of Uganda educationsystem. Level of education included are, primary education, secondary education, and highereducation. A value of 1 was given to entrepreneur who completed primary education and value 0to those who have other level of education.

Number of Employees

Number of employees (EMPLY) is another independent variable in order to test for scaleeffects in the relation to growth SME.

16

3.9. Empirical ModelThis study used cross-sectional data regression model in empirical test, and tested whether MFIimproves SME growth. In empirical test, individuals of cross-sectional data are SMEpractitioners from BRAC and Centenary bank in Lira Municipality. The researcher used thefollowing econometric model to estimate through single equation linear regression model. This isthe multiple regression model of the form

SMEGi = 130 + f31AMOL1i + 132EDU2i + f33EXPp3i + 134STCA 4i + 135EMPLY 5i + ei (5)

Where,

SMEG = SMEs growth,

AMOL = the total amount of micro-loan to the participant,

EXPp Number of years being in the business (Age of the business),

EDUC = Level of education of the SME’s member

STCA = Start-up capital in ugsh,

EMPLY = Number of employee

13’s are multiple regression coefficients estimated

e = the error term.

i = 1 n, where n is the number of SME

The Ordinary Least Squares (OLS) technique was used in estimating the specified econometricmodel. Apart from its simplicity, it gives reliable estimates. The estimation software was SPSSversion.

17

CHAPTER FOUR4.0 DATA ANALYSIS AND DISCUSSION4.1 OverviewThis chapter presents an analysis and discussion of the research findings of the study. In thiscontext the chapter analyzed data with reference to the research objectives, questions andhypothesis. The study provides description of the socio-economic and demographiccharacteristics of the respondents namely age, sex, and education level.

Also the main occupation and years in business (experience) were discussed.

4.2. Socio-economic and Demographic Characteristics of the Respondents.For that matter, socio-economic and demographic characteristics provide a foundation for

understanding the differences and similarities in the human resource base at the household levels.Also, they acts as factors that may influence participation in micro credit’s program that againleads to huge impacts to the credit users. On the other hand, the physical resource base of ahousehold indicates its stock of wealth, life standards and wealth or poverty level (Barnes andKeogh, 1999).

The primary research data from SME’s practitioners in BRAC and Centenary bank were by theuse of structured questionnaires which in turn got analyzed for different significance levels afterbeing employed in the regression model. A total of 150 questionnaires were randomly distributedto SMEs taking loan from BRAC and Centenary bank as shown on table 4.1, thereforeconsidered as adequate to the subsequent data analysis. The demographic profile of respondentswas summarized with age, gender and education. The validity and reliability tests of researchwere conducted prior carrying out the statistical techniques.

Table 4.]. Number ofRespondents Covered

Name of MFI Frequency j PercentBRAC 75 50Centenary bank 75 ________________________Total 150 1100 1

Source: Field Data, 2018

4.2.1 Gender of RespondentsThe characteristics of the respondents according to sex showed that there were more female77.3% among the SMEs members and 22.7% were found to be male as per figure 4.1. Theseresults imply that female were dominant in MFIs involved in this study. This situation attributedby the policy of these MFI for empowering women economically, however, most of womenengaging on SME get loan from these Micro finances by forming groups of 20 — 30 members.This makes micro credit institutions to build up capacities for income generation activitiesamong the micro entrepreneurs and to provide sustainable sources of livelihood to SMEshousehold members.

18

Figure 4.]: Sex ofRespondents

90

80

70

60

5040 Percent

30

20

10

0

Male Female

Source: Field data, 2018

4.2.2 Mean Age of RespondentsAge is an important factor which can influence economic activities to be performed by a healthyindividual. In this case, age indicates the capability of an individual to produce economicmaterial wealth for humankind consumption. The research findings in Table 4.2 shows thatminimum age of respondents was 18 years old and maximum age was 45 years old, mean age ofrespondents was 31.24 years old. This result suggests, therefore, that a large number ofrespondents were in their economically active age; which may imply high level of productivity,ceteris paribus. Moreover, this is also an indication that a high proportion of the active andhealthy labor force still needs more and access to micro credit institutions so as pull them out ofpoverty in the study area.

