the imf at sixty: an unfulfilled potential? · 2016-05-13 · the imf at sixty: an unfulfilled...

TRANSCRIPT

1

The IMF at Sixty: An Unfulfilled Potential?

Ariel Buira

Abstract

The governing structure of the Bretton Woods Institutions –that is, the International

Monetary Fund and the World Bank– was determined sixty years ago. In 1944, a few

industrial countries accounted for the bulk of world output, trade, and capital flows. This

is no longer the case. Developing countries and economies in transition, the more

dynamic elements of the world economy, account today for the same volume of output as

the Group of Seven (G-7) countries in terms of purchasing power parity, and for 84

percent of the world’s population. They can no longer be dismissed as minor partners in

the global economy.

The lack of adequate representation of the developing countries and emerging market

economies in the governance of the global economy and the declining commitment of

major countries to a multilateral rules-based system of international monetary

cooperation has resulted in short-sighted, and politically motivated decisions by major

shareholders, which undermine the efficacy of the IMF and World Bank and have

adverse consequences for world economic growth and stability. Indeed, the non

representative character of the governance of these institutions increasingly threatens the

integrity of the international monetary system, as countries in Asia and elsewhere move

away from the IMF and take distance from the World Bank, leaving the institutions to

deal mainly with low-income countries.

This paper provides an overview of the international monetary system, briefly

discussing six key problems1 in which the concentration of power in a few countries and

the limited participation of developing countries in the discussion of systemic issues

leads to poor results:

1. the correction of global imbalances;

2. the role of the IMF in the adjustment process;

1 For reasons of space, other important problems, such as the issue of negative net transfers of resources to developing countries, and the problems of the low income countries will not be discussed.

2

3. combating deflation through countercyclical policies;

4. financial crises prevention and resolution;

5. the management of international liquidity, and

6. responding to commodity shocks.

Overcoming these problems requires a renewed commitment of industrial countries to a

rules based multilateral system and the participation of developing countries in decision

making in a manner commensurate with their economic importance.

Global Economic Transformation

Over the past half century the world economy has become increasingly interdependent.

Developments in the economy of one country or region are transmitted to other countries

through increased international trade and financial flows. This integration differs from the

patterns of a century ago in that a growing number of multinational firms have spread

their production processes over a number of countries. As a result intra-firm trade and

intra-industry trade have risen sharply as a proportion of international trade.

Developments in information technology have erased distances and the integration of

capital markets has proceeded in a way that essentially creates a single international

capital market. The volume of financial transactions has grown exponentially and now

greatly exceeds the volume of flows in trade of goods and services. The close integration

of the global economy presents new and difficult economic challenges.

The transformation of the global economy has not been matched by a parallel evolution

of the mechanisms and institutions of global economic governance. The current

government structure of the World Bank and the IMF is the result of a political settlement

at the Bretton Woods Conference in 1944. But given the changes that have taken place in

the world economy since then, the current structure is not representative of the size and

importance of the economies of the member countries in terms of GDP, population, share

of world trade, reserves, or of their ability to contribute financial resources. Moreover, as

the “basic votes” of members--intended to ensure that countries with small quotas would

have a sense of participation in the affairs of the Fund--have not increased while quota-

based votes increased 37 fold, the resulting erosion in basic votes has diminished the

3

influence of developing countries in the IMF. This inadequate representation of their

membership undermines the effectiveness, credibility, and legitimacy of the two

institutions.

Some of the most important changes that have taken place in the world economy since

1944 include the following:

• The United States, which was the only large capital-surplus country up to the 1960s

and thus the main provider of resources for the IMF and World Bank, has become a

net debtor as its external liabilities exceed its assets abroad. Today it is the world’s

largest debtor country.

• The European Common Market, later to become the European Union, has introduced

a common currency, but the voting shares of countries in the euro area have not been

adjusted to reflect this change. According to the 1944 Bretton Woods formulas,

international trade is a major factor in determining IMF quotas. This resulted in the

small open economies of EU members having a 74 percent greater voting power than

the United States, despite having a smaller combined GDP. However, trade within a

single currency area is akin to trade within a domestic market and cannot give rise to

balance of payments imbalances. When the calculated quotas of the euro zone

countries are adjusted to exclude intra-eurozone trade, their voting power declines by

40 percent.2

• The G-7 industrial countries, which have effective control of the IMF and World

Bank, represent less than 14 percent of the world population and accounted for about

44 percent of world output in 2002. The developing countries and economies in

transition account for more than 84 percent of the world’s population and the same

proportion of world output as the developed countries measured in terms of

purchasing power parity.3 For this reason, decisions made by the G-7 countries

2 See Appendix on the Adjustment of European Union Quotas for Intra Eurozone Trade. Assuming that basic votes were restored to the original level of 11.3 percent and quotas were solely based on GDP in terms of PPP, developing countries would account for 49 percent and industrial countries for 51 percent of total voting power. 3 Developing countries alone account for over 39 percent of world GDP (IMF 2003). 5 On July 2, 2004, 1 SDR was equivalent to 1.466 U.S. dollars.

4

without the participation of the major developing countries are often perceived by

the developing world as having limited legitimacy.

• From 1950 to 2002, the developing countries have registered higher GDP growth

rates than the industrial countries and have increased their share of world GDP,

measured in terms of purchasing power parity (PPP), from 30 percent to 39 percent--

and to 44.2 percent if economies in transition are included (World Bank 2003). The

developing countries have increased their share of world exports from 26 percent in

1972 to 37 percent in 2002 (IMF 2003). Particularly noteworthy is the rise of output

of the Asian economies excluding Japan; Asian output accounted for only 9 percent

of world output in 1950 but today represents some 23 percent of global GDP.

• Reserves held by developing countries have risen from SDR 33.3 billion in 1972 to

SDR 1,132.3 billion at the end of 2002,5 a figure that greatly exceeds the reserves of

the industrial countries – which stood at SDR 749.5 billion on the same date. The

reserves of Asian countries recorded an extraordinary increase, from SDR 7.9 billion

in 1972 to SDR 720.1 billion at the end of 2002.

The growing breach between world economic and financial realities and the governance

structure of the Bretton Woods institutions argues for reform to enhance the effectiveness

and restore the legitimacy of these institutions. A more representative and inclusive

governance structure of the World Bank and the IMF –achieved by enhancing the

participation of developing countries in resolving the major monetary and financial

problems confronting the world economy– would improve global economic performance.

It would secure a more effective international adjustment process and achieve a more

efficient use of global resources, higher rates of growth and employment, and greater

macroeconomic stability. It would also increase support for primary-producer countries

subject to commodity shocks and contribute to the elimination of world poverty.

Correcting Global Payments Imbalances

5

Under the Bretton Woods system, structural balance of payments disequilibria were to be

corrected by exchange rate movements. Surveillance over exchange rates and exchange

rate arrangements was to be one of the IMF’s key functions. Following the breakdown of

the Bretton Woods system of fixed parities, the world moved to a “non-system” in 1973,

in which each country was free to pursue the exchange rate regime of its choice.

Surveillance is the means by which the international community aims to ensure that all

countries –and particularly those that exert a major influence on the world economy–

pursue policies conducive to sustained growth with stability, avoiding policies that might

lead them into problems or have detrimental effects on other countries. Through its

surveillance function, the IMF, acting on behalf of the international community, assesses

a country’s economic circumstances by reviewing its monetary, fiscal, exchange rate,

trade, and other policies and by offering advice on the appropriate policy measures for

the country to adopt. Article IV consultations –periodic reviews of member country

economies, as prescribed in Article IV of the IMF’s Articles of Agreement, or charter–

are the IMF’s main instrument of surveillance.

More recently, the effectiveness of the IMF is being questioned with regard to its ability

to

• persuade the United States to undertake measures to reduce its large fiscal and

balance of payments deficits;

• persuade the EU countries to tackle labor market and other economic rigidities that

have constrained their GDP growth rates;

• suggest measures to correct the growing payments imbalances between China and

other Asian countries (which peg their currencies to the U.S. dollar) and the United

States, and to reduce the impact on the euro area and others, which operate a floating

currency regime; and

• to prevent financial crises in emerging market economies. The fact that these have

recurred on average at the rate of more than one a year over the last decade suggests

that the IMF has not been successful in either preserving the confidence of financial

markets or inducing countries to make timely changes in their policies.

6

Yet in the words of the Articles of Agreement, the purposes of the IMF include “giving

confidence to members by making the general resources of the Fund temporarily

available to them… thus providing them with the opportunity to correct maladjustments

in their balance of payments without resorting to measures destructive of national or

international prosperity.”7

The effectiveness of IMF surveillance has been weakened by asymmetries in power and

compliance and by the fact that surveillance has not been applied in an evenhanded way.

