the impact of internal governance mechanisms on audit ... · 1 the impact of internal governance...

TRANSCRIPT

1

The impact of internal governance mechanisms on audit quality: a study of large listed

companies in China

Yuan George Shan

Business School, University of Adelaide, Adelaide

10 Pulteney Street, Adelaide, South Australia 5005, Australia

Email: [email protected]

Abstract

Purpose – This paper examines whether audit quality of Chinese listed companies is affected

by internal governance mechanisms (IGMs).

Design/methodology/approach – The sample contains a panel data set of 117 companies

with 540 firm-year observations during 2001–2005. The logistic regression model is used to

investigate the three sets of hypotheses regarded IGMs.

Findings – The results show that foreign ownership and the number of professional

supervisors are positively related to audit quality, but the size of supervisory board shows a

negative correlation. Other IGMs including state ownership, the size of board of directors, the

number of independent directors, the frequency of board meetings, and the frequency of

supervisory board meetings are found to have no impact on audit quality.

Practical implications – This paper offers insights to policy-makers and regulators interested

in enhancing corporate governance in China. It also provides recommendations to prescribe

the legal responsibilities and obligations for two-tier boards in the Chinese context, allowing

them to undertake their duties diligently.

Originality/value – The contribution of this paper is twofold. First, prior literature

incompletely uncovers the impact of concentrated ownership and two-tier board system on

2

audit quality. This paper provides a comprehensive evaluation of independent and

interdependent effects of IGMs of Chinese characters and investigates how these IGMs

jointly affect audit quality in China. Second, this paper considers the improvement of legal

environment as one of external governance mechanisms (EGMs) proposed by Denis and

McConnell (2003) and examine the relationship between company‟s IGMs and it‟s the

decision for audit quality choice.

Keywords Corporate Governance, Audit Quality, China

Paper type Research paper

1. Introduction

From early 2001, corporate financial scandals involving listed companies in China (e.g.,

Guanxia Industry Co. Ltd, Macat Optics and Electronics Co. Ltd, Sanjiu Pharmaceutical Co.

Ltd and Lantian Co. Ltd) prompted policy-makers, regulators and officials at the China

Securities Regulatory Commission (CSRC) and the State Economic and Trade Commission

(SETC) to make corporate governance a priority issue for their agenda in 2002. The

government came under increasing public pressure to improve its policy towards corporate

governance structures and grant permission to a select set of accounting firms to audit public

companies (DeFond et al., 2000). Additionally and importantly, according to the WTO entry

agreement, China should be committed to capital market liberalisation and corporate reform,

in particular with respect to state-owned enterprises (SOEs). An effective and efficient China

corporate governance system must coincide with international standards, allowing both

domestic companies and foreign companies to enjoy free market competition within a fair

economic and policy environment.

3

The purpose of this paper is to examine in a more comprehensive way than has been

the case previously the key internal governance mechanisms (IGMs) of listed companies in

China in their association with audit quality.

According to the Cadbury Report (1992, p. 36) the annual audit is “one of the

cornerstones of corporate governance…The audit provides an external and objective check on

the way in which the financial statements have been prepared and presented.” But the

effectiveness and efficiency of external auditing is subject to the actuality and the

development of the corporate governance environment (Holm and Laursen, 2007). A sound

corporate governance mechanism plays an important role in enhancing the audit function

because it assists in ensuring that directors and management of listed companies appoint high-

quality auditors who will exercise independent and effective monitoring over the financial

reporting process (Lin and Liu, 2009a).

Under agency theory, principal-agent problems stem from the complex set of

contracts engaged in by the firm. Such contracts may be either explicit or implicit in the

separation of ownership from control of the firm. Perhaps best known principal-agent

problem is where a divergence of interests between owners and managers causes the agent

(management) to fail to maximize the welfare of the principal (shareholders) (Jensen and

Meckling, 1976; Shleifer and Vishny, 1997; Denis and McConnell, 2003). From this

perspective, the audit function represents a vital corporate governance mechanism that helps

shareholders in their monitoring and control of company management. The audit of a

company‟s financial statements makes disclosures more credible, thereby instilling

confidence in the company‟s transparency. Indeed, auditing has been considered to play a

role in contract monitoring, as a company‟s auditors contract with debtholders to report any

observed breaches of restrictive covenants and audited earnings numbers are used in bonus

plans (Watts and Zimmerman, 1986). This argument is commonly accepted in prior auditing

4

research that examines the quality of auditing (e.g., DeAngelo, 1981; DeFond, 1992;

O'Sullivan, 2000; Kane and Velury, 2004; Chan et al., 2007; Boo and Sharma, 2008; Al-Ajmi,

2009; Lin and Liu, 2009a, 2009b; Lin et al., 2009; Gul and Goodwin, 2010; Zerni et al., 2010;

Zaman et al., 2011; Liu et al., 2011). Some of these studies introduce corporate governance

mechanism in terms of principal-agent conflicts to analyse audit quality through proxies such

as audit firm size (Kane and Velury, 2004; Lin and Liu, 2009b), audit fees (O'Sullivan, 2000;

Boo and Sharma, 2008; Zaman et al., 2011), auditor switching (Lin and Liu, 2009a; Lin et al.,

2009) and modified audit opinions (Liu et al., 2011). For example, Kane and Velury (2004)

hypothesise that American institutional owners prefer audits conducted by large audit firms

due to their belief that large audit firms provide relatively higher audit quality. Their findings

confirmed the positive association between institutional ownership and audit firm size (Big 6).

O'Sullivan (2000) uses audit fees as a surrogate for audit quality to examine the

impact of board composition and ownership structure on audit quality in the UK prior to the

adoption of the recommendations of the Cadbury Committee (1992). His findings suggest

that audit fees have a positive correlation with the proportion of non-executive directors and a

negative association with the proportion of equity owned by executive directors, but have no

impact with ownership by large institutional blockholders or CEO/chairman duality. Boo and

Sharma (2008) investigate the nature of the relationship between three corporate governance

mechanisms (board/audit committee independence, external auditor size and regulators) for a

sample of industrial firms and financial/utility firms subject to industry-specific regulation.

They find weaker relationships between audit fees and board/audit committee independence

and size for regulated firms. This finding suggests that regulatory oversight partially

substitutes the external audit as a monitoring mechanism. Zaman et al. (2011) examine the

correlation between governance quality and auditor remuneration in the UK based on a

composite measure of four dimensions of audit committee effectiveness (independence and

5

financial expertise of audit committee members, frequency of meetings and size of the audit

committee. They find a significant positive association between audit committee

effectiveness and audit fees for large firms after controlling for board of director

characteristics, which indicates that effective audit committees undertake more monitoring,

resulting in higher audit fees.

Rather than the traditional principal-agent problem, a principal-principal problem is

introduced as a major concern in relation to corporate governance in emerging economies

(Dharwadkar et al., 2000). These economies are characterized by high ownership

concentration, extensive family ownership and control, and weak legal protection of minority

shareholders (Dharwadkar et al., 2000; Young et al., 2008). To moderate the principal-

principal conflict of interests between controlling shareholders and minority shareholders

Denis and McConnell (2003) propose improving IGMs (ownership structure, board of

directors and supervisory board) and external governance mechanisms (EGMs) (corporate

control, legal environment and market development). However, in the context of China,

EGMs such as corporate control and market development are underdeveloped and state

ownership remains for most Chinese listed firms. Even reform of EGMs is an important issue

but arguably a prerequisite for establishment of EGMs is to establish a series of effective

IGMs because they play a substantial role at the juncture of corporate governance

development in China (Hu et al., 2010).

Using a panel data set of 117 companies with 540 firm-year observations during

2001–2005, this paper examines whether audit quality for Chinese listed companies is

associated with IGMs. The results reveal that foreign ownership and the number of

professional supervisors are positively related to audit quality, but the size of the supervisory

board shows a negative correlation. Other IGMs including state ownership, the size of the

6

board of directors, the number of independent directors and the frequency of each of board

and supervisory meetings are found not to be associated with audit quality.

In the context of studying the principal-principal agency conflict of interest between

controlling and minority shareholders the contribution of this paper is twofold. First, prior

literature incompletely uncovers the impact of concentrated ownership and two-tier board

system on audit quality. This paper provides a comprehensive evaluation of independent and

interdependent effects of IGMs of Chinese characters (i.e., highly concentrated state

ownership, board of directors and supervisory board) and investigates how these IGMs

jointly affect audit quality in China. Second, this paper considers the improvement of legal

environment as one of EGMs proposed by Denis and McConnell (2003). Thereby data was

selected during an important regulatory reform period between 2001 and 2005. Within this

period, The Guidelines for Introducing Independent Directors to the Board of Directors of

Listed Companies (The Guidelines) was introduced in August 2001 and mandated by 30 June

2003, and The Code of Corporate Governance for Listed Companies in China (The Code)

was promulgated in January 2002. The improvement on legal environment affords a good

opportunity to examine the relationship between company‟s IGMs and it‟s the decision for

audit quality choice.

The remainder of this paper is organized as follows. The following section provides

an overview of the literature on audit quality in China and develops three sets of hypotheses

in accordance with the IGMs to be tested. Section 3 outlines the research method and

describes the data, while Section 4 presents the results of the analysis and discusses the

findings. Section 5 discusses the implications of the findings and notes the paper‟s

limitations and future research ideas.