Table 4.2: Mean Age ofRespondents

N Minimum Maximum Mean Std deviationrl5o 18 45 31.5 5.880

Source: Field data, 2018: Note NNumber of respondents

4.2.3 Education Level of RespondentsEducation is a process to attain acculturation through which the individual is helped to attain thedevelopment of his potentialities and their maximum activation when necessary, according toright reason and to achieve thereby his perfect self-fulfillment (Okafor, 1984). In its strictlysagacity, this implies that education is an important agent of change as it equipped a person withthe necessary knowledge and skills so as to increase their productivity and income earningability. 19

The study revealed that; 64.6% were primary education, 19.3% have secondary school education,and those with degree accounted for 0.7% of the respondents, while those who have othereducation accounted for 8.0%. The distribution of the educations levels among respondents issummarized in figure 4.2. These results suggest that most of the micro entrepreneurs consultedby the researcher were found to have primary level of education.

Figure 4.2. Respondent ‘s Education Level

Source: Field data, 2018

U Percent

4.2.4 Source of Initial Capital of the SMEBusiness capital is seen as peculiar important and challenge as a start-up businesses in thedeveloping world including Uganda although their policies encourages development ofentrepreneurship because most jobs are reported to be created by small and micro-enterprises(IDRC, 1999). From the study it was realized that 110 clients representing 73.3% had establishedtheir enterprises with their own funds. This was through personal savings, only 29 clientrepresenting 19.3% admitted that their businesses were established by funds from spouse andrelatives. Only 6 client representing 4.0% confirmed that he established his business throughgrants while the remaining 5 representing 3.3% had their businesses established throughborrowing from non-banks. This shows that most people set up their businesses from their ownfunds through personal savings which were either saved in banks or through some collectors.

Table 4.3. Distribution ofsource ofcap

Source of income Number of clients PercentageOwn savings 1 10 73.3Family and friends 29 19.3Grants 6 4.0Loan 5 3.3

70— —

605040 __________

30 -_________

2010

0 ±—

20

igure 4.3: Distribution for Source Capital

PERCENTAGE SOURCE OF INCOME

Own savings Family and relatives Grants

Source: Field data, 2018

19%

4% 4%

73%

Loan

4.2.5 Client’s Start-up CapitalThe study revealed that the minimum start-up capital of the entrepreneurs was Ugsh. 30 000 andthe maximum was Ugshs. 8,000,000. However, table 4.3 depict that, the mean of start-up capitalwas Ugsh. 623 500. The most usual source of finance came from individual saving. Corporateprofits are cited by almost all businesses as a means of financing growth, although this did notexclude other sources. Self-generated funding plays a vital role but it is not enough. The high-growth SME must appeal to outside funding to pursue or consolidate its development. In somecountries, this function is exercised by large industrial or financial groups; the large corporationacquires the SME.

Another possibility is the funding of growth by the financial system.

Table 4.4: Mean Start up Capital ofRespondents in Uganda

N Minimum Maximum Mean Std deviation30,000 8,000,000 623,500 9.157150

Source: Field data, 2018

4.2.6 Amount of Loan AccessedThe researcher examined the impact of the microfinance accessibility on the SMEs growth.However, for the sake of analysis the researcher categorized two groups that representedmembers who accessed and those who did not have access. The figure shows those memberswho get loan amounted less than Ugsh. 500 000 represented those who are not accessed andmembers who get loan amounted Ugsh. 500 000 and above represented accessibility of MFIservices.

21

result in figure 4.4 presen s a summary of loan access of respondents with reference to amountof Uganda shillings accessed from MFIs involved in this study. The results showed 82.7% of therespondents had acquired loan and 17.3% of respondents did not access the loan facilities.

Figure 4.4: Amount ofLoan Accessed by Respondents

90 —_______ ___________________________________80

70

6050

40 • Percent

30————— —-

20

10

Less than 500,000 Above 500,000

Source: Field data, 2018

4.2.7 Number of Years in BusinessThe findings in Table 4.4 indicate that minimum age of business was 1 year and maximum age inbusiness was 13 years from its establishment. The results suggest that most of the entrepreneurwho engage on small business tend to run their business activity for average of 5 years and thenquit to another business. It is estimated that the life period of surviving for small business is atleast one to three years and afterward, these types of small business start to contract quicklytoward decease (Selejio and Mduma, 2005).