Paul Volcker, former Chairman of the Federal Reserve System, has observed “When the

Fund consults with a poor and weak country, the country gets in line. When the Fund

consults with a big and strong country, the Fund gets in line” (Volcker and Gyoten 1992).

The growing asymmetries in IMF surveillance are reflected in the way it is conducted

today. 8 Bilateral surveillance (that is, oversight of the policies of individual member

countries) is the most direct one and has been exercised primarily over developing

countries, particularly those that have adjustment programs supported by IMF resources

and that require IMF support in seeking debt relief. In addition, in the 1990s, the

recurrence of financial crisis that ended often in major currency depreciations encouraged

the reorientation of surveillance to prevent financial crisis. It was then that the

international community gradually accepted the IMF public dissemination of country

surveillance appraisals. As a result, countries with open capital accounts have become

more sensitive to changes in “market sentiment.” Thus, with the publication of its

bilateral surveillance conclusions, IMF surveillance increasingly influences countries

wishing to gain or maintain market access. “Multilateral” and “regional” surveillance are

more analytical than operational in character, since they have not had a direct impact on

member country domestic policies, especially in larger countries or groups of countries

with greater influence on the global economy.

7 Article I Section (v) 8 Three levels of surveillance are described in the 2003 IMF Annual Report: (1) country or “bilateral” surveillance, (2) global or “multilateral”8 surveillance, and (3) “regional” surveillance; for example, of the European Union. Each type of surveillance addresses a different economic arrangement and thus has an impact in surveillance enforcement and effectiveness.

7

Through its “multilateral” surveillance, the IMF highlights for example, the risks for the

international economy of growing U.S. fiscal and payments imbalances in the 2002 and

editions of the IMF’s 2003 World Economic Outlook. In a recent report (IMF 2004), the

increasing world dependence on U.S. growth, the IMF highlights how the U.S. current

account deficit and growing indebtedness, if not corrected, could have a negative impact

not only on the United States but also on the global economy: “Although the dollar's

adjustment could occur gradually over an extended period, the possible global risks of a

disorderly exchange rate adjustment, especially to financial markets, cannot be ignored.

Episodes of rapid dollar adjustments failed to inflict significant damage in the past, but

with U.S. net external debt at record levels, an abrupt weakening of investor sentiments

vis-à-vis the dollar could possibly lead to adverse consequences both domestically and

abroad”…. (Ibid, p.9).

The response of the U.S. Treasury to the IMF report made clear that the Treasury did not

consider any correction in its domestic policy necessary.9 Since the persistence of large

imbalances in the reserve currency country pose significant risks to the system, the U.S.

response weakens the authority of the IMF and its ability to exert influence over other

countries. As a result, the world moves away from a rules-based multilateral system to a

power based system, in which the size of countries largely determines whether they abide

by the rules and large powers feel free to go their own way, based on their short-term

interests.

In recent years, growing U.S. fiscal11 and current account deficits have been financed

mostly through sales of government paper to Asian central banks whose currencies have

been pegged to the U.S. dollar and which have been accumulating high levels of

international reserves. As a result, the burden of dollar depreciation has fallen on

9 The Treasury considered the report was a “breathless hyperbole,” adding “The paper seems to conclude that if everything goes wrong in the U.S. economy, and no one does anything about it, that would be bad. That’s not exactly groundbreaking analysis.” Treasury press release, as quoted by IMF, Morning Press, January 9, 2004.

11 Of nearly 6 percent of GDP, including the social security surplus that is currently being spent.

8

countries with floating exchange rate regimes, which have seen their currencies

appreciate substantially (that is, the euro area and a few industrial countries and

developing countries, mostly in Latin America). In contrast, countries with managed and

fixed exchange rate regimes –such as most Asian countries– have been able to keep their

currencies undervalued, generating growing demands for protection from European and

U.S. labor unions and some industrial sectors that are losing jobs and market share. In

order to ease global adjustments, the IMF has recommended not only a correction of U.S.

imbalances but also greater exchange rate flexibility among Asian countries.

In a recent paper, Dooley, Folkerts-Landau, and Garber (2003) explain why countries in

Asia may not be willing to follow IMF recommendations. They suggest that in order to

maintain export-led development strategies, Asian countries –and China in particular– fix

the exchange rate to the dollar to ensure a competitive edge. As a result, they have run

large current and capital account surpluses and are accumulating international reserves at

a fast pace. In the case of China, this policy has been sustained without giving rise as yet

to overheating and inflation. Dooley et al. believe that the primary motivation in China’s

export-led strategy has been the absorption into the modern sector of a substantial

proportion of the labor force from an underemployed farming sector.

Global payments imbalances can no longer be corrected by exchange rate adjustments

among the major industrial countries with flexible exchange rates. Dooley et al. consider

that with the collapse of communism, the decline in protectionism and the ensuing

integration of Asia and Latin America into the world economy, these countries must now

be seen as a new driving force:

…“now the Asian periphery has reached a similar weight (as Europe-Japan in the

1950s): the dynamics of the international monetary system, reserve accumulation, net

capital flows, and exchange rate movements, are driven by the development of these

periphery countries. The emerging markets can no longer be treated as small countries,

weightless with respect to the center” (Dooley et al. 2003).

Asian countries have maintained very high rates of export growth and large trade

surpluses, which have attracted private investment flows. As a result they have run large

9

trade and capital account surpluses and, since their currencies have not been allowed to

appreciate, they have accumulated high levels of international reserves that have been

heavily invested in U.S. Treasury paper. They have thus financed the U.S. twin deficits

and have made them sustainable, at least for the time being.

A number of problems and risks are apparent in this situation:

• The depreciation of the U.S. dollar, while appropriate to address the U.S. external

deficit, also poses an impediment to the recovery of the European Union and other

countries with floating currencies.

• The dollar depreciation has precipitated rising trade tensions and calls for protection

in Europe and other countries whose currencies have appreciated.

• The rapid growth of Asian exports of textiles and other goods has also given rise to

calls for protection in the United States. Thus, pressures for protectionism are rising

in response to unemployment and political pressures in countries whose industries

are unable to compete with Asian goods.

• There is the risk that at some point the demand for dollars as a reserve currency will

decline as monetary authorities and private investors choose to hold reserve assets

that maintain their value: possibly in euros, yen, or gold. This substitution could take

place among the industrial, oil- exporting countries, and developing countries that

cannot justify capital losses arising from a declining dollar, with gains from higher

rates of growth, employment, and industrialization.

• A disorderly depreciation of the dollar would lead to a sharp rise in dollar interest

rates that would put a sharp brake on the U.S. recovery and on the growth of Asian

and other countries dependent on the U.S. market.

• Although flexible exchange rates contribute to the international adjustment process,

the volatility of exchange rates among major currencies discourages trade, and,

above all, investment flows that require a medium-term planning horizon, since

hedging instruments are unavailable for longer maturities. The euro/dollar rate has

fluctuated by more than 50 percent (from 0.82 to 1.28) since the euro’s introduction.

The IMF’s surveillance has not had a major impact on U.S. domestic policies nor on

Asia’s exchange rate policies. Neither has it influenced the domestic policies of the

10

European Union or Japan. As long as there were no major imbalances and the reserve

currency countries followed policies broadly consistent with internal and external

stability, however, the ineffectiveness of surveillance did not give rise to significant

tensions.

The correction of global imbalances through agreements among a few industrial countries

(such as the Plaza Accord of September 1985) is no longer feasible and solutions arrived

at without the full participation of developing countries, are unlikely to work.12 The

solution of major global imbalances requires the involvement of both deficit and surplus

countries, in this case of key developing countries, in accordance with basic rules and in a

manner commensurate with their economic importance. To overcome the current risks

and correct major imbalances in an orderly manner, the IMF’s governance must become

more participatory and its surveillance more effective and evenhanded. The impact of

surveillance could be enhanced through discussions with all the relevant developing

country players. A larger, more representative IMF could be firmer and more effective in

dealing with global imbalances than an IMF run by a few industrial countries. However,

the stability of the international system requires a degree of self-discipline by major

countries. A lack of discipline by the reserve currency country was at the root of the

demise of the par value system .