7

2. Literature and hypotheses

Study of corporate governance and audit quality has been drawing attention in China recently.

However, none of these studies includes IGMs in a comprehensive way. For example, Chan

et al. (2007) investigate whether the demand for quality-differentiated audits by listed

Chinese firms is related to changes in state or institutional ownership structure. Their results

suggest that a decrease in state ownership and a corresponding increase in institutional

ownership results in demand for higher quality auditing by the firms. They conclude that

managers of listed firms have incentives to supply credible accounting information through

quality audits when the institutional features became absent. Thus, the introduction of large

institutional shareholders represents a sound development in terms of economic reform in

China. Lin and Liu (2009a) examine the association between Chinese listed firms‟ internal

corporate governance mechanisms and their auditor switching decisions. Their results show

that firms with higher ownership concentration and firms with CEO duality are more likely to

switch to a smaller auditor, and this downward switching reduces audit quality and allows the

controlling shareholder to sustain opaque gains. In a similar vein, Lin and Liu (2009b) use

audit firm size as a proxy for audit quality and investigate the determinants of auditor choice

in China in respect of their corporate governance mechanisms. They find that firms with

higher ownership concentration and with smaller supervisory board or CEO duality are less

likely to hire a higher-quality audit firm. Lin et al. (2009) study how investors respond to

audit quality and auditor switches in the Chinese context. Their findings suggest that firms

with positive abnormal earnings, good audit quality and upward auditor switching are

positively correlated with firms‟ earnings response coefficients. Liu et al. (2011) study the

effects of the two types of connection (firm-level connections derived from state ownership

and personal connections developed through management affiliations with the external

8

auditor) and their joint effect on audit quality. Their results suggest that state ownership and

management affiliations with the external auditor impair auditor independence.

However, as alluded to earlier, these studies lack reflection of the full range of IGMs

within the Chinese context. For instance, proxies for the proportions of state and foreign

ownership, board independence, board of directors and supervisory board activity, and the

proportion of professional supervisors are absent from Lin and Liu (2009a) and Lin and Liu

(2009b); proxies for the proportion of foreign ownership, board size and independence, board

of directors and supervisory board activity and the proportion of professional supervisors are

absent from Liu et al. (2011); proxies for the proportion of foreign ownership, board

independence, board of directors and supervisory board activity and the proportion of

professional supervisors are absent from Chan et al. (2007). In order to provide a

comprehensive empirical evaluation of the independent and interdependent effects of

different IGMs, this paper investigates how they jointly affect audit quality in the Chinese

context.

2.1 Ownership structure

A dominant feature of concentrated ownership by the state is the non-tradable nature of the

equity ownership, which is held either through direct investment or indirectly through

holdings by domestic institutions. These institutions are entirely or partially owned by either

China‟s central government or its provincial governments. Thus, China‟s privatisation

program is different from that of many other transition economies. In China, state

shareholders are recognised as the controlling shareholders and often seek objectives other

than efficiency or profitability. For example, they may place a high priority on maintaining

social order and affecting wealth redistribution that may favour increasing employment,

rather than considerations of efficiency or profitability for public shareholders (Xu and Wang,

9

1999). Lin and Liu (2009a) argue that the role of auditing in minimising principal-principal

agency costs does not exist in the context of China because the controlling shareholders are

also seized with the power to appoint the auditor. Thus there is motivation to select low-

quality auditors in order to transfer benefits among related parties maintaining their

operations and expropriating the interests of minority shareholders (Felo et al., 2003).

The objective of foreign investors is to maximize profits and their shareholder wealth.

Most of these foreign investors are financial institutions based in developed economies such

as those in Europe, North America, Japan and Hong Kong. They thereby have resources to

analyse firm performance and have experience as well as capability to effect operational and

management changes when profitability and efficiency are poor (Chen et al., 2006b).

Moreover, foreign investors can play active and positive roles in bringing about

improvements in corporate governance, such as by appointing a high-quality auditor. In light

of the above discussion, the first set of hypotheses is formed as follows:

H1a. Ceteris paribus, state ownership is associated with lower audit quality.

H1b. Ceteris paribus, foreign ownership is associated with higher audit quality.

2.2 Board of directors

China has adopted a two-tier board system as a means to promote better governance. This

choice was made in the early 1990s, partly because many directors and their enterprises were

perceived to be engaged in opaque related-party transactions (Jian and Wong, 2010). The

Code, issued in January 2002 by the CSRC and the SETC, reinforces the role that the two

boards (i.e., board of directors and supervisory board) are supposed to play in corporate

governance. It gives particular attention to aspects of the boards. Since 2003 at least one-third

of the directors on the board of directors has been required to be independent. Independence

is required from both the listed company that appoints them and its major shareholders. The

10

Code also requires that for these directors, their role in the listed company is limited to that of

an independent director. Independence is argued to be important due to the behavioural

motivations that flow from it, or rather from the lack of it. From this perspective, independent

directors work in the best interests of the minority shareholders in order to maintain their own

good reputation in society (Fama and Jensen, 1983). This suggests that both larger boards and

those with a higher proportion of independent directors will have more individuals possessing

these incentives, improving the effectiveness of corporate governance and transparency of

disclosures in a sensitive area such as related party transactions.

Prior literature suggests that independent directors are effective in monitoring the

performance of management because they do not have a financial interest in the company in

the form of shares or psychological ties to management. As such, they are expected to

challenge management objectively and support the auditor (Beasley, 1996; Carcello et al.,

2002; Klein, 2002; Abbott et al., 2003; Abbott et al., 2004; Bedard and Johnstone, 2004; Boo

and Sharma, 2008). For example, Carcello et al. (2002) and Abbott et al. (2003) find a

positive association between the proportion of independent directors and audit fees and infer

that higher audit quality results. Bedard and Johnstone (2004) argue that higher proportions

of independent directors on the board and audit committee are more likely to provide vigilant

oversight of the financial reporting process, and their result also supports this argument.

To extend this argument, board meetings can indicate the level of diligence exercised

by directors (Zaman et al., 2011) and is higher activity expected to work as a good means to

discuss and solve the most widely shared problem that directors face. Hence the number of

board meetings represents an important resource in improving the effectiveness of a board

(Conger et al., 1998). Carcello et al.‟s (2002) results support higher board meeting frequency

indicating a higher level of control in the company, leading to higher audit fees. Based on a

consideration of above arguments, the second set of hypotheses is formed as follows:

11

H2a. Ceteris paribus, the size of the board of directors is positively related to audit

quality.

H2b. Ceteris paribus, the number of independent directors on the board of directors is

positively related to audit quality.

H2c. Ceteris paribus, the frequency of meetings of the board of directors is positively

related to audit quality.

2.3 Supervisory board

Dahya et al. (2003) outline the range of competencies required for a supervisory board to

effectively fulfil its stated roles. The Code identifies four distinct types of roles that

supervisory boards may undertake, depending on the independence and competencies of the

board‟s members; namely honoured guest, friendly advisor, censored watchdog, or

independent watchdog. The role of supervisory board independent watchdog requires that

members on the supervisory board have the necessary competencies in terms of knowledge

and experience to act with expertise and sufficient independence. Logically, this type of

supervisory board has a larger number of members with appropriate professional knowledge

or work experience and hence should be in a better position to improve corporate governance.

Chen (2005) argues that larger supervisory boards enhance their monitoring role. Her finding

confirms a positive correlation between the size of the supervisory board and the level of

corporate governance in Chinese companies. Lin and Liu (2009b) use the size of the

supervisory board as a proxy to monitor the strength of this board. Their finding indicates that

if there is a large supervisory board that is relatively independent from the board of directors

and the management, the firm is motivated to engage a higher-quality auditor to enhance the

supervision or monitoring role. Furthermore, frequent meetings of the supervisory board are

expected to improve the effectiveness and efficiency of the board (Conger et al., 1998), and

12

are more likely to reduce opaque related-party transactions. Accordingly, the third set of

hypotheses is formed as follows:

H3a. Ceteris paribus, the size of the supervisory board is positively related to audit

quality.

H3b. Ceteris paribus, the number of supervisors with professional knowledge or work

experience on the supervisory board is positively related to audit quality.

H3c. Ceteris paribus, the frequency of board meetings of supervisory boards is

positively related to audit quality.

3. Research method

3.1 Sample and data

The data are derived from two main sources. First, the CSRC requires that all listed

companies in China publish information regarding their stock issues, half-year reports, an

annual report and reports in respect of important events. Annual reports are chosen for this

paper as both financial and non-financial data (i.e., ownership structure and board

composition) can be extracted from them. Second, the remaining financial data are sourced

from the China Stock Market Finance Database (CSMAR-A) and the Trading Database

(CSMAR-T) produced by the Shenzhen Guotaian Information Technology Co., Ltd.

This paper focuses on the non-financial sector A-share companies listed on either the

SHSE or the SZSE. In order to test the effects of various types of ownership (i.e., high levels

of state and foreign investor ownership), the sample of companies is divided into three groups:

A-share, AB-share, and AH-share companies. A-share companies are companies that have

issued A-shares1 only, and are listed on the domestic stock exchanges. AB-share companies

are those that have issued both A-shares and B-shares,2 with an initial A-share offering. They

are also listed on the domestic stock exchanges in China. However, AH-share companies are

13

those that have issued both A-shares and H-shares3

and have floated their shares

simultaneously on the Hong Kong Stock Exchange and one of China‟s two mainland stock

exchanges.