Table 4.5: Mean Year ofRespondent in SME

N Minimum Maximum Mean Std deviation150 1 13 5 2.783

Source: Field data, 2018

4.2.8 The Business Type Operated by RespondentsThis study wanted to understand the types of business that are engaged by the respondents inorder to support their family economy, and then a question was posed to collect information onthe matter. The statistical results in Table 5 show the distribution of respondents with respect totheir types of economic activities they are engaged in. Food vending was the main specifiedactivity at the rate of 26.7%, followed by retail shops at the rate of 10%. However, 36.7°c of the

22

business type falls under other type of business which involves different businesses apart fromlisted in figure 4.5.

Figure 4.5: Distribution for Business Operated by Respondents

4.3 Model EstimationThe researcher used correlation analysis to reduce multicollinearity on the econometric model forprocessing and analyzing research data. The study used this method since collinearity of theexplanatory variables is just degree of correlation, so, the matrix measures the relationships ofindividual explanatory variables against another individual explanatory variable withinregression.

The correlation matrix of dependent and explanatory variables is presented in table 5 and is usedto examine the possible degree of collinearity among variables. The table shows that the twomost highly correlated variables are total current investment and amount of loan (a coefficient of0.905). As we observe in table 5, the correlation coefficients are not large enough to causecollinearity problems in the regressions and are statistically significant at the usual levels ofsignificance. To mitigate the problem with possible multicollinearity we gradually exclude thevariables that are expected to be highly correlated with the rest (in this case, STCA and Tci).

Source: Field data, 2018

Table 4. 6. Correlation Matrixfor Model Estimation

~Jariables Sales Busty EMPLY STCA AGE EXPPp AMOL EDUC Tci

Sales 1

Sig

Busty -224 1.006

Sig

EMPLY .100 .411” 1.000

Sig .225

STCA .356” -.305” .000 .114 1.000

Sig .164

AGE .089 -.035 .119 .167~ 1.671 .041

Sig .278 .146

EXPPp .107 -.163 -.133 .031 .422” 1.046 .106 .000

Sig .194 .709

AMOL Z -.351” .000 .080 .597” .125 .097.000 .000

Sig .333 .126 .239

EDUC -.100 .130 -.055 -.317” .056 -.015 -.232”.004.225 .500 .000 .855

Sig .112 .493

Tci .444” -.368” .000 .107 .882” .162W .073 .905” -.304”.000 .000 .047 .000 .000

Sig .190 .374

“Correlation at the 0.01 level (two tails)

‘Correlation at the 0.05 level (Two tails)

Source: Field data, 2018

4.4 Multiple Regression Analysis ResultsThe complete data set based on 150 observations on the chosen variables. Table 4.6 reports themultiple regression analysis on selected variables. The amount of loan (in Ugsh) was 0.37 1 withp - value of 0.002 for the study sample. On number of years in business (Firm’s age) was 0.083with p - value of 0.328, level of education represented 0.040 with p - value of 0.6 13. Similarlyother variables like, respondent’s age representing -0.009, types of business operated byrespondents represented -0.142 and Number of employee represented 0.140 with their p - values0.912, 0.119 and 0.108 respectively.

The estimated result showed R- Squared of 0.223. This indicates that 22% of the variations in thegrowth of SMEs are explained by the independent variables. The F-Statistic which is a key

24

statistic in this cross-section study is 5.8 10 (0.000) and is significant at 95% confident level. Thisimplies that almost all the independent variables in the model have jointly contributed to thegrowth of the SMEs in the Lira Municipality.

Durbin Watson (DW) — Statistics is 2.008. This figure indicates that successive error terms arenot correlated.

Table 4.7: Variables of the Research Model

Variables Coefficients T Sig

(Constant) 1.876 .063

~MOL .304 3.174 .002

EXPp .083 .981 .328

~ge -.028 -.332 .741

STCA .138 1.413 .160

EMPLY .125 1.443 .151

Busty -.119 -1.299 .196

EDUC .040 .506 .613

Dependent variable: Gross sales in Ugsh

R2 = 0.223 F- Statistics = 5.810 (0.000) OW = 2.008

Source: Field data, 2018

4.4.1 To Determine at What Extent Accessibility of Microfinance Lead to Increase theVolume of Gross Sales of ParticipantTo determine the extent of accessibility of microfinance on increasing the volume of gross salesof participants, the study findings shows that accessibility of microfinance has positive influenceon volume of gross sales of SME’s participant. Similarly, this objective was supported by otherstudies, for instance Timmons and Spinelli, (2004) states that lack of access to finance is one ofthe main constraints to the growth and expansion of small businesses.