The Role of IMF Financing in the Adjustment Process

To be effective and in keeping with its mandate, the Fund has to provide member

countries with technical advice and financial support to address their payments

imbalances in a manner that sustains the level of economic activity to the greatest

possible extent. Recall that the purposes of the Fund include:

(ii) “To facilitate the expansion and balanced growth of international trade, and to

contribute thereby to the promotion and maintenance of high levels of employment and

real income and to the development of the productive resources of all members as

primary objectives of economic policy”, and

12 Witness such initiatives as the Contingency Credit Line, the Sovereign Debt Restructuring Mechanism and the Highly Indebted Poor Countries Initiative to reduce debt levels.

11

(v)“To give confidence to members by making the general resources of the Fund

temporarily available to them under adequate safeguards, thus providing them with the

opportunity to correct maladjustments in their balance of payments without resorting to

measures destructive of national or international prosperity” 13

Thus, in addressing each case, the Fund should seek to strike a fine balance between

adjustment and financing. When a country has unlimited financing, like the United States

at present, it may well be able to resist adjustment, however necessary, for long period of

time. At the other extreme, developing countries undertaking adjustment without

adequate financial support increases the economic costs as well as political resistance to

necessary measures, since they are likely to be politically unpopular. Consequently, the

risk of program failure rises. Therefore, the Fund must be able to encourage the adoption

of adjustment programs in a timely manner by offering a level of financing that limits the

undesireable short-term effects of an adjustment program. A Fund without adequate

financial resources will not be able to perform its role. It can not provide incentives to

adjustment, nor can it be seen as a friend to which countries can turn for support and

guidance in uncertain times. Rather, it will be seen as a harsh task master to be held at

bay, particularly when the countries know the IMF is dominated by a few industrial

country creditors who are blocking a badly needed expansion in its financial resources.

The IMF was established to combat a market failure, that is, the collapse of domestic

demand and to counter attempts by countries seeking to emerge from balance of

payments problems through the adoption of protectionist measures, competitive

depreciations, and other “beggar-thy-neighbor policies.” Circumstances led to the

industrial countries drawing on its resources during the early decades of the IMF.

However, with industrial country members no longer needing to use IMF resources, these

were allowed to decline as a proportion of world trade. IMF resources thus fell sharply,

from 58 percent in 1944 to 15 percent in 1965, and further to an estimated 3 percent at

present.

13 IMF, Articles of Agreement, Article I, Section II

12

As a result of the relative decline in the IMF’s resources, the balance between adjustment

and financing in Fund-supported programs, necessarily shifted toward less financing and

more severe adjustment. As resources declined, a hardening of conditionality ensued, -

defined as the number of measures and policies that a country has to adopt to gain access

to Fund resources- and as a result, the rate of success of Fund supported programs

declined. In fact, the rate of non-compliance with Fund programs, measured by the

IMF’s failure to fully disburse approved drawings, rose sharply, reaching 86 percent in

the late 1990s.

Since the increase in conditionality made the IMF dysfunctional, a revision of its

guidelines on conditionality became necessary and was undertaken. However, in any

discussion about revised conditionality, a key question arises: Should conditionality be

determined by the availability of resources, even as these decline sharply over time, or, in

keeping with the IMF’s purposes as an institution for international monetary cooperation,

should its resources increase in step with the liberalization and growth of world trade and

the integration and volatility of international capital markets?

This is not to ignore that, in some cases, large, systemically or strategically important

countries (such as Mexico, Brazil, Russia, Korea and Turkey) have received Fund

financial support and far in excess of their quota access limits. But the circumstances

under which these countries obtained such exceptional support are neither transparent nor

predictable. It is not available to all IMF members and at times comes with questionable

conditions imposed by countries that contribute to the financial rescue package (Feldstein

1998).

IMF officials often make references to the “catalytic role of the IMF” as a means of

justifying its limited financing to members. The rationale here is that the IMF provides a

“seal of approval” to a borrower country’s policies that then spurs other sources of

financing. Since there is no reference in the IMF’s Articles to the Fund playing a

“catalytic role,” this is a strange argument to make. Nevertheless, the argument that a

member’s access to the Fund’s more conditional resources is sufficient to induce

additional private capital flows could be acceptable if, in fact, it assured that market

financing was actually forthcoming. Unfortunately, this is not the case. While the Fund

13

did play a role in inducing capital flows to Latin America during the debt crisis of the

1980s, empirical studies of the catalytic effect conclude that there is little evidence to

support its existence in the 1990s (Bird and Rowlands 1997).

Unfortunately, as is often the case, when the conclusion of negotiations on an IMF-

supported program does not bring forth market financing in sufficient amounts, the

program may be underfinanced to allow an adjustment that is not sharply contractionary.

Indeed, as Bird and Rowlands point out, "Structural adjustment is unlikely to succeed if

starved of finance. The Fund appears to have assumed--perhaps on the basis of partial

and, in the event, unrepresentative evidence--that finance would come from elsewhere,

catalyzed by its own involvement. In practice the catalytic effect was largely

unforthcoming and IMF programs showed an increasing tendency to break down.

Significantly, the likelihood of breakdown appears to vary inversely with the amount of

finance provided by the Fund." Bird and Rowlands add that "The premise of a universally

positive catalytic effect will lead to inappropriate conditionality and will have adverse

consequences for its effectiveness."

Since a large majority of Fund members support an increase in its resources, why have

quotas not kept pace with members’ needs, in a manner related to the expansion of

international trade and capital movements? Under the Articles, an increase in quotas

requires an 85 percent majority of votes, under the weighted voting system. The question

thus becomes, what countries have blocked the increase in Fund resources? Industrial

countries no longer resort to IMF support and are no longer willing to contribute to its

resources, as shown by the Fund’s failure to agree to adopt a quota increase since January

1998. However, in order to preserve their political control of the IMF these countries do

not wish to see their share of quotas and voting power reduced. Thus, the industrial

countries have been reluctant to allow more dynamic emerging-market countries and

other developing countries to increase their quotas and voting power. A different

structure of governance and decision making, one not constrained by an 85 percent

majority requirement for quota changes,14 which gives a veto on quota increases to a

single country, the United States, would have led to a very different outcome.

14 See Article III, section 2(c)

14

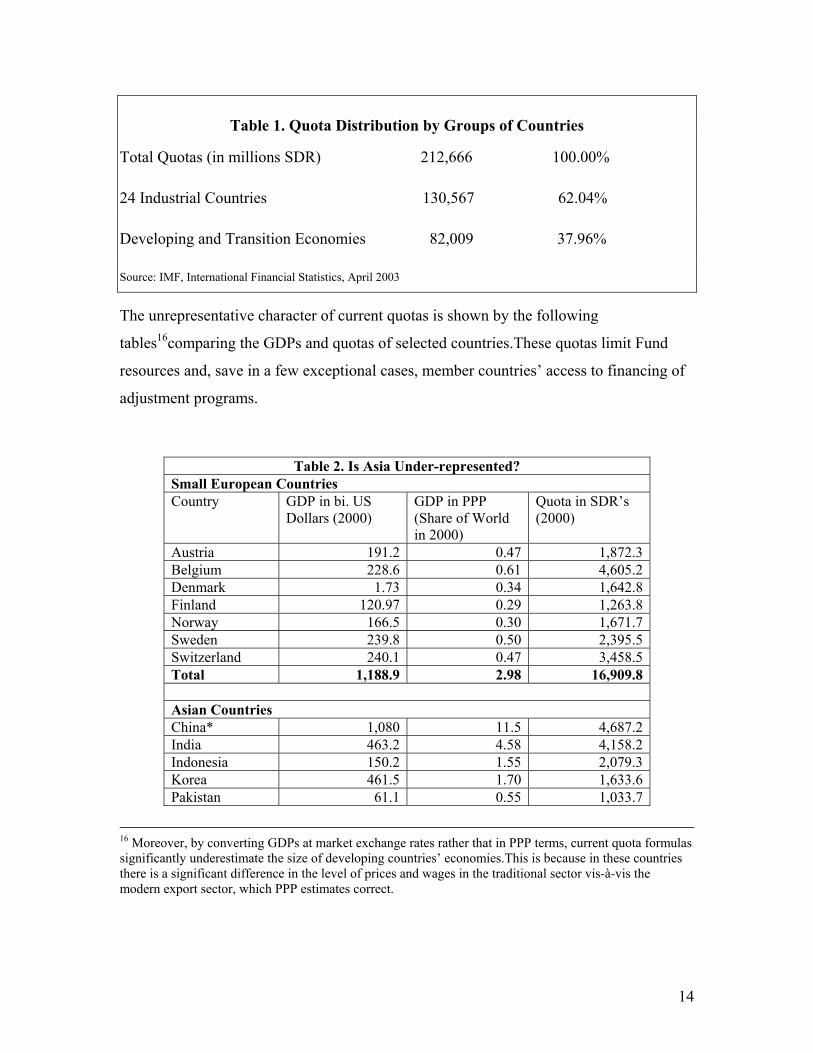

Table 1. Quota Distribution by Groups of Countries

Total Quotas (in millions SDR) 212,666 100.00%

24 Industrial Countries 130,567 62.04%

Developing and Transition Economies 82,009 37.96%

Source: IMF, International Financial Statistics, April 2003

The unrepresentative character of current quotas is shown by the following

tables16comparing the GDPs and quotas of selected countries.These quotas limit Fund

resources and, save in a few exceptional cases, member countries’ access to financing of

adjustment programs.