INSERT FIGURE I ABOUT HERE

According to the rule-of-thumb of Green (1991),4

a sample size of 117 listed

companies was selected from the listed companies included in China‟s Shanghai SSE1805

and Shenzhen SSE1006 for the period from 2001 to 2005. This was achieved through use of a

stratified sampling method. As shown in Figure I, 45 companies7 were randomly selected

from the A-share group, and 42 companies were randomly selected from the AB-share group.

There were only 30 eligible companies listed on both the Hong Kong Stock Exchange and

one of the two mainland Chinese stock exchanges in 2005. For this reason, all of these

companies were selected for the sample.

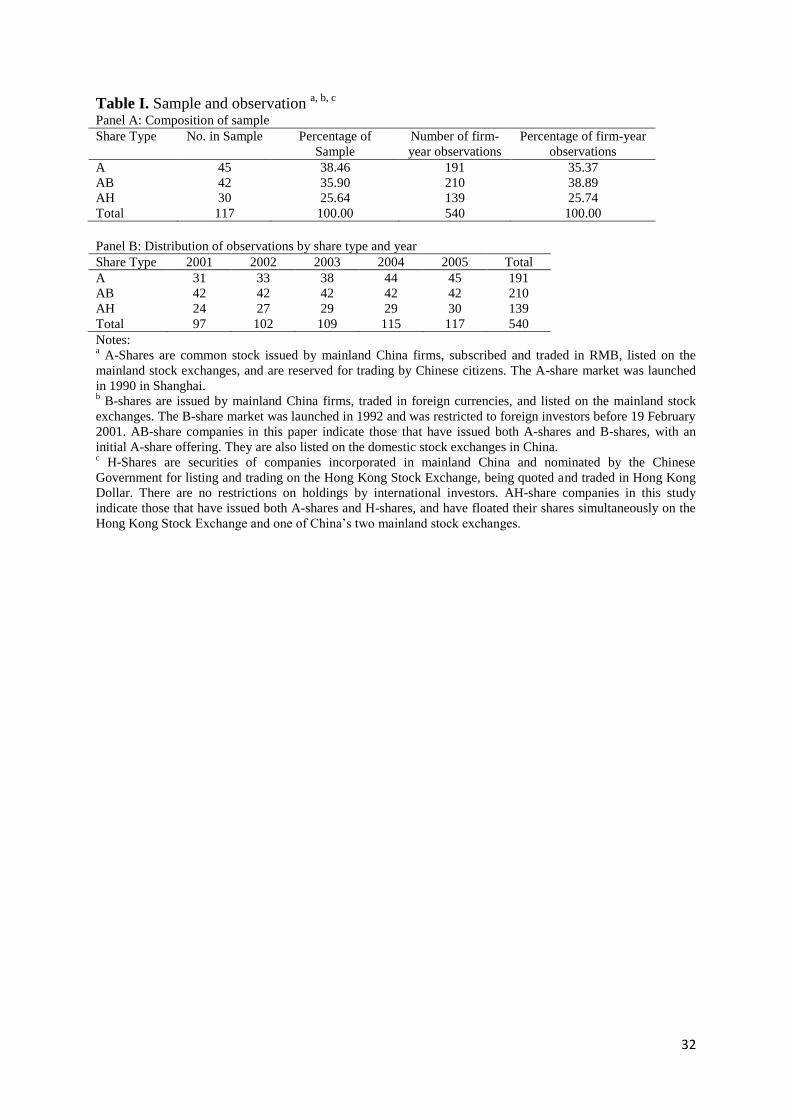

INSERT TABLE I ABOUT HERE

As shown in Table I Panel A, the sample consists of 117 companies listed on the

SHSE and the SZSE in 2005 (45 A-share, 42 AB-share and 30 AH-share companies),

representing weights of 38.46%, 35.9% and 25.64%, respectively, in the sample. Table II

Panel B shows that the panel dataset is unbalanced because some companies were listed after

2001. Over the five-year period from 2001 to 2005, there were 97, 102, 109, 115 and 117

listed companies within the sample frame. This results in the sample data set having a total

of 540 firm-year observations.

3.2 Dependent variable

DeAngelo (1981) proposes that the independence of an auditor has positive correlation with

the probability of the auditor finding and reporting misstatements or irregularities in the

financial statements (i.e., providing a high-quality audit). Independence is particularly

14

relevant to larger auditors, such as members of Big 4 which want to protect their reputation

and avoid costly litigation (Francis and Krishnan, 1999; Francis and Yu, 2009). Prior studies

have substituted audit firm size as a common surrogate for audit quality (e.g., DeAngelo,

1981; Moore and Scott, 1989; Becker et al., 1998; Lennox, 1999, 2005; Kane and Velury,

2004; Lee et al., 2004; Mansi et al., 2004; Lin and Liu, 2009b; Lennox and Pittman, 2010)

because large auditors possess a higher degree of independence and expertise. The Big 4

audit firms is used as the proxy for audit quality (AQ) in this paper.8 The dichotomous

dependent variable–AQ is coded as 1 if the firm is audited by Big 4 audit firm, otherwise

coded as zero.

3.3 Independent variables

The independent variables used to examine the factors that are expected to be associated with

audit quality are divided into three main categories. The first category, ownership structure,

consists of state ownership (STATE), which represents the proportion of shares held by the

state and foreign ownership (FOREIGN), which measures the proportion of shares held by

foreign investors. The second category, board of directors, comprises BSIZE, which

represents the number of directors on the board of directors; INPD, which represents the

number of independent directors on the board of directors and BDMEET, which represents

the number of meetings held by the board of directors in the fiscal year. The third category,

supervisory board characteristics, consists of SBSIZE, which represents the number of

supervisors on the supervisory board, PROFSB which represents the number of supervisors

with professional knowledge or work experience and SBMEET, which represents the number

of meetings held by the supervisory board in the fiscal year.

15

3.4 Control variables

Control variables include return on assets (ROA), Tobin‟s Q (TOBINSQ), firm size (FSIZE)

and firm age (AGE). ROA is equal to a fiscal year's net income divided by total assets, which

provides an indication of how efficient management is at using its assets to generate earnings.

Tobin‟s Q (TOBINSQ) is equal to the market value of stock and the book value of debt

divided by the book value of total assets, which reveals the value investors assign to a firm‟s

tangible and intangible assets based on predicted future revenue and cost streams. Firm size

(FSIZE) is measured by the natural logarithm of total assets, which is often found to have a

significant impact on IGMs (e.g., Chan et al., 2007; Boo and Sharma, 2008). Firm age (AGE)

measures the number of years since initial listing.

In addition, dummy variables representing year effects (YEARDUMMY) and

controlling for listing status (SHAREDUMMY) are included in alternative analyses.

3.5 Model specification

Based on the three sets of hypotheses presented in this paper and the dichotomous nature of

the dependent variable, the logistic regression model to be empirically investigated is as

follows, where the variables are as defined the previous section:

it

4

1l

2

1kkl

4

1jitjit8it7

it6it5it4it3it2it1it

SHAREDUMMYYEARDUMMYCONTROLSSBMEETPROFSB

SBSIZEBDMEETINDPBSIZEFOREIGNSTATEAQ

This model is useful when examining the correlation between the probability of

employing an auditor assumed to provide a greater likelihood of high audit quality and the

factors of IGMs as follows:

1)1()Pr('

itjjx

it ex

16

where, )Pr( itx is the probability that the observation firm i will fail at time t; itjx is a 1j vector

of predictor observations for the ith observation at time t; 'j is a j1 vector of coefficient

estimates.

As shown in Table II Panel A, there are no Spearman correlations between

independent variables that reach .8. However, multicollinearity may still be a concern, even

where the bivariate correlation coefficients are low (Gujarati, 2003). Hence, the degree of

multicollinearity is examined through estimation of Variance Inflation Factors (VIF).9 The

results, reported in Table II Panel B, highlight that the largest VIF is 1.97 while the remainder

are below 1.68. Thus, there is no evidence of a serious multicollinearity problem being

present in the regression model.

INSERT TABLE II ABOUT HERE

4. Results and discussion

4.1 Descriptive statistics

The descriptive statistics presented in Table III Panel A provide a longitudinal profile of the

key variables. With respect to ownership structure, state ownership (STATE) displays a

declining pattern from 68%, 67%, 66%, 62% and 61% during 2001 to 2005 respectively. The

mean ratio of STATE is 65%, which indicates that state ownership continues to maintain a

dominant role. In contrast, the mean foreign ownership (FOREIGN) is only 14%. With

respect to the board of directors, the means of board size (BSIZE) and number of independent

directors (INDP) are 10.41 and 2.93 respectively, which indicates that the mean proportion of

independent directors is around 28.15%. In more detailed, this proportion can be calculated

each year as 9.87% in 2001, 24.55% in 2002, 33.21% in 2003, 34.58% in 2004 and 34.79%

in 2005. These proportions suggest that appointing independent directors was relatively

uncommon before 2002. However, a rapid growth ratio of independent directors occurred

17

between 2001 and 2003, but this growth virtually ceased between 2003 and 2005. Hence the

sample companies only just satisfy the minimum one-third ratio nominated by The Guidelines.