Amount of Loan Accessed

The additional Ugshs 1 000 amount of loan on average, then SME growth increase by 304 unitsper annum ceteris paribus. The higher the access the amount of loan the higher the volume of

25

gross sales per annum. The main interest is in the signs and magnitudes of the variablesmeasuring the impact of accessibility of microloan (amount of loan) because they represent thesensitivity of SME growth to amount of loan in Ugsh. Theoretically, microfinance accessibilityenables poor to smooth their consumption, gradually develop micro enterprises and enhanceincome capacity (Rubambey, 2001). Similarly, lack of broad access to financial services limitsopportunities for agribusiness enterprises and small holders to adopt efficient technologies andefficient resource allocation (Peer, 2010). In fact the entrepreneur who accessed high loan is ableto improve his/her business environment which can attract and monopolize the market throughimproving the quality and increase quantity of product, setting competitive price, increasingadvertising budget and to improve business premise. The coefficients on amount of loans inUgshs are statistically significant under t-test at 5% level of significance. The magnitude of thesecoefficients is consistent with the hypothesis stated that; there is no statistical significantrelationship between microfinance access and SMEs growth. The study suggest that, the nullhypothesis was rejected hence there is statistical significant relationship.

4.4.2 To Examine Other Factors Enhancing SME’s GrowthThe study aimed to understand other factors rather than loan accessibility that enhancing

SME’s growth, in this point of view the researcher analyzed variables of start-up capital in Ugshsand experience of SME practitioners to measure the SME’ s growth. The study reveals that thesevariables were not statistically significant at t statistic 0.05 level of significance.

Number of Employees

The additional 1 worker on average, then SME growth goes up about by 125 units per annumceteris paribus. The main interest is in the signs and magnitudes of the variables measuring theimpact of number of employee on SMEs growth, because they represent the sensitivity of SMEgrowth to number of employee. Ceteris paribus the higher the number of employees the higherthe volume of gross sales per annum, on the study shows that firms have 1 to 5 employees, thisdue to the nature of their business as well as small capital they have. The empirical evidenceshows that the larger the firm (in terms of assets or number of employees) the greater it’spotential to grow (Wiklund and Shepherd, 2005). The coefficients on number of employees arestatistically insignificant under t-test at 5% level of significance.

Experience in Business

The experience of an entrepreneur in his/her business increases by a year on average, then SMEgrowth increase by 0.083 units per annum. The main interest is in the signs and magnitudes ofthe variables measuring the impact of experience of years in business on SMEs growth, becausethey represent the sensitivity of SME growth to experience of years in business. Ceteris paribus,the more experience within the business the higher the

SME growth. Theory states that SME practitioners with more managerial, sector experience orprior SME experience as owner/manager tend to correlate with greater growth (Storey et al,1989). On the study shows that the mean years’ experience of entrepreneurs was 5 years whilethe maximum experience years was 13 and minimum experience years was 1 year. The study

26

reveals that there is no necessity for being in business for long term to influence enterprise’sgrowth; the reason could be low demand on the product or low production on the product withhigh competition. On the other hand, most of the entrepreneurs quit from one business to anotherafter five years for searching more profitable business with high volume of gross sales. Thecoefficients on experience of years in business are statistically insignificant under t-test at 5%leyel of significance. The magnitude of these coefficients are inconsistent with the hypothesisthat; There is no statistical significant that experience on SME activities improves SME’sgrowth. The study result suggests that the null hypothesis was accepted hence there is nostatistical significant relationship.