Table 2. Is Asia Under-represented? Small European Countries Country GDP in bi. US

Dollars (2000) GDP in PPP (Share of World in 2000)

Quota in SDR’s (2000)

Austria 191.2 0.47 1,872.3 Belgium 228.6 0.61 4,605.2 Denmark 1.73 0.34 1,642.8 Finland 120.97 0.29 1,263.8 Norway 166.5 0.30 1,671.7 Sweden 239.8 0.50 2,395.5 Switzerland 240.1 0.47 3,458.5 Total 1,188.9 2.98 16,909.8 Asian Countries China* 1,080 11.5 4,687.2 India 463.2 4.58 4,158.2 Indonesia 150.2 1.55 2,079.3 Korea 461.5 1.70 1,633.6 Pakistan 61.1 0.55 1,033.7

16 Moreover, by converting GDPs at market exchange rates rather that in PPP terms, current quota formulas significantly underestimate the size of developing countries’ economies.This is because in these countries there is a significant difference in the level of prices and wages in the traditional sector vis-à-vis the modern export sector, which PPP estimates correct.

15

Philippines 163.9 0.67 879.9 Thailand 122.6 0.95 1,081.9 Total 2,502.5 21.5 15,553.8

*Following the accession of Hong Kong SAR, China’s GDP was $1,237 billion converted at market exchange rates; its share of world GDP rose to 12.67 percent, and its quota was increased to SDR 6,369 billion.

Source: World Economic Indicators 2003, World Bank.

Table 3. Is Latin America Under-represented? Small European Countries Country GDP in bi. US

Dollars (2000) GDP in PPP (Share of World in 2000)

Quota in SDR’s (2000)

Austria 191.2 0.47 1,872.3 Belgium 228.6 0.61 4,605.2 Denmark 173.0 0.34 1,642.8 Netherlands 371.9 0.91 5,162.4 Norway 166.5 0.30 1,671.7 Sweden 239.8 0.50 2,395.5 Switzerland 240.1 0.47 3,458.5 Total 1,611.1 3.60 20,808.4 Latin American Countries Argentina 284.2 0.88 2,117.1 Brasil 599.8 2.68 3,036.1 Chile 75.0 0.48 856.1 Colombia 78.0 0.65 774.0 Mexico 581.4 1.97 2,585.8 Peru 52.9 0.28 638.4 Venezuela 121.3 0.47 2,659.1 Total 1,756.6 7.41 12,666.6

Source: World Economic Indicators 2003, World Bank.

Combating Deflation and Low Levels of Aggregate Demand

While a number of major industrial countries (United States, France, Germany, Japan,

United Kingdom, and others) have actively pursued their own counter-cyclical policies

and an economic recovery appears to be on the way in these countries, GDP growth rates

remain low in much of the developing world outside Asia. Most developing and

emerging market countries have been unable to adopt expansionary policies, and the

16

Fund has been ineffective in combating the recession prevailing in the international

economy over recent years.

The IMF’s recent passivity in the face of international recession can be contrasted with

the active counter-cyclical stance adopted by the IMF in the mid 1970s. With the world

economy emerging from three years (1969 to 1971) of a combination of recession and

high rates of inflation, the sharp increase in oil prices in 1973 and 1974, which deepened

the recession and fueled inflation, posed for the Fund what was perhaps its greatest

challenge to that date.

In addition, the ensuing massive transfer of wealth from oil-importing to oil-exporting

countries posed another grave problem for the international economy. It was recognized

at an early stage that very poor countries would not be able to borrow from private

markets to pay for the increased cost of oil imports and there were doubts as to the ability

of the banks to recycle the large sums involved.

The IMF’s then Managing Director, Johannes Witteveen, a man of vision and an

outstanding economist, understood the challenge and proposed the establishment of an

Oil Facility in the Fund in 1974 for one year to recycle the surplus from oil-exporting to

oil-importing countries. This recycling would help poor countries finance their external

imbalances without further restricting economic activity and gain time for devising

energy saving and other adjustment strategies to reduce their external imbalances. The

proposal, initially resisted by the United States, was put into place with the strong support

of European and developing countries –several of which intended to resort to it– as well

as that of oil-exporting developing countries who would finance it.

The sole requirement for access to the Oil Facility by oil-importing countries was the

existence of a balance of payments need. There was virtually no other conditionality than

for potential users to refrain from imposing or intensifying restrictions on trade and

payments without the approval of the Fund. As in other cases of the use of resources, the

country was expected to consult with the Fund in order to give it the opportunity to

determine whether the member’s policies were conducive to its balance of payments

17

adjustment. The 1974 Oil Facility proved useful and was followed by another facility in

1975.

Under the 1975 Oil Facility the IMF applied stricter conditionality. Members making

drawings were to describe to the Fund their policies to achieve medium-term solutions to

their balance of payments problems and have the Fund assess the adequacy of these

policies. The borrowing countries were also required to describe the measures they had

adopted or proposed to adopt to conserve oil and/or develop alternative energy sources in

order to reduce their oil imports.

With this strong response, the Fund helped recycle the surpluses from oil-exporting to

oil-importing countries, many of which would not have had access to capital markets.

This allowed borrowing countries to avoid deflating aggregate demand unduly, which

would have compounded the problems besetting the international economy.

In recent years, the developed economies have been able to adopt counter-cyclical

monetary and fiscal policies to deal with recession and the risk of deflation. However,

the failure of countries in large surplus to expand, coupled with the absence of a

mechanism to recycle their surpluses, has obliged emerging market economies and low-

income countries to adopt contractionary measures to protect their balance of payments

and avoid crises of confidence. Given their importance in international output and trade,

this has contributed to a protracted recession in a large group of developing countries and

to a deeper contraction of world trade.

At a time of net negative capital flows to the developing and emerging market countries,

why didn’t the IMF recycle the large (Asian) surpluses, as it did in the 1970s, to sustain

higher levels of economic activity, investment, and structural reform in developing and

emerging market countries that could not pursue anti-cyclical policies on their own?

Perhaps the main reason is that back in the 1970s, several industrial countries wishing to

resort to IMF financial support under the Oil Facility supported its role in recycling.

More recently, however, the developed countries lack of interest in helping the

developing countries by recycling surpluses and their inadequate representation in Fund

decisionmaking has doomed these countries’ ability to pursue anti-cyclical policies.

18

Financial Crises Prevention and Resolution

While capital account volatility has been increasing since the late 1980s, the volatility

became more pronounced in the late 1990s. This is illustrated by Chart 1 below.

The Mexican crisis of 1995, which was followed by those of Thailand, Indonesia, and

Korea in 1997, and later by those of Russia, Brazil, Venezuela, Turkey, Argentina, and

Uruguay, are best-known cases in which the loss of market confidence gave rise to

massive capital outflows. Although the problems posed by the volatility of financial

flows are well recognized, even countries with sound economic policies experience short-

term pressures on their balance of payments or exchange rate do not have a ready source

of emergency financing.

Chart #1- Latin America: Private Flows, External Current Account and Real Exchange Rates

-5

-4.5

-4

-3.5

-3

-2.5

-2

-1.5

-1

-0.5

01990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

% o

f GD

P

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

Rea

l Exc

hang

e R

ate

Private Flows External Current Account Real Exchange Rate(IMF)

19

In 2002, the international community agreed that “Measures that mitigate the impact of

excessive volatility of short-term capital should be considered.”17 Moreover, the IMF’s

own research studies have concluded that capital account liberalization does not promote

growth and that market-friendly capital controls have been effective in crises prevention

in a number of countries (Prasad et al. 2003). Nevertheless, the use of capital controls is

still discouraged and there has been little by way of Fund policy reaction to unilateral

U.S. efforts to decry the use of controls in the conduct of bilateral trade agreements (i.e.,

with Chile and Singapore).