Examining the supervisory board, the means for supervisory board size and professional

supervisors are 4.59 and 1.86 respectively, and these numbers are well below the average size

of board of directors and number of independent directors. Regarding the control variables–

ROA and TOBINSQ, the means are .08 and 1.16 respectively. The mean TOBINSQ shows

that the market value of equity of the sampled companies is high due to surging stock prices.

I suggest that these listed companies utilize the stock market as a means to benefit the

controlling shareholders and expropriate the interests of minority shareholders, which is

indicated by the poor ROA.

INSERT TABLE III ABOUT HERE

4.2 Regression analyses

Table IV provides the regression results of logistic models that examine the three categories

of IGMs concurrently. Results are provided for analyses that exclude year and share-type

effects [model (1)], include year effect but exclude share-type effect [model (2)], include

share-type effect but exclude year effect [model (3)] and include all variables [model (4)].

The model fit is good for each model, reporting pseudo R2s of 16.17%, 16.6%, 26.83% and

26.98% respectively. The Wald 2 statistics for all models indicate that statistically

significant components of the variation in the chosen measure of AQ are explained by

variation in the set of independent variables.

INSERT TABLE IV ABOUT HERE

Regarding the first set of hypotheses, the coefficients for state ownership (β1) are

insignificant at the 5% level for all models. Thus, Hypothesis 1a is not supported. In the

context of China, state shares are still retained by state asset management bureaus (AMBs) or

their agencies, and are not usually allowed to be publicly traded in the market. This highly

18

concentrated ownership (65% on average) creates principal-principal agency problems. The

principal owner is the state, representing all Chinese people (Chan et al., 2007). The

management or agents represents multi-level AMBs (i.e., state AMBs, provincial AMBs, and

their agents). According to agency theory, management or agents will serve the best interests

of the owners. Due to lack of a clear party of ownership, no management or agent has an

adequate motivation to achieve profit maximization for the principal owner – all Chinese

people (Chan et al., 2007). From the results I infer that the controlling party for state shares

has no incentive to engage a high-quality auditor for the company.

The coefficients for foreign ownership (β2) are positively significant at the .1% level

for models (1) and (2), and at the 10% level for models (3) and (4). These findings are

consistent with Hypothesis 1b and suggest that the higher the proportion of equity owned by

foreign investors, the more likely the engagement of a high-quality auditor. I infer a

motivation to secure benefits and not have them expropriated by other parties.

In respect of the second set of hypotheses, the coefficients for board size (β3) are

insignificant at the 5% level for all models. Thus, Hypothesis 2a is not supported. The state/

provincial AMB or their agency relies on control over the board of directors to preserve their

property rights. But arguably most directors actually represent the interests of the state

because they are appointed and remunerated by the various levels of government according to

their administrative rankings rather than their ability (Xu and Wang, 1999; Zhou and Wang,

2000). Hence they may have insufficient managerial ability to monitor management‟s

behaviour. Furthermore, the state, through its control over the board of directors, may seek

objectives other than profit maximization and place a priority on maintaining social order or

reducing unemployment (Xu and Wang, 1999).

The coefficients for the number of independent directors (β4) are insignificant at the

5% level for all models. Thus, Hypothesis 2b is not supported. In the context of China, the

19

key problem of board independence is related to the directors and managers. Most directors

are insiders or executive directors, and listed companies on average only just meet the one-

third ratio of independent directors required by The Guidelines since 2003. Most independent

directors are appointed by the board members or controlling shareholders, hence they owe

their loyalty and patronage to their appointers (Tan and Wang, 2007). As a consequence, the

independent directors of Chinese listed companies may demonstrate limited independence

and easily become „window dressing‟ or „symbolic‟ as board members (Luan and Tang,

2007).

The coefficients for board meeting activity (β5) are insignificant at the 5% level on all

models. Thus, Hypothesis 2c is not supported. This finding is not consistent with Conger et al.

(1998) and Carcello et al. (2002). The frequency of board meetings may be attributable to

many reasons, such as financial distress or controversial decisions on illegal or questionable

activities (Vafeas, 1999; Chen et al., 2006a) and does not necessarily work as a means to

enhance corporate governance.

Regarding the third set of hypotheses, the coefficients for supervisory board size (β6)

are negative and hence opposite to the expected sign as I hypothesized and are inconsistent

with the findings of Lin and Liu (2009b). Hence even though they are significant at the 10%

level in model (1), at the 5% level in model (2) the significances cannot be used to support

Hypothesis 3a. I speculate that the supervisory boards of Chinese listed companies have

tended to become „censored watchdogs‟ in the words of Dahya et al. (2003) during a period

when rapid corporate expansion and the dominance of the board of directors has occurred.

Xiao et al. (2004, p. 47) concluded that supervisory board members describe their behaviour

as where “You sometimes have to open one eye and close the other”. If the „censored

watchdog‟ is the role of the supervisory board, then perhaps what is occurring is that the

more qualified the supervisory board members are, the greater the internal effort made to

20

censor or review works about earnings management and tunneling, which could include

information deemed sensitive to the board of directors and controlling shareholders. In reality,

these supervisory board members could be regarded as „rubber stamp‟ supervisors.

The coefficients for professional supervisors on the supervisory board (β7) are

positively significant at the 1% level in models (1), (2) and (4), and at the 5% level in model

(3). Thus, Hypothesis 3b is supported. This finding suggests that professional supervisors are

relatively independent from management and the board of directors (Lin and Liu, 2009b), and

advocate for high-quality auditors as a means to improve the corporate governance of listed

companies.

The coefficients for supervisory board meetings (β8) are insignificant at the 5% level

on all models. Thus, Hypothesis 3c is not supported. Once more, as with the frequency of the

meetings of board of directors, these results confirm the inferences of Vafeas (1999) and

Chen et al. (2006a) reveal the reason for companies having more board meetings during

periods of financial distress or during times of controversial decisions.

In terms of control variables, the coefficients for ROA are positively significant at the

10% in model (3) and at the 5% level in model (4), but insignificant in models (1) and (2).

The coefficients for TOBINSQ are positively significant at the 1% level in model (1) and at

the 5% level in model (2), but insignificant in models (3) and (4). These findings suggest that

listed companies with better profitability and market performance are more likely to hire a

high-quality auditor. The coefficients for FSIZE are positively significant at least the 5%

level in all models. The coefficients for AGE are positively significant at the 10% level in

model (1) and at the 5% in model (2), but insignificant in models (3) and (4). These findings

suggest that listed companies of larger size or longer listing status are more likely to hire a

high-quality auditor.

21

Concerning year and share-type effects, the results indicate that there are no year

effects, and positively significant share-type effect in models (3) and (4). This suggests that

listed companies that issue both A- and B-shares or A- and H-shares have better are more

likely to choose a high-quality auditor than listed companies that issues A-shares only.

4.3 Sensitivity test

A sensitivity test is used as an alternative technique to examine the regression model and the

empirical results. According to composition of the sample presented in Panel A Table I, I

perform the regression model used in Table IV to investigate the association of the IGMs on

each of the three share-types separately. These findings may differ from the main results

because the proportions of ownership and monitoring power of the board of directors and

supervisory board of each listing status are diversified. The smaller sample sizes need to be

considered in interpreting the results of this secondary analysis.

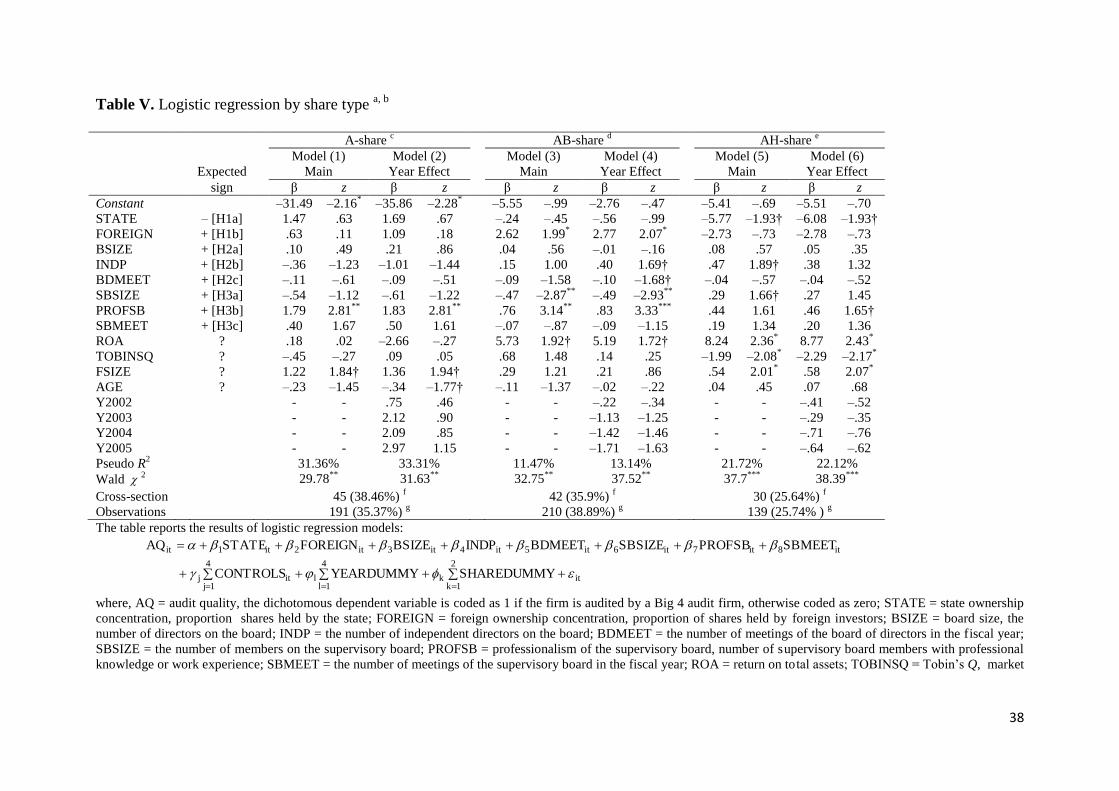

INSERT TABLE V ABOUT HERE

For the companies that issue A-shares only, as shown in Table V, the results are

consistent with the findings in Table IV, except for insignificant coefficients for foreign

ownership on models (1) and (2). This finding suggests that foreign ownership in listed

companies with A-shares is only 2% in comparison with 75% of state ownership (as shown in

Panel B of Table III), and this small stake reduces the efficiency of foreign investors to

actively enhance corporate governance (Chen et al., 2006b).