Education of the SME Member

The education level of an entrepreneur possessed increases by a stage on average, and then SMEgrowth goes up about by 0.040 units per annum. The main interest is in the signs and magnitudesof the variables measuring the impact of education on SMEs growth, because they representsensitivity of SME growth to education. Ceteris paribus, the fact that basic education enhancesthe overall quality of the owner/manager by providing him/her with basic numeric and literacyskills thus increases the chance of survival. Theory states that the fact that a manager has ahigher education degree or even a postgraduate degree seems to stimulate the growth of the firm,thus having an impact on both survival and growth. On the study shows the majority of therespondents were in primary education level fall under 64.6% while owners who undergoneuniversity degree were 0.7%. The study shows those owners who having primary education levelhave average volume of gross sales per annum, the reason could be they have small initial capitalhence they get little amount of loan from MFIs. The coefficients on education of respondents arestatistically insignificant under t-test at 5% level of significance.

Age of Respondents

An extra age of an entrepreneur in a year on average, then SME growth goes down about by0.028 units per annum. The main interest is in the signs and magnitudes of the variablesmeasuring the impact of age of respondent on SMEs growth, because they represent lesssensitivity of SME growth to age of respondents. Theory states that age is an important factorwhich can influence economic activities to be performed by a healthy and energetic individual.In this case, age indicates the capability of an individual to produce economic material wealth forhumankind consumption. Available discussion explaining the influence of the age of theowner/manager advocates for the younger owner/manager; the argument here rests on the factthat the younger owner/manager has the necessary motivation, energy and commitment to workand is more inclined to take risks (Storey, 1994). The logic is that the older owner/manager islikely to have reached his/her initial aspiration. On the study shows that mean age ofentrepreneurs was 31.24 years while the maximum age was 45 years and minimum age was 18years, in the study area most of the people belonging to this age are running businesses whichhave low returns. This could be because of lack of enough capital, low level of business skillsand unfavorable business location. The coefficients on age of respondents are statisticallyinsignificant under t-test at 5% level of significance.

27

Start-up Capital

The additional Ugshs 1 000 start-up capitals on average, then SME growth goes up about by 138units per annum ceteris paribus. The main interest is in the signs and magnitudes of the variablesmeasuring the impact of start-up capital in Ugshs on SMEs growth, because they represent thesensitivity of SME growth to start-up capital. Ceteris paribus the higher the start-up capital thehigher the volume of gross sales per month, on the study shows that those people having enoughcapital during their venture experienced higher volume of gross sales per month. In fact theentrepreneur who have large initial capital may improve his/her business environment which canattract and monopolize the market through improving the product, setting competitive price,advertising as well as good location for the business. The coefficients on start-up capital arestatistically insignificant under t-test at 5% level of significance. The magnitude of thesecoefficients is inconsistent with the hypothesis that; there is no statistical significant relationshipbetween SMEs growth and start-up capital. The study suggests that the null hypothesis wasaccepted hence there is no statistical significant relationship.

Business Type Operated by Entrepreneurs

Moving to food vending decreases by a unit on average, then SME growth goes down about by0.119 units per annum. The main interest is in the signs and magnitudes of the variablesmeasuring the impact of food vending on SMEs growth, because they represent less sensitivityof SME growth to business type operated by entrepreneur. Available theories explaining thesector in which a firm operates is considered an influential factor on the growth processes insmall firms but the extent to which it is a significant factor is less clear-cut. Although the level ofindustrial disaggregation can be expected to influence the results of sector analysis, empiricalstudies Smalibone et al (1995) usually find that there are significant differences amongst sectorsin terms of the typical firm growth rates. On the study shows that most of the people wereoperating food vending, this business operated mostly by female and these are the majority ofrespondents in this study. Similarly this type of business taking large part of SME, this could bebecause the business need small amount of capital to operate the sector. The coefficients onbusiness type are statistically insignificant under t-test at 5% level of significance.

4.5 Summary of Chapter FourThe data analysis in this chapter used descriptive analysis in terms of frequency and descriptiveas well as regression analysis. The study findings reveal that all three specific objectives werecaptured under the field data gathered by a researcher. The three research hypothesis were testedat sig 0.05 level of significance, one research hypothesis out of three was revealed that nullhypothesis has statistically significant; which are (1) HO: There is no significant statisticalrelationship between microfinance access and SME growth. While the rest research hypothesistested and the study findings reveal that the null hypothesis was not statistically significant,which are; HO: There is no statistical significant that experience on SME activities improvesSME’s growth and HO: There is no statistical significant relationship between SME growth andstart-up capital.

28