The IMF’s Contingent Credit Line (CCL) was established in 1999 as a precautionary

facility, intended to give emerging market countries with sound policies and good

fundamentals the assurance of IMF financial support to discourage, and protect countries

from, speculative attacks. But it was designed in such a restrictive manner that, despite

the high costs of self-insurance and the many difficulties developing countries have

encountered, none has resorted to it in its five years of existence. Although most IMF

Executive Directors, particularly those representing potential users, supported the

continuation of a reformed CCL that would fulfill the original purpose of discouraging

speculative attacks, they did not constitute a qualified majority of the vote (85 percent)

required to keep it in existence. So, on November 30, 2003, the IMF terminated the CCL.

The official statement said that many emerging market countries had reduced their

vulnerability to speculative attacks by building up their reserves and adopting flexible

exchange rates and other reforms.

The risks posed by capital market volatility remain high and new financial crises may

recur as financial flows return to emerging markets. Following the cancellation of the

CCL, Tim Geithner, currently President of the Federal Reserve Bank of New York but

previously Director of the IMF’s Policy Development and Review Department, criticized

the Fund’s economic review and lending policies toward emerging market nations and

advocated an alternative policy aimed at crisis prevention. He said the Fund’s policy of

monitoring the performance of countries and then lending after a crisis develops is not

17 Paragraph 25 of the Monterrey Consensus, the outcome of the UN Conference on Financing for Development, Monterrey, Mexico, March 18-22, 2002.

20

well suited for emerging markets. Geithner argued these nations would be better served

through an insurance fund that could be “mobilized quickly and on a sufficiently large

scale.” A similar criticism had been made several years earlier by this writer (Buira

1999).

If market confidence cannot be maintained, and no financing is available, there are

essentially two ways other than default of dealing with crises arising from the volatility of

capital:

• the temporary suspension of debt service payments, that is, through the declaration

of a “standstill” leading to a debt restructuring, and

• the use of capital controls to prevent excessive inflows of short-term money.

To deal with this issue the IMF proposed a Sovereign Debt Restructuring Mechanism

(SDRM).18 This mechanism called for a “standstill” on payments that would give

countries in crisis legal protection against creditor suits for a limited time to allow them

to negotiate the restructuring of their debt in an orderly manner. After initially supporting

the SDRM, the United Sates withdrew support for the standstill proviso that was essential

to make it operational, thus effectively eliminating it. Most emerging market countries

had reservations regarding the SDRM. They feared that their support would be read by

markets as indicating their intent to restructure their debt, which would raise the cost of

borrowing and hinder their access to markets instead of providing an insurance

mechanism, as it was meant to do.

Recent months have seen a sharp fall in the spreads for emerging market borrowers, that

is, a sharp rise in their asset prices that responds to the U.S. Federal Reserve’s policy of

monetary easing, which has pumped large amounts of liquidity into financial markets. As

a result, after years of withdrawal, investors in search of higher yields are again attracted

to emerging markets.

18 The proposal was made by Anne Krueger, Deputy Managing Director of the IMF in 2001. 20 Collective action clauses allow bondholders to modify repayment terms of bonds subject to the approval of a qualified majority of bondholders.

21

If the global economy continues to gain strength and U.S. interest rates remain low,

emerging market countries will be able to borrow with little risk; however, when these

conditions change, as they will in time, the risk of financial crises will again loom large –

particularly for those countries whose borrowing is sustained by market momentum

rather than by their fundamentals. In that event, the recurrence of financial crisis will

simply be a matter of time. Because the emerging market countries that are potentially at

risk did not command sufficient votes in the IMF to retain a modified and effective

precautionary facility, and controls on short-term capital flows are discouraged, the

international financial system has no mechanism to prevent the devastation wrought by

financial crises in emerging market countries. The alternative, including collective action

clauses20 in bond contracts, takes a long time to take effect (only after existing contracts

expire).

The Creation and Management of International Liquidity

International liquidity creation depends on the expansion of capital markets, and in

today’s U.S. dollar-based payments system, on the balance of payments deficit of the

United States.

Concern that global liquidity would not expand in step with the needs of the world

economy, thereby creating a deflationary bias, led the international community in 1969 –

un der the IMF’s auspices– to create the SDR as a supplemental reserve asset. The

subsequent rapid expansion of financial markets, starting in the late 1970s, led the major

countries to believe that it was not necessary to expand liquidity through the allocation of

additional SDRs, since creditworthy countries could resort to market borrowing. This was

always a dubious argument, however, since, at best, access to financial markets was

limited to the industrial countries and to only a few emerging market economies.

As noted earlier, access to financial markets for a number of emerging market countries

is improving currently, the result of increased market confidence and the low demand for

credit in industrial countries. Nonetheless, more than 150 developing countries still have

virtually no access to international financial markets. For these countries, the

accumulation of international reserves (or export of capital) comes at the cost of reduced

22

imports of consumer and investment goods, which means reduced consumption and

investment.

Arguing that an SDR allocation would give rise to inflationary pressures, several major

industrial countries have opposed even a modest allocation; as a result, no SDRs have

been allocated since 1981.This concern about the inflationary consequences of an SDR

allocation, however, would not be valid amid the recessionary global economic

circumstances prevailing in 2001 and 2002; in fact, an SDR allocation would have

contributed to economic recovery.

Should the international community leave the creation of liquidity to market forces? This

was not the view of the founding fathers of the IMF nor is it a view implicit in Article

XVIII of the IMF’s Articles of Agreement, which empowers the IMF to create

international liquidity to promote its purposes.

The international community accordingly gave itself the capability to counter

contractionary forces by expanding international liquidity through the IMF’s capacity to

create international reserve assets through SDR allocations. In this way, the international

community could help developing countries build up their international reserves.

At a time of recession and an incipient international economic recovery, an allocation of

some SDR 70-100 billion would not only not pose no inflationary risks and be helpful to

recipients of SDRs, it would also further the recovery of the world economy. But

approval of an SDR allocation requires an 85 percent majority of the IMF’s Executive

Board. This means that it is subject to a U.S. veto (the U.S. share of the vote is now 17.2

percent) and may also be opposed by other industrial countries, such as the EU countries.

In the past, however, several European countries with a strong interest in Africa have

been favorable to an SDR allocation and one can assume that, in the current

circumstances, they would again be supportive. If this were the case, a coalition of

developing and some EU countries might be able to persuade the United States to

overcome its reluctance to put the matter to Congress.

Under the Articles of Agreement, SDRs are to be allocated to Fund members in

proportion to their quotas; consequently, over 60 percent of any SDR allocation would

23

accrue to the industrial countries. However, short of an amendment of the Articles,

industrial country recipients could donate the SDRs they are allocated to developing

countries at no cost to them, on the condition that the recipients pay the low interest rate

due on the SDRs they receive.

Since the SDR interest rate is equal to the average of the short-term interest rates on a

basket of currencies that compose the SDR, it is market-determined. And although it

would be below the developing country cost of borrowing, it would not impose any

resource transfers or costs on other countries. The liquidity provided as a result of SDR

transfers would be on terms much more attractive to recipients than market borrowing,

even for those few countries that have access to financial markets, as these countries

normally pay a significant spread or premium over interest rates on developed country

Treasury papers. Moreover, the cost of holding international reserves for recipients of

SDRs would decline, since the return they can obtain on the investment of their

international reserves would be similar to the SDR interest rate (with no quasi-fiscal

costs). For those countries unable to borrow in financial markets, the benefits of an SDR

allocation –plus transfers of SDRs originally allocated to industrial countries– are

unquestionably larger. They are, however, more difficult to estimate since there is no

market price with which the cost of external borrowing can be compared.

Responding to Exogenous Shocks

More than fifty developing countries depend on three or fewer commodities for most of

their merchandise export earnings. The poorest countries with less diversified economies

are the ones most affected by commodity shocks. Whether they are the result of price

shocks or those arising from droughts, floods, or other natural disasters, developing

countries with incomes per capita of $1,000 or less are those that suffer the most.

Developing ccountries with incomes of $2,000 per capita or higher are less seriously

affected in relative terms. This is because of the greater diversification of their productive

structure and exports make them better equipped to absorb commodity shocks.

The cost of the average commodity shock has been estimated at some 2.5 percent of GDP

(IMF 2003) and by another estimate at 7 percent of GDP, and if indirect costs are

24

considered, as much as 20 percent of GDP (Collier 2002). On average, shocks occur

every two to three years, and there is reason to believe that natural disasters, particularly

those related to extreme weather, are on the rise.