Regarding the companies that issue A- and B-shares, as shown in Table V, the results

are consistent with the findings in Table IV, except for a positively significant coefficient for

independent directors in model (4), a negatively significant coefficient for board meetings in

model (4), and negatively significant coefficients for supervisory board size in models (3) and

(4). The positively significant coefficient for independent directors adds weight to the agency

22

argument of (Fama and Jensen, 1983) that independent directors of these companies are

motivated to work in the best interests of shareholders in order to maintain their good

personal reputation, and also supports Chen and Jaggi‟s (2000) findings that independent

directors will improve corporate governance even in countries that have fewer incentives for

transparency, such as China. The negatively significant coefficients for board meetings and

supervisory board size suggest that the IGMs of board of directors and supervisory board are

ineffective in enhancing corporate governance, and that the effectiveness of corporate

governance can be improved by increasing the proportion of foreign equity.

In respect of the companies that issue A- and H-shares, as shown in Table V, the

results are consistent with the findings in Table IV, except for negatively significant

coefficients for state ownership in models (5) and (6), positively significant coefficients for

independent directors and supervisory board size in model (5) and insignificant coefficients

for foreign ownership in models (5) and (6). The negative coefficients for state ownership are

consistent with the findings of Lin and Liu (2009a) suggesting controlling shareholders are

less motivated to hire high-quality auditors in order to transfer benefits among related parties.

The discussion in the above two paragraphs in terms of the positive coefficient for

independent directors and the insignificant coefficient for foreign ownership can be applied to

the findings of AH-share companies.

5. Conclusion

The objective of this paper is to investigate whether the audit quality of Chinese listed

companies is associated with IGMs. I used a panel data set comprising 117 companies with a

total of 540 firm-year observations between 2001 and 2005. The results suggest that foreign

ownership and the number of professional supervisors are positively associated with audit

quality, however the size of the supervisory board revealed an unexpected negative

23

association. Other IGMs including state ownership, the size of board of directors, the number

of independent directors, the frequency of board meetings, and the frequency of supervisory

board meetings were found to have no association with audit quality.

At least two implications can be drawn from this paper. First, I believe that the

corporate governance reforms regarding the board of directors and the supervisory board of

Chinese listed companies have not yet been sufficient to ensure that they properly fulfil their

roles of oversight. Rather, they are perhaps playing more a „window dressing‟ or „rubber

stamp‟ or „symbolic‟ role within the current two-tier corporate governance system. Second,

despite recent reforms, such as mandating the introduction of independent directors and

minority foreign ownership after China‟s entrance into the WTO in 2001, the dominance and

influence of state ownership has not changed. Highly concentrated state ownership appears to

have resulted in ineffective IGMs among Chinese listed companies. For example, the

supervisory boards consist of a high proportion of insiders who may be political officers of a

certain level of a government organ, leaders of a non-functional trade union, or close friends

and allies of senior executives. These supervisors, appointed by the senior executives who

also determine their compensation, have virtually no independence from management. In

order to overcome this problem, Tam (2000) suggests that the proportion of inside

supervisors be kept below 20%, and a set of functional committees, such as nomination,

remuneration and audit, should be established to remove some of the grounds on which

insider control has been built.

Other than these innovations, changes could be made to The Company Law and The

Code. The supervisory board could be given greater power to hire and remove directors. This

authority would improve the supervisor‟s status within and outside the company. Moreover,

The Company Law could prescribe legal responsibilities for the supervisory board so that

supervisors would be statutorily obliged to undertake their duties diligently. On the other

24

hand, The Company Law could clarify an obligation of the board of directors to provide

supervisors with timely information regarding the firm so that the supervisory board can

effectively exercise its monitoring function.

There are several limitations of this paper. The first limitation is that I only employed

a dichotomous dependent variable (Big 4 audit firm) as the proxy for audit quality due to

limited data. However, audit quality can also be surrogated by other measures, such as audit

fees (O'Sullivan, 2000; Boo and Sharma, 2008; Zaman et al., 2011), auditor switching (Lin

and Liu, 2009a; Lin et al., 2009) and modified audit opinions (Liu et al., 2011). The second

limitation regards the data set used for this paper. Although the sample was selected from the

Shanghai SSE 180 and the Shenzhen SSE 100, it may not be generalizable to all listed

companies in China. Additionally the proxies for IGMs may not differentiate well the

characteristics of sound corporate. Due to these limitations, the findings of this paper should

be interpreted with care. Future research can be undertaken that improves the degree of

confidence by extending sample sizes in the coming years and by introducing better and

additional proxies for audit quality such as audit fees and audit switching.

Despite these limitations, this is the first study to provide a comprehensive empirical

analysis of the key parameters that underlie China‟s IGMs impact on audit quality during the

important period of regulatory change and organizational reform between 2001 and 2005.

This paper also fills a gap in the literature concerning the impact on audit quality choice of

high state ownership concentration and the two-tier board corporate governance system.

Notes 1A-shares are common stock issued by mainland China firms, subscribed and traded in RMB, listed on the

mainland stock exchanges, and are reserved for trading by Chinese citizens. The A-share market was launched

in 1990 in Shanghai. 2 B-shares are issued by mainland China firms, traded in foreign currencies, and listed on the mainland stock

exchanges. The B-share market was launched in 1992 and was restricted to foreign investors before 19 February

2001.

25

3

H-shares are securities of companies incorporated in mainland China and nominated by the Chinese

government for listing and trading on the Hong Kong Stock Exchange, being quoted and traded in HKD. There

are no restrictions on holdings by international investors. 4 Green (1991) suggests that the power for a test of a multiple correlation with a medium effect size is

approximately 0.80 if N ≥ 50 + 8m, where N is number of subjects, and m is the number of predictors. Thus, the

sample size should be at least 114 (N = 50 + 8 x 8). 5 The Shanghai SSE180 Index was created by restructuring and renaming the SSE30 Index. Through scientific

and objective methods it selects constituents that best represent the market. The SSE is a benchmark index

reflecting the Shanghai market and serves as a performance benchmark for investment and a basis for financial

innovation. 6 The Shenzhen SSE100 is a benchmark index reflecting performance in the Shenzhen market and serves as a

performance benchmark for investment and as a basis for development of financial innovations. 7 These samples are randomly selected from A-share companies included in the Shanghai SSE180 and the

Shenzhen SSE100 after removing dual listed companies (these being either AB-share companies or AH-share

companies). 8According to Chinese government regulation, the international Big 4 accounting firms, i.e., PwC, KPMG,

Deloitte and Ernst & Young, were not permitted to provide auditing services before 2005 in China unless they

became joint-ventures or partnerships with large domestic Chinese CPA firms. Thereby, the Big 4 audit firms in

this paper comprise PwC ZhongTian, KPGM Huazhen, Deloitte Huayong and Ernst & Young Hua Ming. 9 The critical value of the VIF to test for multicollinearity is 10. Gujarati (2003) suggests that there is no

evidence of multicollinearity unless the VIF of a variable exceeds 10. All values used in this paper are well

below this critical level.

26

References

Abbott, L.J., Parker, S. and Peters, G.F. (2004), “Audit committee characteristics and

restatements”, Auditing: A Journal of Practice and Theory, Vol. 23 No.1, pp. 69–87.

Abbott, L.J., Parker, S., Peters, G.F and Raghunandan, K. (2003), “The association between

audit committee characteristics and audit fees”, Auditing: A Journal of Practice and

Theory, Vol. 22 No.2, pp. 17–32.

Al-Ajmi, J. (2009), “Audit firm, corporate governance, and audit quality: evidence from

Bahrain”, Advances in Accounting, Vol. 25 No. 1, pp. 64–74.

Beasley, M.S. (1996), “An empirical analysis of the relation between the board of director

composition and financial statement fraud”, The Accounting Review, Vol. 71 No. 4,

pp. 443–465.

Becker, C.L., DeFond, M.L., Jiambalvo, J. and Subramanyam, K.R. (1998), “The effect of

audit quality on earnings management”, Contemporary Accounting Research, Vol. 15

No. 1, pp. 1–24.

Bedard, J.C. and Johnstone, K.M. (2004), “Earnings manipulation risk, corporate governance

risk, and auditors' planning and pricing decisions”, The Accounting Review, Vol. 79

No. 2, pp. 227–304.

Boo, E. and Sharma, D. (2008), “Effect of regulatory oversight on the association between

internal governance characteristics and audit fees”, Accounting and Finance, Vol. 48

No. 1, pp.51–71.

Cadbury Report. (1992), Report of the Committee on the Financial Aspects of Corporate

Governance: The Code of Best Practice, Gee Professional Publishing, London.

Carcello, J.V., Hermanson, D.R., Neal, T.L. and Riley Jr., R.A. (2002), “Board characteristics

and audit fees”, Contemporary Accounting Research, Vol. 19 No. 3, pp. 365–384.

Chan, K.H., Lin, K.Z. and Zhang, F. (2007), “On the association between changes in

corporate ownership and changes in auditor quality in a transitional economy”,

Journal of International Accounting Research, Vol. 6 No. 1, pp. 19–36.

Chen, C.J.P. and Jaggi, B. (2000), “Association between independent non-executive directors,

family control and financial disclosures in Hong Kong”, Journal of Accounting and

Public Policy, Vol. 19 No. 4/5, pp. 285–310.

Chen, G., Firth, M., Gao, D.N. and Rui, O.M. (2006a), “Ownership structure, corporate

governance, and fraud: evidence from China”, Journal of Corporate Finance, Vol. 12

No. 3, pp.424–448.

Chen, G., Firth, M. and Rui, O.M. (2006b), “Have China's enterprise reforms led to improved

efficiency and profitability?”, Emerging Markets Review, Vol. 7 No.1, pp. 82–109.

27

Chen, J.J. (2005), “China's institutional environment and corporate governance”, Corporate

Governance: A Global Perspective Advances in Financial Economics, Vol. 11, pp.

75–93.

Conger, J.A., Finegold, D. and Lawler III, E.E. (1998), “Appraising boardroom performance”,

Harvard Business Review, Vol. 76 No. 1, pp. 136–148.

Dahya, J., Karbhari, Y., Xiao, J.Z. and Yang, M. (2003), “The usefulness of the supervisory

board report in China”, Corporate Governance: An International Review, Vo. 11 No.

4, pp. 308–321.

DeAngelo, L.E. (1981), “Auditor size and audit quality”, Journal of Accounting and

Economics, Vol. 3 No.3, pp. 183–199.

DeFond, M.L. (1992), “The association between changes in client firm agency costs and

auditor switching”, Auditing: A Journal of Practice and Theory, Vo. 11 No. 1, pp.16–

31.

DeFond, M.L., Wong, T.J. and Li, S. (2000), “The impact of improved auditor independence

on audit market concentration in China”, Journal of Accounting and Economics, Vol.

28 No. 3, pp. 269–305.

Denis, D.K. and McConnell, J.J. (2003), “International corporate governance”, Journal of

Financial and Quantitative, Vol. 38 No. 1, pp. 1–36.

Dharwadkar, B., George, G. and Brandes, P. (2000), “Privatization in emerging economies:

an agency theory perspective”, Academy of Management Review, Vol. 25 No. 3, pp.

650–669.

Fama, E.F. and Jensen, M.C. (1983), “The separation of ownership and control”, Journal of

Law and Economics, Vol. 26 No. 2, pp. 301–325.

Felo, A.J., Krishnamurthy, S. and Solieri, S.A. (2003), “Audit committee characteristics and

the perceived quality of financial reporting: an empirical analysis”, Working paper,

Penn State Great Valley.

Francis, J.R. and Krishnan, J. (1999), “Accounting accruals and auditor reporting

conservatism”, Contemporary Accounting Research, Vol. 16 No. 1, pp. 135–165.

Francis, J.R. and Yu, M.D. (2009), “Big 4 office size and audit quality”, The Accounting

Review, Vol. 48 No. 5, pp. 1521–1552.

Green, S.B (1991), “How many subjects does it take to do a regression analysis?”,

Multivariate Behavioral Research, Vol. 26 No. 3, pp. 499–510.

Gujarati, D.N. (2003), Basic Econometrics, 4th edn. McGraw-Hill, New York .

Gul, F.A. and Goodwin, J. (2010), “Short-term debt maturity structures, credit ratings, and

the pricing of audit services”, The Accounting Review, Vol. 85 No. 3, pp. 877–909.

28

Holm, C. and Laursen, P.B. (2007), “Risk and control developments in corporate governance:

Changing the role of the external auditor?”, Corporate Governance: An International

Review, Vol. 15 No. 2, pp. 322–333.

Hu, H.W., Tam, O.K. and Tan, M.G-S. (2010), “Internal governance mechanisms and firm

performance in China”, Asia Pacific Journal of Management, Vol. 27 No. 4, pp. 727–

749.

Jensen, M.C. and Meckling, W.H. (1976), “Theory of the firm: managerial behavior, agency

costs, and ownership structure”, Journal of Financial Economics, Vol. 3 No. 4, pp.

305–360.

Jian, M. and Wong, T.J. (2010), “Propping through related party transaction”, Review of

Accounting Studies, Vol. 15 No. 1, pp. 70–105.

Kane, G.D. and Velury, U. (2004), “The role of institutional ownership in the market for

auditing services: an empirical investigation”, Journal of Business Research, Vol. 57

No. 9, pp. 976–983.

Klein, A. (2002), “Audit committee, board of director characteristics, and earnings

management”, Journal of Accounting and Economics, Vol. 33 No. 3, pp. 375–400.

Lee, H.Y., Mande, V. and Ortman, R. (2004), “The effect of audit committee and board of

director independence on auditor resignation”, Auditing: A Journal of Practice and

Theory, Vol. 23 No. 2, pp. 131–146.

Lennox, C. (1999), “Non-audit fees, disclosure and audit quality”, European Accounting

Review, Vol. 8 No. 2, pp. 239–252.

Lennox, C. (2005), “Management ownership and audit firm size”, Contemporary Accounting

Research, Vol. 22 No. 1, pp. 205–227.

Lennox, C. and Pittman, J.A. (2010), “Big five audits and accounting fraud”, Contemporary

Accounting Research, Vol. 27 No. 11, pp. 209–247.

Lin, Z.J. and Liu, M. (2009a), “The determinants of auditor switching from the perspective of

corporate governance in China”, Corporate Governance: An International Review,

Vol. 17 No. 4, pp. 476–491.

Lin, Z.J. and Liu, M. (2009b), “The impact of corporate governance on auditor choice:

evidence from China”, Journal of International Accounting, Auditing and Taxation,

Vol. 18 No. 1, pp. 44–59.

Lin, Z.J., Liu, M. and Wang, Z. (2009), “Market implications of the audit quality and auditor

switches: evidence from China”, Journal of International Financial Management and

Accounting, Vol. 20 No. 1, pp: 35–78.

Liu, J., Wang, Y. and Wu, L. (2011), “The effect of Guanxi on audit quality in China”,

Journal of Business Ethics, Vol. 103 No. 4, pp. 621–638.

29

Luan, C-J. and Tang, M-J. (2007), “Where is independent director efficacy?” Corporate

Governance: An International Review, Vol. 15 No. 4, pp. 636–643.

Mansi, S.A., Maxwell, W.F. and Miller, D.P. (2004), “Does auditor quality and tenure matter

to investors? evidence from the bond market”, Journal of Accounting Research, Vol.

42 No. 4, pp.755–793.

Moore, G. and Scott, W.R. (1989), “Auditors' legal liability, collusion with management, and

investors' loss”, Contemporary Accounting Research, Vol. 5 No. 2, pp. 754–774.

O'Sullivan, N. (2000), “The impact of board composition and ownership on audit quality:

Evidence from large UK companies”, British Accounting Review, Vol. 32 No. 4, pp.

397–414.

Shleifer, A. and Vishny, R.W. (1997), “A survey of corporate governance”, Journal of

Finance, Vol. 52 No. 2, pp. 737–782.

Tam, O.K. (2000), “Models of corporate governance for Chinese companies”, Corporate

Governance: An International Review, Vol. 8 No. 1, pp. 52–64.

Tan, L.H. and Wang, J. (2007), “Modelling an effective corporate governance system for

China's listed state-owned enterprises: Issues and challenges in a transitional economy”,

Journal of Corporate Law Studies, Vol. 7 No. 1, pp. 143–183.

Vafeas, N. (1999), “Board meeting frequency and firm performance”, Journal of Financial

Economics, Vol. 53 No. 1, pp. 113–142.

Watts, R.L. and Zimmerman, J.L. (1986), Positive Accounting Theory, Prentice-Hall:

Englewood Cliffs, NJ.

Xiao, J.Z., Dahya, J. and Lin, Z. (2004), “A grounded theory exposition of the role of the

supervisory board in China”, British Journal of Management, Vol. 15 No. 1, pp. 39–

55.

Xu, X. and Wang, Y. (1999), “Ownership structure and corporate governance in Chinese

stock companies”, China Economic Review, Vol. 10 No. 1, pp. 75–98.