The IMF has a facility to assist countries to cope with commodity price shocks and

excess costs of cereal imports. The Compensatory Financing Facility (CFF) whose

purpose is to provide financing to countries for export revenue shortfalls relative to a

medium-term trend, was introduced in 1963 and liberalized in 1966 and again in 1975.21

In principle, access to the CFF is virtually unconditional since exogenous shocks –

whether attributable to a fall in the price of commodity exports to such natural disasters

as a drought– are not the result of government policies. Therefore countries suffering

from a shortfall in their export earnings as a result of such shocks could have access to

the CFF provided the IMF determines that there is assurance of repayment and that the

commodity problem is not the result of a secular deterioration in the borrower country’s

terms of trade. Drawings on Fund resources, however, are limited to 45 percent of a

member’s quota for commodity shocks and 45 percent for excess import costs in any 12-

month period, with a cumulative total of no more than 55 percent of quota. Given the

21 Executive Board Decision No.4912 (75/207), December 24, 1975.

25

small size of IMF quotas relative to world trade and the high dependency of some

countries on exports of a single commodity, this limit is by itself very restrictive.

The CFF was much used by low-income countries in the 1970s and early 1980s.

However, Executive Directors of industrial countries, wishing to limit the facility’s use,

argued that drawings on the CFF allowed countries to postpone adjustments; as a result

the Executive Board imposed heavy conditionality on the use of the CFF in 1983.23 The

conditionality introduced has greatly discouraged use of the CFF and, for practical

purposes, the facility has virtually ceased to exist. A more representative governance

structure at the IMF would be more sympathetic to the needs of countries affected by

exogenous shocks.

Conclusion

Sixty years after the establishment of the Bretton Wood Institutions, a review of the

major monetary and financial problems confronting the world economy, suggests that

existing arrangements fall short of providing an enabling environment for financial

stability and economic growth, particularly for the developing countries. The IMF is not

able to influence the adjustment of global imbalances, sustain market confidence to

reduce volatility of capital flows and prevent financial crises24, does not support

countercyclical policies in emerging markets, nor compensatory financing to assist

primary producers deal with exogenous shocks, and has little influence over the creation

and distribution of international liquidity.

Since the issues are well understood and the potential for improvement exists, the

deficiencies of current arrangements must be seen as a political problem resulting from a

nonrepresentative governance structure that fails to address the concerns of most of the

world and a lack of commitment on the part of major industrial countries to abide by the

rules of a multilateral system.

23 Executive Board Decision No. 7528 (83/140), September 14, 1983. 24 As the catalytic role played by its seal of approval has lost credibility

26

In the BWIs, decisionmaking power is vested in a small group of industrial countries that,

having dealt with their own monetary problems and financial imbalances over the last

quarter century outside the Bretton Woods system, are no longer committed to it as a

multilateral cooperative enterprise. As a result, decisions on major policy isues are rarely

rules based; more often than not, they are opportunistic and short-sighted, giving

inadequate consideration to the interests of developing countries, which account for an

increasing share of the world economy and for the great majority of the world's

population. The major shareholders of the IMF (and World Bank), have shown

themselves unwilling to yield power in order to allow a representative governance

structure to emerge--one in which developing countries would play a role commensurate

with the size of their economies, assume greater responsibilities, and increase their

financial contributions to the international financial institutions. Consequently, the major

shareholders have witnessed a decline in the resources, prestige, and authority of the

institutions.

Industrial countries no longer pay much heed to the Bretton Woods institutions.

Following the United States and Europe, emerging countries in Asia have also largely

walked away; other emerging economies may also be expected to reduce their reliance on

the Fund and Bank over time. Thus, the multilateral system for international monetary

and financial cooperation painfully constructed at Bretton Woods is becoming irrelevant

to all, except the very low income countries, mainly in Africa, where their record is

mixed.

Since the multilateral institutions for monetary cooperation and development have a great

potential to contribute to the better functioning of the international economy by helping

achieve more stable growth and a fuller utilization of economic resources, the decline in

their resources, role, and legitimacy call out for a bold and immediate solution.

27

Appendix I

Adjustment of European Quotas for Intra-Eurozone Trade

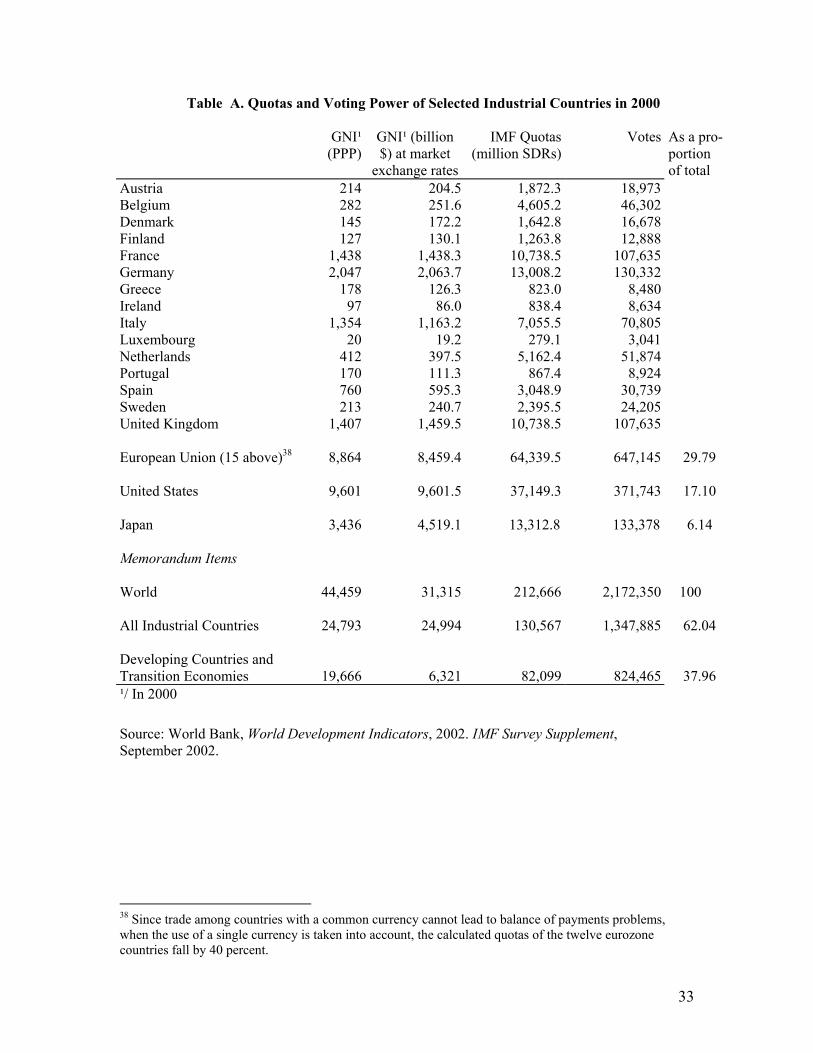

1. The 15-member European Union (EU), with a smaller GDP than the United States has 74 percent greater voting power and is currently represented by nine Executive Directors in the IMF Executive Board (see Table A).25 In addition, the EU has 56 percent greater voting power than the United States in the World Bank and eight Executive Directors on the World Bank Executive Board. The overrepresentation of EU members comes at the expense of other members. The excessive weight of the EU group of countries is partly attributable to the treatment of intra-EU trade in goods and services in the formula used for quota calculations.

2. A number of European countries formed a monetary union in 1999. This fact gives rise to a new situation calling for a revision of the calculated quota of the 12 euro zone members. Since trade within a single currency area cannot give rise to balance of payments problems among its members, it is more akin to domestic trade than to international trade. Thus, trade between California and New York, or between Delhi and Calcutta is not regarded as international trade. Similarly, since trade between euro-zone members cannot give rise to balance of payments problems, it can not be regarded as international trade for the purposes of the IMF quota calculations26.

3. Recognizing the impact of intra-EU trade on quota calculations, an IMF staff report, “External Review of the Quota Formulas,” EBAP/00/52 Sup. 1, May 1, 2000, shows what would be the hypothetical adjustments needed to exclude intra-trade in goods.