Young, M.N., Peng, M.W., Ahlstrom, D., Bruton, G.D. and Jiang, Y. (2008), “Corporate

governance in emerging economies: a review of the principal-principal perspective”,

Journal of Management Studies, Vol. 45 No. 1, pp. 196–220.

Zaman, M., Hudaib, M. and Haniffa, R. (2011), “Corporate governance quality, audit fees

and non-audit services fees”, Journal of Business Finance and Accounting, Vol. 38

No. 1/2, pp. 165–197.

Zerni, M., Kallunki, J-P. and Nilsson, H. (2010), “The entrenchment problem, corporate

governance mechanisms, and firm value”, Contemporary Accounting Research, Vol.

27 No. 4, pp. 1169–1206.

30

Zhou, M. and Wang, X. (2000), “Agency cost and the crisis of China's SOE”, China

Economic Review, Vol. 11 No. 3, pp. 297–317.

31

FIGURE I. Sampling frame a, b, c, d

H-Share firms

B-Share firms

AH-Share firms 30

selected for sample

AB-Share firms 42

selected for sample

A-Share firms 45 selected for sample

from Shanghai

SSE180 and Shenzhen SSE100

Notes: a A-shares are common stock issued by mainland China firms, subscribed and traded in RMB, listed on the

mainland stock exchanges, and are reserved for trading by Chinese citizens. The A-share market was launched

in 1990 in Shanghai. b B-shares are issued by mainland China firms, traded in foreign currencies, and listed on the mainland stock

exchanges. The B-share market was launched in 1992 and was restricted to foreign investors before 19 February

2001. AB-share companies in this paper indicate those that have issued both A-shares and B-shares, with an

initial A-share offering. They are also listed on the domestic stock exchanges in China. c H-shares are securities of companies incorporated in mainland China and nominated by the Chinese

Government for listing and trading on the Hong Kong Stock Exchange, being quoted and traded in Hong Kong

Dollar. There are no restrictions on holdings by international investors. AH-share companies in this study

indicate those that have issued both A-shares and H-shares, and have floated their shares simultaneously on the

Hong Kong Stock Exchange and one of China‟s two mainland stock exchanges. d

The Shanghai SSE180 Index was created by restructuring and renaming the SSE30 Index. Through scientific

and objective methods it selects constituents that best represent the market. The SSE is a benchmark index

reflecting the Shanghai market and serves as a performance benchmark for investment and a basis for financial

innovation. The Shenzhen SSE100 is a benchmark index reflecting performance in the Shenzhen market and

serves as a performance benchmark for investment and as a basis for development of financial innovations.

32

Table I. Sample and observation a, b, c

Panel A: Composition of sample

Share Type No. in Sample Percentage of

Sample

Number of firm-

year observations

Percentage of firm-year

observations

A

45 38.46 191 35.37

AB

42 35.90 210 38.89

AH

30 25.64 139 25.74

Total 117 100.00 540 100.00

Panel B: Distribution of observations by share type and year

Share Type 2001 2002 2003 2004 2005 Total

A

31 33 38 44 45 191

AB

42 42 42 42 42 210

AH

24 27 29 29 30 139

Total 97 102 109 115 117 540

Notes: a A-Shares are common stock issued by mainland China firms, subscribed and traded in RMB, listed on the

mainland stock exchanges, and are reserved for trading by Chinese citizens. The A-share market was launched

in 1990 in Shanghai. b B-shares are issued by mainland China firms, traded in foreign currencies, and listed on the mainland stock

exchanges. The B-share market was launched in 1992 and was restricted to foreign investors before 19 February

2001. AB-share companies in this paper indicate those that have issued both A-shares and B-shares, with an

initial A-share offering. They are also listed on the domestic stock exchanges in China. c H-Shares are securities of companies incorporated in mainland China and nominated by the Chinese

Government for listing and trading on the Hong Kong Stock Exchange, being quoted and traded in Hong Kong

Dollar. There are no restrictions on holdings by international investors. AH-share companies in this study

indicate those that have issued both A-shares and H-shares, and have floated their shares simultaneously on the

Hong Kong Stock Exchange and one of China‟s two mainland stock exchanges.

33

Table II. Collinearity diagnostics a

Panel A: Spearman matrix

Variables (1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11) (12)

(1) STATE –

(2) FOREIGN –.52***

–

(3) BSIZE –.07† .21***

–

(4) INDP –.10*

.20***

.49***

–

(5) BDMEET –.06 .13**

.03 .17***

–

(6) SBSIZE .13**

.02 .43***

.28***

.02 –

(7) PROFSB .06 .09*

.23***

.23***

.06 .62***

–

(8) SBMEET –.04 .09* –.02 .01 .29

*** .02 .01 –

(9) ROA –.05 –.04 .15***

.08† .04 .14**

.09*

–.07 –

(10) TOBINSQ –.28***

.20***

–.15***

–.30***

–.01 –.08†

–.11**

.13**

–.01 –

(11) FSIZE .05 .25***

.28***

.33***

.06 .17***

.17***

–.06 .10*

–.42***

–

(12) AGE –.17***

.14**

–.15***

.08† .05 –.06 .01 .16***

–.27***

.21***

–.14***

–

Panel B: VIF diagnostic b

STATE FOREIGN BSIZE INDP BDMEET SBSIZE PROFSB SBMEET ROA TOBINSQ FSIZE AGE

VIF 1.37 1.41 1.55 1.59 1.14 1.97 1.68 1.13 1.02 1.51 1.58 1.13

Notes: a STATE = state ownership concentration, proportion shares held by the state; FOREIGN = foreign ownership concentration, proportion of shares held by foreign investors;

BSIZE = board size, the number of directors on the board; INDP = the number of independent directors on the board; BDMEET = the number of meetings of the board of

directors in the fiscal year; SBSIZE = the number of members on the supervisory board; PROFSB = professionalism of the supervisory board, number of supervisory board

members with professional knowledge or work experience; SBMEET = the number of meetings of the supervisory board in the fiscal year; ROA = return on total assets;

TOBINSQ = Tobin‟s Q, market value of stock and book value of debt divided by book value of total assets; FSIZE: firm size, natural logarithm of value of total assets at the

end of fiscal year; AGE: firm age, years since initial listing b The critical value of the VIF to test for multicollinearity is 10. Gujarati (2003) suggests that there is no evidence of multicollinearity unless the VIF of a variable exceeds 10.

All values used in this paper were well below this critical level.

†if p<.10; * if p <.05;

** if p<.01;

*** if p<.001 (two-tailed p-values are used in determining significance)

34

Table III. Descriptive statistics a

Panel A: Statistics by year

2001 2002 2003 2004 2005 All years

Variable Mean Med SD Mean Med SD Mean Med SD Mean Med SD Mean Med SD Mean Med SD

STATE .68 .78 .29 .67 .74 .29 .66 .70 .29 .62 .68 .32 .61 .67 .32 .65 .71 .31

FOREIGN .14 .04 .16 .14 .04 .17 .14 .04 .17 .14 .04 .17 .14 .05 .17 .14 .04 .17

BSIZE 10.13 10 2.78 10.55 11 2.31 10.63 10 2.32 10.44 9 2.4 10.29 9 2.33 10.41 10 2.42

INDP 1 0 1.34 2.59 2 .94 3.53 3 .85 3.61 3 .83 3.58 3 .87 2.93 3 1.38

BDMEET 6.04 6 2.29 8.21 8 3.08 7.39 7 3.31 7.32 7 2.78 7.95 7 3.13 7.41 7 3.03

SBSIZE 4.59 5 1.56 4.6 5 1.57 4.67 5 1.8 4.6 5 1.72 4.49 5 1.69 4.59 5 1.67

PROFSB 1.67 2 .84 1.83 2 .92 1.92 2 1.07 1.91 2 1.1 1.93 2 1.17 1.86 2 1.04

SBMEET 3.46 3 1.51 4.35 4 2.02 3.83 3 2.09 3.33 3 1.74 3.42 3 1.99 3.67 3 1.92

ROA .23 .05 1.75 .03 .04 .17 .05 .05 .04 .06 .06 .07 .05 .05 .08 .08 .05 .75

TOBINSQ 1.47 1.36 .57 1.24 1.18 .41 1.14 1.09 .31 1.03 1.00 .26 .96 .93 .25 1.16 1.07 .41

FSIZE 21.74 21.64 1.04 21.88 21.79 1.02 22 21.89 1.05 22.09 22.05 1.11 22.17 22.15 1.18 21.99 21.88 1.09

AGE 5.37 6 2.73 6.06 6 2.99 6.61 7 3.38 7.21 8 3.7 8.07 9 3.82 6.73 7 3.49

Panel B: Statistics by share type

A-share b

AB-share c

AH-share d

Variable Mean Med SD Mean Med SD Mean Med SD

STATE .75 .89 .30 .59 .71 .35 .60 .60 .19

FOREIGN .02 .00 .07 .12 .06 .14 .33 .36 .12

BSIZE 10.09 9 2.51 10.08 9 2.39 11.35 11 2.1

INDP 2.76 3 1.42 2.68 3 1.44 3.53 4 1.01

BDMEET 6.81 6 2.63 7.57 7 3.28 7.99 8 3.03

SBSIZE 4.52 5 1.44 4.38 3 1.63 4.99 5 1.94

PROFSB 1.74 2 .93 1.69 2 1.03 2.27 2 1.08

SBMEET 3.3 3 1.8 3.92 3.5 2.1 3.79 4 1.7

ROA .07 .06 .05 .03 .04 .13 .17 .05 1.47

TOBINSQ 1.00 .93 .36 1.35 1.26 .43 1.08 1.06 .30

FSIZE 21.74 21.85 .77 21.61 21.63 .81 22.9 22.92 1.31

AGE 4.99 5 3.3 8.98 9 2.32 5.71 6 3.39

Notes: a STATE = state ownership concentration, proportion shares held by the state; FOREIGN = foreign ownership concentration, proportion of shares held by foreign investors;