25 In addition, the ECB representative participates in: Article IV consultations, surveillance of the euro area members, Article IV consultations, and use of resources of the 13 accession countries, as well as in discussions of the World Economic Outlook, the international capital market reports, the role of the euro in the international monetary system, and world economic and market developments. 26 See also IMF staff report “The European Monetary Union and the IMF-Main Legal Issues Relating to Rights and Obligations of EMU Members in the Fund," SM/98/131, dated June 8, 1998. R. Sroits, ‘The European Central Bank, Institutional Aspects,’ page 443, argues that once the European Community has a common currency, a single monetary and exchange rate policy, a single monetary authority (the European Central Bank), and a single external position in terms of payments and other financial transactions to and from third countries, it will have assumed the characteristics of a 'country' for the purposes of Article II, Section 2 of the Fund's Articles of Agreement. Sroits further refers to various expressions of the opinion that euro area member states may no longer qualify for membership in the IMF since they no longer possess the necessary characteristic of monetary sovereignty in the international order. J.V. Louis, in "Governing the EMU or Governing the EU," in the Symposium on Monetary Policy and Globalization of the Markets, June 2002, observes that the European Monetary Union is "irreversible and irrevocable" and that "the Member States are not able anymore to comply individually with the commitments inherent to their participation to the IMF."

28

The reason given for exclusion is that intra-trade is seen as entrepôt trade27 in a free trade area. The report explains that if this adjustment were made “EU-15 countries’ share would be reduced by 9.2 percentage points (from about 37.1 percent to about 28.0 percent). The largest declines in percentage points are for Germany, the Netherlands, France, and Belgium.” Note that IMF staff estimates do not include trade in services in these results because of lack of data.

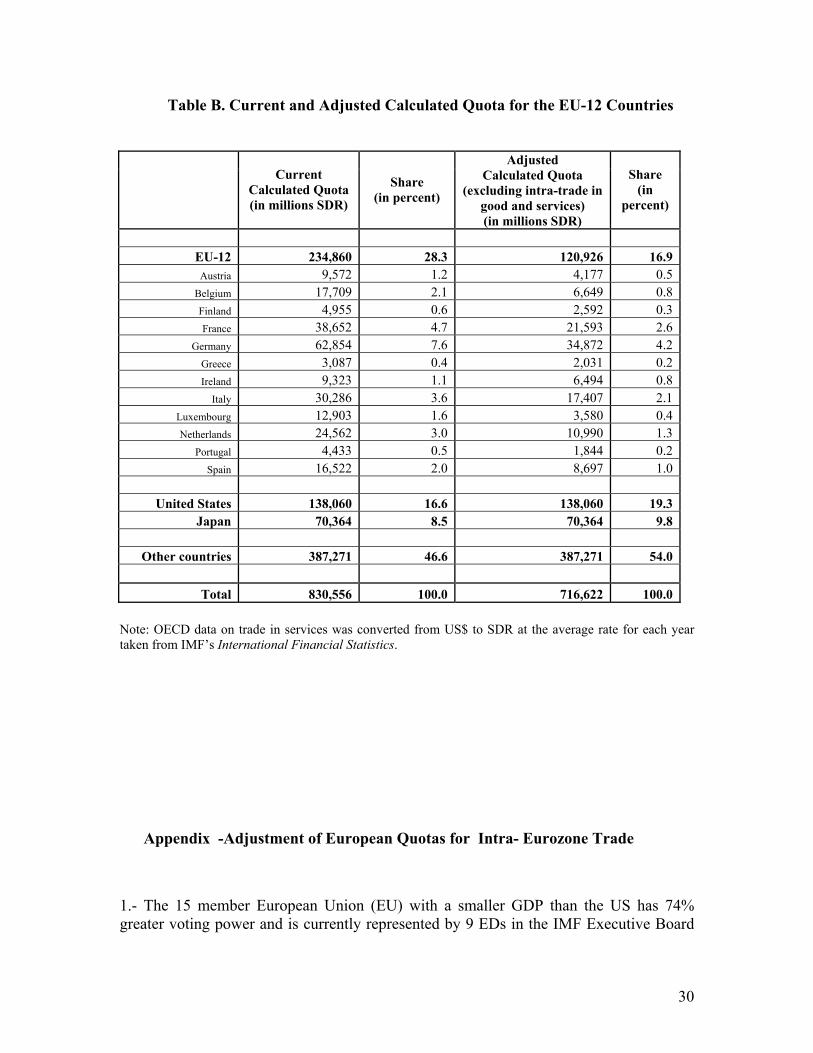

4. Following the methodology of the 12th Quota Review, we have made a new estimate of the calculated quota for the euro-zone countries adjusted for intra-trade in goods and services.28 The new estimate refers only to the 12 euro zone members.29 When this adjustment is made, the share in calculated quotas for the 12 euro zone countries declines, from 28.3 percent to 16.9 percent, a fall of 11.4 percentage points (or 40.3 percent) (see Table B). In addition, if one reduces the actual quotas by the same proportion as the decline in calculated quotas, the quota shares of the EU-12 countries would fall from 23.3 percent to 14.1 percent, a reduction of 9.2 percentage points.30

5. Since total quotas shares add up to 100 percent, the decline in the shares of a group of countries results in an increase in the relative share of IMF quotas of all other countries. With a single exchange rate and a single monetary policy, there is a lot to be said for members of the euro zone having a single representative on the IMF’s Executive Board. This would allow room for an increase in representation by the developing countries. Note that the recently signed Constitutional Treaty of the European Union, which is yet to be ratified, calls for the development of a single external policy for the European Union and a single EU representative in international organizations.

27 IMF adjustments of entrepôt trade is in order to consider only the domestic value added in international transactions. 28 The OECD dataset for services and the same formula and methodology used in the 12th Quota Review. 29 The 12 countries considered in the calculation are: Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Netherlands, Portugal, and Spain. 30 Actual quotas as of July 14, 2003.

29

31 Since trade among countries with a common currency cannot lead to balance of payments problems, when the use of a single currency is taken into account, the calculated quotas of the 12 euro zone countries fall by 40 percent.

Table A. Quotas and Voting Power of Selected Industrial Countries in 2000 GNI¹

(PPP)GNI¹ (billion $) at market

exchange rates

IMF Quotas (million SDRs)

Votes As a pro-portion of total

Austria 214 204.5 1,872.3 18,973 Belgium 282 251.6 4,605.2 46,302 Denmark 145 172.2 1,642.8 16,678 Finland 127 130.1 1,263.8 12,888 France 1,438 1,438.3 10,738.5 107,635 Germany 2,047 2,063.7 13,008.2 130,332 Greece 178 126.3 823.0 8,480 Ireland 97 86.0 838.4 8,634 Italy 1,354 1,163.2 7,055.5 70,805 Luxembourg 20 19.2 279.1 3,041 Netherlands 412 397.5 5,162.4 51,874 Portugal 170 111.3 867.4 8,924 Spain 760 595.3 3,048.9 30,739 Sweden 213 240.7 2,395.5 24,205 United Kingdom 1,407 1,459.5 10,738.5 107,635 European Union (15 above)31 8,864 8,459.4 64,339.5 647,145 29.79 United States 9,601 9,601.5 37,149.3 371,743 17.10 Japan 3,436 4,519.1 13,312.8 133,378 6.14 Memorandum Items World 44,459 31,315 212,666 2,172,350 100 All Industrial Countries 24,793 24,994 130,567 1,347,885 62.04 Developing Countries and Transition Economies 19,666 6,321 82,099 824,465 37.96 ¹/ In 2000 Source: World Bank, World Development Indicators, 2002. IMF Survey Supplement, September 2002.

30

Table B. Current and Adjusted Calculated Quota for the EU-12 Countries

Current Calculated Quota (in millions SDR)

Share (in percent)

Adjusted Calculated Quota

(excluding intra-trade in good and services) (in millions SDR)

Share (in

percent)

EU-12 234,860 28.3 120,926 16.9 Austria 9,572 1.2 4,177 0.5

Belgium 17,709 2.1 6,649 0.8 Finland 4,955 0.6 2,592 0.3 France 38,652 4.7 21,593 2.6

Germany 62,854 7.6 34,872 4.2 Greece 3,087 0.4 2,031 0.2 Ireland 9,323 1.1 6,494 0.8

Italy 30,286 3.6 17,407 2.1 Luxembourg 12,903 1.6 3,580 0.4 Netherlands 24,562 3.0 10,990 1.3

Portugal 4,433 0.5 1,844 0.2 Spain 16,522 2.0 8,697 1.0

United States 138,060 16.6 138,060 19.3

Japan 70,364 8.5 70,364 9.8

Other countries 387,271 46.6 387,271 54.0

Total 830,556 100.0 716,622 100.0

Note: OECD data on trade in services was converted from US$ to SDR at the average rate for each year taken from IMF’s International Financial Statistics.

Appendix -Adjustment of European Quotas for Intra- Eurozone Trade

1.- The 15 member European Union (EU) with a smaller GDP than the US has 74% greater voting power and is currently represented by 9 EDs in the IMF Executive Board

31

(see Table 1)32. In addition, EU has 56% greater voting power than US in the WB and 8 ED in the WB Executive Board. The over representation of the EU members, comes at the expense of other members. The excessive weight of the EU group of countries is partly attributable to the treatment of intra-EU trade in goods and services in the formula used for quota calculations. 2.-A number of European countries have formed a monetary union in 1999. This fact gives rise to a new situation calling for a revision of the calculated quota of the 12 Euro zone members. Since trade within a single currency area cannot give rise to balance of payments problems among its members, it is more akin to domestic trade than to international trade. Thus, trade between California and New York, or between Delhi and Calcutta is not regarded as international trade. Similarly, since trade between euro-zone members cannot give rise to balance of payments problems, it can not be regarded as international trade for the purposes of the quota calculations33. 3.-Recognizing the impact of intra EU trade on quota calculations, IMF staff report “External Review of the Quota Formulas” EBAP/00/52 Sup. 1, May 1, 2000, shows what would be the hypothetical adjustments in order to exclude intra-trade in goods. The reason given for exclusion is that intra-trade is seen as entrepôt trade34 in a free trade area. The report explains that if this adjustment were made “EU-15 countries’ share would be reduced by 9.2 percentage points (from about 37.1 percent to about 28.0 percent). The largest declines in percentage points are for Germany, the Netherlands, France, and Belgium”. Note that IMF staff estimates did not include trade in services in these results because of lack of data.

5.-Following the methodology of the 12th Quota Review, we have made a new estimate of the calculated quota for the euro-zone countries adjusted for intra-trade in goods and services35. The new estimate refers only to the 12 euro zone members36. When this

32 In addition, the ECB representative participates in: Article IV consultations, surveillance of the euro area members, Article IV consultations and use of resources of the 13 accession countries, as well as in discussions of the WEO, the international capital market reports, the role of the euro in the international monetary system and world economic and market developments. 33 See also IMF staff report “The European Monetary Union and the IMF-Main Legal Issues Relating to Rights and Obligations of EMU Members in the Fund," SM/98/131 dated June 8, 1998. R. Sroits, ‘The European Central Bank, Institutional Aspects,’ page 443, argues that once the European Community has a common currency, a single monetary and exchange rate Policy, a single monetary authority (the ESCB), and a single external position in terms of payments and other financial transactions to and from third countries, it will have assumed the characteristics of a 'country' for the purposes of Article II, section 2 of the Fund's Articles of Agreement. He further refers to various expressions of the opinion that Euro Area Member States may no longer qualify for membership in the IMF, since they no longer possess the necessary characteristic of monetary sovereignty in the international order. J.V. Louis, in "Governing the EMU or Governing the EU" in the Symposium on Monetary Policy and Globalization of the Markets, June 2002, observes that the European Monetary Union is "irreversible and irrevocable" and that "the Member States are not able anymore to comply individually with the commitments inherent to their participation to the IMF." 34 IMF adjustments of entrepôt trade is in order to consider only the domestic value added in international transactions. 35 OECD dataset for services and the same formula and methodology used in the 12th Quota Review.

32

adjustment is made, the share in calculated quotas for the 12 euro zone countries declines, from 28.3 to 16.9, a fall of 11.4 percentage points (or 40.3 %) (see Table 2). In addition, if one reduces the actual quotas by the same proportion as the decline in calculated quotas, the quota shares of the EU-12 countries would fall from 23.3% to 14.1 % a reduction of 9.2 percentage points37. Since total quotas shares add up to 100 percent, the decline in the shares of a group of countries results in an increase in the relative share of the quotas of all other countries (See Annex I). With a single exchange rate and a single monetary policy, there is a lot to be said for members of the eurozone having a single representative at the IMF’s Executive Board. This would make room for an increased representation by developing countries. Note that the recently signed Constitutional Treaty of the European Union, which is yet to be ratified, calls for the development of a single external policy for the European Union and a single EU representative at international organizations.

36 The 12 countries considered in the calculation are: Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, Netherlands, Portugal, and Spain 37 Actual quotas as of July 14th 2003.

33

38 Since trade among countries with a common currency cannot lead to balance of payments problems, when the use of a single currency is taken into account, the calculated quotas of the twelve eurozone countries fall by 40 percent.

Table A. Quotas and Voting Power of Selected Industrial Countries in 2000 GNI¹

(PPP)GNI¹ (billion $) at market

exchange rates

IMF Quotas (million SDRs)

Votes As a pro-portion of total

Austria 214 204.5 1,872.3 18,973 Belgium 282 251.6 4,605.2 46,302 Denmark 145 172.2 1,642.8 16,678 Finland 127 130.1 1,263.8 12,888 France 1,438 1,438.3 10,738.5 107,635 Germany 2,047 2,063.7 13,008.2 130,332 Greece 178 126.3 823.0 8,480 Ireland 97 86.0 838.4 8,634 Italy 1,354 1,163.2 7,055.5 70,805 Luxembourg 20 19.2 279.1 3,041 Netherlands 412 397.5 5,162.4 51,874 Portugal 170 111.3 867.4 8,924 Spain 760 595.3 3,048.9 30,739 Sweden 213 240.7 2,395.5 24,205 United Kingdom 1,407 1,459.5 10,738.5 107,635 European Union (15 above)38 8,864 8,459.4 64,339.5 647,145 29.79 United States 9,601 9,601.5 37,149.3 371,743 17.10 Japan 3,436 4,519.1 13,312.8 133,378 6.14 Memorandum Items World 44,459 31,315 212,666 2,172,350 100 All Industrial Countries 24,793 24,994 130,567 1,347,885 62.04 Developing Countries and Transition Economies 19,666 6,321 82,099 824,465 37.96 ¹/ In 2000 Source: World Bank, World Development Indicators, 2002. IMF Survey Supplement, September 2002.

34

Table B. Current and Adjusted Calculated Quota for the EU-12 countries

Current Calculated Quota (in millions SDR)

Share (in percent)

Adjusted Calculated Quota

(excluding intra-trade in good and services) (in millions SDR)

Share (in

percent)

EU-12 234,860 28.3 120,926 16.9 Austria 9,572 1.2 4,177 0.5

Belgium 17,709 2.1 6,649 0.8 Finland 4,955 0.6 2,592 0.3 France 38,652 4.7 21,593 2.6

Germany 62,854 7.6 34,872 4.2 Greece 3,087 0.4 2,031 0.2 Ireland 9,323 1.1 6,494 0.8

Italy 30,286 3.6 17,407 2.1 Luxembourg 12,903 1.6 3,580 0.4 Netherlands 24,562 3.0 10,990 1.3

Portugal 4,433 0.5 1,844 0.2 Spain 16,522 2.0 8,697 1.0

United States 138,060 16.6 138,060 19.3

Japan 70,364 8.5 70,364 9.8

Other countries 387,271 46.6 387,271 54.0

Total 830,556 100.0 716,622 100.0

Note: OECD data on trade in services was converted from US$ to SDR at the average rate for each year taken from IFS.

35

References

Buira, Ariel, 1999, “An Alternative Approach to Financial Crises,” Essays in International Finance No. 212, International Finance Section, Dept. of Economics, Princeton University, Perinceton, N.J.

Chang, Ha-Joon, “Kicking Awway the Ladder,”

Collier, Paul, “Primary Commodity Dependence and Africa’s Future,” World Bank, April 2002, p.3.

Dooley, M., Folkerts-Landau, D., and Garber, P., “An Essay on the Reveived Bretton Woods System,” NBER Working Paper Series, Working Paper 9971, September 2003.

Fedelino, Annalis and Kudina, Alina, “Fiscal Sustainability in African HIPC Countries: A Policy Dilemma?” IMF, WP/03/187.

Gunter, B., “Achieving Long-Term Debt Sustainability in Heavily Indebted Poor Countries” in “Challeges to the World Bank and the IMF” edited by Ariel Buira, 2003.

Helleiner, G., “Marginalization and/or Participation: Africa in Today’s Global Economy,” Lecture to CASS Conference, published in Canadian Journal of African Studies, Vol. 36, No. 3, 2002.

International Financial Statistics Yearbook 2003, IMF.

IMF Occasional Paper 227, January 2004.

IMF, “Fund Assistance for Countries Facing Exogenous Shocks,” prepared by PDR, August 2003.

Prasad, E., Rogoff, K., Wei, S., and Kose, M.A., 2003, “Effects of Financial Globalization on developing Countries: Some Empirical Evidence”

Volcker, P. and Gyoten, T., “Changing Fortunes,” 1992, Random House, New York.

World Development Indicators 2003, World Bank.

World Economic Outlook Database 2993, IMF.