BSIZE = board size, the number of directors on the board; INDP = the number of independent directors on the board; BDMEET = the number of meetings of the board of

directors in the fiscal year; SBSIZE = the number of members on the supervisory board; PROFSB = professionalism of the supervisory board, number of supervisory board

members with professional knowledge or work experience; SBMEET = the number of meetings of the supervisory board in the fiscal year; ROA = return on total assets;

35

TOBINSQ = Tobin‟s Q, market value of stock and book value of debt divided by book value of total assets; FSIZE: firm size, natural logarithm of value of total assets at the

end of fiscal year; AGE: firm age, years since initial listing bA-shares are common stock issued by mainland China firms, subscribed and traded in RMB, listed on the mainland stock exchanges, and are reserved for trading by Chinese

citizens. The A-share market was launched in 1990 in Shanghai. c B-shares are issued by mainland China firms, traded in foreign currencies, and listed on the mainland stock exchanges. The B-share market was launched in 1992 and was

restricted to foreign investors before 19 February 2001. AB-share companies in this paper indicate those that have issued both A-shares and B-shares, with an initial A-share

offering. They are also listed on the domestic stock exchanges in China. d H-shares are securities of companies incorporated in mainland China and nominated by the Chinese Government for listing and trading on the Hong Kong Stock Exchange,

being quoted and traded in Hong Kong Dollar. There are no restrictions on holdings by international investors. AH-share companies in this study indicate those that have

issued both A-shares and H-shares, and have floated their shares simultaneously on the Hong Kong Stock Exchange and one of China‟s two mainland stock exchanges.

36

Table IV. Logistic regression results a, b

Model (1) Model (2) Model (3) Model (4)

Expected Main Year Effect Share-Type Effect Year & Share-Type Effect

sign β z β z β z β z

Constant –20.10 –6.71***

–19.55 –6.41***

–11.56 –3.47***

–11.37 –3.37***

STATE – [H1a] –.16 –.40 –.24 –.61 –.54 –1.28 –.61 –1.41

FOREIGN + [H1b] 2.38 3.53***

2.26 3.32***

1.82 1.78† 1.87 1.83†

BSIZE + [H2a] .09 1.63 .06 1.08 .05 .92 .04 .62

INDP + [H2b] –.08 –.90 .04 .29 –.09 –.85 –.04 –.27

BDMEET + [H2c] –.01 –.32 –.01 –.28 –.04 –1.17 –.05 –1.23

SBSIZE + [H3a] –.16 –1.85† –.18 –2.03*

–.14 –1.52 –.15 –1.57

PROFSB + [H3b] .39 3.07**

.40 3.12**

.36 2.57*

.36 2.58**

SBMEET + [H3c] .04 .82 .03 .45 .01 .20 –.01 –.03

ROA ? .97 .73 1.29 .92 3.35 1.91† 3.58 2.00*

TOBINSQ ? .97 3.21**

.79 2.39*

.01 .04 –.08 –.21

FSIZE ? .77 6.03***

.77 5.99***

.42 2.98**

.43 3.00**

AGE ? .06 1.99† .09 2.44*

–.03 –.79 –.02 –.42

Y2002 - - –.02 –.06 - - .20 .48

Y2003 - - –.38 –.80 - - –.10 –.19

Y2004 - - –.57 –1.14 - - –.25 –.46

Y2005 - - –.70 –1.34 - - –.24 –.43

ABSHARE - - - - 2.75 6.85***

2.72 6.77***

AHSHARE - - - - 3.57 6.97***

3.56 6.90***

Pseudo R2

16.17% 16.6% 26.83% 26.98%

Wald 2 114.4

*** 117.31

*** 189.83

*** 190.68

***

Cross-section 117 117 117 117

Observations 540 540 540 540

The table reports the results of logistic regression models:

it

4

1l

2

1kkl

4

1jitj

it8it7it6it5it4it3it2it1it

SHAREDUMMYYEARDUMMYCONTROLS

SBMEETPROFSBSBSIZEBDMEETINDPBSIZEFOREIGNSTATEAQ

where, AQ = audit quality, the dichotomous dependent variable is coded as 1 if the firm is audited by a Big 4 audit firm, otherwise coded as zero; STATE = state ownership

concentration, proportion of shares held by the state; FOREIGN = foreign ownership concentration, proportion of shares held by foreign investors; BSIZE = board size, the

number of directors on the board; INDP = the number of independent directors on the board; BDMEET = the number of meetings of the board of directors in the fiscal year;

SBSIZE = the number of members on the supervisory board; PROFSB = professionalism of the supervisory board, number of supervisory board members with professional

knowledge or work experience; SBMEET = the number of meetings of the supervisory board in the fiscal year; ROA = return on total assets; TOBINSQ = Tobin‟s Q, market

37

value of stock and book value of debt divided by book value of total assets; FSIZE: firm size, natural logarithm of value of total assets at the end of fiscal year; AGE: firm

age, years since initial listing

Notes: a In logistic regression model we coded as 1 if the firm is audited by a Big 4 auditor, otherwise coded as 0.

b Two-tailed p-values are used in determining significance: †if p<.10;

* if p <.05;

** if p<.01;

*** if p<.001

38

Table V. Logistic regression by share type a, b

A-share c AB-share

d AH-share

e

Model (1) Model (2) Model (3) Model (4) Model (5) Model (6)

Expected Main Year Effect Main Year Effect Main Year Effect

sign β z β z β z β z β z β z

Constant –31.49 –2.16*

–35.86 –2.28*

–5.55 –.99 –2.76 –.47 –5.41 –.69 –5.51 –.70

STATE – [H1a] 1.47 .63 1.69 .67 –.24 –.45 –.56 –.99 –5.77 –1.93† –6.08 –1.93†

FOREIGN + [H1b] .63 .11 1.09 .18 2.62 1.99*

2.77 2.07*

–2.73 –.73 –2.78 –.73

BSIZE + [H2a] .10 .49 .21 .86 .04 .56 –.01 –.16 .08 .57 .05 .35

INDP + [H2b] –.36 –1.23 –1.01 –1.44 .15 1.00 .40 1.69† .47 1.89† .38 1.32

BDMEET + [H2c] –.11 –.61 –.09 –.51 –.09 –1.58 –.10 –1.68† –.04 –.57 –.04 –.52

SBSIZE + [H3a] –.54 –1.12 –.61 –1.22 –.47 –2.87**

–.49 –2.93**

.29 1.66† .27 1.45

PROFSB + [H3b] 1.79 2.81**

1.83 2.81**

.76 3.14**

.83 3.33***

.44 1.61 .46 1.65†

SBMEET + [H3c] .40 1.67 .50 1.61 –.07 –.87 –.09 –1.15 .19 1.34 .20 1.36

ROA ? .18 .02 –2.66 –.27 5.73 1.92† 5.19 1.72† 8.24 2.36*

8.77 2.43*

TOBINSQ ? –.45 –.27 .09 .05 .68 1.48 .14 .25 –1.99 –2.08*

–2.29 –2.17*

FSIZE ? 1.22 1.84† 1.36 1.94† .29 1.21 .21 .86 .54 2.01*

.58 2.07*

AGE ? –.23 –1.45 –.34 –1.77† –.11 –1.37 –.02 –.22 .04 .45 .07 .68

Y2002 - - .75 .46 - - –.22 –.34 - - –.41 –.52

Y2003 - - 2.12 .90 - - –1.13 –1.25 - - –.29 –.35

Y2004 - - 2.09 .85 - - –1.42 –1.46 - - –.71 –.76

Y2005 - - 2.97 1.15 - - –1.71 –1.63 - - –.64 –.62

Pseudo R2

31.36% 33.31% 11.47% 13.14% 21.72% 22.12%

Wald 2 29.78

** 31.63

** 32.75

** 37.52

** 37.7

*** 38.39

***

Cross-section 45 (38.46%) f

42 (35.9%) f

30 (25.64%) f

Observations 191 (35.37%) g

210 (38.89%) g

139 (25.74% ) g

The table reports the results of logistic regression models:

it

4

1l

2

1kkl

4

1jitj

it8it7it6it5it4it3it2it1it

SHAREDUMMYYEARDUMMYCONTROLS

SBMEETPROFSBSBSIZEBDMEETINDPBSIZEFOREIGNSTATEAQ

where, AQ = audit quality, the dichotomous dependent variable is coded as 1 if the firm is audited by a Big 4 audit firm, otherwise coded as zero; STATE = state ownership

concentration, proportion shares held by the state; FOREIGN = foreign ownership concentration, proportion of shares held by foreign investors; BSIZE = board size, the